Europe Pharmacovigilance Market Size, Share, Trends & Growth Forecast Report By Clinical Trial Phase, Service Provider, Method & Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe) - Industry Analysis, From (2026 to 2034)

Market Size, 2025

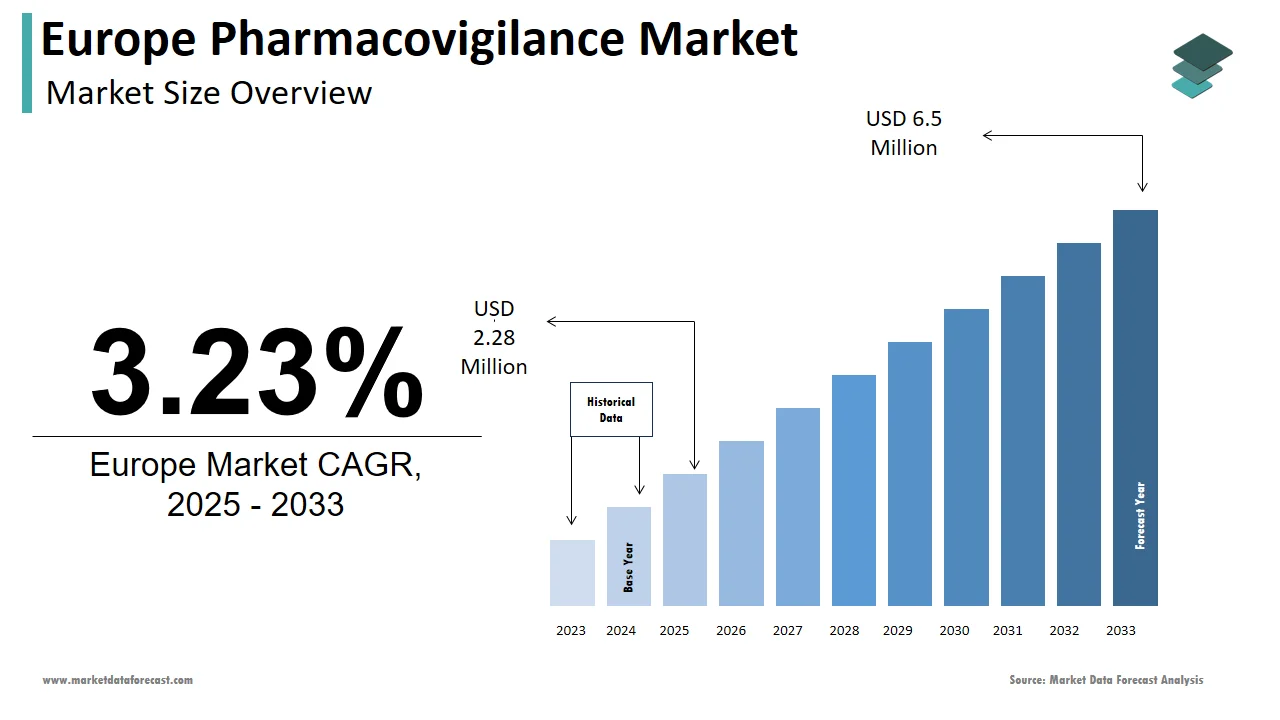

$2.28 MnMarket Estimate, 2026

$2.35 MnMarket Forecast, 2034

$3.04 MnCAGR, 2026–2034

3.23%Europe Pharmacovigilance Market Report Summary

The Europe pharmacovigilance market was valued at USD 2.28 million in 2025, is estimated to reach USD 2.35 million in 2026, and is projected to reach USD 3.04 million by 2034, growing at a CAGR of 3.23% during the forecast period from 2026 to 2034.

The growth of the European pharmacovigilance market is driven by the rising incidence of adverse drug reactions (ADRs), stringent regulatory requirements, and the expansion of post-marketing surveillance activities across the region. Increasing pharmaceutical R&D expenditure, growing drug approvals, and the outsourcing of pharmacovigilance services to specialized providers are further accelerating market expansion across Europe.

Key Market Trends

- Increasing regulatory focus on patient safety and real-time adverse event reporting across European nations.

- Growing adoption of AI and data analytics for automated signal detection and pharmacovigilance data management.

- Rising trend of outsourced pharmacovigilance services to improve operational efficiency and compliance.

- Integration of centralized reporting systems and harmonized EU frameworks to strengthen drug safety monitoring.

- Expanding collaborations between CROs, pharmaceutical firms, and regulatory authorities to enhance risk management and post-marketing surveillance.

Segmental Insights

- Based on clinical trial phase, the phase IV segment held the largest share of 43.6% of the Europe pharmacovigilance market in 2024, driven by increased emphasis on post-marketing safety surveillance and long-term patient outcome tracking after drug commercialization.

- Based on service provider, the contract outsourcing segment led the market in 2024, accounting for a 62.5% share, supported by the growing reliance of pharmaceutical companies on external expertise and cost-effective compliance management.

- Based on method, the spontaneous reporting segment dominated the Europe pharmacovigilance market with a 58.4% share in 2024, attributed to its critical role in early detection of adverse drug events and its wide adoption across healthcare and regulatory frameworks.

Regional Insights

The European pharmacovigilance market is experiencing consistent growth across leading economies, supported by regulatory harmonization, expanding pharmaceutical R&D, and the digitization of safety reporting systems.

- Germany led the regional market and captured an 18.5% share in 2024, driven by its strong pharmaceutical base and advanced pharmacovigilance infrastructure.

- The United Kingdom followed closely, holding a 16.2% share in 2024, supported by its robust regulatory framework and technological adoption in drug safety analytics.

- France is growing steadily due to its centralized national pharmacovigilance network and academic collaboration for real-world evidence studies.

- Switzerland is expected to grow between 2025 and 2033, supported by its concentration of global pharma headquarters and regulatory alignment with EU pharmacovigilance protocols.

Competitive Landscape

The European pharmacovigilance market is moderately consolidated, with key players focusing on technological integration, automation of safety workflows, and strategic collaborations to enhance operational scalability. Companies are investing in AI-powered pharmacovigilance platforms, data analytics solutions, and global outsourcing networks to strengthen compliance and risk management efficiency. Prominent players include Boehringer Ingelheim, Accenture, Bristol-Myers Squibb, IQVIA Holdings Inc, Covance, ICON, Parexel International Corporation, Quintiles, United BioSource, Synowlwedge, and Cognizant Technology Solutions Corporation.

Europe Pharmacovigilance Market Size

The pharmacovigilance market size in Europe was valued at USD 2.28 million in 2025. The European market is estimated to be worth USD 3.04 million by 2034 from USD 2.35 million in 2026, growing at a CAGR of 3.23% from 2026 to 2034.

Pharmacovigilance is the scientific and activity-based process of detecting, assessing, understanding, and preventing adverse effects or other problems related to pharmaceutical products and vaccines. It encompasses the systematic monitoring of pharmaceutical products throughout their life cycle to ensure patient safety and regulatory compliance. The European Medicines Agency plays a central role in coordinating pharmacovigilance activities through the EU pharmacovigilance system, which integrates national competent authorities and marketing authorization holders. According to the European Medicines Agency, over a million suspected adverse drug reaction reports are submitted annually to the EudraVigilance database by all sources, including healthcare professionals, patients, and marketing authorization holders. In 2024, for instance, 1,757,524 ICSRs were collected and managed in EudraVigilance. As per a study, adverse drug reactions are a common cause of hospital admissions and a significant healthcare burden. The system also mandates risk management plans for new medicinal products and requires continuous signal detection and benefit-risk reassessment post-authorization. These structural and procedural requirements distinguish Europe’s pharmacovigilance framework as one of the most comprehensive globally and form the operational backbone of its drug safety ecosystem.

MARKET DRIVERS

Rising Incidence of Adverse Drug Reactions Fuels Pharmacovigilance Demand

Adverse drug reactions represent a significant public health burden across European healthcare systems and serve as a primary driver for the growth of the Europe pharmacovigilance market. Adverse drug reactions are a significant cause of mortality within the European Union. As per sources, A notable proportion of hospital admissions in high-income European countries results from medication-related harms. This burden is exacerbated by polypharmacy trends, especially among aging populations. The European Union has a substantial and aging population, with a significant percentage of individuals aged sixty or above. Patients who take multiple medications concurrently face an increased risk of experiencing an adverse drug event. Regulatory authorities have responded by strengthening post-marketing surveillance mandates under the EU pharmacovigilance legislation, which requires continuous safety monitoring and expedited reporting of serious adverse events. These developments compel pharmaceutical companies and contract research organizations to expand pharmacovigilance operations, driving demand for specialized services and digital safety databases such as EudraVigilance. Consequently, the rising clinical and economic toll of drug-induced complications continues to reinforce the indispensability of pharmacovigilance across Europe.

Stringent Regulatory Frameworks Mandate Comprehensive Safety Monitoring

Its rigorous and evolving regulatory landscape compels continuous investment in drug safety infrastructure, which in turn propels the expansion of the Europe pharmacovigilance market. The legislation that established the harmonized pharmacovigilance system in the EU consists of Directive 2010/84/EU and Regulation (EU) No 1235/2010. According to the European Commission, all marketing authorization holders must establish a pharmacovigilance system master file and appoint a qualified person for pharmacovigilance residing within the EU. The legislation also introduced mandatory risk management plans for all new molecular entities, which must include proactive safety monitoring strategies and mitigation measures. Non-compliance can result in significant penalties or suspension of marketing authorizations. These regulatory requirements have elevated pharmacovigilance from a reactive compliance function to a strategic operational necessity. Consequently, pharmaceutical firms increasingly outsource these activities to specialized providers equipped with trained personnel and technological capabilities to manage complex reporting obligations across multiple jurisdictions while maintaining full alignment with EU Good Pharmacovigilance Practices.

MARKET RESTRAINTS

High Operational Costs of Pharmacovigilance Infrastructure

Establishing and maintaining pharmacovigilance systems entails substantial financial and human resource commitments, which are among the key factors restricting the growth of the Europe pharmacovigilance market. Moreover, staffing a pharmacovigilance department requires highly trained professionals, including qualified persons for pharmacovigilance, signal detection analysts, and medical reviewers with advanced clinical or pharmacological expertise. Apart from these, organizations must invest in validated safety databases compliant with EudraVigilance gateway standards, electronic data capture systems, and signal management software, all of which require continuous updates and validation audits. The cost burden intensifies with the obligation to monitor global safety data even for products marketed only in Europe due to the EU’s requirement for worldwide adverse event reporting. For generic and biosimilar manufacturers operating on narrow profit margins, these expenses can be prohibitive, limiting their capacity to scale pharmacovigilance functions internally. Consequently, while regulatory compliance is non-negotiable, the financial intensity of meeting pharmacovigilance mandates acts as a structural barrier, particularly in an environment of pricing pressures and reimbursement constraints across European healthcare systems.

Shortage of Skilled Pharmacovigilance Professionals

The region faces a critical and growing shortage of qualified personnel capable of managing complex pharmacovigilance operations, which directly impedes the scalability and responsiveness and thereby severely affects the expansion of the Europe pharmacovigilance market. According to sources, the pharmacovigilance sector faces a persistent challenge in finding candidates with the optimal blend of clinical knowledge, regulatory acumen, and data analysis skills, potentially leading to recruitment difficulties in certain areas. As per research, pharmacovigilance is a specialized field, and the number of professionals holding formal, comprehensive certification specific to EU regulations is relatively limited compared to the broader pharmaceutical workforce. Academic institutions across Europe offer limited specialized training programs in drug safety. This educational gap coincides with rising demand. The talent deficit is particularly acute in Eastern and Southern European countries, where brain drain and limited local training infrastructure exacerbate workforce gaps. Consequently, companies face extended recruitment cycles, delayed signal detection processes, and increased reliance on external vendors, often at premium costs. A continued human capital shortfall, absent coordinated investment in education and professional development, will keep affecting the efficiency of pharmacovigilance and regulatory compliance across the continent.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence in Adverse Event Detection

The adoption of artificial intelligence and machine learning gives a major opportunity for the growth of the Europe pharmacovigilance market. The new growth area is driven by enhancing the speed, accuracy, and scalability of adverse event detection and analysis. Real-world data from diverse sources such as hospital databases, patient registries, and wearable devices can now be processed in near real time to detect emerging risks earlier than spontaneous reporting alone allows. Furthermore, AI-driven predictive analytics enable proactive risk stratification of patient populations based on genetic, comorbidity, and concomitant medication profiles. These capabilities align with the EU’s vision for a learning health system where safety monitoring evolves continuously with clinical practice. The development of mature algorithmic transparency and validation frameworks is the key that unlocks AI's potential to reshape pharmacovigilance, which allows it to become a predictive rather than merely reactive discipline.

Expansion of Patient Reported Outcomes in Safety Surveillance

The formal integration of patient-reported outcomes into pharmacovigilance systems can enrich safety data and improve risk detection in the region, which provides fresh prospects for the expansion of the Europe pharmacovigilance market. According to the European Medicines Agency, direct patient reporting of individual case safety reports submitted to EudraVigilance constitutes a growing but minority share of total reports, increasing from a very low base when first introduced to around 10-15% in recent years (e.g., 2023-2024). As per guidance issued by the Heads of Medicines Agencies (HMA) and the EMA, patient reporting enhances the granularity of adverse event descriptions, captures underreported reactions (such as quality-of-life impacts), and reflects real-world medication use beyond clinical trial conditions. The European Commission has actively promoted this shift through its Patient Registries Initiative, which standardized data collection formats to facilitate cross-national safety analyses. Digital platforms such as national pharmacovigilance portals and mobile applications have simplified reporting, with countries achieving notable patient contribution rates. These firsthand accounts often reveal quality-of-life impacts and behavioral responses to adverse events that clinicians may overlook. Moreover, patient narratives provide contextual insights into medication adherence, misuse, and symptom progression. Regulatory acceptance of these data as valid safety evidence has elevated patient voices from anecdotal inputs to integral components of benefit-risk assessments. This democratization of safety surveillance not only strengthens signal detection but also fosters public trust and therapeutic collaboration across the healthcare continuum.

MARKET CHALLENGES

Data Fragmentation Across National Pharmacovigilance Systems

Significant data fragmentation persists across national pharmacovigilance systems, which affects the coherence and efficiency of safety signal detection and impedes the growth of the Europe pharmacovigilance market. For instance, adverse event reports from Germany may use ICD-10 coding while those from France rely on SNOMED CT, resulting in semantic mismatches during aggregate analysis. Furthermore, national competent authorities maintain independent duplicate databases for local surveillance, often duplicating efforts and increasing the risk of inconsistent risk assessments. These inefficiencies compromise the primary objective of pharmacovigilance, timely risk mitigation, particularly for products with low exposure where signals emerge slowly across multiple jurisdictions. The current systemic barriers posed by the fragmented data landscape will continue to hinder agile and unified drug safety governance until full semantic and procedural standardization is achieved via initiatives such as the EU Health Data Space.

Evolving Complexity of Biologics and Advanced Therapy Medicinal Products

The rapid proliferation of biologics, cell and gene therapies, and other advanced therapy medicinal products introduces unprecedented complexity into pharmacovigilance operations in the region, which further slows down the expansion of the Europe pharmacovigilance market. As per sources, these products often exhibit delayed or immune-mediated adverse reactions that may not manifest until months or years post administration, which complicates traditional signal detection windows. For example, chimeric antigen receptor T cell therapies carry risks of cytokine release syndrome and neurotoxicity, requiring specialized monitoring protocols beyond standard adverse event reporting. Moreover, the personalized nature of many advanced therapies limits the statistical power of post-marketing surveillance due to small patient populations per indication. Besides, the lack of standardized biomarkers for early toxicity prediction necessitates bespoke risk management plans for each product. These factors collectively heighten the burden on pharmacovigilance systems, demanding adaptive methodologies, real-world evidence integration, and cross-sectoral collaboration to ensure that innovation does not outpace safety assurance.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Clinical Trial Phase, Service Provider, Method, and Country. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Boehringer Ingelheim, Accenture, Bristol-Myers Squibb, IQVIA Holdings Inc, Covance, ICON, Parexel International Corporation, Quintiles, United BioSource, Synowlwedge, and Cognizant Technology Solutions Corporation. |

SEGMENTAL ANALYSIS

By Clinical Trial Phase Insights

The phase IV segment held the largest share of 43.6% of the Europe pharmacovigilance market in 2024. The dominance of the phase IV segment is mainly driven by the EU’s rigorous post-marketing surveillance mandates and the extended safety monitoring required after product launch. According to the European Medicines Agency, all centrally authorized medicinal products must undergo continuous benefit-risk evaluation throughout their lifecycle, with the entire pharmacovigilance system (including routine activities like collecting adverse reactions and periodically assessing reports) forming the backbone of this obligation. These requirements generate a sustained volume of case processing, signal detection and periodic safety update reporting that significantly exceeds the pharmacovigilance workload of earlier trial phases. Furthermore, the EU Directive on pharmacovigilance obliges marketing authorization holders to monitor real-world data from spontaneous reports, electronic health records, and literature sources indefinitely. This institutionalized emphasis on post-authorization safety ensures Phase IV remains the cornerstone of Europe’s pharmacovigilance architecture.

The phase I segment is expected to exhibit a noteworthy CAGR of 9.2% from 2026 to 2034 due to the surge in first-in-human trials for advanced therapy medicinal products and complex biologics. The European Medicines Agency has observed a significant increase in the number of Phase I clinical trial applications involving cell and gene therapies in recent years. In addition, the majority of these trials are predominantly conducted in specialized academic medical centers located in Germany, the United Kingdom, and the Netherlands, which are known for their exceptionally stringent safety monitoring protocols. Furthermore, early phase trials increasingly incorporate adaptive designs and biomarker-driven safety stopping rules, necessitating real-time pharmacovigilance support. This convergence of scientific complexity, regulatory scrutiny, and funding support positions Phase I as the most dynamic growth frontier in European pharmacovigilance.

By Service Provider Insights

In 2024, the contract outsourcing segment led the Europe pharmacovigilance market and accounted for a 62.5% share. Factors such as cost efficiency, regulatory agility, and access to specialized expertise that in-house teams often lack are propelling the growth of the contract outsourcing segment. This also reflects a structural shift toward externalization among pharmaceutical companies. The complexity of global safety data aggregation, language translation, and EudraVigilance gateway compliance has made outsourcing not just economical but operationally necessary. Moreover, the European Commission’s emphasis on audit readiness and quality management systems has elevated the bar for pharmacovigilance infrastructure, prompting firms to partner with vendors certified under ISO ninety zero zero one and other international standards. Leading contract providers offer scalable cloud-based safety databases, multilingual medical review teams, and AI-enabled signal detection tools that would be prohibitively expensive to replicate internally. This strategic reliance on external partners continues to solidify contract outsourcing as the backbone of Europe’s pharmacovigilance delivery model.

The in-house segment is estimated to register the fastest CAGR of 7.8% from 2026 to 2034 due to large pharmaceutical companies seeking greater control over safety data strategy and intellectual property, especially for high-value biologics and advanced therapies. The EU’s Data Governance Act also incentivizes data sovereignty, prompting firms to bring core safety functions back in-house to comply with cross-border health data transfer restrictions. Investment in digital infrastructure, such as enterprise safety data lakes and automated case processing engines, has further enabled large firms to internalize complex workflows previously outsourced. This strategic recalibration positions in-house pharmacovigilance as a high-growth niche within the broader outsourcing-dominated landscape.

By Method Insights

The spontaneous reporting segment dominated the Europe pharmacovigilance market and accounted for a 58.4% share in 2024. The growth of the spontaneous reporting segment is driven by the legal obligation for healthcare professionals and marketing authorization holders to report serious adverse events to national competent authorities. According to the European Medicines Agency, over 1.7 million individual case safety reports were submitted to EudraVigilance in 2024, with the majority being spontaneous notifications. The European Commission’s pharmacovigilance legislation explicitly designates spontaneous reporting as the primary signal detection mechanism, especially for rare and long-term adverse effects that controlled trials cannot capture. Furthermore, the inclusion of direct patient reporting since 2012 has expanded data sources and improved case completeness. Regulatory reliance on this method for periodic safety update reports and risk minimization measure evaluations ensures its continued centrality in Europe’s safety surveillance framework.

The EHR mining segment is anticipated to witness the fastest CAGR of 12.3% from 2026 to 2034, owing to the EU’s push toward real-world evidence utilization and the maturation of interoperable electronic health record systems across member states. According to sources, Pilot projects within the EU linking electronic health record (EHR) data have demonstrated a capacity to significantly accelerate the detection of safety signals for cardiovascular drugs compared to traditional methods. Furthermore, the EU Health Data Space initiative is facilitating cross-border pharmacovigilance analytics by successfully harmonizing data standards across a majority of member nations. Also, dedicated funding has been allocated to advance the development of natural language processing tools for extracting adverse event information from unstructured clinical documentation. Unlike traditional methods, EHR mining captures medication use in diverse populations, including elderly patients and those with comorbidities who are often excluded from clinical trials. This shift from passive to active surveillance positions EHR mining as the most transformative method in modern pharmacovigilance.

COUNTRY LEVEL ANALYSIS

Germany Pharmacovigilance Market Analysis

Germany led the Europe pharmacovigilance market and captured an 18.5% share in 2024. The dominance of Germany is primarily driven by its status as the continent’s leading pharmaceutical and biotechnology hub. The country hosts a significant number of clinical trial sites and serves as the European headquarters for major firms, including Bayer and Merck KGaA, which maintain extensive internal pharmacovigilance operations. The number of adverse drug reaction (ADR) reports submitted to the German Federal Institute for Drugs and Medical Devices (BfArM) has been rising steadily since 1978, with over 500,000 reports received between 2000 and early 2019 in the European database EudraVigilance, and hundreds of thousands of total reports analyzed in specific multi-year periods. The country’s robust regulatory enforcement, good manufacturing practice compliance, and high density of qualified pharmacovigilance professionals further support its dominance. These structural advantages position Germany as the operational and strategic nucleus of European pharmacovigilance.

United Kingdom Pharmacovigilance Market Analysis

The United Kingdom followed closely in the Europe pharmacovigilance market and accounted for a 16.2% share in 2024, and remains a pivotal player despite its departure from the European Union. The Medicines and Healthcare products Regulatory Agency continues to align closely with European Medicines Agency standards, ensuring seamless safety data exchange and mutual recognition of risk assessments. According to research, a significant majority of UK-based pharmaceutical companies achieve full compliance with EU pharmacovigilance legislation by collaborating with EU-based qualified persons. The UK has a substantial number of contract pharmacovigilance service providers. The country leads in early-phase oncology and gene therapy trials. Leading UK institutions, such as The Royal Marsden Hospital and Oxford University, are major contributors to early-stage advanced therapy clinical trials in Europe. This sustained commitment to scientific and regulatory excellence ensures the UK’s enduring influence in European pharmacovigilance.

France Pharmacovigilance Market Analysis

France is growing consistently in the Europe pharmacovigilance market because of its centralized national pharmacovigilance network and strong academic integration. Safety centers in France generate a substantial number of structured safety reports each year, which significantly contribute to the European Union's pharmacovigilance database (EudraVigilance). France is a leading contributor to patient reporting within the European Union, with a majority of spontaneous submissions coming directly from consumers. The country is also a leader in real-world evidence, with the Système National des Données de Santé covering over a million residents and enabling large-scale cohort event monitoring. These systemic strengths make France a model for integrated national pharmacovigilance within the European framework.

Italy Pharmacovigilance Market Analysis

Italy expanded moderately in the European pharmacovigilance market due to its high volume of generic drug usage and robust spontaneous reporting culture. The country’s decentralized healthcare system, with twenty-one regional authorities, has fostered localized pharmacovigilance initiatives, particularly in Lombardy and Tuscany, where digital reporting tools have been widely adopted. The Italian Medicines Agency collaborates closely with the European Medicines Agency on signal validation and risk communication, especially for cardiovascular and anti-infective agents, which dominate the national formulary. These factors collectively position Italy as a key contributor to Europe’s safety surveillance ecosystem.

Switzerland Pharmacovigilance Market Analysis

Switzerland is likely to grow in the Europe pharmacovigilance market from 2026 to 2034 due to its concentration of global pharmaceutical headquarters and regulatory alignment with the European Union. Swissmedic can directly exchange safety data with the European Medicines Agency because Switzerland has bilateral agreements that integrate it into the European Economic Area pharmacovigilance system, despite being outside the EU. The country’s multilingual workforce and ISO certified pharmacovigilance service providers also attract outsourcing contracts from across Europe. These attributes make Switzerland a critical non-EU node in the European pharmacovigilance network and a model of regulatory cooperation.

COMPETITIVE LANDSCAPE

Competition in the Europe pharmacovigilance market is intense and multidimensional, driven by regulatory complexity, technological innovation, and talent availability. Large global contract research organizations dominate through scale, integrated technology platforms, and deep regulatory relationships, yet face growing competition from specialized mid-tier providers offering agile niche services in areas like advanced therapy monitoring and real-world evidence analytics. The market is characterized by continuous consolidation with frequent acquisitions aimed at expanding geographic coverage, service depth, and data science capabilities. Differentiation increasingly hinges on the ability to combine human expertise with artificial intelligence to manage growing case volumes while meeting stringent European Medicines Agency timelines. Simultaneously, client expectations are shifting toward strategic safety partnerships rather than transactional outsourcing, placing a premium on consultative capabilities and therapeutic specialization. This dynamic environment compels all participants to prioritize compliance, agility, digital transformation, and workforce development to sustain long-term competitiveness.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe pharmacovigilance market include

- Boehringer Ingelheim

- Accenture

- Bristol-Myers Squibb

- IQVIA Holdings Inc

- Covance

- ICON

- Parexel International Corporation

- Quintiles

- United BioSource

- Synowlwedge

- Cognizant Technology Solutions Corporation

TOP PLAYERS IN THE EUROPE PHARMACOVIGILANCE MARKET

- ICON plc maintains a leading role in the Europe pharmacovigilance market through its integrated drug safety services spanning case management, signal detection, and risk minimization. The company operates dedicated pharmacovigilance centers in Ireland, the United Kingdom, and Hungary, staffed by multilingual medical reviewers and regulatory experts. In recent years, ICON has invested heavily in artificial intelligence-driven safety platforms to automate adverse event processing and enhance real-world evidence integration. The firm also expanded its partnership with the European Medicines Agency to support regulatory submissions for advanced therapy medicinal products. These initiatives underscore ICON’s commitment to advancing pharmacovigilance efficiency and compliance across Europe while reinforcing its global footprint through standardized safety operations in over forty countries.

- IQVIA Holdings Inc. leverages its extensive global data assets and advanced analytics capabilities to deliver comprehensive pharmacovigilance solutions across Europe. The company offers end-to-end safety services, including aggregate reporting, literature surveillance, and EudraVigilance gateway compliance, supported by its proprietary ARISg safety database. Recently, IQVIA enhanced its real-world safety monitoring by integrating electronic health records from seventeen European countries into its safety analytics engine. The firm also launched a dedicated pharmacovigilance training academy in Germany to address workforce shortages and ensure adherence to EU Good Pharmacovigilance Practices. These strategic moves strengthen IQVIA’s position as a technology-enabled safety partner for both large pharmaceutical firms and emerging biotechs navigating complex European regulatory requirements.

- Parexel International Corporation plays a pivotal role in the Europe pharmacovigilance landscape by providing tailored safety solutions for complex therapeutic areas, including oncology and rare diseases. The company operates a centralized European safety operations hub in Berlin equipped with AI-powered case processing and multilingual medical review capabilities. In response to evolving regulatory demands, Parexel recently upgraded its safety data warehouse to support direct integration with national competent authority portals across the European Economic Area. The firm also expanded its patient safety services by incorporating direct patient reporting workflows and social media monitoring into its standard pharmacovigilance offerings. These innovations reflect Parexel’s focus on proactive risk detection and patient-centric safety strategies that align with the European Medicines Agency’s vision for modernized pharmacovigilance.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe pharmacovigilance market primarily adopt four strategic approaches to reinforce their competitive stance. First, they invest in artificial intelligence and machine learning platforms to automate case intake signal detection and literature screening, thereby improving accuracy and reducing manual workload. Second, they establish regional pharmacovigilance centers staffed with locally certified qualified persons to ensure compliance with country-specific regulatory mandates. Third, they integrate real-world data sources such as electronic health records and patient registries to enhance post-marketing surveillance capabilities. Fourth, they form strategic alliances with academic institutions and national health authorities to co-develop safety monitoring frameworks and participate in regulatory pilot programs. These strategies collectively enable firms to deliver scalable, compliant, and future-ready pharmacovigilance services across diverse European markets.

MARKET SEGMENTATION

This Europe pharmacovigilance market research report is segmented and sub-segmented into the following categories.

By Clinical Trial Phase

- Pre-clinical

- Phase I

- Phase II

- Phase III

- Phase IV

By Service Provider

- In-house

- Contract Outsourcing

By Method

- Spontaneous Reporting

- Intensified ADR Reporting

- Targeted Spontaneous Reporting

- Cohort Event Monitoring

- EHR Mining

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is the europe pharmacovigilance market?

The europe pharmacovigilance market involves drug safety monitoring systems, ADR reporting, risk management, and regulatory compliance across pharmaceuticals and healthcare sectors

2. What drives growth in the europe pharmacovigilance market?

Growth is driven by increasing clinical trials, stricter drug safety regulations, rising chronic diseases, outsourcing trends, and AI adoption for safety data analysis

3. Which countries dominate the europe pharmacovigilance market?

Germany, UK, France, Italy, and Spain lead due to advanced healthcare, regulatory frameworks, and high clinical trial activities in the europe pharmacovigilance market

4. How does the EudraVigilance system impact the europe pharmacovigilance market?

EudraVigilance centralizes ADR reporting, improving drug safety monitoring and regulatory compliance in the europe pharmacovigilance market

5. What are common pharmacovigilance services in the europe pharmacovigilance market?

Services include adverse event reporting, signal detection, risk management planning, case processing, and regulatory submission support

6. How is AI transforming the europe pharmacovigilance market?

AI enables automated signal detection, case processing, and predictive analytics, enhancing efficiency and accuracy in the europe pharmacovigilance market

7. What challenges exist in the europe pharmacovigilance market?

Challenges include shortage of skilled professionals, high operational costs, complex regulations, and technology adoption barriers

8. How important is outsourcing in the europe pharmacovigilance market?

Outsourcing enables pharmaceutical companies to enhance scalability and cost-efficiency in compliance and safety monitoring

9. Which regulatory bodies influence the europe pharmacovigilance market?

The European Medicines Agency (EMA) and national regulators enforce strict pharmacovigilance rules impacting the europe pharmacovigilance market

10. How does pharmacovigilance support clinical trials in europe?

It ensures safety monitoring, adverse event documentation, and regulatory reporting throughout clinical trial phases in the europe pharmacovigilance market

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com