Global Medical Billing Outsourcing Market Size, Share, Trends, and Growth Analysis Report, Segmented By Service, Type of Deployment, End User, & Region (North America, Europe, Latin America, Asia Pacific, Middle East & Africa), Industry Forecast From 2026 to 2034

Global Medical Billing Outsourcing Market Size

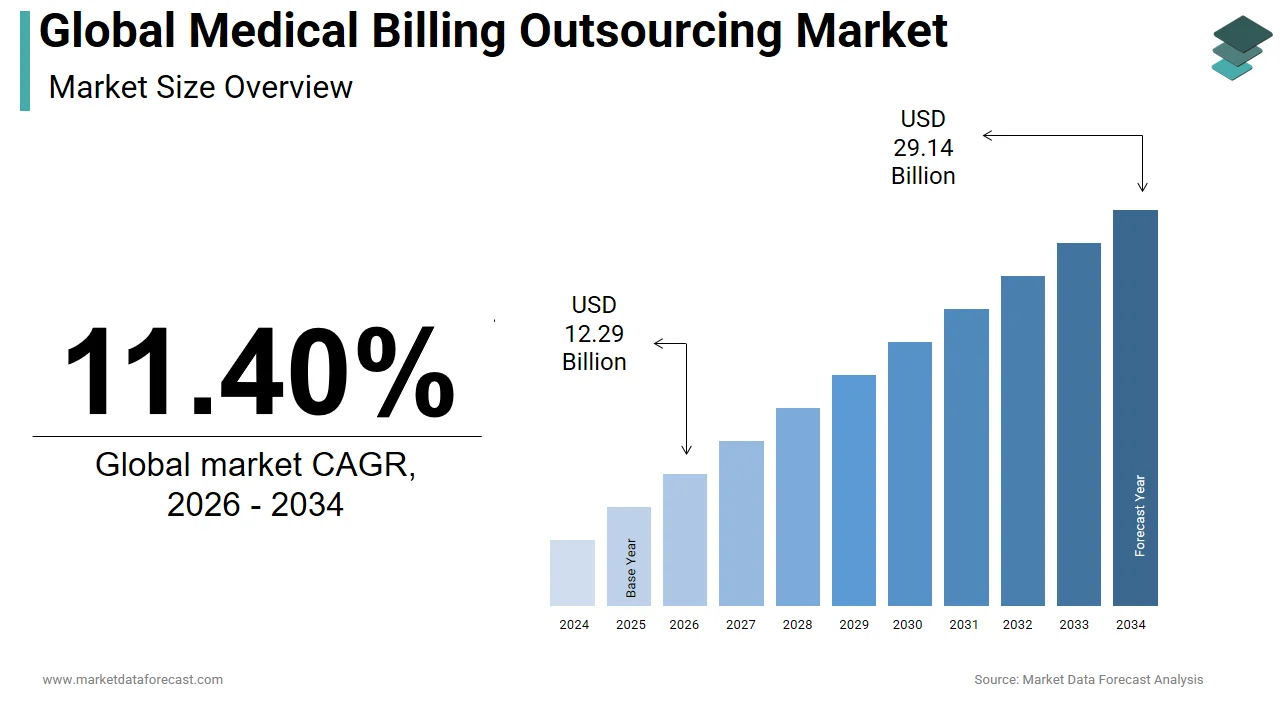

The size of the global medical billing outsourcing market was worth USD 11.03 billion in 2025. The global market is anticipated to grow at a CAGR of 11.40% from 2026 to 2034 and be worth USD 29.14 billion by 2034 from USD 12.29 billion in 2026.

Medical billing outsourcing is the delegation of revenue cycle management tasks such as coding, claims processing, payment posting, and denial management to third-party service providers. These specialized firms streamline administrative operations for healthcare organizations, enabling them to maintain regulatory compliance, reduce operational burdens, and enhance cash flow efficiency. As per the American Medical Association, physicians spend nearly 15.5 hours per week on average dealing with insurance-related administrative tasks, significantly detracting from patient care.

MARKET DRIVERS

Growing Administrative Burden on Healthcare Providers

Healthcare providers face mounting administrative responsibilities that directly impact operational efficiency, and clinical focus is escalating the growth ofthe medical billing outsourcing market. The complexity of coding systems such as ICD-10 and CPT, coupled with frequent updates from payers and regulatory bodies, increases the likelihood of claim errors and denials. The American Academy of Family Physicians reports that nearly 30% of initial claims are denied due to coding inaccuracies or documentation gaps, leading to delayed reimbursements. Outsourcing mitigates these inefficiencies by leveraging expert teams equipped with advanced software and continuous training.

Escalating Costs of In-House Billing Infrastructure

Maintaining an internal medical billing department entails substantial financial and human resource investments, which also enhances the growth of the medical billing outsourcing market. Small and mid-sized practices, which constitute over 88% of physician-owned clinics in the United States, as reported by the American Medical Association, often lack the scale to justify such overheads. Additionally, the integration and maintenance of billing software, compliance tools, and cybersecurity measures further inflate operational costs.

MARKET RESTRAINTS

Data Security and Patient Privacy Concerns

Outsourcing medical billing necessitates the transfer of sensitive patient health and financial information to third-party vendors, which is restraining the growth of the medical billing outsourcing market. Many of these incidents originated from third-party vendors with inadequate cybersecurity frameworks. Smaller outsourcing firms may lack the infrastructure to implement end-to-end encryption, multi-factor authentication, or regular security audits.

Variability in Service Quality and Vendor Reliability

The medical billing outsourcing market is fragmented, with numerous providers offering inconsistent service standards, which is limiting the growth of the medical billing outsourcing market. A 2022 survey by the Healthcare Financial Management Association revealed that 37% of hospitals reported dissatisfaction with outsourced billing vendors due to delayed claim submissions, poor denial management, and a lack of transparency. Many vendors lack domain-specific expertise, particularly in handling specialty-specific coding such as oncology or cardiology, which require a nuanced understanding of procedural nuances. Turnover rates among billing staff at outsourcing firms can exceed 30% annually, as noted by the International Association of Outsourcing Professionals, disrupting continuity and accuracy. Furthermore, inadequate customer support and limited integration capabilities with electronic health record systems hinder seamless operations.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence in Revenue Cycle Management

The incorporation of artificial intelligence (AI) and machine learning into medical billing processes is accelerating the growth of the medical billing outsourcing market. AI-powered platforms can automate claim validation, detect coding errors in real time, and predict payer behavior to reduce denials. Outsourcing firms leveraging AI-driven analytics report a 40% improvement in first-pass claim acceptance rates, as demonstrated by early adopters such as GeBBS Healthcare Solutions. Additionally, natural language processing enables automated extraction of clinical data from physician notes, reducing manual input errors. As per the World Economic Forum, 60% of healthcare organizations plan to invest in AI-enabled revenue cycle tools by 2025.

Expansion of Telehealth and Decentralized Care Models

The rapid growth of telehealth services has created a surge in hybrid billing requirements is quietly enhancing the growth of the medical billing outsourcing market. According to the Centers for Disease Control and Prevention, telehealth utilization in the U.S. stabilized at nearly 30 times pre-pandemic levels by 2023, with over 150 million virtual visits recorded annually. These services involve complex billing codes, varying state-specific reimbursement rules, and cross-jurisdictional compliance challenges. Outsourcing providers with expertise in telemedicine billing are uniquely positioned to manage these intricacies. The American Telemedicine Association notes that nearly 40% of telehealth claims face initial denial due to incorrect modifiers or payer-specific policy mismatches. Specialized billing firms can navigate this complexity with dedicated payer rule databases and real-time compliance tracking. As decentralized care models continue to expand, including remote monitoring and mobile clinics, the demand for agile, tech-enabled billing partners will grow, enabling outsourcing companies to offer scalable, adaptive solutions tailored to emerging care delivery paradigms.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Service, Type of Deployment, End User, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | McKesson Corporation, eClinicalWorks, R1 RCM, Inc., Kareo, Inc., Allscripts (Veradigm). |

SEGMENTAL ANALYSIS

By Service Insights

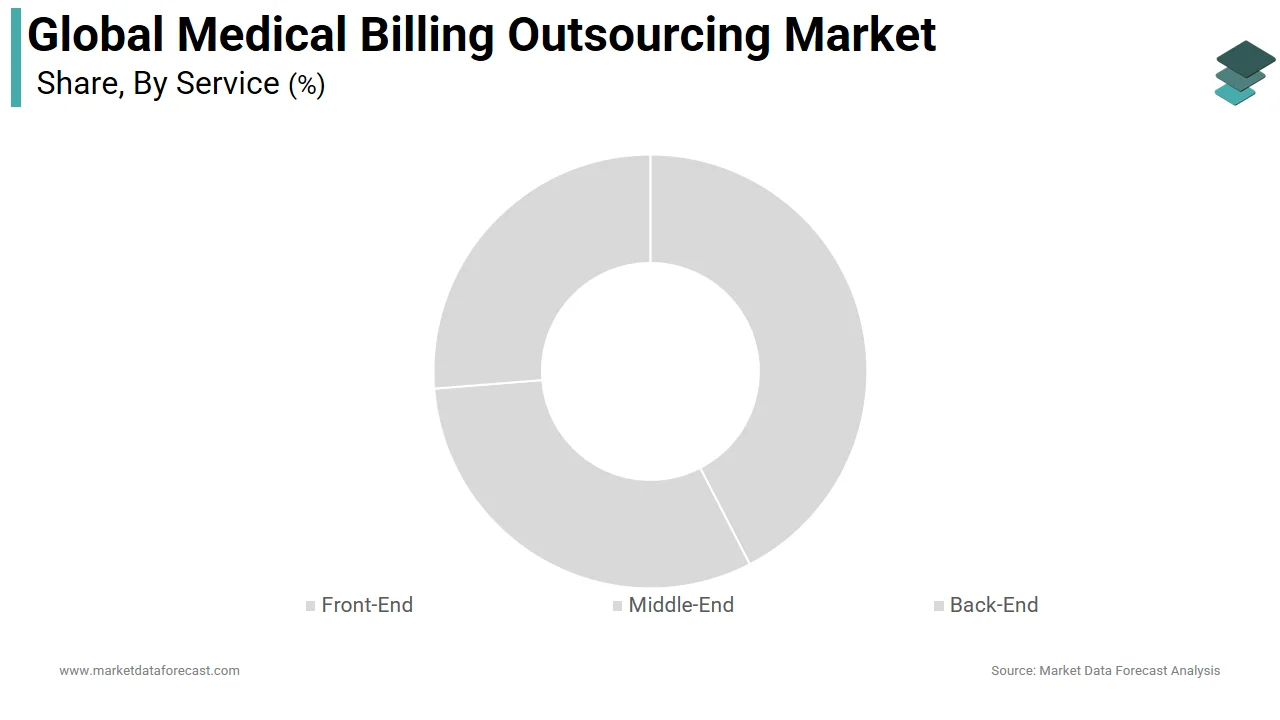

The back-end services segment was the largest and held 48.2% of the medical billing outsourcing market share in 2024, with the high complexity and financial impact of post-claim activities such as payment posting, denial management, and accounts receivable follow-up. Outsourcing firms specializing in back-end services have demonstrated the ability to recover up to 65% of denied claims through systematic appeals and root-cause analysis. According to the American Medical Association, manual denial resolution consumes an average of 16 hours per week for mid-sized practices, severely straining internal resources.

The middle-end services segment is projected to register a CAGR of 12.7% from 2025 to 2033, with increasing reliance on clinical coding, charge capture, and billing audit functions that sit at the core of revenue cycle accuracy. Middle-end outsourcing mitigates such risks by ensuring compliance with evolving coding standards like ICD-10 and CPT, particularly as new telehealth and chronic care management codes are introduced. Additionally, regulatory scrutiny has intensified around documentation integrity and audit preparedness. Outsourcing providers offer real-time coding audits and compliance dashboards, reducing legal exposure. As per a 2023 KLAS Research report, 68% of hospitals now outsource at least part of their middle-end coding operations to ensure accuracy and withstand payer audits.

By Type of Deployment Insights

The cloud-based deployment model segment was the largest and held a dominant share of the medical billing outsourcing market in 2024 with its inherent advantages in scalability, remote accessibility, and lower capital expenditure. According to the Office of the National Coordinator for Health Information Technology, over 90% of U.S. hospitals now use interoperable EHR systems, most of which are cloud-compatible.

The cloud-based deployment segment is projected to expand at a CAGR of 13.4% throughout the forecast period with the rising investments in cybersecurity, interoperability standards, and disaster recovery capabilities inherent to cloud platforms. According to the Healthcare Information and Management Systems Society (HIMSS), cloud-based systems experience 50% fewer downtime incidents than on-premise servers, a major factor for maintaining continuous billing operations. Moreover, the shift toward value-based care demands real-time analytics and performance tracking, which cloud platforms facilitate through integrated dashboards and AI-driven insights. The scalability of cloud systems also supports rapid integration with telehealth platforms and mobile clinics, which are expanding across urban and rural areas.

By End User Insights

Hospitals was the largest by occupying 45.3% of the medical billing outsourcing market share in 2024, with the sheer volume and complexity of transactions processed by acute care facilities. According to the American Hospital Association, the average U.S. hospital handles over 25,000 claims per month, involving multiple departments, payers, and reimbursement models. Outsourcing enables hospitals to deploy specialized teams focused on high-value denial recovery, regulatory compliance, and payer negotiations. Additionally, the transition to value-based reimbursement under Medicare’s Hospital Value-Based Purchasing Program has increased the need for accurate documentation and risk adjustment coding. Large health systems, including those in the Mayo Clinic and Cleveland Clinic networks, have increasingly partnered with third-party vendors to standardize billing across multi-state operations.

The physicians’ offices segment is swiftly emerging with a CAGR of 12.9% from 2025 to 2033, with the financial and operational pressures faced by independent and small-group practices. According to the American Medical Association, over 88% of physician practices in the U.S. employ fewer than 10 doctors, many of whom lack the resources to maintain in-house billing teams. Furthermore, the administrative burden of managing insurance claims has led to physician burnout, with a 2023 JAMA Network Open study revealing that 58% of primary care physicians consider reducing clinical hours due to paperwork overload. Outsourcing alleviates this strain by providing access to expert coders, automated claim scrubbing, and denial management at a fraction of the cost.

REGIONAL ANALYSIS

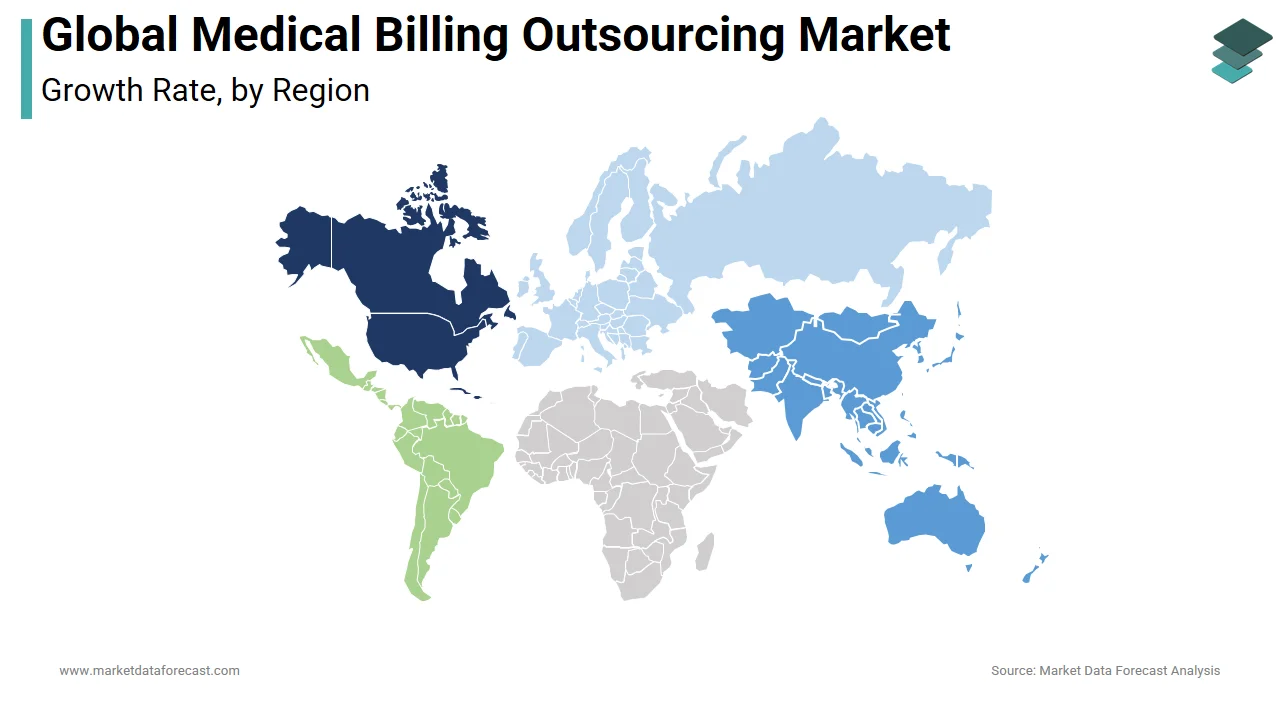

North America Medical Billing Outsourcing Market Analysis

North America was the top performer of the global medical billing outsourcing market by holding 47.3% of the share in 2024. The widespread adoption of EHRs, mandated under the HITECH Act, has further amplified the need for integrated, compliant billing solutions. As per the Centers for Medicare & Medicaid Services, improper payments in federal healthcare programs exceeded $77 billion in 2022, with billing inaccuracies being a primary contributor.

Europe Medical Billing Outsourcing Market Analysis

Europe medical billing outsourcing market was positioned second with a 23.2% share in 2024. While European systems are predominantly public, countries like Germany, the UK, and France are increasingly outsourcing non-clinical functions to improve efficiency. According to the European Commission, healthcare administrative costs in EU member states average 8–10% of total spending, with rising pressure to reduce waste.

Asia Pacific Medical Billing Outsourcing Market Analysis

Asia Pacific medical billing outsourcing market growth is likely to grow with the rapid healthcare digitization and rising private healthcare investment. Countries like India, China, and South Korea are modernizing their medical infrastructure, with India’s National Digital Health Mission aiming to create unified health records for 1.4 billion citizens. According to the World Bank, healthcare expenditure in the region is growing at 7.5% annually, outpacing GDP growth in many countries. This has prompted hospitals and clinics to partner with domestic and international outsourcing firms.

Latin America Medical Billing Outsourcing Market Analysis

Latin America medical billing outsourcing market growth is due to expanding private healthcare sectors and insurance penetration. According to the Pan American Health Organization, private health expenditures in Latin America have risen by 6.8% annually over the past five years, increasing the volume of billable services. Brazil’s National Supplementary Health Agency reports that over 47 million people are covered by private health plans, generating complex billing requirements. However, inconsistent regulatory frameworks and data protection laws have slowed large-scale outsourcing. Recent initiatives, such as Mexico’s digital health strategy launched in 2023, aim to standardize electronic billing and interoperability.

Middle East & Africa Medical Billing Outsourcing Market Analysis

Middle East & Africa medical billing outsourcing market growth is anticipated to have a steady pace in the coming years. The United Arab Emirates and Saudi Arabia are spearheading healthcare modernization under Vision 2030 and similar economic diversification plans. According to the Dubai Health Authority, the UAE aims to digitize 100% of health records by 2025, creating demand for integrated revenue cycle solutions. Saudi Arabia’s Ministry of Health has mandated electronic billing for all private providers, effective 2023, accelerating outsourcing adoption.

COMPETITIVE LANDSCAPE

The medical billing outsourcing market is marked by intense competition driven by technological differentiation and service specialization. Global players compete with regional BPO providers on accuracy, compliance, and turnaround time, while leveraging automation to reduce costs and improve performance. The market is witnessing a shift from transactional outsourcing to outcome-based contracts, where vendors are held accountable for first-pass claim acceptance and denial recovery rates. Providers with advanced analytics, AI-powered coding engines, and integrated compliance frameworks are gaining a competitive advantage.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global medical billing outsourcing market include

- Mckesson Corporation

- EClinicalWorks

- R1 RCM, Inc.

- Kareo, Inc.

- Allscripts (Veradigm)

Top Players in the Medical Billing Outsourcing Market

- R1 RCM Inc. is a leading innovator in revenue cycle management, offering end-to-end medical billing outsourcing solutions across hospitals and health systems. In the Asia Pacific region, the company has expanded its footprint by establishing strategic partnerships with healthcare providers in India and Australia, focusing on digitizing revenue operations and improving claim accuracy. R1 leverages AI-driven analytics and automation to optimize billing workflows, reduce denials, and accelerate cash flow. In 2023, it launched a cloud-based platform tailored for cross-border billing compliance, enabling seamless integration with local payer systems. The company also invested in training centers in Hyderabad to develop a skilled workforce fluent in U.S. and regional coding standards.

- Cotiviti provides data-driven revenue optimization solutions, specializing in risk adjustment, audit support, and claims management for healthcare organizations. While historically focused on North America, Cotiviti has intensified its engagement in the Asia Pacific market through advisory collaborations with payers and providers in Singapore and Japan. The company supports healthcare entities transitioning to value-based models by offering outsourced billing analytics and compliance validation services. It has also developed localized versions of its audit tools to align with regional coding frameworks such as the Japanese Diagnosis Procedure Combination (DPC) system.

- Wipro, through its healthcare BPO division, is a major force in medical billing outsourcing, serving clients across the U.S., Europe, and increasingly in the Asia Pacific region. The company operates large-scale delivery centers in Bangalore, Chennai, and Pune, providing 24/7 billing support with expertise in HIPAA-compliant data handling and multi-payer adjudication. Wipro has strengthened its regional presence by collaborating with Australian private hospitals and Indian diagnostic chains to streamline revenue cycles using automation and robotic process automation (RPA). The company also achieved ISO 27001 and HITRUST certifications to reinforce data security credibility.

Top Strategies Used by the Key Market Participants

Key players in the medical billing outsourcing market deploy a combination of technological innovation, geographic expansion, and strategic alliances to promote their positions. Firms are integrating artificial intelligence and machine learning to automate coding, reduce claim denials, and enhance revenue recovery. Cloud-based platforms are being adopted to ensure scalability, real-time monitoring, and seamless integration with electronic health records. Companies are expanding delivery centers in low-cost regions like India and the Philippines to improve operational efficiency. Strategic partnerships with EHR vendors and healthcare systems enable end-to-end service integration. Additionally, achieving stringent data security certifications such as HITRUST and GDPR compliance strengthens client trust. Talent development and domain-specific training programs ensure adherence to evolving coding standards and payer requirements across global markets.

MARKET SEGMENTATION

This research report on the global medical billing outsourcing market has been segmented and sub-segmented into the following categories.

By Service

- Front-End

- Middle-End

- Back-End

By Type of Deployment

- On-Premise

- Cloud-based

By End User

- Hospitals

- Physicians’ Offices

- Ambulatory/Other Providers

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

1. What is the Medical Billing Outsourcing Market?

The Medical Billing Outsourcing Market includes third-party companies managing healthcare billing tasks such as claims processing, coding, payment posting, and denial management for hospitals, clinics, and private practices worldwide

2. What are common service segments in the Medical Billing Outsourcing Market?

Key segments are front-end (e.g., patient registration), middle-end (claims submission, coding), and back-end (AR follow-up, denial management, payment posting)

3. Why are healthcare providers using medical billing outsourcing?

Outsourcing offers greater compliance, fewer billing errors, lower administrative costs, faster revenue cycles, and allows providers to focus on patient care

4. Which regions lead the Medical Billing Outsourcing Market?

North America dominates with up to 55% share in 2025, while Asia Pacific is the fastest-growing region, driven by increased healthcare digitalization and cost optimization

5. What trends are shaping the Medical Billing Outsourcing Market?

AI and automation, cloud-based RCM platforms, patient-centric billing solutions, remote billing growth post-COVID-19, and tightening regulatory requirements drive market evolution

6. Who are the main customers in the Medical Billing Outsourcing Market?

Hospitals, ambulatory surgery centers, physician groups, specialty clinics, diagnostic labs, and home healthcare providers are top users of outsourced billing services

7. How does telehealth growth impact the Medical Billing Outsourcing Market?

Telehealth expansion increases demand for specialized billing expertise and complex claims processing, further driving adoption of outsourced billing services

8. What is the impact of regulatory compliance on the Medical Billing Outsourcing Market?

Meeting HIPAA, payer-specific, and international data protection rules is critical—outsourcing partners with expertise in compliance are preferred by providers

9. What are key challenges for the Medical Billing Outsourcing Market?

Challenges include managing sensitive patient data, integration with diverse EHR systems, ongoing regulation updates, and ensuring quality/cybersecurity standards

10. How do providers select a medical billing outsourcing partner?

Providers consider specialization, data security credentials, track-record in reducing errors/denials, technology stack (cloud/AI), and integration capabilities with their IT systems

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com