Latin America Spinal Implants Market Research Report By Technology, Product and Country (Mexico, Brazil, Argentina, Chile & Rest of Latin America) - Industry Analysis (2026 to 2034)

Market Size, 2025

$1,276.10 MnMarket Estimate, 2026

$1,334.42 MnMarket Forecast, 2034

$1,907.87 MnCAGR, 2026–2034

4.57%Latin America Spinal Implants Market Summary

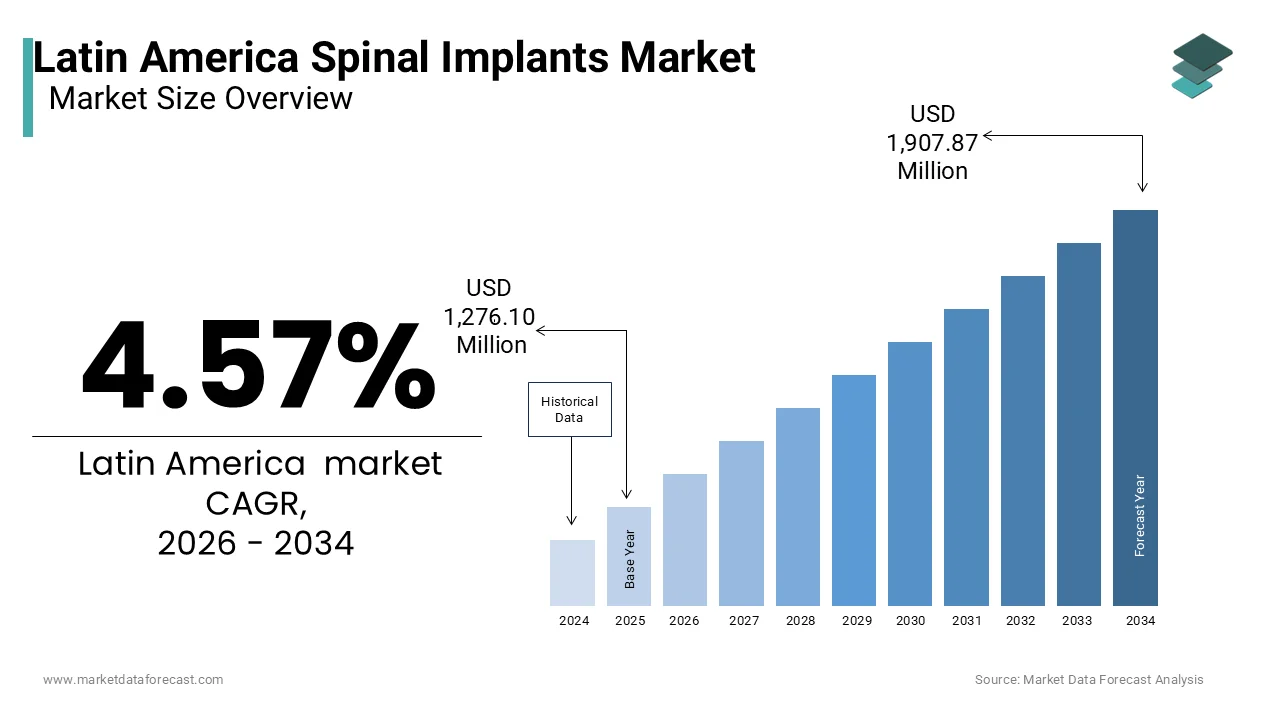

The Latin America spinal implants market, valued at USD 1,276.10 million in 2025, is projected to reach USD 1,907.87 million by 2034, growing at a CAGR of 4.57% driven by rising obesity, an aging population, and increasing adoption of minimally invasive spine surgery technologies.

Key Market Highlights

- 2025 Market Size: USD 1,276.10 million

- 2026 Estimate: USD 1,334.42 million

- 2034 Forecast: USD 1,907.87 million

- CAGR (2026–2034): 4.57%

- Base Year: 2025

- Forecast Period: 2026–2034

Quick Growth Drivers

- Rising geriatric population across Brazil, Mexico, Chile, and Argentina

- Increasing obesity prevalence, leading to degenerative spine disorders

- Growing demand for minimally invasive spine surgery (MISS)

- Technological advancements in fusion, fixation, and motion-preserving implants

- Expansion of private hospitals and specialty orthopedic centers

Principal Restraints

- High cost of spinal implant procedures relative to average income levels

- Uncertain reimbursement frameworks across public healthcare systems

- Lengthy and complex regulatory approval processes

- Limited patient awareness of advanced spine treatment options

- Shortage of adequately trained spine surgeons in secondary cities

High-Value Opportunities

- Expansion of minimally invasive and outpatient spine surgery programs

- Increasing adoption of biologics and spinal stimulators

- Growth of private healthcare investment in Brazil and Mexico

- Introduction of cost-optimized implant systems tailored for emerging markets

- Rising demand for artificial discs and motion preservation technologies

Key Market Challenges

- Limited access to advanced spine care in rural and semi-urban regions

- Variability in clinical outcomes and surgeon expertise

- Budget constraints in public hospitals affecting implant procurement

- Dependence on imported spinal implant systems, increasing pricing volatility

Fastest-Growing Segments

- Motion Preservation Technologies — artificial discs gaining traction

- Minimally Invasive Surgery (MIS) Devices — shorter hospital stays

- Spinal Biologics & Stimulators — enhanced fusion success rates

Regional Leadership & Dynamics

- Brazil — largest and most mature market with strong private hospital penetration

- Mexico — rapid adoption driven by obesity prevalence and healthcare reforms

- Chile — aging population accelerating demand for degenerative spine treatments

- Argentina & Rest of Latin America — steady growth supported by improving infrastructure

What Wins Commercially

- Affordable, durable implant systems with proven clinical outcomes

- Strong local distributor networks and surgeon training programs

- Minimally invasive solutions reducing hospitalization costs

- Alignment with government healthcare cost-containment policies

Top Strategic Ask for Executives

Develop cost-effective, minimally invasive spinal implant portfolios supported by surgeon education and local partnerships to accelerate penetration across Latin America’s emerging spine care markets.

Leading Players

Some of the companies that are playing a dominating role in the Latin America spinal implants market include:

- Medtronic

- DePuy Synthes

- Stryker

- Zimmer Biomet

- Globus Medical

- NuVasive

- Alphatec Holdings

- Orthofix International

Latin America Spinal Implants Market Size

The Latin America spinal implants market was valued at USD 1,276.10 million in 2025, is estimated to reach USD 1,334.42 million in 2026, and is projected to reach USD 1,907.87 million by 2034, growing at a CAGR of 4.57% from 2026 to 2034.

Spinal implants encompass a specialized segment of medical devices designed to stabilize and restore function to the vertebral column. These implants include cages, screws, rods, and artificial discs utilized in procedures such as spinal fusion and decompression. The region is witnessing a paradigm shift driven by an aging demographic and increasing prevalence of degenerative spinal conditions. According to the United Nations Department of Economic and Social Affairs, the population aged 60 years or older in Latin America and the Caribbean is projected to reach 157 million by 2030, representing a significant surge from 74 million in 2015. This demographic transition directly correlates with higher incidences of osteoporosis and spinal stenosis.

Furthermore, the World Health Organization indicates that musculoskeletal conditions are the leading contributor to disability worldwide, affecting approximately 1.71 billion people. In Brazil alone, the Ministry of Health recorded over 120,000 spinal surgeries annually in recent years, underscoring the critical demand for advanced implant solutions. The market is also influenced by the gradual adoption of minimally invasive surgical techniques, which reduce recovery times and hospital stays. Despite economic fluctuations, countries like Mexico and Argentina are expanding their healthcare infrastructure to accommodate these complex procedures. The integration of robotic assistance in spine surgery is gaining traction, although penetration remains low compared to North America. This evolving landscape reflects a growing recognition of spinal health as a priority within public and private healthcare systems across the region.

MARKET DRIVERS

Rising Prevalence of Degenerative Spinal Disorders and Age-Related Conditions

The escalating incidence of degenerative spinal disorders is majorly boosting the expansion of the Latin American spinal implants market. Degenerative disc disease, spinal stenosis, and spondylolisthesis are becoming increasingly common due to sedentary lifestyles and aging populations. According to the Global Burden of Disease Study, low back pain is the single leading cause of disability globally, with Latin America reporting a prevalence rate of approximately 8% among adults. In Mexico, the National Institute of Statistics and Geography stated that nearly 25% of the population suffers from chronic back pain, creating a substantial patient pool requiring surgical intervention. The aging demographic exacerbates this trend, as the risk of spinal degeneration increases significantly after the age of 50. According to the data from the Pan American Health Organization, life expectancy in the region has risen to 75 years, which is leading to a larger elderly cohort susceptible to vertebral fractures and degenerative changes. Additionally, obesity rates are climbing, with the World Obesity Federation noting that over 30% of adults in countries like Chile and Argentina are obese. Excess body weight places additional mechanical stress on the spinal column, accelerating disc degeneration and necessitating implant-based solutions. The convergence of these health trends drives the demand for spinal fixation devices, interbody cages, and dynamic stabilization systems. Healthcare providers are increasingly prioritizing early diagnosis and surgical management to improve quality of life, further stimulating the adoption of advanced spinal implants across public and private hospitals in the region.

Expansion of Healthcare Infrastructure and Medical Tourism Hubs

The strategic development of healthcare infrastructure and the burgeoning medical tourism sector are further contributing to the growth of the Latin American spinal implants market. Countries such as Mexico, Costa Rica, and Brazil are investing heavily in modernizing their hospital facilities to meet international standards, thereby attracting both domestic and international patients. As per the International Trade Administration, medical tourism in Mexico generated approximately 1.2 billion USD in revenue recently, with orthopedic and spinal procedures constituting a significant portion of these services. Patients from the United States and Canada often seek cost-effective yet high-quality spinal surgeries in these destinations, where costs can be 40% to 60% lower than in their home countries. This influx of medical tourists necessitates the availability of state-of-the-art spinal implants and advanced surgical technologies. Furthermore, governments in the region are enhancing public healthcare coverage. For instance, the Brazilian Unified Health System has expanded access to complex surgeries, including spinal fusions, reducing waiting times and increasing procedure volumes. The Joint Commission International has accredited numerous hospitals in Colombia and Peru, which signals a commitment to quality care that encourages the adoption of premium implant products. Private insurance penetration is also rising, with analysts from S&P Global indicating a 5% annual growth in private health expenditure in key markets. This financial accessibility enables more patients to opt for sophisticated spinal interventions, thereby driving the demand for innovative implant solutions that offer better clinical outcomes and faster recovery periods.

MARKET RESTRAINTS

High Cost of Advanced Spinal Implant Procedures and Limited Reimbursement

The prohibitive cost of advanced spinal implant procedures, coupled with inconsistent reimbursement policies, is significantly hampering the expansion of the Latin American market. High-end spinal implants, particularly those featuring robotic compatibility or bioabsorbable materials, carry substantial price tags that are often inaccessible to the majority of the population. According to the World Bank, out-of-pocket health expenditure in several Latin American countries exceeds 30% of total health spending, placing a heavy financial burden on patients. In nations like Peru and Bolivia, public health budgets are constrained, limiting the procurement of expensive imported implants. According to the Inter-American Development Bank, fiscal deficits in the region have led to reduced healthcare funding, forcing public hospitals to rely on lower-cost, generic alternatives rather than premium branded devices. Reimbursement frameworks vary widely and are often inadequate. In Brazil, while the public system covers basic spinal surgeries, coverage for newer technologies such as artificial discs is limited or subject to lengthy approval processes. Private insurers frequently impose caps on spinal procedure reimbursements, discouraging the use of costly advanced implants. As per a study by the Latin American Health Economics Association, nearly 40% of patients requiring spinal surgery delay or forego treatment due to financial constraints. This economic barrier restricts market penetration for high-value products and forces manufacturers to compete primarily on price rather than innovation. Consequently, the adoption of cutting-edge spinal technologies remains sluggish, hindering the overall market potential despite the growing clinical need for effective spinal care solutions.

Regulatory Hurdles and Complex Approval Processes For Medical Devices

Stringent regulatory requirements and protracted approval processes for medical devices are also hindering the growth of the Latin American spinal implants market. Each country in the region maintains its own regulatory authority, such as ANVISA in Brazil, COFEPRIS in Mexico, and ANMAT in Argentina, each with distinct and often cumbersome registration protocols. According to the Pan American Health Organization, the average time for medical device registration in Latin America can range from 12 to 24 months, significantly longer than in the United States or Europe. This delay impedes the timely launch of new products, causing manufacturers to lose competitive advantage and delaying patient access to innovative therapies. In Brazil, ANVISA has implemented stricter post-market surveillance requirements, increasing the compliance burden for foreign manufacturers. The complexity is further exacerbated by frequent changes in regulatory guidelines and local content requirements. For instance, Argentina has historically imposed import restrictions and licensing requirements that disrupt supply chains and increase operational costs. According to the World Trade Organization, non-tariff barriers in the region, including complex customs procedures, add an estimated 15% to the cost of imported medical devices. These regulatory inconsistencies create an unpredictable business environment, discouraging smaller manufacturers from entering the market. Additionally, the lack of harmonization across regional regulatory bodies means that companies must navigate multiple separate approval pathways, increasing administrative overhead. This fragmented regulatory landscape slows down the diffusion of advanced spinal technologies and limits the variety of implants available to surgeons, ultimately constraining market growth and innovation adoption rates.

MARKET OPPORTUNITIES

Adoption of Minimally Invasive Spine Surgery Techniques

The gradual but steady adoption of minimally invasive spine surgery techniques presents a substantial opportunity for market growth in Latin America. These procedures involve smaller incisions, reduced muscle damage, and faster recovery times compared to traditional open surgeries. As per the Journal of Neurosurgery, minimally invasive techniques can reduce hospital stays by up to 50%, which is a critical factor in regions with limited hospital bed capacity. The demand for specialized implants compatible with these techniques, such as expandable cages and percutaneous screw systems, is rising. Hospitals in urban centers like São Paulo and Mexico City are increasingly investing in the necessary equipment and training to offer these advanced services. As per the Latin American Society of Spine Pathology, a 15% annual increase is noticed in the number of minimally invasive spinal procedures performed in the region. This trend is driven by patient preference for less invasive options and the economic benefit of shorter hospitalizations for healthcare providers. Manufacturers who introduce user-friendly, minimally invasive, compatible implants can capture a growing share of the market. Furthermore, telemedicine and remote surgical mentoring platforms are facilitating knowledge transfer from global experts to local surgeons, which is accelerating the learning curve. This technological diffusion creates a favorable environment for the introduction of next-generation spinal devices. As more surgeons become proficient in these techniques, the volume of procedures utilizing advanced implants is expected to rise, offering a lucrative avenue for market expansion and product differentiation.

Growth of Private Healthcare Sector and Insurance Penetration

The expanding private healthcare sector and increasing insurance penetration offer significant opportunities for the Latin American spinal implants market. As public healthcare systems face budgetary constraints, a growing middle class is turning to private providers for faster and higher-quality care. According to Frost and Sullivan, the private healthcare market in Latin America is expected to grow at a compound annual growth rate of 6% over the next five years. This growth is particularly evident in countries like Colombia and Chile, where private insurance coverage is becoming more accessible. Private hospitals are more likely to invest in advanced surgical technologies and premium implant products to attract patients seeking superior outcomes. The rise of corporate health plans and individual insurance policies is enabling patients to afford costly spinal procedures that were previously out of reach. As per the data from the Association of Private Health Insurers in Brazil, a 10% increase is recorded in membership over the last three years. This shift towards private financing reduces the reliance on public reimbursement schemes, allowing for greater flexibility in product selection. Manufacturers can leverage this trend by partnering with private hospital networks and insurance providers to create bundled payment models or preferred provider agreements. Such collaborations can facilitate the adoption of innovative spinal implants by aligning financial incentives with clinical benefits. As the private sector continues to expand, it will serve as a key driver for the introduction and utilization of high-value spinal devices in the region.

MARKET CHALLENGES

Shortage of Skilled Spine Surgeons And Specialized Training Facilities

A critical shortage of highly trained spine surgeons and adequate specialized training facilities constitutes a major challenge for the Latin America Spinal Implants Market. Complex spinal procedures require exceptional surgical expertise, yet the region faces a significant gap in the number of qualified professionals. As per the World Federation of Neurosurgical Societies, there is a disproportionate distribution of neurosurgeons and orthopedic spine specialists, with rural areas severely underserved. In countries like Guatemala and Honduras, the ratio of neurosurgeons to population is less than 1 per 1 million inhabitants, compared to over 10 per 1 million in developed nations. This scarcity limits the volume of complex spinal surgeries that can be performed, thereby restricting the demand for advanced implants. Furthermore, the training infrastructure for minimally invasive spine surgery and robotic-assisted techniques is limited. The Latin American Spine Society indicates that fewer than 20% of orthopedic residents receive comprehensive fellowship training in complex spinal deformities. This skills gap results in a reliance on traditional open surgery techniques, which may not require the same level of sophisticated implant technology. Additionally, brain drain remains a persistent issue, with many skilled surgeons emigrating to North America or Europe for better opportunities. The Pan American Health Organization reports that migration of health workers from Latin America has increased by 20% in the last decade. This exodus further depletes the local talent pool, hindering the adoption of new technologies and limiting the market's ability to expand into advanced procedural segments. Without a robust pipeline of trained specialists, the utilization of high-end spinal implants remains constrained.

Supply Chain Vulnerabilities and Import Dependency For Raw Materials

The Latin America Spinal Implants Market faces significant vulnerabilities due to its heavy reliance on imports and fragile supply chains for raw materials and finished devices. Most high-quality spinal implants are manufactured in the United States, Europe, or Asia, making the region dependent on international logistics networks. According to the Economic Commission for Latin America and the Caribbean, supply chain disruptions during global crises can lead to delays of up to 3 months for medical device deliveries. This dependency exposes the market to currency fluctuations, trade tariffs, and geopolitical tensions. For example, fluctuations in the exchange rate between the US dollar and local currencies like the Argentine peso or Brazilian real can drastically increase the cost of imported implants, making them unaffordable for many healthcare providers. The Inter American Development Bank notes that logistics costs in Latin America are approximately 20% higher than in OECD countries due to inefficient infrastructure and bureaucratic bottlenecks. Additionally, the region lacks a robust domestic manufacturing base for high-precision medical-grade titanium and polyether ether ketone, which are essential materials for spinal implants. Local production is mostly limited to basic instruments or low-value consumables. This lack of local manufacturing capacity means that any disruption in global supply chains, such as those seen during recent pandemics or shipping crises, immediately impacts the availability of critical spinal devices. Hospitals often face stockouts of specific implant sizes or types, forcing surgeons to alter surgical plans or delay procedures. This instability undermines confidence in the supply chain and hinders long-term planning for healthcare institutions, thereby restraining market growth and reliability.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Technology, Product, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | Mexico, Brazil, Argentina, Chile, Rest of Latin America |

| Market Leaders Profiled | Medtronic, plc (Ireland), DePuy Synthes (U.S.), Stryker Corporation (U.S.), NuVasive, Inc. (U.S.), Zimmer Biomet Holdings, Inc. (U.S.), Globus Medical, Inc. (U.S.), Alphatec Holdings, Inc. (U.S.), Orthofix International N.V. (Netherlands), K2M Group Holdings, Inc. (U.S.), and RTI Surgical, Inc. (U.S.).

|

SEGMENTAL ANALYSIS

By Technology Insights

The spinal fusion and fixation technologies segment commanded the largest share of 61.6% of the regional market in 2025. The dominance of spinal fusion and fixation technologies segment in Latin America is primarily driven by the high prevalence of degenerative disc disease and the established clinical efficacy of fusion procedures in alleviating chronic back pain. The widespread acceptance of spinal fusion as the gold standard treatment for degenerative spinal conditions significantly bolsters this segment. According to the Global Burden of Disease Study, low back pain affects nearly 8% of the population in Latin America, with a significant portion requiring surgical intervention due to failed conservative therapies. In Brazil, the Ministry of Health data indicates that over 70,000 spinal fusion procedures are performed annually in public hospitals alone, reflecting the deep integration of this technology into standard care protocols. The aging population further amplifies this demand, as the Pan American Health Organization reports that the number of individuals aged 60 and above will double by 2050, leading to a higher incidence of spondylolisthesis and spinal stenosis. These conditions often necessitate stabilization through pedicle screw systems and rods, which are core components of fusion technologies. Furthermore, the availability of reimbursement for fusion surgeries in major markets like Mexico and Chile encourages hospitals to maintain robust inventory levels of these devices. The technical familiarity of surgeons with fusion techniques, compared to newer non-fusional alternatives, ensures that this segment remains the primary choice for complex spinal pathologies, thereby sustaining its market leadership through consistent procedural volumes and device utilization rates across the region.

On the other hand, the motion preservation and non-fusion technologies segment is projected to expand at a CAGR of 10.4% over the forecast period, owing to the increasing adoption of artificial discs and dynamic stabilization systems that preserve spinal mobility. The shift towards motion preservation technologies is driven by advancements in surgical techniques and a growing patient preference for procedures that maintain natural spinal kinematics. According to the Latin American Spine Society, the number of cervical disc arthroplasty procedures has increased by 15% annually in urban centers likeSãoo Paulo and Buenos Aires. Patients are increasingly seeking alternatives to fusion to avoid adjacent segment disease, a common complication where vertebrae above or below the fused segment degenerate faster. Clinical studies cited by the Brazilian Society of Orthopedics and Traumatology indicate that artificial disc replacement can reduce the risk of adjacent segment pathology by up to 30% compared to fusion. This clinical benefit is driving adoption among younger, active patients who wish to maintain flexibility.

Furthermore, the introduction of minimally invasive approaches for implanting these devices has reduced recovery times, making them more attractive to both surgeons and patients. The availability of advanced imaging technologies, such as intraoperative CT scans, has improved the precision of implant placement, enhancing outcomes and confidence in non-fusion solutions. As training programs expand, more surgeons are becoming proficient in these complex procedures, further accelerating market growth and expanding the patient base eligible for motion preservation interventions across the region.

By Product Insights

The thoracic fusion and lumbar fusion devices segment accounted for the major share of 54.5% of the Latin American market in 2025. This dominance is attributed to the high prevalence of lumbar degenerative diseases and the extensive use of these devices in common spinal surgeries. The high incidence of lumbar degenerative disc disease is the primary factor driving the dominance of thoracic and lumbar fusion devices. According to the World Health Organization, low back pain is the leading cause of disability in Latin America, with lumbar pathologies accounting for the majority of cases. In Argentina, the Ministry of Health reports that over 60% of spinal surgeries performed are related to lumbar conditions, necessitating the use of fusion hardware. The sedentary lifestyle prevalent in urban areas contributes to this trend, as noted by the Pan American Health Organization, which links physical inactivity to increased rates of obesity and subsequent spinal stress. Obesity rates in Mexico have reached 35% among adults, as per the National Health and Nutrition Survey, placing excessive load on the lumbar spine and accelerating disc degeneration. This epidemiological reality creates a sustained demand for lumbar fusion devices, including cages, screws, and rods.

Furthermore, the aging population is particularly susceptible to lumbar stenosis and spondylolisthesis, conditions that frequently require surgical stabilization. The established clinical guidelines for treating these conditions favor fusion techniques, ensuring consistent utilization of these products. Hospitals across the region maintain large inventories of lumbar fusion devices to meet this steady demand, reinforcing the segment's market leadership through high procedural volumes and repeat purchases of consumable components associated with these surgeries.

However, the spine biologics segment is the fastest-growing segment in the Latin America spinal implants market and is expected to register a CAGR of 11.4% over the forecast period, owing to the increasing focus on improving fusion rates and the adoption of advanced biological agents to enhance bone healing. The demand for spine biologics is surging as surgeons seek to improve fusion rates and reduce complications associated with traditional autografts. According to the Journal of Neurosurgery Spine, the use of bone graft substitutes can increase fusion success rates by up to 15% in complex cases. In Latin America, where revision surgeries pose a significant financial burden on healthcare systems, the ability to achieve successful fusion in the primary procedure is highly valued. Data from the Brazilian Society of Spine Surgery indicates that the adoption of demineralized bone matrix and synthetic bone grafts has increased by 20% in major hospitals over the past three years. These biologics offer a viable alternative to iliac crest bone graft harvesting, which is associated with donor site morbidity and prolonged pain. Patients are increasingly aware of these benefits, driving demand for procedures that utilize advanced biologics.

Furthermore, the aging population, which often has compromised bone quality, benefits significantly from the osteoinductive properties of these products. The Pan American Health Organization highlights that osteoporosis affects nearly 20% of women over 50 in the region, making enhanced biological support crucial for successful surgical outcomes. As awareness of these advantages grows, both surgeons and patients are prioritizing the use of spine biologics, fueling rapid segment growth.

COUNTRY LEVEL ANALYSIS

Brazil Spinal Implants Market Analysis

Brazil emerged as the regional leader in 2025, and it is projected to maintain this dominant position during the forecast period. The country’s market is characterized by a dual healthcare system comprising the public Unified Health System and a robust private sector, both of which contribute significantly to spinal care delivery. The primary driver of market growth is the large population base and the increasing prevalence of spinal disorders. According to the Brazilian Institute of Geography and Statistics, the population aged 60 and older is expected to reach 40 million by 2030, leading to a higher incidence of degenerative spinal conditions. This demographic shift is creating a sustained demand for spinal implants, particularly in the public sector,r where the government has expanded coverage for complex surgeries. The Ministry of Health reports that over 100,000 spinal procedures are performed annually, with a significant portion involving fusion devices. Additionally, the private healthcare sector is experiencing growth, with the National Supplementary Health Agency indicating a 5% increase in private health plan memberships. This expansion enables more patients to access advanced spinal technologies, including minimally invasive procedures and premium implants. Local manufacturing capabilities are also developing, with regulatory incentives from ANVISA encouraging domestic production of medical devices. This combination of demographic trends, public health initiatives, and private sector growth positions Brazil as the dominant force in the regional spinal implants market, driving both volume and value growth.

Mexico Spinal Implants Market Analysis

Mexico accounted for a promising share of the Latin American spinal implants market in 2025 and is projected to be the fastest-growing regional market in Latin America during the forecast period. The market in Mexico is influenced by its proximity to the United States and a thriving medical tourism industry. The country is a preferred destination for patients seeking high-quality, cost-effective spinal surgeries. According to the International Trade Administration, medical tourism in Mexico generates over 1 billion USD annually, with orthopedic and spinal procedures being key contributors. This influx of international patients drives demand for advanced spinal implants, as hospitals strive to meet global standards of care. The domestic market is also expanding, supported by social security institutions such as the Mexican Institute of Social Security, which serves millions of beneficiaries. Data from the National Institute of Statistics and Geography indicates that the prevalence of chronic back pain in Mexico is around 25%, creating a substantial local patient pool. The government has been investing in healthcare infrastructure, with the Institute for Social Security and Services for State Workers upgrading hospital facilities to handle complex spinal cases. Additionally, the rise of private insurance coverage is enabling more Mexicans to afford elective spinal surgeries. Regulatory reforms by COFEPRIS have streamlined the approval process for medical devices, facilitating faster market entry for new technologies. These factors collectively strengthen Mexico’s position as a key market player, balancing domestic needs with international demand.

Argentina Spinal Implants Market Analysis

Argentina is anticipated to showcase a healthy CAGR in the Latin American spinal implants market throughout the forecast period. The Argentine market is characterized by a highly educated medical community and a strong tradition of specialized healthcare services. Despite economic challenges, the demand for spinal implants remains resilient due to the high prevalence of spinal disorders and the availability of skilled surgeons. According to the Argentine Society of Orthopedics and Traumatology, spinal surgeries are among the most common orthopedic procedures performed in the country. The public healthcare system, along with various social security obras sociales, provides coverage for essential spinal treatments, ensuring access for a broad segment of the population. Data from the National Institute of Statistics and Censuses shows that the aging population is growing, with life expectancy reaching 77 years, leading to increased instances of age-related spinal conditions. The private healthcare sector also plays a significant role, with prepaid medicine plans covering advanced surgical options for affluent patients. Although import restrictions and currency fluctuations pose challenges, local distributors have adapted by maintaining strategic stockpiles and negotiating favorable terms with international suppliers. The presence of renowned spine centers in Buenos Aires attracts patients from neighboring countries, further boosting the market. These dynamics sustain Argentina’s position as a key contributor to the regional spinal implants landscape, driven by clinical expertise and persistent demand.

TOP LEADING PLAYERS IN THE MARKET

- Medtronic plc stands as a dominant force in the global spinal implants sector with a robust presence across Latin America. The company offers a comprehensive portfolio of surgical technologies, including minimally invasive solutions and robotic-assisted platforms. In recent years, Medtronic has strengthened its regional position by expanding training centers in Brazil and Mexico to educate surgeons on advanced techniques. The company actively collaborates with local healthcare providers to enhance access to high-quality spinal care. Its commitment to innovation is evident through the introduction of next-generation biologics and navigation systems. Medtronic focuses on improving patient outcomes by integrating digital health tools into surgical workflows. This strategic approach allows the company to maintain strong relationships with key opinion leaders and hospitals throughout the region. By prioritizing clinical education and technological advancement, Medtronic continues to shape the standard of care in spinal surgery while addressing the specific needs of diverse patient populations in Latin American markets.

- Johnson & Johnson Services Inc operates through its DePuy Synthes subsidiary to deliver impactful spinal solutions in Latin America. The company is renowned for its extensive range of fixation devices and biological products designed to support complex spinal reconstructions. Recently,y Johnson & Johnson has intensified its efforts to streamline supply chain operations in countries like Argentina and Chile to ensure consistent product availability. The organization invests heavily in research and development to create implants that facilitate faster recovery times. It also engages in partnerships with local distributors to expand market reach in underserved areas. Johnson & Johnson emphasizes value-based healthcare by demonstrating the long-term economic benefits of its premium implant systems. The company regularly hosts symposiums and workshops to foster knowledge exchange among spine specialists. These initiatives help solidify its reputation as a trusted partner in the medical community. By combining product innovation with strategic logistical improvements, Johnson & Johnson effectively addresses the evolving demands of the Latin American spinal implants landscape.

- Stryker Corporation is a leading innovator in the spinal implants industry with a significant footprint in Latin America. The company specializes in advanced surgical equipment and implants that enable minimally invasive procedures. Stryker has recently focused on enhancing its digital ecosystem by introducing augmented reality tools for surgical planning in major hospitals across the region. This technology assists surgeons in achieving greater precision during complex operations. The corporation also strengthens its market position through aggressive expansion of its sales and support teams in key markets such as Colombia and Peru. Stryker prioritizes customer engagement by providing comprehensive post-sale services and technical assistance. It actively participates in local medical conferences to showcase its latest advancements in spine care. The company’s dedication to sustainability and operational efficiency resonates well with modern healthcare institutions. By leveraging cutting-edge technology and maintaining a strong local presence, Stryker continues to drive growth and improve surgical standards in the Latin American spinal implants sector.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Latin America Spinal Implants Market primarily employ strategic partnerships and localized manufacturing to strengthen their competitive stance. Companies frequently collaborate with local distributors to navigate complex regulatory environments and improve supply chain efficiency. This approach ensures the timely delivery of critical devices to hospitals across diverse geographical areas. Another major strategy involves investing in surgeon training programs and educational workshops. By enhancing the skills of local medical professionals, manufacturers foster loyalty and increase the adoption of their proprietary technologies. Product innovation remains central to corporate strategy,s with firms introducing minimally invasive and robotic-assisted solutions to meet rising demand for advanced care. Additionally, key participants focus on expanding their presence in the private healthcare sectors where reimbursement rates are higher. They also engage in mergers and acquisitions to broaden their product portfolios and access new customer bases. These multifaceted strategies enable companies to address unique regional challenges while capitalizing on growth opportunities in emerging economies throughout Latin America.

COMPETITIVE LANDSCAPE

The competitive landscape of the Latin America Spinal Implants Market is characterized by the presence of established multinational corporations and emerging local manufacturers. Global giants dominate the sector due to their extensive product portfolio,s advanced technological capabilities, es and strong brand recognition. These companies leverage their financial resources to invest heavily in research and development,nt resulting in continuous innovation of spinal devices. However, local players are gaining traction by offering cost-effective alternatives that appeal to price-sensitive public healthcare systems. The market exhibits moderate consolidation as larger entities acquire smaller firms to expand their geographic reach and product offerings. Competition is further intensified by the varying regulatory requirements across different countries, which create barriers to entry for new participants. Companies differentiate themselves through superior customer service,e comprehensive surgeon training programs, ms and strategic partnerships with local distributors. The race to introduce minimally invasive robotic-assisted technologies adds another layer of complexity to the competitive dynamics. As healthcare infrastructure improves and demand for advanced spinal care rises, the intensity of competition is expected to increase,e driving further innovation and strategic maneuvering among key market participants in the region.

KEY MARKET PLAYERS

A few of the promising companies dominating the Latin American spinal implants market profiled in the report are

- Medtronic, plc (Ireland),

- DePuy Synthes (U.S.),

- Stryker Corporation (U.S.),

- NuVasive, Inc. (U.S.),

- Zimmer Biomet Holdings, Inc. (U.S.),

- Globus Medical, Inc. (U.S.),

- Alphatec Holdings, Inc. (U.S.),

- Orthofix International N.V. (Netherlands),

- K2M Group Holdings, Inc. (U.S.),

- RTI Surgical, Inc. (U.S.).

MARKET SEGMENTATION

This research report on the Latin American Spinal Implants Market has been segmented and sub-segmented into the following categories.

By Technology

- Fusion

- Fixation

- VCF

- Decompression

- Motion Preservation

By Product

- Thoracic

- Lumbar

- Cervical

- Interbody

- Kyphoplasty

- Artificial Discs

- MIS

- Biologics

- Stimulators

By Country

- Mexico

- Brazil

- Argentina

- Chile

- Rest of Latin America

Frequently Asked Questions

What is the growth rate of the Latin America spinal implants market?

The Latin America spinal implants market is expected to grow at a CAGR of 4.57% from 2024 to 2029.

What factors are driving growth in the Latin America spinal implants market?

Factors such as increasing prevalence of spinal disorders, rising demand for minimally invasive surgeries, and a growing elderly population in the region are majorly propelling the Latin American spinal implants market.

Who are some of the major companies operating in the Latin America spinal implants market?

Medtronic, Johnson & Johnson, Zimmer Biomet, Stryker Corporation, and Globus Medical are some of the noteworthy companies in the Latin America spinal implants market.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1600

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com