Middle East and Africa Probiotics Market Research Report Segmented By Application, Form, End-User, And Country (KSA, UAE, Israel, rest of GCC countries, South Africa, Ethiopia, Kenya, Egypt, Sudan and Rest of MEA) – Analysis on Size, Share, Trends & Growth Forecast (2026 to 2034)

Middle East and Africa Probiotics Market Size

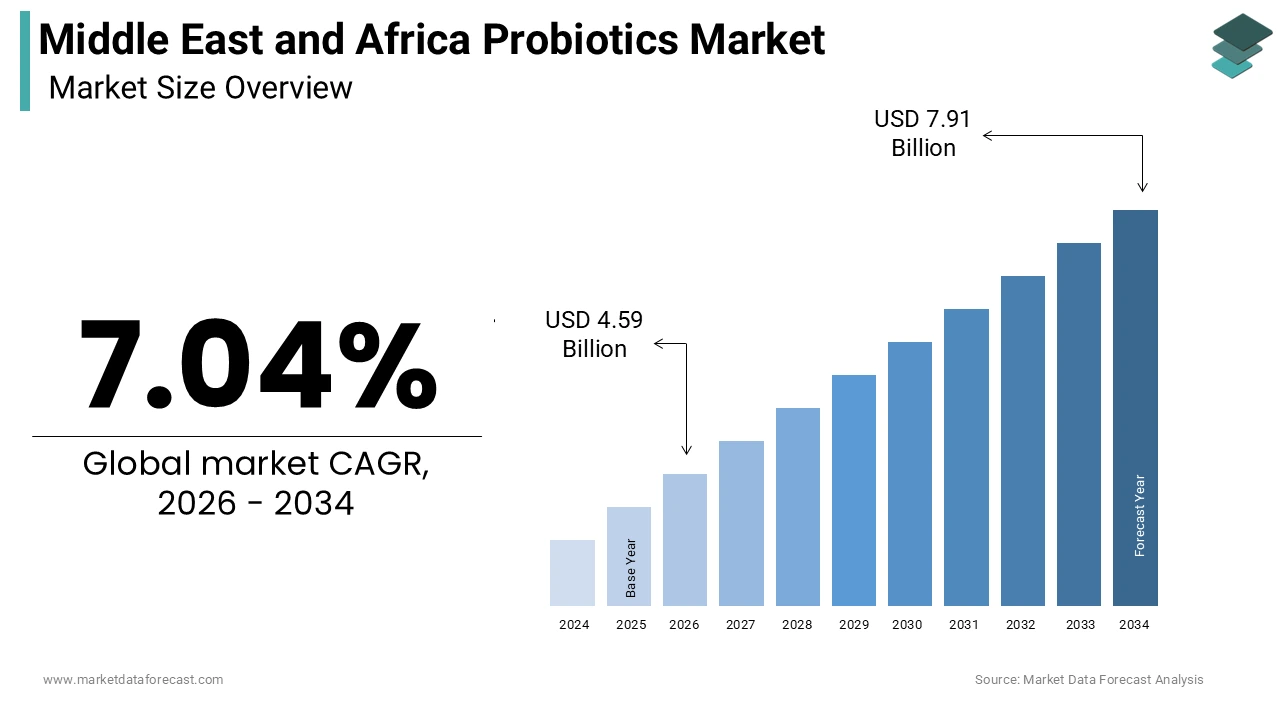

The probiotics market size in the Middle East and Africa was calculated to be USD 4.29 billion in 2025 and is anticipated to be worth USD 7.91 billion by 2034 from USD 4.59 billion in 2026, growing at a CAGR of 7.04% during the forecast period.

Probiotics are a diverse array of live microorganisms that confer health benefits to the host when administered in adequate amounts. This market primarily includes dietary supplements, functional foods, and beverages enriched with beneficial bacteria such as Lactobacillus and Bifidobacterium. The region is witnessing a paradigm shift from traditional medicinal practices toward preventive healthcare solutions, driven by increasing consumer awareness regarding gut health and its systemic impact on immunity. As per the World Health Organization, noncommunicable diseases account for approximately 37% of all deaths in the African Region (compared to 74% globally), a burden that has intensified the focus on implementing preventive policies such as the WHO Global Action Plan for NCDs, which emphasizes reducing risk factors like unhealthy diets. In the Middle East, rapid urbanization and lifestyle changes have led to a surge in metabolic disorders, prompting healthcare providers to recommend probiotic interventions. According to the Food and Agriculture Organization of the United Nations (2023), undernourishment affected nearly 282 million people in Africa (with moderate or severe food insecurity affecting 868 million), a crisis where more than one billion people are unable to afford a healthy diet, underscoring the urgent need for accessible, nutritious food systems rather than niche market trends. The cultural prevalence of fermented foods such as laban and amasi provides a foundational acceptance for probiotic variants. Government initiatives in countries like Saudi Arabia and South Africa are increasingly focusing on public health education, thereby creating a conducive environment for market expansion. The integration of modern biotechnology with traditional fermentation techniques is reshaping the product landscape, offering consumers scientifically validated health benefits while respecting regional dietary preferences and regulatory frameworks.

MARKET DRIVERS

Rising Prevalence of Gastrointestinal Disorders Drives Demand for Gut Health Solutions

The escalating incidence of gastrointestinal disorders across the region fuels the expansion of the Middle East and Africa probiotics market. Chronic conditions such as irritable bowel syndrome, inflammatory bowel disease, and general digestive discomfort are becoming increasingly common due to dietary shifts toward processed foods and high sugar intake. According to the World Gastroenterology Organisation, the global prevalence of irritable bowel syndrome ranges from 10% to 20%, though specific estimates for the Middle East often vary between 7% and 10%, with some local studies reporting higher rates in specific populations. In South Africa, studies indicate that up to 30 percent of the adult population experiences frequent digestive issues, prompting a proactive search for dietary remedies. Consumers are increasingly aware of the gut microbiome's role in overall health, leading to a preference for natural remedies over synthetic drugs. The high prevalence of Helicobacter pylori infection, which affects approximately 70 percent of the population in certain North African countries as per epidemiological studies, further necessitates adjunctive therapies such as probiotics to mitigate antibiotic side effects and improve treatment efficacy. Healthcare professionals in the region are progressively recommending probiotic supplementation alongside standard treatments to enhance patient outcomes. This medical endorsement validates the therapeutic potential of probiotics, thereby boosting consumer confidence and purchase intent. The growing body of clinical evidence supporting the efficacy of specific strains in managing diarrhea and constipation reinforces the perception of probiotics as essential health products rather than mere supplements, driving sustained demand across both urban and semi-urban demographics in the region.

Increasing Consumer Awareness Regarding Immunity and Preventive Healthcare

Heightened consumer awareness regarding immunity and preventive healthcare significantly propels the growth of the Middle East and Africa probiotics market. The post-pandemic era has instilled a lasting focus on immune resilience, with individuals actively seeking products that bolster their natural defense mechanisms. According to the World Health Organization, immunization and preventive health measures are critical in reducing the burden of infectious diseases in Africa, where respiratory and gastrointestinal infections remain the leading causes of morbidity. Probiotics are widely recognized for their ability to modulate the immune system and reduce the severity and duration of common infections. In the Gulf Cooperation Council countries, health literacy rates have improved markedly, with government campaigns emphasizing the importance of nutrition in disease prevention. As per the Saudi Ministry of Health, public awareness programs have reached millions of citizens, encouraging the incorporation of functional foods into daily diets. The rise in health-conscious millennials and Gen Z consumers, who prioritize wellness and transparency in ingredient sourcing, further accelerates market growth. Social media platforms and digital health communities play a pivotal role in disseminating information about the benefits of probiotics, reaching a broad audience across the region. In Nigeria and Kenya, mobile health applications are increasingly used to provide personalized nutrition advice, including probiotic recommendations. This digital engagement empowers consumers to make informed decisions, fostering a culture of self-care and preventive health management that sustains long-term demand for probiotic products.

MARKET RESTRAINTS

Limited Cold Chain Infrastructure Impedes Product Efficacy and Availability

The inadequacy of cold chain infrastructure is a significant restraint on the Middle East and Africa Probiotics Market. This is particularly true for live culture products that require strict temperature control. Probiotic strains are sensitive to heat and humidity, and exposure to temperatures above 25 degrees Celsius can drastically reduce their viability and efficacy. As noted by the Global Cold Chain Alliance (GCCA), a severe deficit in cold chain infrastructure across much of Africa leads to massive post-harvest losses. In many areas, less than 10% of fresh produce enters a proper temperature-controlled system, causing up to 40% of perishable food to spoil before reaching consumers. Also, in many rural and semi-urban areas across the region, consistent electricity supply remains a challenge, affecting the storage capabilities of retailers and distributors. This logistical bottleneck limits the geographical reach of premium probiotic products, confining their availability mainly to major urban centers with advanced retail infrastructure. The high cost of maintaining cold chain logistics further elevates the final retail price, making probiotics less accessible to price-sensitive consumers. In countries like Egypt and Morocco, where ambient temperatures frequently exceed 40 degrees Celsius during summer months, the risk of product degradation during last-mile delivery is acute. Manufacturers face considerable difficulties in ensuring that products retain their promised colony-forming units until consumption. This uncertainty undermines consumer trust and brand loyalty, as users may not experience the expected health benefits from compromised products. Thus, the market growth is restrained by the inability to guarantee product integrity across the entire supply chain, limiting the expansion potential for international and local brands alike.

High Cost of Premium Probiotic Products Limits Mass Market Penetration

The elevated cost of premium probiotic products is a formidable barrier to the mass penetration of the Middle East and Africa probiotics market. This obstacle is driven by the prevalent income disparity and price sensitivity across the region. High-quality probiotic supplements and functional foods often command a price premium due to the costs associated with strain development, clinical validation, and specialized packaging. According to the World Bank, the poverty headcount ratio in Sub-Saharan Africa stands at approximately 35 percent, indicating that a significant portion of the population has limited disposable income for non-essential health products. In many households, basic nutritional needs take precedence over preventive health supplements, restricting the addressable market for probiotics to the upper and middle income segments. The import dependence for many specialized probiotic strains further exacerbates pricing issues, as currency fluctuations and tariffs increase the final cost to consumers. In countries like Lebanon and Turkey, economic instability and inflation have eroded purchasing power, making imported health supplements prohibitively expensive for the average consumer. Local manufacturing capabilities are still developing, and economies of scale have not yet been fully realized to drive down prices. As per the African Development Bank, the cost of healthcare out-of-pocket expenditures remains high in many African nations, discouraging spontaneous purchases of wellness products. This financial constraint forces manufacturers to compete on price, often compromising on quality or marketing spend, which hinders the overall market maturity and slows the adoption rate among the broader population.

MARKET OPPORTUNITIES

Expansion into Traditional Fermented Food Segments Offers Significant Growth Potential

The integration of probiotics into traditional fermented food segments offers a lucrative opportunity for players in the Middle East and Africa probiotics market. The region has a rich heritage of consuming fermented dairy and grain products such as laban, kefir, amasi, and injera, which naturally contain beneficial microbes. Leveraging this cultural acceptance allows manufacturers to introduce fortified versions of these staples with standardized probiotic strains, offering enhanced health benefits without altering consumer habits. Local companies are increasingly collaborating with research institutions to identify indigenous probiotic strains that are well adapted to local conditions and consumer preferences. This approach not only reduces reliance on imported cultures but also appeals to nationalistic sentiments and preferences for locally sourced ingredients. In South Africa, the commercialization of amasi with added probiotic strains has gained traction among health-conscious consumers seeking familiar tastes with added functionality. The regulatory environment in several countries is becoming more supportive of functional food claims, facilitating the launch of such innovative products. Brands can create unique value propositions that resonate deeply with local consumers by aligning modern scientific validation with traditional dietary practices. This approach drives volume growth and market share expansion in both urban and rural settings.

Growing Urbanization and Retail Modernization Facilitate Product Accessibility

The rapid pace of urbanization and the modernization of retail channels in the region create favourable conditions for the proliferation of probiotic products, which sets the stage for the expansion of the Middle East and Africa probiotics market. As populations migrate to cities, lifestyles become more fast-paced, leading to increased demand for convenient and healthy food options. Demographic data from United Nations agencies and the OECD projects that Africa's urban population will surge to approximately 1.4 billion people by 2050. This rapid urban growth will dramatically increase consumer reliance on convenience items and expand the market for packaged functional foods. The expansion of supermarket chains and e-commerce platforms in countries like Nigeria, Kenya, and Saudi Arabia enhances the visibility and accessibility of probiotic products. Modern retail outlets offer the necessary cold storage facilities and promotional spaces that are crucial for launching and sustaining new product lines. In the United Arab Emirates, the penetration of online grocery shopping has surged, with platforms like Noon and Amazon AE offering a wide range of health supplements, including probiotics, to tech-savvy consumers. This digital shift enables brands to reach niche audiences and provide detailed product information, fostering informed purchase decisions. Furthermore, the rise of health and wellness specialty stores in major metropolitan areas provides dedicated shelf space for premium probiotic brands. As per the International Trade Centre, the growth of organized retail in emerging markets is correlated with increased consumption of value-added food products. This structural transformation in the retail landscape lowers entry barriers for new players and supports the scaling of distribution networks, thereby accelerating market growth.

MARKET CHALLENGES

Regulatory Heterogeneity Complicates Market Entry and Compliance

The lack of harmonized regulatory frameworks remains a serious challenge for manufacturers seeking to operate in multiple jurisdictions, which negatively impacts the growth of the Middle East and Africa probiotics market. Each country has distinct guidelines regarding the approval of health claims, labeling requirements, and the classification of probiotics as either food supplements or pharmaceuticals. According to the World Health Organization, regulatory capacity varies widely across the African region, with some nations lacking specific guidelines for functional foods, leading to ambiguity and inconsistent enforcement. In the Gulf Cooperation Council, while there are efforts toward standardization through the Gulf Standardization Organization, individual member states may still impose additional requirements or interpret regulations differently. This fragmentation increases the complexity and cost of compliance, as companies must navigate disparate legal landscapes and adapt their product formulations and marketing materials for each market. In countries like Egypt and South Africa, the registration process for new health products can be lengthy and bureaucratic, delaying time to market. The absence of clear definitions for probiotic strains and potency standards also creates confusion among consumers and healthcare providers regarding product efficacy. As per the African Union, efforts to harmonize food safety regulations are ongoing, but progress is slow due to differing national priorities and resource constraints. This regulatory uncertainty discourages investment and innovation, as companies hesitate to launch new products without guaranteed market access or protection of intellectual property rights, thereby stifling market dynamism.

Consumer Skepticism and Lack of Scientific Literacy Hinder Adoption

Persistent consumer skepticism and limited scientific literacy regarding the specific benefits of probiotics hinder widespread adoption in parts of the region, which impedes the overall expansion of the Middle East and Africa probiotics market. Despite growing health awareness, many consumers remain unfamiliar with the concept of the gut microbiome and the mechanism of action of probiotic strains. According to UNESCO, literacy rates in some Sub-Saharan African countries remain below 60 percent, which limits the ability of consumers to critically evaluate health claims and distinguish between evidence-based products and marketing hype. This knowledge gap makes consumers vulnerable to misinformation and exaggerated claims, leading to distrust in the category when expected results are not immediately visible. In rural areas, traditional beliefs and remedies often take precedence over modern nutritional science, creating cultural barriers to the acceptance of probiotic supplements. The prevalence of counterfeit or substandard health products in informal markets further erodes consumer confidence, as users may experience no benefits or adverse effects from low-quality imitations. As per the World Health Organization, the circulation of falsified medical products is a significant public health threat in Africa, undermining the credibility of legitimate health interventions. Manufacturers face the challenge of educating consumers through costly and sustained marketing campaigns, which may not yield immediate returns. The perceived value of probiotics remains low without robust consumer education and transparent communication from healthcare professionals. Hence, this restricts market growth to educated urban elites, limiting the potential for mass market penetration.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 7.04% |

| Segments Covered | By Ingredient, Application, End User, And Region |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Yakult Honsha Co. Ltd, Nestle S.A, Groupe Danone, PepsiCo Inc, Lifeway Foods Inc, Actimel, Activia, Bright Dairy, BioGaia, And CHR Hansen |

SEGMENTAL ANALYSIS

By Ingredient Insights

In 2025, the bacteria segment held the majority share of the Middle East and Africa Probiotics Market because of its extensive validation in clinical studies and widespread incorporation into dairy-based functional foods. Lactobacillus and Bifidobacterium species are the most extensively researched strains, with decades of scientific evidence supporting their efficacy in managing gastrointestinal health and boosting immunity. Clinical studies have shown Lactobacillus rhamnosus GG can reduce the risk of antibiotic-associated diarrhea, though WHO guidelines primarily emphasize Zinc and ORS for general acute diarrhea treatment. In the Middle East, where dairy consumption is culturally ingrained, manufacturers prefer bacterial strains for their compatibility with fermentation processes used in products like yogurt and laban. According to the FAO, Asia is the fastest-growing region for milk production, driven largely by India and China, while global production has grown by approximately 1.3–1.6% annually. Furthermore, consumer familiarity with bacterial cultures in traditional fermented foods reduces the educational barrier for market entry. Healthcare providers in countries like Saudi Arabia and Egypt frequently recommend bacterial probiotics for digestive ailments, reinforcing their dominance. The stability of certain bacterial spores during processing also makes them preferable for manufacturers seeking longer shelf lives in hot climates. Clinical data indicate that specific Lactobacillus strains can reduce the duration of infectious diarrhea by approximately 1 day (24–25 hours) and may reduce the risk of developing antibiotic-associated diarrhea by roughly 40–50%. This strong clinical backing, combined with cultural acceptance, ensures that bacteria remain the primary ingredient choice for both consumers and producers in the region.

On the other hand, the yeast segment is expected to exhibit a noteworthy CAGR of 8.5% during the forecast period due to increasing demand for non-dairy probiotic options and superior thermal stability. Saccharomyces boulardii, a prominent probiotic yeast, is gaining traction due to its resistance to antibiotics and ability to survive harsh gastric conditions without refrigeration. The CDC identifies antibiotic resistance as a global threat, including resistant yeast species like Candida auris. While Saccharomyces boulardii is a probiotic yeast that resists antibiotics, the CDC does not officially recommend its prescription as a strategy for antimicrobial resistance in Africa. This unique attribute makes yeast an ideal supplement for patients undergoing long-term antibiotic therapy for tuberculosis and other infectious diseases prevalent in the region. The rising vegan population in urban centers like Cape Town and Tel Aviv also fuels demand for non-dairy probiotic sources, where yeast serves as a key alternative to bacterial cultures derived from milk. Research indicates that the retail sales of plant-based protein in the UAE doubled between 2019 and 2023, reflecting a rapidly expanding market for functional ingredients. Additionally, yeast probiotics are increasingly used in animal feed applications to improve livestock gut health, further accelerating segment growth. The ease of storage and transport without cold chain requirements makes yeast particularly attractive for distribution in rural areas with limited infrastructure. Manufacturers are investing in research to develop novel yeast strains tailored for specific health benefits, enhancing product differentiation and market appeal.

By Application Insights

The dairy products segment dominated the Middle East and Africa Probiotics Market and accounted for a substantial share in 2025. Factors such as the deep-rooted cultural tradition of consuming fermented milk products such as yogurt, kefir, and laban drive the dominance of this segment. These products serve as natural carriers for probiotic bacteria, offering a familiar taste profile that encourages regular consumption across all age groups. A study indicates that the Middle East yogurt market is expanding steadily due to urbanization, with traditional products like Labneh holding a central place in Levant diets and Saudi Arabia leading overall regional dairy market share. This high baseline consumption provides an established distribution channel for probiotic fortified variants, allowing manufacturers to leverage existing supply chains and consumer loyalty. The perception of dairy as a wholesome and nutritious food item further enhances the acceptance of probiotic-enriched versions. In North Africa, traditional drinks like rayeb and lben are being commercialized with added probiotic strains, bridging the gap between traditional diets and modern health trends. According to the FAO and World Bank reports, the dairy value chains in Egypt and Morocco offer significant development opportunities, with a growing focus on upgrading informal markets and expanding commercial processing infrastructure. Government initiatives promoting calcium intake and bone health also support the dairy segment, as probiotics are often marketed alongside these benefits. The availability of affordable local milk supplies reduces production costs, making probiotic dairy products accessible to a broader demographic. Retailers prioritize shelf space for dairy items due to their high turnover rates, ensuring consistent visibility for probiotic brands.

However, the dietary supplements segment is predicted to witness the highest CAGR of 9.2% from 2026 to 2034, owing to rising health consciousness and the demand for targeted therapeutic solutions beyond general nutrition. Consumers are increasingly seeking convenient and potent forms of probiotics that offer specific health benefits such as immune support, weight management, and mental well-being. According to the World Health Organization, noncommunicable diseases are a leading cause of mortality in the Eastern Mediterranean Region, prompting regional frameworks that focus on reducing risk factors like unhealthy diets and physical inactivity. The proliferation of pharmacies and online health stores in urban areas facilitates easy access to a wide variety of probiotic capsules, powders, and tablets. In South Africa, the wellness industry has seen a surge in demand for personalized nutrition, with probiotic supplements tailored to individual gut microbiome profiles gaining popularity. The ability of supplements to deliver higher colony-forming units compared to food products appeals to consumers seeking maximum efficacy. Furthermore, the expansion of telemedicine platforms allows healthcare providers to recommend specific supplement regimes remotely, boosting adoption. Manufacturers are introducing multi-strain formulations backed by clinical trials, enhancing consumer trust and willingness to pay premium prices. This trend is particularly pronounced among the educated middle class who prioritize evidence-based health interventions.

By End User Insights

The human end-user segment led the Middle East and Africa Probiotics Market and occupied a significant share in 2025. This supremacy of the segment was supported by the increasing prevalence of lifestyle-related diseases and heightened awareness of preventive healthcare. The rising incidence of obesity, diabetes, and digestive disorders in the region has prompted individuals to seek natural remedies for health management. According to the International Diabetes Federation, the Middle East and North Africa region has the highest adult diabetes prevalence globally, affecting approximately 16.2% of the population, which highlights a massive regional need for metabolic health solutions. Urbanization and sedentary lifestyles have further exacerbated these health issues, creating a large addressable market for gut health solutions. Consumer education campaigns by health authorities and private organizations have successfully highlighted the link between gut health and overall wellness, encouraging regular probiotic consumption. In countries like the United Arab Emirates and Qatar, government-led health initiatives promote healthy eating habits, indirectly boosting the uptake of functional foods and supplements. Data from the World Health Organization indicates that health expenditure per capita in high-income Gulf Cooperation Council nations is among the highest globally, reflecting strong consumer purchasing power for healthcare and wellness goods. The growing middle class with disposable income prioritizes health and wellness, sustaining demand for diverse probiotic offerings. Retail expansion and digital marketing efforts target health-conscious demographics effectively, ensuring continuous market growth. The cultural emphasis on family health also leads to bulk purchases for household use, reinforcing the dominance of the human segment.

On the contrary, the animal end-user segment is estimated to register the fastest CAGR of 7.8% between 2026 and 2034. This swift expansion of the segment is propelled by the intensification of livestock farming and the ban on antibiotic growth promoters. Farmers are increasingly adopting probiotic feed additives to enhance animal productivity, improve feed efficiency, and maintain gut health without relying on antibiotics. The FAO projects that the Near East and North Africa region will rely heavily on imports to meet its growing demand for meat by 2030, highlighting the need to scale up efficient, sustainable local livestock systems. Probiotics help reduce mortality rates in poultry and cattle, which is critical for meeting the rising demand for animal protein. Poultry represents the largest component of South Africa's animal agricultural sector, where producers are increasingly looking at non-antibiotic alternatives, including probiotics, to improve gut health and prevent common flock diseases like necrotic enteritis. The World Organisation for Animal Health actively pushes for a global ban on using antimicrobials as animal growth promoters, encouraging nations across Africa and other regions to transition toward safe alternatives like biosecurity and vaccines. Large-scale farming operations in Egypt and Saudi Arabia are investing in advanced animal nutrition strategies to optimize yield and quality. The cost-effectiveness of probiotics in reducing veterinary expenses and improving weight gain ratios appeals to commercial farmers. Additionally, the growing pet ownership trend in urban areas is contributing to the demand for probiotic supplements for dogs and cats, further accelerating segment growth. Manufacturers are developing specialized strains for different animal species, enhancing product efficacy and market penetration.

REGIONAL ANALYSIS

Saudi Arabia Probiotics Market Analysis

Saudi Arabia was the top performer in the regional market and occupied a 41.7% share in 2025. This prominence of the country’s market was driven by its large population, high healthcare spending, and strong government support for health initiatives. The Kingdom’s Vision 2030 framework emphasizes preventive healthcare and lifestyle improvement, which directly boosts the demand for functional foods and probiotics. According to the latest data from the General Authority for Statistics (GASTAT), Saudi Arabia's population reached 35.3 million in mid-2024, though the prevalence of lifestyle-related conditions remains a significant concern, with diabetes affecting a substantial portion of the adult population. The Ministry of Health has launched various campaigns to promote healthy eating, encouraging the consumption of probiotic-rich dairy products. Also, the local dairy industry, led by companies like Almarai, is heavily investing in probiotic innovation, introducing new yogurt and drink variants fortified with beneficial bacteria. As per the Saudi Food and Drug Authority, regulations regarding health claims on food products are becoming more structured, providing clarity for manufacturers and building consumer trust. The high disposable income of citizens allows for the purchase of premium imported probiotic supplements, diversifying the market landscape. Retail expansion in major cities like Riyadh and Jeddah ensures the wide availability of probiotic products. The growing awareness of gut health among the younger demographic drives demand for innovative formats such as gummies and shots. Strategic partnerships between local distributors and international brands facilitate the introduction of advanced probiotic strains. The country’s robust logistics infrastructure supports efficient distribution, minimizing product spoilage and ensuring quality.

United Arab Emirates Probiotics Market Analysis

The United Arab Emirates was positioned second in the regional market and captured a 22.4% share in 2025. This expansion was fuelled by a highly diverse population and advanced retail infrastructure. The country’s status as a global tourism and business destination exposes consumers to international health trends, accelerating the adoption of probiotic products. According to the Dubai Department of Economy and Tourism, the UAE hosts millions of expatriates from around the world, creating a multicultural market with varied dietary preferences and health needs. The government’s focus on wellness tourism and medical tourism further stimulates demand for high-quality health supplements. Local retailers such as Carrefour and Lulu Hypermarket offer extensive ranges of probiotic foods and beverages, catering to different income segments. The rise of e-commerce platforms like Amazon AE and Noon enables convenient access to niche probiotic brands, driving online sales growth. Health-conscious residents in Dubai and Abu Dhabi are increasingly seeking personalized nutrition solutions, leading to the popularity of customized probiotic supplements. The hospitality sector also contributes to market growth by incorporating probiotic options in menus and wellness packages. Investment in local manufacturing facilities by international companies reduces dependency on imports and lowers costs. The competitive landscape encourages innovation in product formulation and packaging, keeping the market dynamic and responsive to consumer preferences.

South Africa Probiotics Market Analysis

South Africa plays a key role in the Middle East and Africa market due to a developed retail sector and increasing health awareness among the middle class. The country’s diverse demographic profile includes a significant urban population with access to modern healthcare and nutritional information. According to Statistics South Africa, over 60% of the country's population resides in urban areas, providing a centralized demographic that is serviced by established retail and supermarket chains. Local manufacturers such as Clover and Danone dominate the dairy-based probiotic segment, offering affordable options that appeal to a broad consumer base. The prevalence of HIV and AIDS in the region has heightened interest in immune-boosting supplements, including probiotics, as adjunctive therapies. As per the South African Medical Research Council, research into the benefits of probiotics for immune health is ongoing, supporting medical recommendations for their use. The growth of the private healthcare sector enables wider access to diagnostic services and personalized nutrition advice, driving demand for specialized probiotic supplements. Retailers are expanding their health and wellness sections, dedicating more shelf space to functional foods. The government’s National Development Plan emphasizes health promotion, aligning with the industry’s growth trajectory. Challenges such as income inequality limit mass market penetration, but targeted marketing towards the upper and middle income segments sustains steady growth. Innovation in local sourcing of probiotic strains offers opportunities for differentiation and cost reduction.

Egypt Probiotics Market Analysis

Egypt is likely to grow significantly in the Middle East and Africa probiotics market over the forecast period, owing to its large population and traditional consumption of fermented dairy products. The country’s rich history of producing baladi cheese and zabadi provides a cultural foundation for the acceptance of probiotic-enhanced variants. According to the Central Agency for Public Mobilization and Statistics, Egypt’s population exceeds 100 million, creating a vast potential consumer base for affordable health products. The government’s efforts to improve public health and reduce the burden of infectious diseases encourage the adoption of preventive nutritional strategies. Local dairy companies like Juhayna and Domty are leading the market by introducing probiotic yogurts and drinks at competitive prices. As per the Egyptian Ministry of Health, initiatives to combat malnutrition and digestive disorders include promoting the consumption of fortified foods. The economic challenges faced by the country require manufacturers to balance quality with affordability, driving innovation in cost-effective production methods. The expansion of modern retail outlets in Cairo and Alexandria improves product accessibility for urban consumers. Rising health awareness among the educated middle class drives demand for imported premium probiotic supplements. The pharmaceutical sector also plays a role, with doctors recommending probiotics for gastrointestinal issues. Regulatory improvements by the Egyptian Drug Authority enhance market transparency and consumer protection. Despite infrastructure challenges, the sheer size of the market ensures sustained demand and growth potential for both local and international players.

COMPETITION OVERVIEW

The competitive landscape of the Middle East and Africa Probiotics Market is characterized by a mix of multinational corporations and agile local manufacturers striving for dominance. Global giants leverage their extensive research capabilities and brand equity to introduce innovative products, while local players capitalize on deep cultural insights and established distribution channels. Competition intensifies as companies differentiate through strain-specific clinical validation and targeted health claims. The market sees frequent launches of novel formats, including gummy shots and fortified traditional foods, to appeal to diverse consumer preferences. Strategic alliances between pharmaceutical firms and food producers are becoming common to bridge the gap between nutrition and medicine. Price competition remains fierce, particularly in price-sensitive segments, prompting manufacturers to optimize supply chains and explore local sourcing options. Regulatory heterogeneity across countries adds complexity, requiring companies to maintain flexible compliance strategies. Digital marketing and influencer partnerships are increasingly utilized to reach tech-savvy urban populations. The entry of new startups focusing on niche segments such as vegan or antibiotic-free probiotics further fragments the market. Overall, the competitive environment drives continuous innovation and improvement in product quality, benefiting consumers through wider choices and enhanced health outcomes.

KEY MARKET PLAYERS

A few major players of the Middle East and Africa Probiotics Market include

- Yakult Honsha Co. Ltd

- Nestle S.A

- GroupeDanone

- PepsiCo Inc

- Lifeway Foods Inc

- Actimel

- Activia

- Bright Dairy

- BioGaia

- CHR Hansen

Top Strategies Used by Key Market Participants in the Middle East and Africa Probiotics Market

Key players in the Middle East and Africa Probiotics Market primarily employ product localization and strategic partnerships to strengthen their positions. Companies increasingly adapt formulations to align with traditional dietary habits, such as incorporating probiotics into laban and amasi. This cultural resonance enhances consumer acceptance and drives adoption rates across diverse demographics. Manufacturers also focus on expanding distribution networks through collaborations with local retailers and e-commerce platforms to overcome infrastructure challenges. Investing in cold chain logistics ensures product integrity and builds consumer trust in efficacy. Educational campaigns play a vital role in raising awareness about gut health benefits, targeting both healthcare professionals and end users. Firms prioritize research and development to discover indigenous probiotic strains that offer unique health advantages and reduce dependency on imports. Regulatory compliance remains a central strategy with companies actively engaging with authorities to navigate complex approval processes. Pricing strategies are tailored to address income disparities, ensuring accessibility for middle-income segments while maintaining premium options for affluent consumers. These multifaceted approaches enable market participants to capture growth opportunities and establish long-term competitiveness in the evolving regional landscape.

Leading Players in the Latin America Probiotics Market

- Danone maintains a robust presence in Latin America through its extensive portfolio of dairy and plant-based probiotic products. The company leverages its strong brand recognition with Actimel and Activia to drive consumer engagement across key markets such as Brazil and Mexico. Recent initiatives focus on sustainability and local sourcing to enhance supply chain resilience. Danone has invested in expanding its production facilities in the region to meet rising demand for functional foods. The company actively collaborates with local farmers to ensure high-quality raw materials while supporting community development. Digital marketing campaigns target health-conscious consumers, emphasizing immune health benefits. Danone continues to innovate by launching new flavors and formats tailored to regional preferences. Their strategic partnerships with retailers ensure wide distribution and visibility. The company also prioritizes educational programs to increase awareness about gut health. These efforts solidify Danone’s position as a leading innovator and trusted provider of probiotic solutions in the diverse Latin American landscape.

- Nestlé strengthens its footprint in Latin America by integrating probiotics into a wide range of nutritional products, including infant formula and adult nutrition. The company utilizes its global research capabilities to develop strains specifically suited for regional health needs. Nestlé has recently expanded its manufacturing capacity in countries like Argentina and Chile to improve market responsiveness. The firm focuses on affordable pricing strategies to reach broader demographics in emerging economies. Collaborations with healthcare professionals help promote the clinical benefits of their probiotic offerings. Nestlé invests heavily in digital platforms to engage directly with consumers and provide personalized nutrition advice. Their commitment to sustainability is evident in eco-friendly packaging initiatives across the region. The company also supports local agricultural communities to secure sustainable ingredient supplies. By combining scientific expertise with local market insights, Nestlé effectively addresses the growing demand for preventive health solutions. This approach enhances brand loyalty and drives consistent growth in the competitive Latin American probiotics sector.

- Lallemand specializes in the production of high-quality probiotic strains and ingredients serving both human and animal nutrition sectors in Latin America. The company partners with local manufacturers to incorporate its specialized bacterial and yeast cultures into various functional foods and supplements. Lallemand has recently inaugurated new research and development centers in Brazil to accelerate innovation tailored to regional microbiomes. The firm emphasizes technical support and education for its clients, ensuring optimal application of probiotic technologies. Strategic alliances with academic institutions facilitate advanced research on gut health and disease prevention. Lallemand’s focus on sustainability includes responsible sourcing and efficient production processes. The company actively participates in industry conferences to share scientific findings and build credibility. Its diverse product portfolio caters to the growing demand for natural and effective health solutions. By providing reliable and scientifically validated ingredients, Lallemand empowers local brands to create competitive probiotic products. This B2B approach establishes Lallemand as a critical enabler of market growth and innovation throughout the Latin American region.

MARKET SEGMENTATION

This research report on the Middle East and Africa probiotics market has been segmented and sub-segmented based on ingredient, application, end user, form, and region.

By Ingredient

- Bacteria

- Yeast

By Application

- Food and Beverages

- Dairy Products

- Non-dairy Beverages

- Infant Formula

- Cereals

- Dietary Supplements

- Animal Feed

By End-User

- Human

- Animal

By Form

- Dry

- Liquid

By Region

- KSA

- UAE

- Israel

- Rest Of GCC Countries

- South Africa

- Ethiopia

- Kenya

- Egypt

- Sudan

- Rest Of MEA

Frequently Asked Questions

1. What factors are driving growth in the MEA probiotics market?

Growth is driven by increasing consumer awareness of digestive and immune health, rising prevalence of lifestyle-related disorders, expanding health and wellness segments, growth in dietary supplement consumption, and increasing incorporation of probiotics in functional foods and beverages.

2. What types of probiotic products are available in the MEA market?

Product types include probiotic dietary supplements (capsules, tablets, powders), probiotic functional foods such as yogurt and fermented dairy products, probiotic beverages (fermented drinks, shots), and infant nutrition products fortified with probiotics.

3. How are probiotics consumed by consumers in the MEA region?

Consumers commonly consume probiotics through dietary supplements, fermented dairy foods, probiotic drinks, and fortified nutrition products. Capsules and sachets are popular for convenience, while functional beverages and yogurts appeal to lifestyle consumers.

4. What role does consumer awareness play in the probiotics market?

Increased awareness of gut health and immune support drives demand. Educational campaigns, media influence, and healthcare professional recommendations contribute to broader acceptance of probiotic products.

5. What challenges does the MEA probiotics market face?

Challenges include limited consumer awareness in some regions, price sensitivity, regulatory variability across different countries, skepticism about product efficacy, and the need to ensure product stability and shelf life under high ambient temperatures.

6. How important are regulations in the MEA probiotics market?

Regulatory compliance is essential, as probiotic products must meet food safety, labeling, and health claim guidelines set by individual countries. Harmonization of regulations remains a challenge in the region.

7. What are the major applications of probiotics in the MEA market?

Major applications include digestive health support, immune function enhancement, women’s health, and inclusion in infant and children’s nutrition products. Functional foods with probiotics further expand consumer usage occasions.

8. How is product innovation shaping the MEA probiotics market?

Product innovation includes new delivery formats (beverages, gummies, chewables), multi-strain formulations, synbiotic products combining probiotics and prebiotics, and heat-stable probiotic strains suited for regional climates.

9. What trends are emerging in the MEA probiotics market?

Emerging trends include personalized probiotic solutions, plant-based probiotic foods, fortified sports nutrition products with probiotics, and growing interest in women’s and infant health formulations.

10. What is the future outlook for the MEA probiotics market?

The future outlook is positive, with continued market expansion driven by health-focused consumer behavior, innovation in product formats, expanded retail reach, and rising demand for functional nutrition products. As awareness grows and regulations evolve, adoption of probiotic products is expected to increase across demographic segments.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1600

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com