Global Jars Market Size, Share, Trends, and Growth Analysis Report, Segmented By Material Type, Capacity, End Use, & Region (North America, Europe, Latin America, Asia Pacific, Middle East & Africa), Industry Forecast From 2026 to 2034

Global Jars Market Summary

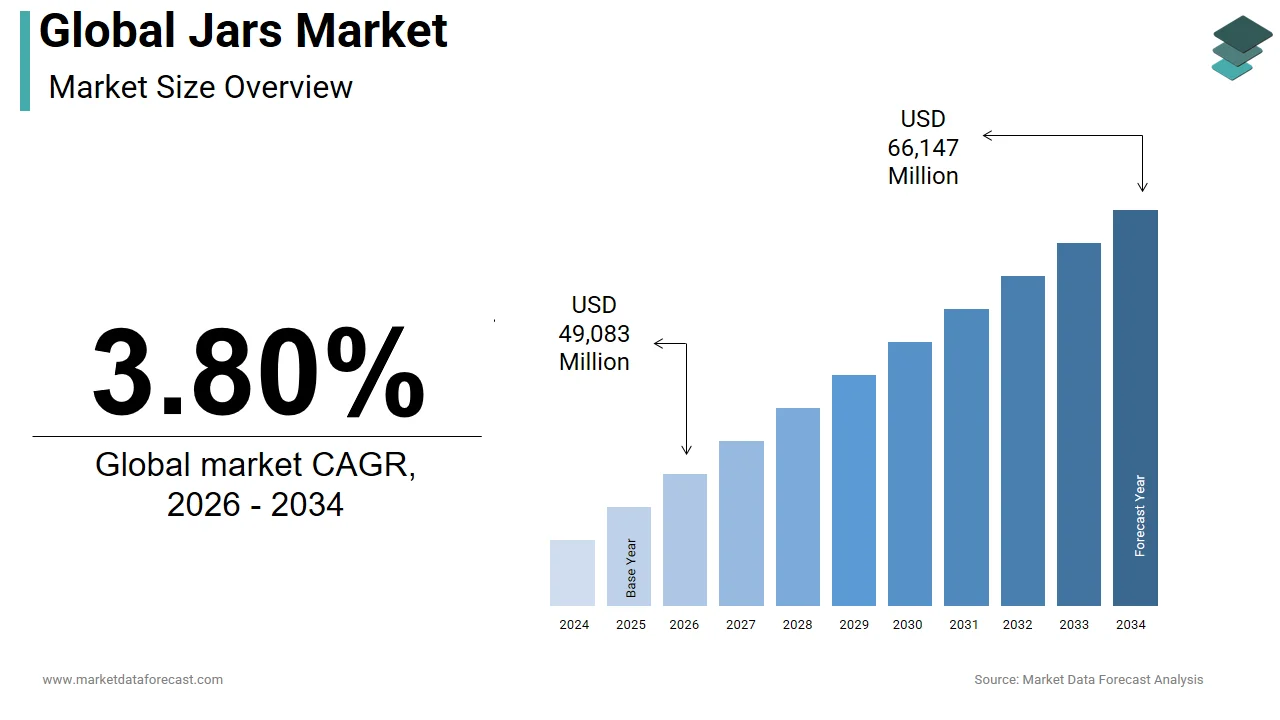

The global jars market was valued at USD 47,28.09 million in 2025, is estimated to reach USD 49,083 million in 2026, and is projected to grow to USD 66,147 million by 2034, expanding at a CAGR of 3.80% from 2026 to 2034. The growth of the global jars market is attributed to the increasing demand from the food & beverage industry, rising use in cosmetics and personal care packaging, and growing preference for lightweight, cost-effective, and recyclable materials. The expansion of e-commerce and convenience packaging further supports steady growth.

Key Market Trends

- Rising demand for plastic jars due to affordability, durability, and lightweight properties.

- Strong use of jars in food & beverage packaging, particularly for sauces, spreads, and beverages.

- Increasing adoption of eco-friendly and recyclable packaging solutions.

- Growth of online retail is fueling demand for protective and convenient jar packaging.

- Expanding use of customized and premium jars in cosmetics and personal care.

Segmental Insights

- By material type, the plastic jars segment dominated with a 47.1% share in 2024, driven by cost-effectiveness and versatility.

- By capacity, the 10–50 OZ jars segment held the largest share at 52.8% in 2024, reflecting widespread consumer and industrial usage.

- By end use, the food & beverages segment accounted for 63.5% of the global market in 2024, making it the largest application sector.

Regional Insights

- Asia-Pacific led the global jars market in 2024 with a 35.1% share, driven by strong food & beverage consumption, expanding retail networks, and growing personal care industries.

- North America shows steady demand, supported by innovation in packaging formats and sustainability initiatives.

- Europe emphasizes eco-friendly packaging regulations, boosting demand for recyclable and glass jars.

- Latin America and the Middle East & Africa are emerging regions, fueled by growing packaged food consumption and retail expansion.

Competitive Landscape

Key players in the global jars market include Berry Global Group, Amcor plc, Owens-Illinois Group Inc., Graham Packaging Company, Silgan Plastics, Gerresheimer AG, Alpha Packaging, Olcott Plastics, Cospak Ltd., and Great Western Containers Inc. These companies are focusing on sustainable packaging innovations, product customization, and global distribution expansion to strengthen their market share.

Global Jars Market Size

The global jars market was valued at USD 47,28.09 million in 2025, is estimated to reach USD 49,083 million in 2026, and is projected to reach USD 66,147 million by 2034, growing at a CAGR of 3.80% from 2026 to 2034.

Jars are containers that are primarily made of glass and plastic. It is designed for storing food, pharmaceuticals, cosmetics, and artisanal goods. These rigid packaging units are valued for their durability, reusability, and ability to preserve product integrity. In recent years, consumer preference for sustainable packaging has significantly influenced manufacturing trends. Also, glass jars are witnessing renewed demand due to their infinite recyclability. According to the research, a notable share of glass collected for recycling in the United States is remelted into new containers, emphasizing the material’s circular economy potential. Apart from these, as per the research, containers and packaging constitute a key share of landfill waste, driving regulatory and corporate initiatives toward reusable and recyclable jar solutions. This evolving environmental consciousness is reshaping design, material selection, and end-of-life management across the jars market.

MARKET DRIVERS

Rising Demand for Packaged Food and Beverages

The escalating demand for packaged food and beverages, driven by urbanization and changing consumption pattern,s propels the growth ofthe jars market. Reliance on ready-to-eat and preserved foods has surged due to the shift toward city living by the population in emerging economies, which increases the need for reliable and long-shelf-life storage solutions. Jars, particularly glass ones, are preferred for products like sauces, jams, pickles, and baby food due to their impermeability and non-reactivity. According to the study, close to 56.2% of the global population resided in urban areas in 2021, a figure projected to rise to around 60% by 2030. This demographic transition correlates directly with higher demand for packaged perishables. Furthermore, as per the study, a notable share of household food expenditures is on processed and packaged items. Consequently, this strengthens the necessity for safe, transparent, and shelf-stable packaging such as jars, especially in retail-centric supply chains.

Shift Toward Sustainable and Eco-Friendly Packaging

The growing consumer preference for sustainable and eco-friendly packaging is boosting the growth of the jars market. Brands across food, cosmetics, and wellness sectors are shifting to recyclable and reusable jar formats owing to the increasing awareness of plastic pollution and regulatory actions against single-use plastics. According to data from the plastics industry group Plastics Europe, approximately 29.5 million tonnes (Mt) of post-consumer plastic waste were collected in the EU27+3 in 2020. In response, companies are adopting refillable glass jars to align with circular economy goals. As per the study, glass containers have a notable recycling rate in the U.S., with higher recovery rates in countries like Switzerland. Moreover, a study revealed that many global consumers are willing to pay more for sustainable packaging, which accelerates the transition from plastic to glass jars in premium and organic product lines.

MARKET RESTRAINTS

High Carbon Footprint of Glass Production and Transport

The high carbon footprint associated with glass manufacturing and transportation is hindering the growth of the jars market. The production of glass jars requires melting raw materials at temperatures exceeding 1,500°C. It’s a process heavily reliant on fossil fuels. According to the International Energy Agency, the global glass industry accounts for a portion of total industrial energy consumption and emits millions of tons of CO₂ annually. Apart from these, glass jars are significantly heavier than plastic or aluminum alternatives, and that increases fuel consumption and emissions during distribution. As per the research, freight transport contributes a key share of total U.S. greenhouse gas emissions, with weight being an important factor. These environmental costs challenge the sustainability claims of glass jars, particularly when logistics span long distances. Consequently, companies face growing scrutiny over lifecycle emissions, which limits the scalability of glass jar adoption in carbon-sensitive markets.

Fragility and Logistical Challenges of Glass Jars

The fragility and logistical vulnerability of glass jars, which increase breakage risks and associated costs across the supply chain, are impeding the growth of the jars market. Unlike plastic or flexible packaging, glass is prone to cracking during handling, storage, and transit, leading to product loss and safety hazards. According to the study, a portion of cargo damage in U.S. trucking incidents is attributed to breakage of fragile goods, with glass containers being among the most affected. Apart from these, the U.S. Occupational Safety and Health Administration shows that manual handling of heavy glass packaging contributes to workplace injuries, especially in warehousing and retail environments. These operational challenges necessitate additional protective packaging, specialized handling equipment, and insurance coverage, which raises overall distribution costs. As a result, many manufacturers, particularly in high-volume or remote distribution markets, remain hesitant to adopt glass jars despite their environmental benefits.

MARKET OPPORTUNITIES

Growth of the Artisanal and Premium Food Sector

The expansion of the artisanal and premium food sector, where glass jars serve as both functional packaging and branding tools, is setting up new opportunities for the growth of the jars market. Consumers are increasingly purchasing small-batch preserves, organic honey, fermented foods, and gourmet condiments. These products are often associated with authenticity and quality, which is strengthened by glass packaging. According to the Specialty Food Association, sales of specialty foods in the U.S. "neared $194 billion in 2022," and grew by 9.3% over 2021. Glass jars enhance product visibility and perceived value, which makes them ideal for direct-to-consumer and e-commerce platforms. Furthermore, as per research, premium-priced packaged foods in glass containers exhibit times higher year-over-year growth compared to standard plastic-packaged alternatives. This trend enables producers to command higher margins while aligning with consumer expectations for transparency and sustainability.

Smart Labeling and Digital Traceability in Jar Packaging

The integration of smart labeling and digital traceability in jar packaging, particularly within the pharmaceutical and premium cosmetics industries, is setting up new opportunities for the expansion of jar market. Manufacturers are adopting QR codes, NFC tags, and tamper-evident seals on glass and plastic jars because of the rising regulatory demand for product authenticity and supply chain transparency. According to the World Health Organization, 1 in 10 medical products in low- and middle-income countries is substandard or falsified, driving demand for secure, trackable packaging. In response, companies have introduced smart glass jars with embedded digital identifiers for real-time tracking. Apart from these, as per the study, many pharmaceutical firms have already implemented serialization technology, as regulatory deadlines in major markets like the U.S. and Europe have already passed or are taking full effect in 2025. These advancements reduce counterfeiting and enhance consumer engagement through mobile-based product information, which creates new value layers beyond basic containment.

MARKET CHALLENGES

Volatile Raw Material Supply in Glass Jar Production

The volatile supply of raw materials, particularly soda ash and silica sand, which are essential for glass production, challenges the growth of the jars market. Geopolitical disruptions, mining restrictions, and environmental regulations have led to inconsistent availability and price fluctuations. According to the U.S. Geological Survey, China, the United States, and Turkey account for a substantial majority in 2024 of global soda ash production. In addition, European soda ash prices surged due to energy crises and reduced output from key producers. Apart from these, according to the study, silica sand extraction faces increasing scrutiny due to ecosystem degradation. The study notes that sand is the most extracted solid material globally, surpassing fossil fuels in volume. These supply constraints threaten production continuity and cost stability for jar manufacturers.

Rising Energy Costs in Glass Jar Manufacturing

The rising cost of energy-intensive manufacturing processes, particularly for glass jar producers, challenges the growth of jars market. The melting phase in glass production consumes vast amounts of thermal energy, which is primarily derived from natural gas. This makes operations highly sensitive to energy price volatility. According to the research, energy accounts for a major share of total production costs in glass manufacturing. Moreover, during the 2022 European energy crisis, natural gas prices in Germany spiked compared to the previous year. That is forcing several glass plants to reduce output or idle furnaces. Furthermore, as per the European Container Glass Federation, maintaining furnace operations at optimal temperatures requires continuous energy input, which limits the feasibility of intermittent production. These financial and operational burdens hinder scalability and profitability, especially for smaller manufacturers lacking access to alternative fuels or energy-efficient technologies, which threatens long-term competitiveness in the jars market.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Material Type, Capacity, End Use, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Market Leaders Profiled | Berry Global Group, Amcor plc, Owens Illinois Group Inc., Graham Packaging Company, Silgan Plastics, Gerresheimer AG, Alpha Packaging, Olcott Plastics, Cospak Ltd., Great Western Containers Inc, and Others. |

SEGMENTAL ANALYSIS

By Material Type Insights

The plastic jars segment dominated the global jars market by capturing 47.1% of the global market share in 2024. The growth of plastic jars segment is primarily driven by the material’s lightweight nature and cost-effective production, which makes it ideal for mass distribution across supply chains. Plastic jars, particularly those made from PET and HDPE, require significantly less energy to manufacture and transport than glass. According to the research, transportation of plastic packaging generates lower greenhouse gas emissions compared to equivalent glass containers due to reduced weight. Furthermore, a study points out that freight fuel efficiency improves for every 100 pounds of weight reduction in cargo, amplifying the logistical advantage of plastic jars. Their durability during shipping and resistance to breakage also reduces product loss. That makes them a preferred choice for high-volume food and personal care brands. A further factor supporting the growth of plastic jars is their adaptability in design and compatibility with automation in high-speed filling lines. The material allows for complex molding, enabling brand differentiation through unique shapes, integrated dispensing mechanisms, and tamper-evident features.

The glass jars segment is projected to register the highest CAGR of 6.8% from 2026 to 2034 due to a pronounced consumer shift toward sustainable and premium packaging, particularly in organic food and natural cosmetics. Glass is 100% recyclable without degradation in quality, a property emphasized by the European Container Glass Federation, which states that recycled glass (cullet) can reduce furnace energy consumption when used in new production. Consumers increasingly associate glass with purity and longevity. This is a perception leveraged by premium brands in artisanal foods and clean beauty. As per a study, products in glass packaging are perceived as more trustworthy than those in plastic by eco-conscious shoppers in Western Europe. Regulatory burdens on single-use plastics, particularly in developed economies, are a different factor propelling the growth of this segment. The European Union’s Single-Use Plastics Directive, formally adopted in 2019, sets a 90% separate collection target for plastic bottles by 2029

By Capacity Insights

The 10–50 OZ capacity segment led the global jars market by capturing 52.8% of the global market share in 2024. The growth of10-50OZ segment is propelled by its alignment with standard household consumption patterns for food and personal care products. Jars in this range are ideal for condiments, sauces, lotions, and supplements. It offers a balance between usability and shelf life. According to data from the U.S. Department of Agriculture (USDA) and the U.S. Census Bureau, the average American consumes approximately 4.4 pounds of peanut butter per person per year. Retailers point out that a notable share of shelf space allocated to jarred goods is occupied by containers within this capacity bracket. Furthermore, as per the study, consumer preference for bulk purchasing, driven by cost efficiency, has increased sales of mid-sized jars year-on-year in the U.S. This segment’s compatibility with standard pallet configurations and automated warehouse systems further enhances its logistical appeal.

The less than 10 OZ segment is anticipated to grow at the fastest CAGR of 7.4% from 2025 2026 to 2034 due to the rising popularity of portion-controlled packaging in health, beauty, and gourmet food sectors. Consumers increasingly seek single-serve or trial-sized products to minimize waste and experiment with new brands. According to the study, many U.S. consumers prefer smaller packaging for new food products to assess taste and quality before committing to larger sizes. In the cosmetics industry, travel-sized serums and creams in 1–8 oz jars have become essential, especially with the resurgence of global air travel. The expansion of subscription box services and sample-based marketing models, which rely heavily on sub-10-oz jars, also drives the growth of the less than 10-oz segment. Brands use small-format jars to introduce customers to premium products, which increases conversion rates, according to research.

By End Use Insights

The food & beverages segment dominated the jars market by capturing 63.5% of the global market share. The growth of the food & beverages segment is accelerated by the widespread use of jars for preserving perishable and semi-perishable food items such as jams, pickles, sauces, and baby food. Glass and plastic jars provide an excellent barrier against oxygen and moisture, preserving flavor and nutritional value over extended periods. According to the study, vacuum-sealed glass jars can extend the shelf life of acidic foods like tomato sauce by several months without refrigeration. The growing demand for plant-based and organic foods has further amplified this trend. A study found that U.S. organic food sales surged in recent years, with a notable share of products packaged in jars for authenticity and freshness retention. Retailers like Whole Foods and Trader Joe’s rely heavily on jarred formats for their private-label preserves and fermented goods.

The cosmetic & personal care segment is estimated to register the fastest CAGR of 8.1% from 2026 to 2034 due to the premiumization of skincare and the growing consumer emphasis on natural, transparent, and aesthetically pleasing packaging. Jars are widely used for creams, masks, and balms, where visibility of the product and tactile experience influence purchase decisions. These brands increasingly use glass jars to convey luxury and sustainability. As per a study, a portion of consumers in Europe associate glass packaging with higher product quality in cosmetics. Furthermore, refillable glass jars are gaining traction, with brands introducing take-back programs to reduce waste.

REGIONAL ANALYSIS

Asia-Pacific Jars Market Insights

Asia-Pacific was the top performer in the jars market in 2024 and accounted for 35.1% of the global market share in 2024. The domination of Asia Pacific in the global market is primarily driven by rapid urbanization, population growth, and expanding middle-class consumption. The region’s food processing industry is a major consumer of jars, particularly in countries like India, China, and Indonesia, where traditional pickling, sauce-making, and dairy preservation are deeply embedded in culinary culture. As per the study, Asia accounts for a notable share of global fruit and vegetable production, much of which is processed and stored in jars. China alone produces substantial tons of pickled vegetables annually, as per the study. Apart from these, the rise of domestic e-commerce platforms like Alibaba and Flipkart has accelerated the distribution of jarred specialty foods. Apart from these, online grocery sales in the region grew, with packaged foods being the top category. These factors and increasing investments in packaging infrastructure position the Asia-Pacific as the most dynamic and voluminous market for jars.

North America Jars Market Insights

North America is the second largest in the jars market and accounted for 24.1% of the global market share in 2024. The growth of North America in the global market is propelled by high consumer demand for convenience, premiumization, and sustainable packaging. The U.S. is the dominant force in the region, with a well-established food preservation culture and a robust cosmetics industry. According to the study, the U.S. imported significant tons of glass containers, primarily for food and beverage packaging, reflecting strong domestic demand. The rise of health-conscious consumers has driven growth in organic and gluten-free products. Many of which are packaged in glass jars to signal purity. As per the study, many American households purchase organic products, with jams and nut butters being the top categories. Apart from these, these socio-economic and environmental trends sustain North America’s dominance in premium and sustainable jar adoption.

Europe Jars Market Insights

Europe grew steadily in the global jars market, with strong regulatory and cultural support for sustainable packaging. The European Union’s Circular Economy Action Plan has significantly influenced the shift from plastic to glass jars, particularly in food and cosmetics. Germany, France, and Italy are major producers and consumers of glass packaging, with Germany recycling a significant share of its glass containers, according to the study. The European Commission also requires that packaging be reusable or recyclable, which pushes manufacturers toward glass and metal alternatives. Apart from these, the region’s artisanal food sector, covering olive oils, cheeses, and fermented products, relies heavily on jar packaging for authenticity. These regulatory, cultural, and economic factors strengthen Europe’s position as a leader in sustainable and high-value jar usage.

Latin America Jars Market Insights

Latin America grew steadily in the jars market with Brazil and Mexico driving demand. The region’s rich culinary traditions, such as salsa, dulce de leche, and preserved fruits, create consistent demand for glass and plastic jars. According to the research, Brazil is the world’s major producer of guava paste, with significant tons produced annually, mostly packaged in jars. Apart from these, the rise of domestic food brands and supermarket penetration has increased the use of standardized packaging. However, infrastructure limitations and economic volatility constrain growth. The region’s growing middle class and increasing health awareness are fostering demand for organic and long-shelf-life products. This shift creates opportunities for jar manufacturers to expand in both urban and emerging rural markets.

Middle East and Africa Jars Market Insights

Middle East and Africa are likely to grow in the global jars market, with South Africa, Saudi Arabia, and the UAE leading adoption. The region’s demand is driven by urbanization, rising disposable incomes, and the expansion of modern retail. According to the study, packaged food sales in the Middle East grew, fueled by expatriate populations and Western dietary influences. In South Africa, there has been a shift towards private label products due to economic burdens, an increase in online shopping since 2018, and a growing consumer demand for ethnic flavors and convenient meal solutions. Apart from these, the Gulf Cooperation Council has introduced regulations to improve food safety, encouraging the use of sealed, tamper-proof jars. However, logistical challenges and limited recycling infrastructure hinder the adoption of heavier materials like glass. Hence, the region’s growing population and retail modernization provide significant long-term potential for the jars market despite these constraints.

COMPETITIVE LANDSCAPE

The jars market is marked by intense competition driven by innovation, sustainability mandates, and shifting consumer preferences. Established players differentiate themselves through material science advancements, design customization, and circular economy integration. The Asia Pacific region has emerged as a key battleground due to rapid urbanization, growth in processed food consumption, and regulatory burden on single-use plastics. Companies are competing not only on cost and functionality but also on environmental performance, with glass and recyclable plastic formats gaining favor. Barriers to entry remain high due to capital-intensive production and logistical complexity, allowing dominant firms to leverage scale and R&D capabilities. Regional players are increasingly challenging multinationals by offering localized solutions. On the other hand, digital branding and e-commerce compatibility are becoming important competitive levers in premium and specialty segments.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global jars market include

- Berry Global Group

- Amcor plc

- Owens Illinois Group Inc.

- Graham Packaging Company

- Silgan Plastics

- Gerresheimer AG

- Alpha Packaging

- Olcott Plastics

- Cospak Ltd.

- GREAT WESTERN CONTAINERS INC.

Top Strategies Used By Key Market Participants

Key players in the jars market are deploying a range of strategic initiatives to consolidate their positions and respond to evolving market dynamics. Vertical integration enables companies to control raw material sourcing and production efficiency, which reduces dependency on external suppliers. Expansion into emerging markets, particularly in the Asia Pacific and Latin America, allows firms to tap into rising consumer demand and industrial growth. Strategic partnerships with FMCG brands facilitate the co-development of innovative, brand-specific jar designs. Investment in sustainable materials and lightweighting technologies supports compliance with environmental regulations and appeals to eco-conscious consumers. Apart from these, companies are adopting digital printing and smart packaging features to enhance shelf appeal and traceability. Mergers and acquisitions are also employed to broaden product portfolios and geographic reach. This ensures long-term competitiveness in a rapidly transforming industry.

Top Players in the Market

Ardagh Group

Ardagh Group is a global leader in metal and glass packaging, with a growing presence in the Asia Pacific jars market. The company supplies high-quality glass containers to food, beverage, and cosmetics brands across India, Southeast Asia, and Australia. Ardagh has invested in advanced glass manufacturing technologies that enhance clarity, strength, and sustainability. The company has also partnered with regional clients to develop lightweight jar designs that reduce material use and transportation emissions. Ardagh emphasizes closed-loop recycling and has collaborated with municipal waste agencies in Thailand and Malaysia to improve glass recovery. Its focus on innovation, sustainability, and localized production strengthens its integration into Asia Pacific’s evolving packaging ecosystem.

Owens-Illinois, Inc. (O-I Glass)

Owens-Illinois is a dominant force in glass container manufacturing, with extensive operations across the Asia Pacific region. The company serves major food, pharmaceutical, and beauty brands in China, Japan, and Vietnam, providing custom-engineered glass jars with high barrier properties and aesthetic appeal. O-I Glass has prioritized decarbonization by investing in furnace efficiency and increasing the use of recycled glass (cullet) in production. The company also collaborates with consumer goods giants like Unilever and Nestlé to develop 100% recyclable jar solutions. Its regional innovation centers in Shanghai and Singapore enable rapid prototyping and market-specific design, which strengthens its role as a strategic packaging partner in high-growth Asian markets.

Amcor plc

Amcor is a leading global developer of flexible and rigid plastic packaging, including a broad portfolio of plastic jars for food, healthcare, and personal care applications in the Asia Pacific region. The company has strengthened its footprint in India, South Korea, and Australia by launching recyclable, lightweight HDPE and PP jars tailored to local consumer preferences. It also partnered with major FMCG brands to launch refillable jar systems in urban retail hubs. Amcor’s investment in digital printing technology allows for high-impact branding on small-batch artisanal products, catering to the region’s booming premium food and clean beauty sectors. Its integrated supply chain and sustainability initiatives position it as a forward-looking leader in the evolving jars landscape.

MARKET SEGMENTATION

This global jars market research report is segmented and sub-segmented into the following categories.

By Material Type

- Plastic Jars

- Polypropylene (PP)

- Polyethylene (PE)

- Polyethylene Terephthalate (PET)

- Polystyrene (PS)

- Others (PVC, EVOH)

- Glass Jars

- Metal Jars

- Paper Jars

By Capacity

- Less than 10 OZ

- 10-50 OZ

- More than 50 OZ

By End Use

- Food & Beverages

- Pharmaceuticals

- Cosmetic & Personal Care

- Homecare

- Oil & Lubricants

- Chemical & Fertilizers

By Region

- North America

- Europe

- Asia-Pacific

- Middle East Africa

- Latin America

Frequently Asked Questions

1. What is the Jars Market?

The Jars Market covers the production, distribution, and innovation in glass, plastic, metal, and specialty jars, serving the food, beverage, cosmetics, pharmaceuticals, and personal care industries globally

2. What segments are included in the Jars Market?

Major segments are by material (glass, plastic, metal, paper), by capacity (below 10 oz, 10–50 oz, above 50 oz), and by end use (food & beverage, pharmaceuticals, cosmetics & personal care, homecare, oils, chemicals)

3. Who are the top end-users in the Jars Market?

Food and beverage, cosmetics and personal care, pharmaceuticals, and homecare are the largest users of jars, fueled by consumer and regulatory demands for quality packaging

4. How is sustainability driving the Jars Market?

Strong focus on recyclable, BPA-free, refillable, and biodegradable jar solutions is driven by regulatory measures, environmental advocacy, and consumer preference for green packaging

5. Which regions are growing fastest in the Jars Market?

Asia-Pacific (China, Japan, South Korea), North America (USA), and Europe (Germany, France, UK, Italy) show robust growth in jars market adoption and innovation

6. What are the key trends in cosmetic jar packaging?

The cosmetic jars market is projected to reach USD 7.2 billion by 2035, with premium beauty, organic skincare, and refillable sustainable packaging shaping industry growth

7. How does the food and beverage industry impact the Jars Market?

Growing preferences for glass and BPA-free jars in organic, artisanal, and convenience food drive segment expansion; fresh designs and vacuum-sealing enhance product shelf-life

8. What impact do government regulations have on the Jars Market?

Stricter regulations against single-use plastics and mandates for recycling and green packaging are accelerating market transformation and innovation in packaging materials

9. Which materials are most popular in the Jars Market?

Plastic jars (PET, PP, PE) dominate due to cost efficiency and versatility, while glass jars appeal for sustainability, premium positioning, and health safety

10. What innovations are emerging in the Jars Market?

UV-protected, shatter-resistant, lightweight, multi-layered, vacuum-sealed, and smart-labeled jars are enhancing product safety, quality, and traceability

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com