North America Architectural Flat Glass Market Size, Share, Trends & Growth Forecast Report By Product (Basic, Tempered, Laminated, Insulated, Others), Application (Residential, Non-residential, Industrial), and Country (United States, Canada, Mexico, Rest of North America) – Industry Analysis From 2026 to 2034

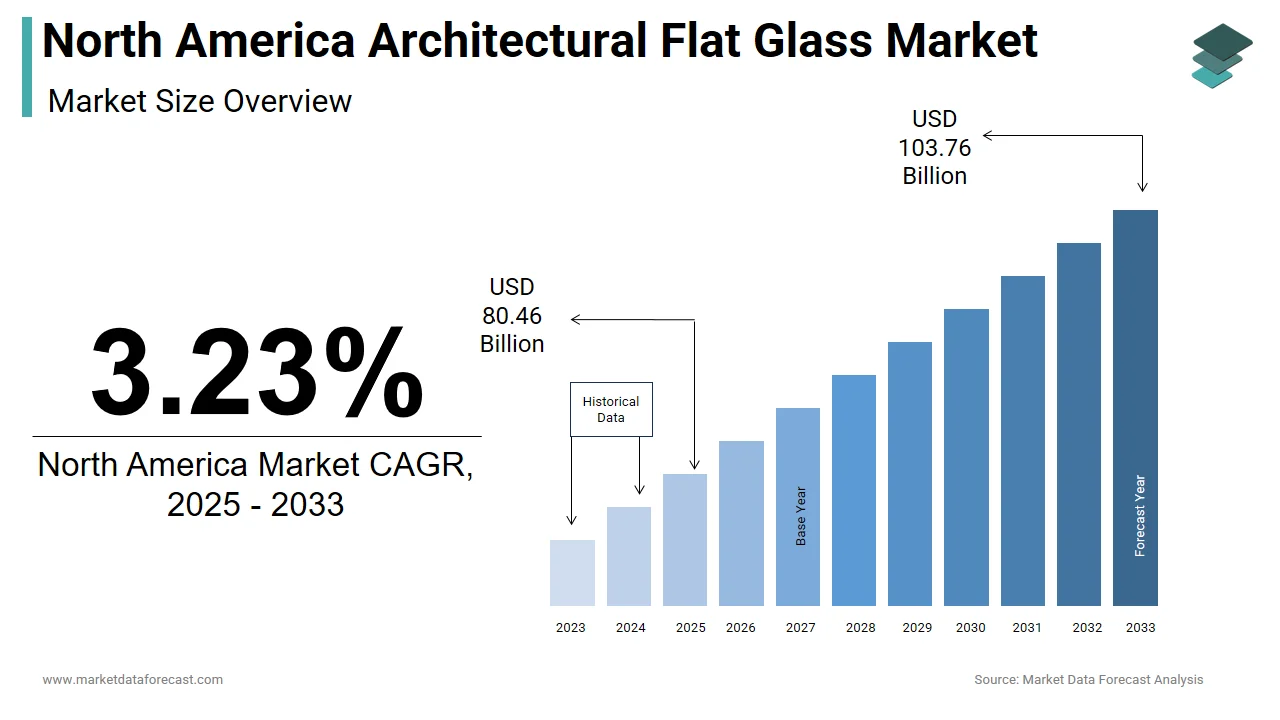

Market Size, 2025

$80.46 BnMarket Estimate, 2026

$83.06 BnMarket Forecast, 2034

$107.11 BnCAGR, 2026–2034

3.23%North America Architectural Flat Glass Market Size

The size of the North America architectural flat glass market was worth USD 80.46 billion in 2025. The North America market is anticipated to grow at a CAGR of 3.23% from 2026 to 2034 and be worth USD 107.11 billion by 2034 from USD 83.06 billion in 2026.

The North America architectural flat glass market involves a wide range of glass products used in building construction, including tempered, laminated, and insulated glass units designed for windows, facades, curtain walls, and interior partitions. These products are essential components in both residential and commercial structures, contributing to aesthetics, energy efficiency, safety, and environmental sustainability.

A key factor shaping the market is the ongoing shift toward green building practices and high-performance materials that enhance thermal insulation and reduce energy consumption.

Additionally, urbanization trends and infrastructure modernization efforts have contributed to sustained demand for flat glass in new construction and renovation projects.

Another influential trend is the rising preference for aesthetically pleasing and structurally transparent designs in commercial developments such as office towers, airports, and retail complexes.

MARKET DRIVERS

Rise in Green Building Initiatives and Energy Efficiency Standards

Among the primary drivers behind the growth of the North America architectural flat glass market is the increasing adoption of green building initiatives and stringent energy efficiency regulations. Governments at both federal and state levels have implemented policies aimed at reducing carbon emissions and promoting sustainable construction practices.

To address this, programs like ENERGY STAR and Leadership in Energy and Environmental Design (LEED) certification encourage the use of high-performance glazing solutions such as low-emissivity (Low-E) coatings and insulated glass units (IGUs). These technologies help regulate indoor temperatures, reduce HVAC loads, and minimize reliance on artificial lighting.

Moreover, cities such as New York and San Francisco have introduced local mandates requiring the use of energy-efficient materials in new constructions and major renovations. This regulatory push has spurred demand for advanced architectural flat glass products that offer superior thermal performance without compromising visual clarity or structural integrity, reinforcing their role in the evolving built environment.

Expansion of Commercial and Institutional Construction Activities

Another significant driver fueling the North America architectural flat glass market is the robust expansion of commercial and institutional construction activities, particularly in sectors such as healthcare, education, and corporate real estate.

Architectural flat glass plays a critical role in these developments due to its ability to create open, light-filled spaces that enhance occupant well-being and productivity. Hospitals, universities, and government buildings increasingly incorporate large glazed façades and curtain wall systems to improve aesthetics, natural lighting, and environmental connectivity.

Additionally, the rise of mixed-use developments integrating retail, office, and residential spaces has further increased demand for expansive glass façades that blur the boundaries between indoor and outdoor environments.

MARKET RESTRAINTS

Limited Raw Material Availability and Supply Chain Disruptions

One of the primary restraints affecting the Middle East and Africa Galacto-Oligosaccharide (GOS) market is the limited availability of raw materials and persistent supply chain disruptions. GOS is primarily derived from lactose, which is sourced from dairy products. However, several countries in the Middle East and Africa face challenges in securing consistent supplies of high-quality lactose due to inadequate dairy farming infrastructure and fluctuating milk production.

According to the Food and Agriculture Organization (FAO), milk production in Sub-Saharan Africa grew at a slower annual rate between 2015 and 2022, significantly lower than the global average. This slow growth hampers the availability of lactose required for GOS synthesis.

Moreover, geopolitical instability in regions like North Africa and the Arabian Peninsula has disrupted trade routes, leading to delays in the import of raw materials and finished products. For example, the Suez Canal blockage in 2021 caused widespread logistics delays across global markets, including food ingredients.

These supply-side constraints not only increase production costs but also limit the ability of local manufacturers to scale up output. Consequently, the lack of a stable and sufficient supply of raw materials remains a key obstacle to the expansion of the GOS market in the region.

High Production Costs and Technological Barriers

Another significant restraint impacting the Middle East and Africa Galacto-Oligosaccharide (GOS) market is the high cost of production combined with technological limitations in processing facilities. GOS production involves enzymatic synthesis using β-galactosidase enzymes, a process that requires specialized biotechnological equipment and skilled labor. Many countries in the region lack access to advanced fermentation and purification technologies, resulting in inefficient production cycles and higher operational expenses.

According to the African Development Bank, limited share of food processing companies in sub-Saharan Africa utilize modern bioprocessing techniques, limiting their ability to produce high-purity GOS at competitive prices.

Moreover, the cost of importing enzymes and catalysts from Europe or Asia adds to the financial burden

Additionally, energy costs in many parts of the Middle East and Africa remain volatile, further escalating production expenses. For instance, Egypt faced a notable increase in industrial electricity tariffs in 2023, according to the Egyptian Ministry of Electricity. These economic and technical barriers hinder the development of a self-sustaining GOS industry in the region, compelling manufacturers to rely on imported finished products rather than local production, thereby restraining market growth.

MARKET OPPORTUNITIES

Rising Demand for Functional Foods and Probiotic Supplements

The increasing consumer preference for functional foods and probiotic supplements presents a major opportunity for the expansion of the Middle East and Africa Galacto-Oligosaccharide (GOS) market. GOS is widely recognized for its prebiotic properties, promoting the growth of beneficial gut bacteria and enhancing digestive health. As awareness about gut health and immunity grows across urban populations, there has been a noticeable shift toward fortified food and beverage products.

Additionally, the prevalence of lifestyle diseases such as diabetes and obesity has prompted consumers to seek healthier dietary alternatives, boosting the incorporation of GOS in low-calorie yogurts, infant formulas, and nutritional supplements.

The African Union's 2063 Agenda emphasizes improved nutrition and health outcomes, encouraging governments to support the development of health-focused food industries.

Furthermore, multinational food companies are entering the regional market with fortified product lines. These developments indicate a favorable environment for GOS producers to capitalize on the rising demand for health-enhancing food ingredients in the region.

Government Initiatives Supporting Nutritional Security

Government-backed initiatives aimed at improving nutritional security are creating new avenues for the Galacto-Oligosaccharide (GOS) market in the Middle East and Africa. Several national health programs have prioritized the fortification of staple foods to combat malnutrition, particularly among children and pregnant women. GOS, with its ability to enhance calcium absorption and promote intestinal health, aligns well with these public health goals.

According to the World Bank, over 30% of children under five in Sub-Saharan Africa suffer from stunting, prompting increased investment in nutrient-rich food interventions. The African Development Bank has allocated USD 1.2 billion under its Feed Africa Strategy to support food fortification projects, including those involving prebiotics.

Additionally, the Gulf Cooperation Council (GCC) Standardization Organization has updated food labeling regulations to encourage the use of functional ingredients, providing a regulatory boost for GOS adoption. These policy-driven developments offer a promising outlook for the expansion of the GOS market across the region.

MARKET CHALLENGES

Regulatory Fragmentation Across Countries

A significant challenge facing the Middle East and Africa Galacto-Oligosaccharide (GOS) market is the fragmented regulatory landscape governing food additives and functional ingredients. Each country in the region maintains its own set of food safety standards, approval processes, and labeling requirements, making market entry complex and time-consuming for manufacturers.

For instance, while the Gulf Cooperation Council (GCC) has harmonized food regulations for member states such as Saudi Arabia, UAE, and Kuwait, countries like Egypt and Morocco follow different compliance frameworks. This inconsistency creates uncertainty for suppliers seeking to distribute GOS-based products across multiple jurisdictions.

Additionally, the absence of clear guidelines on prebiotic claims in food labeling complicates marketing efforts. As per a study published by the African Journal of Food Science, over 60% of food manufacturers in East Africa cited regulatory hurdles as a major barrier to introducing functional ingredients.

Moreover, the lengthy approval timelines for novel food additives often discourage smaller players from entering the market. The Southern African Development Community (SADC) has made progress toward regional harmonization, but full implementation remains pending. Until a more unified regulatory framework is established, regulatory fragmentation will continue to pose a considerable challenge to the growth of the GOS market in the region.

Consumer Awareness and Education Gaps

Limited consumer awareness regarding the health benefits of Galacto-Oligosaccharides (GOS) remains a key challenge impeding market growth in the Middle East and Africa. While GOS is widely recognized for its prebiotic properties, including improved digestion and immune support, a large portion of the population in these regions lacks understanding of functional ingredients and their role in overall wellness.

Similarly, in the Middle East, despite rising health consciousness, confusion persists between prebiotics and probiotics, affecting purchasing decisions. This knowledge gap is further exacerbated by the limited presence of educational campaigns and promotional activities by ingredient suppliers and food manufacturers.

Besides, rural populations, which constitute a significant portion of the region’s demographics, have minimal exposure to scientific health messaging due to low literacy rates and limited digital connectivity. Without targeted efforts to educate consumers and build trust in GOS-containing products, market penetration will remain constrained, especially in non-urban areas where awareness levels are lowest.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Application, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | United States, Canada, Mexico, Rest of North America |

| Market Leaders Profiled | AGC Inc., Guardian Industries, Saint-Gobain, Şişecam, Vitro Architectural Glass, CARDINAL GLASS INDUSTRIES, INC, Schott AG, Paragon Tempered Glass, LLC, Xinyi Glass Holdings Limited., Vitrum Glass Group, and others. |

SEGMENTAL ANALYSIS

By Product Insights

The insulated glass units (IGUs) segment commanded the North America architectural flat glass market, accounting for 45% of total revenue in 2024. This dominance is primarily attributed to the growing emphasis on energy efficiency and thermal insulation in both residential and commercial construction.

One of the key drivers behind this segment’s leadership is the increasing adoption of IGUs in new building projects and retrofitting initiatives aimed at reducing heating and cooling costs. IGUs, which typically consist of two or more glass panes separated by a gas-filled space, offer superior insulation and noise reduction properties compared to single-pane alternatives.

Also, the rise in green building certifications such as LEED and ENERGY STAR has further reinforced demand for insulated glass products. With ongoing advancements in smart glass integration and low-emissivity coatings, the insulated glass units segment continues to solidify its position as the cornerstone of the architectural flat glass industry.

The laminated glass segment is projected to grow at the fastest CAGR of nearly 7.1%. This rapid expansion is largely driven by increasing safety regulations, rising use in high-rise buildings, and expanding applications in hurricane-resistant and soundproof glazing.

A major factor contributing to this segment’s acceleration is the growing requirement for impact-resistant materials in urban infrastructure and public buildings. The International Building Code (IBC) mandates the use of laminated glass in areas prone to human impact, such as doors, side panels, and near walking surfaces.

Another key driver is the increasing deployment of laminated glass in hurricane-prone regions such as Florida and the Gulf Coast, where building codes require shatter-resistant materials to mitigate damage from extreme weather events. Additionally, laminated glass is gaining traction in luxury residential developments and high-end commercial spaces for its ability to reduce external noise while maintaining optical clarity. These trends position laminated glass as the fastest-growing product type in the North America architectural flat glass market.

By Application Insights

The non-residential application segment prevailed in the North America architectural flat glass market, representing 52.1% of total demand in 2024. This dominance is credited to the extensive use of flat glass in office buildings, retail complexes, airports, hospitals, and institutional structures that prioritize natural lighting, aesthetic appeal, and structural transparency.

One of the primary drivers behind this segment’s leadership is the robust growth in commercial construction activity across major metropolitan areas. According to the U.S. Census Bureau, non-residential construction spending reached USD 1.1 trillion in 2023, with architects increasingly specifying high-performance glass for curtain walls, skylights, and façades to meet sustainability standards and modern design preferences. The trend toward open-plan offices and daylighting strategies has also contributed to heightened demand for large-format, thermally efficient glass systems.

Apart from these, government and corporate investments in infrastructure modernization have played a crucial role. With continued urban development and regulatory support for sustainable building practices, the non-residential segment remains the dominant application area for architectural flat glass in North America.

The residential application segment is anticipated to expand at the highest CAGR of around 6.8%. This accelerated growth is being propelled by the increasing preference for energy-efficient homes, rising home renovation activities, and evolving architectural trends favoring expansive glazing and daylight optimization.

One significant factor driving this segment’s momentum is the surge in high-end residential construction, particularly in urban and suburban markets where floor-to-ceiling windows, sliding glass doors, and multi-glazed facades are becoming standard features.

Another key contributor is the growing consumer interest in passive house designs and net-zero energy buildings, which rely heavily on high-performance glass to minimize HVAC usage. Moreover, the popularity of home improvement shows and digital design platforms has raised awareness among homeowners about the benefits of premium glazing products, further accelerating adoption. These developments underscore the residential segment’s status as the fastest-growing application category in the North America architectural flat glass market.

COUNTRY-LEVEL ANALYSIS

United States Architectural Flat Glass Market Insights

The United States maintained the dominant position in the North America architectural flat glass market, commanding more than 82% of regional market share in 2024. As one of the world’s most developed construction economies, the U.S. benefits from a strong pipeline of commercial, residential, and institutional building projects that drive consistent demand for high-performance glazing materials.

One of the key factors behind this dominance is the country’s proactive approach to sustainable building practices. Besides, federal and state-level incentives for green construction have encouraged widespread adoption of insulated and coated glass variants in both new builds and retrofit projects.

Another contributing element is the continuous expansion of urban infrastructure and mixed-use developments, particularly in major metropolitan areas like New York, Los Angeles, and Chicago. With ongoing technological innovation and policy support, the United States remains the core hub of the North America architectural flat glass industry.

Canada Architectural Flat Glass Market Insights

Canada's market is distinguished by its strong emphasis on sustainable building practices, energy efficiency mandates, and seismic-resistant construction requirements, all of which influence glass selection and usage patterns.

A major growth catalyst is the Canadian government’s commitment to reducing greenhouse gas emissions through green building policies. Another key contributor is the increasing adoption of laminated and tempered glass in seismic zones, particularly in British Columbia and Quebec, where building codes mandate impact-resistant materials for safety compliance. With continued investment in eco-conscious architecture and code-driven safety standards, Canada is emerging as a key player in the architectural flat glass landscape.

Mexico Architectural Flat Glass Market Insights

Mexico is positioned as a rapidly developing market. Mexico has seen rising demand for flat glass, particularly in commercial real estate, industrial parks, and government-led infrastructure projects aimed at modernizing public buildings and transportation hubs.

One of the key growth drivers is the country’s expanding manufacturing sector, especially in the automotive and electronics industries, which require climate-controlled environments with high-performance glazing for administrative and operational spaces.

Another contributing factor is the increasing presence of international architectural firms and global construction companies entering the Mexican market, bringing with them design philosophies that emphasize daylighting, thermal efficiency, and visual connectivity. With continued investment in urban development and cross-border partnerships, Mexico is playing an increasingly influential role in shaping the broader North America architectural flat glass market.

COMPETITIVE LANDSCAPE

The competition in the North America architectural flat glass market is characterized by technological differentiation, brand strength, and strategic positioning within the broader construction ecosystem. A few dominant players control a significant portion of the market, leveraging extensive distribution networks, long-standing relationships with architects and contractors, and a strong reputation for quality and performance. However, smaller regional manufacturers are gaining traction by offering cost-effective alternatives and localized service models tailored to specific geographic demands.

A key battleground for competitive advantage lies in product innovation, particularly in energy-efficient and safety-enhanced glass technologies. Companies are increasingly focused on developing advanced coatings, smart glass integration, and customized glazing solutions to meet evolving architectural trends and regulatory requirements. Additionally, sustainability commitments and carbon reduction initiatives are shaping purchasing decisions among developers and government agencies, prompting suppliers to emphasize eco-friendly manufacturing processes and recyclable materials.

Market participants are also engaging in strategic collaborations with building consultants, green certification bodies, and real estate developers to drive adoption in high-profile projects. As demand for resilient, thermally efficient, and aesthetically versatile materials continues to rise, the architectural flat glass sector remains highly dynamic, requiring continuous adaptation to maintain relevance and leadership.

MARKET KEY PLAYERS

Companies playing a dominant role in the North America architectural flat glass market profiled in this report are

- AGC Inc.

- Guardian Industries

- Saint-Gobain

- Şişecam

- Vitro Architectural Glass

- CARDINAL GLASS INDUSTRIES, INC

- Schott AG

- Paragon Tempered Glass, LLC

- Xinyi Glass Holdings Limited.

- Vitrum Glass Group

TOP LEADING PLAYERS IN THE MARKET

Guardian Glass is a leading global manufacturer of glass products for architectural, residential, and automotive applications. In North America, the company plays a pivotal role in shaping the architectural flat glass landscape through its innovative product lines such as SunGuard coated glass and Clarity Extra Clear glass. Guardian’s focus on sustainability, energy efficiency, and design flexibility has made it a preferred supplier for high-performance glazing solutions across commercial and institutional buildings.

Saint-Gobain, operating under CertainTeed in North America, is a major contributor to the architectural flat glass market, offering a comprehensive portfolio that includes insulated, laminated, and tempered glass solutions. The company's commitment to green building standards and material innovation has positioned it as a key player in sustainable construction. Saint-Gobain’s extensive R&D capabilities and integration with smart building technologies further reinforce its leadership in modern architectural design.

Vitro Architectural Glass is a dominant force in the North American flat glass industry, known for its high-performance glass products designed to enhance building aesthetics, thermal efficiency, and occupant comfort. The company provides a wide range of coated and uncoated flat glass products tailored for curtain walls, windows, and facades. Vitro’s strategic partnerships with architects, builders, and sustainability organizations have significantly influenced the adoption of energy-efficient glazing systems across the continent.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Leading companies are continuously investing in research and development to introduce next-generation glass solutions that offer superior thermal insulation, solar control, and acoustic performance. Innovations such as low-emissivity coatings, triple-glazed units, and smart glass integration are enhancing the functional and aesthetic value of architectural flat glass, enabling firms to differentiate themselves in a competitive marketplace.

To meet growing demand and reduce lead times, key players are expanding their production facilities and logistics networks across North America. Establishing regional hubs allows companies to respond more efficiently to local market needs while ensuring compliance with evolving building codes and environmental regulations, strengthening their foothold in both urban and emerging markets.

Major market participants are forging strategic alliances with design professionals, construction firms, and green certification bodies to promote the use of high-performance glass in new developments. By aligning with industry stakeholders, companies influence specification trends and support the widespread adoption of advanced glazing systems in LEED-certified and energy-efficient buildings.

RECENT MARKET DEVELOPMENTS

- In March 2024, Guardian Glass launched a new line of ultra-thin, high-performance coated glass products specifically engineered for curved façade applications, catering to the growing trend of architecturally distinctive building designs in urban centers.

- In June 2024, Saint-Gobain expanded its technical training center in Chicago to provide architects, contractors, and glazing professionals with hands-on education on the installation and benefits of high-performance architectural glass, reinforcing its brand authority in the construction sector.

- In September 2024, Vitro Architectural Glass introduced a digital visualization tool for architects and designers, allowing them to simulate how different glass types would perform in real-world conditions, enhancing customer engagement and streamlining the specification process.

- In December 2024, AGC Glass North America announced a joint venture with a U.S.-based window systems provider to co-develop integrated framing and glazing solutions optimized for passive house and net-zero building standards.

- In February 2025, Cardinal Glass Industries inaugurated a new float glass manufacturing facility in Texas, aimed at increasing domestic production capacity and reducing dependency on external supply chains amid rising demand for energy-efficient building materials.

MARKET SEGMENTATION

This research report on the North America architectural flat glass market is segmented and sub-segmented into the following categories.

By Product

- Basic

- Tempered

- Laminated

- Insulated

- Others

By Application

- Residential

- Non-residential

- Industrial

By Country

- United States

- Canada

- Mexico

- Rest of North America

Frequently Asked Questions

What factors are driving growth in the North America Architectural Flat Glass Market?

Market growth is driven by rising construction activity, urbanization, new home sales, renovation projects, and increased demand for energy-efficient and aesthetic building materials

Which glass types are most popular in the North America Architectural Flat Glass Market?

Laminated, tempered, basic float, and insulating glass are widely used, with tempered glass favored for its safety and strength in construction applications

How does urbanization impact the North America Architectural Flat Glass Market?

Urbanization boosts demand for new residential and commercial buildings, increasing the need for architectural flat glass in city infrastructure

What role does the construction industry play in the North America Architectural Flat Glass Market?

The construction sector is the largest end-user, accounting for about 70% of flat glass consumption, especially in windows, facades, and doors

How is the commercial sector influencing the North America Architectural Flat Glass Market?

Growth in offices, retail, hospitality, and R&D facilities is driving demand for flat glass in commercial construction and renovation

What are the key trends in the North America Architectural Flat Glass Market?

Trends include energy-efficient glass, smart glass, advanced coatings, solar control, and sustainable materials for green building initiatives

How is technological innovation shaping the North America Architectural Flat Glass Market?

Innovations such as smart glass, self-cleaning coatings, and improved thermal insulation are expanding product applications and market appeal

How are government policies and regulations affecting the North America Architectural Flat Glass Market?

Policies promoting energy efficiency, sustainability, and infrastructure investment are fueling market expansion and adoption of advanced glass solutions

What challenges does the North America Architectural Flat Glass Market face?

Key challenges include fluctuating raw material costs, environmental regulations, supply chain disruptions, and competition from substitute materials

What future opportunities exist for vendors in the North America Architectural Flat Glass Market?

Opportunities include expanding into smart glass, energy-efficient products, and capitalizing on infrastructure investments and urbanization trends

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com