Europe Peaches and Nectarines Market Size, Share, Trends & Growth Forecast Report – Segmented By Product Type (Peaches, Nectarines, Combos), Distribution Channel, Application, Packaging Type, and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2026 to 2034

Europe Peaches and Nectarines Market Report Summary

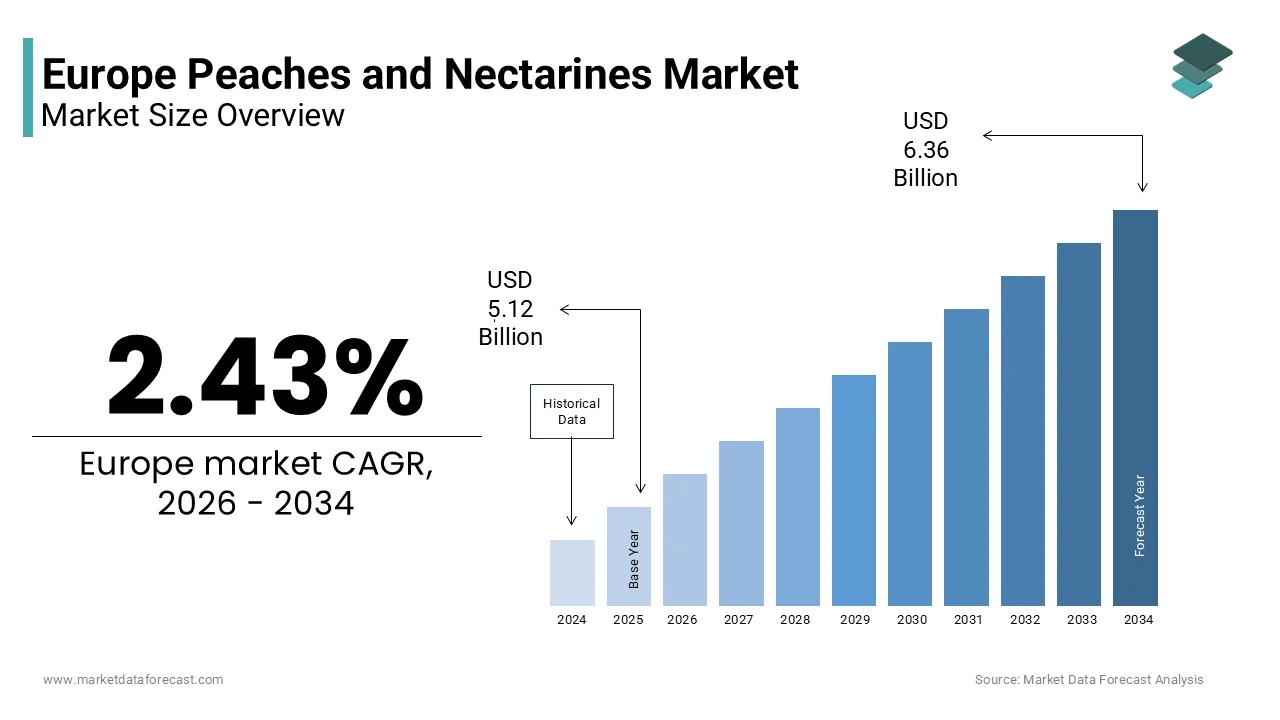

The Europe peaches and nectarines market was valued at USD 5.12 billion in 2025, is estimated to reach USD 5.25 billion in 2026, and is projected to reach USD 6.36 billion by 2034, growing at a CAGR of 2.43% during the forecast period from 2026 to 2034. The growth of the Europe peaches and nectarines market is driven by increasing consumer preference for fresh seasonal fruits, rising awareness of healthy eating habits, and expanding retail distribution networks. Growing demand for nutrient-rich stone fruits, improvements in cultivation practices, and advancements in cold chain logistics are further supporting market growth. Additionally, increasing consumption of peaches and nectarines in fresh, processed, and foodservice applications is contributing to the steady expansion of the market across Europe.

Key Market Trends

-

Rising consumer preference for fresh, healthy, and naturally sweet fruits is driving demand for peaches and nectarines across Europe.

-

Increasing awareness of the nutritional benefits of stone fruits is supporting market growth.

-

Expansion of supermarkets, hypermarkets, and online grocery platforms is improving product availability and accessibility.

-

Advancements in cultivation techniques, post-harvest handling, and cold chain logistics are enhancing fruit quality and reducing wastage.

-

Growing demand for fresh fruits in salads, desserts, beverages, and processed food applications is creating new market opportunities.

Segmental Insights

-

Based on product type, the peaches segment dominated the Europe peaches and nectarines market in 2025. The segment's leadership is attributed to its widespread consumer preference, extensive cultivation, and versatile use in fresh consumption and processed food products.

-

Based on distribution channel, the supermarkets segment held the largest share of the Europe peaches and nectarines market in 2025. The segment's dominance is driven by broad product availability, organized retail expansion, efficient supply chains, and consumer preference for one-stop shopping.

-

Based on application, the fresh consumption segment accounted for the largest share of the Europe peaches and nectarines market in 2025. The segment's growth is supported by strong cultural traditions, seasonal consumption patterns, and increasing consumer preference for fresh, minimally processed fruits.

Regional Insights

-

The Europe peaches and nectarines market is witnessing steady growth due to rising health consciousness, increasing fresh fruit consumption, and improvements in agricultural productivity.

-

Spain dominated the Europe peaches and nectarines market in 2025. The country's leadership is supported by favorable climatic conditions, extensive stone fruit cultivation, strong export capabilities, advanced farming practices, and a well-developed agricultural supply chain.

-

Italy remains a significant market due to its large production capacity, established horticulture sector, and growing domestic and export demand.

Competitive Landscape

The Europe peaches and nectarines market is moderately competitive, with producers and distributors focusing on product quality, sustainable farming practices, and expansion of distribution networks to strengthen their market positions. Companies are investing in advanced cultivation methods, post-harvest technologies, and strategic partnerships to meet the growing demand across retail, foodservice, and export markets. Key players operating in the Europe peaches and nectarines market include Agrupalmería, Anecoop, Consorzio Agricolo Frutticolo Veronese, SAT Royal, Frutas Montosa, Grupo El Ciruelo, Afrucat, Apoexpa, SanLucar Fruit S.L., BeFresh Ltd., and Gold Scorpion S.

Europe Peaches and Nectarines Market Size

The Europe peaches and nectarines market size was valued at USD 5.12 billion in 2025 and is projected to reach USD 6.36 billion by 2034 from USD 5.25 billion in 2026, growing at a CAGR of 2.43%.

Peaches and nectarines are virtually identical summer fruits that belong to the exact same plant species, Prunus persica. They are both stone fruits (drupes), meaning they feature juicy, sweet flesh wrapped around a large, hard central pit. The only true botanical difference between them comes down to a single gene variant. This market is deeply rooted in agricultural traditions, particularly in Southern Europe, where climatic conditions favor high quality production. Peaches and nectarines are prized for their sensory attributes, including sweetness, juiciness, and aromatic profiles, making them staple summer fruits for European consumers. According to Eurostat and the European Commission’s Agricultural Market Observatories, the European Union's structural stone fruit production typically generates upwards of 3 million tonnes of peaches and nectarines during stable harvest years, heavily concentrated across the core Mediterranean producing nations of Spain, Italy, and Greece. The sector is increasingly influenced by consumer preferences for sustainably grown produce, driving adoption of integrated pest management and organic farming practices. Regulatory frameworks such as the Common Agricultural Policy support farmers through direct payments and rural development programs, aiming to enhance competitiveness and environmental sustainability. As per the Eurostat, long-term monitoring of European fruit orchards reveals that while overall cultivation footprints undergo gradual consolidation and active orchard renewal, seasonal crop yields remain highly sensitive to changing regional weather anomalies and spring frost impacts. The market dynamics are shaped by seasonal availability, with peak consumption occurring between June and September. Retailers and wholesalers play a crucial role in distributing these perishable goods, requiring efficient cold chain logistics to maintain freshness. Consumer awareness regarding the nutritional benefits, including high vitamin C and fiber content, further supports demand. The industry faces ongoing transitions toward climate resilient varieties and water efficient irrigation systems to address environmental challenges.

MARKET DRIVERS

Rising Health Consciousness and Demand for Nutrient Dense Fresh Produce

The escalating focus on health and wellness among the consumers in the region contributes to the growth of the Europe peaches and nectarines market. This is because these fruits are recognized for their rich nutritional profile and low caloric density. Peaches and nectarines are excellent sources of vitamins A and C, potassium, and dietary fiber, which contribute to immune function, skin health, and digestive regularity. According to Eurostat and European Commission, statistical surveys tracking continental dietary habits show that only 12% of the EU population meets the recommended benchmark of five portions of fruit and vegetables daily, driving targeted regional health initiatives to increase fresh stone fruit consumption. The natural sweetness of these fruits makes them an ideal substitute for processed sugary snacks, aligning with trends toward clean eating and weight management. Nutritionists often recommend peaches and nectarines for their antioxidant properties, which help combat oxidative stress and inflammation. This scientific backing enhances consumer confidence and drives regular purchasing habits, particularly among health conscious demographics such as millennials and aging populations. Retailers have responded by highlighting the health benefits of stone fruits in marketing materials and in store displays, educating shoppers about their nutritional value. The versatility of peaches and nectarines in culinary applications, from fresh salads to grilled desserts, further encourages consumption. The perception of these fruits as natural, unprocessed, and wholesome resonates with consumers seeking to improve their overall well being. This health driven motivation creates a stable and growing demand base that supports market expansion despite seasonal limitations.

Expansion Of Premium And Organic Segments In Retail Channels

The rapid growth of premium and organic segments within the retail landscape significantly drives the Europe peaches and nectarines market. Consumers are increasingly prioritizing quality, safety, and sustainability. Organic peaches and nectarines are perceived as safer alternatives due to the absence of synthetic pesticides and fertilizers, appealing to environmentally conscious shoppers. As per the Research Institute of Organic Agriculture (FiBL), European organic retail sales have climbed past 54 billion euros annually, led by dominant national markets in Germany and France where fresh seasonal fruits represent a high-demand retail asset. Major supermarket chains across Germany, France, and the United Kingdom have expanded their organic produce sections, dedicating more shelf space to certified organic stone fruits. Consumers are willing to pay a price premium for organic certification, viewing it as a guarantee of higher quality and ethical production standards. The introduction of protected geographical indication labels for specific regional varieties, such as the Peach of Verona or the Nectarine of Calanda, further enhances product differentiation and value. These labels assure consumers of authentic origin and traditional cultivation methods, fostering brand loyalty. Retailers leverage these premium offerings to attract discerning customers who seek unique flavor profiles and superior texture. The trend toward local and seasonal sourcing also supports the premium segment, as consumers prefer fruits with shorter supply chains and lower carbon footprints. This shift toward quality over quantity ensures sustained growth for high value peach and nectarine varieties.

MARKET RESTRAINTS

Climate Change Induced Weather Volatility And Crop Instability

The increasing frequency and severity of extreme weather events caused by climate change directly impact crop yields and quality, which hampers the growth of the European peaches and nectarines market. Stone fruits are particularly sensitive to temperature fluctuations during critical growth stages, such as flowering and fruit set. Late spring frosts can devastate blossoms, leading to substantial production losses, while heatwaves during ripening can cause sunburn and premature drop. According to the European Environment Agency, the frequency of extreme weather events in Southern Europe has increased markedly in recent years, posing a serious threat to agricultural stability. In regions like Spain and Italy, which are major producers, irregular rainfall patterns and prolonged droughts have strained water resources, forcing farmers to reduce irrigation and accept lower yields. This volatility disrupts supply chains, leading to inconsistent availability and price spikes that deter consumers. The unpredictability of harvests makes it difficult for growers to plan long term investments and secure contracts with buyers. Furthermore, changing climatic conditions may alter the suitability of traditional growing regions, necessitating costly adaptations such as shifting to more resilient varieties or investing in advanced protection systems like anti hail nets. Small scale farmers, who constitute a significant portion of the sector, often lack the financial resources to implement these measures, making them particularly vulnerable. This environmental pressure threatens the long term viability of peach and nectarine cultivation in its traditional heartlands.

High Susceptibility to Pests and Diseases Increases Production Costs

The inherent susceptibility of peach and nectarine trees to various pests and diseases is a major restraint for the European market. This increases production costs and complicates cultivation practices. Common threats include brown rot, peach leaf curl, and fruit flies, which can severely damage crops if not managed effectively. According to the European and Mediterranean Plant Protection Organization, stone fruits require intensive monitoring and intervention to prevent outbreaks, leading to higher input costs for pesticides and labor. The strict regulatory environment in the European Union limits the use of certain chemical treatments, forcing growers to adopt more expensive and labor intensive integrated pest management strategies. Organic farmers face even greater challenges, as they rely on biological controls and natural remedies that may be less effective or slower acting. These constraints can result in lower yields and higher rejection rates due to cosmetic defects, reducing profitability. The need for frequent spraying and manual inspection increases operational expenses, squeezing margins for producers. Additionally, the emergence of resistant pest strains requires continuous research and development of new control methods, adding to the financial burden. Consumers are increasingly demanding residue free fruit, which further pressures growers to minimize chemical use while maintaining quality. This balance between efficacy, cost, and compliance creates a challenging operating environment. The risk of crop loss due to disease outbreaks remains a persistent concern, discouraging new entrants and limiting expansion.

MARKET OPPORTUNITIES

Development Of Climate Resilient and Low Chill Varieties

The development of climate-resilient and low-chill peach and nectarine varieties offers a significant opportunity for the Europe market. This helps to adapt to changing environmental conditions and extend production seasons. Breeders are focusing on creating cultivars that require fewer chilling hours, allowing for cultivation in warmer regions and earlier harvesting. According to the Joint Research Centre of the European Commission, research initiatives under the Horizon Europe program are prioritizing the development of crop varieties with enhanced tolerance to abiotic stresses such as drought and heat. These innovations enable farmers to mitigate the risks associated with late frosts and high temperatures, ensuring more stable yields. Low chill varieties also allow for production in Northern European regions, diversifying the geographic base of supply and reducing dependency on Southern countries. The introduction of new flavors and textures, such as flat peaches or donut peaches, appeals to consumers seeking novel sensory experiences, driving premium pricing. These unique varieties differentiate products in a crowded market and attract younger demographics interested in culinary experimentation. Collaborations between public research institutions and private breeding companies accelerate the commercialization of these advanced traits. The ability to offer extended season availability through staggered maturation times enhances market presence and revenue potential. This technological advancement supports the long term sustainability of the sector by aligning production capabilities with future climatic realities.

Growth Of Processed Peach Products And Value Added Innovations

The expansion of processed peach products and value-added innovations provides a major prospect for the Europe peaches and nectarines market. This paves the way to reduce waste and capture additional revenue streams. A significant portion of the peach harvest is suitable for processing into jams, juices, purees, and canned slices, providing stability against fresh market fluctuations. As per the European Association of Fruit and Vegetable Processors (PROFEL), the processed stone fruit pipeline relies on structured regional peach production to meet international consumer demand for value-added industrial canned, pureed, and frozen fruit products. Manufacturers are developing convenient ready to eat formats such as fruit cups, dried slices, and frozen chunks, catering to busy consumers seeking healthy snack options. The baby food industry increasingly utilizes peach puree for its mild taste and high nutritional value, opening a specialized niche. Innovations in packaging, such as resealable pouches and sustainable materials, enhance product appeal and shelf life. The use of byproducts like peach kernels for oil extraction adds further value, promoting a circular economy approach. Retailers are expanding their assortments of processed peach products, recognizing their consistent demand and longer storage capabilities. This diversification allows producers to utilize imperfect or surplus fruit that would otherwise be discarded, improving overall efficiency. The alignment with convenience and health trends ensures sustained growth for the processed segment. By leveraging processing technologies, the industry can stabilize incomes and reduce vulnerability to seasonal oversupply.

MARKET CHALLENGES

Labor Shortages and Rising Production Costs Challenge Profitability

Persistent labor shortages and rising production costs threaten the economic viability of many orchards, which challenges the growth of the Europe peaches and nectarines market. Harvesting peaches and nectarines is labor intensive, requiring careful hand picking to prevent bruising and ensure quality. According to COPA-COGECA and Eurostat, European fruit producers face severe operational pressures due to a structural deficit in seasonal field workers, accelerating the demand for automated harvesting alternatives. The aging demographic of farmers and the reluctance of younger generations to engage in physically demanding farm work exacerbate this issue. Reliance on migrant labor has become increasingly uncertain due to changing immigration policies and post pandemic restrictions. Labor shortages lead to delayed harvesting, resulting in overripe fruit and higher waste rates. Additionally, rising costs for energy, water, and fertilizers squeeze profit margins, making it difficult for small and medium sized farms to remain competitive. The investment required for mechanization is often prohibitive for stone fruit orchards due to the delicate nature of the fruit. These financial pressures force some growers to abandon production or switch to less labor intensive crops. The lack of affordable and efficient harvesting technology remains a bottleneck. Addressing this challenge requires policy interventions, improved working conditions, and innovation in automation. Without adequate solutions, the sector risks contraction and reduced domestic supply.

Intense Competition from Imported Stone Fruits and Substitutes

Intense competition from imported stone fruits and alternative fresh fruits exerts pressure on prices and the European peaches and nectarines market share. During the off season, imports from South America, particularly Chile and Argentina, flood the European market, offering lower priced alternatives that compete with stored domestic produce. As per the European Commission Eurostat COMEXT, counter-seasonal stone fruit imports entering EU borders ensure year-round availability for retail channels but place pressure on domestic Mediterranean growers during early and late shoulder marketing windows. Additionally, consumers have a wide array of substitute fruits such as berries, apples, and plums, which may be preferred due to price, convenience, or perceived health benefits. Berries, in particular, have gained popularity for their high antioxidant content and ease of consumption, diverting spending away from stone fruits. The global nature of the fruit market means that European producers must compete with regions having lower labor and land costs. Price sensitivity among consumers leads to switching behavior when domestic prices rise due to poor harvests or high production costs. Retailers often prioritize cheaper imported options to maintain margin targets, marginalizing local suppliers. The lack of strong branding for generic peaches and nectarines makes it difficult to differentiate them from imports. To remain competitive, European producers must focus on quality, sustainability, and local provenance. However, overcoming the price advantage of imports remains a persistent structural challenge.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 2.43% |

| Segments Covered | By Product Type, Distribution Channel, Application, Packaging Type, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | Agrupalmería, Anecoop, Consorzio Agricolo Frutticolo Veronese, SAT Royal, Frutas Montosa, Grupo El Ciruelo, Afrucat, Apoexpa, SanLucar Fruit S.L |

SEGMENTAL ANALYSIS

By Product Type Insights

The peaches segment led the Europe peaches and nectarines market and captured a significant share in 2025. This leading position of the segment was attributed to deep-rooted cultural preferences and traditional culinary applications across Mediterranean nations. Consumers in Spain, Italy, and Greece have historically favored the fuzzy texture and aromatic sweetness of peaches over their smooth skinned counterparts for fresh eating and dessert preparation. According to Eurostat and the European Commission, peach and nectarine production across the EU has balanced into a near-equal market split, with combined yields fluctuating dynamically across dominant Mediterranean growing clusters based on seasonal microclimatic changes. This dominance is reinforced by the extensive use of peaches in processed goods such as jams, canned slices, and baby food, where their softer flesh and higher juice content are technically superior. The established supply chains for peaches benefit from decades of infrastructure investment, ensuring efficient distribution from orchards to retail shelves. Older demographics, who constitute a significant portion of stone fruit consumers, demonstrate strong brand loyalty to traditional peach varieties. Retailers allocate prime shelf space to peaches during peak summer months, recognizing them as traffic drivers for the produce department. The versatility of peaches in both sweet and savory dishes further cements their status as a household staple. This cultural entrenchment creates a stable demand floor that buffers against short term market fluctuations.

The domination of the peach segment is further secured by its unparalleled versatility in industrial processing applications compared to nectarines. Food manufacturers prefer peaches for canning and puree production because their flesh maintains structural integrity during thermal processing while releasing desirable flavors. As per the European Association of Fruit and Vegetable Processors (PROFEL) Industrial Overviews, yellow clingstone peaches constitute the absolute foundation of the continent's processed stone fruit industry, utilizing specialized regional orchard supplies to fuel massive automated canning and pureeing plants. This industrial demand provides a crucial outlet for fruit that does not meet fresh market cosmetic standards, thereby stabilizing farm gate prices and reducing waste. The high sugar content and balanced acidity of processing grade peaches reduce the need for added sweeteners in final products, aligning with clean label trends. Beverage producers also favor peach concentrate for juices and nectars due to its consistent flavor profile and color stability. Long term contracts between growers and processors ensure predictable volumes and mitigate the risks associated with fresh market volatility. The economic efficiency of processing peaches makes them a more attractive crop for large scale agricultural operations. This symbiotic relationship between fresh and industrial markets ensures the continued leadership of the peach segment.

The nectarines segment is predicted to witness the highest CAGR of 4.8% from 2026 to 2034. This rapid expansion of the segment is fuelled by shifting consumer preferences toward convenience and superior eating quality. Modern consumers, particularly millennials and Gen Z, increasingly favor nectarines for their smooth skin which eliminates the need for peeling and offers a crispier texture reminiscent of apples. According to a study, smooth-skinned nectarines command high household penetration rates across Northern and Western European supermarkets, driven by consumer demand for snackable, peel-free fresh produce choices. The absence of fuzz addresses sensory aversions that some consumers associate with traditional peaches, expanding the addressable market. Nectarines are perceived as easier to eat on the go, fitting seamlessly into busy urban lifestyles and lunchbox routines. Retailers respond to this trend by featuring nectarines prominently in grab and go sections and promotional displays. Breeding programs have successfully improved the flavor and shelf life of nectarine varieties, overcoming historical issues with mealiness or blandness. This quality improvement has rebuilt consumer trust and encouraged repeat purchases. The visual appeal of shiny, unblemished nectarines also enhances impulse buying behavior in self service environments. As younger demographics gain purchasing power, this preference for convenient and texturally pleasing fruit is expected to accelerate.

The swift growth of the nectarines segment is significantly accelerated by innovation in flat and specialty varieties that offer unique sensory experiences and premium positioning. Flat nectarines, also known as donut nectarines or paraguayos, have gained immense popularity due to their intense sweetness, low acidity, and convenient shape. As per the Freshfel, European growers are actively diversifying their orchards with innovative, flat specialty stone fruit variations to capture premium retail margins and fulfill modern consumer lunchbox habits. These novel varieties command higher price points and attract adventurous eaters seeking differentiation from standard offerings. Their distinct appearance serves as a natural marketing tool on social media platforms, driving viral interest among younger consumers. Breeders continue to introduce new cultivars with enhanced aromas and extended harvest windows, ensuring consistent availability. Retailers leverage these specialty nectarines to differentiate their produce assortments and build customer loyalty. The premium nature of these varieties improves profit margins for both growers and retailers, incentivizing further investment. Educational campaigns highlighting the unique taste profiles help convert first time triers into regular buyers. This continuous stream of innovation keeps the category exciting and prevents commoditization. The success of flat nectarines demonstrates the market's readiness for novelty and quality driven growth.

By Distribution Channel Insights

The supermarkets segment dominated the Europe peaches and nectarines market and accounted for a substantial share in 2025. This dominance of the segment was driven by its extensive cold chain infrastructure that guarantees product quality and year round availability. These retail giants possess sophisticated logistics networks capable of maintaining optimal temperature and humidity levels from distribution centers to store shelves, which is critical for highly perishable stone fruits. According to EuroCommerce and the CBI, traditional supermarkets and modern discounters process over two-thirds of the fresh produce retail volume in major European consumer nations, utilizing highly optimized cold chains to anchor daily retail operations. Advanced ripening rooms allow retailers to deliver fruit at the perfect stage of maturity, enhancing consumer satisfaction and reducing household waste. The ability to source from multiple global origins enables supermarkets to offer peaches and nectarines even during the European off season, smoothing out seasonal supply gaps. Consistent quality standards and private label programs build consumer trust and encourage habitual purchasing. Promotional pricing and bundle deals drive volume sales during peak harvest periods. The physical presence of well lit and organized produce sections stimulates impulse purchases. This logistical superiority makes supermarkets the default destination for most consumers seeking reliable and high quality stone fruits.

The supremacy of the supermarket segment is reinforced by aggressive private label strategies and competitive pricing that make peaches and nectarines accessible to mass market consumers. Major chains like Tesco, Carrefour, and Rewe have developed proprietary stone fruit brands that offer consistent quality at lower price points than national brands. According to sources, private label fresh produce has grown faster than branded equivalents in key European markets, capturing value conscious shoppers. Direct sourcing relationships with growers eliminate intermediary markups, allowing retailers to pass savings onto customers while maintaining farmer margins. High volume purchasing power enables supermarkets to negotiate favorable terms and secure priority access to premium harvests. Weekly leaflets and digital apps feature peaches and nectarines as loss leaders or special offers, driving foot traffic and basket size. The integration of loyalty programs allows for targeted promotions based on individual purchase history. Consumers perceive supermarket private labels as trustworthy alternatives to premium brands, especially for everyday consumption. This price competitiveness is crucial during economic downturns when disposable income is constrained. The sheer volume of transactions through supermarkets solidifies their leadership position in the distribution landscape.

The online retail segment is estimated to register the fastest CAGR of 12.5% during the forecast period. This quick surge of the segment is fuelled by digital convenience and the proliferation of subscription box models. Busy urban consumers increasingly value the time saving aspect of home delivery, avoiding the hassle of in store shopping for heavy or bulky produce items. According to a study, digital grocery platforms in Europe retain elevated post-pandemic transaction volumes, though fresh fruit distribution remains predominantly tied to brick-and-mortar stores due to lingering consumer preferences for hands-on quality selection. Subscription services offering weekly boxes of seasonal stone fruits create recurring revenue streams and foster brand loyalty through curated experiences. Algorithms personalize recommendations based on past purchases, increasing cross selling opportunities for complementary products like yogurt or granola. Detailed product descriptions and customer reviews reduce the perceived risk of buying perishables unseen. Flexible delivery slots and contactless options cater to diverse lifestyle needs. The ability to compare prices and origins instantly empowers informed decision making. Digital platforms also facilitate direct to consumer sales for niche growers, bypassing traditional wholesale channels. This technological enablement lowers barriers to entry and expands market reach beyond geographic limitations. As digital natives age into primary household shoppers, this growth trajectory is poised to continue.

The rapid expansion of online retail is fueled by its ability to offer premium positioning and enhanced traceability that justifies higher price points for specialty peaches and nectarines. E commerce platforms excel at storytelling, providing detailed information about farm practices, varietal characteristics, and sustainability credentials that physical stores cannot easily display. As per European Commission, consumer groups highlight a clear willingness among premium retail cohorts to pay a higher market margin for fresh stone fruit that carries verifiable geographic indicators (such as IGP) and ethical supply chain certifications. High resolution imagery and video content showcase the visual appeal and texture of premium varieties, stimulating desire. Direct feedback loops allow sellers to quickly address quality concerns and build trust. Exclusive online only varieties or limited edition harvests create scarcity and urgency. Integration with social media influencers amplifies reach and validates product quality through authentic endorsements. The transparency of digital supply chains appeals to ethically minded consumers seeking connection with producers. Data analytics optimize inventory management, reducing waste and ensuring peak freshness upon delivery. This value added proposition differentiates online retail from commoditized brick and mortar competition. The alignment with modern values of transparency and convenience drives sustained adoption.

By Application Insights

In 2025, the fresh consumption segment held the majority share of the Europe peaches and nectarines market because of entrenched cultural traditions and seasonal rituals surrounding stone fruit enjoyment. In Mediterranean countries, eating fresh peaches and nectarines is an integral part of summer dining, often served as dessert or incorporated into salads and breakfasts. According to the OECD FAO, fresh fruit consumption per capita in Southern Europe remains among the highest globally, underpinned by dietary habits passed down through generations . The sensory experience of biting into a ripe, juicy fruit is irreplaceable and deeply emotional for many consumers. Farmers markets and roadside stands reinforce this connection to seasonality and local agriculture. Retailers capitalize on this nostalgia through evocative merchandising and sampling events. The health halo associated with fresh produce further supports daily intake as part of balanced diets. Unlike processed forms, fresh fruit retains maximum nutritional value and fiber content, appealing to wellness focused individuals. Social gatherings and family meals frequently feature fresh stone fruits as centerpieces. This cultural embeddedness creates resilient demand that withstands price fluctuations. The immediacy of fresh consumption ensures it remains the primary application for the vast majority of production.

The prominence of fresh consumption is reinforced by rising health awareness and clean label trends that prioritize whole, unprocessed foods. Consumers increasingly scrutinize ingredient lists and avoid added sugars, preservatives, and artificial additives commonly found in processed fruit products. According to the European Commission’s Farm to Fork Strategy, promoting fresh fruit and vegetable consumption is a key pillar of public health policy aimed at reducing diet related diseases . Nutritionists and healthcare providers actively recommend fresh peaches and nectarines for their vitamin, mineral, and antioxidant content. The natural sweetness satisfies sugar cravings without the glycemic impact of refined sweets. Schools and workplace cafeterias are replacing processed snacks with fresh fruit options to promote healthier environments. Media coverage of the benefits of plant based diets further elevates the status of fresh stone fruits. Transparency in farming practices, such as organic or regenerative agriculture, enhances the appeal of fresh produce. The perception of freshness equates to purity and safety in the minds of many shoppers. This health driven paradigm shift structurally favors fresh consumption over alternative applications. Government initiatives subsidizing fresh fruit in schools also bolster long term habit formation.

The beverages segment is growing at the fastest CAGR of 6.2% due to innovation in functional drinks and the demand for natural sweetening agents. Beverage manufacturers are increasingly incorporating peach and nectarine purees and concentrates into smoothies, kombuchas, and sparkling waters to provide natural flavor and sweetness without artificial additives. According to research, launches of fruit based functional beverages in Europe grew by double digits last year, with stone fruits being a top trending ingredient. The mild acidity and floral notes of peaches pair well with probiotics and adaptogens, enhancing palatability. Consumers seek hydration solutions that offer additional health benefits beyond basic thirst quenching. The rise of sober curiosity and alcohol alternatives has created new opportunities for sophisticated non alcoholic beverages featuring complex fruit profiles. Ready to drink formats cater to on the go consumption occasions. Clean label mandates push formulators toward recognizable fruit ingredients over synthetic flavors. The versatility of peach concentrate allows for consistent flavor across batches and seasons. Marketing emphasizes the natural origin and functional benefits, resonating with health conscious demographics. This convergence of wellness and indulgence fuels rapid category expansion.

The swift growth of the beverages segment is further propelled by the alcohol alternative trend and the rise of craft mixology utilizing peach and nectarine ingredients. Bartenders and home enthusiasts are experimenting with fresh muddled fruit, syrups, and shrubs to create complex non alcoholic cocktails and low ABV spritzes. According to sources, the no and low alcohol category in Europe is projected to grow significantly, with fruit forward flavors leading innovation. Peaches and nectarines provide body and mouthfeel that mimics alcoholic spirits, enhancing the sensory experience of abstention. Seasonal menus at bars and restaurants highlight fresh stone fruits as premium ingredients, driving visibility and trial. Bottled and canned cocktail alternatives featuring real fruit juice are gaining shelf space in retail and convenience channels. The aesthetic appeal of peach colored beverages performs well on social media, generating organic buzz. Collaborations between fruit growers and beverage brands create co marketed products that leverage dual audiences. The sophistication of modern mixology elevates peaches from simple garnish to star ingredient. This cultural shift redefines the role of stone fruits in adult beverage occasions. The premiumization of non alcoholic options supports higher value utilization of fruit.

REGIONAL ANALYSIS

Spain Peaches and Nectarines Market Analysis

Spain outperformed other countries in the Europe peaches and nectarines market in 2025. This leading position was due to its position as the continent’s leading producer and exporter. According to the Spanish Ministry of Agriculture, Fisheries and Food (MAPA) and FEPEX, Spain acts as the definitive market leader in European stone fruit cultivation, generating roughly 40% of the entire European Union's fresh peach and nectarine supply. The country’s diverse microclimates, particularly in Murcia, Valencia, and Aragon, enable an extended harvest window from May to October, ensuring consistent supply to domestic and export markets. As per the Spanish Ministry of Agriculture, Fisheries and Food (MAPA), Spain manages a highly concentrated export window that ships roughly 700,000 tonnes of fresh stone fruits into foreign European distribution chains annually. Advanced irrigation technologies and intensive planting systems maximize yield efficiency despite water scarcity challenges. Spanish growers lead in the adoption of flat nectarine varieties, responding swiftly to evolving consumer preferences. Strong cooperative structures facilitate collective marketing and investment in post harvest infrastructure. The proximity to key European markets reduces transport times and costs, enhancing competitiveness against Southern Hemisphere imports. Domestic consumption remains robust, supported by cultural affinity for fresh stone fruits. Government support through CAP funds aids modernization and sustainability transitions. Spain’s integrated supply chain from nursery to retail sets the benchmark for the region. Its strategic role as the primary supplier underpins the entire European market’s stability.

Italy Peaches and Nectarines Market Analysis

Italy was positioned second in the Europe peaches and nectarines market in 2025. It is renowned for its high-quality Protected Geographical Indication varieties and strong domestic consumption culture. Regions like Emilia Romagna and Lazio produce premium peaches such as the Pesca di Verona IGP, commanding price premiums in both domestic and export markets. According to ISMEA, Italy securely tracks as Europe's second-largest stone fruit producer, contributing roughly one-fifth of total EU peach and nectarine volume with a heavy commercial focus on premium fresh retail varieties. Italian consumers exhibit strong loyalty to local and regional varieties, supporting shorter supply chains and sustainable agriculture. The processing sector is well developed, absorbing surplus fruit for canned and pureed products, stabilizing farm incomes. Research institutions collaborate closely with growers to develop climate resilient cultivars suited to changing conditions. Tourism boosts direct sales through agritourism and farm shops, enhancing consumer education. Export markets in Germany and Austria value Italian stone fruits for their superior flavor and safety standards. Challenges include aging orchards and labor shortages, prompting mechanization investments. Italy’s emphasis on quality over quantity distinguishes its market position. The cultural prestige of Italian stone fruits sustains demand despite competitive pressures.

France Peaches and Nectarines Market Analysis

France is a significant player in the Europe peaches and nectarines market due to strong domestic production and premium retail positioning. The Rhône Valley and Provence regions are celebrated for their aromatic and flavorful varieties, including the Pêche de Vigne and Nectarine de Drôme. As per Agreste (the statistical service of the French Ministry of Agriculture), France sustains a high-value stone fruit sector that accounts for approximately 6% of overall EU output, prioritizing specialized domestic marketing channels and stringent eco-certifications. French consumers prioritize taste and origin, willingly paying premiums for locally grown and labeled products. Retailers like Monoprix and Biocoop emphasize organic and regional stone fruits, aligning with national sustainability goals. The processing industry utilizes domestic fruit for artisanal jams and compotes, supporting value addition. Climate change poses risks, but adaptation efforts include shade nets and drought tolerant rootstocks. Imports supplement domestic supply during early and late seasons, primarily from Spain. Government policies support agroecological transitions and young farmer installation. The cultural appreciation for gastronomy elevates stone fruits beyond commodity status. France’s market is defined by discerning consumers and quality driven production. This focus on terroir and authenticity secures its niche in the broader European landscape.

Germany Peaches and Nectarines Market Analysis

Germany plays a key role in the European market. It holds a major position as the largest import landscape and consumer base for peaches and nectarines in Northern Europe, despite minimal domestic production. German consumers exhibit high per capita consumption of stone fruits, driven by health consciousness and multicultural dietary influences. According to the Federal Office for Agriculture and Food (BLE) and Destatis, Germany serves as the primary European import hub for fresh stone fruits, drawing over 240,000 tons of fresh peaches and nectarines annually to fulfill consumer retail demand. Retailers like Aldi, Lidl, and Rewe dominate distribution, leveraging private labels and aggressive promotions to drive volume. Organic and fair trade certified stone fruits enjoy strong demand, reflecting environmental and ethical priorities. The discount channel plays a crucial role in making stone fruits accessible to mass market consumers. Seasonal peaks coincide with summer holidays, boosting sales. Logistics hubs in Hamburg and Rotterdam facilitate efficient redistribution to Central and Eastern Europe. Consumer education campaigns promote the nutritional benefits of stone fruits. Price sensitivity is balanced with quality expectations, especially for organic segments. Germany’s role as the primary demand engine shapes production planning in supplying countries. Its mature retail infrastructure ensures consistent availability and quality standards.

Greece Peaches and Nectarines Market Analysis

Greece maintains a vital position in the Europe peaches and nectarines market as a key producer of high-quality processing and fresh varieties, particularly in the regions of Imathia and Pella. According to Eurostat, Greece maintains a unique market profile within the EU by contributing roughly 15% of total stone fruit volumes, intentionally weighting its supply chains toward processed industrial peach output. As per Enterprise Greece and the Greek Canners Association (DELCOF), Greece stands as the undisputed global leader in the processed stone fruit market, operating as the number-one international exporter of canned peaches worldwide. Domestic fresh consumption is culturally embedded, with peaches featuring prominently in summer diets. Growers benefit from favorable climatic conditions and traditional expertise, though water management is an increasing concern. Cooperatives play a central role in aggregation, processing, and marketing, ensuring smallholder viability. Exports to Balkan and Eastern European markets are growing, diversifying beyond traditional Western destinations. Organic production is expanding, supported by EU rural development funds. Labor availability remains a challenge, prompting seasonal worker programs. Greece’s dual strength in fresh and processed segments provides resilience against market volatility. The reputation for safe and tasty fruit sustains export competitiveness. Strategic investments in modern packing houses enhance quality and efficiency.

COMPETITIVE LANDSCAPE

The competition in the Europe peaches and nectarines market is characterized by a mix of large agricultural cooperatives and independent producers who vie for dominance through quality differentiation and supply chain efficiency. The market exhibits moderate fragmentation with established players holding strong positions in specific geographic regions and retail channels. Key competitors distinguish themselves through certified sustainable practices protected geographical indications and innovative variety offerings rather than price alone. Barriers to entry remain significant due to high capital requirements for orchard establishment and compliance with strict phytosanitary regulations. Companies invest significantly in research and development to create climate resilient cultivars that ensure stable yields despite weather volatility. Brand reputation and trust are critical assets as retailers prioritize reliable suppliers with consistent quality standards. Strategic alliances with retail chains enhance market penetration and shelf visibility. The competitive landscape is further shaped by the growing demand for transparency which forces players to adopt digital traceability systems. Innovation in post harvest technologies serves as a key differentiator. Overall the market rewards entities that can combine agricultural excellence with robust logistical capabilities and genuine commitment to sustainability.

KEY MARKET PLAYERS

Some of the notable key players in the Europe peaches and nectarines market are

- Agrupalmería

- Anecoop

- Consorzio Agricolo Frutticolo Veronese

- SAT Royal

- Frutas Montosa

- Grupo El Ciruelo

- Afrucat

- Apoexpa

- SanLucar Fruit S.L.

- BeFresh Ltd.

- Gold Scorpion S.

Top Players in the Market

- Agrupalmería operates as a leading cooperative based in Almería Spain with a significant footprint in the European peaches and nectarines market through its extensive network of affiliated growers. The company focuses on producing high quality stone fruits that meet stringent international safety and sustainability standards. Recent actions include investing in advanced sorting and packaging technologies to enhance fruit presentation and extend shelf life for export markets. Agrupalmería has strengthened its market position by obtaining GlobalGAP and GRASP certifications which reassure European retailers of ethical and safe production practices. The cooperative actively promotes integrated pest management techniques to reduce chemical usage aligning with EU environmental goals. Their commitment to social responsibility includes fair labor practices and community support programs. Agrupalmería collaborates closely with research institutions to develop climate resilient varieties suited to changing weather patterns. This holistic approach ensures consistent supply and premium quality reinforcing their reputation among major European distributors and retailers.

- Anecoop is a prominent agricultural cooperative headquartered in Valencia Spain specializing in the production and export of peaches and nectarines to key European markets. The company leverages its large member base to achieve economies of scale and consistent product availability throughout the harvest season. Recent strategic initiatives include expanding its cold storage infrastructure to maintain optimal fruit quality during transportation and distribution. Anecoop has strengthened its position by launching private label programs for major supermarket chains offering customized packaging and branding solutions. The cooperative emphasizes sustainable water management practices addressing regional scarcity issues through efficient irrigation systems. Their focus on traceability allows consumers to verify the origin and farming methods of their purchases. Anecoop actively participates in international trade fairs to showcase new varieties and build relationships with buyers. This customer centric strategy enhances brand loyalty and secures long term contracts. Their dedication to innovation and sustainability drives continuous improvement in product quality and operational efficiency.

- Consorzio Agricolo Frutticolo Veronese represents a key player in the Italian peach sector managing the production and marketing of protected geographical indication varieties such as the Pesca di Verona IGP. The consortium unites local growers to preserve traditional cultivation methods while adopting modern quality control standards. Recent actions include implementing rigorous certification protocols to protect the authenticity and reputation of their regional brand in European markets. The consortium has strengthened its market position by promoting direct sales channels and agritourism initiatives that connect consumers with producers. They invest in educational campaigns highlighting the unique sensory attributes and cultural heritage of their peaches. Collaborations with gourmet restaurants and specialty retailers enhance visibility and prestige. The consortium supports members in transitioning to organic farming practices meeting growing demand for chemical free produce. Their focus on territorial identity and quality differentiation commands premium pricing. This strategic emphasis on heritage and excellence sustains their competitive advantage in the premium segment of the European market.

Major Strategies Used By Key Market Participants

Key players in the Europe peaches and nectarines market employ several strategic approaches to maintain competitiveness and drive growth amidst evolving consumer preferences and environmental challenges. Product differentiation through protected geographical indications and organic certification serves as a primary strategy to command premium prices and build brand loyalty. Companies invest heavily in sustainable farming practices including water conservation and integrated pest management to align with regulatory requirements and consumer values. Supply chain optimization through advanced cold chain logistics and automated sorting technologies ensures consistent quality and reduces waste. Strategic partnerships with major retailers facilitate private label opportunities and secure stable distribution channels. Innovation in variety development focuses on creating climate resilient and novel textures such as flat peaches to attract diverse consumer segments. Digital marketing and traceability platforms enhance transparency and consumer trust. These combined strategies enable participants to navigate market volatility and capitalize on the growing demand for high quality sustainable stone fruits.

MARKET SEGMENTATION

This research report on the Europe peaches and nectarines market has been segmented and sub-segmented based on categories.

By Product Type

- Peaches

- Nectarines

- Combos

By Distribution Channel

- Supermarkets

- Online Retail

- Farmers' Markets

- Convenience Stores

By Application

- Fresh Consumption

- Processing

- Canning

- Beverages

By Packaging Type

- Bags

- Boxes

- Cans

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is the Europe peaches and nectarines market?

The Europe peaches and nectarines market comprises the cultivation, production, distribution, import, export, and consumption of fresh and processed peaches and nectarines across European countries.

2. What factors are driving the growth of the Europe peaches and nectarines market?

The market is driven by increasing consumer demand for fresh fruits, growing awareness of healthy eating, expanding retail networks, and rising exports of premium-quality stone fruits.

3. Which countries are the leading producers of peaches and nectarines in Europe?

Spain, Italy, Greece, France, and Portugal are among the leading producers, benefiting from favorable climatic conditions and well-established horticultural industries.

4. Which product type dominates the Europe peaches and nectarines market?

Peaches account for the largest market share due to their widespread consumption as fresh fruit and use in processed food products.

5. Which distribution channel holds the largest share of the Europe peaches and nectarines market?

Supermarkets and hypermarkets dominate the market owing to their extensive retail networks, consistent product availability, and consumer convenience.

6. What are the major applications of peaches and nectarines?

Peaches and nectarines are widely consumed fresh and are also used in processing, canning, juices, desserts, jams, bakery products, and beverages.

7. What challenges does the Europe peaches and nectarines market face?

The market faces challenges such as climate change, seasonal production, labor shortages, pest infestations, and fluctuations in transportation and logistics costs.

8. How is sustainability influencing the Europe peaches and nectarines market?

Growers are increasingly adopting sustainable farming practices, efficient irrigation systems, integrated pest management, and eco-friendly packaging to meet environmental regulations and consumer expectations.

9. What are the key trends shaping the Europe peaches and nectarines market?

Major trends include increasing demand for organic fruits, premium fruit varieties, sustainable packaging, digital traceability, and growth in online grocery retail.

10. Who are the key players in the Europe peaches and nectarines market?

Major companies include Agrupalmería, Anecoop, Consorzio Agricolo Frutticolo Veronese, SAT Royal, Frutas Montosa, Grupo El Ciruelo, SanLucar Fruit S.L., and BeFresh Ltd.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com