Europe Private LTE Market Size, Share, Trends, & Growth Forecast Report By Component (FDD and TDD), End User (Manufacturing, Energy & Utilities, Healthcare, Transportation, Mining, and Others), Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2026 to 2034

Market Size, 2025

$1.90 BnMarket Estimate, 2026

$2.08 BnMarket Forecast, 2034

$4.21 BnCAGR, 2026–2034

9.24%Europe Private LTE Market Size

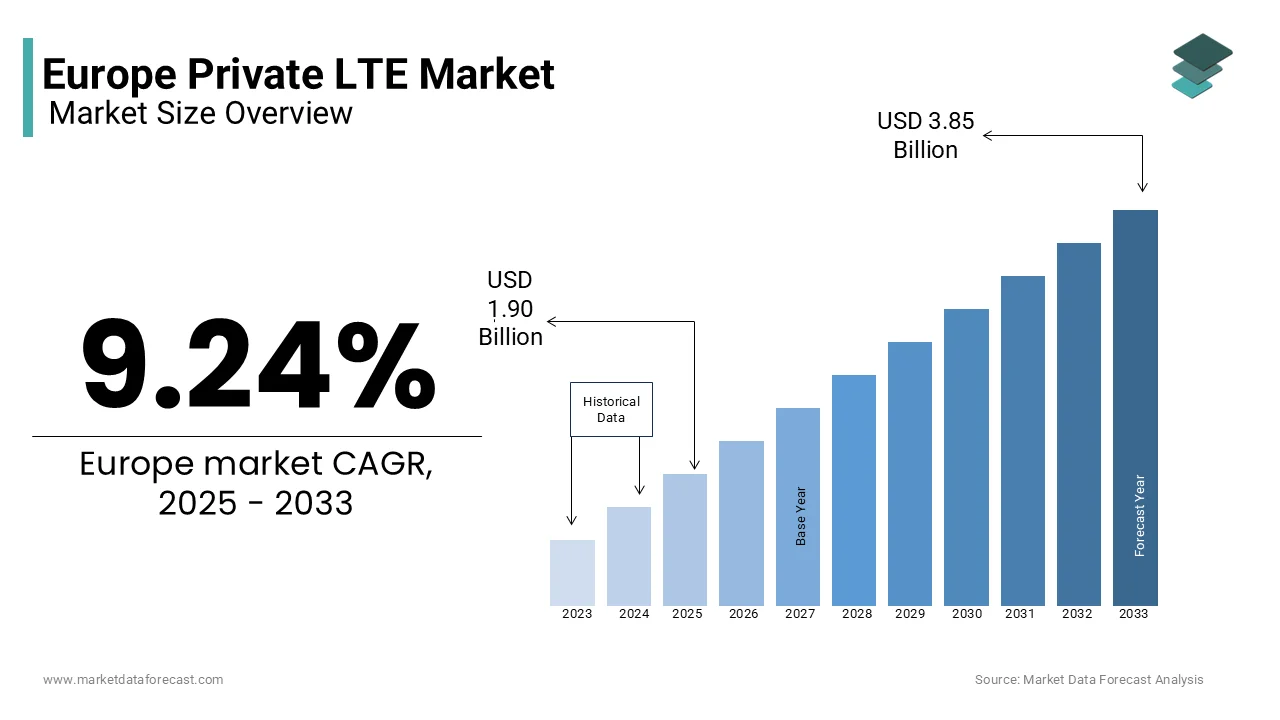

The Europe private LTE market was worth USD 1.90 billion in 2025. The European market is estimated to reach USD 4.21 billion by 2034 from USD 2.08 billion in 2026, growing at a CAGR of 9.24% from 2026 to 2034.

Private LTE networks are dedicated wireless communication systems that operate within licensed, shared, or unlicensed spectrum bands, offering enhanced security, reliability, and control compared to public networks. These networks are increasingly adopted across industries such as manufacturing, energy, healthcare, and transportation to support mission-critical applications. In Europe, the private LTE market is witnessing robust growth due to the region's strong industrial base and stringent regulatory frameworks promoting secure and efficient connectivity.

The demand for private LTE market has been consistently in the European region from the last few years due to the proliferation of Industry 4.0 initiatives and the deployment of smart factories. Furthermore, as per the European Commission, more than 60% of enterprises in the EU are exploring private LTE solutions to meet their operational needs. This underscores the critical role of private LTE in enabling advanced IoT applications, ultra-low latency communication, and seamless integration with 5G technologies.

MARKET DRIVERS

Industrial Automation and Digital Transformation

The rapid adoption of industrial automation and digital transformation across Europe is a key driver of the private LTE market. According to Eurostat, the adoption of industrial automation in Europe has surged, with over 70% of large enterprises implementing IoT-enabled solutions by 2022. Private LTE networks serve as the backbone for these transformations, providing reliable and secure connectivity for automated machinery, robotics, and real-time data analytics. The European Investment Bank estimates that investments in digital transformation across industries exceeded EUR 200 billion in 2022, with private LTE playing a pivotal role in enabling seamless operations. Highlighting this trend, Germany alone witnessed a 25% year-on-year increase in private LTE deployments in its manufacturing sector.

Government Initiatives and Spectrum Allocation

Government initiatives aimed at fostering innovation through spectrum allocation have also significantly driven the private LTE market. According to the European Commission, governments across Europe have allocated dedicated spectrum bands for private LTE, fostering innovation and adoption. For instance, the UK’s Ofcom introduced Local Access Licenses, allowing businesses to deploy private LTE networks at affordable rates. Similarly, France’s ARCEP has streamlined spectrum allocation processes, resulting in a 40% rise in private LTE deployments in 2022. These initiatives have significantly reduced barriers to entry, encouraging SMEs and large enterprises alike to adopt private LTE solutions.

MARKET RESTRAINTS

High Initial Deployment Costs

One of the primary restraints hindering the widespread adoption of private LTE networks is the high initial deployment costs. According to the European Central Bank, the average cost of deploying a private LTE network ranges from EUR 500,000 to EUR 2 million, depending on scale and complexity. This high upfront investment acts as a deterrent, particularly for small and medium-sized enterprises. A study by the European Association of Electrical Contractors revealed that nearly 45% of SMEs cite financial constraints as the primary barrier to adopting private LTE solutions.

Spectrum Fragmentation Across Countries

Another significant restraint is the lack of harmonized spectrum regulations across European countries. According to the European Telecommunications Network Operators’ Association (ETNO), spectrum regulations vary significantly across European countries, creating challenges for cross-border operations. For example, while Germany has allocated 3.7-3.8 GHz for private LTE, other nations like Italy and Spain have yet to standardize similar frameworks. This fragmentation complicates network planning and increases operational costs for multinational enterprises.

MARKET OPPORTUNITIES

Integration with 5G Technologies

The convergence of private LTE with 5G technologies presents a significant opportunity for market growth. According to the European 5G Observatory, over 70% of private LTE networks in Europe are expected to integrate with 5G by 2025. This convergence will unlock new use cases, such as autonomous vehicles and smart city applications. The European Investment Fund predicts that 5G-enabled private LTE solutions could generate an additional EUR 150 billion in economic value by 2030.

Expansion in Rural and Remote Areas

Private LTE networks also offer immense potential for bridging the digital divide in rural and remote areas. According to the European Network Against Rural Exclusion (ENARE), private LTE networks can provide reliable connectivity in regions where public network coverage is often limited. By 2023, pilot projects in Sweden and Norway demonstrated a 30% improvement in connectivity for remote communities using private LTE. This expansion not only enhances quality of life but also supports economic development in underserved areas.

MARKET CHALLENGES

Regulatory Uncertainty

Regulatory uncertainty remains a significant challenge for private LTE operators. According to the European Union Agency for Cybersecurity (ENISA), evolving cybersecurity regulations pose challenges for private LTE operators. Compliance costs are estimated to increase by 20% annually, impacting profitability. Enterprises must navigate complex regulatory landscapes to ensure compliance, which adds to operational burdens.

Interoperability Issues

Interoperability between private LTE networks and legacy systems is another major challenge. According to the European Telecommunications Standards Institute (ETSI), interoperability issues remain a significant hurdle. Over 60% of enterprises reported compatibility issues during initial deployments, leading to delays and increased costs. Addressing these challenges requires standardized protocols and greater collaboration between stakeholders.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 9.24% |

| Segments Covered | By Component, End User, and Region |

|

Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and Rest of Europe |

|

Market Leaders Profiled | Cisco Systems Inc, Telefonaktiebolaget LM Ericsson, Huawei Investment & Holding Co Ltd, Samsung Group, Verizon Communications Inc, CommScope Holding Co Inc, Star Solutions, Sierra Wireless Inc, and Kyndryl Holdings Inc. |

SEGMENTAL ANALYSIS

By Component Insights

The Frequency Division Duplexing (FDD) segment dominated the private LTE market in Europe by accounting for 65.9% of the European market share in 2024. The ability of FDD to provide symmetrical upload and download speeds that is making it ideal for industries requiring real-time data exchange is majorly boosting the domination of the FDD segment in the European market. The reliability and proven performance have made it the preferred choice for enterprises across various sectors.

The Time Division Duplexing (TDD) segment is anticipated to witness the highest CAGR of 22.8% over the forecast period. The cost-effectiveness and suitability of TDD for IoT applications are primarily driving the growth of the TDD segment in the European market. As industries increasingly adopt IoT devices, TDD's flexibility and scalability make it an attractive option for future deployments.

By End User Insights

The manufacturing segment captured 36.8% of the European market share in 2024. The growth of the manufacturing segment in the European market is driven by the need for low-latency communication in smart factories. Private LTE enables seamless integration of IoT devices, robotics, and AI-driven analytics, enhancing operational efficiency.

The healthcare segment is expected to witness the fastest CAGR of 26.1% over the forecast period owing to the increasing adoption of telemedicine and remote patient monitoring. Private LTE networks provide secure and reliable connectivity, ensuring uninterrupted healthcare services.

REGIONAL ANALYSIS

Western Europe held the leading share of the European private LTE market in 2024. Its dominance is driven by advanced infrastructure, high industrialization, and favorable regulatory frameworks. Eastern Europe is the fastest-growing region, with a CAGR of 20%. According to the European Bank for Reconstruction and Development, this growth is supported by government incentives and increasing investments in smart manufacturing and IoT.

KEY MARKET PLAYERS

The major players in the Europe Private LTE market include Cisco Systems Inc, Telefonaktiebolaget LM Ericsson, Huawei Investment & Holding Co Ltd, Samsung Group, Verizon Communications Inc, CommScope Holding Co Inc, Star Solutions, Sierra Wireless Inc, and Kyndryl Holdings Inc.

MARKET SEGMENTATION

This research report on the Europe private LTE market is segmented and sub-segmented into the following categories.

By Component

- FDD

- TDD

By End User

- Manufacturing

- Energy & Utilities

- Healthcare

- Transportation

- Mining

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is driving the growth of the Europe private LTE market?

The Europe private LTE market is growing due to increased demand for secure, high-speed, and low-latency communication networks across industries such as manufacturing, transportation, and energy. Governments and enterprises are investing in private LTE to enhance operational efficiency and security.

Which industries are the primary adopters of private LTE in Europe?

Key industries adopting private LTE in Europe include manufacturing, energy, utilities, transportation, logistics, and public safety. These sectors require reliable and dedicated connectivity to support automation, IoT, and critical communications.

How is private LTE supporting 5G adoption in Europe?

Private LTE acts as a stepping stone for 5G, enabling enterprises to deploy LTE now and upgrade to private 5G when available. Many companies are integrating LTE with 5G-ready infrastructure to ensure a smooth transition.

What is the future outlook for the Europe private LTE market?

The market is expected to expand with increasing adoption across industries, improved spectrum regulations, and advancements in LTE and 5G technologies. More enterprises are likely to invest in private LTE to enhance connectivity and digital transformation efforts.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com