North America HVAC Compressor Market Size, Share, Trends & Growth Forecast Report By Type (Reciprocating, Rotary, Scroll, Screw, Centrifugal), By Application (Residential, Commercial, Industrial), By Refrigerant Type (R-410A, R-407C, R-134A, R-22, Others), By End-User (Air Conditioning, Refrigeration, Heat Pumps), and By Country (The U.S., Canada, Rest of North America) – Industry Analysis, 2026 to 2034

North America HVAC Compressor Market Size

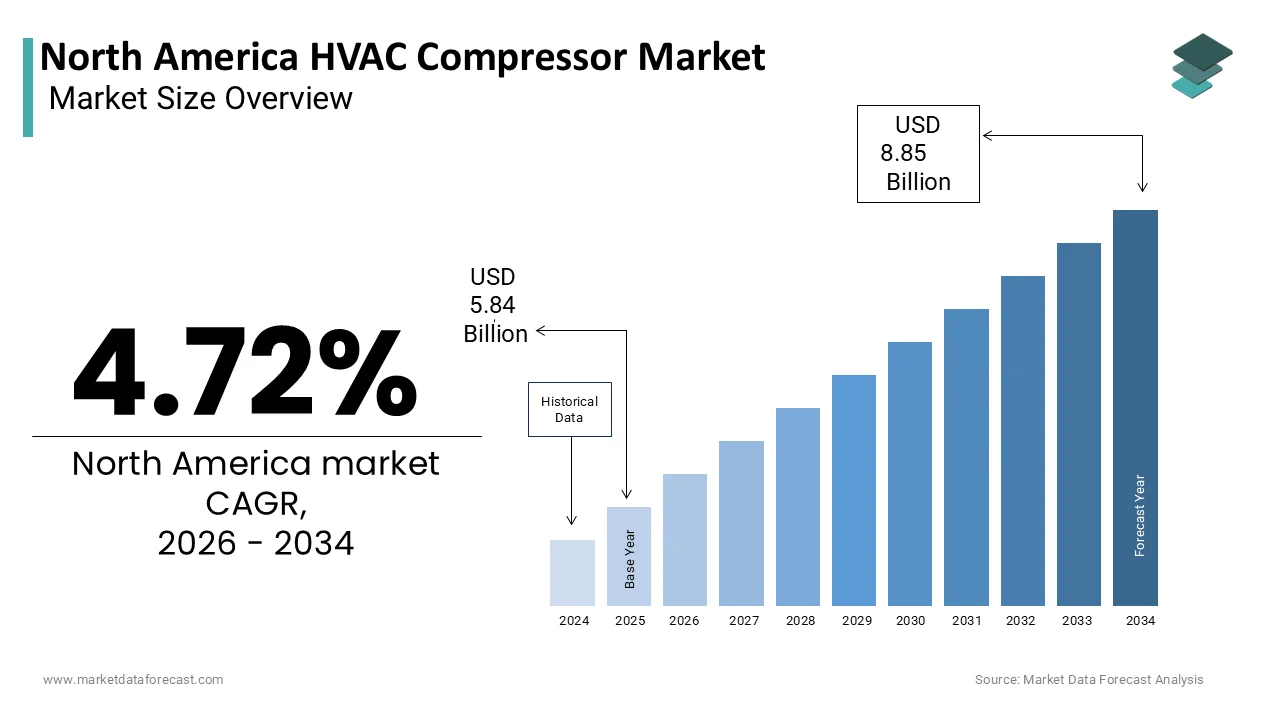

The North America HVAC compressor market was valued at USD 5.84 billion in 2025, is estimated to reach USD 6.12 billion in 2026, and is projected to reach USD 8.85 billion by 2034, growing at a CAGR of 4.72% from 2026 to 2034.

The HVAC compressor is the production, distribution, and integration of compression technologies essential for heating, ventilation, air conditioning, and refrigeration systems across residential, commercial, and industrial infrastructures. The expansion of smart buildings and the integration of Internet of Things (IoT)-enabled HVAC controls have further refined compressor performance requirements. As per the U.S. Census Bureau, over 1.4 million residential units were authorized in 2025, indicating sustained construction momentum that directly fuels HVAC equipment demand. Moreover, the U.S. Department of Labor reports that employment in HVAC installation and maintenance occupations is projected to grow 6% from 2022 to 2032, which is outpacing the national average, reflecting systemic reliance on climate control infrastructure.

MARKET DRIVERS

Rising Residential Construction and Urbanization Trends

The surge in residential construction across North America is propelling the growth of the North America HVAC compressor market. According to the U.S. Census Bureau, 1.44 million housing units were authorized in 2025 with a sustained upward trajectory from previous years. According to the National Association of Home Builders, over 90% of newly constructed homes in the U.S. are equipped with central air conditioning. According to the Environmental Protection Agency, the cooling degree days in major metropolitan areas such as Phoenix and Atlanta have risen by 12% and 9%, respectively,y over the past decade. Furthermore, urban densification is driving the development of high-rise residential complexes that rely on centralized chiller systems, which utilize large-scale screw and centrifugal compressors. These systems require higher-capacity and more energy-efficient compression technologies, encouraging manufacturers to innovate. The integration of smart thermostats and zoned HVAC systems in modern homes also increases the number of compressors per dwelling.

Stringent Energy Efficiency Regulations and Environmental Standards

The regulatory frameworks aimed at reducing energy consumption and greenhouse gas emissionareis ascribed to fuel the growth of the North American HVAC compressor market. As per the DOE, these standards are expected to save consumers nearly $2.5 billion annually in energy costs by 2035. This regulatory shift necessitates the adoption of advanced compressor technologies such as variable-speed scroll and inverter-driven compressors, which offer superior modulation and energy savings compared to traditional fixed-speed units. As per the Air-Conditioning, Heating, and Refrigeration Institute (AHRI), shipments of variable-capacity HVAC systems increased by 27% between 2020 and 2025. Additionally, the Kigali Amendment to the Montreal Protocol, ratified by the U.S. in 2022, mandates an 85% reduction in hydrofluorocarbon (HFC) consumption by 2036. This has prompted a transition toward low-global-warming-potential (GWP) refrigerants such as R-32 and R-454B, which require compressors engineered for different thermodynamic properties. Manufacturers like Emerson and Danfoss have responded by launching compressors specifically designed for these next-generation refrigerants.

MARKET RESTRAINTS

High Initial Costs of Advanced Compressor Technologies

The adoption of next-generation HVAC compressors, such as variable-speed and inverter-driven models, is significantly hindering the growth of the North American HVAC compressor market. According to the U.S. Energy Information Administration, the average installed cost of a high-efficiency residential HVAC system equipped with a variable-speed compressor exceeds $10,000, nearly 40% higher than conventional fixed-speed systems. According to the National Renewable Energy Laboratory, low-to-moderate income housing sectors, which constitute over 45% of the U.S. rental market as per the Joint Center for Housing Studies at Harvard University, financial constraints severely limit investment in premium HVAC equipment. Additionally, skilled labor shortages in HVAC installation, with the Bureau of Labor Statistics projecting a 6% workforce growth despite high demand, lead to increased labor costs and delays, compounding the financial burden.

Supply Chain Disruptions and Material Dependencies

The vulnerability due to its reliance on globally sourced materials and components, particularly rare earth elements, copper, and specialized steel, all of which is also hampering the growth of the North American HVAC compressor market. China controls over 85% of the global rare earth refining capacity, as stated by the U.S. Geological Survey, which is essential for manufacturing high-efficiency permanent magnet motors used in inverter-driven compressors. Additionally, copper, a fundamental material in compressor windings and heat exchangers, experienced price peaks exceeding $4.50 per pound in 2022, as recorded by the Commodity Futures Trading Commission, driven by global demand and mining constraints. The HVAC industry consumes over 300,000 metric tons of copper annually in North America alone, per the Copper Development Association. Disruptions in logistics networks, such as the 2021 Suez Canal blockage and West Coast port congestion in 2022, further exacerbated delivery timelines, with some manufacturers reporting lead times extending beyond 20 weeks. These supply chain instabilities force OEMs to maintain higher inventory levels, increasing operational costs.

MARKET OPPORTUNITIES

Integration of HVAC Compressors in Renewable Energy and Grid-Interactive Buildings

The integration of HVAC systems with renewable energy infrastructure presents a transformative opportunity for compressor manufacturers,s urging the growth of the North American HVAC compressor market. Advanced compressors equipped with inverter technology and smart controls are uniquely positioned to modulate operation based on real-time energy availability, reducing grid strain and optimizing self-consumption of solar power. According to the Department of Energy, grid-interactive efficient buildings (GEBs), which dynamically adjust HVAC loads in response to grid signals, could reduce peak electricity demand by up to 15% by 2030. Utilities such as Austin Energy and Con Edison are offering incentives for HVAC systems that participate in demand response programs, with over 120,000 smart thermostats enrolled in such initiatives as of 2025, according to the Smart Electric Power Alliance.

Expansion of Data Centers and Cooling Infrastructure

The exponential growth of digital infrastructure, such as hyperscale data centers, is creating robust growth opportunities for the North American HVAC compressor market. According to Synergy Research Group, the U.S. accounted for 40% of the world’s data center capacity in 2025, with over 500 large facilities in operation. These installations rely heavily on precision cooling systems that utilize centrifugal and screw compressors for continuous, reliable operation. Furthermore, the push for sustainability is driving the adoption of chiller plants with integrated heat recovery and low-GWP refrigerants, aligning with corporate net-zero commitments by firms like Microsoft and Google.

MARKET CHALLENGES

Rapid Technological Obsolescence and R&D Investment Pressures

The rapidly changing technologies and R&D investment pressure are likely to limit the growth of the North American HVAC compressor market. The shift toward variable-speed drives, low-GWP refrigerants, and smart controls has shortened product life cycles, compelling companies to invest heavily in research and development to remain competitive. According to the Air-Conditioning, Heating, and Refrigeration Institute, leading OEMs now allocate between 5% and 7% of annual revenue to R&D, a figure that has increased by nearly 40% over the past five years. As per the U.S. Environmental Protection Agency, over 60% of residential HVAC units installed before 2020 will require replacement or retrofit by 2030 due to regulatory non-compliance. This rapid turnover creates inventory and service challenges for distributors and contractors. Additionally, the integration of digital twins, predictive analytics, and IoT-enabled monitoring requires compressors to be not only mechanically advanced but also digitally connected, demanding new expertise in software engineering and cybersecurity. The National Institute of Standards and Technology warns that unsecured HVAC control systems can serve as entry points for cyberattacks on building networks. Furthermore, small and mid-sized manufacturers often lack the capital to sustain such innovation cycles, leading to market consolidation.

Workforce Skill Gaps in HVAC System Design and Commissioning

The shortage of skilled technicians capable of designing, installing, and commissioning next-generation systems is also slowing the growth of the North American HVAC compressor market. Modern compressors are integrated with inverter drives, smart controls, and low-GWP refrigerants, and require specialized knowledge in electrical systems, refrigerant handling, and digital diagnostics. As per the U.S. Bureau of Labor Statistics, while employment in HVACR occupations is projected to grow 6% from 2022 to 2032, there is a significant mismatch between workforce skills and technological demands. The Air-Conditioning, Heating, and Refrigeration Institute estimates that only 38% of currently practicing HVAC technicians are certified to handle A2L refrigerants such as R-454B, which are becoming standard under new DOE regulations. This certification gap delays system installations and increases the risk of improper commissioning, leading to reduced efficiency and warranty claims. Moreover, the average age of an HVAC technician in the U.S. exceeds 45 years, according to the PHCC Educational Foundation, indicating an aging workforce with limited exposure to digital HVAC platforms. Apprenticeship completion rates remain below 50%, as reported by the Department of Labor, due to inconsistent training quality and lack of standardized curricula across states. This skills deficit is particularly acute in rural and underserved urban areas, where access to technical education is limited. The consequence is a bottleneck in system deployment, with some contractors reporting project delays of up to 12 weeks due to technician availability.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Application, Refrigerant Type, End-User, and Country |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | The U.S., Canada, and the Rest of North America |

| Market Leaders Profiled | Ryder System, Inc., FedEx Corp, DHL International GmbH, NFI Industries, Inc., and others |

SEGMENTAL ANALYSIS

By Type Insights

The scroll compressors segment accounted in holding 42.3% of the North American HVAC compressor market share in 2025. The proliferation of high-efficiency air conditioning systems in single-family homes has cemented scroll compressors as the preferred choice. Their designs feature orbiting and fixed spiral elements that eliminate clearance volume, enabling near-continuous compression with minimal vibration and noise. According to the U.S. Energy Information Administration, over 94% of new homes constructed in 2025 included central air conditioning, with more than 75% of these systems utilizing scroll compressors due to their compatibility with variable-capacity and inverter-driven platforms. Manufacturers such as Copeland and Emerson have reported that over 80% of their residential HVAC compressor shipments in 2025 were scroll-based, reflecting deep market entrenchment.

The rise of ductless mini-split and multi-split systems in retrofit and urban residential applications has amplified demand. The U.S. Department of Energy notes that ductless system installations grew by 18% annually between 2020 and 2025, driven by their zoning capabilities and energy savings. These systems almost exclusively use scroll compressors due to their compact footprint and ability to operate efficiently at partial loads.

The centrifugal compressor segment is likely to grow with an expected CAGR of 7.8% from 2025 to 2033. The explosive expansion of data centers and facilities is driving unprecedented demand for high-capacity, energy-efficient cooling systems. Centrifugal compressors, capable of delivering cooling capacities exceeding 1,000 tons, are the backbone of chilled water plants in hyperscale data centers. As per Cisco’s Annual Internet Report, global data traffic is expected to reach 4.8 zettabytes annually by 2026, necessitating continuous cooling for server racks that generate immense heat. According to the U.S. Department of Energy, these advanced chillers can reduce cooling energy consumption by up to 40% compared to older screw compressor systems. Google and Microsoft have publicly committed to using only high-efficiency centrifugal chillers in new data center builds, with over 60 such installations completed across Virginia, Iowa, and Ontario between 2021 and 2025, as documented by the Uptime Institute.

By Application Insights

The residential application segment wccounted in holding 58.3% of the North American HVAC compressor market share in 2025. The sustained pace of single-family home construction in sensitive regions ensures consistent demand for HVAC compressors. The U.S. Census Bureau reports that 1.44 million housing units were authorized in 2025, with over 80% being single-family homes. In southern states like Texas, Florida, and Arizona, where cooling degree days have increased by 10–15% over the past decade, as documented by the National Oceanic and Atmospheric Administration, central air conditioning is not a luxury but a necessity. The National Association of Home Builders indicates that 96% of newly built homes in the South include central AC, most of which rely on scroll or rotary compressors.

The commercial application segment is expected to grow with an expected CAGR of 6.9% throughout the forecast period. The modernization of office, retail, and healthcare facilities is accelerating the replacement of aging HVAC infrastructure with smart, energy-efficient systems. According to the U.S. General Services Administration, the average commercial building in the U.S. is 43 years old, with many still operating on outdated reciprocating or screw compressors that fail to meet current efficiency standards. The 2025 DOE regulations requiring higher SEER2 and heating seasonal performance factor (HSPF2) values have triggered widespread retrofits, particularly in buildings over 50,000 square feet. The Urban Land Institute reports that over 1,200 commercial properties in major cities underwent HVAC system upgrades in 2025 alone, with a preference for variable-refrigerant-flow (VRF) systems using scroll and inverter-driven compressors.

By Refrigerant Insights

The R-410A refrigerant segment accounted in holding 52.3% of the North American HVAC compressor market share in 202,5 with the vast installed base of HVAC systems designed for R-410A continuing to drive service and replacement demand. The U.S. Department of Energy estimates that over 120 million residential and commercial air conditioning units installed between 2005 and 2022 operate on R-410A, which became the standard refrigerant after the phaseout of R-22. These systems, with an average lifespan of 15–20 years, are still within their operational window, creating a steady need for compressor replacements and refrigerant recharges. The Environmental Protection Agency notes that R-410A accounted for 60% of all refrigerant sales in 2025, primarily for servicing existing equipment.

The “Others” refrigerant category is likely to grow with an expected CAGR of 9.2% during the forecast period, with the implementation of the AIM Act (American Innovation and Manufacturing Act) mandating an 85% reduction in HFC production and consumption by 2036. As per the EPA, hydrofluorocarbons like R-410A have a global warming potential (GWP) of 2,088, whereas R-32 has a GWP of 675 and R-454B a GWP of 466, making them compliant with the phasedown schedule. The EPA’s Significant New Alternatives Policy (SNAP) has approved R-32 and R-454B for residential and commercial use, prompting manufacturers like Daikin and Carrier to launch new product lines. Daikin reports that its R-32-based mini-split systems achieved a 35% sales increase in North America in 2025, reflecting growing market acceptance.

By End-User Insights

The air conditioning segment accounteforng a prominent share of the North American HVAC compressor market in 2025. The rising ambient temperatures and increased cooling degree days are expanding the geographic and seasonal demand for mechanical cooling. NOAA reports that 2025 was the warmest year on record for the contiguous U.S., with cooling degree days 12% above the 30-year average. Cities like Phoenix and Las Vegas experienced over 150 days above 100°F, driving consumer reliance on air conditioning for health and comfort. The EIA notes that space cooling accounts for nearly 17% of residential electricity consumption, the highest among end uses, reinforcing the centrality of AC systems.

The heat pump segment is expected to witness a CAGR of 11.3% from 2025 to 2033. The federal and state-level electrification initiatives are incentivizing the replacement of fossil-fuel heating systems with high-efficiency heat pumps. The Inflation Reduction Act provides tax credits of up to $8,000 for heat pump installations, with additional rebates under the HOMES program. As per the White House Council on Environmental Quality, over 400,000 heat pump rebates were claimed in 2025, a 150% increase from 2022. States like New York and California have set targets to install 6 million and 5 million heat pumps, respectively, by 2030.

COUNTRY-LEVEL ANALYSIS

United States HVAC Compressor Market Insights

The United States was the top performer in the North American HVAC compressor market by capturing 78.3% of the share in 2025, with its vast residential and commercial infrastructure, coupled with aggressive energy efficiency policies. The Department of Energy’s 2025 efficiency standards have triggered a wave of equipment upgrades, particularly in the Sun Belt, where cooling demand is highest. Additionally, federal incentives under the Inflation Reduction Act are accelerating the adoption of heat pumps and high-efficiency compressors. The National Association of Home Builders notes that 1.44 million housing units were authorized in 2025 by ensuring sustained demand.

Canada HVAC Compressor Market Insights

Canada was ranked second with 14.3% of the North American HVAC compressor market share in 2025. While its colder climate traditionally emphasized heating, rising summer temperatures and urbanization are increasing cooling demand. Environment and Climate Change Canada reports that cooling degree days in Toronto and Vancouver have risen by 18% and 22%, respectively, since 2010. The federal government’s Greener Homes Grant has supported over 200,000 heat pump installations since 2021, as documented by Natural Resources Canada. Additionally, building codes in provinces like British Columbia and Quebec now mandate higher energy performance, favoring advanced compressor technologies. The shift toward net-zero buildings is further driving demand for variable-capacity systems, positioning Canada as a growing market for next-generation compressors.

KEY MARKET PLAYERS

Companies playing a prominent role in the North America HVAC compressor market are Ryder System, Inc., FedEx Corp, DHL International GmbH, NFI Industries, Inc., and others.

TOP LEADING PLAYERS IN THE MARKET

Emerson

Emerson has established itself as a pivotal innovator in the North American HVAC compressor landscape by leveraging its expertise in climate technologies and automation. The company’s Copeland brand is synonymous with reliability and efficiency, offering a broad portfolio of compressors for residential, commercial, and industrial applications. Emerson focuses on sustainable innovation, integrating digital diagnostics, variable-speed technology, and low-global-warming-potential refrigerants into its product lines. Its strong distribution network and collaborative approach with OEMs enable seamless integration of compressors into next-generation HVAC systems.

Danfoss

Danfoss is a leading force in advancing energy-efficient compression technologies, with a strong footprint in North America’s HVAC sector. The company emphasizes sustainability through its range of scroll, reciprocating, and variable-speed compressors designed for optimal performance with eco-friendly refrigerants. Danfoss actively collaborates with policymakers, industry groups, and manufacturers to drive regulatory compliance and technological advancement. Its commitment to decarbonization is reflected in its R&D focus on electrification, heat pump integration, and digital controls.

Carrier Global Corporation

Carrier Global Corporation stands as an industry pioneer, integrating compressor technology within its end-to-end HVAC systems and chillers. The company’s in-house development of advanced compression solutions supports its broader ecosystem of smart, connected buildings and energy-efficient infrastructure. Carrier emphasizes system-level optimization, where compressors are engineered to work cohesively with controls, heat exchangers, and refrigerants for maximum efficiency. Its influence extends beyond North America through global projects in urban cooling, data center thermal management, and sustainable aviation infrastructure.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

One major strategy employed by leading players is vertical integration of compressor design within broader HVAC system architectures. Companies are increasingly engineering compressors not as standalone components but as integral elements of smart, connected systems. This approach allows for tighter control over performance, energy efficiency, and interoperability with building management platforms.

Another prevalent strategy is strategic collaboration with regulatory bodies and industry consortia to influence standards development. Market leaders actively participate in shaping energy efficiency regulations, refrigerant transition pathways, and safety codes. This proactive engagement ensures their technologies are aligned with future compliance requirements by giving them a first-mover advantage in adopting next-generation refrigerants and digital controls.

A third key strategy involves investment in digitalization and predictive maintenance ecosystems. Companies are embedding sensors and IoT-enabled diagnostics into compressors to enable real-time monitoring, fault detection, and remote optimization. These digital services not only extend equipment lifespan but also create recurring revenue streams through subscription-based monitoring and analytics, transforming the traditional hardware-centric business model into a service-integrated offering.

COMPETITION OVERVIEW

The competitive landscape of the North America HVAC compressor market is defined by technological differentiation, strategic alliances, and a race toward sustainability. While a few dominant players control significant market influence, the pressure to innovate has intensified due to evolving regulatory standards and shifting consumer expectations. Companies are no longer competing solely on compressor efficiency or durability but on holistic value propositions that include digital integration, environmental impact, and lifecycle support. The transition to low-GWP refrigerants and the rise of smart buildings have blurred the lines between component manufacturing and system intelligence, compelling firms to expand beyond hardware into software and services. Smaller niche players are gaining traction by specializing in emerging applications such as cold-climate heat pumps and modular data center cooling, challenging established OEMs. At the same time, consolidation is evident as larger corporations acquire innovative startups to accelerate R&D in areas like magnetic bearing compressors and AI-driven load optimization.

RECENT MARKET DEVELOPMENTS

- In March 2025, Emerson launched a new line of A2L-compliant scroll compressors under its Copeland brand, designed specifically for next-generation low-GWP refrigerants by enhancing its dominance in sustainable HVAC solutions.

- In June 2025, Danfoss expanded its compressor manufacturing facility in Tallahassee, Florida, to increase production capacity for variable-speed models and strengthen regional supply chain resilience.

- In September 2025, Carrier Global Corporation introduced a fully integrated heat pump system featuring an in-house developed twin-rotary compressor optimized for cold-climate performance by targeting the growing electrification market.

- In January 2025, Daikin Applied acquired a minority stake in a Canadian startup specializing in AI-driven chiller optimization, integrating advanced analytics into its centrifugal compressor controls.

- In May 2025, Johnson Controls partnered with a leading semiconductor firm to develop IoT-enabled compressor monitoring modules, whichares advancing its digital service capabilities for commercial HVAC systems.

MARKET SEGMENTATION

This research on the North America HVAC compressor market has been segmented and sub-segmented into the following.

By Type

- Reciprocating

- Rotary

- Scroll

- Screw

- Centrifugal

By Application

- Residential

- Commercial

- Industrial

By Refrigerant Type

- R-410A

- R-407C

- R-134A

- R-22

- Others

By End-User

- Air Conditioning

- Refrigeration

- Heat Pumps

By Country

- The U.S.

- Canada

- Rest of North America

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com