Middle East and Africa Ophthalmic Drugs Market Size, Share, Trends & Growth Forecast Report By Therapeutic Class, Product Type, Distribution Channel, Disease Indication, Dosage Form, Technology and Country (KSA, UAE, Israel, Rest of GCC, South Africa, Ethiopia, Kenya, Egypt, Sudan, Rest of MEA) – Industry Analysis From 2025 to 2033.

Middle East and Africa Ophthalmic Drugs Market Size

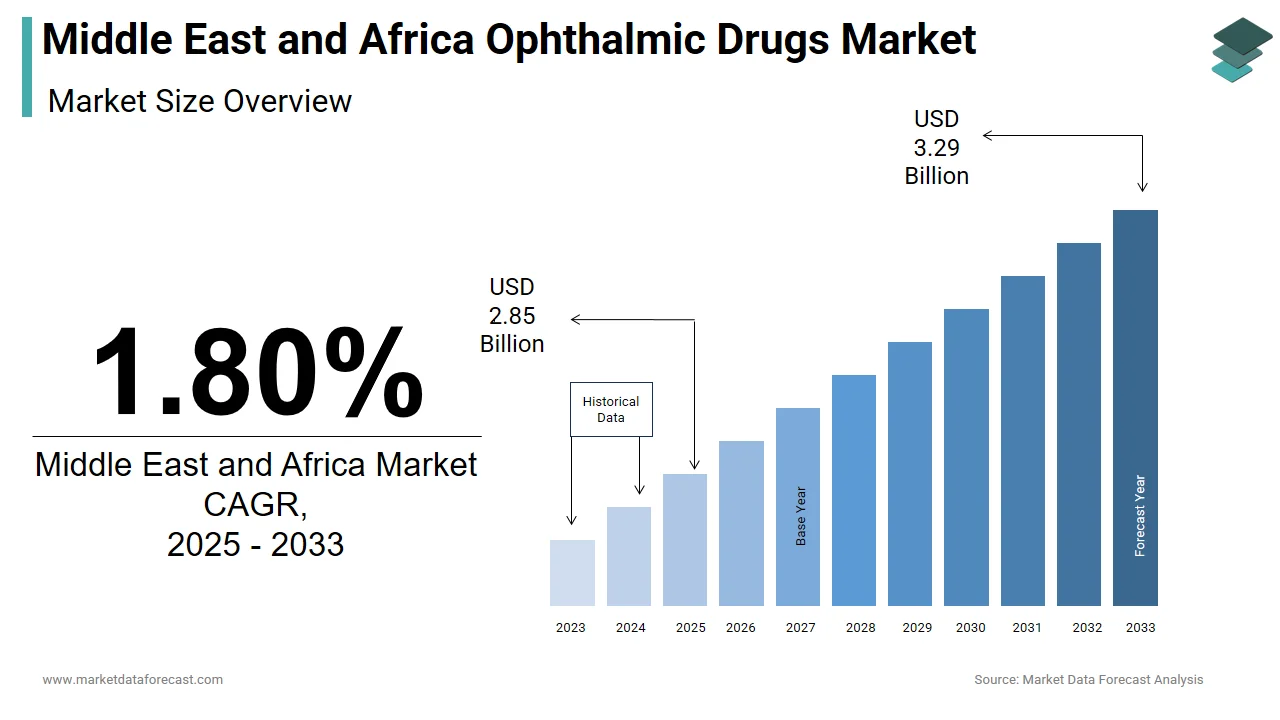

The size of the Middle East and Africa ophthalmic drugs market was worth USD 2.80 billion in 2024. The market is anticipated to grow at a CAGR of 1.80% from 2025 to 2033 and be worth USD 3.29 billion by 2033 from USD 2.85 billion in 2025.

MARKET DRIVERS

The rise in the prevalence of eye diseases such as glaucoma, cataract, macular degeneration, and the spike in demand for ophthalmic medications and increased investment in R&D activities by various healthcare businesses are a few factors promoting the growth of the ophthalmic drugs market in the MEA region. Because intraocular lenses are implanted in humans when the natural lens is surgically removed due to cataracts, and phacoemulsification devices are required to perform cataract surgeries, an increase in the incidence of ocular and ophthalmic conditions is driving demand for intraocular lenses and phacoemulsification devices. The rise in middle-class families, advancements in medical infrastructure, and rising health insurance coverage in the Middle East and Africa are expected to impact this growth substantially. In addition, the ophthalmic medication industry is bolstered by introducing new effective ophthalmic drugs. In addition, pollution of the air and water put the eyes in more danger. As a result, demand for the medications increases, driving the Middle East and Africa ophthalmic drug market forward.

The market is further expected to be favored by the increase in demand for ophthalmic medications, increased awareness about healthcare to avoid the risk of eye diseases, and government initiatives to develop and manufacture various combinations of ophthalmic drugs. Additionally, increased awareness of the prevention and treatment of eye disease and increased demand for sophisticated healthcare facilities and significant companies operating in the area are driving the market forward. Furthermore, over the forecast period, the growing prevalence of eye-related diseases such as diabetic retinopathy, macular degeneration, and presbyopia is likely to drive market expansion. Furthermore, ophthalmic pharmaceutical firms are pursuing strategic collaborations, acquisitions, and partnerships to extend their product pipeline with new clinical-stage opportunities, which is a positive trend.

MARKET RESTRAINTS

During the forecast period, the market growth is likely to be restricted by the length of time required to manufacture and formulate ophthalmic medications and the adverse effects of ophthalmic drugs. In addition, the ophthalmology business has a significant challenge due to a lack of health insurance among the public, particularly in this region, or a lack of insurance in nations that cover all types of IOLs or contact lenses.

SEGMENTAL ANALYSIS

By Product Type Insights

GEOGRAPHICAL ANALYSIS

Geographically, it is expected to grow robustly in the forecast period. The ophthalmological drugs market in the Middle East and Africa is primarily supported by the private sector initiatives in the United Arab Emirates and high healthcare spending in undeveloped African nations such as Rwanda, Uganda, and Malawi. The government of the United Arab Emirates has taken steps to improve ophthalmological medical care in the nation, including the creation of eye specialty hospitals throughout the country's major and semi-urban regions. The need for ophthalmic medicines is growing as the frequency of eye disorders rises. Diabetic retinopathy has been put on the priority list since diabetes has increased in many areas. Hereditary ophthalmic diseases, neurovascular retinal abnormalities, and retinoblastoma benefit from gene therapy for diagnosis and treatment. As a result, further research is needed to optimize and broaden gene therapy's applicability across ophthalmic diseases.

KEY MARKET PLAYERS

Companies leading the MEA ophthalmic drugs market profiled in the report are Carl-Zeiss AG, Ellex Medical Lasers Ltd., Hoya Corporation, Novagali Pharma S A, Abbott Medical Optics, Inc., Essilor International S.A. Other players in the market include Insight Vision Inc., Nidek Co.Ltd, Topcon Corporation, and Ziemer Ophthalmic Systems AG.

MARKET SEGMENTATION

This Middle East and Africa ophthalmic drugs market research report is segmented and sub-segmented into the following categories.

By Therapeutic Class

- Anti-inflammatory Drugs

- Anti-infective Drugs

- Anti-glaucoma Drugs

- Anti-allergy Drugs

- Anti-VEGF Agents

- Others

By Product Type

- Prescription Drugs

- Over-the-Counter Drugs

By Distribution Channel

- Hospital Pharmacies

- Online Pharmacies

- Independent Pharmacies

- Drug Stores

By Disease Indications

- Dry Eye

- Glaucoma

- Infection/Inflammation

- Retinal Disorders

- Allergy

- Uveitis

- Others

By Dosage Form

- Liquid Ophthalmic Drug Forms

- Solid Ophthalmic Drug Forms

- Semisolid Ophthalmic Drug Forms

- Multicompartment Drug Delivery Systems

- Other Ophthalmic Drug Forms

By Technology

- Biologics

- Cell Therapy

- Gene Therapy

- Drug Delivery

- Small molecule

- Others

By Country

- KSA

- UAE

- Israel

- Rest of the GCC countries

- South Africa

- Ethiopia

- Kenya

- Egypt

- Sudan

- rest of MEA

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1600

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com