Europe Ultrafiltration Market Size, Share, Trends & Growth Forecast Report, Segmented By Membrane Type (Polymeric Membranes, Ceramic Membranes, Metallic And Other Inorganic Membranes), Application, End User Industry, And Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest Of Europe) - Industry Analysis From (2026 To 2034)

Market Size, 2025

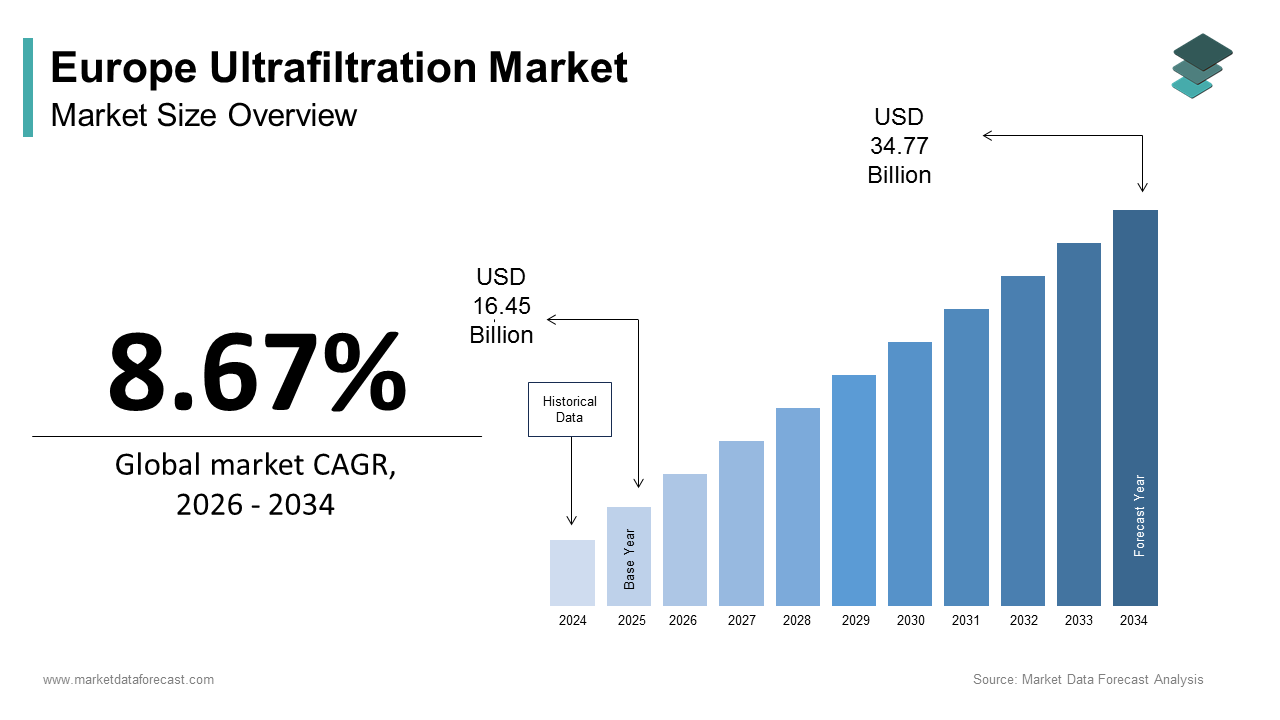

$16.45 BnMarket Estimate, 2026

$17.88 BnMarket Forecast, 2034

$34.77 BnCAGR, 2026–2034

8.67%Europe Ultrafiltration Market Report Summary

The Europe ultrafiltration market was valued at USD 16.45 billion in 2025 and is projected to reach USD 34.77 billion by 2034, growing from USD 17.88 billion in 2026 at a CAGR of 8.67% during the forecast period. Market growth is driven by increasing demand for advanced water and wastewater treatment solutions, strict European regulations on water quality, and rising investments in sustainable municipal infrastructure. The growing adoption of membrane-based filtration technologies across municipal and industrial applications is further supporting market expansion. Continuous technological advancements in polymeric membranes, along with rising emphasis on water reuse and recycling, are strengthening the long-term growth outlook of the Europe ultrafiltration market.

Key Market Trends

- Increasing adoption of ultrafiltration systems in municipal water and wastewater treatment to comply with stringent EU environmental standards

- Rising preference for polymeric membranes due to their cost-effectiveness, durability, and high filtration efficiency

- Growing investments in decentralized water treatment and water reuse projects across urban regions

- Ongoing technological innovations aimed at improving fouling resistance, energy efficiency, and membrane lifespan

- Expanding use of ultrafiltration across industrial sectors such as food and beverage, pharmaceuticals, and chemicals

Segmental Insights

- Based on membrane type, the polymeric membranes segment held the largest share of the Europe ultrafiltration market in 2024, supported by wide applicability, ease of installation, and lower operating costs.

- Based on application, the water and wastewater treatment segment dominated the market in 2024, driven by increasing urbanization, aging water infrastructure, and rising focus on water reuse.

- Based on the end-user industry, the municipal segment captured a significant share in 2024 due to large-scale public investments in drinking water purification and wastewater management systems.

Regional Insights

- Germany led the Europe ultrafiltration market by accounting for 24.6% of the total market share in 2024

- Market growth in Germany is supported by advanced water infrastructure, high environmental compliance standards, and strong adoption of membrane filtration technology.s

- Other Western European countries are experiencing steady growth due to increasing emphasis on sustainable water management and industrial wastewater treatment.nt

Competitive Landscape

The Europe ultrafiltration market is moderately consolidated, with leading companies focusing on technological innovation, strategic partnerships, and expansion of advanced membrane portfolios. Market participants are strengthening their presence through long-term service contracts and customized filtration solutions for municipal and industrial customers.

Prominent players in the Europe ultrafiltration market include SUEZ, Veolia, DuPont Water Solutions, Pentair, Toray Industries, Koch Separation Solutions, Alfa Laval, Merck Millipore, Asahi Kasei, Pall Corporation, Nitto Denko Corporation, 3M, Lanxess, and Synder Filtration.

Europe Ultrafiltration Market Size

The Europe ultrafiltration market size was calculated to be USD 16.45 billion in 2025 and is anticipated to be worth USD 34.77 billion by 2034, growing from USD 17.88 billion in 2026 at a CAGR of 8.67% during the forecast period.

Ultrafiltration refers to a pressure-driven membrane separation process that removes suspended solids, bacteria, viruses, and macromolecules from water and industrial process streams using semipermeable membranes with pore sizes typically between 0.01 and 0.1 micrometers. The technology is widely deployed across municipal drinking water treatment, industrial process purification, and wastewater reuse applications due to its ability to deliver high-quality permeate without chemical additives. The European market is shaped by stringent water quality directives, including the EU Drinking Water Directive, which mandates microbiological safety standards that ultrafiltration reliably meets. Western European municipalities are increasingly adopting advanced membrane filtration technologies to combat emerging contaminants and modernize infrastructure. EU Circular Economy initiatives are driving industrial sectors to significantly reduce water abstraction and increase water reuse, particularly in food and beverage and pharmaceutical manufacturing. Ultrafiltration is no longer just a niche step; it is now a pillar of European water sustainability, essential for managing the millions of cubic meters of wastewater reclaimed daily for non-potable use.

MARKET DRIVERS

Stringent EU Drinking Water and Wastewater Reuse Regulations Driving Municipal Adoption

Binding EU legislation that mandates pathogen removal and water reuse standards unattainable through conventional treatment alone drives the growth of the Europe ultrafiltration market. Regulatory updates across the region are placing increased emphasis on removing specific bacterial indicators in drinking water quality, highlighting the role of physical barrier technologies. Ultrafiltration is recognized for its ability to reduce bacterial and viral loads while minimizing disinfection byproduct formation. The use of membrane filtration in water treatment facilities is becoming more widespread. New, more stringent quality standards for agricultural irrigation water are prompting greater reliance on advanced filtration technologies to manage turbidity and microbial safety. Large-scale initiatives for reusing treated water in agricultural settings are utilizing membrane technologies to meet these updated quality requirements. Rising urban populations and intensifying drought conditions have reclassified ultrafiltration from a luxury to a necessity for water security and public health.

Expansion of Ultrafiltration in Food and Beverage Processing for Product Clarification and Sterility

The food and beverage sector is a major growth engine for the Europe ultrafiltration market. This is propelled by demand for clean-label products, microbial stability, and process efficiency. Dairy producers use ultrafiltration to concentrate proteins in milk for cheese and yogurt manufacturing while removing lactose and minerals, a process that increases yield. Ultrafiltration is increasingly used in large-scale cheese production facilities across France and Germany to maintain consistent milk composition throughout the year, minimizing the impact of seasonal variations on the final product. Similarly, the wine and juice industries adopt ultrafiltration to replace diatomaceous earth filtration, eliminating silicate residues and achieving brilliant clarity without preservatives. Driven by strong consumer demand for products free from artificial additives, the adoption of ultrafiltration technology within the European fruit juice processing industry has seen significant growth in recent times. The technology also enables cold sterilization of heat-sensitive beverages like craft beer and plant-based milk, preserving flavour and nutrients. In alignment with the EU’s Farm to Fork Strategy, ultrafiltration is gaining traction across the food sector as a sustainable alternative to traditional heat and chemical processing.

MARKET RESTRAINTS

High Capital and Operational Expenditure Limiting Adoption in Small and Medium Facilities

The high upfront and recurring costs associated with membrane system deployment, particularly for small municipalities and mid-sized industrial users, restrict the expansion of the Europe ultrafiltration market. Installing municipal ultrafiltration technology for mid-sized communities requires substantial capital investment, while maintenance and energy usage represent a significant, ongoing annual expenditure for utilities. For industrial users like small dairies or breweries, the payback period often exceeds five years, deterring adoption despite long-term savings. Energy consumption remains a concern. The high energy intensity of advanced membrane treatment, combined with elevated energy prices in Europe, creates substantial operational costs for wastewater treatment facilities. Furthermore, membrane fouling necessitates frequent chemical cleaning with citric acid or sodium hypochlorite, increasing both operational complexity and waste disposal costs. EU funding, such as Horizon Europe, offers grants but rarely covers significant project costs, leaving SMEs reliant on traditional solutions despite pressure to modernize.

Membrane Fouling and Limited Lifespan Increasing Total Cost of Ownership

Persistent membrane fouling hinders the growth of the Europe ultrafiltration market. This fouling reduces flux efficiency, increases energy demand, and shortens membrane lifespan to several years. Fouling occurs due to organic colloidal or biological matter in feedwater, forming irreversible layers that cannot be fully removed by backwashing. In industrial applications such as biopharmaceutical processing, protein adsorption causes rapid performance decline, requiring costly cleaning protocols with enzymatic detergents. Pre-treatment with coagulation or microfiltration can mitigate fouling but adds capital expense and chemical handling complexity. Additionally, the EU’s Industrial Emissions Directive restricts the discharge of cleaning chemicals like chlorine-based agents, forcing operators to adopt more expensive, eco-friendly alternatives. These operational realities undermine the technology’s economic appeal despite its technical superiority and constrain widespread deployment, particularly in regions with variable or high contaminant feedwater quality.

MARKET OPPORTUNITIES

Integration of Ultrafiltration in Industrial Water Reuse Under the EU Green Deal

The European Green Deal’s Industrial Emissions Directive and Circular Economy Action Plan offer a major opportunity for the Europe ultrafiltration market. These initiatives drive the technology by mandating water reuse and pollution prevention across manufacturing sectors. The EU strategy targets a reduction in industrial freshwater use by 2030, requiring companies to implement closed-loop water systems where ultrafiltration serves as a critical pre-treatment step before reverse osmosis or evaporation. Many industrial sites in Europe, especially in the chemical, textile, and metal finishing sectors, are committing to sustainable water management programs. These industries are increasingly using ultrafiltration technology to enable the safe recycling of process water streams. This trend indicates a movement toward more circular water usage within the European industrial sector. Similarly, automotive plants in Germany employ ultrafiltration to treat paint booth wastewater for reuse in scrubbers. Ultrafiltration has shifted from a voluntary treatment option to a mandatory operational requirement, driven by stricter European regulations and water scarcity.

Adoption of Hybrid Ultrafiltration Systems with Advanced Oxidation for Emerging Contaminants

The region’s growing concern over pharmaceuticals, microplastics, and per- and polyfluoroalkyl substances in water supplies is driving innovation in hybrid ultrafiltration systems combined with advanced oxidation processes. This is expected to boost the growth of the Europe ultrafiltration market. Ultrafiltration is excellent at removing suspended solids and bacteria, but requires tandem treatments such as ozonation or UV to tackle dissolved organic matter. Pilot studies in specific European regions indicate that combining ultrafiltration with UV advanced oxidation processes effectively lowers the presence of certain pharmaceutical compounds, such as diclofenac and carbamazepine. This treatment approach has shown potential in reducing targeted substance concentrations to levels consistent with established monitoring benchmarks. Municipal wastewater facilities, including those managing hospital effluents, have begun implementing this combined treatment system to address trace antibiotics. These hybrid configurations are gaining traction in sensitive catchments and drinking water sources where regulatory scrutiny is intensifying. The European Commission’s Zero Pollution Action Plan explicitly encourages integrated treatment trains for emerging contaminants, creating a policy tailwind for advanced ultrafiltration applications. Advancements in analytical capability and lower detection limits will make these technologies standard in Europe’s next-generation water systems.

MARKET CHALLENGES

Fragmented Regulatory Frameworks Across Member States Delaying Standardization

National rule variations that clash with EU directives are plaguing the Europe ultrafiltration market. This is causing uncertainty and delayed project approvals. While the Drinking Water Directive sets health-based targets, each member state defines its own monitoring frequency, pre-treatment requirements, and acceptable membrane integrity testing protocols. According to sources, operators in Southern Europe face more stringent turbidity limits than those in Northern Europe, leading to inconsistent system designs. Additionally, permitting for industrial wastewater reuse varies widely. Spain allows agricultural reuse with minimal oversight, while Germany requires multiple barriers, including ultrafiltration and disinfection, even for non-food crops. This regulatory fragmentation increases engineering complexity and discourages standardized modular ultrafiltration solutions that could reduce costs. Regional, standardized regulations are required to prevent patchy ultrafiltration implementation and inconsistent project scheduling.g

Limited Skilled Workforce for Membrane System Operation and Maintenance

A shortage of technicians and engineers trained in membrane process optimization, particularly in rural and Eastern European regions, holds back the growth of the Europe ultrafiltration market. European water authorities are facing a growing demand for qualified specialists to meet new sustainability goals, leading to a substantial talent shortage in the sector. Ultrafiltration systems require daily monitoring of transmembrane pressure flux rates and fouling indicators as well as periodic chemical cleaning and integrity testing, tasks beyond the scope of traditional plant operators. Many smaller municipal treatment plants in Germany are increasingly outsourcing specialized membrane maintenance tasks because they lack the necessary in-house expertise. Vocational training programs have been slow to incorporate membrane technology. Certified training for advanced membrane technology remains limited in scope across the European Union, with only a minority of member states offering such specialized vocational education. This human capital gap undermines system reliability and deters investment in advanced water treatment despite regulatory and environmental imperatives to upgrade.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 8.67% |

| Segments Covered | By Membrane Type, Application, End User Industry, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | SUEZ, Veolia, DuPont Water Solutions, Pentair, Toray Industries, Koch Separation Solutions, Alfa Laval, Merck Millipore, Asahi Kasei, Pall Corporation, Nitto Denko Corporation, 3M, Lanxess, Synder Filtration |

SEGMENTAL ANALYSIS

By Membrane Type Insights

The polymeric membranes segment held the largest share of the Europe ultrafiltration market in 2024. The dominance of the polymeric membranes segment is driven by their cost efficiency, ease of manufacturing, and broad compatibility with municipal and industrial feedwaters. Materials like polyethersulfone (PES) and polyvinylidene fluoride (PVDF) dominate due to their chemical resistance, thermal stability, and tunable pore structures. Polyvinylidene fluoride (PVDF) hollow fiber modules are heavily utilized in large-scale drinking water treatment across Western Europe due to their durability and efficiency, making them a standard material in advanced water purification. The technology’s affordability is critical for public utilities operating under tight budgets. A standard polymeric ultrafiltration system costs less than ceramic alternatives. Furthermore, polymeric membranes integrate seamlessly with existing pretreatment infrastructure such as sand filters and cartridge systems, minimizing retrofitting expenses. Driven by updated regulatory directives targeting micropollutants and stricter environmental standards, European municipal wastewater plants are experiencing rapid modernization, with numerous facilities upgrading to membrane filtration technology. Polymeric ultrafiltration remains the default choice for scalable, reliable, and economically viable water purification across the continent.

The ceramic ultrafiltration membranes segment is on the rise and is expected to be the fastest-growing segment in the market by witnessing a CAGR of 12.4% from 2025 to 2033 due to demand in high fouling industrial applications, where polymeric membranes degrade rapidly. Ceramic membranes, made from alumina zirconia or titania, offer exceptional chemical, thermal, and mechanical stability, enabling operation in extreme pH temperatures up to 100 degrees Celsius and aggressive cleaning cycles. The dairy industry has shown an increasing interest in advanced membrane technologies for processing whey, with ceramic ultrafiltration gaining some adoption in parts of Europe. This shift is generally driven by the recognition that ceramic membranes can offer improved resistance to protein fouling and a longer operational lifespan compared to many traditional organic membrane systems. Similarly, the pharmaceutical industry prefers ceramics for sterile filtration of heat-sensitive biologics, where extractables from polymers pose contamination risks. The European Commission’s Industrial Emissions Directive incentivizes durable technologies by linking environmental permits to lifecycle performance. Though initial costs remain higher than polymeric systems, declining manufacturing costs and rising demand for zero liquid discharge are driving ceramic adoption beyond niche applications into mainstream industrial water reuse.

By Application Insights

The water and wastewater treatment segment led the Europe ultrafiltration market by accounting for a substantial share in 2024. The supremacy of the water and wastewater treatment segment is underpinned by binding EU directives on drinking water safety and wastewater reuse. Regulations for public drinking water supply now place a stronger emphasis on ensuring the absence of pathogenic microorganisms. Membrane filtration technology is increasingly recognized as an effective method for achieving high-standard water quality in public supplies. The adoption of membrane filtration technology for drinking water has expanded across various European regions and urban systems. New regulations for agricultural water reuse are tightening requirements for turbidity and bacterial levels, encouraging the use of advanced filtration methods. Certain regions are demonstrating leadership in implementing treated wastewater reuse for agricultural purposes. Aging infrastructure also drives upgrades. Rising drought frequency necessitates the use of ultrafiltration to ensure reliable, high-quality water, especially for securing water sources.

The microelectronics segment is expected to exhibit a noteworthy CAGR of 10.8% during the forecast period, owing to the semiconductor industry’s escalating demand for ultrapure water with particle counts below 1 per milliliter and total organic carbon under 1 part per billion. Semiconductor manufacturing necessitates substantial daily quantities of high-purity water, where ultrafiltration commonly serves as a crucial pre-treatment stage for additional purification. Growing investment in domestic manufacturing initiatives is encouraging the development of new semiconductor production sites, consequently increasing the need for water-dependent manufacturing abilities. More recent or expanded production sites are integrating advanced, multi-stage water purification technologies to comply with strict cleanroom requirements. The growth in production capacity underscores the continuous requirement for sturdy, dependable, and extensive water treatment infrastructure within the semiconductor sector. Additionally, EU regulations like REACH restrict chemical contaminants in process water, forcing fabs to adopt physical removal methods. Europe's push for chip independence makes ultrafiltration essential, shifting it from a secondary to a core technology in high-tech water systems, as the continent builds its semiconductor industry.

By End User Industry Insights

The municipal segment dominated the Europe ultrafiltration market by capturing a significant share in 2024. The prominence of the municipal segment is credited to regulatory mandates, public health imperatives, and infrastructure modernization programs. EU directives require continuous monitoring of microbiological parameters, with ultrafiltration providing a fail-safe physical barrier against Cryptosporidium and Giardia that conventional treatment cannot reliably remove. European water utilities are increasingly adopting advanced membrane technologies like ultrafiltration for new drinking water treatment projects to meet rising water quality demands. National programs further accelerate adoption. The German government, under its National Water Strategy, is significantly increasing financial support for municipal water infrastructure, focusing on upgrading wastewater treatment plants to handle micropollutants and improving overall efficiency. Additionally, urban population growth strains existing systems. A significant portion of Europe's urban population resides in areas facing water scarcity, placing pressure on water resource management to adapt to climate change and rising demand. Ultrafiltration has emerged as the foundational technology for Europe’s future municipal water security, particularly as public utilities focus on reliability mandates and sustained operational performance.

The industrial end-user segment is predicted to witness the highest CAGR of 11.6% from 2025 to 2033. The swift growth of the industrial end-user segment is propelled by the EU Green Deal’s Circular Economy Action Plan, which mandates a reduction in industrial freshwater abstraction by 2030. Industries like food and beverage, pharmaceuticals, and chemicals are adopting ultrafiltration to reclaim process water and reduce discharge volumes. Industrial sites are increasingly adopting water sustainability commitments, with filtration technologies facilitating high levels of water recovery in specialized applications. The use of membrane filtration is becoming a common practice for concentrating proteins in the food manufacturing sector. Facilities are utilizing membrane technology to treat byproduct streams, allowing for the reuse of water within cleaning processes. Water management strategies in the biotech and dairy sectors are shifting toward increased resource recovery. Additionally, the Industrial Emissions Directive imposes stricter limits on organic pollutants in effluents, making physical separation via ultrafiltration more viable than chemical treatment. Industrial ultrafiltration has transitioned from a mere cost factor to a strategic driver of environmental compliance and resource optimization as sustainability becomes critical to business continuity.

REGIONAL ANALYSIS

Germany Ultrafiltration Market Analysis

Germany outperformed other regions in the Europe ultrafiltration market by accounting for a 24.6% share in 2024. The dominance of the German market is driven by its rigorous water quality standards and advanced industrial base. The country’s Federal Environment Agency enforces some of the strictest drinking water regulations in Europe, requiring continuous integrity testing of membrane systems in all plants serving thousands of people. A significant majority of large municipal wastewater treatment facilities in the country have adopted ultrafiltration technology, with certain major cities reaching full implementation of this process. Industrial water demand is influenced by the chemical and automotive sectors, with specific industrial sites utilizing ultrafiltration to recycle process water for operational reuse. Governmental support is directed towards funding research and pilot projects aimed at implementing hybrid membrane systems for treating emerging contaminants. Germany leads Europe in ultrafiltration deployment, driven by its advanced engineering, strict environmental rules, and intricate urban infrastructure.

France Ultrafiltration Market Analysis

France followed closely in the Europe ultrafiltration market by capturing a share of 16.1% in 2024. The growth of the French market is fuelled by its national strategy for treated wastewater reuse in agriculture. Regulatory trends indicate a move towards mandatory, large-scale implementation of treated wastewater reuse for irrigation in large population areas. Ultrafiltration is becoming a prioritized technology for producing high-quality irrigation water. Water management strategies in agricultural areas are increasingly using treated wastewater reuse to secure supplies for high-value crops. Large urban wastewater treatment plants are adding significant filtration streams to facilitate safe, large-scale reuse. The food processing industry is widely adopting membrane technology to enhance product standardization and process efficiency. France is bridging the gap between urban wastewater and rural resilience via ultrafiltration, addressing intensifying droughts and rising agricultural demand in Southern Europe.

Netherlands Ultrafiltration Market Analysis

The Netherlands continues to be a major player in the Europe ultrafiltration market and functions as a global hub for membrane technology development and export. Home to leading companies like Pentair and NX Filtration, the country hosts Europe’s most advanced ceramic and polymeric membrane R&D facilities. The drinking water supply for Amsterdam relies on natural dune filtration, supplemented by advanced treatment processes, rather than a majority share originating from ultrafiltration. The Netherlands also pioneers industrial applications. The Geleen chemical site is implementing initiatives to enhance circularity and increase the recovery of process water. Dutch engineering firms export turnkey ultrafiltration systems to numerous countries, leveraging EU regulatory experience as a quality benchmark. The Dutch ecosystem, strong in PPPs and skilled English speakers, drives innovation in membrane tech, making the nation a key R&D hub that boosts Europe's global presence in ultrafiltration.

Spain Ultrafiltration Market Analysis

Spain experienced a consistent growth in the Europe ultrafiltration market. It leads Europe in wastewater reuse due to chronic water scarcity and progressive regulatory frameworks. Treated wastewater is increasingly utilized for agricultural irrigation, with a significant portion of the European Union's total reuse occurring in one specific country. Ultrafiltration technology is frequently utilized as a core component in major water reclamation projects to support agricultural needs. Agricultural areas, particularly those cultivating rice and citrus, are expanding their water treatment capabilities to comply with environmental regulations regarding nutrient management. Municipalities are upgrading water treatment facilities with advanced filtration to secure water supplies during periods of prolonged drought. The adoption of advanced water treatment infrastructure is accelerating in response to water scarcity affecting large parts of the country. Spain views ultrafiltration as critical infrastructure, a necessity, not a choice, due to climate models forecasting reduced rainfall by 2050.

Italy Ultrafiltration Market Analysis

Italy is likely to expand in the Europe ultrafiltration market from 2025 to 2033, owing to its world-renowned food and beverage industry’s demand for product quality and process efficiency. Many producers of traditional Italian hard cheeses are adopting ultrafiltration techniques to concentrate milk proteins, which enhances cheese yield and improves waste management efficiency. Winemakers in specific Italian regions are increasingly using ultrafiltration to achieve high product clarity and align with trends emphasizing fewer additives. Municipalities in drought-prone areas of Italy are investing in large-scale ultrafiltration infrastructure to secure water supplies during periods of shortage. Increasing water stress across Italian territory is accelerating investment in advanced treatment technologies. Italy's agri-food sector merges rich artisanal heritage with eco-conscious goals, using ultrafiltration to cut waste and boost efficiency while safeguarding traditional quality.

COMPETITION OVERVIEW

Competition in the Europe ultrafiltration market is shaped by a dual dynamic: large integrated water utilities like Suez and Veolia dominate municipal contracts through turnkey plant delivery and long-term operation agreements, while specialized membrane manufacturers such as Pentair NX Filtration and Alfa Laval compete on technology differentiation in industrial niches. The market is further segmented by material, with polymeric membranes leading in volume due to cost, but ceramic membranes gain share in high-value applications demanding durability and chemical resistance. Regulatory pressure from the EU Drinking Water and Wastewater Reuse Directives creates a baseline demand that all players must address, but differentiation arises through energy efficiency, digital integration, and lifecycle cost management. Small and medium municipalities often favor modular plug-and-play systems while large industrial users seek customized high-flux solutions. The competitive edge now belongs to pioneers combining advanced filtration, smart data, and sustainable branding, driven by tightening water scarcity and Green Deal requirements.

KEY MARKET PLAYERS

A few major players of the Europe ultrafiltration market include

- SUEZ

- Veolia

- DuPont Water Solutions

- Pentair

- Toray Industries

- Koch Separation Solutions

- Alfa Laval

- Merck Millipore

- Asahi Kasei

- Pall Corporation

- Nitto Denko Corporation

- 3M

- Lanxess

- Synder Filtration

Top Strategies Used by the Key Market Participants

Key players in the Europe ultrafiltration market focus on regulatory alignment by designing systems that meet EU Drinking Water and Wastewater Reuse Directive requirements out of the box. They expand ceramic membrane production capacity to serve high fouling industrial applications in food, pharma, and semiconductors, where longevity offsets initial costs. Companies integrate digital monitoring and predictive maintenance into skid-mounted systems to reduce operational complexity for small municipalities. Strategic partnerships with dairy chemical and microelectronics industries enable co-development of application-specific ultrafiltration solutions. Additionally, they pursue modular and energy-optimized designs to lower the total cost of ownership and accelerate adoption in water-stressed regions facing budget constraints and drought pressures.

Leading Players in the Market

- Suez SA is a French multinational water and waste management leader with a strong footprint in the Europe ultrafiltration market through its advanced membrane technologies and large-scale municipal projects. The company contributes globally by developing proprietary polymeric and ceramic ultrafiltration modules used in drinking water and industrial reuse applications across multiple countries. In Europe, Suez has strengthened its position by integrating ultrafiltration into its smart water management platforms that combine real-time monitoring, predictive maintenance, and digital twin simulations. Its initiatives align with EU water reuse directives and reinforce Suez as a full-cycle water solutions provider.

- Pentair plc is a UK-headquartered global water treatment company with significant operations in the Netherlands and Germany, driving ultrafiltration adoption across municipal and industrial sectors in Europe. The company contributes globally by manufacturing X-Flow hollow fiber ultrafiltration membranes known for high flux and fouling resistance in challenging feedwaters. In Europe, Pentair has deepened its market presence by launching energy-optimized skid-mounted systems for small and medium municipalities complying with the EU Drinking Water Directive. Pentair’s focus on modular, scalable, and digitally enabled solutions positions it as a preferred partner for decentralized and industrial water reuse projects across the continent.

- NX Filtration B.V. is a Dutch innovator specializing in high-performance ceramic ultrafiltration membranes with a growing footprint in Europe’s industrial and microelectronics sectors. The company contributes globally by commercializing hydrophilic ceramic membranes that operate at lower pressures and higher flux than traditional polymeric alternatives, reducing energy use. In Europe, NX Filtration has strengthened its position by securing contracts with semiconductor fabs in Germany and France requiring ultrapure water for chip manufacturing under the European Chips Act. The company also collaborates with the European Dairy Association to validate its membranes for protein separation in cheese production. NX Filtration is changing the landscape of industrial water treatment by making durable, sustainable ceramic ultrafiltration a cost-effective choice for tackling new, complex contaminants.

MARKET SEGMENTATION

This research report on the Europe ultrafiltration market has been segmented and sub-segmented based on membrane type, application, end-user industry, and region.

By Membrane Type

- Polymeric Membranes

- Ceramic Membranes

- Metallic and Other Inorganic Membranes

By Application

- Water and Wastewater Treatment

- Food and Beverage Processing

- Pharmaceuticals and Biotechnology

- Chemicals and Petrochemicals

- Micro-electronics

By End User Industry

- Municipal

- Industrial

- Healthcare

- Agriculture

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What factors are driving the growth of the Europe ultrafiltration market?

Key drivers include stringent water quality regulations, rising demand for clean drinking water, increasing wastewater reuse, and growing adoption in the food, beverage, and pharmaceutical industries.

2. Which industries are the major end users of ultrafiltration systems in Europe?

Major end users include municipal water treatment, wastewater treatment, food and beverage processing, pharmaceuticals, biotechnology, chemicals, and dairy industries.

3. How does ultrafiltration differ from microfiltration and reverse osmosis?

Ultrafiltration removes smaller particles than microfiltration but larger molecules than reverse osmosis, offering a balance between filtration efficiency, energy consumption, and operational cost.

4. What membrane materials are commonly used in ultrafiltration systems in Europe?

Common materials include polyethersulfone (PES), polyvinylidene fluoride (PVDF), polysulfone (PS), and cellulose-based membranes.

5. What role do European regulations play in the ultrafiltration market?

Strict EU regulations related to drinking water quality, wastewater discharge, and industrial effluent treatment significantly support the adoption of ultrafiltration technologies.

6. What are the key challenges faced by the Europe ultrafiltration market?

Challenges include membrane fouling, high initial installation costs, maintenance requirements, and the need for skilled operation.

7. How does ultrafiltration support water reuse and recycling initiatives in Europe?

Ultrafiltration enables effective removal of contaminants, making treated wastewater suitable for reuse in industrial processes, agriculture, and indirect potable applications.

8. What is the role of ultrafiltration in the food and beverage industry in Europe?

Ultrafiltration is used for concentration, clarification, sterilization, and protein separation in dairy, beverage, and brewing applications.

9. What trends are shaping the Europe ultrafiltration market?

Key trends include advancements in membrane materials, integration with smart monitoring systems, modular system designs, and increasing use in decentralized water treatment.

10. How is ultrafiltration used in the pharmaceutical and biotechnology sectors?

It is used for sterilization, protein purification, concentration of biological products, and removal of endotoxins.

11. Which European regions show high adoption of ultrafiltration technology?

Western and Northern Europe show high adoption due to advanced water infrastructure, while Eastern and Southern Europe are witnessing growing demand due to infrastructure upgrades.

12. What is the future outlook for the Europe ultrafiltration market?

The market is expected to grow steadily, supported by sustainability goals, increasing water stress, industrial expansion, and continuous technological innovation.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com