North America Legal Process Outsourcing Market Size, Share, Trends & Growth Forecast Report By Location, End-user Enterprise Size, Delivery Model, Technology Adoption and Country (United States, Canada, Mexico, Rest of North America) – Industry Analysis, 2026 to 2034

Market Size, 2025

$10.19 BnMarket Estimate, 2026

$12.51 BnMarket Forecast, 2034

$64.61 BnCAGR, 2026–2034

22.78%North America Legal Process Outsourcing (LPO) Market Size

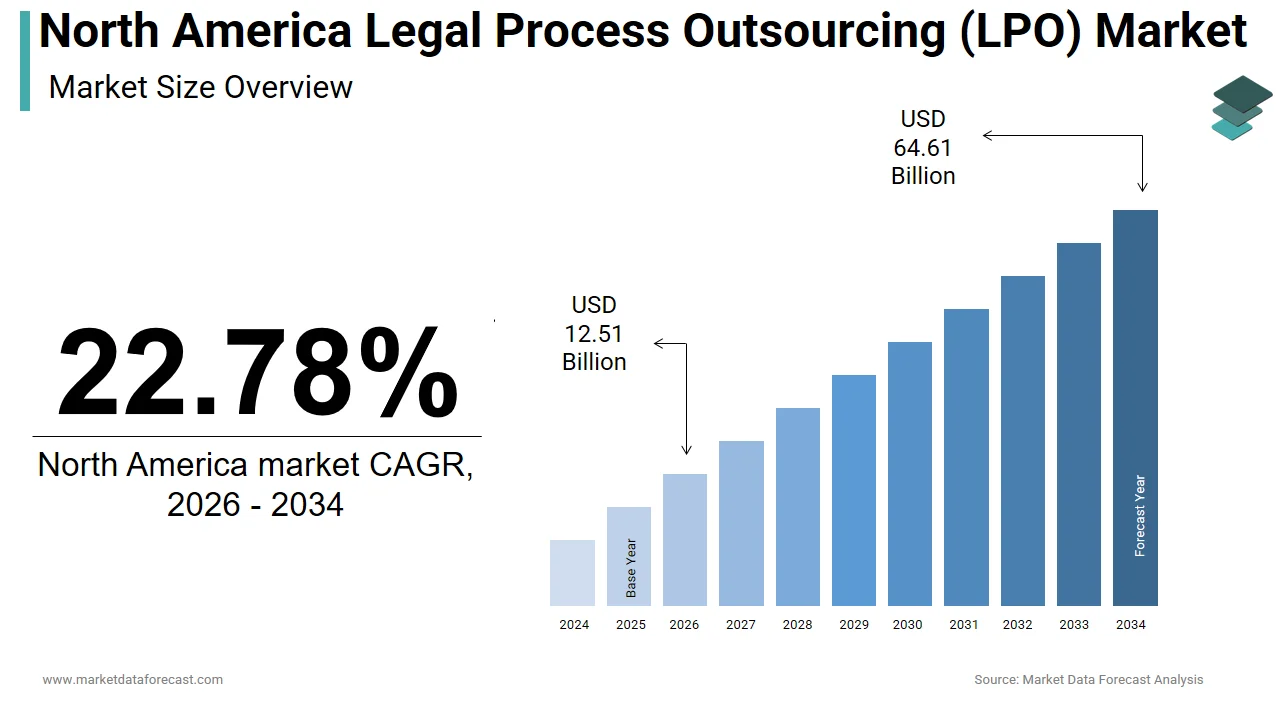

The North America legal process outsourcing market was valued at USD 10.19 billion in 2025, is estimated to reach USD 12.51 billion in 2026, and is projected to reach USD 64.61 billion by 2034, growing at a CAGR of 22.78% from 2026 to 2034.

The legal process outsourcing (LPO) is the delegation of legal support services such as contract management, legal research, compliance monitoring, e-discovery, and document review by law firms, corporate legal departments, and regulatory entities to external service providers, often leveraging cost-efficient, technology-integrated solutions. As of 2023, over 68% of Am Law 100 firms engage with LPO providers for at least one core legal function, according to Thomson Reuters’ Legal Executive Institute. Additionally, the integration of artificial intelligence in legal workflows has enabled LPO vendors to deliver faster and more accurate services, particularly in litigation support and due diligence.

MARKET DRIVERS

Escalating Complexity of Regulatory Compliance in Corporate Legal Functions

The growing intricacy of federal and state-level regulatory frameworks is driving the growth of the North America legal process outsourcing (LPO) market. This regulatory burden necessitates continuous monitoring, reporting, and documentation, which internal legal teams often lack the bandwidth to manage efficiently. A 2023 survey by the Association of Corporate Counsel revealed that 74% of in-house legal departments in the U.S. are outsourcing compliance-related tasks to specialized LPO providers. These providers offer scalable solutions for regulatory tracking, audit preparation, and policy documentation by enabling corporations to mitigate legal risks. Furthermore, financial institutions subject to the Bank Secrecy Act and anti-money laundering (AML) regulations increasingly rely on LPO firms for transaction monitoring and suspicious activity reporting. According to the U.S. Department of the Treasury’s Financial Crimes Enforcement Network, over 2.3 million suspicious activity reports were filed in 2022, requiring extensive legal review.

Rising Volume of Litigation and E-Discovery Demands

The exponential growth in digital data and the consequent surge in litigation cases involving electronic evidence have intensified the need for specialized e-discovery and litigation support services, which is prompting the growth of the North America LPO market. U.S. federal courts received over 333,000 civil case filings in 2022, as reported by the Administrative Office of the U.S. Courts, many of which involved substantial electronic data. The average e-discovery process for a mid-sized litigation case now involves over 1.8 million documents, according to a 2023 analysis by the RAND Institute for Civil Justice. Managing this volume internally is prohibitively expensive and resource-intensive, prompting law firms and corporations to outsource document review, data processing, and privilege logging. LPO providers equipped with AI-powered review platforms can reduce review time by up to 50%, as noted in a 2022 study by the International Legal Technology Association. Additionally, the rise in class-action lawsuits, particularly in sectors like pharmaceuticals and consumer technology, has further strained internal legal resources. For instance, over 4,000 multidistrict litigation (MDL) cases were active in 2023, each requiring coordinated document management across jurisdictions. LPO firms offer not only cost efficiency but also expertise in handling complex litigation workflows, enabling faster case resolution.

MARKET RESTRAINTS

Data Privacy and Confidentiality Concerns in Cross-Border Legal Outsourcing

The persistent concerns over data privacy and client confidentiality are hampering the growth of the North America legal process outsourcing (LPO) market. The American Bar Association’s Model Rules of Professional Conduct, specifically Rule 1.6, mandate that attorneys preserve the confidentiality of client information, creating ethical and legal risks when data is transferred outside North America. In 2022, the ABA issued formal guidance cautioning law firms against using offshore providers without stringent data protection safeguards. The risk is further compounded by the lack of harmonization between U.S. privacy laws and those of common LPO destinations such as India and the Philippines. For instance, the U.S. does not have a comprehensive federal privacy law akin to the EU’s GDPR, yet state laws like the CCPA impose strict data handling obligations. In 2023, the Federal Trade Commission recorded 1,877 data breaches involving sensitive personal information, many linked to third-party service providers. Moreover, the U.S. Cloud Act allows federal authorities to access data stored abroad, creating jurisdictional conflicts that may compromise client confidentiality.

Resistance from Traditional Legal Institutions and Professional Ethics Constraints

The deeply entrenched culture within North American legal institutions, particularly large law firms, continues to resist the widespread adoption of legal process outsourcing due to perceived threats to professional autonomy and ethical standards. The American Bar Association’s Model Rule 5.4 prohibits non-lawyer ownership of law firms, which indirectly restricts the integration of third-party legal service providers into core legal decision-making processes. As per a 2023 study by the Georgetown Law Center for the Study of the Legal Profession, 42% of partners in U.S. law firms believe that outsourcing undermines the quality of legal work and client relationships. This skepticism is particularly pronounced in high-stakes litigation and transactional work, where judgment and strategy are considered inseparable from attorney involvement. Additionally, bar associations in states like New York and California have issued opinions cautioning against the delegation of legal analysis to non-attorney personnel, even within outsourced teams. A 2022 survey by the National Association for Law Placement revealed that only 28% of law firms allow paralegals or offshore teams to conduct independent legal research without attorney supervision. This regulatory and cultural resistance limits the scope of tasks that can be outsourced, confining LPO primarily to administrative and document-intensive functions. Furthermore, the billable hour model, still dominant in 67% of U.S. law firms as per the Legal Executive Institute, disincentivizes efficiency-driven outsourcing that reduces time spent on tasks.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence and Legal Technology in LPO Services

The rapid advancement of artificial intelligence and legal technology is prompting new opportunities for the growth of the North America legal process outsourcing market. Natural language processing (NLP) and machine learning algorithms are now being deployed to automate contract analysis, legal research, and compliance monitoring with increasing accuracy. According to a 2023 report by the Stanford Institute for Human-Centered Artificial Intelligence, AI-powered legal tools can analyze contracts 80% faster than human reviewers while maintaining over 95% accuracy in identifying critical clauses. LPO firms that integrate such technologies can offer scalable, real-time solutions for due diligence, lease abstraction, and regulatory change tracking. For instance, AI-driven platforms like Kira Systems and Luminance are being adopted by major LPO providers to enhance document review efficiency. The U.S. Patent and Trademark Office recorded over 650,000 patent applications in 2022, many requiring AI-assisted prior art searches, a service increasingly outsourced to tech-enabled LPO vendors. Furthermore, the global legal tech market is projected to reach $35 billion by 2027, as per Statista, indicating strong demand for digital legal solutions. North American LPO providers are uniquely positioned to capitalize on this trend by combining AI with domain expertise and regulatory compliance knowledge. Early adopters are already offering AI-augmented litigation forecasting and risk assessment tools, shifting the LPO value proposition from cost reduction to strategic advisory.

Growth of In-House Legal Operations and Legal Operations (Legal Ops) Teams

The institutionalization of legal operations within corporate legal departments is also expected to fuel the growth of the North America legal process outsourcing (LPO) market. These teams are increasingly responsible for vendor management, legal spend analytics, and workflow automation functions that align closely with LPO capabilities. Legal Ops professionals are prioritizing outsourcing for routine legal tasks to redirect internal resources toward strategic initiatives. A 2023 CLOC survey found that 71% of Legal Ops leaders plan to increase spending on external legal service providers over the next three years, particularly for contract lifecycle management and compliance automation. The average corporate legal department now manages over 25,000 contracts annually, as reported by Gartner, necessitating scalable support. LPO providers offering managed legal services with transparent pricing and performance metrics are becoming preferred partners. Additionally, the rise of legal project management frameworks has enabled better integration of outsourced teams into corporate legal workflows.

MARKET CHALLENGES

Talent Retention and Skill Gaps in Specialized Legal Domains

The North America legal process outsourcing market faces a persistent challenge in attracting and retaining skilled legal professionals, particularly in niche practice areas such as intellectual property, securities law, and healthcare compliance. While LPO providers rely on trained attorneys and paralegals for high-quality output, competition with law firms and in-house legal departments for top talent remains intense. This disparity leads to high turnover rates, with some LPO providers reporting annual attrition exceeding 30%, as noted in a 2022 study by the Center for Legal Economics. The U.S. Patent and Trademark Office licensed only 1,200 patent attorneys in 2022, highlighting the scarcity of qualified professionals. LPO firms often struggle to maintain consistent quality when rapidly scaling teams to meet client demand. Additionally, the hybrid work model has intensified competition, as legal professionals now seek flexibility and career advancement opportunities that traditional LPO structures may not provide. Without robust training programs and career progression pathways, LPO providers risk service degradation and client attrition.

Regulatory Fragmentation Across U.S. States and Jurisdictional Complexity

The decentralized nature of the U.S. legal system, with 50 distinct state jurisdictions and varying regulatory requirements, poses a significant challenge for the growth of the North America legal process outsourcing (LPO) market. Each state maintains unique rules on attorney conduct, data handling, and court procedures, complicating the uniform delivery of outsourced legal services. For example, 28 states have enacted their own data privacy laws as of 2023, with differing definitions of personal information and compliance timelines, as documented by the National Conference of State Legislatures. LPO providers must ensure that their workflows comply with the specific regulations of each jurisdiction in which their clients operate, requiring substantial legal oversight and customization. This fragmentation increases the complexity of tasks such as multi-state litigation support, regulatory filings, and contract enforcement. Additionally, the unauthorized practice of law (UPL) statutes in states like Texas and Florida prohibit non-licensed individuals from performing certain legal functions, even if supervised, limiting the scope of outsourced work. A 2023 report by the American Bar Association revealed that 44 states have active UPL enforcement mechanisms, creating legal risks for LPO firms operating across state lines.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Location, Service, End-user Enterprise Size, End-user, Delivery Model, Technology Adoption, and Country. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | United States, Canada, Mexico, Rest of North America |

| Market Leaders Profiled | Integreon Managed Solutions, Inc., Elevate Services, Inc., QuisLex, Inc., Epiq Global, Inc., and Axiom Law Inc. |

SEGMENTAL ANALYSIS

By Location Insights

The onshore outsourcing segment held a dominant share of the North America legal process outsourcing market in 2025, with the heightened regulatory scrutiny and the prioritization of data sovereignty in legal workflows. The United States, in particular, lacks a unified federal privacy law, yet enforces stringent state-level regulations such as the California Privacy Rights Act (CPRA) and Virginia’s Consumer Data Protection Act. According to the National Conference of State Legislatures, 18 states had comprehensive privacy laws in effect by 2023, each imposing distinct obligations on data handling. Law firms and corporate legal departments increasingly avoid cross-border data transfers to mitigate risks under Model Rule 1.6 of the American Bar Association, which mandates client confidentiality. A 2023 survey by the International Legal Technology Association found that 78% of U.S. corporate counsel prefer onshore providers for matters involving sensitive litigation or intellectual property.

The onshore segment is likely to grow with an expected CAGR of 11.4% from 2026 to 2034, owing to the rise of legal operations (Legal Ops) teams within corporations, which demand seamless integration between internal legal departments and external service providers. Unlike offshore models that face latency and communication barriers, onshore LPO enables real-time collaboration, aligning with agile legal project management frameworks. The Corporate Legal Operations Consortium (CLOC) reported in 2023 that 85% of Legal Ops leaders prioritize vendor proximity for workflow synchronization and quality control. A study by the Stanford CodeX Center revealed that AI models trained on U.S.-based legal data achieve 27% higher accuracy in predicting case outcomes when managed within domestic infrastructure.

By Service Insights

The contract drafting and management segment held 38.25% of the North America LPO market share in 2024, with the exponential growth in corporate contractual obligations across industries such as technology, healthcare, and energy. Legal departments are increasingly outsourcing these labor-intensive tasks to reduce cycle times and ensure standardization. A 2023 report by McKinsey & Company found that companies using LPO for contract management reduced negotiation timelines by 40% on average. Another factor is the integration of contract lifecycle management (CLM) platforms, which rely on human-in-the-loop validation for clause extraction and risk assessment.

The e-discovery services segment is swiftly emerging with a CAGR of 13.2% during the forecast period, with the escalating volume of digital evidence in litigation and regulatory investigations. In 2022, U.S. federal courts processed over 330,000 civil cases, many involving terabytes of electronic data, as reported by the Administrative Office of the U.S. Courts. The increasing use of artificial intelligence in document classification. Platforms like Relativity and Everlaw are being deployed in tandem with outsourced legal reviewers, enhancing accuracy and speed. The U.S. Department of Justice filed over 315,000 civil and criminal cases in 2023, many requiring extensive discovery, according to the Bureau of Justice Statistics. Furthermore, the Securities and Exchange Commission initiated 784 enforcement actions in 2023, each demanding comprehensive data analysis. These factors collectively position e-discovery as the most dynamic and technologically advanced segment within the LPO ecosystem.

By Enterprise Size Insights

The large enterprises segment was the largest and held a dominant share of the North America LPO market in 2025, owing to the complex legal and compliance demands faced by multinational corporations operating across multiple jurisdictions. The average Fortune 500 company faces over 1,200 regulatory requirements annually, according to the Mercatus Center’s Regulatory Dashboard, necessitating dedicated legal infrastructure. A 2023 survey by the Corporate Legal Operations Consortium (CLOC) revealed that 91% of large enterprises outsource at least one legal function, with an average annual LPO expenditure of $4.2 million per company. Another factor is the institutionalization of Legal Ops teams, which prioritize vendor management and process optimization. Additionally, the rise in cross-border transactions, evidenced by $1.9 trillion in U.S. foreign direct investment in 2023, as per the Bureau of Economic Analysis, has intensified the need for multilingual and multi-jurisdictional legal support.

The small and medium-sized enterprises (SMEs) segment is substantially to grow with a CAGR of 10.8% from 2026 to 2034, owing to the increasing regulatory burdens on smaller firms, which lack the resources to maintain full-scale legal departments. The U.S. Small Business Administration reported in 2023 that over 32 million SMEs operate in the U.S., collectively facing rising exposure to litigation and compliance risks. For instance, the number of employment-related lawsuits filed by SMEs increased by 22% between 2020 and 2023, as recorded by the Equal Employment Opportunity Commission.

By End-User Insights

The corporate segment held a prominent share of the North America LPO market in 2025, owing to the strategic transformation of corporate legal functions into cost-optimized, operationally efficient units. The average corporate legal department now manages legal spend exceeding $12 million annually, according to Deloitte’s 2023 Legal Benchmarking Study, compelling organizations to outsource non-core tasks to improve ROI. The Corporate Legal Operations Consortium (CLOC) reported in 2023 that 79% of corporate legal departments have formal LPM practices, enabling structured outsourcing. The Securities and Exchange Commission’s enforcement actions rose to 784 in 2023, up from 459 in 2020, increasing pressure on in-house teams. Furthermore, the integration of AI-driven contract analytics platforms, used by 65% of Fortune 500 legal departments as per Gartner, requires outsourced legal analysts for data annotation and validation.

The law firms segment is expected to grow with a CAGR of 12.1% from 2025 to 203,3, owing to the competitive pressures to reduce costs while maintaining service quality. Mid-sized and large law firms are increasingly outsourcing document review, legal research, and due diligence to remain competitive in fixed-fee and alternative fee arrangements. Additionally, the surge in litigation volume, 333,000 civil cases filed in U.S. federal courts in 2022, has strained internal resources. Firms are leveraging LPO for e-discovery, depositions, and trial preparation, reducing turnaround time by up to 50%, as noted in a 2022 study by the International Legal Technology Association. The adoption of legal tech platforms like Casetext and Westlaw Edge further enables seamless integration with outsourced teams.

By Delivery Model Insights

The third-party segment was the largest by capturing a prominent share of the North America market in 2025, with the flexibility, scalability, and cost-efficiency offered by external vendors compared to captive centers. Establishing and maintaining a captive center requires significant capital investment, regulatory compliance, and HR infrastructure, which many organizations seek to avoid. The third-party providers offer pay-per-use models and immediate access to skilled legal professionals. A 2023 study by the International Association of Legal Administrators found that 82% of corporate legal departments prefer third-party vendors for their agility and specialized expertise.

The captive centers segment is projected to grow at a CAGR of 9.7% from 2026 to 2034, owing to the large corporations seeking greater control over data security, quality, and intellectual property. Multinational enterprises in highly regulated sectors such as pharmaceuticals, finance, and defense are increasingly establishing captive centers in the U.S. and Canada to ensure compliance with strict data governance standards. According to the U.S. Department of Commerce, 67% of captive centers established by U.S. firms in 2023 were located domestically, reflecting a shift toward onshore control. A key factor is the sensitivity of legal data; a 2023 Federal Trade Commission report revealed that 42% of data breaches in the legal sector originated from third-party vendors, prompting firms to bring operations in-house. Additionally, companies like JPMorgan Chase and Pfizer have reported 30% improvement in service quality after transitioning to captive models, as noted in a 2023 McKinsey case study. These centers also enable tighter integration with internal legal teams and proprietary systems, supporting long-term strategic objectives.

COUNTRY-LEVEL ANALYSIS

United States Legal Process Outsourcing (LPO) Market Insights

The United States was the top performer in the North America legal process outsourcing market with 93.2% of the share in 2024. The country’s legal system generates over 330,000 federal civil filings annually, according to the Administrative Office of the U.S. Courts, necessitating extensive support for e-discovery and documentation. Additionally, the U.S. leads in legal technology adoption, with 70% of Fortune 500 legal departments using AI-powered tools, as per the Stanford Institute for Human-Centered AI. This digital transformation has amplified reliance on LPO providers for data annotation, model training, and compliance monitoring. The absence of a federal privacy law has also led to a fragmented regulatory landscape, with 18 states enacting their own data protection statutes by 2023, as reported by the National Conference of State Legislatures. This complexity drives demand for specialized, onshore LPO services. Furthermore, the U.S. Securities and Exchange Commission initiated 784 enforcement actions in 2023, underscoring the need for scalable legal support.

Canada Legal Process Outsourcing (LPO) Market Insights

Canada held 7.1% of the North America LPO market share in 2025. Positioned as a strategic nearshoring destination, Canada is increasingly leveraged by U.S. firms seeking bilingual, common-law-compliant legal support with reduced data privacy risks. The country’s legal framework closely mirrors that of the U.S., facilitating seamless integration for cross-border legal workflows. According to the Canadian Bar Association, over 60% of Canadian law firms now collaborate with U.S. counterparts on litigation and transactional matters, creating demand for outsourced legal drafting and research. A key driver is linguistic alignment; Canada’s 22 million English-speaking residents, as recorded by Statistics Canada, provide a skilled labor pool fluent in U.S. legal terminology. Additionally, the Personal Information Protection and Electronic Documents Act (PIPEDA) offers a balanced data protection regime, making Canada a preferred alternative to offshore jurisdictions. The Toronto-Waterloo corridor has emerged as a legal tech hub, hosting firms like Blue J Legal and Ross Intelligence, which integrate AI with outsourced legal analysis.

COMPETITIVE LANDSCAPE

The competitive landscape of the North America legal process outsourcing market is marked by a convergence of legal expertise, technological innovation, and operational agility. While traditional legal service providers continue to dominate, a new generation of legal operations firms is challenging conventional models by offering integrated, tech-enabled solutions. Differentiation increasingly hinges not on cost alone but on the ability to deliver secure, scalable, and compliant services aligned with corporate legal strategy. Firms are investing heavily in artificial intelligence, data analytics, and workflow automation to enhance service quality and responsiveness. Client expectations have evolved, demanding transparency, performance metrics, and collaboration rather than mere task execution. As a result, competition is shifting from price-based rivalry to value creation, with providers positioning themselves as strategic enablers of legal transformation. The absence of significant regulatory barriers to entry has also encouraged niche players to emerge, focusing on specialized domains or industry-specific compliance. This dynamic environment fosters continuous innovation, with market leaders striving to balance scalability with customization, and offshore efficiency with onshore control. The growing emphasis on data security, ethical compliance, and seamless integration with internal legal teams further intensifies the need for differentiation, making the market both highly competitive and rapidly evolving.

KEY MARKET PLAYERS

Noteworthy Companies dominating the North America Legal process outsourcing market profiled in the report are

- Integreon Managed Solutions, Inc.

- Elevate Services, Inc.

- QuisLex, Inc.

- Epiq Global, Inc.

- Axiom Law Inc.

TOP LEADING PLAYERS IN THE MARKET

- Thomson Reuters has established itself as a leader in the North America legal process outsourcing market by integrating its authoritative legal content and research platforms with managed services. The company offers end-to-end legal support, including regulatory compliance, contract management, and litigation readiness, leveraging its deep domain expertise and proprietary technology. Its seamless integration with Westlaw and other legal research tools enables clients to benefit from consistent, high-quality outputs.

- Elevate Services has redefined the legal services delivery model by combining legal operations expertise with advanced technology and process optimization. The firm specializes in providing flexible, on-demand legal support across contract management, e-discovery, compliance, and legal transformation consulting. Known for its client-first philosophy, Elevate emphasizes transparency, performance metrics, and value-based pricing, aligning closely with the evolving needs of in-house legal teams. Its investment in proprietary platforms like Canvas and Align enables clients to manage legal workflows with greater visibility and control.

- Integreon has emerged as a key player by delivering high-value legal and compliance services through a blend of skilled professionals and cutting-edge technology. The company specializes in e-discovery, due diligence, contract lifecycle management, and legal research, serving a broad client base that includes global law firms and Fortune 500 companies. Integreon differentiates itself through its focus on AI-augmented services, enabling faster document review and improved accuracy in large-scale legal projects. With a strong delivery infrastructure and a commitment to quality, the firm has built long-term partnerships by offering tailored solutions that adapt to dynamic legal demands. Its strategic investments in legal tech and talent development have strengthened its reputation as a forward-thinking provider capable of supporting complex, high-stakes legal initiatives across jurisdictions.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

One major strategy employed by leading players is the integration of proprietary legal technology platforms with outsourced services to enhance efficiency, accuracy, and client transparency. By developing in-house tools for contract analysis, e-discovery, and legal project management, firms are able to deliver more consistent and measurable outcomes. Another key approach is strategic specialization, where providers focus on niche practice areas such as intellectual property, regulatory compliance, or M&A due diligence, allowing them to offer deeper expertise and build trusted advisory relationships. A third strategy is the emphasis on legal operations consulting, where LPO providers work alongside corporate legal departments to redesign workflows, implement process improvements, and adopt value-based pricing models, thereby transitioning from transactional vendors to strategic partners in legal transformation.

RECENT MARKET DEVELOPMENTS

- In March 2023, Thomson Reuters launched a new AI-powered contract intelligence module within its Legal Managed Services suite by enhancing its ability to support enterprise clients in automated clause extraction and risk assessment.

- In June 2023, Elevate Services partnered with a leading legal tech platform to integrate predictive analytics into its legal project management offerings, which is enabling clients to forecast costs and timelines with greater accuracy.

- In September 2023, Integreon expanded its U.S.-based delivery center in Houston with its onshore capabilities and strengthened its focus on data-sensitive legal work for energy and healthcare clients.

- In January 2024, Elevate Services introduced a comprehensive legal operations maturity assessment tool by allowing corporate legal departments to benchmark performance and identify outsourcing opportunities.

- In May 2024, Thomson Reuters acquired a niche regulatory compliance consultancy to bolster its expertise in state-level privacy laws and expand its support for multi-jurisdictional compliance programs.

MARKET SEGMENTATION

This North America Legal process outsourcing market research report is segmented and sub-segmented into the following categories.

By Location

- Offshore Outsourcing

- Onshore Outsourcing

By Service

- Contract Drafting

- Review and Contract Management

- e-Discovery

- Litigation Support

- Patent Support

- Compliance Management

- Due Diligence and Legal Research

- Others

By End-user Enterprise Size

- SMEs

- Large Enterprises

By End-user

- Law Firms

- Corporate Legal Departments

- Government and Public Sector

- Others

By Delivery Model

- Captive Centers

- Third-Party Providers

By Technology Adoption

- AI-Enabled Services

- Traditional Services

By Country

- United States

- Canada

- Mexico

- Rest of North America

Frequently Asked Questions

1. What drives growth in the North America Legal Process Outsourcing (LPO) Market?

Growth factors include rising legal costs, complex regulatory requirements, litigation volume, demand for scalable operations, and rapid technology adoption such as AI and automation.

2. Which countries lead the North America Legal Process Outsourcing (LPO) Market?

The United States is by far the largest market, followed by Canada and Mexico supporting hybrid nearshore and onshore models.

3. Who are the leading players in the North America Legal Process Outsourcing (LPO) Market?

Top firms include UnitedLex, Integreon, Clairvolex, Clutch Group, Cobra Legal Solutions, CPA Global, Evalueserve, Exigent, QuisLex, Mindcrest, Legal Advantage LLC, Lex Outsourcing, and Pangea3.

4. What types of services are offered in the North America LPO Market?

Key services include litigation and e-discovery support, contract management, due diligence, intellectual property (IP) services, compliance management, and legal research.

5. How is technology shaping the North America Legal Process Outsourcing (LPO) Market?

AI, cloud platforms, and automation tools are revolutionizing document review, legal research, workflow management, and compliance monitoring.

6. What industries outsource legal processes in North America?

Major industries include finance, healthcare, technology, energy, and consumer goods, each seeking cost savings and expertise for regulatory-driven legal work.

7. How is data privacy addressed in the North America LPO Market?

Strict adherence to regulatory standards like CCPA and FTC, plus robust cybersecurity frameworks and compliance protocols, are essential for data privacy and legal confidentiality.

8. What are the main challenges in the North America Legal Process Outsourcing (LPO) Market?

Challenges involve regulatory complexity, data security, cross-border workflow integration, talent retention, and evolving client expectations around transparency and control.

9. How do LPO providers ensure compliance in North America?

Providers invest in modular compliance frameworks, real-time monitoring, staff training, and collaboration with industry bodies and regulators to ensure adherence.

10. Which service segments are seeing the fastest growth in North America LPO Market?

E-discovery, contract lifecycle management, IP support, and compliance analytics are growing rapidly due to increased complexity and technology integration.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com