Europe Spinal Implants Market Research Report By Technology, Product and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe) - Industry Analysis on Size, Share, Trends, COVID-19 Impact & Growth Forecast (2026 to 2034)

Market Size, 2025

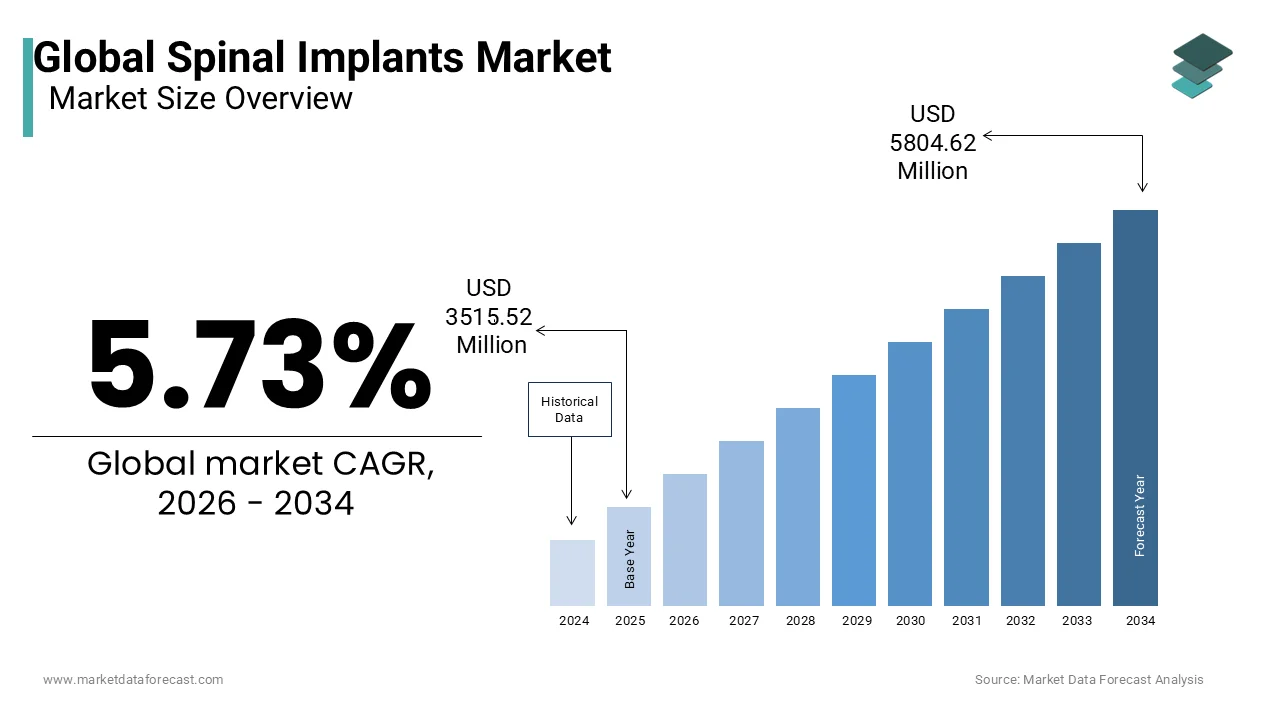

$3,515.52 MnMarket Estimate, 2026

$3,716.96 MnMarket Forecast, 2034

$5,804.62 MnCAGR, 2026–2034

5.73%Europe Spinal Implants Market Size

The europe spinal implants market was valued at USD 3515.52 million in 2025, is expected to have a 5.73% CAGR from 2026 to 2034, and be worth USD 5804.62 million by 2034 from USD 3716.96 million in 2026.

The spinal implants are surgically implanted devices designed to stabilize correct, or replace damaged spinal structures due to degenerative conditions, trauma, or deformities. These include interbody fusion cages, fixation systems, artificial discs, and dynamic stabilization devices manufactured under stringent EU Medical Device Regulation requirements. The European Medicines Agency does not regulate implants, but the European Commission’s Medical Device Coordination Group oversees conformity assessments through notified bodies, ensuring compliance with ISO 13485 and ISO 14971 risk management st,, standards. Furthermore, the EU’s Cross Border Healthcare Directive facilitates patient mobility for specialized spinal surgery, driving demand for high-quality implant systems in destination co, countries like Germany.

MARET DRIVERS

Aging Population and Rising Prevalence of Degenerative Spinal Disorders

Europe’s demographic shift toward an older population is a primary driver of spinal implant demand as age correlates strongly with degenerative spinal conditions. The growing aging population and rising prevalence of degenerative spinal disorders are propelling the growth of the European spinal implants market. Additionally, the European Osteoporosis Foundation estimates that vertebral compression fractures due to osteoporosis are increasing every year by requiring kyphoplasty or spinal stabilization. As life expectancy extends and active aging policies encourage mobility preservation, surgical correction rather than conservative management is increasingly favored, sustaining structural demand for advanced spinal implant systems across public and private healthcare settings.

Advancements in Minimally Invasive Surgical Techniques and Implant Design

Technological innovation in minimally invasive spine surgery is accelerating the adoption of next-generation implants that reduce tissue trauma, shothe rtethe n recovery, and improve. The advancements in minimally invasive surgical techniques and implant design are also boosting the growth of the European spinal implants market. Thearee techniques require specialized implants such as expandable interbody cages and ultra-low-profile pedicle screws engineered for precise navigation through narrow corridors. Companies like Medtronic and NuVasive have introduced 3D printed titanium implants with trabecular surfaces that enhance bone ingrowth clinical studies published in the European Spine Journal at 12 months, compared to smooth surface cages. Furthermore, intraoperative navigation and robotic assistance deployed in spine centers in France and the UK demand implants with embedded fiducial markers for real-time tracking.

MARKET RESTRAINTS

Stringent Regulatory Pathway Unreal-timedical Device Regulation

The EU Medical Device Regulation 2017/745 has significantly increased the evidentiary and quality management burden for spinal implant manufacturers seeking market access. The stringent regulatory pathway under the EU medical device regulation is hampering the growth of the European spinal implants market. As per the European Commission, legacy spinal devices required new clinical evaluations or post-market surveillance plans to maintain CE marking after the May 2025 transition deadline. Notified bodies now mandate extensive biocompatibility testing per ISO 10993 and long-term implantation data often exceeding five years for novel, matelong-termPEEK composites or resorbable polymers. The European Database on Medical Devices EUDAMED, although partially implemented, requires unique device identification and adverse event reporting within 15 days of discovery. According to the German Federal Institute for Drugs and Medical Devices, BfArM, average review timelines for Class III spinal implants have extended under the former Medical Device Directive. These requirements disproportionately impact small and mid-sized innovators lacking resources for large-scale clinical trials, thereby slowing the introduction of novel technologies and reinforcing the dominance of established players with legacy data portfolios.

High Cost Pressure and Reimbursement Constraints in Public Healthcare Systems

Spinal implants face intense scrutiny under Europe’s predominantly publicly funded healthcare models, where budget sustainability often outweighs technological novelty is restricting the growth of Europe's spinal implants market. As per the European Observatory on Health and Policies, EU member states apply health technology assessment to medical devices, with spinal implants frequently subjected to cost per quality adjusted life year thresholds. In France, the Haute Autorité de Santé downgraded reimbursement for certain artificial discs in 2023, citing insufficient long-term outcome differentiation from fusion cases. Similarly, the long-term Institute for Health and Care Excellence recommends spinal fusion only after 12 months of failed conservative therapy, limiting procedural volume. In Italy and Spain, budget caps on orthopedic procurement have led hospitals to adopt reverse auction systems where price outweighs design features.

MARKET OPPORTUNITIES

Integration of 3D Printing and Patient-Specific Implant Solutions

Europe is emerging as a leader in patient-specific spinal implants enabled by industrial-scale metal 3D patient-specific surgical planning. The Theindustrial-scale3D printing and patient implant solutions are specifically designed to escalate the growth of the European spinal implants market. As per the European Consortium for Additive Manufacturing, over 140 hospitals in Germany, France, and the Netherlands now use CT-based preoperative modeling to design custom interbody cages for individual endplate anatomy. The EU Horizon Europe program has allocated 62 million euros to the PERSONA SPINE initiative, developing AI-driven design automation that cuts customization lead time from six weeks to 72 hours. Regulatory pathways are adapting too, with the European Commission issuing guidance in 2023 allowing CE ma,, marking for patient-matched devices under streamlined cl, clinical evaluation if a patient-matched platform.

Expansion of Robotic-Assisted and Navigation-Guided Spine Surgery

The adoption of robotic and computer Navigation-Guidedms systems is creating implants engineered for digital surgery ecosystems, which is another attribute that is creating new opportunities for the growth of the European spinal implants market. These platforms require implants with the the Europeananic geometric tolerances, radiographic markers, and instrumentation compatibility to function w, withiclosed-loopfe feedback systems. Companies like Zimmer Biomet and Globclosed-loopnow offer “robot-ready” implant families with embedded QR codes and standardized driver interfaces, ensuring seamless integration. As hospitals invest in digital OR inf, infrastructure to meet EU quality benchmarks, they simultaneously create locked-in demand for compatible implant portfolios, transforming hardware into a component of a broader surgical intelligence platform.

MARKET CHALLENGES

Shortage of Specialized Spine Surgeons and Training Bottlenecks

The deficit in surgeons trained in advanced spinal implant procedures, with rising disease burden, is limiting the growth of the European spinal i, implants market. Fellowships, programs in complex deformity minimally invasive spine surgery accept fewer than 200 trainees annually across the EU, limiting procedural capacity. As per the European Association of Neu, Neurological Surgeons, a few spinal fusion cases in Poland and Romania are referred to neighboring countries due to a lack of local expertise. Furthermore, the EU Medical Device Regulation requires surgeon training logs as part of post-market clinical follow up yet standardized curricula are absent in post-market states.

Post-Market Surveillance and Long-Term Implant Performance Uncertainty

The long-term clinical performance of newer spinal implants remains uncertain due to limited real-world evidence, and fragmented post-market monitoring is additionally real-world degrading, the growth of the post-market implants market. As per the European Commission’s 2023 safety alert on certain PEEK-based cages linked to radiolucent degradation and migration in cPEEK-based gap material surveillance. Unlike pharmaceuticals, medical devices lack mandatory EU-wide registries, and data collection is siloed in national or hospital-based systems, with inconsistent coding. Until robust longithospital-based generated through mandatory registries and standardized endpoints, both clinicians and payers will remain cautious about adopting novel implants by slowing innovation diffusion despite regulatory approval.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Technology, Product, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Medtronic, plc (Ireland), DePuy Synthes (U.S.), Stryker Corporation (U.S.), NuVasive, Inc. (U.S.), Zimmer Biomet Holdings, Inc. (U.S.), Globus Medical, Inc. (U.S.), Alphatec Holdings, Inc. (U.S.), Orthofix International N.V. (Netherlands), K2M Group Holdings, Inc. (U.S.), and RTI Surgical, Inc. (U.S.) |

SEGMENTAL ANALYSIS

By Technology Insights

The Spinal Fusion and Fixation Technologies segments accounted in holding 58.3% of the European spinal implants market share in 2025. Spinal fusion remains the gold standard for managing degenerative disc disease, spondylolisthesis, and spinal instability across Europe due to decades of validated outcomes and procedural familiarity. The European Federation of Neurological Societies reaffirms fusion as the first-line surgical intervention for symptomatic stenosis, with 75% long-term pain reduction in Level I evidence. National guidelines in long-term France mandate fusion for cases with >3 millimeters of vertebral slippage, further entrenching its use.

The motion preservation technologies segment is projected to grow at a CAGR of 9.8% in next coming years owing to the rising demand for anatomically conservative solutions that maintain spinal kinematics and reduce adjacent segment disease. As per the European Board of Orthopaedics and Traumatology, artificial disc replacement procedures increased by 24% year on year in 2025, with Germany and Switzerland leading adoption due to favorable health technology assessment outcomes. Regulatory evolution also supports growth with the European Commission’s 20 guidance, allowing CE marking for novel non-fusion devices through abbreviated clinical pathways if biomechanically equivalent to predicate implants. Companies like LDR Medical and Globus Medical have launched next-generation discs with adaptive center of rotation mimicking natunext-generationyounger actian ve patients increasingly seek alternatives to fusion, and EU value-based healthcare frameworks prioritize long-term functional outcomes non Non-fusion solutions are gaining clinical long-term traction.

By Produnon-fusionights

In 2025, the Interbody Thoracic Fusion and Lumbar Fusion Devices segment held a prominent share of the European spinal implants market 2025. Interbody fusion devices dominate Europe due to their ability to restore disc height, correct alignment, and promote high fusion rates through anterior column load sharing. The rise of minimally invasive transforaminal and lateral lumbar interbody approaches has further accelerated adoption, with over 55% of fusions in Western Europe now using these techniques, according to the European Minimally Invasive Spine Society. 3D printed titanium cages with trabecular surfaces enhance osseointegration and reduce subsidence worldwide. Furthermore, interbody devices are reimbursed as primary procedural components under DRG codes in 23 EU countries, ensuring consistent hospital procurement.

The spine biologics segment is expected to grow at a CAGR of 11.2% during the forecast periodrivenn by the imperative to enhance fusion success and reduce reliance on autograft harvesting. The European Medicines Agency’s 2023 classification of certain demineralized bone matrices as Class III medical devices has improved safety oversight and clinician confidence. Clinical trials published in the European Spine Journal demonstrate that recombinant human bone morphogenetic protein 2 increases fusion rates to 95% in smokers with a high-risk group historically prone to pseudoarthrosis. Additionally, EU Horizon Europe funding has supported the development of next-generation biologics, including stemcell-seeded scaffolds and genext-generationtrices now, in Phase II trcell-seededden and the Netherlands.

COUNTRY LEVEL ANALYSIS

Germany Spinal Implants Market Analysis

Germany was the top performer of the European spinal implants market by holding 28.3% of the share in 2025, with European world-class spine surgery centers having high procedural volumes and an early adoption of advanced technologies. Over 120,000 spinal implant procedures were performed in 2025, according to the German Society for Orthopaedics and Trauma Surgery, with tertiary hospitals in Berlin,n Muni, and Heidelberg serving as r,, referral hubs for complex cases from across,s Europe. The country’s DRG reimbursement system fully covers robotic-assisted fusion and 3D printed implants, creating financial viability. Germany also hosts leading research institutions like the Charité Center for Musculoskeletal Surgery, which partners with industry on next-generation motion preservation trials.

France Spinal Implants next-generation

France's growth is driven by centralized clinical guidelines and standards. Public hospitals perform 75% of spinal procedures under fixed tariff schemes that prioritize cost-effective high-volume devices, yet still reimburse biologics. For a cost-effective high-volume national registr launched in 2022, now tracks over50,0000 annual procedures, real-time outcome onitori monitoring0nters like Pitié Sa, lpêtriè and and,real-timemepioneersr endoscopic decompression and cervical disc arthroplasty within regulated pathways. This balance of fiscal discipline and clinical rigor ensures sustainable high-quality care and steady market growth anchored in public health policy.

United Kingdom Spinal Implants Market Analysis

The United Kingdom market growth is likely to grow with the strong emphasis on cost effectiveness, and National Institute for Health and Care Excellence guidelines restrict spinal fusion to cases with confirmed neurological deficit or failed 12-month conservative management, limiting volume but ensuring high clinical justification. The adoption of spine biologics is growing under the Innovation and Technology Payment Program, which fast-tracks high-value devices like osteoinductive scaffolds.

Italy Sfast-tracks high-value Analysis

Italy's market growth is driven by high procedural throughput and a vibrant private hospital sector. Regions like Lombardy and Emilia Romagna have integrated robotic spine systems into both public and private settings, accelerating the adoption of advanced fixation and interbody devices. It,aly’s national health service reimburses spinal fusion comprehensively while allowing top-up payments for innovative biologics or motion preservation by a top-up hybrid model that supports both access and choice.

COMPETITIVE LANDSCAPE

The European spipost-markets market is characterized by intense competition among global medtech giants who differentiate through technological sophistication, clinical evidence, and service integration rather than price. Regulatory compliance und, er the EU Medical Device Regulation acts as a significant barrier, favoring established players with legacy data and robust quality systems. Competition centers on innovation in biomaterials, minimally invasive approaches, and digital surgery enablement with co, coco-companiesoto-toend-to-enddural solutions. National health care systems exert cost pressure, yet premium reimbursement exists for technologies demonstrating supe,,rior long-term outcomes. Smaller innovators struggle to scale due to limited-term clinical trial resources and fragmented reimbursement landscapes. Strategic partnerships with academic hospitals, spine registries,s,a n d robotic platform developers are critical for ma,,rket validation.

KEY MARKET PLAYERS

Some of the prominent companies operating in the European spinal implants market.

- Medtronic, plc (Ireland)

- DePuy Synthes (U.S.)

- Stryker Corporation (U.S.)

- NuVasive, Inc. (U.S.)

- Zimmer Biomet Holdings, Inc. (U.S.)

- Globus Medical, Inc. (U.S.)

- Alphatec Holdings, Inc. (U.S.)

- Orthofix International N.V. (Netherlands)

- K2M Group Holdings, Inc. (U.S.)

- RTI Surgical, Inc. (U.S.)

TOP LEADING PLAYERS IN THE MARKET

- Medtronic is a global leader in spinal technologies with a deeply entrenched presence across Europe’s leading orthopedic and neurosurgical centers. The company offers a comprehensive portfolio including interbody fusion systems, posterior fixation platforms, motion preservation devices, CT with EU Medical Device Re, Regulation. Medtronic has strengthened its position by integrating its Mazor X robotic guidance system with inext-generation3D printed titanium implants tailored for European sun next generations. Recently, it launched the InQuatro lateral interbody system in Germany and France, designed for minimally invasive lumbar fusion with enhanced endplate contact. The company also partners with European spine registries to generate real-world evidence supporting reimbursement and clinical adoption. Real-world to surgeon training through the Medtronic Spine Academy ensures consistent technique standardization across diverse healthcare systems.

- Johnson & Johnson MedTech operating through DePuy Synthes is a major force in the European spine ndimplantnmarkeket,, known for its innovation in biologics and non-invasive solutions. The company’s Viper Prime fixation system and CONCORDE Clear interbody cage are widely used in complex deformity and degenerative cases. DePuy Synthes recently introduced its ENTRÉE lateral access platform across Western Europe, enabling safer transpsoas approaches with integrated neuromonitoring. It also expanded its collaboration with European hospitals on the VELYS Robotic-Assisted Solution for forspine-enhancingg procedural accuracy. The company actively participates in spine-enhancing research consortia focused on regenerative biomaterials and has aligned its portfolio with value-based healthcare metrics by publishing long-term outcome data from the Scandinavian Spine Registry. This long-term approach reinforces trust among clinicians and payers alike.

- Stryker is a key player in Europe’s spinal market, leveraging its proprietary 3D printing capabilities and robotic integration to differentiate its offerings. The company’s Tritanium PL Posterior Lumbar and C Anterior Cervical cages feature porous titanium structures that promote bone ingrowth and are CE marked under the new Medical Device Regulation. Stryker has accelerated adoption of its Mako Spine platform in the U.S., Germany, and Aly al, enabling precise implant placement in fusion proce,,dures. R, Recently, I,t launched the Centinel Ti 3D printed interbody system with controlled porosity validated in multicenter European trials. Stryker also invests in digital surgery ecosys, terms including intraoperative imaging and data analytics, to support sur, geon decision-making.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the European spinal implants market are investing in 3D printed porous titanium implants to enhance osseointegration and reduce revision rates. They are integrating robotic and navigation platforms with proprietary implant systems to create closed-loop surgical ecosystems. Companies are generating real-world closed-loop participation in national and multinational real-world industries to support reimbursement and clinical guidelines. They are aligning product development with EU Medical Device Regulation requirements, including comprehensive biocompatibility and post-market surveillance,e planned.

MARKET SEGMENTATION

This research report on the europe spinal implants market has been segmented and sub-segmented into the following categories.

By Technology Insights

- Spinal Fusion and Fixation Technologies

- Vertebral Compression Fracture Treatment

- Motion Preservation/Non-Fusion Technologies

- Spinal Decompression

By Product Insights

-

Thoracic Fusion and Lumbar Fusion Devices

-

Posterior Thoracic Fusion and Lumbar Fusion Devices

-

Interbody Thoracic Fusion and Lumbar Fusion Devices

- By Approach

- Anterior Lumbar Interbody Fusion Devices

- Posterior Lumbar Interbody Fusion Devices

- Transforaminal Lumbar Interbody Fusion Devices

- Axial Lumbar Interbody Fusion Devices

- By Material

- Non-Bone Interbody Fusion Devices

- Bone Interbody Fusion Devices

- Anterior Thoracic Fusion and Lumbar Fusion Devices

- Cervical Fusion Devices

- Anterior Cervical Fusion

- Anterior Cervical Plates

- Cervical Interbody Fusion Devices

- Anterior Cervical Screw Systems

- Posterior Cervical Fusion

- Posterior Cervical Plates

- Posterior Cervical Screws

- Posterior Cervical Rods

- Spine Biologics

- Demineralized Bone Matrix

- Bone Morphogenetic Proteins

- Bone Substitutes

- Machined Bones

- Cell-Based Matrices

- Allografts

- Vcf Treatment Devices

- Balloon Kyphoplasty Devices

- Vertebroplasty Devices

- Spinal Decompression

- Discectomy

- Laminoplasty, Laminectomy, and Laminotomy

- Foraminotomy and Foraminectomy

- Facetectomy

- Corpectomy

- Non-Fusion Devices

- Dynamic Stabilization Devices

- Interspinous Process Spacers

- Pedicle-Based Dynamic Rod Devices

- Facet Replacement Products

- Artificial Discs

- Artificial Cervical Discs

- Artificial Lumbar Discs

- Annulus Repair Devices

- Nuclear Disc Prostheses

- Spine Bone Stimulators

- Non-Invasive Spine Bone Stimulators

- Pulsed Electromagnetic Field Devices

- Cc and Cmf Devices

- Invasive Spine Bone Stimulators

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1.What drives growth in the Europe Spinal Implants Market?

Growth in the Europe Spinal Implants Market stems from rising spinal disorders,

aging population, and demand for minimally invasive surgeries and advanced implants.

2. Who are the top companies in the Europe Spinal Implants Market?

Medtronic and DePuy Synthes lead the Europe Spinal Implants Market, dominating

segments like thoracolumbar fixation, interbody devices, and VCF treatment.

3. What are the main products in the Europe Spinal Implants Market?

Key products in the Europe Spinal Implants Market include fusion devices, non-fusion

devices, spine biologics, bone growth stimulators, and VCF treatment devices.

4. What trends shape the Europe Spinal Implants Market?

Trends in the Europe Spinal Implants Market include minimally invasive techniques,

3D-printed patient-specific implants, and growth in spine biologics for better fusion.

5. How do minimally invasive surgeries impact the Europe Spinal Implants Market?

MIS boosts the Europe Spinal Implants Market by reducing recovery time, pain,

and hospital stays, with innovations in navigation and robotic-assisted procedures

6. What is Italy's position in the Europe Spinal Implants Market?

Italy is the fastest-growing in the Europe Spinal Implants Market, due to

healthcare investments, spinal health awareness, and advanced surgical adoption.

7. What challenges face the Europe Spinal Implants Market?

Challenges in the Europe Spinal Implants Market include high costs, complex

reimbursements, regulations, and awareness gaps for new treatments.

8. What future opportunities exist in the Europe Spinal Implants Market?

Opportunities in the Europe Spinal Implants Market involve non-fusion tech,

robotics, smart implants, and retail sales growth for advanced devices.

9. Q: What is the CAGR forecast for the Europe Spinal Implants Market?

The European Spinal Implants Market expects a CAGR of 5.73% CAGR from 2025 to 2033

fueled by technological advances and rising spinal procedure demand

10. What is the role of fusion devices in the Europe Spinal Implants Market?

Fusion devices lead the Europe Spinal Implants Market with 38-60% share, used

for spine stabilization, deformity correction, and degenerative disease treatment.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com