North America Digital Banking Market Size, Share, Trends & Growth Forecast Report, Segmented By Deployment, Component, Mode, Service, Type, And By Country (The United States, Canada, Mexico), Industry Analysis From 2026 to 2034

Market Size, 2025

$8.92 BnMarket Estimate, 2026

$9.18 BnMarket Forecast, 2034

$11.57 BnCAGR, 2026–2034

2.93%North America Digital Banking Market Summary

The North America digital banking market size was valued at USD 8.92 billion in 2025 and is anticipated to reach USD 9.18 billion in 2026 to USD 11.57 billion by 2034, growing at a CAGR of 2.93% during the forecast period from 2026 to 2034.

Key Market Trends & Insights

- The United States was the top performer of the North American digital banking market in 2025

- Canada is expected to showcase strong growth throughout the forecast period.

- Based on Deployment, the cloud deployment segment dominated the market in 2025

- Based on Component, the platform segment held a significant share in the market in 2025.

Market Size & Forecast

2026 Market Size: USD 9.18 Billion

2034 projected Market Size: USD 11.57 Billion

CAGR (2026 to 2034): 2.93%

United States: Largest Market in 2026

Canada: Strongest Growth Region

North America Digital Banking Market Size

The North America digital banking market size was valued at USD 8.92 billion in 2025 and is anticipated to reach a valuation of USD 9.18 billion in 2026 and USD 11.57 billion by 2034, growing at a CAGR of 2.93%, from 2026 to 2034.

Digital banking is a range of services including online account management, mobile payments, digital wallets, peer-to-peer transfers, remote check deposit, loan applications, and investment management through interconnected technological platforms that eliminate or minimize the need for physical branch interactions. According to the Office of the Comptroller of the Currency (OCC), chartered national banks now offer an average of 12 digital service channels per institution, reflecting the comprehensive digital transformation of banking operations. Consumer behavior has fundamentally shifted toward digital-first financial interactions, with the Pew Research Center noting that 72% of North American consumers prefer digital channels for routine banking activities over in-person branch visits. The regulatory landscape, particularly concerning data security, privacy protection, and financial inclusion, continues to shape the market's trajectory while requiring institutions to balance innovation with compliance under frameworks such as the Gramm-Leach-Bliley Act and state-level data protection laws. The integration of real-time payment systems and instant fund transfer capabilities has accelerated the adoption of digital banking services across diverse demographic segments.

MARKET DRIVERS

Consumer Preference for Convenience and Accessibility

The fundamental shift in consumer preferences toward convenience, accessibility, and 24/7 service availability is escalating the growth of the North American digital banking market. Modern consumers increasingly expect banking services to be available whenever and wherever they need them, without the constraints of traditional branch operating hours or geographical limitations. The integration of mobile banking applications with biometric authentication, voice recognition, and one-touch transaction capabilities has created seamless user experiences that align with contemporary lifestyle expectations and digital behavior patterns. Remote work trends and geographical mobility have intensified demand for banking services that can be accessed from any location and device, particularly among professionals who travel frequently or work in distributed environments. The integration of artificial intelligence-powered virtual assistants and chatbots has enabled instant customer support and personalized financial guidance that operates continuously without human intervention. Consumer expectations for real-time transaction processing and immediate fund availability have driven financial institutions to invest heavily in digital infrastructure and instant payment capabilities. The ability to conduct complex banking activities, including loan applications, investment management, and insurance purchases, through digital channels has eliminated the need for time-consuming branch visits and paperwork submission. Social media influence and digital marketing have amplified awareness of innovative banking features and services by creating competitive pressure for traditional institutions to enhance their digital offerings.

Technological Innovation and Advanced Capabilities

The rapid advancement of cutting-edge technologies and the integration of sophisticated capabilities within digital banking platforms are driving the growth of the North American digital banking market. Financial institutions are increasingly investing in artificial intelligence, machine learning, and predictive analytics to deliver personalized financial services, fraud detection, and automated decision-making capabilities that enhance customer experiences and operational efficiency. Blockchain technology adoption has enabled faster cross-border payments, smart contract execution, and transparent transaction processing that appeals to tech-savvy consumers seeking innovative financial solutions. The integration of Internet of Things (IoT) devices with banking applications has created opportunities for contextual financial services that respond to user behavior patterns and environmental triggers. Cloud computing adoption has enabled financial institutions to scale digital services rapidly, reduce infrastructure costs, and improve system reliability while maintaining regulatory compliance and data security standards. Real-time payment systems and instant fund transfer capabilities have transformed consumer expectations for transaction speed and availability, driving demand for advanced digital banking features and continuous service improvement. The convergence of banking with social media platforms and messaging applications has enabled peer-to-peer payment solutions and social commerce integrations that resonate with digitally native consumers.

MARKET RESTRAINTS

Cybersecurity Concerns and Data Privacy Issues

The escalating cybersecurity concerns and data privacy issues that create consumer hesitancy and regulatory compliance challenges for financial institutions is restricting the growth of the North America digital banking market. Regulatory compliance requirements under frameworks such as the Gramm-Leach-Bliley Act, state privacy laws, and international data protection regulations create additional operational burdens and compliance costs for digital banking providers. Insider threats and employee-related security incidents remain significant concerns, as authorized personnel with access to sensitive systems can potentially compromise data security through negligence or intentional actions. The rapid evolution of cyber threats, including advanced persistent threats, zero-day exploits, and ransomware attacks, requires continuous security updates and patches that can impact system availability and user experience. Cross-border data transfers and international operations present additional security challenges, as financial institutions must comply with varying regulatory requirements and security standards across different jurisdictions.

Digital Divide and Accessibility Barriers

The digital divide and accessibility barriers are hampering the growth of the North American digital banking market. According to the Federal Communications Commission (FCC), approximately 19 million Americans lack access to broadband internet service meeting minimum speed requirements, with rural and low-income communities disproportionately affected by connectivity limitations. Language barriers and cultural differences create additional accessibility challenges for immigrant communities and non-English speaking populations who may struggle with digital interface navigation and financial terminology. Digital literacy limitations and technological anxiety prevent many consumers from fully utilizing advanced digital banking features, potentially limiting the value proposition and user engagement with sophisticated platforms. The complexity of modern digital banking interfaces and authentication processes can create usability challenges for individuals with disabilities, requiring specialized design considerations and accessibility features that may not be universally implemented. Rural banking populations often face unique challenges, including limited cellular coverage, slower internet speeds, and fewer technical support resources that can impact digital banking performance and reliability. The preference for human interaction and personalized service among certain demographic segments creates resistance to fully digital banking models and necessitates hybrid service approaches. Educational and training barriers prevent effective utilization of digital banking services, particularly among older adults and individuals with limited formal education who may require extensive support and guidance.

MARKET OPPORTUNITIES

Open Banking and API Ecosystem Development

The advancement of open banking frameworks and application programming interface (API) ecosystem development is lucratively creating new opportunities for the growth of the North American digital banking market. Open banking initiatives facilitate secure data sharing between financial institutions and authorized third-party providers by creating opportunities for innovative financial applications, personalized services, and streamlined customer experiences that were previously impossible with traditional closed banking systems. According to the Conference of State Bank Supervisors (CSBS), 73% of North American state-chartered banks have implemented open banking APIs or are actively developing API capabilities to enable third-party integrations and expand their service offerings. Fintech companies and technology startups have leveraged open banking frameworks to develop specialized financial applications, including budgeting tools, investment platforms, and expense management solutions that provide value-added services to banking customers. The standardization of API protocols and data formats has enabled faster integration development, reduced implementation costs, and improved interoperability between different financial institutions and technology providers. Consumer demand for comprehensive financial management solutions has driven the development of aggregation platforms that consolidate account information, transaction data, and financial insights from multiple institutions into unified dashboards and analytical tools. Regulatory support for open banking initiatives through frameworks such as the Consumer Financial Protection Bureau's guidance on data access has provided legal clarity and encouraged responsible innovation in the financial services sector. The integration of artificial intelligence and machine learning capabilities with open banking data has enabled advanced analytics, predictive modeling, and personalized financial recommendations that enhance customer value and engagement. Cross-institutional collaboration opportunities have emerged as banks and credit unions leverage API ecosystems to offer expanded services without significant internal development investments.

Embedded Finance and Non-Banking Integration

The expansion of embedded finance and integration with non-banking platforms is greatly influencing the growth of the North American digital banking market. Embedded finance refers to the integration of banking services and financial products directly into non-financial platforms, applications, and business processes, creating seamless financial experiences that occur naturally within consumers' daily activities and purchasing decisions. According to the Embedded Finance Coalition, over 200 major retailers, e-commerce platforms, and service providers in North America will have integrated banking services, including payment processing, lending, and savings products, into their customer experiences by 2023. The automotive industry has embraced embedded finance through dealer financing platforms, insurance integration, and vehicle subscription services that combine transportation with comprehensive financial solutions. The healthcare sector has adopted embedded finance for medical billing, insurance integration, and health savings account management that streamlines patient financial interactions and improves healthcare accessibility. Travel and hospitality industries have integrated banking services, including currency exchange, travel insurance, and loyalty program management, directly into booking platforms and customer experiences. The real estate market has embraced embedded finance through mortgage pre-qualification tools, escrow services, and property management payment systems that simplify complex financial transactions for buyers and sellers. The gig economy has driven demand for embedded banking solutions, including instant payment processing, tax management, and retirement savings integration that address the unique financial needs of independent contractors and freelancers. Supply chain and B2B platforms have integrated trade financing, invoice factoring, and cash management services that improve working capital efficiency and reduce transaction costs. The convergence of lifestyle applications with financial services has created opportunities for integrated solutions that combine banking with shopping, entertainment, and social activities in seamless user experiences.

MARKET CHALLENGES

Regulatory Compliance and Supervisory Requirements

The complex regulatory compliance requirements and evolving supervisory expectations are likely to hinder the growth of the North American digital banking market. According to the American Bankers Association (ABA), North American banks spend an average of 18% of their technology budgets on regulatory compliance and risk management activities, with digital banking initiatives requiring extensive documentation, testing, and approval processes before implementation. Anti-money laundering and know-your-customer requirements have become more complex in digital environments where customer onboarding occurs remotely and transaction patterns may differ significantly from traditional banking activities. The emergence of new service delivery models, including embedded finance, open banking, and API integrations, has required regulatory agencies to develop new supervisory frameworks and examination procedures that may not yet be fully mature or consistently applied. Cross-jurisdictional regulatory requirements create additional complexity for financial institutions operating in multiple states or serving customers across different regulatory regimes.

Legacy System Integration and Technology Modernization

The legacy system integration and technology modernization of innovation capabilities and create operational inefficiencies for financial institutions, is also challenging the growth of the North American digital banking market. The complexity of legacy system architectures, with multiple interconnected databases, proprietary interfaces, and outdated programming languages, creates significant technical challenges for integration with modern cloud-based platforms, mobile applications, and real-time processing systems. The cost of core system replacement and modernization can be prohibitively expensive, with major system upgrades requiring investments of hundreds of millions of dollars and multi-year implementation timelines that create financial and operational risks for financial institutions. The interdependence of legacy systems with existing business processes, regulatory reporting requirements, and third-party integrations creates cascading effects when modifications are made, requiring extensive testing and validation to ensure system stability and regulatory compliance. Vendor dependency and limited support for legacy systems create additional challenges, as original equipment manufacturers may discontinue support or require expensive maintenance agreements to keep aging systems operational. The skills gap in legacy system maintenance and modernization creates workforce challenges, as experienced technicians and programmers familiar with older technologies become increasingly scarce and expensive to retain. Integration challenges between legacy core systems and modern digital channels can result in data inconsistencies, processing delays, and customer experience degradation that impact competitive positioning and market reputation.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 2.93% |

| Segments Covered | By Deployment, Mode, Component, Service, Type, and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | The United States, Canada, Mexico, Rest of North America |

| Market Leaders Profiled | Appway AG, Alkami Technology Inc., Finastra, Fiserv, Inc., Crealogix AG, Temenos, Urban FT Group, Inc., Q2 Software, Inc., Sopra Banking Software, Tata ConsultancServicesce. |

SEGMENTAL ANALYSIS

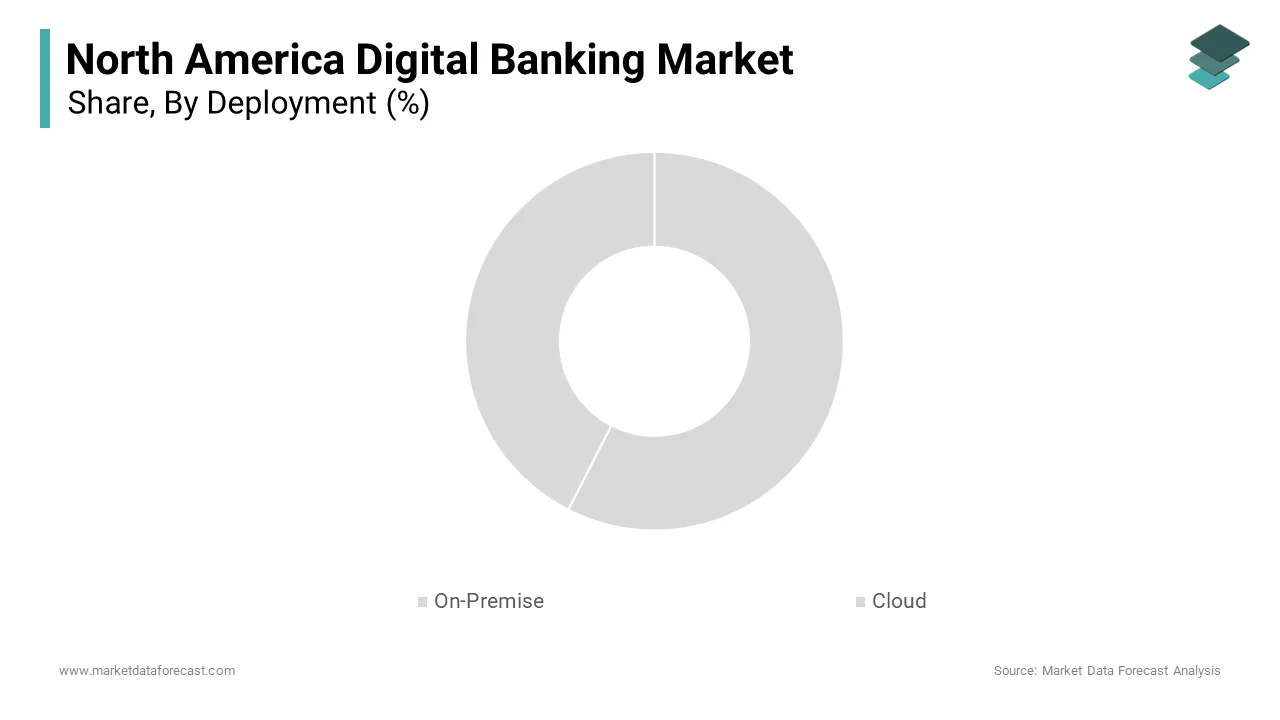

By Deployment Insights

The cloud deployment segment dominated the North American digital banking market share in 2025. Cloud deployment models offer significant financial advantages over traditional on-premise solutions, with banks reporting a 40-50% reduction in total cost of ownership, according to the Cloud Security Alliance's 2023 financial services survey. The average cloud deployment requires 6-8 months for implementation compared to 18-24 months for on-premise solutions by enabling faster time-to-market for new digital services as documented by cloud service provider implementation reports. Cloud platforms provide superior integration capabilities with emerging technologies and third-party services by enabling banks to rapidly deploy innovative digital banking features. Application programming interface (API) integration advantages enable seamless connectivity with fintech partners, with 90% of cloud-deployed digital banking platforms supporting real-time third-party integrations compared to 45% of on-premise systems, according to banking technology research firm Aite-Novarica.

The on-premise deployment segment is anticipated to grow with an expected CAGR of 12.4% in the coming years. Certain financial institutions, particularly large banks and credit unions handling sensitive government contracts, maintain a preference for on-premise deployment due to stringent data security and regulatory compliance requirements. Cybersecurity insurance requirements increasingly favor on-premise deployment for financial applications, with 55% of insurance providers offering reduced premiums for institutions utilizing on-premise solutions as documented by the Cybersecurity & Infrastructure Security Agency's risk assessment guidelines. Government contracting requirements for defense-related financial services mandate on-premise deployment, creating stable demand from 40% of federal credit unions, according to the National Credit Union Administration's regulatory guidance.

By Component Insights

The platform segment held a significant share of the North American digital banking market in 2025. Modern digital banking platforms provide integrated solutions that encompass core banking functions, customer relationship management, and regulatory compliance capabilities by making them essential for financial institutions seeking comprehensive digital transformation. The average comprehensive digital banking platform supports 15-20 core banking functions, including account management, loan processing, payment services, and compliance reporting, according to banking technology research firm Aite-Novarica's platform functionality analysis. Integration advantages enable financial institutions to streamline operations and reduce system complexity, with banks reporting a 40% reduction in system maintenance costs after implementing unified platform solutions, according to the Federal Reserve's 2023 banking operations survey.

The service segment is likely to witness a CAGR of 15.8% from 2025 to 203, as the complexity of digital banking platform deployment has created substantial demand for specialized implementation and integration services that ensure successful technology adoption and minimal operational disruption. According to the Professional Services Marketing Association, 80% of financial institutions require external implementation services for major digital banking platform deployments, with average implementation projects requiring 12-18 months and involving 15-25 specialists according to consulting firm implementation methodology reports. Integration challenges with legacy banking systems create demand for specialized middleware and data migration services, with 65% of regional banks reporting successful cloud migration only after engaging integration specialists, according to the Financial Services Technology Consortium's migration success analysis.

COUNTRY ANALYSIS

United States

The United States was the top performer of the North American digital banking market with 88.3% of the share in 20254. According to the Federal Reserve's 2023 Banking and Financial Institutions Report, U.S. financial institutions manage over $23 trillion in assets, with digital banking adoption reaching 95% among major banks and 80% among community banks. The concentration of major global financial centers in New York, San Francisco, and Chicago has created demand for cutting-edge digital banking platforms that support complex financial transactions and international operations. Consumer banking sophistication drives extensive digital banking feature adoption, with 85% of American adults utilizing mobile banking services according to the Federal Reserve's 2023 Consumer Payment Study. The Dodd-Frank Act and other regulatory requirements have created demand for digital banking solutions that provide comprehensive audit trails and risk assessment capabilities, with 80% of major banks utilizing regulatory technology (RegTech) solutions integrated into their digital banking platforms, according to the Financial Stability Oversight Council's technology adoption analysis. Innovation-friendly regulatory sandboxes in states like Arizona and Wyoming have encouraged fintech partnerships and digital banking experimentation, with 45 states now operating regulatory programs that support digital banking innovation, according to the Conference of State Bank Supervisors' regulatory innovation survey.

Canada

Canada was positioned second with 12.3% of the North American digital banking market share in 2025. As per the Canadian Bankers Association, 92% of Canadian adults utilize digital banking services, with mobile banking adoption reaching 88% compared to 85% in the United States, according to Statistics Canada's 2023 financial services survey. The universal banking model enables efficient technology deployment across extensive branch networks, with Canadian banks achieving 40% faster digital service rollout times compared to more fragmented banking systems, according to the Canadian Bankers Association's digital transformation analysis. Investment in artificial intelligence and machine learning technologies has positioned Canadian banks at the forefront of digital banking innovation, with 75% of major Canadian banks utilizing AI-powered customer service platforms, according to the Financial Services Innovation Council's technology adoption study.

KEY MARKET PLAYERS

Appway AG, Alkami Technology Inc., Finastra, Fiserv, Inc., Crealogix AG, Temenos, Urban FT Group, Inc., Q2 Software, Inc., Sopra Banking Software, and Tata Consultancy Services are the market players that are dominating the North American digital banking market.

Top Players In The Market

JPMorgan Chase & Co.

JPMorgan Chase & Co. held a dominant position in the North America digital banking market through its comprehensive suite of mobile and online banking services that serve millions of customers across consumer, commercial, and investment banking segments. The company's commitment to technological innovation has resulted in advanced digital platforms, including the Chase Mobile app, which offers sophisticated features such as real-time fraud monitoring, biometric authentication, and personalized financial insights. Their extensive investment in artificial intelligence and machine learning has enabled the development of predictive analytics capabilities that enhance customer experiences and operational efficiency. JPMorgan Chase's focus on cybersecurity and data protection has established industry-leading security standards that protect customer information and maintain trust in digital channels. The company's global technology infrastructure and cloud computing capabilities support scalable digital banking services that can accommodate peak usage periods and rapid customer growth. Their commitment to financial inclusion and accessibility has driven the development of user-friendly interfaces and multilingual support that serve diverse customer populations. JPMorgan Chase's extensive branch network integration with digital channels provides customers with seamless omnichannel experiences that combine the convenience of digital banking with personalized human assistance when needed.

Bank of America Corporation Bank of America Corporation has established itself as a major player in the North American digital banking market through its innovative mobile and online banking platforms that deliver comprehensive financial services to consumers and businesses. The company's Erica virtual assistant represents a pioneering advancement in artificial intelligence-driven banking services, providing customers with personalized financial guidance and automated support through conversational interfaces. Their commitment to user experience design has resulted in intuitive mobile applications and web platforms that simplify complex banking activities and enable self-service capabilities for routine transactions. Their extensive research and development capabilities have enabled the creation of advanced security features, including biometric authentication, behavioral analytics, and fraud detection systems. Bank of America's commitment to accessibility and inclusive design has resulted in digital banking solutions that accommodate users with disabilities and diverse technological capabilities. The company's strategic acquisitions of fintech companies and digital banking specialists have accelerated innovation and expanded its technological capabilities.

Wells Fargo & Company

Wells Fargo & Company has emerged as a key player in the North American digital banking market through its comprehensive digital transformation initiatives and customer-centric technology solutions that serve diverse banking needs across consumer, commercial, and corporate segments. The company's Wells Fargo Mobile app provides customers with advanced features, including mobile check deposit, person-to-person payments, and integrated financial management tools that enhance convenience and accessibility. Their commitment to cybersecurity and fraud prevention has resulted in sophisticated authentication systems and real-time monitoring capabilities that protect customer accounts and maintain trust in digital channels. Wells Fargo's focus on small business banking has driven the development of specialized digital platforms that address the unique needs of entrepreneurial customers and commercial clients. Their extensive branch network integration with digital channels provides customers with seamless omnichannel banking experiences that combine digital convenience with personalized human assistance. Wells Fargo's commitment to financial education and community development has integrated educational resources and financial planning tools within its digital platforms. Their focus on regulatory compliance and risk management has ensured successful navigation of complex regulatory environments while maintaining competitive service delivery standards.

Top Strategies Used By Key Market Participants

Artificial Intelligence and Machine Learning

Integration Leading players in the North American digital banking market are heavily investing in artificial intelligence and machine learning technologies to enhance customer experiences, improve operational efficiency, and enable predictive analytics capabilities. Companies are developing sophisticated virtual assistants and chatbots that provide instant customer support, personalized financial recommendations, and automated transaction processing without human intervention. This strategy involves creating advanced algorithms that can analyze customer behavior patterns, predict financial needs, and deliver proactive service recommendations based on individual preferences and historical data. Market participants are also leveraging machine learning for fraud detection, risk assessment, and credit decision-making processes that can process vast amounts of data in real-time while maintaining accuracy and compliance standards. The focus on natural language processing and conversational interfaces has enabled more intuitive customer interactions and reduced reliance on traditional menu-based navigation systems. Investment in predictive analytics capabilities has allowed financial institutions to anticipate customer needs, identify potential issues before they occur, and optimize resource allocation for maximum efficiency.

Ecosystem Development and Strategic Partnerships

Key market participants are increasingly focusing on ecosystem development and strategic partnerships to expand their service offerings, accelerate innovation, and capture value across the broader financial services landscape. Companies are forming alliances with fintech startups, technology providers, and non-financial organizations to integrate banking services into everyday consumer activities and business processes. This approach involves creating comprehensive API ecosystems that enable third-party developers to build innovative applications and services that extend the reach and functionality of traditional banking platforms. Market leaders are also partnering with e-commerce platforms, social media companies, and lifestyle applications to deliver embedded finance solutions that provide seamless financial experiences within existing customer journeys. The emphasis on open banking initiatives has facilitated data sharing and service integration while maintaining security and regulatory compliance standards. Strategic acquisitions of specialized technology companies and digital banking innovators have enabled rapid capability expansion and market penetration.

Cybersecurity Enhancement and Trust Building

Market participants are prioritizing cybersecurity enhancement and trust-building initiatives to address consumer concerns about data security and privacy while maintaining competitive service delivery capabilities. Companies are investing heavily in advanced security technologies, including biometric authentication, behavioral analytics, encryption systems, and real-time fraud monitoring, to protect customer information and prevent unauthorized access. This strategy involves implementing multi-layered security architectures that provide comprehensive protection across all digital touchpoints while maintaining user convenience and accessibility. Market leaders are also focusing on transparency and communication about security measures to build customer confidence and differentiate their services from competitors. The emphasis on regulatory compliance and industry best practices has driven the adoption of standardized security frameworks and third-party security certifications that demonstrate commitment to data protection. Investment in customer education and awareness programs has helped consumers understand security features and best practices for protecting their financial information.

COMPETITION OVERVIEW

The North American digital banking market exhibits highly competitive dynamics characterized by the presence of traditional banking giants, specialized fintech companies, and emerging technology innovators. Market competition is intensifying as financial institutions recognize the strategic importance of digital capabilities for customer retention, operational efficiency, and competitive differentiation. Large traditional banks leverage their existing customer bases, regulatory expertise, and financial resources to offer comprehensive digital banking solutions that compete directly with fintech disruptors. Specialized fintech companies compete through technological innovation, user experience design, and focused functionality that addresses specific customer pain points and market opportunities. The competitive landscape is further complicated by the entry of technology companies, telecommunications providers, and non-financial organizations seeking to capitalize on the convergence of banking with everyday consumer activities. Organizations are differentiating themselves through technological advancement, customer service quality, and product innovation rather than competing solely on pricing or traditional banking metrics. The market is experiencing consolidation through strategic acquisitions as larger players seek to expand their technological capabilities and market reach. Partnerships between traditional banks and fintech companies have become common strategies for combining institutional security and regulatory compliance with startup agility and customer-centric design approaches.

RECENT HAPPENINGS IN THE MARKET

- In February 2025, JPMorgan Chase & Co. launched Finn AI, an advanced banking chatbot powered by generative artificial intelligence, to provide customers with sophisticated financial guidance and automated support across mobile and web platforms.

- In June 2025, Bank of America Corporation announced the acquisition of SoFi Technologies' banking division, expanding its digital lending capabilities and enhancing its mobile banking platform with advanced personal finance management features.

- In March 2025, Wells Fargo & Company partnered with Microsoft Corporation to migrate its core banking systems to Azure cloud infrastructure, enabling enhanced scalability and improved digital service delivery capabilities.

- In October 2023, JPMorgan Chase & Co. introduced their new digital wallet solution, Chase Pay+, featuring advanced security protocols and integration with major e-commerce platforms for seamless online and in-store payment experiences.

- In August 2023, Bank of America Corporation launched the Erica Business Assistant, an AI-powered virtual assistant specifically designed for small business customers to provide financial insights, cash flow management, and automated bookkeeping support.

MARKET SEGMENTATION

This research report on the North American digital banking market is segmented and sub-segmented into the following categories.

By Deployment

- On-Premise

- Cloud

By Mode

- Online Banking

- Mobile Banking

By Component

- Platforms

- Services

By Service

- Professional Service

- Managed Service

By Type

- Retail Banking

- Corporate Banking

- Investment Banking

By Country

- The United States

- Canada

- Mexico Rest of North America

Frequently Asked Questions

What is digital banking?

Digital banking refers to financial services delivered through online platforms and mobile apps, allowing users to manage accounts, transfer money, apply for loans, and access customer support remotely. It eliminates the need for in-person visits to physical bank branches.

Why is digital banking growing so fast in North America?

More consumers prefer the speed, convenience, and 24/7 access offered by digital platforms, especially after increased comfort with online transactions during recent years. Banks and fintechs are also investing heavily to meet rising demand for seamless digital experiences.

Who uses digital banking the most?

Millennials and Gen Z lead in adoption, but usage is growing rapidly among older adults who now rely on digital tools for everyday banking. Small business owners also use digital platforms for faster loan approvals and cash flow management.

Are traditional banks keeping up with digital trends?

Yes, most major banks have launched robust mobile apps, upgraded back-end systems, and partnered with fintech firms to stay competitive. Many now offer features like instant payments, AI-driven budgeting tools, and video-based customer service.

What are neobanks and how are they changing the market?

Neobanks are digital-only banks with no physical branches, offering simple, low-fee accounts and intuitive interfaces designed for smartphone users. They’re gaining popularity by focusing on user experience and transparency, pushing traditional banks to innovate.

How is AI being used in digital banking?

Banks use AI to power chatbots, detect fraud in real time, personalize financial advice, and automate loan underwriting. These tools improve efficiency and help deliver faster, smarter services tailored to individual users.

Is digital banking secure?

Most platforms use advanced encryption, multi-factor authentication, and biometric login options like fingerprint and facial recognition to protect user data. While risks exist, financial institutions continuously strengthen security to combat evolving cyber threats.

What is open banking and why does it matter?

Open banking allows third-party apps to securely access a user’s financial data (with consent) to offer services like budgeting, credit scoring, or payment automation. It’s increasing competition and giving consumers more control over their finances.

How do digital banks handle customer support?

Many offer instant support through AI chatbots, in-app messaging, or video calls with representatives. Some also provide hybrid models, combining digital tools with access to human advisors when needed.

What’s next for digital banking in North America?

Expect deeper personalization, wider use of voice-activated banking, integration with smart devices, and more embedded financial services in non-banking apps. The focus will remain on speed, security, and creating a frictionless user journey.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com