Europe Wearable Technology Market Research Report By Product (Wristwear, Eyewear and Headwear, and Others), Application (Consumer Electronics, Healthcare, and Others), and Country (Germany, United Kingdom, France, and Rest of Europe) – Industry Analysis on Size, Share, Trends, and Growth Forecast (2026 to 2034)

Europe Wearable Technology Market Summary

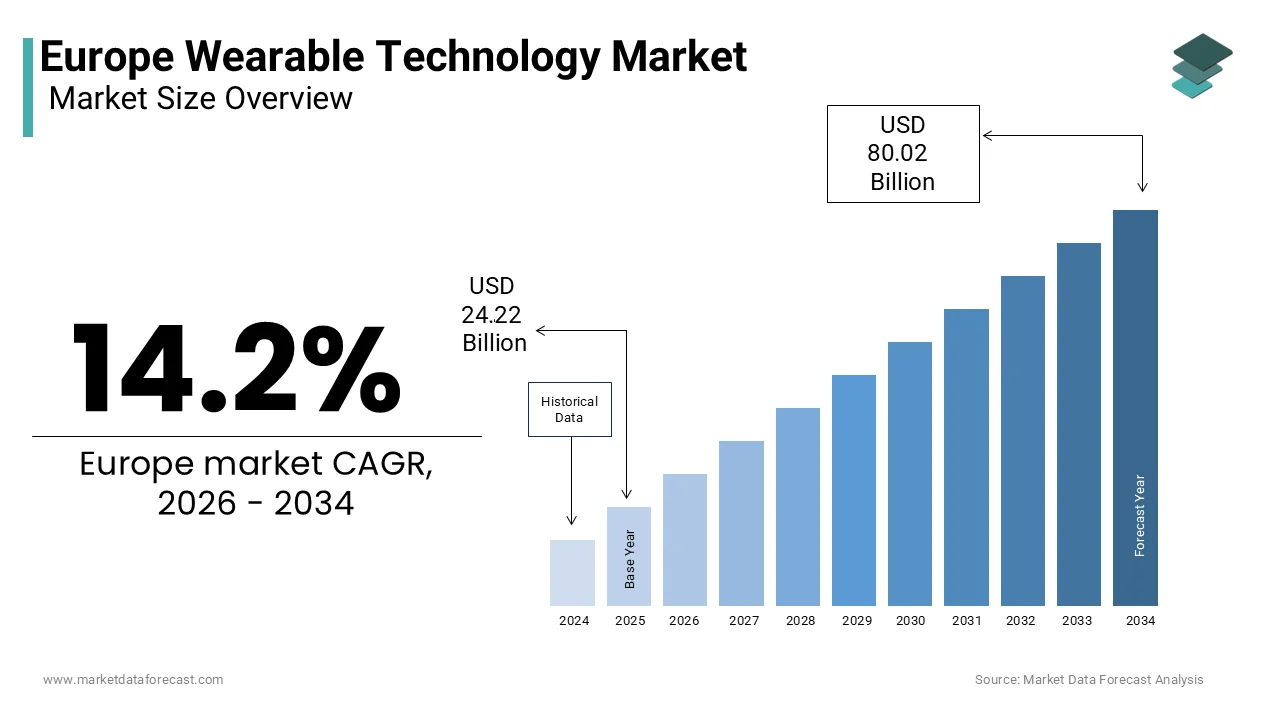

The Europe wearable technology market was valued at USD 24.22 billion in 2025 and is projected to reach USD 80.02 billion by 2034, growing at a CAGR of 14.2% from 2026 to 2034, driven by national digital health integration, preventive healthcare adoption, and expanding clinical and occupational wearable use.

Market Snapshot

- 2025 Market Size: USD 24.22 billion

- 2026 Market Size: USD 27.66 billion

- 2034 Forecast: USD 80.02 billion

- CAGR (2026–2034): 14.2%

- Base Year: 2025

- Forecast Period: 2026–2034

Quick Growth Drivers

- Integration of wearables into national digital health and reimbursement frameworks

- Rising preventive healthcare awareness among aging European populations

- Expansion of remote patient monitoring (RPM) and telemedicine ecosystems

- Growing use of wearables in occupational health and safety programs

- High consumer adoption of smartwatches, fitness trackers, and biosensors

Principal Restraints

- Stringent EU Medical Device Regulation (MDR) delaying clinical-grade adoption

- Limited availability of notified bodies for wearable certification

- High certification costs and long approval timelines

- GDPR-driven biometric data privacy and consent complexity

- Restricted cross-border health data interoperability

High-Value Opportunities

- Expansion of wearables in occupational health, industrial safety, and fatigue monitoring

- Convergence of wearables with telemedicine and remote diagnostics platforms

- Reimbursement-backed adoption in chronic disease management

- Growth of medical-grade biosensors for cardiovascular, diabetes, and sleep disorders

- Integration with national electronic health record (EHR) systems

Key Market Challenges

- Limited battery life and lack of wearable-specific charging infrastructure

- Gaps in clinical validation for consumer-grade devices

- Fragmented interoperability standards across healthcare systems

- Low adoption of FHIR-compliant data exchange among wearable vendors

Fastest-Growing Segments

- Healthcare Applications – fastest CAGR due to reimbursement and RPM programs

- Eyewear & Headwear – driven by AR smart glasses and enterprise use cases

- Medical-Grade Wearables – accelerated by CE certification and insurer coverage

Regional Leadership & Dynamics

- Germany (22.4%) — statutory insurance reimbursement, strong medtech ecosystem

- United Kingdom (16.8%) — NHS digital health programs and RPM leadership

- France — public health integration and fashion-tech convergence

- Nordic countries — preventive health and occupational safety adoption

What Wins Commercially

- CE-marked devices compliant with EU MDR and GDPR

- Clinical validation and insurer reimbursement eligibility

- Long battery life and continuous monitoring reliability

- Seamless integration with telemedicine platforms and EHRs

- Strong data privacy, on-device processing, and consent transparency

Top Strategic Ask for Executives

Invest in clinically validated, GDPR-compliant wearables that integrate seamlessly into national health systems and occupational safety programs while improving battery performance and interoperability.

Leading Players

Some of the companies that are playing a dominating role in the Europe wearable technology market include

Apple Inc., Samsung Electronics Co., Ltd., Fitbit, Inc. (Google LLC), Garmin Ltd., Huawei Technologies Co., Ltd., Xiaomi Corporation, Sony Corporation, Fossil Group, Inc., Withings SA, Polar Electro Oy, Suunto Oy, TomTom International BV, Amazfit (Huami Corporation), Bosch Sensortec GmbH, TAG Heuer (LVMH Group), Lenovo Group Limited, Google LLC, Pebble Technology Corp., and Nike, Inc.

Europe Wearable Technology Market Size

The europe wearable technology market was valued at USD 24.22 billion in 2025, is expected to have a 14.2% CAGR from 2026 to 2034, and be worth USD 80.02 billion by 2034 from USD 27.66 billion in 2026.

The wearable technology is an electronic device integrated into clothing accessories or worn directly on the body that collects, processes, and transmits physiological, behavioral, or environmental data in real time. These include smartwatch, e-s fitness track, e-s smart eyewear, biosensors, and medical-grade wearables used across consumer health enterprise and clinical settings. According to Eurostat, 58% of adults in the European Union used a health or fitness tracking device at least once per week in 2024. As per the European Commission, over 1200 digital health startups in Europe developed wearable-based solutions in 2024, with 63% focused on chronic disease management. The European Medicines Agency granted 28 CE certifications for wearable medical devices in 2024, enabling remote patient monitoring under regulated care pathways. Furthermore, national health systems in Germany, France, the Netherlands, and other countries integrated wearable data into electronic health records for diabetes and cardiovascular programs.

MARKET DRIVERS

Integration of Wearables into National Digital Health Strategies

The European governments are systematically embedding wearable technology into public health infrastructure to enable preventive care and reduce hospitalization costs, which is certainly a major factor fuelling the growth of the European wearable technology market. According to the European Observatory on Health Systems and Policies, 17 EU member states launched state-sponsored wearable pilot programs in 2024, targeting chronic conditions such as hypertension and type 2 diabetes. Germany’s Digital Health Applications Ordinance now reimburses approved wearable systems under statutory health insurance,ce with over 420000 patients enrolled in remote monitoring as of early 2025. Similarly, the UK’s National Health Service integrated Apple Watch and Fitbit data into its digital diabetes prevention program, which reported a 23% reduction in HbA1c levels among participants. As per the European Commission’s Digital Transformation of Health and Care initiative, wearable data interoperability with national electronic health records is now mandatory for all new digital therapeutics. This policy-driven adoption transforms wearables from lifestyle gadgets into clinically validated tools supported by public funding and regulatory frameworks.

Rising Consumer Awareness of Preventive Health and Longevity

European consumers are increasingly prioritizing proactive health management driven by aging demographics and digital literacy, which is also accelerating the growth of the European wearable technology market. According to Eurostat, 29% of the EU population was aged 55 or older in 2024, and this cohort shows the highest adoption rate of health-focused wearables. The European Consumer Organisation reports that many adults aged 45 to 65 use wearables to monitor heart rate, sleep quali, ty or physical activity,ity with 52% sharing data with their general practitioners. Educational campaigns have amplified this trend. The European Heart Network’s 2024 “Know Your Numbers” initiative reached 14 million citizens, promoting wearable use for blood pressure and arrhythmia detection. Additionally, longitudinal studies validate efficacy. This behavioral shift is reinforced by employer wellness programs. These converging social and institutional forces are normalizing continuous health monitoring as a daily practice.

MARKET RESTRAINTS

Stringent Medical Device Regulations Delaying Clinical Adoption

The European Union’s Medical Device Regulation imposes rigorous conformity assessment requirements that are limiting the growth of Europe's wearable technology market. According to the European Commission, only 34% of wearable health startups achieved full MDR certification in 2024 due to complex clinical evidence and quality management system demands. Many innovators opt for general wellness classification to avoid these hurdles but forfeit reimbursement and clinical integration opportunities. The European Medicines Agency acknowledges that regulatory uncertainty has discouraged investment in venture funding for MDR-compliant wearables, declining by 19% in 2024. Furthermore, notified bodies remain overloaded. As per the European Association of Notified Bodies,s only 22 organizations across the EU are authorized to certify digital health devices, leading to application backlogs exceeding six months.

Data Privacy and Consent Complexity Under the General Data Protection Regulation

The collection of sensitive biometric data by wearables triggers strict obligations under the General Data Protection Regulation, creating compliance friction for developers and users alike, which is also hindering the growth of the European wearable technology market. According to the European Data Protection Board, continuous heart rate location and sleep pattern data qualify as special category personal data requiring explicit informed consent and purpose limitation. Moreover, cross-border data transfers face additional scrutiny. As per the European Court of Justice, the 2020 Schrems II ruling invalidated standard contractual clauses for health data sent to non-EU cloud providers unless supplementary safeguards are implemented. This forces European wearable firms to localize data infrastructure,e increasing operational costs. The European Consumer Organisation reports that 53% of users disable certain tracking features due to privacy concerns, reducing data utility.

MARKET OPPORTUNITIES

Expansion of Wearables in Occupational Health and Safety Programs

European industries are increasingly deploying wearables to enhance worker safety, productivity,y and fatigue management, particularly in high-risk sectors, which is creating new opportunities for the growth of the European wearable technology market. According to the European Agency for Safety and Health at Work, 38% of construction and logistics companies in the EU piloted wearable exoskeletons or fatigue monitoring bands in 2024. In Germany, the Employers’ Liability Insurance Association mandated smart helmets with proximity sensors for all large infrastructure sites, reducing collision incidents. The Nordic countries lead in adoption. As per Sweden’s Work Environment Authority 64% of manufacturing firms use real-time physiological monitoring to prevent heat stress and overexertion. These applications are supported by EU funding. The European Social Fund allocated 210 million euros in 2024 to digitize occupational health through wearable integration.

Emergence with Telemedicine and Remote Patient Monitoring Ecosystems

The wearable technology is emerging as the foundational data layer for Europe’s rapidly scaling telemedicine infrastructure. According to the European Commission, 22 EU countries now include remote patient monitoring in national telehealth reimbursement schemes with wearables as the primary data source. In the Netherlands, Philips and local GPs launched a heart failure program in 202,4 where patients used ECG-enabled patches to transmit daily readings, reducing hospital readmissions by 34%. Similarly, Italy’s National Health Service integrated glucose monitoring wearables into its diabetes care pathway,y covering 180000 patients. The European Innovation Partnership on Active and Healthy Ageing reports that wearable-supported telemonitoring cuts per patient annual costs by 1200 euros on average. Crucially, interoperability standards are advancing.

MARKET CHALLENGES

Limited Battery Life and Charging Infrastructure Constraints

European consumers continue to cite battery limitations as a primary barrier to sustained wearable use. This is substantially one of the major challenges for the growth of the European wearable technology market. According to the European Consumer Organisation, 59% of smartwatch users in 2024 reported daily charging requirements as inconvenient, particularly for sleep and continuous health tracking. As per the European Coordination Committee of the Radiological, Electromedical, and Healthcare IT Industry, 72% of ECG and glucose monitoring wearables require recharging or sensor replacement every 48 to 72 hours, disrupting data continuity. Public infrastructure offers little relief. Unlike smartphones, one's wearable-specific charging stations are virtually absent in European transport hubs or workplaces. The European Environment Agency notes that frequent charging increases energy consumption, with an estimated 1.2 terawatt hours used annually across EU wearable devices. While solid state and kinetic energy harvesting technologies are in development,t none have reached mass commercialization.

Lack of Clinical Validation and Interoperability Standards

Many consumer wearables lack rigorous clinical validation and cannot integrate with professional healthcare systems, ms limiting their utility in medical decision making. The lack of clinical validation and interoperability standards is also inhibiting the growth of the European wearable technology market. According to the European Society of Cardiology, only 28% of commercially available heart rate monitors meet clinical-grade accuracy standards for arrhythmia detection. Similarly, the European Federation of Clinical Chemistry found that optical glucose estimation wearables showed significant deviation from laboratory results. This credibility gap prevents adoption in formal care pathways. Interoperability exacerbates the issue. As per the European Institute for Health Records, wearables support the Fast Healthcare Interoperability Resources standard required for integration with national electronic health records. Consequently, clinicians often disregard wearable data.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Application, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe |

| Market Leaders Profiled | Apple Inc., Samsung Electronics Co., Ltd., Fitbit, Inc. (now part of Google LLC), Garmin Ltd., Huawei Technologies Co., Ltd., Xiaomi Corporation, Sony Corporation, Fossil Group, Inc., Withings SA, Polar Electro Oy, Suunto Oy, TomTom International BV, Amazfit (Huami Corporation), Bosch Sensortec GmbH, Montblanc International GmbH, TAG Heuer (LVMH Group), Lenovo Group Limited, Google LLC, Pebble Technology Corp., Nike, Inc. |

SEGMENTAL ANALYSIS

By Product Insights

The wristwear segment was the largest by holding a dominant share of the Europe wearable technology market in 2025, owing to its dual functionality as both a health monitor and a lifestyle accessory with seamless integration into daily routines. According to Eurostat, 64% of European adults who wear wearables own a smartwatch or fitness tracker worn on the wrist primarily due to comfort and social acceptability. The European Consumer Organisation notes that wrist-worn devices are perceived as less intrusive than head-mounted alternatives, with users reporting consistent all-day wear. Major manufacturers have optimized this form factor for health applications. As per the European Commission’s Digital Health Certification Database, many CE-marked wearable medical devices in 2024 were wrist-based, including ECG and SpO2 monitors from Apple, Samsung, and Withings. Furthermore, Ristwear benefits from mature supply chains and ecosystem lock-in. The European Telecommunications Standards Institute reports that European smartphone users prefer wrist devices that pair effortlessly with their mobile operating systems. These ergonomic, technological, and behavioral advantages solidify wristwear as the default wearable interface across consumer and clinical domains.

The eyewear and headwear segment is expected to grow at the fastest CAGR of 24.6% throughout the forecast period in augmented reality smart glasses and enterprise safety applications, rather than consumer fashion. According to the European Agency for Safety and Health at Work, 41% of logistics and manufacturing firms in Germany, France, and the Netherlands deployed AR-enabled smart glasses for hands-free workflow guidance in 2024, reducing task errors by 33%. Medical adoption is equally significant. As per the European Society of Radiology, surgeons at 28 university hospitals across Europe used Microsoft HoloLens 2 in 2024 for real-time 3D anatomical visualization during complex procedures. The European Consumer Organisation reports that 19% of tech early adopters expressed intent to purchase smart eyewear in 2025, driven by Meta Ray Ban integration with social sharing and navigation. Crucially, European privacy norms favor headwear with on-device processing. The European Data Protection Board highlighted in 2024 that locally processed AR glasses pose lower surveillance risks than cloud-dependent alternatives.

By Application Insights

The consumer electronics segment was the largest by capturing a significant share of the European wearable technology market in 2025, with the mass adoption of fitness trackers and smartwatches for activity monitoring, ng sleep analysis,s and smartphone notifications among the general population. According to Eurostat, 58% of European adults used a consumer-grade wearable at least weekly in 2024, with peak adoption among 25 to 44-year-olds. As per the European Commission, it notes that over 80% of these devices are purchased out of pocket rather than through the health system,s indicating strong discretionary demand. Brand ecosystems play a crucial role. As per the European Telecommunications Standards Institute, 76% of European iPhone users own an Apple Watch, creating powerful cross-device retention. Marketing and social influence further drive uptake. Unlike clinical devices, consumer wearables benefit from rapid iteration, low regulatory barriers, and a global distribution channel,s making them the primary gateway for wearable adoption across the continent.

The healthcare application segment is expected to register the fastest CAGR of 26.3% in the coming years, owing to the policy-driven integration of wearables into national health systems, chronic disease burden,n and clinical validation of remote monitoring. According to the European Observatory on Health Systems and Policies, 19 EU countries now reimburse or subsidize wearable devices for conditions like diabetes, heart failure, and COPD. Germany’s statutory health insurers covered 420000 patients with connected wearables in 2024 under its Digital Health Applications Ordinance. Similarly, the UK’s National Health Service reported a 28% reduction in hospital admissions for heart failure patients using wearable ECG patches. The European Medicines Agency granted 34 CE certifications for medical-grade wearables in 2024 by enabling use in regulated care pathways.

COUNTRY LEVEL ANALYSIS

Germany Wearable Technology Market Analysis

Germany was the top performer of the European wearable technology market by holding 22.4% in 2025, with a robust medtech industry, strong statutory health insurance integration,n and high consumer tech adoption. According to Germany’s Federal Statistical Office, 67% of adults used a health tracking wearable in 2024, with 41% sharing data with physicians. The Federal Ministry of Health’s Digital Health Act mandates that all certified wearable health apps be reimbursed by public insurers, a policy that spurred 120 CCE-marked wearable solutions by early 2025. Companies like Bosch and Siemens Healthineers develop clinical-grade biosensors while startups such as Preventicus gain traction with arrhythmia detection algorithms. As per the German Employers’ Liability Insurance Association, over 1800 industrial sites deployed smart helmets and fatigue monitors in 2024, enhancing occupational safety. Additionally, Germany hosts Europe’s largest medical technology trade fair, MEDICA, where 340 wearable health innovations were showcased in 2024.

United Kingdom Wearable Technology Market Analysis

The United Kingdom held 16.8% of Europe's wearable technology market share in 2025, with its strength lying in digital health innovation, strong consumer electronics retail, and early adoption of remote care models. According to the UK’s Office for National Statistics, 63% of adults owned a wearable device in 2024, with the highest penetration among urban professionals. The National Health Service has been pivotal. As per NHS England, its digital diabetes prevention program enrolled over 250000 participants in 2024 using Fitbit and Apple Watch data to personalize coaching. The Medicines and Healthcare products Regulatory Agency fast-tracked 22 wearable medical device approvals in 2024, including continuous glucose monitors and respiratory trackers. Academic research also drives progress.

France Wearable Technology Market Analysis

The French wearable technology market is likely to have prominent growth opportunities in the coming years, with the public health strategy, strong engineering talent, and consumer fashion tech convergence. According to France’s National Institute of Statistics and Economic Studies, 59% of adults used wearables in 2024, with notable uptake in elderly monitoring. The French National Health Insurance Fund allocated 210 million euros in 2024 to subsidize wearables for fall prevention and chronic disease management, covering over 300000 patients. Homegrown companies like Withings lead in design and medical integration,n with its ScanWatch receiving CE certification for atrial fibrillation detection. The French Alternative Energies and Atomic Energy Commission launched a flexible biosensor platform in 20,24 enabling sweat-based electrolyte monitoring.

Sweden Wearable Technology Market Analysis

Sweden's wearable technology market growth is driven by the preventive health culture, public digital infrastructure,e and ethical technology design. The Swedish e-Health Agency integrated wearable data into national electronic health records in 2024 by enabling seamless clinician access for 1.2 million patients. Companies like Aifloo and Minut leverage wearables for elderly care with real-time anomaly detection in nursing homes. Sweden also prioritizes sustainability. The Swedish Environmental Research Institute reports that Swedish consumers prefer wearables with replaceable batteries and repairable designs. This alignment of public health digital governance and environmental consciousness makes Sweden a model for human-centered wearable adoption.

Netherlands Wearable Technology Market Analysis

The Netherlands wearable technology market growth is likely to grow with the advanced telemedicine infrastructure, strong medtech collaboration,n and data interoperability. According to Statistics Netherlands, many adults used health wearables in 20,24 with 48% participating in insurer-sponsored wellness programs. As per the Research, wearable data from over 200000 patients is now standardized using the Fast Healthcare Interoperability Resources protocol, enabling cross-institutional analytics. The country also hosts the European Institute for Health Records, which sets wearable data exchange benchmarks for the EU. This ecosystem of clinical integration,n technical standards, and corporate innovation secures the Netherlands’ position as a key enabler of scalable wearable health solutions.

COMPETITIVE LANDSCAPE

The European wearable technology market features a dynamic interplay between global consumer electronics giants, European medtech specialists, and agile health tech startups. Apple, Samsung, and Garmin dominate the consumer segment with brand recognition and ecosystem lock-in, yet face growing competition from European firms like Withings and Garmin’s regional rivals that emphasize medical validation and data sovereignty. On the clinical side, Philips Biofourmis and Preventicus lead with hospital-integrated solutions backed by regulatory approvals and health system partnerships. Startups thrive through public funding and digital health accelerators, but struggle with scale due to stringent Medical Device Regulation requirements. Competition is further shaped by national policies,s with Germany and France enabling reimbursement, while Nordic countries prioritize preventive public health programs. Differentiation increasingly hinges on clinical evidence interoperability, ty privacy by design,ign, and alignment with Europe-values-driven digital health vision rather than hardware specifications alone.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global europe wearable technology market include

- Apple Inc.

- Samsung Electronics Co., Ltd.

- Fitbit, Inc. (now part of Google LLC)

- Garmin Ltd.

- Huawei Technologies Co., Ltd.

- Xiaomi Corporation

- Sony Corporation

- Fossil Group, Inc.

- Withings SA

- Polar Electro Oy

- Suunto Oy

- TomTom International BV

- Amazfit (Huami Corporation)

- Bosch Sensortec GmbH

- Montblanc International GmbH

- Tag Heuer (LVMH Group)

- Lenovo Group Limited

- Google LLC

- Pebble Technology Corp.

- Nike, Inc. Lenovo Group Limited

TOP LEADING PLAYERS IN THE MARKET

- Apple maintains a commanding presence in the European wearable technology market through its Apple Watch and AirPods, which combine advanced health sensors with seamless ecosystem integration. The company contributes globally by setting up in ECG blood oxygen and fall detection capabilities while driving regulatory acceptance of consumer wearables as medical tools. In Europe, Apple has deepened clinical partnerships by enabling Apple Watch data integration with national electronic health records in the UK, Germany, and the Netherlands. Apple collaborated with European cardiology societies to validate its atrial fibrillation detection algorithm across diverse populations. It also enhanced privacy features to comply with the General Data Protection Regulation, ensuring device processing for sensitive health metrics.

- Withings, a French innovator,r stands out in the European wearable technology market by blending medical-grade accuracy with elegant design in products such as the ScanWatch and Body Comp scale. The company contributes globally by demonstrating that consumer devices can meet stringent clinical standards while remaining accessible. Withings devices hold CE certification as Class IIa medical devices, enabling reimbursement through European health systems. Withings launched a hypertension monitoring program in partnership with French insurers, allowing users to share validated blood pressure trends with physicians. It also integrated its ecosystem with Doctolib Europe’s largest telemedicine platform to enable remote consultations triggered by wearable alerts. These initiatives position Withings at the intersection of preventive care,e digital therapeutics, and user-centric design.

- Philips plays a pivotal role in the Europe wearable technology market through its professional-grade health monitoring solutions, including the Philips Biosensor Patch and wearable sleep diagnostics. Headquartered in the Netherlands, the company bridges clinical care and home monitoring by developing hospital-validated wearables for remote patient management. Globally, Philips sets standards for interoperability and data security in medical wearables. Philips expanded its telehealth partnerships across Germany, Italy, and Sweden, enabling real-time transmission of vital signs to hospital command centers. It also received European Medicines Agency approval for a wearable sepsis prediction algorithm now deployed in over 40 European hospitals.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe wearable technology market prioritize regulatory compliance by pursuing CE certification under the Medical Device Regulation to enable clinical use and reimbursement. They invest in clinical validation studies in collaboration with European universities and hospitals to establish medical credibility. Companies enhance data privacy through on-device processing and transparent consent mechanisms aligned with the General Data Protection Regulation. Strategic partnerships with national health services, insurers, and telemedicine platforms facilitate ecosystem integration. Many firms also differentiate through design sustainability and battery longevity to address consumer fatigue. Additionally, they develop enterprise solutions for occupational health, targeting logistics, manufacturing, and healthcare sectors. These strategies reflect a dual focus on consumer appeal and institutional trust.

MARKET SEGMENTATION

This research report on the europe wearable technology market is segmented and sub-segmented into the following categories.

By Product

- Wristwear

- Eyewear and Headwear

- Others

By Application

- Consumer Electronics

- Healthcare

- Others

By Country

- Germany

- United Kingdom

- France

- Rest of Europe

Frequently Asked Questions

1. How is health awareness influencing the Europe Wearable Technology Market?

Increasing health consciousness in Europe drives demand for wearable health monitors and fitness trackers, significantly boosting the Europe Wearable Technology Market.

2. Which countries dominate the Europe Wearable Technology Market?

Germany, the United Kingdom, and France are dominant regions in the Europe Wearable Technology Market, supported by advanced tech infrastructure and high consumer adoption.

3. What role does IoT play in the Europe Wearable Technology Market?

IoT integration enhances real-time data capabilities of wearable devices, expanding applications in fitness, healthcare, and enterprise within the Europe Wearable Technology Market.

4. How are medical wearables regulated in the Europe Wearable Technology Market?

The EU Medical Device Regulation (MDR) enforces strict guidelines ensuring safety and accuracy of medical wearables sold in Europe, strengthening consumer trust in the Europe Wearable Technology Market.

5. What are the key drivers for growth in the Europe Wearable Technology Market?

Growth in the Europe Wearable Technology Market is driven by technological innovation, rising health concerns, increased digital connectivity, and supportive government policies.

6. How is AI integrated into the Europe Wearable Technology Market devices?

AI integration in wearable devices provides personalized health insights and predictive analytics, enhancing the consumer experience in the Europe Wearable Technology Market.

7. What are the current trends in the Europe Wearable Technology Market?

Trends include multifunctional devices, eco-friendly materials, seamless platform integration, and advanced biometric sensing in the Europe Wearable Technology Market.

8. Who are the leading companies in the Europe Wearable Technology Market?

Major players include Apple, Samsung, Fitbit, Garmin, Xiaomi, and European brands like Withings, dominating the Europe Wearable Technology Market through continuous innovation.

9. What challenges does the Europe Wearable Technology Market face?

Challenges include data privacy concerns, manufacturing costs, limited battery life, and the need for compliance with stringent regulatory standards in the Europe Wearable Technology Market.

10. How is wearable technology being used in healthcare within Europe?

Wearable technology facilitates real-time health monitoring, chronic disease management, and remote patient care, making healthcare a leading application in the Europe Wearable Technology Market.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com