Europe Non-Vascular Stents Market Research Report By End User, Material, Type and Country (United Kingdom, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands and Rest of Europe) - Industry Analysis, Size, Share, Growth, Trends and Forecast (2026 to 2034)

Market Size, 2025

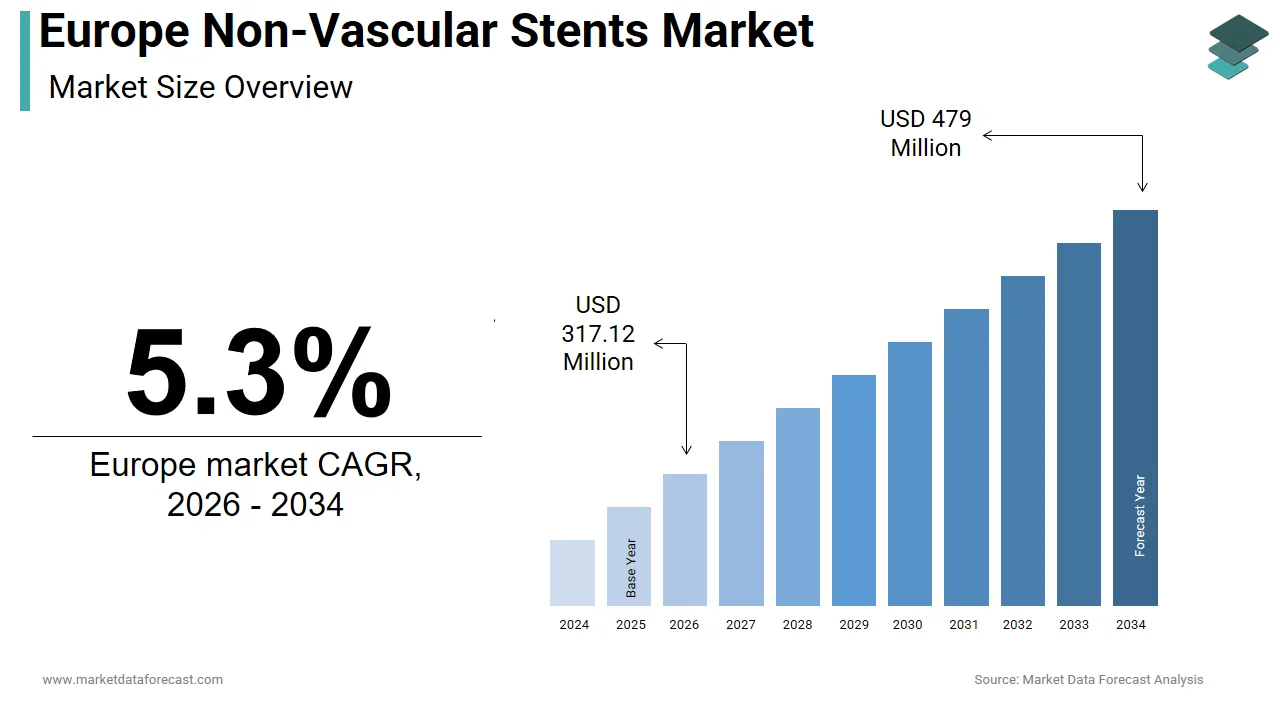

$301.16 MnMarket Estimate, 2026

$317.12 MnMarket Forecast, 2034

$479 MnCAGR, 2026–2034

5.3%Europe Non-Vascular Stents Market Report Summary

The Europe non-vascular stents market was valued at USD 301.16 million in 2025, is estimated to reach USD 317.12 million in 2026, and is projected to reach USD 479 million by 2034, growing at a CAGR of 5.3% from 2026 to 2034. Market growth is driven by the increasing prevalence of chronic diseases, rising number of minimally invasive procedures, and growing demand for effective treatment solutions in urology, gastroenterology, and pulmonary applications. Non-vascular stents are widely used to maintain patency in non-blood vessel structures such as the urinary tract, bile ducts, and airways. Advancements in stent materials, improved biocompatibility, and expanding healthcare infrastructure are further supporting the growth of the market across Europe.

Key Market Trends

- Increasing adoption of minimally invasive procedures across medical specialties.

- Rising demand for non-vascular stents in urology, gastrointestinal, and pulmonary treatments.

- Growing advancements in biocompatible and durable stent materials.

- Expansion of hospital infrastructure and interventional treatment capabilities.

- Increasing focus on improving patient outcomes and reducing procedure complications.

Segmental Insights

- Based on type, the urinary tract stents segment dominated the Europe non-vascular stents market by capturing 36.3% share in 2025, driven by the high prevalence of urological conditions and procedures.

- Based on end user, the hospitals segment led the market by accounting for 74.4% share in 2025, supported by the availability of advanced medical infrastructure and high volume of interventional procedures.

- Based on material, the metallic stents segment held the largest share of 59.5% in 2025, driven by their durability, strength, and widespread clinical use.

Regional Insights

The Europe non-vascular stents market is witnessing steady growth across major countries due to increasing healthcare demand and advancements in interventional procedures.

- Germany led the regional market in 2025 with 25.5% share, supported by advanced healthcare infrastructure and high adoption of minimally invasive procedures.

- The United Kingdom held the second-largest position in the regional market in 2025, driven by strong healthcare systems and increasing surgical volumes.

- France is expected to hold a significant share during the forecast period due to its extensive network of public and private healthcare facilities performing high volumes of interventional procedures.

Competitive Landscape

The Europe non-vascular stents market is characterized by the presence of leading medical device manufacturers and specialized healthcare solution providers. Market players are focusing on developing innovative stent designs, improving material quality, and expanding product portfolios to cater to diverse medical applications. Strategic collaborations, product launches, and investments in research and development are shaping competitive dynamics across the region.

Prominent companies operating in the Europe non-vascular stents market include CONMED Corporation, Taewoong Medical Co., Medtronic, C. R. Bard Inc., Boston Scientific Corporation, HOBBS Medical Inc., Cook Medical, ELLA-CS s.r.o., Synchron Med Inc., and Glaukos Corporation.

Europe Non-Vascular Stents Market Size

The Europe non-vascular stents market was valued at USD 301.16 million in 2026, is estimated to reach USD 317.12 million in 2026, and is projected to reach USD 479 million by 2034, growing at a CAGR of 5.3% from 2026 to 2034.

Non-Vascular stents encompass a specialized sector of medical devices designed to maintain patency in bodily lumens outside the cardiovascular system, specifically targeting the urinary, biliary, gastrointestinal, and respiratory tracts. These implants serve as critical therapeutic solutions for managing strictures, obstructions, and leaks caused by malignancies, benign conditions, or post-surgical complications. The clinical urgency for these devices is underscored by the escalating burden of oncological diseases across the continent, which frequently result in ductal obstructions requiring palliative or curative stenting. According to the European Commission, cancer remains the second leading cause of death in the European Union, with certain types such as pancreatic and colorectal cancers often requiring stenting procedures to relieve obstruction. Furthermore, the aging demographic profile of Europe significantly amplifies the prevalence of benign strictures and stones that require interventional management. As per Eurostat, a substantial proportion of the EU population is aged 65 or older, a cohort highly susceptible to urological and biliary disorders. According to the World Health Organization Regional Office for Europe, the incidence of kidney stones and urinary tract obstructions has been rising, driving the need for ureteral stents. This market, therefore, operates at the nexus of advanced urology, gastroenterology, and oncology, which is providing life-enhancing interventions that restore physiological function and improve quality of life for patients facing complex anatomical challenges.

MARKET DRIVERS

Rising Incidence of Gastrointestinal and Biliary Malignancies

The escalating prevalence of gastrointestinal and biliary tract cancers is one of the major factors propelling the expansion of the European non-vascular stents market. Malignancies such as pancreatic, bile duct, and colorectal cancer frequently cause severe obstructions that block the flow of bile or food, necessitating immediate decompression via stent placement to alleviate symptoms and enable nutrition. According to the International Agency for Research on Cancer, Europe accounts for a significant proportion of global cancer cases, with pancreatic cancer incidence showing a steady upward trend in several member states. As per the European Society of Gastrointestinal Endoscopy, self-expanding metal stents have become the standard of care for palliating malignant strictures due to their superior patency compared to plastic alternatives. This clinical preference drives consistent volume growth as oncologists and gastroenterologists rely on stenting to manage unresectable tumors in an aging population. Furthermore, the shift toward minimally invasive endoscopic procedures over open surgery reduces hospital stays and recovery times, making stenting the preferred first-line intervention. The increasing diagnosis of early-stage cancers through improved screening programs also leads to earlier interventions where stents are used to manage complications.

Growing Prevalence of Urological Disorders and Stone Disease

The increasing burden of urological conditions, including kidney stones, ureteral strictures, and benign prostatic hyperplasia, is further supporting the European non-vascular stents market growth. Sedentary lifestyles, dietary habits high in oxalates and sodium, and an aging population have contributed to a surge in nephrolithiasis across Europe. As per the European Association of Urology, the lifetime risk of developing kidney stones in Europe is significant, with recurrence rates remaining high within five years of the initial episode. Each episode of stone passage or surgical intervention, such as ureteroscopy, typically requires the temporary placement of a double J stent to ensure ureteral drainage and prevent stricture formation. As per the European Centre for Disease Prevention and Control, an aging male population also drives demand for stents related to prostate enlargement, which can obstruct urinary flow. Additionally, advancements in stent technology, such as anti-encrustation coatings and biodegradable materials, are encouraging urologists to use stents more liberally in complex cases. The high volume of endourological procedures performed annually, coupled with the chronic nature of stone disease requiring repeated interventions, creates a continuous and high-frequency demand cycle for ureteral stents throughout the region.

MARKET RESTRAINTS

High Risk of Device-Related Complications and Infections

The persistent risk of device-related complications, including migration, encrustation, occlusion, and severe infections, is primarily impeding the European non-vascular stents market expansion. These adverse events often necessitate unplanned re-interventions, increasing the clinical burden on healthcare systems and eroding confidence in long-term indwelling devices. According to the Journal of Urology, ureteral stents are associated with notable complication rates, with encrustation and biofilm formation being major causes of obstruction that can lead to sepsis if not managed promptly. As per the European Centre for Disease Prevention and Control, healthcare-associated infections linked to implanted devices remain a critical public health challenge, prompting hospitals to adopt stricter protocols that may limit the duration of stent placement. In the biliary sector, stent occlusion due to sludge or tumor ingrowth frequently requires exchange procedures, increasing patient discomfort and healthcare costs. The fear of these complications sometimes leads clinicians to opt for alternative management strategies such as percutaneous drainage or surgical bypass in complex cases, thereby limiting market volume. Furthermore, the discomfort and lower urinary tract symptoms associated with indwelling ureteral stents significantly impact patient quality of life, leading to calls for earlier removal, which shortens the replacement cycle.

Stringent Regulatory Frameworks and Reimbursement Complexities

The rigorous regulatory environment governing medical device approval and the fragmented reimbursement landscape across European nations are further hindering the growth of the regional market. The implementation of the European Union Medical Device Regulation has intensified scrutiny on clinical evidence requirements, which is forcing manufacturers to conduct extensive and costly post-market surveillance and clinical investigations to maintain certification. As per the European MedTech Industry, the transition to the new regulations has delayed the launch of innovative stent technologies as companies struggle to compile the necessary technical documentation and clinical data. Additionally, reimbursement policies for non-vascular stents vary significantly between member states, with some countries imposing strict caps on the number of stents reimbursable per patient or favoring lower-cost plastic stents over premium metal options. According to the European Observatory on Health Systems and Policies, budget constraints in public healthcare systems often lead to tender processes that prioritize price over clinical superiority, squeezing margins for manufacturers of high-end devices. In certain regions, the lack of specific reimbursement codes for newer biodegradable or drug-eluting stents discourages hospitals from adopting these advanced solutions. The combination of prolonged approval timelines, heterogeneous payment structures, and cost-containment pressures stifles innovation and limits the accessibility of advanced stenting therapies for patients across the continent.

MARKET OPPORTUNITIES

Development of Biodegradable and Drug-Eluting Stent Technologies

The emergence of biodegradable and drug-eluting stent platforms is a promising opportunity in the European non-vascular stents market. Biodegradable stents eliminate the need for secondary removal procedures, reducing patient trauma, healthcare costs, and the risk of complications associated with retained devices. As per the European Association of Urology, next-generation biodegradable ureteral stents have shown promising clinical outcomes, offering comparable patency to conventional polymers while resorbing naturally. Simultaneously, drug-eluting stents coated with antiproliferative or antimicrobial agents offer the potential to inhibit tissue hyperplasia and prevent biofilm formation, thereby extending patency periods in malignant and benign strictures. According to the European Commission’s Horizon Europe program, funding is being directed toward smart biomaterials that respond to physiological changes, accelerating innovation in this field. Manufacturers who successfully commercialize these advanced products can capture premium market segments and establish strong differentiation. The ability to offer solutions that either resorb naturally or actively prevent restenosis aligns with value-based healthcare goals, positioning these technologies as a major growth driver.

Expansion of Minimally Invasive Interventional Radiology and Endoscopy

The continuing shift toward minimally invasive therapeutic procedures performed by interventional radiologists and gastroenterologists offers a significant growth avenue for the non-vascular stent market in Europe. As surgical techniques evolve, there is a growing preference for endoluminal approaches that reduce morbidity, shorten hospital stays, and accelerate recovery compared to open surgical reconstruction. As per the Cardiovascular and Interventional Radiological Society of Europe, image-guided interventions for biliary, urinary, and gastrointestinal obstructions have been steadily increasing, supported by advancements in imaging modalities and delivery systems. This trend expands the patient pool to include those who are poor surgical candidates due to comorbidities or advanced age. The integration of fusion imaging and robotic assistance allows for more precise stent placement in complex anatomies, improving success rates and broadening indications. National health systems across Europe are also promoting day-case procedures to optimize bed occupancy and reduce costs, further favoring stent-based interventions. The development of dedicated stents for emerging applications such as esophageal fistula repair or bronchial stenosis management broadens the market scope. Aligning product portfolios with these procedural trends enables manufacturers to leverage the structural shift in surgical practice for sustained expansion.

MARKET CHALLENGES

Intense Price Pressure from Public Procurement and Tendering

The reliance on centralized public procurement and competitive tendering processes across European healthcare systems exerts immense downward pressure on pricing, which is severely impacting profitability for stent manufacturers and challenging the expansion of the regional market. Public hospitals, which constitute the majority of end-users, are mandated to award contracts based largely on the lowest bid to meet strict budgetary constraints. As per the European Health Management Association, consolidation of purchasing power into large regional or national tenders has commoditized many standard stent categories, forcing suppliers into aggressive price competition that erodes margins. Smaller innovators are disproportionately affected, as they lack the scale to absorb deep discounts, potentially stifling competition and reducing product diversity. The focus on cost containment often overshadows clinical differentiation, making it difficult to justify premium pricing for advanced features. In some cases, tenders result in single-supplier monopolies, creating barriers for new entrants and limiting physician choice. According to the European MedTech Industry, sustained price erosion threatens the financial viability of research and development programs, slowing innovation. Navigating this procurement landscape while maintaining quality standards remains a formidable challenge for all market participants.

Variability in Clinical Practices and Physician Adoption Rates

The lack of standardized clinical guidelines and significant variability in physician preferences across European regions pose a persistent challenge to uniform market growth. Practices regarding stent type selection, duration of indwelling time, and placement indications differ widely between countries and even hospitals. As per surveys conducted by United European Gastroenterology, there is considerable divergence in the choice between plastic and metal stents for malignant biliary obstruction, often influenced by local expertise rather than unified evidence-based protocols. This fragmentation complicates market access strategies, requiring manufacturers to tailor educational and marketing efforts to diverse local ecosystems. The learning curve associated with newer, more complex stent systems can slow adoption among conservative practitioners who prefer legacy products. The absence of harmonized training programs means skill levels in advanced stenting techniques vary, limiting the utilization of sophisticated devices in centers with less experienced staff. Overcoming these entrenched practice patterns requires substantial investment in physician education and the generation of robust local clinical data to drive consensus. Until greater alignment in clinical standards is achieved, market penetration will remain uneven and dependent on localized advocacy efforts.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, End User, Material, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | CONMED Corporation, Taewoong Medical Co., Medtronic; C. R. Bard, Inc.; Boston Scientific Corporation; HOBBS MEDICAL, INC; Cook Medical; ELLA - CS, s.r.o.; Ltd.; Synchron Med Inc.; and Glaukos Corporation. |

SEGMENTAL ANALYSIS

By Type Insights

The urinary tract stents segment dominated the market by commanding for 36.3% of the European market share in 2025 due to the high prevalence of urolithiasis and benign prostatic hyperplasia across the continent and the large volume of endourological procedures performed annually to manage kidney stones and ureteral obstructions. The rising incidence of nephrolithiasis that frequently requires the temporary placement of double J stents following surgical intervention is another major factor boosting the dominance of the urinary tract stents segment in the European market. As per the European Association of Urology, the lifetime risk of developing kidney stones in Europe is significant, with recurrence rates remaining high, creating a continuous cycle of demand for ureteral stenting. The second major driver is the aging male demographic, which suffers increasingly from benign prostatic hyperplasia, causing urinary retention that requires stent placement for relief. According to Eurostat, men aged 65 and older constitute a rapidly growing segment of the population, directly correlating with higher rates of obstructive uropathy. Furthermore, the standardization of ureteroscopy as the first-line treatment for stones ensures that stent usage remains integral to urological practice. The combination of high disease prevalence, an aging population, and established clinical protocols secures the urinary tract segment in its position as the market leader.

On the other hand, the pancreatic and biliary stents segment is projected to be the fastest growing category in the Europe non-vascular stents market and expand at a CAGR of 8.5% over the forecast period, owing to the increasing incidence of pancreatic and bile duct cancers that often present with malignant obstructions requiring palliative stenting to restore bile flow and improve quality of life. As per the International Agency for Research on Cancer, pancreatic cancer cases in Europe are projected to rise significantly by 2030, driving urgent demand for self-expanding metal stents that offer longer patency than plastic alternatives. The second critical driver is the technological shift toward fully covered metal stents and drug-eluting variants, which reduce tumor ingrowth and migration, making them the preferred choice for complex strictures. According to the European Society of Gastrointestinal Endoscopy, clinical guidelines increasingly recommend metal stents for unresectable malignancies, boosting adoption rates. Additionally, the expansion of therapeutic endoscopy capabilities in community hospitals allows more patients to access these interventions earlier. The convergence of rising cancer rates, superior product performance, and broader procedural access propels this segment to the forefront of market expansion.

By End User Insights

The hospitals segment led the market by capturing 74.4% of the European market share in 2025. This supremacy is driven by the necessity for advanced imaging equipment, specialized surgical teams, and intensive care units, which are essential for managing patients undergoing non-vascular stenting. A key driving factor is the concentration of oncological and urological surgeries within large hospital settings where multidisciplinary teams coordinate care for patients with severe obstructions. As per the Organisation for Economic Co-operation and Development, the majority of inpatient procedures involving stent placement for malignant strictures or complex stone disease are performed in acute care hospitals equipped with hybrid operating rooms. The second major driver is the reimbursement structure in many European countries, which favours inpatient procedures for high-risk interventions, ensuring a steady flow of patients to hospital departments. According to the European Hospital and Healthcare Federation, hospitals continue to invest heavily in endoscopic and radiological infrastructure to maintain their status as referral centers for complex cases. Furthermore, the ability of hospitals to manage post-procedural complications and provide long-term follow-up makes them the preferred setting for deploying expensive metal stents.

The ambulatory surgical centers (ASCs) segment represents the fastest expanding end-user segment in the Europe non-vascular stents market and is expected to register a CAGR of 10.6% over the forecast period. Factors such as the strategic shift toward minimally invasive day-case procedures that reduce hospital stays and lower overall healthcare costs, and the increasing adoption of simple ureteral stent placements and biliary exchanges that can be safely performed under local anaesthesia or light sedation in an outpatient setting, are propelling the expansion of the ambulatory surgical centers segment in the European market. As per the European Centre for Disease Prevention and Control, moving suitable procedures to ambulatory settings can reduce infection risks and free up acute hospital beds for more critical cases. National health services across Europe are incentivizing this transition through bundled payment models that reward efficiency and rapid turnover. Data from the European Association of Urology indicates a marked increase in the volume of ureteroscopy procedures performed in day surgery units, driven by patient preference for avoiding overnight hospitalization. Additionally, advancements in portable imaging and compact endoscopic towers have made it feasible for ASCs to handle increasingly complex stenting tasks.

By Material Insights

The metallic stents segment led the market by holding 59.5% of the European market share in 2025. The growth of the metallic stents segment in the European market is driven by their superior radial strength, durability, and longer patency rates compared to non-metallic alternatives. The clinical preference for self-expanding metal stents in palliative care for unresectable cancers, as they resist compression from growing tumors better than plastic stents, is further contributing to the dominance of the metallic stents segment in the European market. As per the European Society of Gastrointestinal Endoscopy, metal stents demonstrate lower occlusion rates and require fewer re-interventions than plastic stents in malignant biliary obstruction, making them the cost-effective choice despite higher upfront costs. The second major driver is the development of covered metal stents, which prevent tissue ingrowth and allow for easier removal if necessary, expanding their utility in benign conditions. The International Journal of Surgery notes that adoption of fully covered metal stents has risen for treating esophageal fistulas and bronchial stenosis. Furthermore, the aging population suffering from advanced cancers ensures consistent demand for durable solutions that minimize repeated hospital visits.

However, the non-metallic stents segment is another major segment and is estimated to grow at a CAGR of 11.5% over the forecast period in this regional market. Factors such as the urgent need to eliminate secondary removal procedures and reduce long-term complications associated with permanent implants and the commercialization of biodegradable ureteral and biliary stents that naturally resorb within the body after fulfilling their therapeutic function are propelling the expansion of the non-metallic stents segment in the European market. As per the European Association of Urology, biodegradable stents have shown promising results in maintaining ureteral patency while dissolving naturally within weeks, thereby removing the discomfort and risk of forgotten stents. The second significant driver is innovation in anti-encrustation polymer coatings, which extend the functional life of plastic stents, making them viable for longer durations in patients who are not candidates for metal stents. According to the European Commission, funding for smart biomaterials has accelerated the development of stents that release drugs or respond to physiological changes, enhancing their therapeutic profile. Additionally, the lower cost of production for advanced polymers compared to alloys makes them attractive for cost-conscious healthcare systems. The convergence of patient comfort, technological innovation, and economic viability positions non-metallic stents as the most rapidly expanding category.

COUNTRY-LEVEL ANALYSIS

Germany Non-Vascular Stents Market Analysis

Germany held the leading position in the Europe non-vascular stents market in 2025 with 25.5% of the regional market share. The dominating position of Germany in the European market is attributed to the world-class medical infrastructure, high volumes of interventional procedures, strong adoption of advanced stent technologies such as drug-eluting and biodegradable variants, and the high incidence of cancer and urological disorders in an aging population that sustains demand for both palliative and therapeutic stenting. According to the Robert Koch Institute, pancreatic and colorectal cancers remain major contributors to biliary and gastrointestinal stent placements. Renowned university hospitals and specialized centers act as hubs for complex endoscopic and interventional radiology procedures, while the German Medical Device Act enforces rigorous quality standards, fostering trust in premium products. The country’s strong manufacturing base accelerates innovation, and initiatives from the Federal Ministry of Health to improve cancer care pathways indirectly boost stent utilization. This synergy of demographic pressure, clinical excellence, and supportive regulation cements Germany’s position as the largest and most sophisticated market in the region.

United Kingdom Non-Vascular Stents Market Analysis

The United Kingdom held the second largest position in the Europe non-vascular stents market in 2025 due to its centralized National Health Service (NHS), which drives standardized procurement and broad access to stenting procedures. The market emphasizes cost-effectiveness, with guidelines favoring metal stents for malignant obstructions to reduce re-admission rates. A key driver is the high prevalence of gallstone disease and liver cancer, necessitating frequent biliary and pancreatic interventions. Cancer Research UK reports rising incidence rates of liver and pancreatic cancers, creating steady demand for stenting. The NHS Long Term Plan prioritizes expansion of endoscopic services to reduce waiting times and improve cancer survival rates, while NHS England data shows a strategic push to increase therapeutic endoscopy capacity. The UK is also an early adopter of biodegradable stent technologies through pilot programs in teaching hospitals. The combination of a unified healthcare system, rising disease burden, and modernization of gastroenterology services secures the UK’s role as a vital high-volume market.

France Non-Vascular Stents Market Analysis

France is anticipated to capture a promising share of the Europe non-vascular stents market during the forecast period, owing to its extensive network of public and private clinics performing high volumes of interventional procedures. The French market is characterized by balanced adoption of metallic and non-metallic stents, guided by clinical protocols tailored to patient prognosis and stricture type. A major driver is the integration of gastroenterology and urology into the national cancer control plan. According to the French National Cancer Institute, comprehensive screening and treatment programs ensure early detection and timely stent placement. Favorable reimbursement under the French social security system covers a wide range of stent types, including premium metal options. The Ministry of Solidarity and Health highlights ongoing investments in hospital equipment to support minimally invasive surgeries. France also serves as a hub for clinical research in urology, hosting trials for next-generation biodegradable stents. The synergy of strong public health policies, advanced clinical practice, and research leadership sustains France’s position as a key market.

Italy Non-Vascular Stents Market Analysis

Italy is expected to showcase a healthy CAGR in the Europe non-vascular stents market during the forecast period. Factors such as its aging population and high prevalence of chronic urological and biliary conditions are driving the expansion of the Italian market. The market relies heavily on public hospitals for complex cases, complemented by a vibrant private sector offering rapid access to advanced stenting solutions. Italy’s demographic reality—one of the oldest populations in Europe—correlates directly with higher rates of benign prostatic hyperplasia, kidney stones, and age-related cancers. According to the Italian National Institute of Statistics, the proportion of citizens over 65 continues to grow, driving consistent demand for urinary and biliary stents. Regional healthcare variation fosters competition among regions to adopt advanced technologies. The Italian Association of Urology notes the rising use of metal stents for complex strictures to minimize repeat interventions. Additionally, dietary habits contribute to high gallstone prevalence, boosting biliary stent demand. This blend of demographic inevitability, regional dynamics, and disease patterns ensures Italy remains a vital player in the European landscape.

Spain Non-Vascular Stents Market Analysis

Spain is anticipated to register a notable CAGR in the Europe non-vascular stents market during the forecast period, owing to its robust public healthcare system and growing investment in oncology and urology infrastructure. The market is shifting toward self-expanding metal stents as budget constraints ease and clinical evidence supports their long-term value. The rising incidence of digestive system cancers, particularly colorectal and pancreatic, has prompted government initiatives to enhance early diagnosis and palliative care programs. According to the Spanish Society of Medical Oncology, cancer mortality rates remain a concern, driving demand for effective obstruction management. Hospital endoscopy units across autonomous regions are being modernized with European recovery funds, enabling more complex stent placements. Spain’s climate and dietary habits also contribute to high kidney stone prevalence, sustaining demand for urinary stents. The convergence of cancer strategies, infrastructure upgrades, and lifestyle-related disease burdens creates a dynamic environment for stent adoption, securing Spain’s role as a key growth market in the region.

COMPETITIVE LANDSCAPE

The competition in the Europe Non-Vascular Stents Market is characterized by a dynamic mix of established multinational corporations and specialized regional manufacturers vying for dominance through technological differentiation and clinical evidence. Major players compete intensely on product performance features such as patency duration, ease of deployment, and resistance to migration or occlusion to secure preference among gastroenterologists and urologists. The market sees frequent consolidation as larger entities acquire smaller innovators to fill gaps in their portfolios regarding biodegradable materials or drug-eluting technologies. Price pressure from centralized public procurement tenders forces companies to balance cost efficiency with the need to fund ongoing research and development activities. Regulatory compliance with the stringent European Union Medical Device Regulation has become a critical competitive factor where only those with robust quality systems can maintain market access. New entrants continue to challenge incumbents by offering disruptive solutions like fully resorbable stents that promise to transform standard care protocols. This evolving landscape requires continuous adaptation and strategic agility from all participants to sustain growth and profitability amidst shifting clinical guidelines and economic constraints.

KEY MARKET PLAYERS

The leading companies operating in the Europe non-vascular stents market include:

- CONMED Corporation

- Taewoong Medical Co.

- Medtronic

- R. Bard, Inc.

- Boston Scientific Corporation

- HOBBS MEDICAL, INC.

- Cook Medical

- ELLA-CS, s.r.o.

- Synchron Med Inc.

- Glaukos Corporation

TOP PLAYERS IN THE MARKET

- Boston Scientific Corporation stands as a global leader in the development and commercialization of non-vascular stents with a particularly strong footprint in urological and biliary applications. The company contributes significantly to the global market by offering a comprehensive portfolio that includes metal, plastic, and biodegradable stents designed for complex anatomical challenges. Recently, Boston Scientific has focused on expanding its urology division through the launch of next-generation stone management solutions and anti-encrustation ureteral stents that improve patient comfort. The firm actively invests in clinical research to validate the efficacy of its drug-eluting biliary stents aimed at reducing tumor ingrowth. Their strategic acquisitions of specialized endoscopic device manufacturers have broadened their technological capabilities and distribution reach across Europe. Boston Scientific continues to strengthen its market position by partnering with key opinion leaders to promote best practices in interventional urology and gastroenterology. These initiatives demonstrate their commitment to innovation and clinical excellence in the competitive landscape of non-vascular interventions.

- Cook Medical operates as a pivotal player in the Europe non-vascular stents market, renowned for its extensive range of biliary, pancreatic, and airway stenting solutions. The company contributes to the global sector by providing high-quality devices that address both benign and malignant strictures with a focus on durability and ease of deployment. Recently, Cook Medical has accelerated its investment in biodegradable stent technologies, aiming to eliminate the need for secondary removal procedures and reduce long-term complications. The firm actively collaborates with European hospitals to conduct real-world evidence studies that highlight the clinical benefits of their fully covered metal stents. Their recent expansion of manufacturing facilities in Europe ensures a robust supply chain capable of meeting rising demand promptly. Cook Medical also focuses on educational programs for physicians to advance skills in complex stent placement techniques. These strategic efforts reinforce their reputation as a trusted partner in improving patient outcomes through innovative non-vascular device solutions.

- ConMed Corporation is a prominent medical technology company that plays a significant role in the Europe non-vascular stents market through its specialized biliary and pancreatic product lines. The company contributes to the global marketplace by delivering advanced stent systems that facilitate effective drainage and obstruction management in diverse clinical settings. Recently, ConMed has strengthened its position by introducing novel stent delivery systems that offer enhanced precision and control during endoscopic procedures. The firm actively pursues strategic partnerships with distributors across Eastern and Southern Europe to expand market access for its premium stent offerings. Their recent investments in research and development have led to the creation of stents with improved radial force and migration resistance tailored for difficult anatomies. ConMed also emphasizes surgeon education through workshops and simulation training to ensure optimal utilization of their devices. These actions underscore their dedication to advancing therapeutic standards and capturing growth opportunities in the evolving European healthcare environment.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Europe Non-Vascular Stents Market primarily employ product innovation and diversification strategies to address unmet clinical needs such as stent migration and encrustation. Companies frequently engage in strategic acquisitions of niche technology firms to gain access to proprietary biomaterials or novel delivery mechanisms that enhance their portfolios. Another prevalent strategy involves heavy investment in clinical research and real-world evidence generation to demonstrate superior outcomes and justify premium pricing amidst cost containment pressures. Market participants also focus on expanding their geographic reach through partnerships with local distributors and establishing regional manufacturing hubs to ensure supply chain resilience. Additionally, firms are increasingly leveraging digital health tools and physician training programs to improve procedural success rates and foster brand loyalty among interventional specialists. These approaches enable companies to maintain competitiveness and drive sustainable growth in a highly regulated and clinically demanding market environment.

MARKET SEGMENTATION

This research report on the European Non-Vascular Stents Market has been segmented and sub-segmented into the following categories.

By Type

-

Pancreatic and Biliary Stents

-

Biliary Stents

-

Pancreatic Stents

-

-

Gastrointestinal Stents

-

Airway Stents

-

Urinary Tract Stents

By End User

- Hospitals

- Ambulatory Surgical Centers

- Others

By Material

- Metallic Stents

- Non-Metallic Stents

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

What is the Europe non-vascular stents market?

The Europe non-vascular stents market provides airway and gastrointestinal stents for obstruction relief. Germany leads endoscopic adoption while Nordics excel in advanced applications.

How does the Europe non-vascular stents market function?

The Europe non-vascular stents market functions through minimally invasive deployment via endoscopy. Self-expanding designs maintain patency in digestive and respiratory tracts.

What drives growth in the Europe non-vascular stents market?

Cancer prevalence drives the Europe non-vascular stents market alongside aging populations requiring palliative stenting. Cost-efficiency favors endoscopic alternatives to surgery.

Which countries lead the Europe non-vascular stents market?

Germany dominates the Europe non-vascular stents market through procedural expertise. UK follows rapidly with NHS cancer pathway integration.

What types define the Europe non-vascular stents market?

Airway and biliary stents lead the Europe non-vascular stents market alongside enteral colorectal stents. Covered metal designs prevent tissue ingrowth complications.

What applications shape the Europe non-vascular stents market?

Palliative cancer care dominates the Europe non-vascular stents market treating esophageal and tracheal obstructions. Benign strictures expand elective applications.

How does regulation influence the Europe non-vascular stents market?

EU MDR certification governs the Europe non-vascular stents market ensuring device safety and performance. Harmonized standards facilitate cross-border approvals.

What trends affect the Europe non-vascular stents market?

Biodegradable stents transform the Europe non-vascular stents market eliminating reintervention needs. Drug-eluting coatings reduce restenosis rates significantly.

What challenges face the Europe non-vascular stents market?

Migration risks challenge the Europe non-vascular stents market though anchoring techniques help. Tumor ingrowth requires covered stent innovations.

How has endoscopy impacted the Europe non-vascular stents market?

Endoscopic techniques revolutionized the Europe non-vascular stents market enabling outpatient procedures. Bronchoscopy facilitates rapid airway stent deployment.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com