Global Kefir Market Size, Share, Trends & Growth Forecast Report - Segmented By Composition (Water Kefir And Milk Kefir), Type, and Region (North America, Europe, Asia Pacific, Latin America, Middle East And Africa) – Industry Analysis 2026 to 2034

Global Kefir Market Report Summary

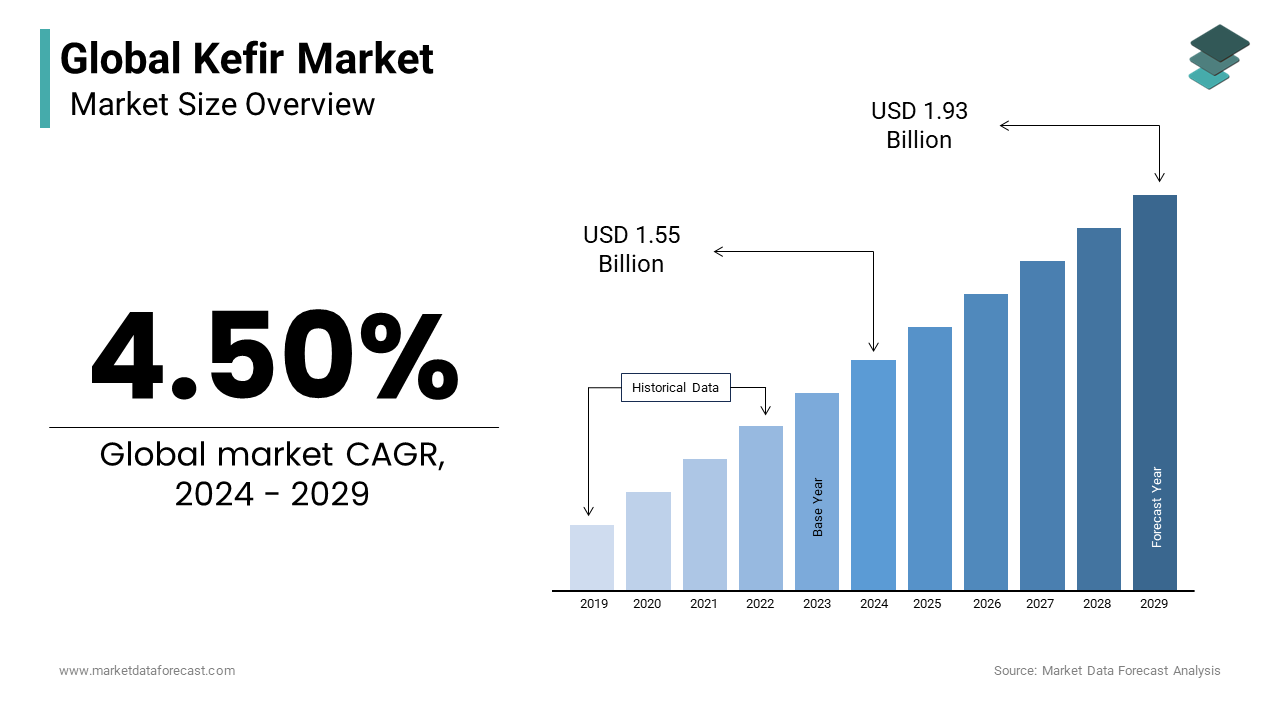

The global kefir market was valued at USD 1.62 billion in 2025, is estimated to reach USD 1.69 billion in 2026, and is projected to reach USD 2.41 billion by 2034, growing at a CAGR of 4.53% during the forecast period. Market growth is driven by increasing consumer awareness regarding gut health, rising demand for probiotic beverages, and growing preference for functional dairy products. Kefir is widely consumed due to its probiotic benefits, nutritional value, and digestive health support. The expanding trend toward natural and fermented food products is further supporting steady market growth globally.

Key Market Trends

- Rising consumer awareness regarding digestive and gut health is driving market growth.

- Increasing demand for probiotic and functional beverages is boosting kefir consumption.

- Growing preference for organic and natural dairy products is supporting market expansion.

- Expansion of health conscious consumer trends is enhancing product adoption.

- Innovation in flavored, plant based, and functional kefir products is influencing market development.

Segmental Insights

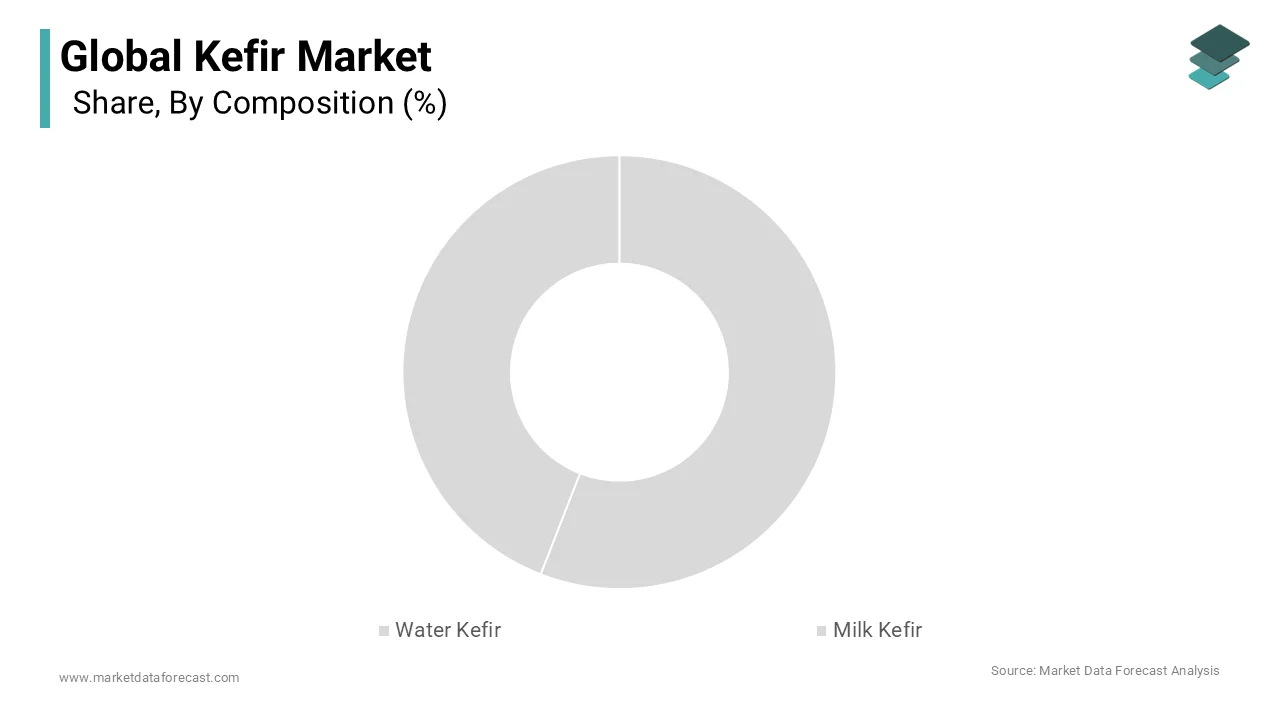

- Based on composition, the milk kefir segment held the leading share of the global kefir market in 2025. This dominance is attributed to widespread consumer familiarity and strong nutritional benefits associated with dairy based kefir products.

- Based on type, the organic kefir segment dominated the global kefir market in 2025, driven by rising demand for clean label and organic food products.

- Based on distribution channel, the supermarkets and hypermarkets segment held the highest share of the global kefir market in 2025, supported by extensive retail availability and organized distribution networks.

Regional Insights

- The global kefir market is experiencing steady growth across regions, supported by rising health consciousness and increasing probiotic product consumption.

- Europe was the leading regional market in 2025, driven by kefir’s historical roots in Eastern European cultures, strong consumer awareness regarding fermented foods, and growing demand for functional dairy beverages.

Competitive Landscape

The global kefir market is moderately competitive, with key players focusing on probiotic innovation, organic product development, and expansion of retail distribution channels to strengthen their market position. Companies are investing in flavored variants, plant based alternatives, and functional beverage formulations. Prominent players in the global kefir market include Lifeway Foods Inc, The Greek Gods, Helios Ingredients, Fresh Made Inc, Groupe Danone, Krasnystaw OSM, Nestle SA, Danisco, Danlac Canada Inc, and The KEFIR Company.

Global Kefir Market Size

The global kefir market size was valued at USD 1.62 billion in 2025, and the global market size is expected to reach USD 1.69 billion in 2026 to USD 2.41 billion by 2034 with a CAGR of 4.53% throughout the forecast period 2026 to 2034.

Kefir represents a traditional fermented milk beverage characterized by its unique symbiotic culture of bacteria and yeast. This probiotic drink has transcended its Caucasian origins to become a staple in European dietary habits due to its perceived health benefits. The product is distinct from yogurt due to its liquid consistency and broader spectrum of microbial diversity. Consumers increasingly view kefir as a functional food that supports digestive health and immune system regulation. The European landscape for this beverage is shaped by a growing consciousness regarding gut health and natural food sources. As per the European Food Safety Authority, the recognition of specific health claims related to probiotics remains a critical regulatory framework influencing product labeling and marketing strategies across the region. The demographic shift towards an aging population in Europe further amplifies the demand for foods that support overall wellness. According to Eurostat, the proportion of individuals aged 65 and older in the European Union reached 21.3% in 2023. This demographic trend underscores the importance of nutrient dense and easily digestible food options. Furthermore, the rise in lactose intolerance awareness has prompted manufacturers to innovate with lactose free variants. The cultural integration of kefir into mainstream retail channels reflects its transition from a niche ethnic product to a widely accepted dietary supplement. The market dynamics are thus influenced by both traditional consumption patterns and modern health trends.

MARKET DRIVERS

Rising Prevalence of Gastrointestinal Disorders Drives Demand

The increasing incidence of gastrointestinal disorders across Europe is majorly fuelling the expansion of the global kefir market. Modern lifestyles characterized by high stress levels and poor dietary choices have contributed to a surge in digestive issues among the population. According to the World Gastroenterology Organisation, functional gastrointestinal disorders affect approximately 40% of the global population, with significant prevalence in developed regions such as Europe. Consumers are actively seeking natural remedies to alleviate symptoms such as bloating, irregularity, and discomfort. Kefir, rich in diverse probiotic strains, offers a viable solution by restoring gut microbiota balance. The scientific community has extensively documented the efficacy of fermented dairy products in improving digestive health. As per a study published in the Journal of Clinical Gastroenterology, regular consumption of probiotic enriched beverages can significantly reduce the severity of irritable bowel syndrome symptoms. Additionally, the rising awareness of the gut brain axis has linked digestive health to mental well-being, which is further motivating consumers to incorporate probiotics into their daily routines. Healthcare professionals increasingly recommend dietary interventions over pharmaceutical solutions for mild digestive ailments. This shift in medical advice encourages patients to explore functional foods like kefir. The convenience of ready to drink formats aligns with the busy schedules of urban populations who seek effective yet easy health solutions.

Growing Consumer Preference for Natural and Clean Label Products

The shifting consumer preference towards natural and clean label products significantly propels the growth of the kefir market in Europe. Modern shoppers are increasingly scrutinizing ingredient lists and avoiding artificial additives, preservatives, and synthetic flavors. This trend is driven by a desire for transparency and authenticity in food production. According to a survey conducted by the International Food Information Council, 71% of consumers consider the presence of natural ingredients as a crucial factor when making purchasing decisions. Kefir inherently aligns with this preference as it is traditionally made from just milk and kefir grains, requiring no additional chemical enhancers. The simplicity of its composition appeals to health conscious individuals who prioritize minimally processed foods. Furthermore, the organic segment within the dairy industry has witnessed substantial growth, reflecting this broader trend. As per data from the Research Institute of Organic Agriculture, the European organic market continued to expand, with dairy products representing a significant share of sales. Manufacturers are responding by launching organic kefir variants that cater to this discerning customer base. The perception of kefir as a wholesome and traditional beverage reinforces its image as a trustworthy choice. Retailers are also prioritizing shelf space for brands that emphasize clean labeling and sustainable sourcing practices. This alignment with contemporary values ensures that kefir remains relevant in a competitive beverage landscape. The emphasis on natural fermentation processes distinguishes kefir from other fortified drinks, thereby attracting consumers who seek genuine nutritional benefits without artificial intervention.

MARKET RESTRAINTS

Stringent Regulatory Frameworks for Health Claims Impede Growth

Stringent regulatory frameworks governing health claims pose a significant restraint to the kefir market in Europe. The European Food Safety Authority maintains rigorous standards for approving probiotic health claims, which limits the ability of manufacturers to communicate specific benefits to consumers. According to the European Commission, only a limited number of health claims related to probiotics have been authorized, leaving many companies unable to highlight the digestive or immune boosting properties of their products on packaging. This regulatory ambiguity creates confusion among consumers who may not fully understand the benefits of kefir without clear labeling. The lack of approved claims restricts marketing strategies and reduces the competitive advantage of premium kefir brands. Furthermore, the classification of kefir as either a food or a supplement varies across different European countries, leading to inconsistent labeling requirements. As per the European Dairy Association, navigating these disparate regulations increases compliance costs and operational complexity for multinational producers. Small and medium sized enterprises often struggle to meet these regulatory demands, limiting market entry and innovation. The inability to make explicit health statements also hinders educational efforts aimed at new consumers who are unfamiliar with fermented dairy products. The ongoing debate regarding the scientific substantiation of probiotic benefits further delays the approval of new claims, perpetuating uncertainty in the market.

High Sensitivity to Temperature and Short Shelf Life Constraints Distribution

The high sensitivity of kefir to temperature fluctuations and its relatively short shelf life present substantial challenges to the expansion of the global kefir market. As a live fermented product, kefir requires consistent cold chain management to maintain its probiotic viability and prevent spoilage. According to the Cold Chain Federation, maintaining uninterrupted temperature control during logistics is a complex and costly endeavor, particularly for perishable dairy items. Any deviation from the recommended storage conditions can lead to product degradation, resulting in financial losses for retailers and manufacturers. This requirement limits the availability of kefir to regions with robust refrigeration infrastructure, excluding remote or less developed areas. Furthermore, the short shelf life necessitates frequent restocking and efficient inventory management to minimize waste. As per the Waste and Resources Action Programme, food waste in the dairy sector remains a significant concern, with perishable products contributing disproportionately to landfill volumes. Retailers are often hesitant to allocate extensive shelf space to products with high spoilage risks, thereby restricting market penetration. The logistical complexities also increase the final retail price, making kefir less accessible to price sensitive consumers. Additionally, the environmental impact of cold chain logistics contradicts the sustainability goals of many modern brands. Companies face pressure to reduce carbon footprints while ensuring product quality, creating a delicate balance. These operational hurdles constrain the scalability of kefir brands and limit their ability to compete with shelf stable beverages that offer greater convenience and lower distribution costs.

MARKET OPPORTUNITIES

Expansion into Plant Based and Vegan Kefir Variants Offers Growth Potential

The expansion into plant based and vegan kefir variants presents a lucrative opportunity for market players in Europe. The rising adoption of vegetarian and vegan diets has created a demand for non dairy alternatives that offer similar health benefits to traditional kefir. According to ProVeg International, the number of vegans in Europe has increased significantly, reaching approximately 2.6 million people in 2023. Manufacturers are responding by developing kefir products using coconut water, almond milk, oat milk, and other plant bases. These alternatives appeal to consumers who are lactose intolerant or ethically opposed to animal derived products. The versatility of plant based substrates allows for innovation in flavor profiles and nutritional enhancements. As per the Good Food Institute Europe, investment in alternative protein and dairy sectors reached over 2.5 billion dollars in 2022, indicating strong market confidence in these categories. Plant based kefirs often incorporate additional functional ingredients such as prebiotic fibers and vitamins, enhancing their value proposition. This diversification enables brands to tap into new customer segments that were previously excluded from the traditional dairy kefir market. Retailers are increasingly dedicating shelf space to plant based options, reflecting consumer demand. The alignment with sustainability trends further boosts the appeal of these products, as plant based generally have a lower environmental impact than dairy. By leveraging existing fermentation expertise, companies can efficiently expand their product portfolios. This strategic move not only broadens market reach but also future proofs brands against declining dairy consumption trends.

Integration of Kefir into Functional Food and Beverage Innovations

The integration of kefir into broader functional food and beverage innovations offers significant opportunities for market expansion. Manufacturers are exploring ways to incorporate kefir cultures into diverse product formats such as smoothies, salad dressings, and even baked goods. This approach transforms kefir from a standalone beverage into a versatile ingredient that enhances the nutritional profile of various foods. According to Innova Market Insights, 1 in 3 consumers globally say they have increased their intake of functional foods in 2023. By embedding kefir into everyday items, companies can increase consumption frequency and reach consumers who may not traditionally drink kefir. The development of kefir based snacks addresses the demand for on the go nutrition without compromising health goals. As per the European Snacks Association, the healthy snacking segment is experiencing robust growth, driven by health conscious millennials and Gen Z consumers. These demographics prioritize products that support active lifestyles and mental clarity. Collaborations between kefir producers and food technologists enable the creation of novel textures and flavors that appeal to adventurous palates. Furthermore, the use of kefir in culinary applications promotes cultural acceptance and normalizes its presence in daily diets. Educational campaigns highlighting recipe ideas can further stimulate demand. This strategic diversification reduces reliance on single product sales and mitigates market volatility. By positioning kefir as a foundational element of a healthy diet, brands can establish deeper connections with consumers and drive long term loyalty.

MARKET CHALLENGES

Intense Competition from Established Probiotic Yogurts and Supplements

Intense competition from established probiotic yogurts and dietary supplements is one of the major challenges to the expansion of the kefir market globally. Yogurt enjoys a dominant position in the European dairy sector, with widespread consumer familiarity and extensive distribution networks. According to the European Dairy Association, yogurt remains one of the most consumed dairy products, with the average European consuming approximately 20 kg of yogurt per year. Consumers often perceive yogurt as a sufficient source of probiotics, reducing the incentive to switch to kefir. Additionally, the supplement market offers concentrated probiotic capsules and powders that appeal to individuals seeking targeted health interventions without dietary changes. As per the Council for Responsible Nutrition, roughly 74% of U.S. adults take dietary supplements, with probiotics representing a major category. These alternatives often provide higher colony forming units per dose, which attracts serious health enthusiasts. Kefir brands struggle to differentiate themselves in a crowded marketplace where shelf space is limited. The price premium associated with kefir compared to standard yogurt further complicates consumer decision making. Marketing budgets for kefir are typically smaller than those of major yogurt conglomerates, limiting brand visibility. Educating consumers about the unique benefits of kefir, such as its yeast content and broader bacterial diversity, requires sustained effort and resources. Competitors also rapidly innovate, launching improved yogurt formulations that mimic the benefits of kefir. These dynamic environment forces kefir producers to constantly innovate while battling entrenched market leaders.

Inconsistency in Taste and Texture Due to Natural Fermentation

Inconsistency in taste and texture due to the natural fermentation process presents a notable challenge for kefir manufacturers. Unlike standardized industrial products, kefir relies on live cultures that can vary in activity based on temperature, time, and raw material quality. This variability can lead to differences in acidity, carbonation, and viscosity between batches. According to the International Dairy Federation, maintaining consistent sensory attributes in fermented products is a technical challenge that requires precise control measures. Consumers accustomed to uniform tastes in commercial beverages may find these variations unsettling, potentially leading to brand switching. The slight effervescence and tangy flavor of kefir, while appreciated by enthusiasts, can be off putting to first time users who expect a milder profile. As per consumer feedback analysis by Mintel, 57% of consumers consider taste the most important factor when purchasing healthy beverages. Manufacturers must invest in advanced quality control systems to minimize batch to batch differences, which increases production costs. Furthermore, the separation of whey and curds during storage can affect visual appeal, requiring consumers to shake the product before consumption. This extra step may be perceived as inconvenient compared to ready to drink alternatives. Educating consumers about the natural nature of these variations is essential but difficult to achieve at scale. Brands that fail to manage these sensory expectations risk negative reviews and reduced customer retention. Ensuring a balanced profile that appeals to mass markets while retaining authentic characteristics remains a delicate operational hurdle.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.53% |

| Segments Covered | By Type, Composition, Flavour, Distribution Channel And Region |

| Various Analyses Covered | Global, Regional and Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Lifeway Foods Inc, The Greek Gods, Helios Ingredients, Fresh Made Inc, Groupe Danone, Krasnystaw OSM, Nestle SA, Danisco, Danlac Canada Inc, The KEFIR Company. |

SEGMENTAL ANALYSIS

By Composition Insights

The milk kefir segment led the market by accounting for the highest share of the global market in 2025. The dominance of milk kefir segment in the global market is primarily attributed to its deep rooted integration into traditional dairy consumption habits across Europe and North America. The segment benefits from a well-established supply chain and high consumer familiarity with fermented milk products. According to the International Dairy Federation, milk based fermented products account for over 60% of the global fermented dairy market, providing a robust foundation for milk kefir sales. Consumers perceive milk kefir as a direct alternative to yogurt and buttermilk, making it an easy substitution in daily diets. The rich nutritional profile of milk kefir, including high calcium and protein content, aligns with dietary recommendations for bone health and muscle maintenance. As per the European Food Safety Authority, dairy products remain a primary source of essential nutrients for the European population, reinforcing the demand for milk based variants. Furthermore, the availability of diverse fat contents such as whole, semi skimmed, and skimmed options cater to varied consumer preferences. Major dairy corporations have leveraged their existing infrastructure to produce and distribute milk kefir efficiently, ensuring widespread availability. The cultural acceptance of cow milk in Western societies further solidifies the dominance of this segment. Manufacturers continue to innovate within the milk kefir category by adding fruits and flavors, which enhances appeal without altering the core product identity. This strategic alignment with traditional dietary patterns ensures that milk kefir remains the preferred choice for the majority of consumers seeking probiotic benefits.

On the other hand, the water kefir segment is emerging as the fastest growing segment in the kefir market and is expected to exhibit a promising CAGR in the global market during the forecast period owing to the rising demand for plant based and lactose free beverages. This non-dairy alternative appeals to vegans, individuals with lactose intolerance, and health conscious consumers seeking lower calorie options. According to ProVeg International, the plant based food market in Europe reached 5.7 billion euros in 2022, reflecting a significant shift in consumer preferences. Water kefir, made from sugar water and fruit juices, offers a refreshing and light alternative to heavy dairy products. The segment benefits from the broader trend of reducing animal product consumption, which is particularly strong among younger demographics. As per the Good Food Institute, retail sales of plant based milk grew 9% in 2022, indicating strong market confidence in non dairy innovations. Water kefir also aligns with the clean label movement, as it typically contains fewer ingredients and no artificial additives. The versatility of water kefir allows for creative flavor combinations using natural fruits and herbs, attracting adventurous consumers. Additionally, the lower sugar content in many water kefir formulations compared to soft drinks makes it an attractive option for those monitoring their sugar intake. Retailers are increasingly stocking water kefir alongside other functional beverages, enhancing its visibility. The combination of health benefits, ethical considerations, and taste variety positions water kefir for sustained rapid expansion in the global market.

By Type Insights

The organic kefir segment dominated the market by holding the leading share of the global market in 2025 due to the increasing consumer preference for organic and chemical free food products. Shoppers are becoming more discerning about the origin and production methods of their food, prioritizing items that are free from synthetic pesticides and hormones. According to the Research Institute of Organic Agriculture, the European organic market has continued to expand, reaching approximately 54.3 billion euros in 2022. Organic kefir appeals to health conscious individuals who believe that organic farming practices result in higher nutritional value and better taste. The certification of organic status provides a trust signal that reassures consumers about the quality and safety of the product. As per the Soil Association, sales of organic dairy products in the UK grew by 1.1% in 2023, indicating strong consumer loyalty. Parents are particularly inclined to choose organic kefir for their children, seeking to minimize exposure to potential contaminants. The premium pricing of organic kefir is accepted by consumers who view it as an investment in their long term health. Retailers support this segment by dedicating specific shelf space to organic products, enhancing their visibility. The alignment with sustainability goals also attracts environmentally conscious buyers who prefer farming methods that protect biodiversity. This strong consumer demand for transparency and purity ensures that organic kefir maintains its dominant position in the market.

However, the low fat kefir segment is estimated to register a promising CAGR in the global market during the forecast period due to the rising prevalence of obesity and cardiovascular diseases. Consumers are actively seeking healthier alternatives that provide probiotic benefits without the high saturated fat content associated with full fat dairy. According to the World Health Organization, more than 1 billion people worldwide are living with obesity as of 2022, prompting a global shift towards low calorie and low fat dietary choices. Low fat kefir offers a solution by delivering essential nutrients and probiotics while supporting weight management goals. The segment appeals to individuals following specific dietary plans such as the DASH diet or Mediterranean diet, which emphasize reduced fat intake. As per the American Heart Association, keeping saturated fat intake to less than 6% of daily calories is recommended for heart health, influencing consumer purchasing decisions. Manufacturers have improved the texture and taste of low fat kefir through advanced processing techniques, addressing previous concerns about thin consistency or bland flavor. The availability of flavored low fat options further enhances its appeal to a broader audience. Fitness enthusiasts and athletes also prefer low fat kefir for post workout recovery due to its high protein and low fat profile. The growing awareness of the link between diet and chronic diseases drives the adoption of low fat variants. This health driven demand ensures that low fat kefir continues to experience robust growth rates in the global market.

By Distribution Channel Insights

The supermarkets and hypermarkets segment held the highest share of the global market in 2025. The growth of supermarkets and hypermarkets segment in the global market can be credited to their extensive reach and ability to offer a wide variety of brands and flavors. These retail formats provide consumers with the convenience of one stop shopping, allowing them to purchase kefir alongside other grocery items. According to Eurostat, supermarkets and hypermarkets account for nearly 80% of food retail sales in several European countries, reflecting their central role in consumer purchasing behavior. The large shelf space in these stores enables manufacturers to display multiple SKUs, including different flavors, sizes, and types of kefir. Promotional activities such as discounts and bundle offers are frequently implemented in supermarkets, attracting price sensitive consumers. As per NielsenIQ, 60% of shoppers are influenced by in store promotions when choosing dairy products. The cold chain infrastructure in supermarkets ensures that kefir is stored at optimal temperatures, maintaining product quality and safety. Consumers trust these established retail channels for fresh dairy products, leading to higher footfall and repeat purchases. The presence of private label kefir brands in supermarkets also offers affordable options, broadening the customer base. The ability to physically inspect products before purchase further enhances consumer confidence. This combination of convenience, variety, and trust solidifies the dominance of supermarkets and hypermarkets in the kefir distribution landscape.

However, the online retailers segment is on the rise and is predicted to expand at a healthy CAGR in the global market during the forecast period owing to the increasing adoption of e commerce and the convenience of home delivery. The pandemic accelerated the shift towards online grocery shopping, a trend that has persisted as consumers value time saving solutions. According to Statista, the global online grocery market is projected to reach 1.1 trillion dollars by 2027. Online retailers offer the advantage of subscription services, allowing customers to receive regular deliveries of kefir without the need for frequent store visits. This model ensures consistent consumption and builds brand loyalty. As per McKinsey and Company, roughly 45% of consumers have used a grocery delivery service in the last year. The ability to access niche and artisanal kefir brands that may not be available in local stores also drives online sales. Detailed product descriptions and customer reviews help consumers make informed decisions, reducing the perceived risk of buying perishable items online. Improved logistics and cold chain delivery solutions have addressed previous concerns about product freshness during transit. Social media marketing and influencer collaborations often direct consumers to online platforms, which is further boosting sales. The seamless integration of digital payment and fast delivery options makes online retail an attractive channel for modern consumers, ensuring its rapid expansion.

REGIONAL ANALYSIS

Europe Kefir Market Analysis

Europe stands as the largest regional market for kefir, driven by its historical roots in Eastern European cultures and widespread health consciousness. The region benefits from a long standing tradition of consuming fermented dairy products, which has facilitated the mainstream adoption of kefir. According to the European Dairy Association, the demand for functional dairy products continues to rise, with the market for fermented milks growing steadily in Western Europe. Countries such as Russia, Poland, and Germany have high per capita consumption rates, reflecting deep cultural integration. The presence of major dairy companies in Europe ensures robust production and distribution networks. As per Eurostat, the number of health conscious consumers in the EU increased by 15% between 2019 and 2023. Regulatory support for healthy eating initiatives also contributes to market growth. The availability of organic and lactose free variants caters to diverse consumer needs. Retailers in Europe prioritize shelf space for probiotic products, enhancing visibility. The strong emphasis on quality and safety standards in the European Union builds consumer trust. Innovation in flavors and packaging keeps the product relevant to younger demographics. The combination of traditional acceptance and modern health trends ensures that Europe remains the dominant force in the global kefir market.

North America Kefir Market Analysis

North America captured a promising share of the global kefir market in 2025. The United States and Canada are expected to see a significant surge in probiotic beverage adoption as gut health becomes a mainstream wellness priority over the next few years. North America represents a significant and rapidly growing market for kefir, propelled by the rising interest in functional foods and gut health. The United States and Canada are witnessing increased adoption of kefir as consumers become more educated about the benefits of probiotics. According to the International Food Information Council, 74% of U.S. consumers are trying to consume probiotics as of 2023. Kefir fits this criterion perfectly, offering a convenient source of beneficial bacteria. The presence of key market players in North America drives innovation and marketing efforts. As per the USDA, sales of yogurt and fermented dairy reached 8.2 billion dollars in the U.S. in 2022. The influence of social media and health influencers has raised awareness about kefir among millennials and Gen Z. Retailers are expanding their offerings to include various flavors and plant based options. The high disposable income in the region allows consumers to purchase premium kefir products. Educational campaigns by healthcare professionals further validate the health claims associated with kefir. The integration of kefir into smoothies and other culinary applications broadens its appeal. The strong retail infrastructure ensures wide availability across urban and rural areas. This dynamic environment supports sustained growth in the North American kefir market.

Asia Pacific Kefir Market Analysis

Asia Pacific emerges as a high potential market due to rising disposable incomes. Major economies in the Asia Pacific region are anticipated to drive the next wave of global kefir demand as urbanization and middle class spending power continue to climb. The Asia Pacific region is emerging as a high potential market for kefir, driven by rising disposable incomes and increasing health awareness. Countries such as China, Japan, and Australia are experiencing a shift towards Western dietary habits, including the consumption of dairy products. According to the Food and Agriculture Organization, milk production in Asia increased to 401 million tonnes in 2022, creating opportunities for fermented products. The growing middle class is willing to spend on premium health foods, including kefir. As per Euromonitor International, the health and wellness market in China was valued at over 100 billion dollars in 2023. Local manufacturers are adapting kefir recipes to suit regional tastes, incorporating familiar flavors. The rising prevalence of lifestyle diseases is prompting consumers to seek preventive health solutions. Government initiatives promoting healthy eating also contribute to market growth. E commerce platforms are facilitating access to kefir in remote areas. The young population in the region is open to trying new food trends, driving trial and adoption. Collaborations with local distributors help international brands penetrate the market. The combination of economic growth and health consciousness positions Asia Pacific as a key growth engine for the global kefir market.

Latin America Kefir Market Analysis

Latin America displays moderate growth due to cultural affinity for dairy. Brazil and Argentina are likely to experience steady growth in functional dairy segments as domestic production capabilities for fermented beverages modernize through 2028. Latin America displays moderate growth in the kefir market, supported by a cultural affinity for dairy products and increasing urbanization. Countries such as Brazil and Argentina have strong dairy traditions, which provide a favorable environment for kefir adoption. According to the Inter American Institute for Cooperation on Agriculture, dairy remains a vital sector in Latin America with production reaching 80 billion liters annually. Consumers are becoming more aware of the health benefits of fermented foods, driving demand for kefir. As per Statista, the health and wellness food market in Brazil was valued at approximately 18 billion dollars in 2022. Local producers are introducing kefir variants that cater to local preferences, such as tropical fruit flavors. The expansion of supermarket chains improves access to kefir in urban centers. Economic challenges in some countries may limit premium product sales, but basic kefir remains accessible. Educational efforts by nutritionists are slowly building consumer knowledge.

COMPETITIVE LANDSCAPE

The competition in the kefir market is characterized by a mix of established dairy giants and agile niche producers vying for consumer attention. Large multinational corporations leverage their extensive distribution networks and substantial marketing budgets to dominate shelf space in major retail outlets. These entities often compete on brand recognition and product consistency while investing in scientific research to substantiate health claims. Smaller artisanal brands differentiate themselves through unique flavor profiles organic certifications and local sourcing practices. They appeal to discerning consumers who prioritize transparency and sustainability. The barrier to entry remains moderate due to the specialized fermentation process required for quality production. Price competition is evident in the standard segment while premium products command higher margins through value added features. Innovation plays a crucial role as companies introduce plant based alternatives and functional ingredients to capture diverse demographic segments. Strategic alliances with retailers and online platforms further intensify rivalry. The market sees frequent product launches and promotional activities aimed at educating consumers. This dynamic environment fosters continuous improvement in product quality and accessibility driving overall market expansion.

KEY MARKET PLAYERS

Some of the key players in kefir market are

- Lifeway Foods Inc

- The Greek Gods

- Helios Ingredients

- Fresh Made Inc

- Groupe Danone

- Krasnystaw OSM

- Nestle SA

- Danisco

- Danlac Canada Inc

- The KEFIR Company

Top Players in the Market

- Lifeway Foods Inc stands as a prominent figure in the global kefir landscape with its extensive distribution network across North America and Europe. The company focuses exclusively on fermented dairy products and has pioneered the mainstream availability of kefir in retail channels. Lifeway Foods continuously innovates by launching new flavors and functional variants such as probiotic sparkling waters to diversify its portfolio. Recent actions include expanding production capacity to meet rising demand and enhancing sustainability initiatives within its supply chain. The company actively engages in educational campaigns to inform consumers about gut health benefits. By leveraging strong relationships with major grocery chains and online retailers, Lifeway Foods ensures high product visibility. Their commitment to quality and consistent branding reinforces consumer trust. The introduction of organic and low sugar options aligns with current health trends. These strategic moves solidify their position as a key influencer in the fermented beverage sector.

- Danone S.A. leverages its vast global infrastructure to promote kefir through its diverse brand portfolio including Actimel and other fermented milk drinks. The French multinational emphasizes scientific research to validate health claims associated with its probiotic products. Danone invests heavily in marketing campaigns that highlight digestive wellness and immune support. Recent strategies involve acquiring local kefir brands in emerging markets to strengthen regional presence. The company prioritizes sustainable packaging solutions to appeal to environmentally conscious consumers. Danone collaborates with healthcare professionals to endorse its products as part of a balanced diet. Their robust distribution network ensures widespread availability in supermarkets and convenience stores globally. Innovation in plant based alternatives allows Danone to cater to vegan demographics. The integration of digital tools for customer engagement enhances brand loyalty. These efforts demonstrate Danone's commitment to maintaining leadership in the functional dairy segment.

- Yakult Honsha Co. Ltd. is renowned for its specialized focus on probiotic beverages and maintains a strong presence in Asia and expanding globally. The company utilizes a unique direct sales model alongside traditional retail channels to reach consumers effectively. Yakult emphasizes the scientific backing of its proprietary Lactobacillus casei Shirota strain. Recent actions include expanding manufacturing facilities in Europe and North America to reduce logistical costs. The company launches targeted marketing campaigns to educate consumers on the importance of daily probiotic intake. Yakult also explores partnerships with fitness and wellness centers to promote healthy lifestyles. Their commitment to product consistency and quality control builds long term consumer trust. The introduction of smaller pack sizes caters to on the go consumption trends. Yakult continues to invest in research to discover new health benefits. These initiatives reinforce its reputation as a trusted provider of probiotic solutions worldwide.

Top Strategies Used by the Key Market Participants

Key players in the kefir market primarily employ product innovation and strategic partnerships to strengthen their competitive position. Companies frequently launch new flavors and functional variants such as low sugar or plant based options to cater to evolving consumer preferences. Expansion into emerging markets through localized production facilities helps reduce costs and improve supply chain efficiency. Brands invest heavily in digital marketing and educational campaigns to raise awareness about gut health benefits. Collaborations with healthcare professionals and influencers enhance credibility and reach. Sustainability initiatives including eco friendly packaging are increasingly adopted to appeal to environmentally conscious buyers. Mergers and acquisitions allow larger corporations to integrate niche brands and broaden their product portfolios. Retailers prioritize shelf space for premium and organic kefir products to attract high value customers. Subscription models via online platforms ensure recurring revenue and customer loyalty. These strategies collectively drive growth and maintain market relevance in a dynamic industry landscape.

Global Kefir Market News

- In March 2023, Lifeway Foods Inc launched a new line of organic kefir smoothies to expand its product portfolio and strengthen the Kefir Market presence

- In June 2023, Danone S.A. acquired a minority stake in a plant based fermentation startup to innovate alternative dairy options and strengthen the Kefir Market presence

- In September 2023, Yakult Honsha Co. Ltd. opened a new manufacturing facility in Poland to enhance European distribution capabilities and strengthen the Kefir Market presence

- In January 2024, Lifeway Foods Inc introduced a subscription service for direct to consumer delivery to improve customer retention and strengthen the Kefir Market presence

- In May 2024, Danone S.A. partnered with a major online grocery platform to increase digital visibility and accessibility of its probiotic drinks and strengthen the Kefir Market presence

MARKET SEGMENTATION

This research report on the global kefir market has been segmented and sub-segmented based on composition, type, flavour, distribution channel & region.

By Composition

- Water Kefir

- Milk Kefir

By Type

- Greek Type Kefir

- Frozen Kefir

- Organic Kefir

- Low fat Kefir

- Others

By Flavour

- Regular Kefir

- Flavoured Kefir

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Grocery Stores

- Online Retailers

- Others

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1.What is the kefir market?

The kefir market includes the production, distribution, and consumption of kefir, a fermented dairy and non-dairy beverage rich in probiotics and nutrients.

2.What factors are driving growth in the kefir market?

Market growth is driven by increasing health and wellness awareness, rising demand for probiotic foods, and expanding functional beverage consumption.

3.What types of kefir products are available in the market?

Common types include dairy kefir, water kefir, and plant-based kefir made from almond, soy, coconut, or oat milk.

4.How are kefir products used by consumers?

Kefir is consumed as a drink, used in smoothies, breakfast bowls, and as a probiotic supplement for digestive health.

5.What are the health benefits associated with kefir?

Kefir is known for digestive support, immune system enhancement, nutrient supply, and probiotic benefits that help maintain gut health.

6.Which regions are major markets for kefir?

North America, Europe, and Asia Pacific are major markets due to growing health consciousness and expanding retail availability.

7.What are the key distribution channels for kefir products?

Major distribution channels include supermarkets, health food stores, specialty beverage outlets, and online retail platforms.

8.How do consumer trends influence the kefir market?

Trends such as clean label, plant-based diets, gut health focus, and functional foods boost demand for kefir products.

9.Who are the key players in the kefir market?

Key players include Lifeway Foods, Danone, Nestlé, Yakult, and local dairy and beverage producers.

10.What challenges does the kefir market face?

Challenges include product perishability, cold chain logistics, consumer education, and competition from other fermented beverages.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com