North America Data Center Liquid Cooling Market Size, Share, Trends & Growth Forecast Report By Component (Solutions, Services), End User (Colocation Providers, Enterprises, Hyperscale Data Centers), Data Center Type (Small & Mid-Sized Data Centers, Large Data Centers), and Country (United States, Canada, Mexico, Rest of North America) – Industry Analysis, 2026 to 2034

Market Size, 2025

$0.97 BnMarket Estimate, 2026

$1.28 BnMarket Forecast, 2034

$12.19 BnCAGR, 2026–2034

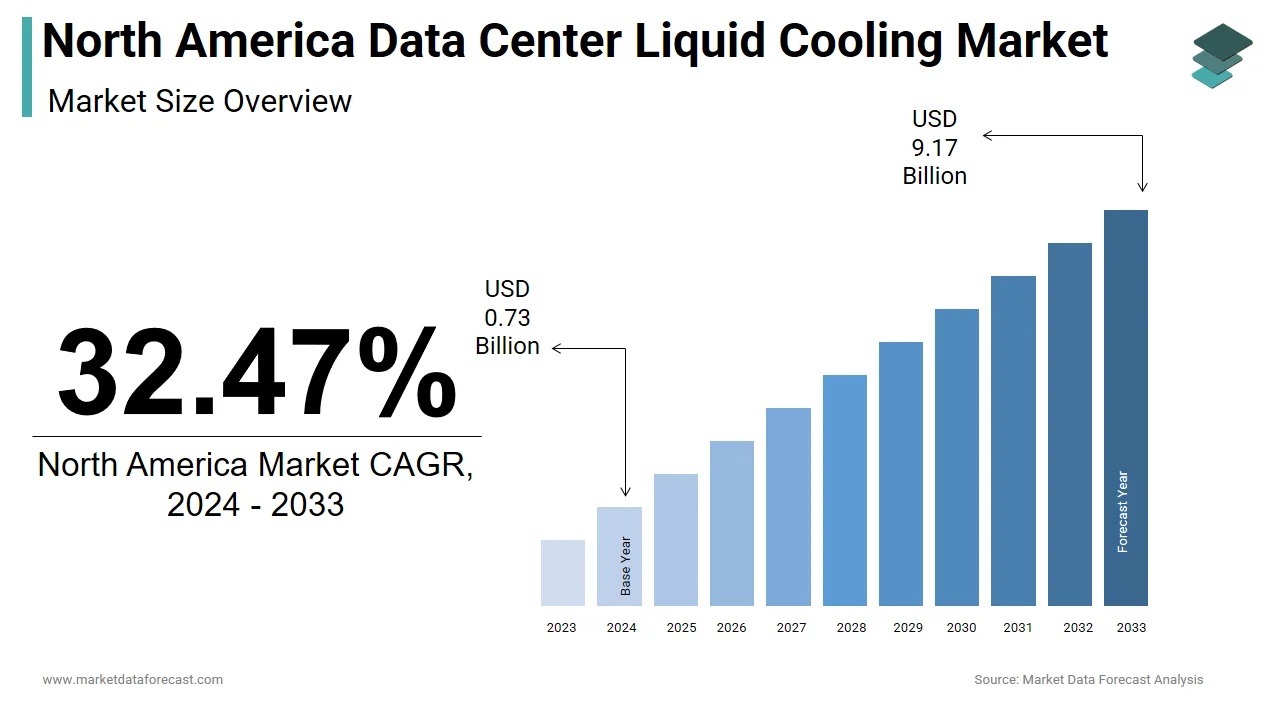

32.47%North America Data Center Liquid Cooling Market Size

The North America data center liquid cooling market was valued at USD 0.97 billion in 2025, is estimated to reach USD 1.28 billion in 2026, and is projected to reach USD 12.19 billion by 2034, growing at a CAGR of 32.47% from 2026 to 2034.

Data center liquid cooling is deploying advanced thermal management solutions that utilize liquid-based methods such as direct-to-chip, immersion cooling, and rear door heat exchangers to dissipate heat generated by high-density computing infrastructure. As data centers evolve to support AI, machine learning, cloud computing, and edge processing, traditional air-cooling systems are proving inadequate in managing rising power densities and energy consumption.

North America has become a focal point for liquid cooling adoption due to its concentration of hyperscale data centers operated by companies like Google, Microsoft, Meta, and Amazon. These firms are increasingly seeking sustainable and efficient ways to manage server rack densities exceeding 20 kW per cabinet a level at which air cooling becomes inefficient and costly. This growing demand has prompted industry leaders to explore more effective cooling technologies to reduce operational costs and environmental impact.

In parallel, regulatory pressure to meet sustainability goals is accelerating the shift toward liquid cooling. Apart from these, Canada has seen increased investment in green data center initiatives, with provinces such as Quebec and British Columbia promoting colocation facilities powered by renewable energy and supported by liquid cooling infrastructures.

MARKET DRIVERS

Rising Power Density and Thermal Demands in Data Centers

The escalating power density within modern server racks is one of the primary drivers fueling the North America data center liquid cooling market. As data centers transition from conventional 5–10 kW per rack configurations to ultra-high-density setups exceeding 30–50 kW per rack, traditional air-based cooling systems struggle to maintain optimal operating temperatures efficiently. According to the Uptime Institute, over 60% of new hyperscale data center builds in 2024 featured rack densities above 20 kW, signaling a structural shift in thermal management requirements.

This trend is largely attributed to the proliferation of artificial intelligence (AI) accelerators, graphics processing units (GPUs), and high-performance computing (HPC) clusters, which generate significantly more heat than standard processors. For instance, NVIDIA’s latest AI chips can draw up to 700 watts per GPU, necessitating advanced cooling solutions to prevent thermal throttling and hardware degradation. Also, maintaining recommended inlet air temperatures for these components using air cooling alone leads to inefficiencies, prompting operators to adopt liquid cooling alternatives such as direct-to-chip and two-phase immersion cooling.

Moreover, leading cloud service providers, including Google, Meta, and Microsoft, have publicly endorsed liquid cooling as a strategic solution for next-generation data centers. Their pilot programs with companies like Submer and Green Revolution Cooling highlight the growing industry consensus on the necessity of liquid-based thermal management.

Increasing Emphasis on Energy Efficiency and Sustainability

The growing emphasis on energy efficiency and sustainability across the technology sector is a critical driver propelling the North America data center liquid cooling market. Data centers are among the largest consumers of electricity globally, and with increasing scrutiny from regulators, investors, and environmental organizations, operators are under pressure to reduce their carbon footprint while optimizing operational expenditures.

Liquid cooling offers a compelling alternative to conventional air-based systems by delivering superior thermal transfer capabilities, reducing overall energy consumption, and improving power usage effectiveness (PUE). This improvement translates into significant cost savings and reduced greenhouse gas emissions, aligning with corporate ESG commitments.

Besides, major cloud providers such as Apple, Amazon, and Microsoft have pledged to achieve net-zero carbon emissions by 2030 or earlier, further incentivizing the adoption of energy-efficient cooling technologies. In response, colocation providers and enterprise data center operators are increasingly integrating liquid cooling solutions into their designs.

MARKET RESTRAINTS

High Initial Investment and Infrastructure Complexity

The high initial capital expenditure required for implementation, along with the complexity involved in retrofitting existing infrastructure, is one of the most significant restraints affecting the North America data center liquid cooling market. Unlike conventional air cooling systems, which rely on well-established mechanical layouts, liquid cooling demands specialized engineering, plumbing modifications, and precision integration with IT equipment. In addition, the upfront cost of deploying a full-scale liquid cooling system, including piping, coolant distribution units, and compatible server racks, can be up to three times higher than upgrading an existing air-based system.

Furthermore, the installation of liquid cooling systems requires extensive planning to ensure leak prevention, compatibility with server hardware, and redundancy in case of system failure. Many legacy data centers were not designed with liquid cooling in mind, making retrofitting both technically challenging and financially burdensome.

Moreover, the lack of standardized protocols for liquid cooling deployments complicates procurement and long-term maintenance strategies. While some vendors offer proprietary cooling loops tailored to specific server models, interoperability remains limited, forcing customers to commit to single-source suppliers.

Operational Risks and Maintenance Concerns

The apprehension surrounding operational risks and ongoing maintenance complexities is another notable restraint on the North America data center liquid cooling market. Despite the efficiency advantages of liquid cooling, many data center operators remain cautious about introducing liquids, particularly water or dielectric fluids, into close proximity with sensitive electronic equipment.

Maintenance of liquid cooling systems also presents unique challenges compared to air-based alternatives. Regular monitoring of coolant quality, pump performance, and heat exchanger efficiency is essential to prevent performance degradation or hardware damage. As per a study by the Electric Power Research Institute (EPRI), liquid cooling systems require more frequent inspections and preventive maintenance interventions, increasing labor costs and operational overhead.

Further, the availability of trained technicians familiar with liquid cooling technologies is limited, creating a skills gap that hampers large-scale adoption. While leading vendors provide training and support services, many enterprises still prefer to stick with well-understood air cooling methodologies rather than invest in new expertise.

MARKET OPPORTUNITIES

Expansion of AI and High-Performance Computing Workloads

The rapid expansion of artificial intelligence (AI) and high-performance computing (HPC) workloads is one of the most promising opportunities emerging in the North America data center liquid cooling market. As enterprises and research institutions increasingly deploy AI-driven analytics, deep learning models, and real-time processing applications, the demand for powerful computational infrastructure has surged.

These AI and HPC workloads are driving a fundamental shift in data center architecture, characterized by denser server configurations and accelerated computing hardware such as GPUs and TPUs. As per NVIDIA, its latest generation of AI chips delivers over 2.5 times the performance per watt compared to predecessors, yet still generates significantly more heat per unit area. As a result, traditional air cooling systems are becoming inadequate in managing thermal loads, pushing data center operators to explore more efficient alternatives such as direct-to-chip and immersion cooling.

Leading hyperscalers, including Microsoft, Meta, and Google, have already initiated large-scale trials of liquid cooling solutions to support their AI clusters. In collaboration with startups like Asperitas and Submer, they are testing both single-phase and two-phase immersion cooling techniques to maximize performance while minimizing energy consumption.

Growth of Edge Data Centers and Modular Deployments

The increasing deployment of edge data centers and modular computing infrastructures presents a significant opportunity for the North America data center liquid cooling market. As industries embrace digital transformation, there is a growing need for low-latency computing resources closer to end-users, particularly in sectors such as manufacturing, healthcare, autonomous vehicles, and smart cities. According to Gartner, over 75% of enterprise-generated data will be processed outside centralized data centers by 2025, necessitating robust and efficient cooling solutions for compact, high-density edge environments.

Edge data centers often operate in constrained spaces with limited access to traditional HVAC infrastructure, making liquid cooling an attractive alternative due to its space-saving attributes and superior thermal efficiency. Modular data centers, which are pre-fabricated and rapidly deployable, are increasingly being equipped with integrated liquid cooling systems to handle intensive workloads without requiring extensive mechanical modifications.

Several liquid cooling vendors have responded by developing compact, self-contained cooling units tailored for edge and micro-data centers. Companies like CoolIT Systems and Iceotope Technologies have introduced scalable, rack-level cooling solutions that can be seamlessly embedded into modular enclosures.

MARKET CHALLENGES

Lack of Industry Standards and Interoperability Issues

The absence of universally accepted industry standards and interoperability guidelines is a significant challenge facing the North America data center liquid cooling market. Unlike air cooling, which benefits from decades of standardized airflow management practices and equipment compatibility, liquid cooling lacks a cohesive framework for integration across different vendors and data center architectures. Also, the lack of standardized interfaces, fluid types, and safety protocols creates uncertainty for operators considering large-scale deployments.

This fragmentation results in vendor-specific cooling solutions, limiting flexibility and increasing dependency on single suppliers. For example, some manufacturers design cooling loops exclusively for their own server platforms, making it difficult for customers to mix and match hardware from multiple vendors within the same liquid-cooled environment.

Apart from these, discrepancies in coolant composition ranging from water-glycol mixtures to synthetic dielectric fluids complicate maintenance procedures and increase operational complexity.

Integration Complexity with Existing Data Center Architectures

Integrating liquid cooling systems into existing data center architectures poses a major technical and logistical challenge, hindering widespread adoption across North America. Most legacy data centers were originally designed around air-based cooling infrastructures, with raised floors, CRAC units, and hot/cold aisle containment strategies optimized for conventional airflow patterns. Retrofitting these facilities to accommodate liquid cooling requires extensive modifications to plumbing, electrical systems, and rack configurations, often resulting in prolonged downtime and increased capital expenditure.

This complexity is further compounded by the need to ensure leak detection, fluid containment, and redundancy mechanisms to protect against potential failures.

Moreover, hybrid deployments where portions of a data center utilize liquid cooling while others remain air-cooled introduce additional coordination challenges. Temperature gradients, humidity control, and airflow dynamics must be carefully managed to prevent condensation or thermal imbalances.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Component, End User, Data Center Type, Cooling Type, Enterprise, Cooling Medium, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | United States, Canada, Mexico, Rest of North America |

| Market Leaders Profiled | Rittal GmbH & Co. KG, Vertiv Group Corp, Green Revolution Cooling Inc. (GRC), Submer, Schneider Electric, LiquidStack Holding B.V., Iceotope Precision Liquid Cooling, COOLIT SYSTEMS, DUG Technology, DCX Liquid Cooling Systems, Delta Power Solutions, Wiwynn Corporation, LiquidCool Solutions, Inc., Midas Immersion Cooling, BOYD, Kaori Heat Treatment Co, Ltd, Chilldyne, Inc., Modine Manufacturing Company, Asperitas, Zutacore, Inc., Flex Ltd, Asetek, STULZ GMBH, Teimmers, Koolance, Inc, GIGA-BYTE Technology Co., Ltd., PEZY Computing, TAS, OptiCool Technologies, Accelsius LLC, and Seguente Inc. |

SEGMENTAL ANALYSIS

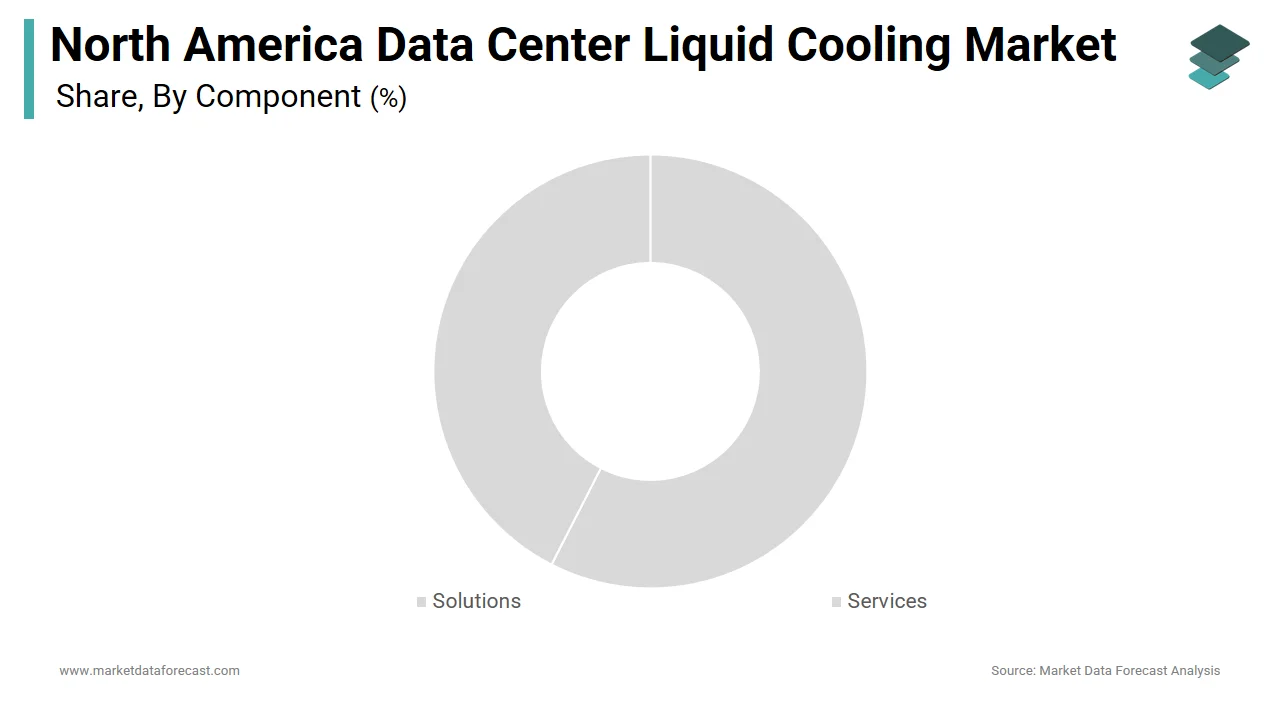

By Component Insights

The solution segment dominated the North America data center liquid cooling market by capturing a substantial portion of total revenue in 2025. Increasing deployment of hardware-based liquid cooling systems, such as direct-to-chip cooling, rear door heat exchangers, and immersion cooling solutions that are essential for managing high-density computing environments, is primarily driving the dominance of the solution segment.

Also, the rising power density within server racks, particularly in hyperscale and colocation data centers, is another key factor behind this segment’s growth. According to the Uptime Institute, over 60% of new data center builds in 2024 featured rack densities exceeding 20 kW, necessitating advanced cooling solutions that traditional air-based systems cannot efficiently manage. As a result, operators are investing heavily in liquid cooling hardware tailored for GPU clusters, AI accelerators, and edge computing nodes.

Besides, major cloud service providers such as Microsoft, Meta, and Google have initiated large-scale trials and deployments of liquid cooling technologies. For instance, Microsoft's Project Natick explored underwater data centers using liquid-based thermal management, while Meta has been testing two-phase immersion cooling with vendors like Green Revolution Cooling and Submer.

Moreover, advancements in modular and scalable cooling units have made it easier for enterprises and colocation providers to integrate these solutions into existing or newly constructed facilities.

The services segment is emerging as the fastest-growing part of the North America data center liquid cooling market and is projected to expand at a CAGR of 23.5% from 2026 to 2034. This rapid growth is attributed to the Increasing complexity of liquid cooling deployments, and the need for expert consultation, installation, maintenance, and monitoring services is propelling the rapid growth of the services segment.

In addition, the lack of in-house expertise among many data center operators regarding the integration and operation of liquid cooling systems is another primary driver for this expansion. Unlike conventional air cooling, liquid-based infrastructures require specialized knowledge in fluid dynamics, leak prevention, system compatibility, and long-term maintenance.

In addition, leading technology firms and colocation providers are engaging consulting firms and managed service vendors to optimize their thermal strategies. Companies such as Schneider Electric, Vertiv, and Airedale by Modine offer comprehensive lifecycle support from feasibility studies and system design to predictive analytics and remote diagnostics, helping clients ensure reliability and performance.

Furthermore, as more organizations adopt hybrid cooling models (combining air and liquid systems), the demand for integration and optimization services is accelerating.

By End User Insights

The hyperscale data centers segment represented the biggest end-user in the North America data center liquid cooling market by accounting for 58.7% of total share in 2024. The exponential growth of artificial intelligence (AI), machine learning, and high-performance computing (HPC) workloads is one key driver behind this dominance ofthe hyperscale data centers segment. These facilities, operated by global cloud service providers such as Amazon Web Services, Microsoft Azure, and Google Cloud, are at the forefront of adopting advanced thermal management solutions due to their massive scale and high-performance computing demands. Traditional air-cooling methods struggle to manage these extreme thermal loads efficiently, making liquid cooling an increasingly viable alternative.

Moreover, hyperscale operators are under pressure to meet aggressive sustainability targets. Many have pledged net-zero emissions by 2030, prompting them to explore energy-efficient cooling options that reduce overall power usage effectiveness (PUE). As per ASHRAE, liquid cooling can lower PUE values to below 1.1, compared to typical air-cooled data centers that operate between 1.4 and 1.8, offering significant improvements in operational efficiency and carbon footprint reduction.

Major hyperscalers have also launched pilot programs with liquid cooling vendors to test immersion cooling, direct-to-chip, and rear-door heat exchanger technologies. These initiatives are expected to transition from experimental to mainstream adoption in the coming years.

The enterprise segment is the fastest-growing in the North America data center liquid cooling market and is expanding at a CAGR of 24.1% during the forecast period. Increasing digital transformation efforts across industries such as finance, healthcare, manufacturing, and government, which are driving the need for high-density computing and efficient thermal management solutions, is attributed to the rapid growth of the enterprise segment.

Also, the rise of AI-driven analytics and real-time processing applications that require powerful computational resources is another catalyst for enterprise adoption. According to Gartner, over 70% of large enterprises in North America were piloting AI applications by mid-2024, many of which rely on GPU clusters generating substantial heat. To maintain optimal operating conditions without excessive energy consumption, companies are turning to liquid cooling alternatives such as direct-to-chip and single-phase immersion systems.

The push toward sustainability and energy efficiency within corporate IT departments is an additional key driving factor. Many Fortune 500 companies have committed to reducing their environmental impact, aligning with broader ESG goals. As per Deloitte, over 65% of enterprise CIOs listed energy-efficient infrastructure upgrades as a top priority in 2024, directly influencing investment decisions around cooling technologies.

Moreover, enterprises are increasingly deploying edge computing infrastructure closer to end-users, where space and airflow constraints make air cooling less effective. Modular and compact liquid cooling systems offer an ideal solution for these distributed environments

COUNTRY-LEVEL ANALYSIS

United States Data Center Liquid Cooling Market Insights

The United States held the dominant position in the North America data center liquid cooling market by contributing 79.5% of regional revenue in 2024. As home to the world’s largest hyperscale cloud providers, including Amazon, Microsoft, Google, and Meta, the U.S. leads in both the scale and sophistication of data center infrastructure, driving early adoption of advanced thermal management technologies.

A primary driver of this leading position is the country’s concentration of AI research centers, high-performance computing facilities, and financial trading platforms, all of which generate immense heat loads that exceed the capacity of traditional air cooling.

Further, U.S.-based colocation providers such as Digital Realty, Equinix, and CoreSite are actively integrating liquid cooling into their offerings to cater to enterprise and cloud customers seeking high-density hosting environments. The Department of Energy (DOE) has also supported innovation in cooling technologies through research grants and public-private partnerships, fostering a conducive environment for market growth.

Canada Data Center Liquid Cooling Market Insights

Canada is another key player in the North America data center liquid cooling market, which is driven by growing investments in sustainable infrastructure, AI research hubs, and regional colocation expansions. The country’s commitment to reducing carbon emissions and leveraging renewable energy sources has created a favorable climate for advanced cooling technologies.

A key growth driver is Canada’s emergence as a hub for AI and machine learning research, particularly in cities like Toronto, Montreal, and Vancouver. Universities and private research institutions are also deploying liquid cooling to manage computational demands in deep learning and scientific modeling.

In addition, Canadian provinces such as Quebec and British Columbia have promoted colocation development due to abundant hydroelectric power and cooler ambient temperatures. As per Natural Resources Canada, data centers in Quebec alone accounted for over 20% of national IT infrastructure investments in 2024, many of which incorporated liquid cooling to enhance energy efficiency and compliance with provincial sustainability mandates.

Furthermore, multinational cloud providers, including IBM, AWS, and Microsoft have expanded their presence in Canada, bringing with them next-generation thermal management strategies.

Rest of North America Data Center Liquid Cooling Market Insights

The Rest of North America, comprising Mexico and select Caribbean territories, accounts for a notable share of the regional data center liquid cooling market in 2024. While smaller in scale compared to the U.S. and Canada, this segment is undergoing gradual transformation due to increasing digitalization, economic modernization, and investments in edge computing infrastructure.

Mexico, in particular, is emerging as a focal point for data center expansion, driven by proximity to the U.S., growing outsourcing opportunities, and expanding cloud adoption across banking, manufacturing, and logistics sectors.

Some of these new facilities are incorporating liquid cooling to support high-performance computing and AI-driven analytics.

Caribbean nations such as Jamaica and Puerto Rico are also witnessing interest in modular and edge data centers, particularly in sectors like fintech, tourism, and government services.

COMPETITIVE LANDSCAPE

The competition in the North America data center liquid cooling market is marked by rapid technological advancements, increasing vendor specialization, and a growing emphasis on sustainability. As data centers continue to scale in complexity and power density, particularly with the rise of AI, machine learning, and edge computing, the demand for efficient and reliable cooling solutions has intensified. This has led to a surge in innovation, with both established players and emerging startups introducing differentiated offerings tailored to specific use cases and deployment models.

Market participants are vying not only on technical performance but also on ease of integration, operational simplicity, and environmental impact. The lack of standardized protocols and interoperability frameworks further complicates the landscape, prompting vendors to differentiate themselves through proprietary technologies, modular designs, and comprehensive service portfolios. While some firms focus on niche applications such as immersion cooling for GPU clusters, others emphasize scalable, plug-and-play solutions for broader enterprise adoption.

In parallel, hyperscale operators and colocation providers are playing an increasingly influential role in shaping market dynamics, often working closely with vendors to co-develop custom cooling infrastructures. This evolving ecosystem fosters both collaboration and competition, creating opportunities for agile players who can align with shifting industry priorities around efficiency, reliability, and long-term sustainability.

KEY MARKET PLAYERS

Noteworthy Companies dominating the North America data center liquid cooling market profiled in the report are

- Rittal GmbH & Co. KG

- Vertiv Group Corp

- Green Revolution Cooling Inc.

- Submer

- Schneider Electric

- LiquidStack Holding B.V.

- Iceotope

- COOLIT SYSTEMS

- DUG Technology

- DCX Liquid Cooling Systems

- Delta Power Solutions

- Wiwynn Corporation

- LiquidCool Solutions

- Midas Immersion Cooling

- BOYD

- Kaori Heat Treatment Co, Ltd

- Chilldyne

- Modine Manufacturing

- Asperitas

- Zutacore

- Flex Ltd

- Asetek

- STULZ GMBH

- Teimmers

- Koolance

- GIGA-BYTE Technology

- PEZY Computing

- TAS

- OptiCool Technologies

- Accelsius LLC

- Seguente Inc

TOP LEADING PLAYERS IN THE MARKET

One of the leading players in the North America data center liquid cooling market is Submer, a company that specializes in sustainable, high-performance liquid cooling solutions for data centers. Submer’s innovative approach to immersion cooling enables enterprises and hyperscalers to manage extreme heat loads while significantly improving energy efficiency. Its SmartPod technology allows seamless integration with existing infrastructure, making it a preferred choice for next-generation data centers focused on AI and edge computing.

Another key player is Green Revolution Cooling (GRC), known for pioneering two-phase immersion cooling systems tailored for high-density environments. GRC's technology leverages dielectric fluids to directly cool hardware components, eliminating the need for traditional air-based cooling. The company has been instrumental in driving adoption across government, research institutions, and cloud providers seeking scalable, eco-friendly thermal management strategies.

CoolIT Systems also holds a prominent position in the market by offering advanced liquid cooling technologies for enterprise servers, HPC clusters, and data center racks. CoolIT’s direct-to-chip cooling solutions are widely adopted by OEMs and colocation providers looking to enhance performance and sustainability. The company continues to expand its footprint through strategic partnerships and customized cooling platforms designed for evolving IT infrastructure demands.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

A major strategy employed by key players in the North America data center liquid cooling market is technology innovation and product diversification. Companies are continuously developing new cooling architectures such as single-phase and two-phase immersion cooling, rear door heat exchangers, and modular cooling units to meet the diverse needs of different end users, including hyperscale operators, colocation providers, and enterprise clients.

Another critical approach is strategic collaboration and ecosystem development. Leading vendors are partnering with server manufacturers, data center designers, and cloud service providers to create integrated cooling solutions that can be easily deployed within existing or new infrastructure, ensuring compatibility and scalability without disrupting operations.

Lastly, companies are focusing on expanding their regional presence through localized support and deployment expertise. Establishing regional service hubs and engaging with local consultants and system integrators helps ensure smoother implementation, better after-sales support, and faster response times, which are essential for maintaining customer trust and gaining a competitive edge in an evolving market landscape.

RECENT MARKET DEVELOPMENTS

- In January 2024, Submer announced a strategic partnership with a leading U.S.-based cloud service provider to deploy its SmartPod immersion cooling technology in a new AI-driven data center facility. This initiative aims to optimize thermal efficiency while supporting high-density GPU workloads, reinforcing Submer’s position in the rapidly expanding AI infrastructure segment.

- In March 2024, Green Revolution Cooling launched a new line of modular immersion cooling units designed specifically for hybrid deployments in edge data centers. This development targets distributed computing applications across manufacturing, healthcare, and financial services, expanding GRC’s reach beyond traditional hyperscale environments.

- In June 2024, CoolIT Systems expanded its engineering team and opened a dedicated R&D center in Toronto, focusing on next-generation direct-to-chip cooling solutions tailored for enterprise and colocation markets. This move supports CoolIT’s commitment to innovation and regional expansion in North America.

- In September 2024, Asetek Industrial Products signed a distribution agreement with a major North American data center equipment wholesaler to increase accessibility of its rack-level liquid cooling systems. This partnership enhances Asetek’s market visibility and accelerates adoption among mid-sized data center operators.

- In November 2024, Iceotope Technologies unveiled a new self-contained immersion cooling module designed for retrofitting into legacy data centers without requiring structural modifications. This innovation addresses a key industry challenge and positions Iceotope as a leader in adaptable, scalable cooling solutions for existing facilities.

MARKET SEGMENTATION

This North America data center liquid cooling market research report is segmented and sub-segmented into the following categories.

By Component

- Solutions

- Indirect Liquid Cooling Solutions

- Direct Liquid Cooling Solutions

- Services

- Design & Consulting

- Installation & Deployment

- Support & Maintenance

By End User

- Colocation Providers

- Enterprises

- Hyperscale Data Centers

By Data Center Type

- Small & Mid-Sized Data Centers

- Large Data Centers

By Cooling Type

- Cold Plate Liquid Cooling

- Immersion Liquid Cooling

- Spray Liquid Cooling

By Enterprise

- BFSI

- IT & Telecom

- Media & Entertainment

- Healthcare

- Government & Defense

- Retail

- Research & Academia

- Other Enterprises

By Cooling Medium

- Water

- Dielectric

- Refrigerants

By Country

- United States

- Canada

- Mexico

- Rest of North America

Frequently Asked Questions

What is driving growth in the North America Data Center Liquid Cooling Market?

Growth is driven by rising AI workloads, cloud computing, edge deployments, high power densities, and the need for energy efficiency

How does liquid cooling compare to air cooling in North American data centers?

Liquid cooling offers higher energy efficiency, manages greater heat loads, and supports denser rack configurations compared to air cooling

Which is the largest component segment in the North America Data Center Liquid Cooling Market?

The solution segment leads, including immersion cooling, direct-to-chip, and high-performance cooling systems

Who are the key players in the North America Data Center Liquid Cooling Market?

Major companies include CoolIT Systems, Schneider Electric, Vertiv, LiquidStack, Rittal, Stulz, and Asetek

What end-users drive demand in the North America Data Center Liquid Cooling Market?

Hyperscale, cloud service providers, colocation, and enterprises with AI and high-performance computing workloads drive demand

What role does sustainability play in the North America Data Center Liquid Cooling Market?

Sustainability drives adoption due to lower power usage effectiveness (PUE), compliance with carbon reduction targets, and reduced environmental impact

How is liquid cooling used for artificial intelligence and HPC in North America?

AI and HPC increase rack densities and heat, making liquid cooling vital to maintain operational efficiency and performance

What are the main trends in technology for this market?

Key trends include direct-to-chip cooling, immersion cooling, smart control systems, and integration with renewable energy for green data centers

What challenges or barriers exist for liquid cooling adoption in North America?

Challenges include higher upfront costs, retrofitting legacy facilities, operational complexities, and control system integration

How do regulations and standards impact the North America Data Center Liquid Cooling Market?

Stricter energy efficiency regulations and carbon reduction targets promote the use of advanced cooling solutions, including liquid cooling

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com