Europe Peptide Therapeutics Market Size, Share, Trends & Growth Forecast Report By Type, Application, Type of Manufacturers, Route of Administration, Synthesis Technology and Country (Germany, UK, France, Italy, Rest of Europe) – Industry Analysis From 2025 to 2033.

Europe Peptide Therapeutics Market Size

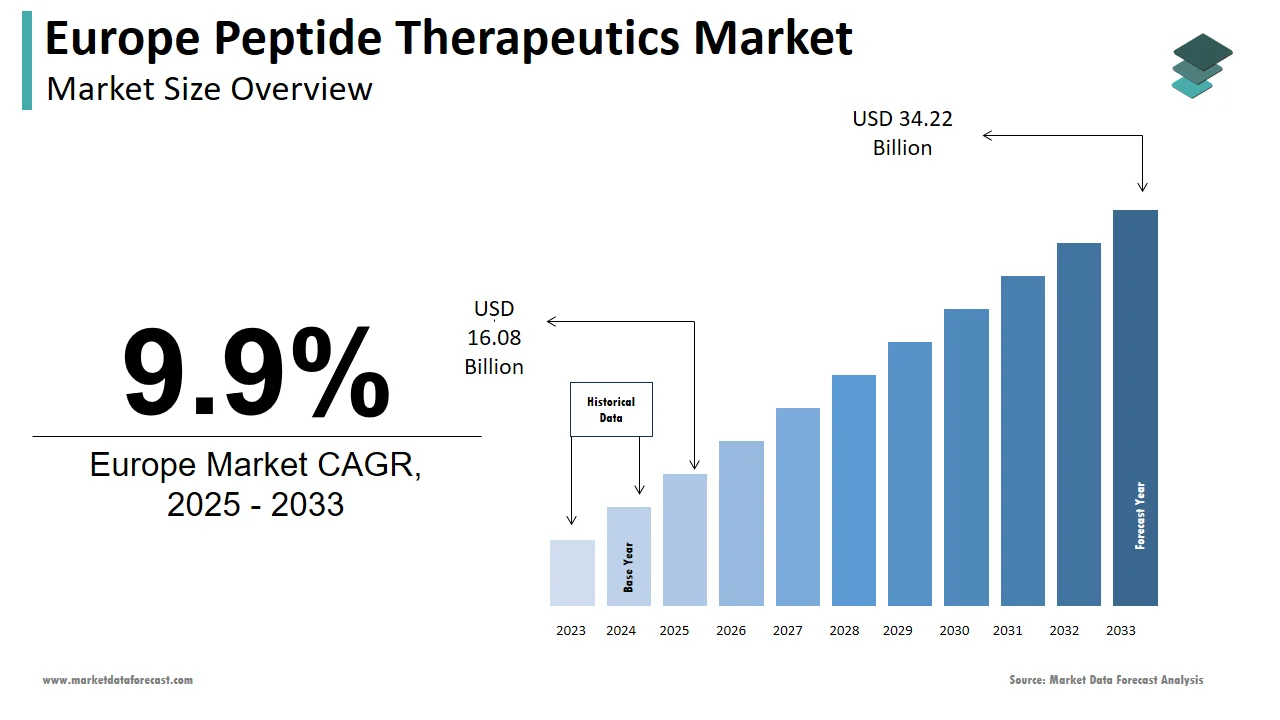

The peptide therapeutics market size in Europe was valued at USD 14.63 billion in 2024. The European market is estimated to be worth USD 34.22 billion by 2033 from USD 16.08 billion in 2025, growing at a CAGR of 9.9% from 2025 to 2033.

MARKET DRIVERS

Prevalence of Chronic and Metabolic Disorders

The growing prevalence of chronic and metabolic disorders across Europe primarily drives the growth of the European peptide therapeutics market. Peptide-based therapies are derived from naturally occurring peptides in the human body that offer the potential for hormone growth, neurotransmission and anti-infective treatments. With approximately 7,000 naturally occurring peptides identified, peptide therapeutics help maintain balanced peptide levels. The rising number of cancer cases in Europe, reported at around 1.4 million in males and 1.2 million in females, has led to increased demand for peptide therapeutics in cancer treatment. Researchers are focused on diagnosing and treating cancer early to improve patient outcomes, and peptide-based therapies have shown promise in this area. Recombinant peptides and laboratory-developed peptides are utilized in the treatment of cancer, contributing to the advancement of anticancer therapies.

Advancements in New Therapies and Treatments

An increasing number of advancements in the development of new therapies and treatments further boost the growth rate of the European peptide therapeutics market. Researchers are focusing on peptide-based therapies for various diseases, including oral peptide drug nanoparticles for managing glucose levels in diabetic patients. The growing support from healthcare organizations, investments from public and private organizations, and the approval of therapies and drugs contribute to market growth in the European region.

The growing demand for peptide therapeutics in the treatment of various diseases, rapid adoption of peptide-based therapies for cancer treatment, advancements in the development of new therapies and drugs based on peptides and growing focus on the development of oral peptide drug nanoparticles for diabetes management boost the growth rate of the European peptide therapeutics market.

Support from Healthcare Organizations for Peptide Therapeutics R&D

Support from healthcare organizations for peptide therapeutics research and development, increased investment from public and private organizations in peptide therapy development, growing number of therapy and drug approvals for peptide-based treatments, rising awareness among healthcare professionals about the benefits of peptide therapeutics and favorable government regulations and policies supporting the use of peptide therapeutics in healthcare boost the growth rate of the European market.

MARKET CHALLENGES

High Cost of Novel Peptide Drug Development

The high cost of novel peptide drug development is one of the key factors hampering the growth of the European peptide therapeutics market. Lack of awareness, shortage of skilled professionals, stringent regulations, and inadequate reimbursement policies impede market growth in Europe. The side effects associated with peptide therapeutics such as numbness of hands and feet and fatigue hinders the market's growth rate in the European region.

COUNTRY LEVEL ANALYSIS

Europe had a substantial share of the global market in 2024 and is expected to grow at a healthy CAGR during the forecast period owing to the widespread adoption of peptide therapeutics, increased healthcare spending, initiatives from the governments of European countries to facilitate the introduction of novel drugs and therapies and awareness campaigns promoting the benefits of peptide therapies.

Germany led the peptide therapeutics market in Europe in 2024 and is expected to continue to lead the regional market throughout the forecast period. The availability of a robust pharmaceutical industry, increasing manufacturing activities of peptide drugs and advanced laboratory facilities in Germany drive the German market growth. The availability of peptide drugs in medical stores and pharmacies further fuels the growth rate of the German market.

The UK peptide therapeutics market is anticipated to grow at a prominent CAGR during the forecast period owing to the presence of clinical trial centers and hospitals adopting peptide therapies, manufacturing capabilities that ensure the production of high-quality peptides.

KEY MARKET PLAYERS

Companies playing a significant role in the European peptide therapeutics market profiled in this report are Eli Lilly and Company, Amgen, Inc., Pfizer, Inc., Bristol-Myers Squibb Company, Ever Neuro Pharma GmbH, Takeda Pharmaceutical Company Limited, AstraZeneca PLC, GlaxoSmithKline plc, Novo Nordisk A/S., Novartis AG, Zealand Pharma AG, AmbioPharm Inc., Bachem Holding AG, PolyPeptide Group, Sanofi SA, Amylin Pharmaceuticals, CirclePharma, Inc., PeptiDream Inc., Apitope Technology, Arch NioPartners, and Galena Biopharmaceuticals.

MARKET SEGMENTATION

This Europe peptide therapeutics market research report is segmented and sub-segmented into the following categories.

By Type

- Generic

- Innovative

By Application

- Metabolic

- Cardiovascular Disorder

- Respiratory

- GIT

- Anti-infection

- Pain

- Dermatology

- CNS

- Renal

- Others

By Type of Manufacturers

- In-house

- Outsourced

By Route of Administration

- Parenteral Route

- Oral Route

- Pulmonary

- Mucosal

- Others

By Synthesis Technology

- Solid Phase Peptide Synthesis (SPPS)

- Liquid Phase Peptide Synthesis (LPPS)

- Hybrid Technology

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com