Europe Plastic Additives Market Size, Share, Trends & Growth Forecast Report By Primary Type, Detailed Type, Plastic Type, Application, and By Country (Germany, France, Italy, United Kingdom, Netherlands & Rest of Europe) – Industry Analysis and Forecast, 2025 to 2033

Europe Plastic Additives Market Summary

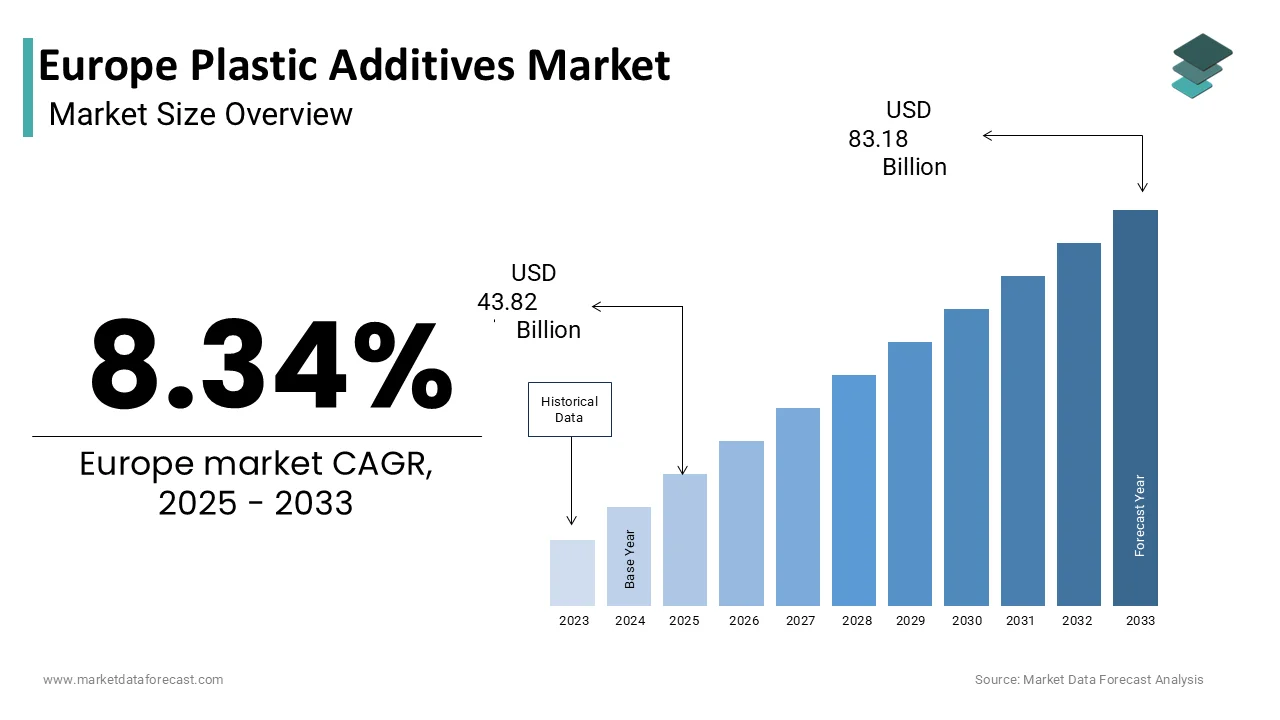

Europe plastic additives market was valued at USD 40.45 billion in 2024, is estimated at USD 43.82 billion in 2025, and is projected to reach USD 83.18 billion by 2033, growing at a CAGR of 8.34% from 2025 to 2033, driven by stringent EU regulations, circular economy mandates, recycled plastics growth, and rising demand from electric mobility and sustainable packaging.

Key Market Insights

- 2024 value: USD 40.45 billion

- 2025 (est): USD 43.82 billion

- 2033 (forecast): USD 83.18 billion

- CAGR (2025–2033): 8.34%

Quick Growth Drivers

- Strict fire safety and chemical compliance regulations across construction, transport, and electronics.

- Rapid growth of recycled plastics, increasing demand for stabilizers, compatibilizers, and odor-control additives.

- Expansion of electric vehicles requires flame retardants and thermal stabilizers for battery and connector systems.

- Rising demand for high-performance and specialty plastics in automotive, healthcare, and electronics.

- EU push toward lightweighting and decarbonization in industrial materials.

Principal Restraints

- REACH restrictions on hazardous additives (phthalates, brominated flame retardants).

- High reformulation and compliance costs, especially for SMEs.

- Reduced performance or higher costs of substitute additives.

- Regulatory uncertainty dis elaying approval of new chemical formulations.

High-Value Opportunities

- Development of bio-based, non-toxic additives aligned with the European Green Deal.

- Additives designed for recycling compatibility and circular plastics.

- Tailored additive systems for EV lightweighting and battery safety.

- Growth in food-contact and medical-grade additives with low migration profiles.

Key Market Challenges

- Lack of standardized EU testing frameworks for additive behavior in recycled plastics.

- Supply chain volatility for key raw materials (phosphorus, antimony, rare earths).

- Rising carbon disclosure and lifecycle assessment requirements.

- Managing legacy additives contaminating recycling streams.

Fastest-Growing Segments

- Flame retardants: fastest growth driven by EVs, construction, and public safety norms.

- Antimicrobial additives: rising use in healthcare, packaging, and public transport.

- High-performance plastics: strong uptake in EVs, aerospace, and semiconductor equipment.

Regional Leadership & Dynamics

- Germany (lead, 25.5%) — strong chemical industry, automotive base, and circular economy leadership.

- France (18.4%) — aggressive packaging regulations and recycling infrastructure.

- Italy — large flexible PVC and construction demand.

- United Kingdom — premium demand from automotive and medical applications.

- Netherlands — chemical distribution hub and leader in sustainable logistics packaging.

What Wins Commercially

REACH-compliant, halogen-free, and bio-based additive portfolios.

- Additives enabling recycled-content performance restoration.

- Strong regulatory foresight and lifecycle data transparency.

- Co-development with automotive OEMs, recyclers, and packaging brands.

Top Strategic Ask for Executives

- Accelerate green and circular additive innovation.

- Secure raw material supply chains and alternative feedstocks.

- Invest in recycling-compatible additive certification and testing.

- Expand partnerships across EV, packaging, and recycling ecosystems.

Leading Players

Some of the companies that are playing a dominating role in the European plastic additives market include:

- BASF SE

- Clariant AG

- Solvay SA

- Evonik Industries

- LANXESS

- Songwon Industrial

- Adeka Corporation

- Arkema Group

- Baerlocher GmbH

- Emery Oleochemicals

Europe Plastic Additives Market Size

The Europe plastic additives market was valued at USD 40.45 billion in 2024, is estimated at USD 43.82 billion in 2025, and is projected to reach USD 83.18 billion by 2033, growing at a CAGR of 8.34% from 2025 to 2033.

Plastic additives are specialized chemical compounds, such as stabilizers, plasticizers, flame retardants, fillers,s and colorants, that are incorporated into polymers to enhance performance,ce durability, processability, and safety across packaging, automotive, construction, and medical applications. In a region defined by stringent chemical regulation,s, circular economy mandates, and decarbonization goals, additives have evolved from functional enhancers to critical enablers of material compliance and sustainability. According to sources, a vast majority of plastic products sold within the European Union incorporate additives to fulfill specific technical or safety standards. As per research, thousands of distinct chemical substances serve as plastic additives, many of which are undergoing regulatory scrutiny due to concerns regarding their environmental persistence or biological toxicity. Furthermore, the transition toward plastic packaging that is either reusable or recyclable is dependent on the innovation of non-hazardous additive alternatives. These regulatory and functional imperatives position plastic additives as pivotal yet highly scrutinized components in Europe’s transition toward safer and more circular material systems.

MARKET DRIVERS

Stringent Fire Safety Regulations in Construction and Transportation

European Union fire safety directives mandate the use of flame-retardant additives in plastic components used in public transport and electrical equipment to prevent ignition and slow flame spread, which is among the key accelerators of the European plastic additives market. Specifications for insulation materials used in buildings frequently reference the need to meet a specific level of fire safety performance, which influences the types of fire-retardant additives selected. The requirements for plastic materials within vehicle interiors are subject to specific flammability limits, contributing to demand for certain phosphorus-based and intumescent additives. A significant majority of a common type of rigid foam utilized for building insulation incorporates non-halogenated flame retardants, in alignment with various regional restrictions on brominated compounds. Interior materials for rail transport are often required to pass a specific series of fire safety tests, which have been associated with the increased adoption of aluminum diethyl phosphinate and melamine polyphosphate systems. This regulatory enforcement creates structural and discretionary demand for advanced flame-retardant additives across high-volume industrial sectors.

Growth of Recycled Plastics and Need for Performance Restoration Additives

The surge in mechanically recycled plastic content, driven by the European Union Packaging and Packaging Waste Regulation and Extended Producer Responsibility schemes, is further fueling the expansion of the European microencapsulation market. This has intensified demand for additives that restore mechanical and thermal properties degraded during recycling. According to sources, post-consumer plastic recycling volumes in the European Union are largely driven by the processing of packaging materials. However, recycled polyolefins often suffer from reduced melt strength yellowin,g and odor due to polymer chain scission and contamination. The integration of specific chemical additives, such as stabilizers and compatibilizers, enhances the mechanical properties of recycled polypropylene to meet the requirements of demanding technical applications. Companies like BASF and Clariant now offer additive masterbatches specifically formulated for recycled streams, such as Irgastab and Licocene, that neutralize catalyst residues and prevent odor formation. Legislative mandates for minimum recycled content in packaging are shifting industry focus toward performance restoration technologies. Chemical additives serve as critical components in achieving the material quality necessary for a functional circular economy.

MARKET RESTRAINTS

REACH Regulation Restrictions on Hazardous Substances

The European Union’s Registration, Evaluation, Authorisation and Restriction of Chemicals framework continuously restricts or bans additive substances deemed hazardous to human health or the environment, severely limiting formulation options for manufacturers, which restricts the growth of the European plastic additives market. According to research, A significant number of plastic additives have been identified as substances of great concern within the regulatory framework for chemical use in the region. Some of these substances have progressed to a stage requiring specific authorization for their continued use in various applications. Phthalate plasticizers like DEHP and flame retardants such as decabromodiphenyl ether have been phased out,t forcing formulators to adopt alternatives that are often less effective, more expensive,e or not yet fully validated. In the medical sector, changes in the formulation of plastic components, such as a shift to alternative plasticizers in medical tubing, have resulted in both increased expenses associated with production processes and a noticeable change in material properties, specifically reduced flexibility. Moreover, the authorization process can take severalyears creating regulatory uncertainty that deters investment in new formulations. This compliance burden disproportionately affects small and medium compounders lacking regulatory expertise and accelerates market consolidation among large additive producers with global compliance teams.

Incompatibility of Additives with Recycling Streams

Many conventional additives, particularly halogenated flame retardants, colorants with heavy metals, and certain stabilizers, contaminate plastic recycling loops and compromise the quality of secondary raw materials. These issues also hinder the expansion of the European microencapsulation market. A notable portion of post-consumer plastic waste is downcycled or directed to landfills, a situation influenced more by the presence of certain additives than by the type of polymer itself. Brominated flame retardants in electronic waste plastics, for instance, can render entire batches unsuitable for food contact high-value applications even at parts per million levels. Specific legacy stabilizing materials, which are now subject to restrictions, continue to be present in recycled material streams, complicating contemporary recycling processes. Certain coloring agents, including those based on particular white or black pigments, hinder common automated sorting technologies, which in turn affects material recovery volumes. Contaminated streams remain hard to pre-sort because Europe hasn't fully implemented DPPs, a crucial step in its Ecodesign for Sustainable Products Regulation. This systemic incompatibility undermines circular economy goals and discourages brand owners from using complex additive formulations even when technically necessary.

MARKET OPPORTUNITIES

Development of Bio-Based and Non-Toxic Additives Under the Green Deal

The European Green Deal is accelerating innovation in sustainable additives derived from renewable feedstocks and free from substances of concern, and creates major opportunities for green chemistry leaders, which is expected to drive the growth of the European plastic additives market. A range of bio-based alternatives for conventional plasticizers is now available across the continent, designed to offer similar performance characteristics without associated endocrine risks. Companies have launched bbio-sourcedhindered amine light stabilizers for agricultural films that meet organic farming standards. Additionally, regulatory frameworks are increasingly emphasizing the inherent safety and sustainability of all chemicals introduced into the market within the European Union by a specific target date. There is a clear trend toward approving certain high molecular weight additives for applications involving food contact, based on their stability and reduced potential for migration into food items. This regulatory and consumer push toward benign chemistry opens new markets in food packaging, medical devices,s and children’s toys where safety is paramount.

Integration of Additives in Lightweighting for Electric Mobility

The automotive sector’s shift toward electric vehicles is driving demand for high-performance additives that enable lightweight yet durable plastic components to offset heavy battery packs, thereby generating fresh prospects for the European microencapsulation market. Electric vehicles incorporate a higher volume of engineered plastics compared to internal combustion engine models to support specialized components such as battery housings and connectors. These applications demand heat stabilizers, UV absorbers, and impact modifiers that withstand high temperatures and mechanical stress. Advanced polymer composites reinforced with glass fiber and thermal stabilizers serve as functional alternatives to metal for structural brackets. The use of lightweight plastic materials in vehicle architecture contributes to an overall reduction in component weight while preserving necessary crash resistance. Furthermore, Regulatory requirements for circularity necessitate that battery components are designed for efficient disassembly and subsequent recycling. Material selection for battery systems increasingly favors non-halogenated flame retardants to ensure that safety additives do not interfere with material recovery processes. Companies are developing additive packages tailored to electric vehicle plastics that combine flame retardancy, thermal stability, t,y and recyclability. This convergence of mobility transformation and material science positions additives as enablers of Europe’s clean transport future.

MARKET CHALLENGES

Lack of Standardized Testing and Certification for Recycled Content Compatibility

There is no harmonized European standard to evaluate how additives behave in recycled plastic matrices or how they affect recyclate quality, despite the push for circularity, which holds back the growth of tEuropeanope plastic additives market. Currently, there is an absence of standardized test methods for evaluating how additives interact or break down within multi-cycle recycling systems. This gap leads to inconsistent performance and liability risks for compounders and brand owners. A significant number of recyclers observe production issues, such as off-odors, changes in color, or material brittleness, which they attribute to the interactions of various additives, including some that are no longer in common use. Formulators encounter difficulties in confirming an additive's compatibility with existing recycling processes in the absence of established evaluation methods. The European Chemicals Agency has called for mandatory additive declarations, but implementation remains voluntary. This metrological and regulatory void stifles innovation in circular additives and perpetuates a trial-and-error approach that increases costs and delays product development across the value chain.

Supply Chain Volatility and Geopolitical Dependence on Key Raw Materials

High exposure to global supply disruptions for critical raw materials such as phosphorus, antimony oxide,e and rare earth elements used in flame retardants and stabilizers continues to impede the expansion of the European plastic additives market. According to sources, a notable share of antimony, a key component in halogen-free flame retardants, is imported from China, creating strategic vulnerability. The two thousand twenty two energy crisis further destabilized production. Average additive prices showed an upward trend over the specified period, influenced by synthesis routes reliant on natural gas inputs. Additionally, the European Union’s Carbon Border Adjustment Mechanism now imposes indirect costs on imported precursors,s distorting input economics. Many smaller manufacturers adjusted their production levels or reduced their output as a consequence of increasing and unaffordable feedstock expenses. This fragility undermines long term planning and discourages investment in capacity expansion j, just as demand from circular and electric mobility sectors peaks, making raw material security a critical unresolved challenge.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Primary Type, Detailed Type, Plastic Type, Application, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | BASF SE, Clariant AG, LANXESS AG, Evonik Industries AG, Lubrizol Corporation, Eastman Chemical Company, Arkema S.A., Solvay S.A., Italmatch Chemicals S.p.A., Adeka Corporation, Songwon Industrial Co., Ltd., SI Group, Inc., Cabot Corporation, Croda International Plc, Nouryon (formerly part of AkzoNobel Specialty Chemicals), Albemarle Corporation, Huntsman Corporation, Cabot (performance additives), Omya AG, Greencore (or regional specialty additive suppliers) |

SEGMENTAL ANALYSIS

By Primary Type Insights

The plasticizers segment led the European plastic additives market in 2024. The supremacy of the plasticizers segment is credited to its indispensable role in imparting flexibility to rigid polymers, particularly polyvinyl chloride,e used extensively in construction cables and medical devices. Plasticizers are widely incorporated into many flexible PVC products to achieve desired levels of softness and enhance long-term durability. A significant amount of plasticized PVC material is utilized each year across various construction applications, including within flooring, wall coverings, and roofing membranes. Despite regulatory pressure on ortho phthalate, es the market has transitioned to non-phthalate alternatives such as diisononyl cyclohexane, one or two dicarboxylate, and epoxidized vegetable oils, which now account for a portion of new formulations. This combination of material necessity, regulatory adaptation, and vendor-use base ensures plasticizers remain the market’s cornerstone segment.

The flame retardants segment is on the rise and is expected to be the fastest-growing segment in the market by witnessing a CAGR of 6.8% from 2025 to 2033. The rapid acceleration of the flame retardants segment is fuelled by tightening fire safety regulations across construction, electric vehicles, and electronics. Regulatory changes within the European Union are requiring insulation foams to meet a specific fire safety classification, which in turn necessitates the use of advanced, non-halogenated systems for flame resistance. New regulations governing electric mobility in Europerequireg battery enclosures to maintain fire resistance for a minimum duration during thermal events, driving demand for specific additive types such as intumescent and phosphorus-based compounds. A significant majority of newly installed rigid polyurethane insulation in a key region now incorporates non-halogenated flame retardants. Revised safety standards for materials used in railway applications have increased the adoption of certain phosphorus-based compounds in interior components. This convergence of infrastructure safety and clean tech mandates positions flame retardants as the highest growth frontier in Europe’s additive landscape.

By Detailed Type Insights

The antioxidants segment dominated the European plastic additives market in 2024. The leading position of the antioxidants segment is driven by its universal necessity in preventing thermal and oxidative degradation during plastic processing and product lifetime across all polymer types. Polyolefin production frequently involves the use of certain types of antioxidants to help with stability during melting and to maintain strength. A significant quantity of these polymers is utilized within the packaging industry each year, where these additives play a role in ensuring food contact integrity during processing, including recycling efforts. The shift toward recycled content has intensified demand. Furthermore, the European Food Safety Authority strictly regulates antioxidant migration, ensuring only non-volatile, le non-migrating types are approved, favoring European specialty producers. This technical indispensability, regulatory specificity,y and circular economy relevance cement antioxidants as the foundational additive segment.

The antimicrobial additives segment is expected to exhibit a noteworthy CAGR of 9.2% from 2025 to 2033 due to heightened hygiene awareness post pandemic and regulatory mandates in healthca, re, food packaging,g and public infrastructure. Regulatory frameworks in Europe require evidence for claims made about antimicrobial properties, which has led to widespread adoption of specific antimicrobial substances. The substances most frequently utilized to meet these requirements include zinc pyrithione, silveionson, and quaternary ammonium compounds. In food packaging, the European Food Safety Authority now permits antimicrobials that inhibit surface mold on cheese and meat trays, reducing food waste. Data regarding surface materials used in healthcare settings indicates a substantial portion of newly installed materialsincorporatese approved antimicrobial additives. The incorporation of these additives is commonly understood as a measure intended to help address concerns regarding healthcare-associated infections. Additionally, public transport authorities in France and the Netherlands mandate antimicrobial handrails and seat fabrics in buses and trains. This policy-driven health focus transforms antimicrobials from niche to mainstream across high-contact applications.

By Plastic Type Insights

The commodity plastics segment dominated the European plastic additives market in 2024. The prominence of the commodity plastics segment is attributed to its overwhelming volume in packaging, ng building products,ct,s and disposable goods. Polyethylene, polypropylene, and polyvinyl chloride make up the majority of plastics produced in Europe, requiring various additives like stabilizers, plasticizers, and fillers to meet processing and performance needs. A current pattern is the increased use of these additives. This trend has been noted as a response to requirements for greater recycled content in products. The purpose of the additives in this context is to help restore properties to materials that have been mechanically recycled. This practice emphasizes the ongoing challenge of maintaining material quality while incorporating recycled streams. Additionally, commodity plastics domisingle-usee use medical and agricultural films, where UV stabilizers and slip agents are essential. The sheer scale of production ensures that even minor additive loadings translate into massive market volume, making commodity plastics the structural backbone of additive consumption.

The high-performance plastics segment is predicted to witness the highest CAGR of 11.4% from 2025 to 2033. The swift expansion of the high-performance plastics segment is fueled by demand for extreme durability in electric vehicle components, aerospace parts,s and semiconductor manufacturing equipment. Polymers like polyetheretherketone, polyphenylene sulfide, and polyimide require specialized additives, including high temperature antioxidants, graphite fillers,s and laser direct structuring agents, to function in environments exceeding two hundred fifty degrees Celsius. Additionally, the European Semiconductor Equipment Association mandates that all wafer carriers use static dissipative high-performance plastics with non-outgassing additives to prevent particle contamination. This convergence of clean tech, advanced manufacturing,g and material science drives premium additive adoption in low volume high value applications.

By Application Insights

The packaging segment was the largest in the European plastic additives market in 2025. The growth of the packaging segment is propelled by the sheer volume of plastic used in food, beverage,e and consumer product containers across the region. Plastic packaging placed on the European Union market often contains additives intended to enhance material properties like clarity, UV protection, or barrier function. The need to incorporate more recycled content into products has increased the demand for specific types of additives, such as chain extenders and odor scavengers, to help restore the performance of mechanically recycled plastics. Various substances, including antimicrobials and antioxidants, are approved for use in food contact materials, which helps ensure safety during storage. Additionally, the Packaging and Packaging Waste Regulation requires that all materials be designed for recyclability, thereby driving adoption of non-halogenated slip agents and compatibilizers. This regulatory scale and material necessity make packaging the highest volume application for plastic additives in Europe.

The automotive segment is estimated to register the fastest CAGR of 8.7% due to vehicle lightweighting, electric mobility, and interior air quality mandates. Electric vehicles require up to fifteen percent more engineered plastics than internal combustion models, particularly for battery housings, connectors, and charging components, demanding high-performance additives like flame retardants, thermal stabilizers, and impact modifiers. There is a clear material change occurring, where a specific reinforced polymer composite is being utilized as a substitute for aluminum in certain structural components. This substitution has a notable impact on the final product, specifically resulting in a significant reduction in weight for the component in question. The wider regulatory landscape influences material choices, with specific guidelines requiring that interior plastics do not contain certain chemical additives. In response to these guidelines and market demands, the use of bio-based additives and non-halogenated stabilizers is increasing within the industry. The shift to cabin air quality standards under ISO one two two one nine further drives the use of low-emission antioxidants and odor control additives. This technical and regulatory intensity positions automotive as the highest growth application segment.

COUNTRY LEVEL ANALYSIS

Germany Plastic Additives Market Analysis

Germany was the top performer in the European plastic additives market and accounted for a 25.5% share in 2024. The dominance of the German market is driven by its world-class chemical industry, automotive sector, and strict regulatory enforcement. Home to global leaders like BA, SF Evo,nik, and Lanxess, Germany sets the benchmark for additive innovation and compliance. The country’s Building Energy Act mandates low-emission additives in construction plastics, while the Automotive Recycling Ordinance restricts hazardous substances in interior components. Additionally, Germany leads in circular economy implementation with numerous certified recyclers requiring performance restoration additives for post-consumer streams. This integration of industrial-scale regulatory rigor and circular infrastructure cements Germany as the market’s innovation and compliance nucleus.

France Plastic Additives Market Analysis

France followed closely in the European plastic additives market and held a 18.4% share in 2024. The growth of the French market is fuelled by aggressive packaging regulations and public investment in recycling infrastructure. A regulation encourages the use of packaging that can be reused or recycled by a specified near-future date, while also requiring a certain amount of reclaimed materials be incorporated into products. This framework helps to foster the demand for processing aids and materials that address sensory attributes. The volume of material needing special treatment to comply with standards has reached a notable level in recent practice. This processing is necessary to meet requirements for sensitive applications, such as those involving consumables. France also pioneered the Extended Producer Responsibility scheme for packaging with fees scaled by recyclability, favoring formulations with non-problematic additives. Companies supply bio-based impact modifiers for recycled polypropylene used in household goods. This policy-driven circularity creates a high compliance high volume market for sustainable additives.

Italy Plastic Additives Market Analysis

Italy is moving ahead steadfastly in the European plastic additives market because of its extensive construction sector and leadership in flexible PVC manufacturing. A considerable amount of plasticized material is used each year in various applications like flooring, roofing, and cables; this requires substantial quantities of non-phthalate plasticizers and heat stabilizers. A government recovery and resilience plan is providing significant funding for building renovation projects, which includes mandates for using low-emission materials under established environmental criteria. Additionally, Italy’s strong furniture and appliance industries drive demand for impact modifiers and UV stabilizers in durable goods. A majority of new flooring products observed use specific alternative compounds as primary plasticizers, aligning with established requirements for acceptable indoor air quality. This concentration in construction and flexible polymers ensures consistent additive demand across industrial and consumer applications.

United Kingdom Plastic Additives Market Analysis

The United Kingdom is another key player in the European plastic additives market due to its advanced automotive and medical device sectors. Despite Brexit, the UK aligns closely with European chemical regulation,s ensuring continued additive compatibility. Moreover, the Medicines and Healthcare products Regulatory Agency enforces strict additive migration limits in medical tubing and packaging, favoringnon-phthalatee plasticizers like Hexamoll DINCH. Companies like Victrex supply high-performance polymer additives for surgical instruments and implants. The UK’s National Health Service procurement guidelines prioritize low-emission materials, further driving adoption. This focus on high-value regulated applications positions the UK as a premium additive market.

Netherlands Plastic Additives Market Analysis

The Netherlands is likely to expand in the European plastic additives market from 2025 to 2033, owing to its role as Europe’s chemical distribution hub and leader in sustainable logistics packaging. The Port of Rotterdam handles over forty percent of Europe’s chemical imports, including additive raw materials distributed across the continent. Large quantities of plastic packaging are manufactured for electronic commerce and temperature-sensitive logistics, necessitating the use of specialized stabilizers and protective agents to maintain product quality. Governmental mandates regarding packaging recyclability are driving a transition toward the use of specific chemical additives that support environmental standards. The requirement for fully recyclable materials is increasing the integration of non-halogenated agents and compatibilizers within the production process. Companies operate additive compounding plants in the Chemelot industrial cluster, serving European clients. This combination of logistics, scale, chemical infrastructure, and circular policy makes the Netherlands a strategic gateway for additive distribution and innovation.

COMPETITIVE LANDSCAPE

The European elastic additives market features intense competition among global chemical giants, European specialty formulators, and emerging green chemistry innovators, each navigating a complex Clariant leverage scaleleveragingle regulatory expertise,e and integrated R and D to dominate high compliance segments such as food contact and flame retardancy. Meanwhile, niche players focus obio-baseded or circular additives for recycled streams where differentiation lies in sustainability credentials rather than cost. The market is increasingly bifurcated between conventional additives under REACH scrutiny and next-generation solutions designed for circularity and safety by design. Competition is not solely on price but on regulatory foresight, material compatibility with the recycling loop,s and alignment with the European Union’s net zero and zero pollution ambitions. Success requires deep collaboration across the value chain from recyclers to brand owners to ensure additives enable both performance and circularity without compromising safety.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the europe plastic additives market include

- BASF SE

- Clariant AG

- LANXESS AG

- Evonik Industries AG

- Lubrizol Corporation

- Eastman Chemical Company

- Arkema S.A.

- Solvay S.A.

- Italmatch Chemicals S.p.A.

- Adeka Corporation

- Songwon Industrial Co., Ltd.

- SI Group, Inc.

- Cabot Corporation

- Croda International Plc

- Nouryon (formerly part of AkzoNobel Specialty Chemicals)

- Albemarle Corporation

- Huntsman Corporation

- Cabot (performance additives)

- Omya AG

- Greencore (or regional specialty additive suppliers)

TOP LEADING PLAYERS IN THE MARKET

- BASF SE is a global chemical leader with a dominant footprint in the European plastic additives market through its comprehensive portfolio of stabilizers, plasticizers, rs and impact modifiers under brands like Irganox and Ultramid. The company supplies high-performance additives to automotive packaging and construction sectors across Germany, France, and Italy, supporting compliance with REACH and circular economy mandates. The company also enhanced its additive masterbatches for electric vehicle battery components to meet European Battery Regulation flame retardancy requirements. These innovations reinforce BASF’s role as a sustainability and compliance partner while extending its influence in global specialty chemicals markets.

- Clariant AG is a Swiss specialty chemicals company renowned for its advanced additive solutions tailored to Europe’s stringent regulatory and circular economy landscape. Its AddWorks portfolio includes halogen-free flame retardants, bio-based plasticizers, and odor control additives for recycled plastics. The company also expanded its Licocene compatibilizers to improve adhesion inmulti-layerr recycled packaging films. By aligning with European Green Deal objectives and offering certified sustainable solutions, Clariant strengthens its position as a trusted enabler of circular plastic value chains globally.

- Solvay SA is a Belgium-based innovator providing high-performance additives for engineering and high-temperature plastics used in electric mobility, aerospace, and electronics. Its portfolio includes specialty stabilizers, RRS antimicrobials, and laser direct structuring additives that meet European semiconductor and automotive safety standards. The company also partnered with major European battery cell manufacturers to develop flame-retardant packages for polyamide battery housings. These strategic moves position Solvay at the intersection of advanced manufacturing and sustainable chemistry, enhancing its global reputation in high-value additive technologies.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the European plastic additives market prioritize regulatory compliance by developing non-hazardous halogen-free and bio-based additives that align with REACH, European Food Safety Authority,y and Biocidal Products Regulation requirements. They invest in circular economy solutions such as compatibilizers, rs odor scavengers, ers non-migratingting stabilizers to enhance the quality of mechanically recycled plastics. Companies strengthen partnerships with recyclers, brand owners, and automotive manufacturers to co-develop application-specific additive packages for electric vehicles and food packaging. Strategic expansion of sustainable feedstocks, including waste oils and castor derivatives,s supports European Green Deal objectives. Additionally, many vendors pursue certification under EU Ecolabel and food contact compliance frameworks to build trust and differentiate in a highly scrutinized market.

MARKET SEGMENTATION

This research report on the europe plastic additives market is segmented and sub-segmented into the following categories.

By Primary Type

- Plasticizers

- Flame Retardants

- Stabilizers

- Impact Modifiers

- Lubricants

- Others

By Detailed Type

- Antioxidants

- Antimicrobial Additives

- UV Stabilizers

- Heat Stabilizers

- Processing Aids

- Others

By Plastic Type

- Commodity Plastics

- Engineering Plastics

- High-Performance Plastics

By Application

- Packaging

- Automotive

- Construction

- Electrical & Electronics

- Consumer Goods

- Healthcare

- Others

By Country

- Germany

- France

- Italy

- United Kingdom

- Netherlands

- Rest of Europe

Frequently Asked Questions

1. What are the major types of plastic additives used in the Europe Plastic Additives Market?

The Europe Plastic Additives Market comprises several key types including plasticizers (accounting for over 46% revenue share), flame retardants, impact modifiers, antioxidants, UV stabilizers, antimicrobials, lubricants, and color additives, each serving specific functional requirements.

2. What are the primary applications driving the Europe Plastic Additives Market?

Packaging dominates the Europe Plastic Additives Market applications, followed by building and construction (over 18% revenue share in 2022), automotive, consumer goods, electrical and electronics, agriculture, and medical devices.

3. How do regulatory frameworks impact the Europe Plastic Additives Market?

The Europe Plastic Additives Market is significantly influenced by regulatory bodies such as the European Commission, which enforces acts like REACH and RoHS to regulate plasticizers, flame retardants, and other additives due to health and environmental concerns.

4. How is sustainability affecting the Europe Plastic Additives Market?

Sustainability initiatives are reshaping the Europe Plastic Additives Market through EU regulations requiring 100% recyclable or reusable plastic packaging by 2030, mandatory recycled content requirements from 2030 onwards, and increasing adoption of bio-based additives

5. What role does the automotive industry play in the Europe Plastic Additives Market?

The automotive industry is a major driver of the Europe Plastic Additives Market, with Germany's automotive industry accounting for over 28% of the European automotive market share and increasing lightweighting trends in electric vehicles boosting demand for impact modifiers and flame retardants

6. What are the key growth opportunities in the Europe Plastic Additives Market?

The Europe Plastic Additives Market presents growth opportunities through development of specialty additives for 3D printing, medical devices, food-contact safe additives for packaging applications, and bio-based alternatives to meet sustainability targets.

7. How is the construction sector influencing the Europe Plastic Additives Market?

The Europe Plastic Additives Market benefits from the growing construction industry driven by increasing urbanization, population growth, infrastructural development, and the rising trend of green construction projects and modular/prefabricated construction in developed economies.

8. What are the major challenges facing the Europe Plastic Additives Market?

The Europe Plastic Additives Market faces challenges including stricter plastic usage regulations, environmental concerns over plastic pollution, phase-out of certain hazardous flame retardants and plasticizers, and the need to develop additives compatible with recycling processes.

9. How do plasticizers function in the Europe Plastic Additives Market?

Plasticizers are the largest segment in the Europe Plastic Additives Market, accounting for over 46% revenue share, primarily used to improve flexibility and processability of plastics, particularly in PVC applications for packaging films, flooring, cables, and automotive interior components.

10. How are flame retardants regulated in the Europe Plastic Additives Market?

Flame retardants in the Europe Plastic Additives Market are subject to strict REACH and RoHS regulations that restrict hazardous substances, driving manufacturers to develop safer phosphorus-based and halogen-free alternatives for electronics, construction, and transportation applications.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com