Latin America Pharmaceutical Market Size, Share, Trends & Growth Forecast Report By Molecule Type (Biologics & Biosimilars [Monoclonal Antibodies, Vaccines, Cell & Gene Therapy, Others], Conventional Drugs), Product (Branded, Generics), Type (Prescription, OTC), Disease, Age Group, Distribution Channel, and Country (Brazil, Mexico, Argentina, Chile, Rest of Latin America) – Industry Analysis, 2026 to 2034

Latin America Pharmaceutical Market Size

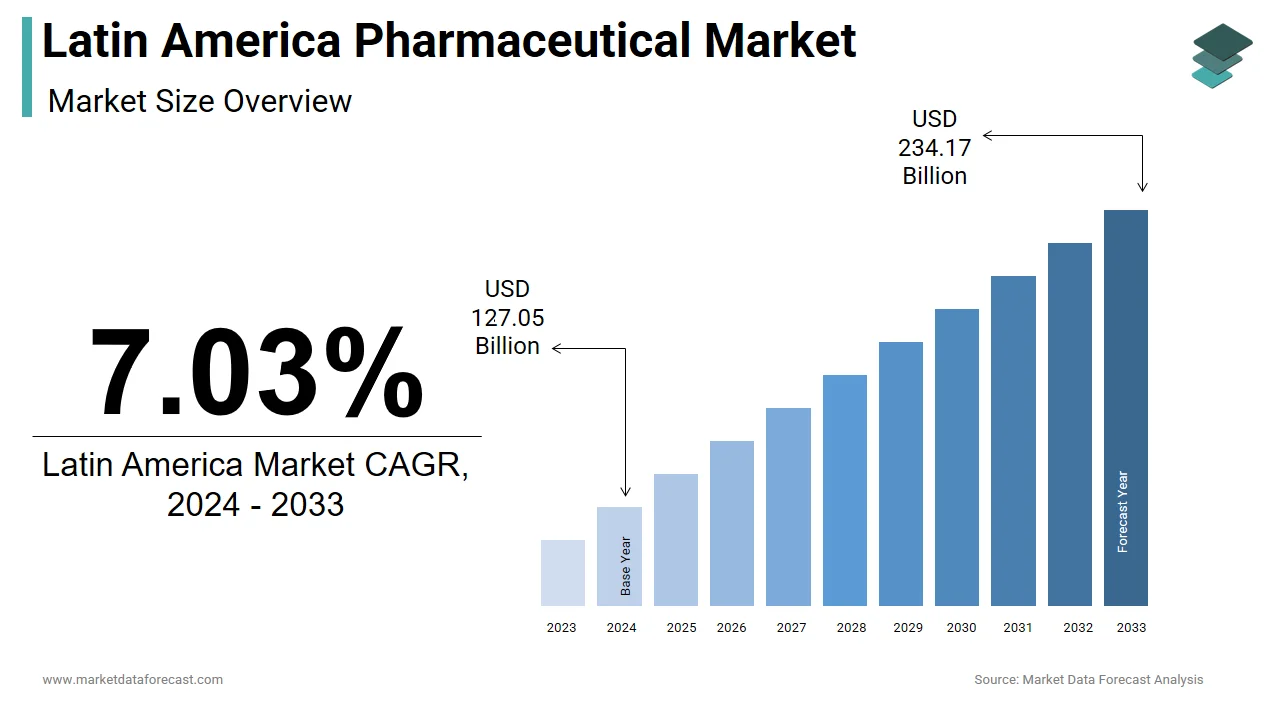

The size of the Latin America pharmaceutical market was valued at USD 135.98 billion in 2025. This market is expected to grow at a CAGR of 7.03% from 2026 to 2034 and be worth USD 250.63 billion by 2034 from USD 145.54 billion in 2026.

Pharmaceuticals include prescription drugs, generic medicines, over-the-counter (OTC) products, and biopharmaceuticals across countries such as Brazil, Mexico, Argentina, Colombia, Chile, and Peru. As a critical component of the region’s healthcare ecosystem, the sector plays a vital role in addressing both communicable and non-communicable disease burdens while supporting national health systems and private medical providers.

According to the Pan American Health Organization (PAHO), access to essential medicines has improved significantly in recent years due to government-led initiatives aimed at expanding healthcare coverage and promoting local pharmaceutical production. As per the Economic Commission for Latin America and the Caribbean (ECLAC), several governments have implemented policies to reduce import dependency by encouraging domestic drug manufacturing through tax incentives and regulatory reforms.

Moreover, rising prevalence of chronic diseases, increasing life expectancy, and growing awareness about preventive healthcare are shaping demand dynamics across the region. With evolving regulatory frameworks and technological advancements, the Latin America pharmaceutical market is undergoing transformational shifts aimed at improving accessibility, affordability, and innovation.

MARKET DRIVERS

Rising Prevalence of Chronic Diseases and Aging Population

The rising prevalence of chronic diseases such as diabetes, cardiovascular disorders, cancer, and respiratory conditions is one of the most significant drivers influencing the Latin America pharmaceutical market. According to the World Health Organization (WHO), non-communicable diseases (NCDs) account for more than 70% of all deaths in the region, necessitating increased demand for long-term medication and specialty therapeutics. Also, in Mexico, as per the National Institute of Public Health (INSP), cardiovascular diseases contributed to nearly 30% of annual mortality cases, driving up prescription volumes and treatment adherence requirements. Furthermore, demographic shifts toward an aging population are amplifying the need for geriatric medications and chronic care management solutions. The United Nations Economic Commission for Latin America and the Caribbean (ECLAC) estimates that by 2030, the number of people aged 60 and above will surpass 100 million in Latin America, significantly altering pharmaceutical demand patterns.

Expansion of Healthcare Infrastructure and Government Initiatives

The expansion of healthcare infrastructure and the implementation of government-led initiatives aimed at improving medicine accessibility and affordability is another key driver of the Latin America pharmaceutical market. According to the Pan American Health Organization (PAHO), public health spending in Latin America increased by nearly 5% annually between 2018 and 2023 , directly impacting pharmaceutical procurement and distribution systems. Brazil has been at the forefront of this initiative through the Unified Health System (SUS), which provides free or subsidized medications to millions of citizens. As per the Brazilian Health Regulatory Agency (ANVISA), in 2023, more than 400 million prescriptions were dispensed under federal health programs, reinforcing the role of public procurement in driving pharmaceutical sales. Similarly, Mexico’s Seguro Popular program (now integrated into the new National Health System) has expanded insurance coverage to previously underserved populations. In addition, Argentina and Colombia have introduced price control mechanisms and local production incentives to support domestic pharmaceutical companies, further stimulating market activity.

MARKET RESTRAINTS

Regulatory Complexity and Bureaucratic Delays

The complex and often inconsistent regulatory environment across the region is a major restraint affecting the Latin America pharmaceutical market. Unlike the harmonized approval frameworks seen in the European Union or ASEAN, Latin American countries maintain disparate regulatory standards, clinical trial requirements, and drug registration procedures, complicating market entry and commercialization timelines. According to the International Society for Pharmacoeconomics and Outcomes Research (ISPOR), obtaining regulatory approval for a new drug can take twice as long in Latin America compared to North America or Europe, primarily due to fragmented oversight bodies and prolonged review cycles. Also, some countries impose stringent pricing controls and mandatory bioequivalence testing for generics, increasing compliance costs for manufacturers. As per the Pan American Health Organization (PAHO), in 2023, delays in regulatory approvals led to shortages of critical medicines in parts of Central America, affecting treatment continuity for chronic disease patients.

Limited Access to Financing and R&D Constraints

Limited access to financing and constrained research and development (R&D) capabilities pose significant challenges to the Latin America pharmaceutical market, particularly for small and mid-sized domestic firms. Unlike multinational corporations with robust financial backing, many regional players struggle to secure funding for innovation, technology upgrades, and regulatory compliance. According to the Inter-American Development Bank (IDB), a smaller share of total pharmaceutical industry expenditures in Latin America are allocated to R&D, compared to that in developed markets like the United States and Germany. This disparity hampers the ability of local firms to develop novel drugs or invest in advanced formulation technologies. Moreover, venture capital and institutional investment in biotech startups remain underdeveloped in the region. In addition, banks and financial institutions are often reluctant to extend credit to pharmaceutical SMEs due to long product development cycles and uncertain returns.

MARKET OPPORTUNITIES

Growth of Generic and Biosimilar Markets

The rapid expansion of generic and biosimilar drug is a significant opportunity emerging in the Latin America pharmaceutical market. Driven by patent expirations of blockbuster biologics and growing pressure to reduce healthcare costs, governments and payers across the region are increasingly promoting the use of cost-effective alternatives to branded medicines.

According to the Pan American Health Organization (PAHO), generic medicines accounted for over 60% of total pharmaceutical prescriptions in Latin America in 2023, with Brazil, Mexico, and Colombia leading adoption due to favorable regulatory reforms and procurement policies. Brazil’s National Health Surveillance Agency (ANVISA) has streamlined the approval process for generics, reducing time-to-market and encouraging domestic production. In addition, the biosimilars market is gaining traction, particularly in oncology and autoimmune disease treatments. As per the Mexican Federal Commission for the Protection against Sanitary Risk (COFEPRIS), in 2023, biosimilar uptake in Mexico increased by 25% compared to the previous year, supported by government tenders and reimbursement schemes. Colombia and Argentina have also introduced policies to facilitate biosimilar integration into national formularies, aiming to improve treatment affordability for low-income populations.

Digital Health Integration and Telemedicine Expansion

The integration of digital health technologies and the expansion of telemedicine services represent a compelling opportunity for the Latin America pharmaceutical market. As healthcare delivery models evolve, digital tools are playing an increasingly important role in medication adherence, remote diagnostics, and virtual consultations, reshaping how pharmaceutical products reach consumers. Moreover, mobile health applications and online pharmacy services are transforming the retail pharmaceutical landscape. As per the Latin American E-commerce Association (eLatam), in 2023, online pharmacy sales in the region grew, driven by increased smartphone penetration and consumer trust in digital transactions. Pharmaceutical companies are leveraging these trends by partnering with e-health platforms to offer personalized treatment plans, digital medication tracking, and AI-driven symptom checkers.

MARKET CHALLENGES

Supply Chain Disruptions and Drug Shortages

The vulnerability of supply chains and recurring drug shortages, particularly for essential medicines and raw materials is a major challenge facing the Latin America pharmaceutical market. The region remains heavily reliant on imported active pharmaceutical ingredients (APIs), primarily from China and India, making it susceptible to global disruptions caused by geopolitical tensions, trade restrictions, and logistical bottlenecks. These shortages were attributed to delays in API imports, customs clearance issues, and limited domestic manufacturing capacity.

According to Brazil’s National Health Surveillance Agency (ANVISA), approximately 30% of generic drug producers faced supply constraints due to delayed shipments of raw materials, highlighting the fragility of the current sourcing model. To mitigate these risks, governments and private-sector stakeholders are exploring localized production partnerships and strategic stockpiling initiatives.

Pricing Pressures and Reimbursement Constraints

Pricing pressures and reimbursement constraints pose significant challenges to the Latin America pharmaceutical market, particularly for multinational companies seeking profitability in a region characterized by cost-sensitive buyers and government-imposed price controls. Many Latin American countries implement strict price regulation mechanisms to ensure affordability, which often limits revenue potential for pharmaceutical firms. According to the International Federation of Pharmaceutical Manufacturers & Associations (IFPMA), over 60% of pharmaceutical products in Latin America are subject to direct price controls, with Brazil, Argentina, and Mexico enforcing mandatory price caps on essential medicines. While these policies enhance patient access, they also discourage investment in innovation and high-cost therapies. In Colombia, the Ministry of Health revised its drug pricing framework in 2023, introducing additional reference pricing mechanisms that further compressed margins for pharmaceutical suppliers. Similarly, in Argentina, inflationary pressures and currency depreciation have made it difficult for pharmaceutical companies to maintain stable pricing structures. These pricing and reimbursement challenges underscore the need for balanced policy approaches that protect patient access while ensuring sustainable business models for pharmaceutical companies operating in Latin America.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Molecule Type, Product, Disease, Route of Administration, Age Group, Distribution Channel, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | Brazil, Mexico, Argentina, Chile, Rest of Latin America |

| Market Leaders Profiled | F. Hoffmann-La Roche Ltd, Novartis AG, AbbVie Inc., Johnson & Johnson Services, Inc., Merck & Co., Inc., Pfizer Inc., Bristol-Myers Squibb Company, Sanofi, GlaxoSmithKline plc, AstraZeneca, and Takeda Pharmaceutical Co., Ltd. |

SEGMENTAL ANALYSIS

By Molecule Type Insights

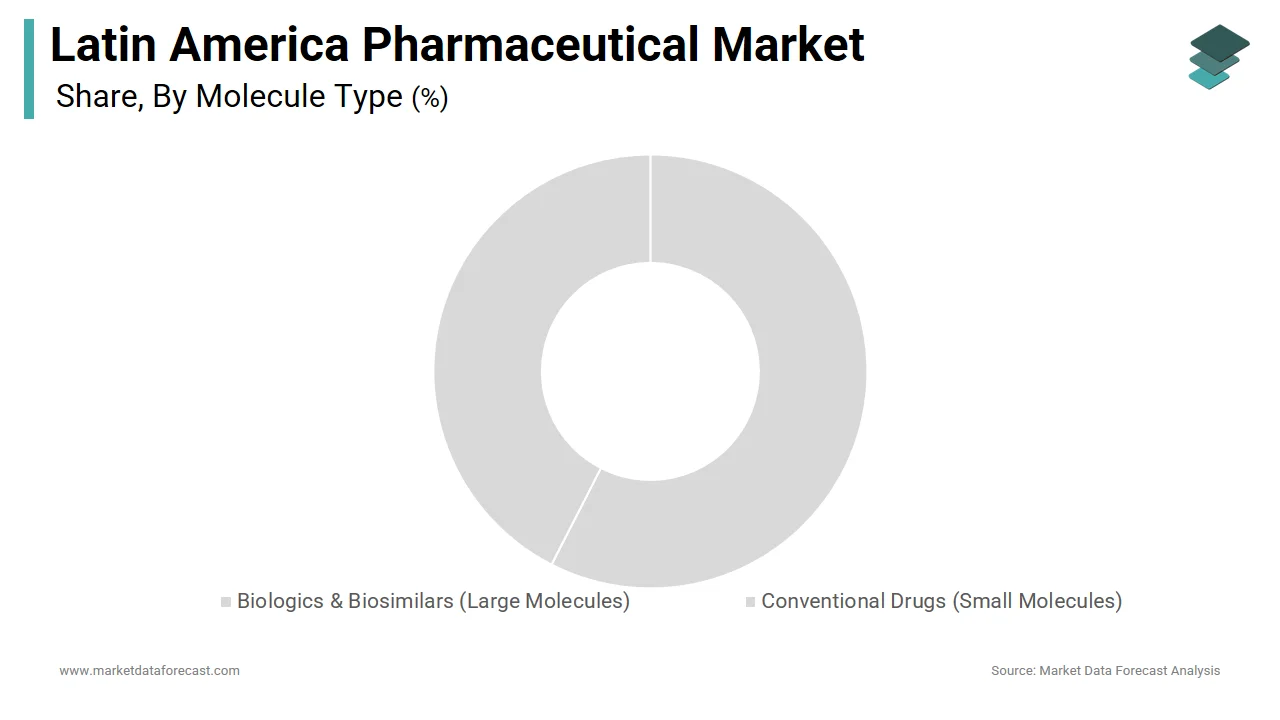

The conventional drugs segment, particularly small-molecule pharmaceuticals, dominated the Latin America pharmaceutical market by capturing 66.5% in 2024. Its widespread use in treating prevalent conditions such as hypertension, diabetes, infectious diseases, and respiratory illnesses is driving the growth of the conventional drugs segment. The high affordability and availability of generic small-molecule drugs, which are heavily promoted through government health programs across the region, also contribute to the growth of the conventional drugs segment. According to Brazil’s National Health Surveillance Agency (ANVISA), over 60% of all prescriptions dispensed under public health systems in 2023 were for generic small-molecule medications, reflecting strong integration into national healthcare delivery models. In addition, established manufacturing capabilities and regulatory support for domestic production have reinforced the accessibility of these drugs.

The biologics and biosimilars segment represented the fastest-growing segment in the Latin America pharmaceutical market and is projected to expand at a CAGR of 11.4% between 2025 and 2033. The increasing adoption of biosimilars as cost-effective alternatives to branded biologics, supported by regulatory reforms and government-backed reimbursement policies, is a primary growth catalyst for the Biologics and biosimilars segment. While still a smaller portion of the overall market, this segment is gaining momentum due to rising demand for targeted therapies in oncology, autoimmune disorders, and chronic inflammatory diseases. Moreover, expanding access to advanced treatments through public-private partnerships has accelerated market penetration. Argentina’s Administration National de Medicamentos (ANMAT) approved several new biosimilars, facilitating broader patient access to high-cost therapies.

By Product Insights

The generics segment constituted the largest category in the Latin America pharmaceutical market by holding 62.4% in 2024. The strong policy support from governments encouraging the prescription and dispensing of generic medicines to reduce healthcare costs is a major driver of the generics segment. This dominance is also due to the critical role generics play in expanding affordable medication access, especially within publicly funded healthcare systems. In Brazil, where generics are widely integrated into the Unified Health System (SUS), as per the Ministry of Health, in 2023, more than 400 million generic prescriptions were filled nationwide, reinforcing their foundational role in public health delivery. Moreover, regulatory modernization and streamlined approval pathways have enabled rapid market entry for new generic products. Mexico’s Federal Commission for the Protection against Sanitary Risk (COFEPRIS) introduced expedited review procedures in 2023, resulting in faster approvals and expanded competition among generic manufacturers. Furthermore, rising consumer awareness and acceptance of quality-assured generic alternatives have contributed to stronger retail sales.

The branded pharmaceuticals segment is emerging as the fastest-growing segment in the Latin America pharmaceutical market and is projected to grow at a CAGR of 9.8% during the forecast period. This growth of the branded pharmaceuticals segment is being propelled by increasing investments in innovative therapies, expansion of private healthcare coverage, and rising consumer preference for premium treatment options. The expansion of private health insurance and out-of-pocket spending on specialized medicines, particularly in urban centers of Brazil, Mexico, and Chile, also contributes to propelling the branded pharmaceuticals segment. Moreover, multinational pharmaceutical companies are intensifying their presence in the region, launching novel therapeutics and leveraging strategic pricing models to capture market share. Besides, growing collaborations between branded drugmakers and local distributors have improved market penetration in previously underserved regions.

By Type Insights

The prescription drugs segment commanded the Latin America pharmaceutical market by accounting for a substantial share in 2024. The regulatory framework requiring physician authorization for dispensing many essential and high-impact medications, particularly in chronic disease management and hospital settings, is mainly driving the growth of the prescription drugs segment. The integration of prescription medications into public health programs, ensuring consistent demand across both rural and urban populations, is another factor propelling the segment. Also, government-led initiatives promoting adherence to prescribed treatment regimens have strengthened the role of prescription drugs in managing non-communicable diseases. Moreover, regulatory enforcement against unauthorized dispensing of controlled substances continues to reinforce the necessity of medical oversight in medication access.

The over-the-counter (OTC) pharmaceuticals segment is the fastest-growing segment in the Latin America pharmaceutical market and is projected to expand at a CAGR of 10.2%. This rapid ascent is fueled by changing consumer behavior, increased self-care trends, and greater availability of OTC products through digital and traditional retail channels. Also, the rising consumer preference for convenience-driven healthcare solutions, particularly among younger and digitally savvy populations, is another growth catalyst. Apart from these, the expansion of pharmacy chains and drugstore networks, which have significantly broadened access to OTC products, is another reason behind this progress. Also, regulatory easing in certain markets has facilitated the reclassification of previously prescription-only drugs, allowing wider consumer access. As health literacy improves and retail infrastructure expands, the OTC pharmaceutical market in Latin America is expected to sustain its robust growth trajectory.

COUNTRY LEVEL ANALYSIS

Brazil Pharmaceutical Market Insights

Brazil held the largest share of the Latin America pharmaceutical market in 2025. As the region’s most populous country, Brazil benefits from a well-established public health system, extensive pharmaceutical manufacturing base, and a growing burden of chronic diseases, all of which drive continuous demand for medicines. A key strength lies in the Unified Health System (SUS) , which ensures broad access to essential medicines through centralized procurement and distribution mechanisms. Also, Brazil has made strides in localizing pharmaceutical production, with ANVISA implementing regulatory reforms to streamline drug approvals and encourage domestic manufacturing. Despite economic fluctuations, Brazil remains a dominant force in the Latin American pharmaceutical sector, offering a mix of public and private market opportunities that attract both multinational and domestic firms seeking long-term growth.

Mexico Pharmaceutical Market Insights

Mexico is another key player in the Latin America pharmaceutical market. The country serves as a strategic hub for pharmaceutical trade, benefiting from its proximity to the United States and Canada under the USMCA trade agreement. A defining feature of Mexico’s pharmaceutical landscape is its strong industrial base and integration into global supply chains, particularly in active pharmaceutical ingredient (API) manufacturing and contract development. Moreover, Mexico has seen a rise in biosimilar and specialty drug adoption, supported by regulatory modernization and expanded health coverage under the new National Health System. Also, digital health innovations and telemedicine expansion have transformed how pharmaceutical products reach consumers, particularly in urban centers.

Argentina Pharmaceutical Market Insights

Argentina is maintaining a modest yet historically significant presence despite economic volatility. The country’s pharmaceutical sector is shaped by currency fluctuations, inflationary pressures, and evolving consumer preferences, all of which influence drug pricing and accessibility. A key strength lies in Argentina’s tradition of scientific research and biotechnology innovation, particularly in vaccine development and biosimilars. Despite macroeconomic challenges, public health programs continue to drive demand for essential medicines, with the Ministry of Health allocating additional funds for chronic disease management. In addition, telemedicine and digital pharmacy platforms gained traction, improving medication access in remote areas. With renewed focus on local manufacturing and regulatory harmonization, Argentina is gradually recovering its pharmaceutical competitiveness despite ongoing financial constraints.

Chile Pharmaceutical Market Insights

Chile is positioning itself as a progressive leader in regulatory transparency and healthcare innovation, as per the Chilean Ministry of Health. The country benefits from a stable legal framework, strong intellectual property protections, and a well-developed private healthcare system, making it an attractive destination for pharmaceutical investment. A defining feature of Chile’s market is the early adoption of biosimilars and specialty medicines, supported by favourable reimbursement policies and clinical trial facilitation. Also, Chile has implemented digital health initiatives that enhance medication tracking and patient adherence, including e-prescription platforms and mobile pharmacy services.

Rest of Latin America

The Rest of Latin America (RoLA), encompassing countries such as Colombia, Peru, Ecuador, Costa Rica, and Central American nations, collectively holds a notable share of the regional pharmaceutical market. While individually these markets are smaller, they present substantial growth potential due to urbanization, improving economic conditions, and increasing access to healthcare services. Colombia stands out as a key contributor. The country is also witnessing a shift toward digital pharmacy platforms and biosimilar integration, reinforcing its growing influence in the regional pharmaceutical landscape. Meanwhile, Central American nations such as Panama and Costa Rica are attracting foreign investment in healthcare infrastructure, leveraging political stability and geographic advantages. With improving governance, digital health adoption, and cross-border collaboration, RoLA is gradually strengthening its pharmaceutical footprint, with international companies expanding into secondary cities and underserved regions.

COMPETITIVE LANDSCAPE

The competition in the Latin America pharmaceutical market is shaped by a mix of multinational corporations, regional pharmaceutical firms, and growing generic and biosimilar manufacturers. While global players like Roche, Pfizer, and Novartis dominate the branded and specialty segments, domestic companies such as Hypera Pharma in Brazil and Laboratorios Liomont in Mexico are gaining influence through cost-effective formulations and localized production capabilities.

Market dynamics are further influenced by regulatory disparities across countries, pricing pressures from government procurement policies, and increasing demand for affordable medicines. In response, pharmaceutical firms are adopting differentiated strategies, including vertical integration, digital health solutions, and collaborative R&D initiatives to maintain competitiveness.

The rise of biosimilars and generic drugs is intensifying competition in therapeutic categories such as diabetes, cardiovascular diseases, and oncology. Additionally, the expansion of private healthcare networks and online pharmacies is reshaping distribution channels and consumer access patterns. As the region continues to evolve, companies that can balance affordability, innovation, and regulatory agility will be best positioned to capture long-term growth opportunities.

KEY MARKET PLAYERS

Noteworthy Companies dominating the Latin America pharmaceutical market profiled in the report are

- F. Hoffmann-La Roche Ltd

- Novartis AG

- AbbVie Inc.

- Johnson & Johnson Services, Inc.

- Merck & Co., Inc.

- Pfizer Inc.

- Bristol-Myers Squibb Company

- Sanofi

- GlaxoSmithKline plc

- AstraZeneca

- Takeda Pharmaceutical Co., Ltd.

TOP LEADING PLAYERS IN THE MARKET

Roche maintains a strong presence across Latin America, particularly in Brazil and Mexico, where it supplies innovative medicines for oncology, immunology, and diagnostics. The company’s focus on personalized healthcare and biologics has positioned it as a leader in specialty pharmaceuticals. Roche also collaborates with local governments and research institutions to enhance access to advanced therapies and support public health initiatives.

Pfizer is a dominant player in the Latin American pharmaceutical market, known for its extensive portfolio of vaccines, anti-infectives, and chronic disease treatments. The company plays a critical role in vaccine distribution and has been instrumental in strengthening regional immunization programs. Pfizer also engages in public-private partnerships to improve medicine accessibility and supports regulatory harmonization efforts across the region.

Novartis operates through both its generics arm Sandoz, and its innovative medicines division, making it a dual force in the Latin America pharmaceutical landscape. It contributes significantly to biosimilars development and affordable drug manufacturing. The company invests in digital health platforms and sustainable supply chain initiatives to expand its footprint and meet evolving patient needs across key markets.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Latin America pharmaceutical market are leveraging strategic approaches tailored to the region’s diverse regulatory environments and healthcare demands. One of the most prevalent strategies is local manufacturing and supply chain localization, allowing companies to reduce costs, comply with national regulations, and ensure consistent product availability even amid global disruptions.

Another crucial approach is expanding partnerships with government health systems and private insurers, enabling pharmaceutical firms to integrate their products into national formularies and insurance coverage plans. These collaborations help increase market penetration while aligning with public health objectives.

Additionally, digital transformation and telehealth integration have become essential strategies for enhancing patient engagement and streamlining medication access. Companies are investing in e-health platforms, mobile pharmacy services, and AI-driven diagnostics to strengthen commercial reach and offer more accessible treatment pathways across urban and rural populations.

RECENT MARKET DEVELOPMENTS

- In January 2023, Roche expanded its biologics manufacturing facility in São Paulo, Brazil, focusing on producing biosimilars tailored to the Latin American market, aiming to improve treatment accessibility and reduce dependency on imports.

- In May 2023, Pfizer partnered with a leading Mexican hospital network to launch a digital prescribing platform, enhancing prescription accuracy and improving medication adherence among patients managing chronic conditions.

- In October 2023, Novartis announced a joint venture with a Colombian pharmaceutical distributor, aimed at expanding the reach of its generic and biosimilar portfolio across Central and South America.

- In February 2024, Hypera Pharma acquired a Chilean OTC brand, reinforcing its leadership in the over-the-counter segment and broadening its retail footprint in the Southern Cone region.

- In July 2024, AstraZeneca launched a regional clinical trial hub in Argentina, designed to accelerate drug development and regulatory approvals for therapies targeting prevalent diseases in Latin American populations.

MARKET SEGMENTATION

This Latin America pharmaceutical market research report is segmented and sub-segmented into the following categories.

By Molecule Type

- Biologics & Biosimilars (Large Molecules)

- Monoclonal Antibodies

- Vaccines

- Cell & Gene Therapy

- Others

- Conventional Drugs (Small Molecules)

By Product

- Branded

- Generics

By Type

- Prescription

- OTC

By Disease

- Cardiovascular diseases

- Cancer

- Diabetes

- Infectious diseases

- Neurological disorders

- Respiratory diseases

- Autoimmune diseases

- Mental health disorders

- Gastrointestinal disorders

- Women’s health diseases

- Genetic and rare genetic diseases

- Dermatological conditions

- Obesity

- Renal diseases

- Liver conditions

- Hematological disorders

- Eye conditions

- Infertility conditions

- Endocrine disorders

- Allergies

- Others

By Route of Administration

- Oral

- Tablets

- Capsules

- Suspensions

- Other

- Topical

- Parenteral

- Intravenous

- Intramuscular

- Inhalations

- Other

By Age Group

- Children & Adolescents

- Adults

- Geriatric

By Distribution Channel

- Hospital Pharmacy

- Retail Pharmacy

- Others

By Country

- Brazil

- Mexico

- Argentina

- Chile

- Rest of Latin America

Frequently Asked Questions

How large is the Latin America Pharmaceutical Market in 2025?

The Latin America Pharmaceutical Market generated USD 135.98 billion in 2025, with Brazil as the largest contributor, followed by Mexico and Argentina.

What is the projected value of the Latin America Pharmaceutical Market by 2034?

The Latin America Pharmaceutical Market is expected to surpass USD 250.63 billion by 2034, growing at a CAGR of 7.03% from 2026 to 2034.

What drives growth in the Latin America Pharmaceutical Market?

Growth in the Latin America Pharmaceutical Market is driven by population growth, chronic diseases, rising healthcare spending, and generics.

What is the role of generics in the Latin America Pharmaceutical Market?

Generic drugs are a fast-growing segment in the Latin America Pharmaceutical Market, meeting demand for affordable and accessible medicines.

Who are the top players in the Latin America Pharmaceutical Market?

Top players in the Latin America Pharmaceutical Market include Bayer, Novartis, Pfizer, Merck, GSK, Roche, Hypera Pharma, and EMS.

How important is contract manufacturing in the Latin America Pharmaceutical Market?

Contract manufacturing is vital in the Latin America Pharmaceutical Market, projected to surpass USD 39 billion by 2027.

What is the trade balance in the Latin America Pharmaceutical Market?

The Latin America Pharmaceutical Market faces a large trade deficit, importing five times more pharmaceuticals than it exports.

How do local companies compete in the Latin America Pharmaceutical Market?

Local companies in the Latin America Pharmaceutical Market compete with multinationals, especially in branded generics and biosimilars.

What are the main challenges for the Latin America Pharmaceutical Market?

Challenges in the Latin America Pharmaceutical Market include regulatory barriers, trade deficits, limited R&D, and infrastructure gaps.

How is Pharma 4.0 impacting the Latin America Pharmaceutical Market?

Pharma 4.0 is driving digital transformation and efficiency in the Latin America Pharmaceutical Market, with rapid adoption expected by 2033.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1600

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com