Europe Telemedicine Market Size, Share, Trends & Growth Forecast Report By Technology, Service, Application, End User and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis from to 2025 to 2033

Europe Telemedicine Market Summary

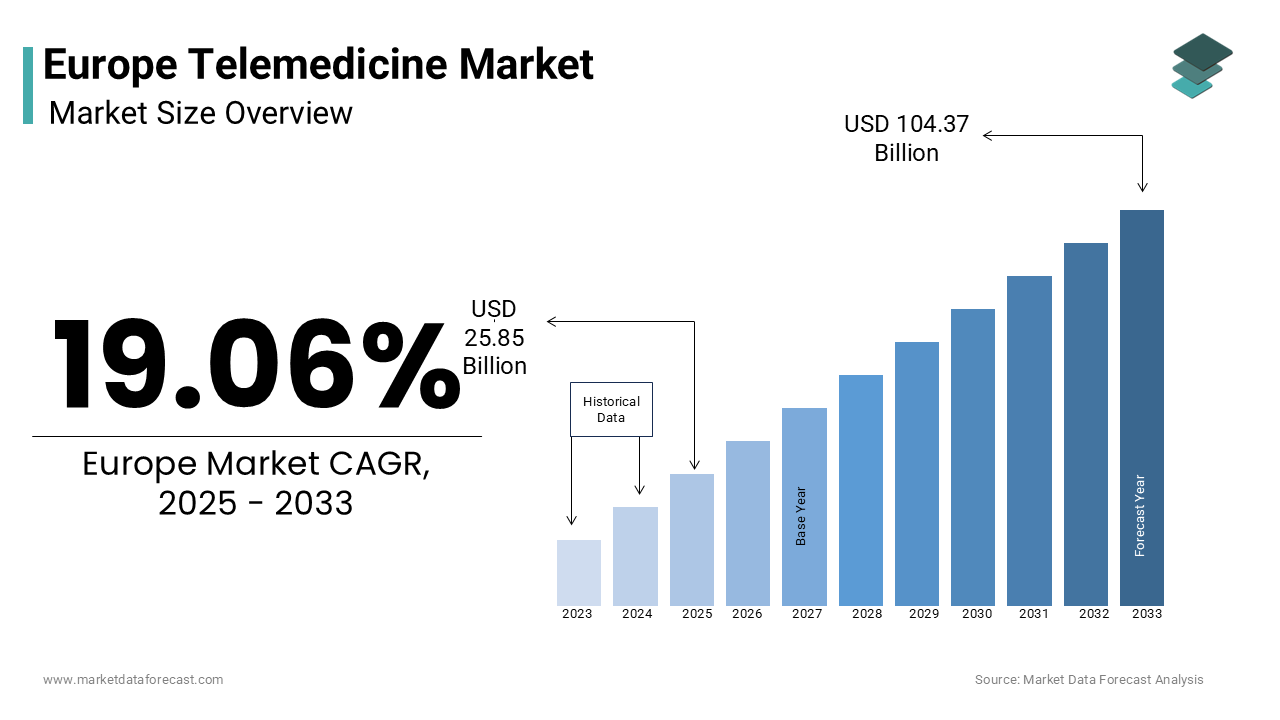

The European telemedicine market was valued at USD 21.71 billion in 2024 and is projected to grow to USD 25.85 billion in 2025 and further expand to USD 104.37 billion by 2033, registering a strong CAGR of 19.06% from 2025 to 2033. The growth of the European telemedicine market is driven by increasing adoption of digital healthcare solutions, growing demand for remote patient monitoring, and rising prevalence of chronic diseases. Supportive government initiatives, expanding broadband access, and the integration of cloud-based platforms are also accelerating the telemedicine industry across the region.

Key Market Trends

- Expansion of cloud-based telemedicine platforms offering secure and scalable healthcare delivery.

- Rising popularity of tele-cardiology and chronic disease management applications.

- Increasing investments in AI-powered diagnostics and digital health monitoring tools.

- Growing emphasis on cross-border healthcare access within the EU.

- Strategic partnerships between healthcare providers and technology companies.

Segmental Insights

- Based on type, the service segment dominated the European telemedicine market with a 60.1% share in 2024, supported by growing demand for virtual consultations and remote healthcare services.

- Based on application, the tele-cardiology segment led with a 25.4% share in 2024, reflecting high demand for cardiovascular monitoring and remote care solutions.

- Based on delivery mode, the cloud-based segment accounted for a significant share in 2024, driven by its scalability, security, and integration capabilities.

- Based on end users, the tele-hospitals segment held the leading share in 2024, highlighting strong adoption of digital health platforms in hospital networks.

Regional Insights

- Germany dominated the European telemedicine market in 2024, driven by advanced healthcare infrastructure, favorable regulatory support, and early adoption of digital health technologies.

- The UK is showing robust growth, supported by the NHS’s telehealth initiatives and expanding digital health startups.

- France is witnessing steady adoption, particularly in chronic disease management and elderly care.

- Italy and Spain are emerging markets, benefiting from growing digitalization in healthcare and supportive government investments.

- Other European countries are gradually expanding telemedicine adoption, especially in rural and underserved areas.

Competitive Landscape

Prominent companies in the European telemedicine market include AMD Global Telemedicine, CISCO Systems Inc., Medtronic Inc., GE Healthcare (UK), Honeywell Lifesciences, Philips Healthcare, McKesson Corp, Aerotel Medical Systems, CardioComm, and Cerner Corporation. These players are focusing on AI integration, telemonitoring solutions, and cross-border healthcare collaborations to strengthen their market presence.

Europe Telemedicine Market Size

The telemedicine market size in Europe was worth USD 21.71 billion in 2024 and is expected to reach USD 104.37 billion by 2033 from USD 25.85 billion in 2025, growing at a CAGR of 19.06% from 2025 to 2033.

Europe Telemedicine Market Overview

- The Europe telemedicine market has experienced exponential growth owing to the advancements in digital healthcare and the increasing need for remote medical services. This surge is attributed to the widespread adoption of telehealth technologies during the post-pandemic era, as patients and providers recognize its convenience and efficiency.

- Key cities like London, Berlin, and Paris have emerged as hubs for telemedicine innovation, supported by robust healthcare infrastructure and favorable regulatory frameworks.

- According to a study by McKinsey, 70% of European patients expressed satisfaction with telemedicine services, citing reduced travel time and improved access to specialists as key benefits. Additionally, government initiatives promoting digital health solutions have further amplified adoption by positioning Europe as a leader in telemedicine innovation globally.

MARKET DRIVERS

Rising Demand for Remote Healthcare

- The escalating demand for remote healthcare is a cornerstone driving the European telemedicine market.

- According to Deloitte, over 65% of European patients now prefer virtual consultations for non-emergency conditions by creating a fertile ground for telemedicine adoption. This trend is particularly evident in rural and underserved areas, where access to healthcare facilities remains limited.

- A key factor amplifying this growth is the aging population across Europe.

- As per Eurostat, the region’s elderly population (aged 65+) is projected to reach 30% of the total population by 2030 by necessitating scalable healthcare solutions.

- Telemedicine platforms offer cost-effective and convenient alternatives is enabling seniors to receive timely care without physical visits.

Integration of AI and IoT Technologies

- The integration of artificial intelligence (AI) and Internet of Things (IoT) technologies has significantly bolstered the European telemedicine market.

- According to Frost & Sullivan, AI-driven diagnostic tools accounted for 40% of telemedicine applications in 2023 by enabling accurate and real-time analysis of patient data.

- These innovations are particularly valuable in managing chronic conditions like diabetes and cardiovascular diseases.

- Additionally, IoT-enabled wearables have transformed patient monitoring is allowing continuous tracking of vital signs such as heart rate and blood pressure.

- A study by Accenture reveals that 50% of European healthcare providers adopted IoT devices in 2023 by improving early detection of health issues.

- These advancements not only enhance operational efficiency but also align with the EU’s Digital Health Strategy is fostering innovation and sustainability in healthcare delivery.

MARKET RESTRAINTS

Data Privacy Concerns

- Data privacy concerns pose a significant restraint for the Europe telemedicine market.

- According to a report by Kaspersky, cyberattacks targeting telehealth platforms increased by 35% in 2023 is raising fears about unauthorized access to sensitive patient information.

- These vulnerabilities stem from the decentralized nature of telemedicine systems, which rely on cloud storage and multiple access points.

- Moreover, stringent regulations like the General Data Protection Regulation (GDPR) have complicated compliance efforts for telemedicine providers.

- According to a study by Capgemini, 45% of European healthcare organizations cited GDPR compliance as a barrier to adopting telemedicine solutions.

- Addressing these concerns requires significant investments in advanced encryption technologies and threat detection systems, which may not be feasible for all stakeholders, impeding broader adoption.

Limited Reimbursement Policies

- Limited reimbursement policies represent another pressing challenge for the Europe telemedicine market.

- According to a report by Ernst & Young, only 30% of European countries have comprehensive insurance coverage for telemedicine services is creating financial barriers for patients and providers alike.

- For instance, a study by the European Health Insurance Card (EHIC) reveals that out-of-pocket expenses for teleconsultations deterred 25% of patients from utilizing these services in 2023.

- While some nations like Germany and France have introduced pilot programs to expand coverage, disparities persist across the region. These inconsistencies hinder equitable access to telemedicine is slowing market progress and limiting its potential impact on healthcare delivery.

MARKET OPPORTUNITIES

Expansion into Mental Health Services

- The expansion into mental health services presents a transformative opportunity for the Europe telemedicine market.

- According to a report by the World Health Organization (WHO), over 100 million Europeans suffer from mental health disorders, yet only 30% receive adequate treatment.

- Telemedicine platforms offer accessible and stigma-free solutions is bridging the gap between demand and supply.

- For example, a study by Mind reveals that teletherapy sessions grew by 50% in 2023 owing to the anonymity and convenience of virtual consultations.

- Additionally, partnerships with mental health organizations have enabled brands to introduce specialized programs, such as cognitive behavioral therapy (CBT) apps. These innovations not only attract new customers but also position telemedicine as a holistic healthcare solution.

Growth of mHealth Applications

- The rapid growth of mobile health (mHealth) applications offers another promising avenue for expansion in the Europe telemedicine market.

- For instance, a report by App Annie highlights that fitness and wellness apps accounted for 60% of total mHealth downloads, catering to younger demographics.

- Additionally, collaborations with wearable manufacturers have amplified functionality by enabling features like medication reminders and symptom tracking. These developments not only drive revenue but also reinforce telemedicine’s role in preventive healthcare.

MARKET CHALLENGES

Resistance to Technological Adoption

- Resistance to technological adoption among healthcare providers and patients represents a significant challenge for the Europe telemedicine market.

- Over 40% of European physicians expressed reluctance to adopt telemedicine due to concerns about technical proficiency and workflow disruptions.

- Additionally, older demographics remain skeptical about virtual consultations is preferring traditional in-person interactions.

- According to a report by Age UK, only 20% of seniors aged 70+ utilized telemedicine services in 2023 with the need for user-friendly interfaces and educational initiatives.

- Bridging this gap requires significant investments in training and awareness campaigns, which may

Fragmented Regulatory Frameworks

- Fragmented regulatory frameworks across European countries pose another pressing challenge for the telemedicine market.

- According to the European Federation of Pharmaceutical Industries and Associations (EFPIA), inconsistencies in licensing and approval processes have delayed the rollout of telehealth solutions in regions like Eastern Europe.

- For instance, a study by Deloitte reveals that cross-border telemedicine services face significant hurdles due to varying national standards and legal requirements.

- While the EU aims to harmonize regulations through initiatives like the European Health Data Space (EHDS), bureaucratic delays persist by complicating market entry for multinational providers.

SEGMENTAL ANALYSIS

By Type Insights

The service segment dominated the Europe telemedicine market and held 60.1% of the share in 2024.

- The growth of the services segment is driven by the growing demand for virtual consultations, remote monitoring, and diagnostic services among patients with chronic conditions.

- A key factor fueling this dominance is the cost-effectiveness of telemedicine services compared to traditional in-person care.

- According to McKinsey, virtual consultations reduced healthcare costs by 25% in 2023 by making them an attractive option for both providers and patients.

- Additionally, partnerships with insurance companies have expanded reimbursement coverage that further escalates the growth of the market.

- For instance, as per a study by PwC, over 70% of European insurers now offer telemedicine benefits by enhancing accessibility and affordability for patients.

- Another driving factor is the aging population across Europe.

- As per Eurostat, the region’s elderly population (aged 65+) is projected to reach 30% of the total population by 2030.

- Telemedicine services, such as remote monitoring and chronic disease management, cater specifically to this demographic by ensuring timely care without physical visits. These innovations not only improve patient outcomes but also alleviate pressure on healthcare facilities.

The technology segment is projected to grow with a CAGR of 18.2% during the forecast period.

- This growth is fueled by the increasing adoption of AI-driven diagnostic tools and IoT-enabled devices, which enhance patient monitoring and data collection.

- For example, a report by Accenture highlights that sales of smartwatches and fitness trackers grew by 40% in 2023 owing to their integration with telemedicine platforms.

- These devices enable real-time tracking of vital signs such as heart rate, blood pressure, and glucose levels by providing actionable insights for healthcare providers.

- Additionally, advancements in blockchain technology have improved data security and interoperability by addressing concerns about privacy and compliance with GDPR regulations. These innovations not only drive revenue but also position telemedicine as a cornerstone of modern healthcare delivery.

By Application Insights

The tele-cardiology segment was the largest in the European telemedicine market by capturing 25.4% of the share in 2024.

- The leading position of the tele-cardiology segment in the regional market is credited to the rising prevalence of cardiovascular diseases (CVDs), the need for scalable solutions to manage these conditions remotely and the high incidence of CVDs across Europe.

- According to the European Society of Cardiology, CVDs account for 45% of all deaths in the region, creating a critical demand for specialized telehealth services.

- Tele-cardiology platforms enable remote monitoring of heart conditions through wearable devices by reducing hospital readmissions by 30%, as reported by Philips Healthcare.

- Additionally, partnerships with hospitals and cardiology clinics have expanded access to diagnostic tools like ECG monitoring and echocardiography. Another driving factor is the integration of AI-driven analytics into tele-cardiology platforms.

- A study by Capgemini reveals that AI-powered tools improved diagnostic accuracy by 20% in 2023 by enabling early detection of heart abnormalities. These innovations not only enhance patient outcomes but also align with the EU’s push for preventive healthcare solutions.

The tele-dermatology segment is likely to have a prominent CAGR of 20.5% during the forecast period.

- This growing prevalence of skin conditions and the convenience of virtual consultations for dermatological care is propelling the growth of the tele-dermatology segment in the European market.

- For instance, a report by App Annie, downloads of dermatology-focused telemedicine apps grew by 50% in 2023, driven by features like photo-based diagnosis and personalized skincare plans. These platforms cater to younger demographics, who prioritize accessible and stigma-free solutions for managing conditions like acne and eczema.

- Additionally, collaborations with pharmacies and skincare brands have enabled seamless prescription deliveries by enhancing the overall patient experience. These developments not only drive adoption but also position tele-dermatology as a future-proof segment.

By Delivery Mode Insights

The cloud-based delivery segment was accounted in holding a prominent share of the Europe telemedicine market in 2024.

- The growth of the segment is attributed due to the scalability, flexibility, and ability to support real-time data sharing across multiple locations.

- A key factor fueling this dominance is the growing emphasis on interoperability and data accessibility.

- As per a study by PwC, 80% of European healthcare providers adopted cloud-based platforms in 2023 by enabling seamless integration with electronic health records (EHRs).

- Additionally, advancements in encryption technologies have addressed data privacy concerns, further solidifying the segment’s position as the largest in the market.

- For instance, a report by Kaspersky highlights that cloud-based systems reduced data breaches by 15% in 2023 by enhancing trust among patients and providers.

- The cost-effectiveness of cloud-based solutions is fuelling the expansion of the cloud-based segment in the European telemedicine market.

- According to Deloitte, healthcare institutions saved up to 40% on IT infrastructure costs by transitioning to cloud platforms by allowing them to allocate resources toward patient care.

- These innovations not only improve operational efficiency but also align with the EU’s Digital Health Strategy that is fostering innovation and sustainability.

The web-based delivery segment is the fastest-growing category, with a projected CAGR of 16.7% over the forecast period.

- This growth is fueled by the increasing demand for user-friendly and accessible telemedicine platforms among small clinics and independent practitioners. These platforms require minimal setup and maintenance by making them ideal for smaller healthcare providers with limited IT resources.

- Additionally, partnerships with local health authorities have expanded access to underserved regions is ensuring equitable healthcare delivery. These factors collectively propel the segment’s rapid expansion.

By End-Users Insights

The tele-hospitals segment dominated the Europe telemedicine market share in 2024.

- The growth of this segment is attributed to be driven by the growing need for scalable healthcare solutions in hospital settings for managing chronic conditions and emergency care and increasing burden on hospital infrastructure.

- According to Eurostat, hospital overcrowding remains a persistent issue, with occupancy rates exceeding 90% in major cities like London and Berlin.

- Tele-hospital platforms enable remote consultations and diagnostics by reducing the strain on physical facilities.

- For instance, a study by Philips Healthcare reveals that tele-hospital solutions reduced emergency room wait times by 25% in 2023 is improving patient satisfaction and outcomes.

- Another driving factor is the integration of advanced technologies like AI and IoT into hospital workflows.

- According to a report by Accenture, 60% of European hospitals adopted AI-driven diagnostic tools in 2023 by enhancing operational efficiency and accuracy.

- These innovations not only streamline processes but also align with the EU’s push for digital transformation in healthcare.

The tele-homes segment is likely to grow with a CAGR of 19.3% during the forecast period.

- This growth is fueled by the increasing preference for home-based healthcare solutions among elderly and chronically ill patients.

- According to a study by Mind, telehome services grew by 45% in 2023 is driven by features like remote monitoring and virtual consultations.

- These platforms cater to seniors by enabling them to receive timely care without physical visits. Additionally, government subsidies supporting home healthcare have amplified adoption by positioning tele-homes as a future-proof segment. These factors collectively propel the segment’s rapid expansion.

REGIONAL ANALYSIS

Germany is dominating the telemedicine market in Europe.

Germany was the top performer in the European telemedicine market with a 22.3% share in 2024. The country’s growth is driven by its robust healthcare infrastructure and favorable regulatory frameworks, supported by initiatives like the Digital Healthcare Act (DVG). A pivotal factor fueling this dominance is the widespread adoption of telemedicine in rural areas. According to Eurostat, teleconsultations reduced travel time for patients in underserved regions by 30% in 2023.

The UK is expected to register healthy growth in the European telemedicine market in the coming years.

The UK telemedicine market is estimated to have a CAGR of 9.7% during the forecast period. London and Manchester have emerged as critical hubs, supported by robust investments in digital health technologies. The rise of mHealth applications has significantly bolstered demand. According to App Annie, downloads of telemedicine apps in the UK grew by 50% in 2023, driven by features like virtual GP consultations and prescription deliveries. Additionally, partnerships with private insurers have expanded reimbursement options, further enhancing accessibility.

France is a noteworthy location in the European telemedicine market.

The French telemedicine market is likely to hold prominent growth opportunities throughout the forecast period. Paris has emerged as a key player by hosting major telehealth startups and innovation hubs. A major driver of this growth is the integration of AI-driven diagnostic tools. As per a study by Capgemini, 60% of French healthcare providers adopted AI-powered platforms in 2023 is improving diagnostic accuracy and efficiency. Additionally, government initiatives promoting telemedicine reimbursement have accelerated adoption by positioning France as a leader in digital healthcare.

COMPETITIVE LANDSCAPE

Key Market Players

A few of the prominent companies playing an active role in the European telemedicine market include AMD Global Telemedicine, CISCO Systems, Inc., Medtronic, Inc., GE Healthcare (U.K.), Honeywell Lifesciences, Philips Healthcare, McKesson Corp, Aerotel Medical Systems, CardioComm, and Cerner Corporation.

The Europe telemedicine market is characterized by intense competition, driven by the presence of global giants and regional innovators vying for market share. Major players like Teladoc Health, Babylon Health, and KRY International dominate the landscape, leveraging their extensive expertise in digital healthcare solutions. However, the market also features niche players specializing in mental health and chronic disease management, creating a fragmented yet dynamic ecosystem.

Technological innovation is a key battleground, with companies investing heavily in AI, IoT, and blockchain to differentiate themselves. According to McKinsey, over 60% of European enterprises prioritize secure and scalable telemedicine solutions, intensifying competition among providers to offer cutting-edge technologies. Additionally, stringent EU regulations mandating data privacy have forced companies to innovate responsibly, further raising the stakes.

Mergers and acquisitions are another hallmark of the competitive landscape. Larger firms acquire smaller innovators to expand their product portfolios and geographic reach. Meanwhile, price wars and aggressive marketing strategies are common in saturated markets like Germany and the UK. Despite these challenges, the market remains ripe for growth, with opportunities in emerging segments such as mental health and mHealth driving future competition.

Strategies Used by Key Market Participants

- Strategic Partnerships: Leading players in the Europe telemedicine market have embraced strategic partnerships to expand their reach and enhance service offerings. For instance, collaborations with insurance providers enable companies to offer comprehensive reimbursement options, fostering broader adoption. These alliances not only foster innovation but also ensure compliance with EU regulations by strengthening their competitive edge.

- Investment in R&D: Investments in research and development are a cornerstone strategy for staying ahead in the market. Companies are focusing on developing AI-driven diagnostic tools and IoT-enabled devices that cater to evolving patient needs. This approach allows them to address challenges such as interoperability and scalability while maintaining its dominance in technological advancements.

- Geographic Expansion: Expanding into emerging markets within Europe, such as Eastern Europe and Scandinavia, has become a priority for key players. By establishing localized services and partnerships, companies can better serve regional demands while capitalizing on favorable regulatory frameworks. This strategy ensures sustained growth amid intensifying competition.

Telemedicine Market News

- In March 2024, Teladoc Health partnered with NHS Scotland to expand its virtual care services in rural areas. This initiative aims to enhance accessibility and reduce hospital overcrowding.

- In June 2023, Babylon Health launched an AI-driven mental health platform in France, designed to provide personalized therapy sessions. This move underscores the company’s commitment to addressing mental health challenges.

- In September 2023, KRY International introduced a multilingual telemedicine app in Switzerland, targeting expatriates and cross-border workers. This launch seeks to capitalize on the growing demand for accessible healthcare solutions.

- In January 2024, Philips Healthcare acquired a Dutch startup specializing in IoT-enabled wearables, enhancing its remote monitoring capabilities. This acquisition strengthens Philips’ position in the telemedicine market.

- In November 2023, Siemens Healthineers unveiled its cloud-based telemedicine platform in Germany, designed to support real-time data sharing between hospitals. This initiative positions Siemens as a leader in interoperable healthcare solutions.

EUROPE TELEMEDICINE MARKET REPORT SCOPE

| Metric | Value |

|---|---|

| Base Year | 2024 |

| Market Size Available | 2024 to 2033 |

| Forecast Period | 2025 to 2033 |

| Market Size in 2024 | USD 21.71 billion |

| Projected Market Size in 2025 | USD 25.85 billion |

| Projected Market Size by 2033 | USD 104.37 billion |

| Projected CAGR | 19.06 |

| Quantitative Units | Market Size in USD Billion and CAGR from 2025 to 2033 |

| Various Analyses Included | Regional & Country-Level Analysis; Segment-Level Analysis; DROC; PESTLE; Porter's Five Forces; Competitive Landscape; Investment Opportunities |

| Segments Covered | Type, Application, End-User and Country |

| Key Market Players Covered | AMD Global Telemedicine, CISCO Systems, Inc., Medtronic, Inc., GE Healthcare (U.K.), Honeywell Lifesciences, Philips Healthcare, McKesson Corp, Aerotel Medical Systems, CardioComm, and Cerner Corporation. |

| Regions Analyzed | Europe |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest Of Europe |

| Report Format | PDF, Excel, PPT, BI |

| Customization | Report customization as per your requirements with respect to countries, region and segmentation. |

MARKET SEGMENTATION

This research report on the Europe telemedicine market is segmented and sub-segmented based on type, application, delivery mode, end-users and region.

By Type

- Technology

- Hardware

- Software

- Telecommunications

- Service

- Remote Patient Monitoring

- Store-and-Forward

- Real-Time Interactive

By Application

- Tele-Cardiology

- Tele-Radiology

- Tele-Pathology

- Tele-Dermatology

- Tele-Neurology

- Emergency Care

- Home Health

- Others

By Delivery Mode

- Web-Based

- Cloud-Based

- Others

By End-Users

- Tele-Hospitals

- Tele-Homes

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the Europe Telemedicine Market?

The Europe Telemedicine Market refers to the industry that provides remote healthcare services through digital technologies such as video conferencing, mobile apps, and remote monitoring tools across European countries.

What is driving the growth of telemedicine in Europe?

Growth is driven by increased adoption of digital health post-COVID, aging populations, high rates of chronic diseases, healthcare workforce shortages, and favorable regulatory reforms.

Which countries lead the telemedicine adoption in Europe?

Germany, the United Kingdom, France, the Netherlands, and Sweden are among the leading adopters due to well-developed digital infrastructure and supportive national healthcare policies.

What are the main applications of telemedicine in Europe?

Key applications include teleconsultation, telepsychiatry, teleradiology, telecardiology, and remote patient monitoring, serving both urban and rural populations.

How is the regulatory environment shaping the market?

EU data privacy laws (GDPR), national licensing frameworks, and reimbursement policies vary by country but increasingly support cross-border and insurance-covered telemedicine services.

What is the projected size of the Europe Telemedicine Market by 2033?

The European telemedicine market is expected to exceed USD 104.3 billion by 2033, fueled by sustained demand and healthcare digitalization efforts.

Who are the major players in the European telemedicine market?

Leading providers include HealthHero, Doctolib, KRY (Livi), Siemens Healthineers, Philips, and TeleClinic, alongside global players expanding regionally.

What technologies are enabling telemedicine in Europe?

Technologies include AI-driven diagnostics, IoT health devices, electronic health records (EHRs), cloud platforms, and 5G connectivity for real-time data sharing.

What challenges does the Europe Telemedicine Market face?

Key challenges include fragmented regulations, unequal access in rural areas, limited digital literacy among elderly populations, and lack of integration with traditional care systems.

What are the emerging trends in this market?

Emerging trends include tele-rehabilitation, mental health apps, virtual care platforms for chronic disease management, and interoperability between EU healthcare systems.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com