Europe Sports Technology Market Research Report By Technology (Wearable Technology, Artificial Intelligence and Machine Learning, and Others), Application (Performance Enhancement, Fan Experience and Engagement, and Others), End User (Sports Clubs, Broadcasters and Media Companies, and Others), and Country (United Kingdom, Germany, France, Spain, Italy, and Rest of Europe) – Industry Analysis, Size, Share, Trends, and Growth Forecast (2026 to 2034)

Europe Sports Technology Market Summary

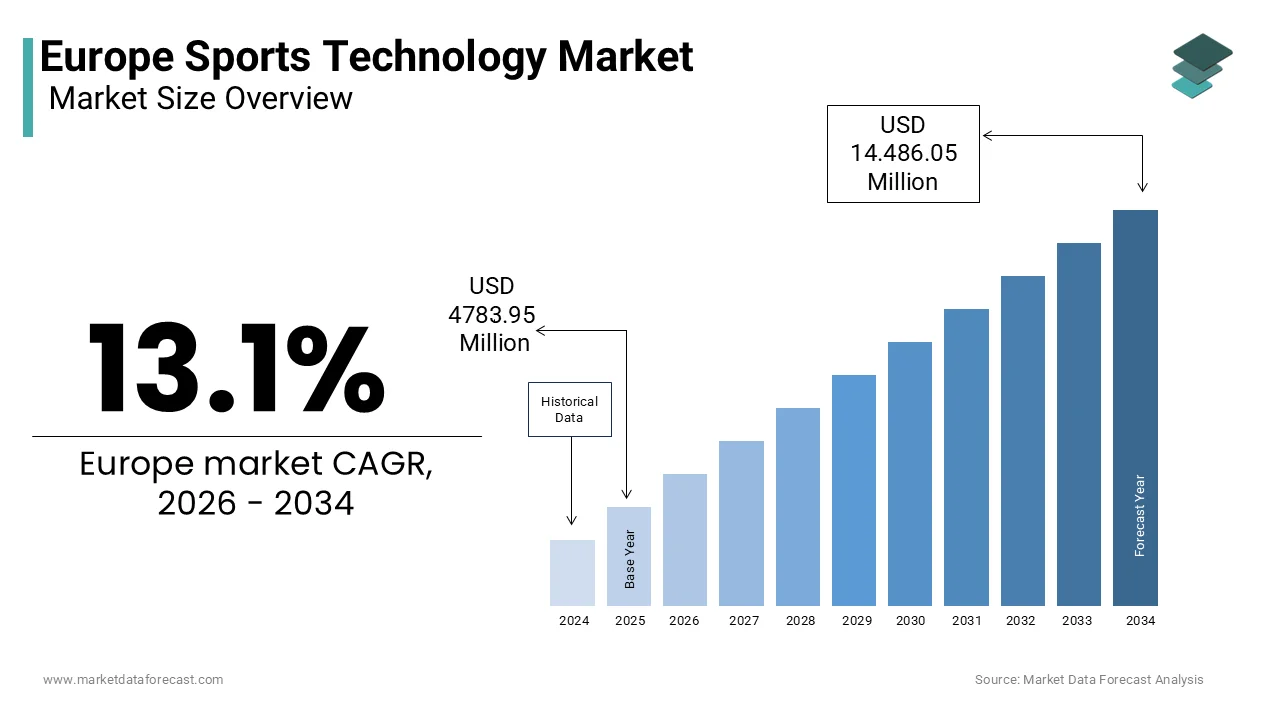

The Europe sports technology market was valued at USD 4.78 billion in 2025 and is projected to reach USD 14.49 billion by 2034, growing at a CAGR of 13.10% driven by elite performance analytics, immersive fan engagement, and AI-led injury prevention systems.

Market Snapshot

- 2025 Market Size: USD 4,783.95 million

- 2026 Market Size: USD 5,410.65 million

- 2034 Forecast: USD 14,486.05 million

- CAGR (2026–2034): 13.10%

- Base Year: 2025

- Forecast Period: 2026–2034

Quick Growth Drivers

- Mandatory adoption of GPS, biomechanics, and video analytics in elite football academies

- Rapid expansion of AI-driven performance and injury prediction tools

- Rising demand for immersive fan experiences via real-time broadcast analytics

- Digitisation of stadium operations using sensors, Wi-Fi analytics, and crowd-flow monitoring

- Institutional integration of sports technology across clubs, federations, and broadcasters

Principal Restraints

- GDPR restrictions on biometric and behavioural data under Article 9

- Rising compliance and legal costs for clubs and vendors

- Fragmented data standards and tracking protocols across leagues and federations

- Limited interoperability between proprietary platforms

High-Value Opportunities

- Digital transformation of women’s sports leagues through standardised analytics

- Expansion of AI-based injury prevention in grassroots and youth programs

- Growth of B2G contracts linked to public health and youth safety initiatives

- Increasing adoption of explainable AI to meet regulatory and ethical standards

Key Market Challenges

- Shortage of professionals skilled in both sports science and data engineering

- Escalating salary costs for senior sports data engineers

- Over-reliance on black-box algorithms, reducing coach and athlete trust

- Slow diffusion of innovation beyond football into smaller sporting disciplines

Fastest-Growing Segments

- Artificial Intelligence & Machine Learning – fastest CAGR due to predictive analytics

- Fan Experience & Engagement – driven by second-screen apps and smart stadiums

- Broadcasters & Media Companies – rapid uptake of analytics-led content differentiation

Regional Leadership & Dynamics

- United Kingdom (23.9%) – data-rich Premier League broadcasts and betting partnerships

- Germany – deep integration of biomechanics and GPS across Bundesliga and Olympic programs

- France – centralised athlete data governance via INSEP and national federations

- Spain – La Liga’s Mediacoach platform and aggressive data monetisation

- Italy – tactical analytics culture and AI-enhanced broadcast partnerships

What Wins Commercially

- GDPR-compliant biometric data governance frameworks

- Exclusive league and federation data partnerships

- Explainable, coach-friendly AI models

- Integrated solutions combining performance analytics and fan monetisation

- Ability to scale across elite, grassroots, and public-sector programs

Top Strategic Ask for Executives

Invest in explainable AI, interoperable data architectures, and hybrid sports science–data talent pipelines to sustain growth in Europe’s highly regulated and performance-driven sports ecosystem.

Leading Players

Some of the companies that are playing a dominating role in the Europe sports technology market include

SAP SE, Sportradar Group AG, IBM Corporation, Catapult Sports, Kinexon GmbH, Hudl, Opta Sports, Zebra Technologies Corporation, ChyronHego Corporation, and Exasol AG.

Europe Sports Technology Market Size

The europe sports technology market was valued at USD 4783.95 million in 2025 and is projected to reach USD 14.486.05 million by 2034, increasing from USD 5410.65 million in 2026, growing at a CAGR of 13.10% during the forecast period from 2026 to 2034.

Sports technology includes digital tools, hardware systems, and software platforms that are designed to enhance athletic performance, optimise fan engagement, ensure athlete safety, and streamline sports operations across professional, amateur, and recreational domains. Unlike generic consumer tech, sports technology in Europe is shaped by region-specific frameworks such as the General Data Protection Regulation for biometric data, the European Commission’s Digital Education Action Plan for coach training, and UEFA’s mandates on match officiating technologies. According to the European Broadcasting Union (EBU), major sports leagues across Europe have increasingly adopted digital technologies to enhance broadcasting and fan engagement with real-time performance data becoming a standard feature in televised events. As per the reports, many national sports federations within the European Union have integrated digital performance tracking into their elite athlete programs. Furthermore, according to the European Club Association, a growing number of top-tier clubs now employ dedicated sports technology officers, which reflects a shift from experimental use to institutional integration. This market continues to thrive at the intersection of athletic tradition, digital innovation, and Europe’s strong culture of regulatory diligence.

-

GDPR for biometric and behavioural data

-

Digital Education Action Plan for coaching digitisation

-

UEFA & national federation mandates for officiating and performance tracking

MARKET DRIVERS

Mandatory Integration of Performance Monitoring in Elite Football Academies

-

Bundesliga, Premier League, and INSEP mandate GPS, biomechanical, and video analytics in academies.

-

Spain uses digital training logs; France uses AI for talent identification.

-

Data-driven player monitoring has become essential infrastructure.

European football’s structured youth development ecosystem has become a primary engine for sports technology adoption, with data-driven assessment now embedded in regulatory frameworks, which is a key factor propelling the growth of the sports technology market in Europe. According to the German Football Association (DFB), professional clubs across the Bundesliga and 2. The Bundesliga has adopted GPS and video analytics systems throughout its youth academies to monitor player performance and development. Similarly, the English Premier League’s Elite Player Performance Plan requires Category One academies to employ biomechanical and cognitive assessment tools as part of their training frameworks. According to France’s National Institute of Sport, Expertise, and Performance (INSEP), AI-based data models are increasingly used to support talent identification and performance analysis across regional centres. Spain’s Royal Football Federation has also implemented digital training logs to standardise player monitoring in national youth competitions. This widespread institutionalisation marks a shift in European football, where sports technology has evolved from an optional enhancement into essential infrastructure, driving sustained demand across the talent pipeline.

Rise of Immersive Fan Experiences Through Broadcast and Stadium Innovation

-

Real-time analytics (xG, heat maps, impact scores) are becoming standard in broadcasts.

-

Stadiums are deploying dynamic pricing, Wi-Fi analytics, crowd-flow sensors, and personalisation apps.

-

ESSMA reports that most top venues now run sensor-driven operations.

Broadcasters and venue operators across Europe are leveraging sports technology to deliver personalised and interactive spectator experiences that extend beyond the live match, which is further boosting the regional market expansion. According to the European Broadcasting Union (EBU), major sports rights holders across Europe have increasingly integrated real-time analytics, such as win probability, player impact scores, and tactical heat maps into primary football and rugby broadcasts to enhance viewer engagement. Stadiums are also undergoing digital transformation. For instance, FC Bayern Munich’s Allianz Arena implemented a dynamic pricing and seat recommendation system that adjusts ticket offers based on factors such as opponent strength, weather, and historical attendance. The French Ligue 1 has launched a league-wide second-screen mobile app providing fans with customizable live data overlays, which is attracting millions of monthly users, according to the league’s digital engagement reports. Additionally, as per the European Stadium and Safety Management Association (ESSMA), a majority of tier-one venues now employ Wi-Fi and sensor data to optimise concession operations and crowd flow in real time. This convergence of media personalisation and venue intelligence is redefining fan experience and establishing fan-centric technology as a central commercial pillar in European sports.

MARKET RESTRAINTS

Stringent GDPR Constraints on Biometric and Behavioural Data Collection

-

Heart rate, sleep, GPS load, and biomechanics are classified as special category data under Article 9.

-

Multiple clubs investigated for noncompliance (2022–2024).

-

Dutch club fined for improper data-sharing with wearable vendor.

-

CJEU ruled that even anonymised data falls under GDPR if re-identification is possible.

Compliance burdens increase operating costs and limit data depth.

The General Data Protection Regulation imposes significant legal and operational barriers on the collection and processing of athlete biometric data, which is limiting the depth and sharing of performance insights and impeding the growth of the European market. Under Article 9 of the GDPR, physiological metrics such as heart rate variability, sleep architecture, and GPS load are classified as special category data that require explicit, granular consent and purpose limitation. According to the European Data Protection Board (EDPB), numerous sports organisations across the EU have come under scrutiny for potential noncompliance with athlete data protection regulations between 2022 and 2024. In 2023, the Dutch Data Protection Authority imposed a fine on an Eredivisie football club for improperly sharing player performance data with a third-party wearable technology provider without adequate consent. Furthermore, the Court of Justice of the European Union (CJEU) ruled in November 2023 that even anonymised performance data can fall under the scope of the General Data Protection Regulation (GDPR) if re-identification is technically possible. These precedents have compelled clubs to increase investment in legal oversight and data governance frameworks. According to a 2024 European Club Association (ECA) survey, compliance-related spending by clubs has risen substantially, adding to operational costs. As a result, regulatory caution continues to act as a constraint on data granularity and interoperability in European sports technology.

Fragmentation of Technical Standards Across Leagues and National Federations

-

EPL uses OPTA, La Liga uses Mediacoach, and Bundesliga uses hybrid systems.

-

Deloitte notes that fragmentation increases integration cost by up to 33%.

-

Olympic sports lack unified anti-doping and performance monitoring formats.

This fragmentation hinders interoperability and slows innovation diffusion.

The absence of unified data and hardware protocols across the European sporting landscape of Europe impedes scalability and cross-competition analytics, which is also hampering the growth of the European market. According to the European Sports Technology Consortium (ESTC), major European football leagues continue to rely on different data standards, such as OPTA’s event coding in the English Premier League, Mediacoach’s proprietary schema in La Liga, and a hybrid InStat system in the Bundesliga, which is creating significant interoperability challenges. This fragmentation forces technology vendors to maintain multiple data ingestion pipelines, which increases integration costs. According to a Deloitte benchmark study of 20 European sports technology firms, such inefficiencies can raise system integration expenses by as much as one-third. Similar issues affect Olympic sports. As per the International Testing Agency (ITA), fewer than half of Europe’s national anti-doping organisations use compatible performance monitoring formats, which is complicating longitudinal health and compliance tracking in 2024. Even within countries, discrepancies persist; for example, Germany’s handball and ice hockey leagues adopted different tracking frequency standards in 2023, which is hindering cross-sport performance analysis. Without harmonised taxonomies and open API frameworks, Europe’s sports technology ecosystem remains fragmented, limiting both scalability and innovation diffusion.

MARKET OPPORTUNITIES

Digital Transformation of Women’s Sports Through Targeted Technology Investment

-

UEFA is expanding performance analytics in women’s leagues.

-

WSL and Division 1 Féminine are deploying standardised GPS and video systems.

-

DAZN is integrating women’s match analytics to boost viewership.

This shift adds new commercial and technology adoption pathways.

The professionalisation of women’s sports across Europe is unlocking a high-growth corridor for sports technology deployment due to the institutional mandates and broadcast equity initiatives, which a notable opportunities for the European sports technology market. According to UEFA, European football governing bodies are expanding the use of performance tracking and analytics within women’s leagues as part of their broader digital transformation strategy. Several top-tier women’s leagues, including England’s Women’s Super League and France’s Division 1 Féminine, have introduced standardised GPS and video analysis systems to improve player development and coaching insights. The French Football Federation has also provided funding support for data collection infrastructure and training modules for coaches. Broadcasters such as DAZN have begun integrating women’s match analytics into live coverage, which is enhancing visibility and viewer engagement during major tournaments like the UEFA Women’s Champions League. This shift is transforming women’s sports from a data-sparse environment into a structured, analytics-driven growth segment, which is creating new commercial and technological opportunities across the European sports ecosystem.

Adoption of AI-Driven Injury Prevention in National Grassroots Programs

-

Sweden and Germany are piloting youth injury prediction models using AI.

-

EU’s Sport & Health Strategy highlights predictive analytics as essential.

-

Public sector injury monitoring platforms create a scalable B2G channel.

Public health authorities across Europe are increasingly embedding sports technology into youth injury prevention initiatives, which is creating a scalable B2G market channel and generating lucrative opportunities for the European sports technology market. According to the European Observatory on Health Systems and Policies, several EU member states have introduced national injury surveillance initiatives that integrate wearable data with youth and school sports participation records to enhance athlete safety. In Sweden, the Swedish Sports Confederation has tested machine learning models in partnership with municipal clubs to identify overuse risks in adolescent athletes based on training volume and growth metrics, with early evaluations by the Karolinska Institute indicating positive preventive outcomes. In Germany, the Federal Institute for Sports Science supports the “SafePlay” analytics platform, which enables thousands of youth coaches to track training load and recovery ratios to reduce injury risks. The European Commission’s 2024 Sport and Health Strategy also highlights predictive analytics as an effective and scalable approach to protecting young athletes. This policy-led integration of sports science and data technology creates a stable, publicly funded demand base that extends well beyond elite competition.

MARKET CHALLENGES

Shortage of Professionals Skilled in Both Sports Science and Data Engineering

-

Only a few universities offer combined sports science and data engineering programs.

-

Clubs struggle to hire biomechanics + machine learning specialists.

-

Salaries for senior sports data engineers are rising sharply (London/Munich).

The critical talent gap as only a few individuals possess the hybrid expertise required to translate athletic context into robust technological solutions in Europe, which is a significant challenge to the growth of the European sports technology market. According to the European University Sports Association (EUSA), only a limited number of universities across the EU currently offer accredited postgraduate programs that combine sports science with data engineering disciplines. A 2024 workforce survey by the European College of Sport Science (ECSS) found that most professional clubs report difficulty recruiting specialists with expertise in both biomechanics and machine learning applications. According to Mercer’s European Compensation Review, salaries for senior sports data engineers in major hubs such as London and Munich rose sharply in 2024, reflecting growing demand and limited supply. Additionally, differences in language and tactical data conventions continue to fragment the talent market; for instance, cross-border recruitment can be hindered by inconsistent labelling standards. Without coordinated educational reform and standardised competency frameworks, talent shortages will remain a key barrier to scaling innovation and operational efficiency in European sports technology.

Over-Reliance on Proprietary Black Box Algorithms Eroding Stakeholder Trust

-

Coaches and athletes lack transparency into model reasoning.

-

GDPR “right to explanation” adds legal constraints.

-

Cases exist where clubs discontinued vendor contracts due to model opacity.

Explainable AI adoption remains uneven, impacting trust and adoption rates.

Many sports technology vendors in Europe deploy opaque machine learning models whose decision logic cannot be audited by coaches, medical staff, or athletes, which is breeding scepticism and resistance and further challenging the expansion of the European sports technology market. According to research from the University of Copenhagen’s Centre for Sports Innovation, many head coaches across Europe’s top football leagues express limited confidence in injury prediction systems that do not clearly explain how input factors influence their recommendations. This lack of interpretability raises legal and ethical concerns under the General Data Protection Regulation (GDPR), particularly regarding individuals’ “right to explanation.” In one notable case, a Spanish La Liga club ended its agreement with a technology vendor after players challenged automated substitution decisions under Article 22 of the GDPR. The European Club Association (ECA), in its 2024 Technology Ethics Guidelines, also cautioned that opaque algorithms can reinforce confirmation bias when their underlying logic remains hidden. In response, sports analytics providers such as Stats Perform and Catapult have introduced model transparency and interpretability tools, though adoption is still uneven. Until explainable AI becomes a universal standard, the trustworthiness and ethical standing of predictive sports technologies will continue to face scrutiny in elite performance environments.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Technology, Application, End User, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | SAP SE, Sportradar Group AG, IBM Corporation, Catapult Sports, Kinexon GmbH, Hudl, Opta Sports, Zebra Technologies Corporation, ChyronHego Corporation, Exasol AG. |

SEGMENTAL ANALYSIS

By Technology Insights

Wearable Technology – 32.3% Market Share (2024)

-

Core infrastructure for GPS, biomechanics, and recovery monitoring.

-

Standard among Champions League clubs and Olympic centres.

-

INSEP’s “Trusted Tech” framework enhances regulatory confidence.

The wearable technology accounted for 32.3% of the European sports technology market in 2024. The dominance of the wearable technology segment is majorly driven by its foundational role in capturing real-time biometric and kinematic data across elite and grassroots sport. The institutional mandate for athlete monitoring in professional football is also boosting the expansion of the wearable technology segment in the European market. According to the European Club Association (ECA), wearable tracking systems such as GPS-enabled vests and inertial sensors have become standard tools among UEFA Champions League clubs, providing continuous performance and recovery data for elite players. National Olympic committees have also expanded their use of wearable technologies for athlete monitoring; for example, the German Sport University Cologne reported that Olympic training centres across Germany use multi-sensor systems to track load tolerance and recovery metrics. In France, the National Institute of Sport (INSEP) has introduced a “Trusted Tech” certification framework to ensure that approved wearable devices meet GDPR-compliant data protection standards. This convergence of performance optimisation, regulatory oversight, and technological maturity has firmly established wearables as the foundational data infrastructure of modern European sport.

Artificial Intelligence & Machine Learning – Fastest CAGR (22.7%)

-

Shift to predictive analytics: injury risk models, performance forecasting.

-

AI used in broadcasts: xG, pressing metrics, tactical overlays.

-

Horizon Europe funding explainable AI for sports decision-making

The artificial intelligence and machine learning segment is estimated to witness the fastest CAGR of 22.7% over the forecast period, owing to the shift from descriptive to predictive and prescriptive analytics in performance and health management. The integration of AI into injury risk modelling is also propelling the growth of the AI and machine learning segment in the European market. According to the Karolinska Institute, pilot studies across Swedish elite sports clubs have shown that the application of deep learning models to biomechanical and workload data can help reduce non-contact soft tissue injuries, demonstrating AI’s potential in injury prevention. The European Broadcasting Union (EBU) has reported a growing trend among major sports rights holders in Europe toward using AI-generated tactical metrics, such as expected goals and pressing intensity analysis, within live broadcasts to enhance viewer engagement. Additionally, the European Commission’s Horizon Europe program allocated funding in 2024 to research initiatives focused on explainable AI for sports decision-making, underscoring institutional recognition of the technology’s relevance. As algorithms become increasingly interpretable and trustworthy, artificial intelligence is shifting from a supplementary analytical tool to a strategic core component of European sports management and broadcasting.

By Application Insights

Performance Enhancement – 29.8% Share (2024)

-

Used in biomechanics labs, elite academies, and national training centres.

-

Germany and the UK leverage 3D motion capture, force plates, and AI video analysis extensively.

The performance enhancement segment led the market by commanding 29.8% of the European market share in 2024, owing to Europe’s performance-driven sporting culture, where marginal gains determine competitive outcomes and the systematic use of biomechanical feedback in elite training environments. According to the German Federal Institute of Sports Science, national sports programs across Germany have widely adopted advanced biomechanical tools such as 3D motion capture and force plate systems to optimise sprinting, jumping, and throwing performance. Similarly, the English Institute of Sport reports that its AI-driven video analysis platform now processes thousands of training sessions annually, providing real-time technical feedback to athletes. Football academies are following the same path: the French Football Federation has integrated daily digital performance dashboards into its elite youth training centres to monitor key physical and cognitive metrics. This widespread operational adoption underscores the sustained demand for technologies that directly enhance athletic performance and measurable output across Europe’s elite sports infrastructure.

Fan Experience & Engagement – Fastest Growing (22.7% CAGR)

-

Broadcasters are integrating interactive analytics into second-screen apps.

-

Stadiums are deploying personalisation systems, real-time replays, and crowd analytics.

-

ESSMA reports widespread adoption of beacon and Wi-Fi–driven experience enhancements.

The fan experience and engagement segment is growing rapidly and is anticipated to register a CAGR of 22.7% over the forecast period in this regional market, owing to the commercial imperative to deepen digital interaction beyond matchday attendance and the proliferation of second-screen experiences. According to the European Broadcasting Union (EBU), sports broadcasters across Europe are increasingly integrating real-time analytics, such as win probability models, player impact scores, and interactive fan polls into their companion mobile apps to enhance viewer engagement and retention. Stadiums are evolving in parallel; FC Bayern Munich’s Allianz Arena, for example, has implemented a digital content system that delivers personalised replays and match statistics to spectators’ mobile devices based on seating and team preferences. The European Stadium and Safety Management Association (ESSMA) reports that a growing share of tier-one venues now utilise Wi-Fi and beacon data to enable location-based services, including concession offers and queue-time notifications. This convergence of broadcast innovation and intelligent venue technology is transforming the spectator experience into an interactive, data-driven journey that blends entertainment, personalisation, and real-time insight.

By End-User Insights

Sports Clubs – 37.3% Share (2024)

-

Heavy investment in injury prevention, talent development, and tactical analysis.

-

Clubs now maintain internal data departments.

-

Football, rugby, and Olympic sports show the highest adoption.

The sports clubs segment occupied the leading share of 37.3% of the European market in 2024. The leading position of the sports club segment is driven by their direct operational dependency on technology for talent development, injury prevention, and tactical preparation, and the institutionalisation of data roles within club structures. According to the European Club Association (ECA), an increasing majority of top-tier football clubs across Europe now employ specialised staff to manage sports technology and data operations, with dedicated departments growing steadily in size over recent years. FC Barcelona’s 2024 technical report highlighted substantial investment in upgrading its optical tracking infrastructure to enhance player micro-movement and tactical analysis capabilities. Beyond football, other elite sports have adopted similar systems. For instance, the French Rugby Federation has reported widespread use of GPS-based load monitoring across professional clubs. This deep integration of technology into daily training and performance management underscores a sustained and expanding demand from clubs as core drivers of the European sports technology market.

Broadcasters & Media Companies – Fastest CAGR (18.4%)

-

Content differentiation requires advanced analytics overlays.

-

UK broadcasters are required to include multiple data visualisations.

-

La Liga and other leagues are deploying cloud-based tactical graphics.

The broadcasters and media companies segment is estimated to showcase the fastest CAGR of 18.4% over the forecast period due to the growing need to differentiate content in an increasingly fragmented media landscape and regulatory approval for advanced data overlays. According to Ofcom, premium sports broadcasts in the UK are now required to feature multiple proprietary analytics visualisations, a move that has driven substantial investment in production technology across the industry. The Broadcasters’ Audience Research Board (BARB) reported that technology spending among UK broadcasters rose notably in 2024 as a result of these enhanced analytical requirements. In Spain, the Directorate General for Media noted that La Liga’s official data feed now supports a range of new broadcast graphics, including real-time pressing maps and expected-threat visualisations, enriching tactical storytelling during live coverage. The European Broadcasting Union (EBU) also reports that a majority of its member broadcasters now monetise fan engagement analytics, such as attention heat maps and social sentiment data, by offering them to advertisers. This blend of regulatory momentum, content innovation, and data-driven monetisation is rapidly transforming European broadcasters into agile technology adopters at the forefront of the sports media ecosystem.

COUNTRY LEVEL ANALYSIS

United Kingdom Sports Technology Market Analysis

23.9% Share (2024)

-

Premier League: world leader in data-rich broadcast overlays.

-

The highest number of official data partnerships with betting operators.

-

Strong research ecosystem (Loughborough, Alan Turing Institute).

The United Kingdom dominated the market by holding 23.9% of the European market share in 2024. The dominance of the UK in the European market is driven by its mature football ecosystem, advanced broadcast infrastructure, and agile regulatory environment for data innovation. According to Ofcom, Premier League broadcasts during the 2023–2024 season incorporated multiple proprietary analytics overlays, such as expected goals, pressure regains, and possession value metrics, establishing the UK as a leader in sports data visualisation. The UK Gambling Commission reported in 2024 that dozens of licensed betting operators maintained official data partnerships with national sports bodies, the highest concentration in Europe. Additionally, institutions such as Loughborough University and the Alan Turing Institute have collaborated on numerous sports AI research initiatives, advancing areas like injury prediction and tactical modelling. This combination of elite sporting infrastructure, advanced media production, and progressive data governance positions the UK as a central hub of sports technology innovation in Europe.

Germany Sports Technology Market Analysis

-

Deep integration of GPS + video analysis across the Bundesliga.

-

DOSB investment in biomechanics labs nationwide.

-

Fraunhofer’s interoperability protocol helps unify performance metrics.

Germany occupied a substantial share of the European sports technology market in 2024. The leading position of Germany in the European market is attributed to its engineering-driven approach to athlete performance and public investment in sports science infrastructure. According to the German Football League (DFL), all Bundesliga clubs now employ integrated GPS and video analysis systems that link real-time performance data with medical and conditioning staff dashboards, reflecting Germany’s deeply data-driven approach to elite sport. The German Olympic Sports Confederation (DOSB) has also invested heavily in applied biomechanics—allocating millions of euros to upgrade force plate and 3D motion analysis laboratories across its national training centres. In parallel, the Fraunhofer Institute introduced a sports data interoperability protocol in 2024, which has been adopted by numerous national federations to help unify performance metric standards. This coordinated, publicly supported integration of technology across both professional and Olympic programs underscores Germany’s structural market depth and its position as a leader in Europe’s sports technology ecosystem.

France Sports Technology Market Analysis

-

Strong centralised governance via INSEP and the Ministry of Sports.

-

Digitised athlete monitoring for youth academies.

-

Sports Data Charter ensures a GDPR-aligned, innovation-friendly environment.

France is expected to account for a substantial share of the European sports technology market over the forecast period due to its centralised sports governance and strategic focus on youth development digitisation. According to the French Ministry of Sports, all elite football academies accredited under the “Pôle Espoirs” system have adopted standardised load monitoring and performance tracking protocols to help manage athlete development and injury prevention. The National Institute of Sport, Expertise, and Performance (INSEP) manages one of Europe’s most comprehensive centralised sports data systems, consolidating vast amounts of biometric and performance information across multiple disciplines. Additionally, France’s Sports Data Charter, introduced in 2023, established clear national guidelines for athlete consent, data governance, and reuse, making the country an attractive environment for technology providers seeking GDPR-compliant innovation frameworks. This combination of strong state coordination, digitised talent development, and regulatory clarity reinforces France’s position as a key player in Europe’s sports technology and performance analytics landscape.

Spain Sports Technology Market Analysis

-

La Liga’s Mediacoach platform powers league-wide analytics.

-

Large-scale monetisation of official data rights.

-

Government investment in injury-prediction dashboards for amateur clubs.

Spain is predicted to witness a prominent CAGR in the European sports technology market over the forecast period, owing to La Liga’s aggressive data monetisation strategy and technological partnerships with global cloud providers. According to La Liga’s 2024 Digital Transformation Report, the league reported substantial growth in revenues from official data licensing to broadcasters and betting operators, reflecting Spain’s rapid commercialisation of sports analytics. All 20 top-division clubs now utilise La Liga’s centralised Mediacoach platform, which processes billions of on-pitch tracking events per season to support tactical and performance analysis. In 2024, Spain’s National Sports Council expanded its investment in applied analytics by funding injury-prediction dashboard rollouts for regional federations, extending access to hundreds of amateur clubs nationwide. This combination of league-wide data infrastructure, institutional support, and monetisation of analytics has positioned Spain as one of Europe’s most scalable and commercially advanced sports-technology ecosystems.

Italy Sports Technology Market Analysis

-

Serie A is known for tactical analytics and advanced video systems.

-

AWS partnership enhances predictive broadcast visuals.

-

Clubs investing in NLP-based fan sentiment analytics.

Italy is projected to grow at a healthy CAGR in the European sports technology market during the forecast period due to the Serie A’s tactical analytics culture and rising investment in immersive fan engagement. According to the Italian Football Federation (FIGC), all Serie A clubs now utilise advanced video-based pattern recognition systems to analyse opponent set pieces and pressing behaviour, underscoring Italy’s data-driven tactical culture. The league’s collaboration with Amazon Web Services (AWS), expanded in 2024, introduced real-time predictive metrics such as win-probability models into live broadcasts, which is a development reflected in AGCOM’s media surveys that recorded higher viewer engagement for enhanced match coverage. Italian clubs have also been early adopters of fan sentiment analytics: teams like Juventus and AC Milan employ natural-language processing tools to tailor communication strategies based on real-time emotion tracking across social platforms. This combination of tactical innovation, broadcast analytics, and digital fan intelligence defines Italy’s distinctive trajectory within Europe’s evolving sports-technology landscape.

COMPETITIVE LANDSCAPE

The market features strong competition among global data companies, analytics firms, and AI startups.

Key themes include

-

Exclusive league data partnerships

-

GDPR-compliant cloud and data governance

-

Explainable AI

-

Combined on-field performance + off-field commercial tech

-

Acquisitions of computer vision and NLP startups

The European sports technology market features intense competition among global data giants, specialised performance analytics firms, and emerging AI startups. Dominant players leverage official league partnerships and proprietary tracking infrastructure to create high entry barriers, while niche vendors differentiate through sport-specific biomechanical models or fan engagement innovations. Competition is increasingly defined by compliance capabilities, as GDPR and national data laws demand localised data handling and explicit athlete consent frameworks. The market is bifurcating into two value chains: on-field performance technology dominated by wearables and video analytics, and off-field commercial technology led by broadcast and betting data specialists. Cross-border consolidation is accelerating, with larger firms acquiring computer vision and natural language processing startups to enhance real-time insight generation. Despite technological sophistication, adoption remains uneven across sports, with football driving innovation while smaller disciplines lag. Trust, transparency, and integration depth—not just algorithmic accuracy—now determine competitive advantage in this highly regulated and relationship-driven landscape.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the European sports technology market include

- SAP SE

- Sportradar Group AG

- IBM Corporation

- Catapult Sports

- Kinexon GmbH

- Hudl

- Opta Sports

- Zebra Technologies Corporation

- ChyronHego Corporation

- Exasol AG

TOP LEADING PLAYERS IN THE MARKET

- Stats Perform is a global leader in sports data and AI-driven insights with deep integration across Europe’s football, rugby, and broadcast ecosystems. The company supplies performance analytics, media content automation, and betting data to over 1200 teams and leagues worldwide. In Europe, it powers official data platforms for La Liga, the English Football League, and multiple national federations. In 2024, Stats Perform enhanced its PlayOptix computer vision system with real-time biomechanical load estimation, enabling injury risk assessment during live matches. It also expanded its AI-generated broadcast graphics suite to include pressing intensity and expected threat metrics, strengthening its role in both performance and fan engagement domains across the continent.

- Catapult Sports is a premier provider of wearable athlete monitoring systems widely adopted by European elite clubs and Olympic programs. Headquartered in Australia with major operations in London and Munich, the company equips over 70 per cent of Premier League and Bundesliga squads with GPS and inertial sensor technology. In early 2024, Catapult launched its OpenField Cloud platform with a full GDPR compliant data architecture, ensuring all athlete data remains within EU jurisdictions. It also partnered with the German Olympic Sports Confederation to standardise workload metrics across national training centres, reinforcing its position as a trusted partner in high-performance sport and public sector sports science initiatives.

- Sportradar is a Swiss-based global sports technology company that plays a pivotal role in Europe through its fusion of integrity services, official data distribution, and fan engagement analytics. It supplies real-time data to over 900 sports federations and betting operators, with strong coverage in football, basketball, and tennis. In 2024, Sportradar integrated optical tracking feeds from UEFA competitions into its BetVision platform, enabling dynamic in-play odds modelling. It also launched an AI-powered broadcast analytics suite that delivers second-screen content such as win probability and player impact scores, solidifying its dual presence in commercial and media technology segments across Europe.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the European sports technology market secure official data partnerships with leagues and federations to ensure exclusivity and regulatory legitimacy. They invest in GDPR aligned cloud infrastructure to meet EU data residency and biometric consent requirements. Companies enhance product differentiation through explainable AI models for injury prediction and tactical analysis. Strategic collaborations with broadcasters and betting operators unlock dual revenue streams from performance and commercial applications. Additionally, they expand into grassroots and Olympic sports through public sector tenders, broadening market reach beyond elite clubs while building long-term data ecosystems.

MARKET SEGMENTATION

This research report on the europe sports technology market is segmented and sub-segmented into the following categories.

By Technology

- Wearable Technology

- Artificial Intelligence and Machine Learning

- Others

By Application

- Performance Enhancement

- Fan Experience and Engagement

- Others

By End User

- Sports Clubs

- Broadcasters and Media Companies

- Others

By Country

- United Kingdom

- Germany

- France

- Spain

- Italy

- Rest of Europe

Frequently Asked Questions

1. Which technologies are leading the revenue generation in the Europe Sports Technology Market?

Smart venues currently generate the highest revenue, while analytics and statistics technology is the fastest growing segment in the Europe Sports Technology Market.

2. Which European countries dominate the Sports Technology Market?

Germany, UK, France, and Spain are key players in the Europe Sports Technology Market, with Germany historically dominating and Spain showing the highest expected CAGR.

3. What are the main segments of the Europe Sports Technology Market?

The market segments include devices, smart venues, analytics & statistics, and esports within the Europe Sports Technology Market.

4. How is sports analytics impacting the Europe Sports Technology Market?

Sports analytics is a critical driver, enhancing player performance, reducing injury risks, and providing valuable data insights within the Europe Sports Technology Market.

5. What role does wearable technology play in the Europe Sports Technology Market?

Wearable devices are widely adopted to monitor athlete performance and health, playing a significant role in the Europe Sports Technology Market.

6. How is the Europe Sports Technology Market integrating AI and machine learning?

AI and ML are used for player analytics, injury prevention, fan engagement, and smart decision-making tools in the Europe Sports Technology Market.

7. What impact do smart stadium technologies have on the Europe Sports Technology Market?

Smart stadiums improve fan experiences, security, and operational efficiency, contributing substantially to the Europe Sports Technology Market growth.

8. How is eSports influencing the Europe Sports Technology Market?

eSports is an emerging and rapidly growing segment within the Europe Sports Technology Market, driven by increasing audience engagement and technology adoption.

9. Which companies are key players in the Europe Sports Technology Market?

Major players include Apple Inc., Cisco Systems, IBM, SAP SE, Microsoft, Genius Sports Ltd., and Sportradar Group AG.

10. What are the recent innovations in the Europe Sports Technology Market?

Innovations include integration of AR/VR for fan engagement, advanced data analytics, optical tracking, and video assistant referee technology across Europe.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com