North America Liquid Fertilizers Market Size, Share, Trends & Growth Forecast Report, Segmented By Nutrient Type, Form, Mode Of Application, Crop Type, and Country (The U.S, Canada, Mexico, and Brazil), Industry Analysis From 2026 to 2034

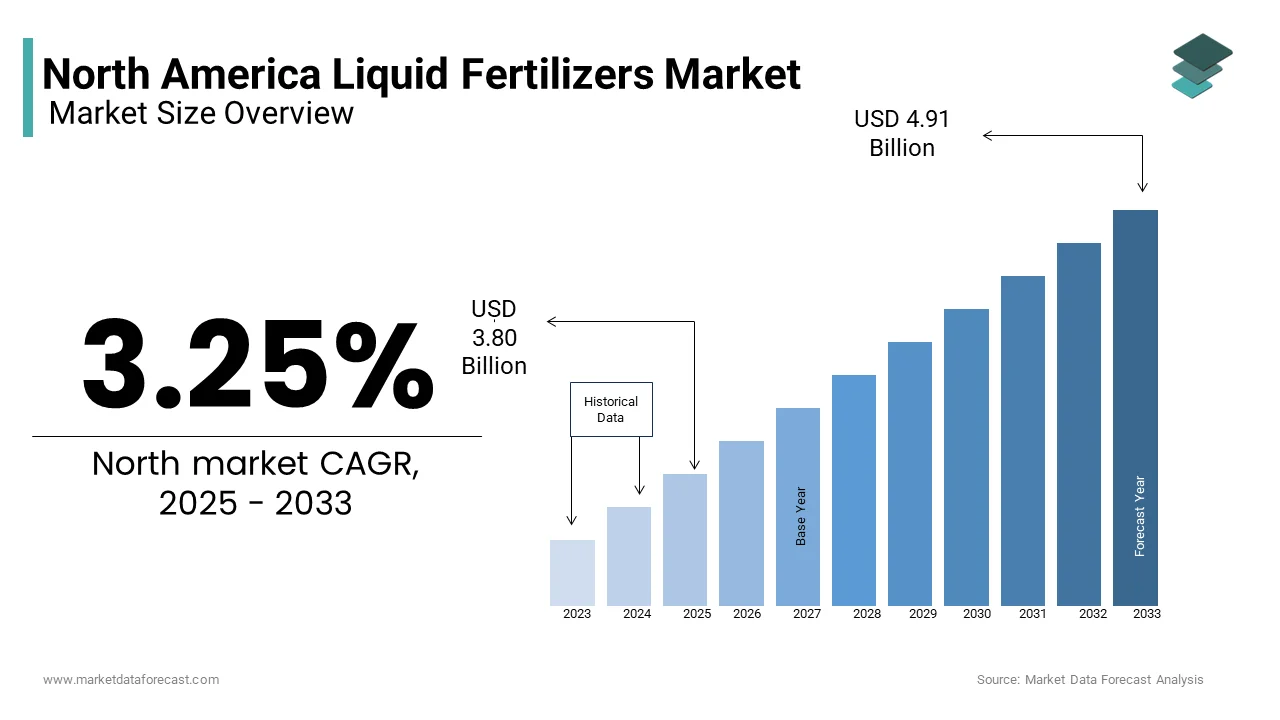

Market Size, 2025

$3.80 BnMarket Estimate, 2026

$3.92 BnMarket Forecast, 2034

$5.07 BnCAGR, 2026–2034

3.25%North America Liquid Fertilizers Market Size

The North American liquid fertilizers market size was valued at USD 3.80 billion in 2025 and is expected to reach USD 3.92 billion in 2026 to reach USD 5.07 billion by 2034, growing at a CAGR of 3.25% during the forecast period from 2026 to 2034.

Current Scenario of the North American Liquid Fertilizers Market

Liquid fertilizers are formulations that deliver essential nutrients such as nitrogen, phosphorus, potassium, and micronutrients in a soluble form, enabling rapid absorption by plants. These products are particularly valued for their ease of application, uniform nutrient distribution, and compatibility with modern farming technologies like fertigation and precision agriculture.

MARKET DRIVERS

Rising Adoption of Precision Agriculture Technologies

The increasing adoption of precision agriculture technologies has emerged as a primary driver for the North America Liquid Fertilizers Market. Liquid fertilizers are highly compatible with fertigation and foliar spraying techniques, enabling farmers to apply nutrients with pinpoint accuracy and minimize waste. A key factor driving this trend is the growing need to optimize resource utilization in agriculture. Moreover, the ability to tailor nutrient formulations to specific soil and crop requirements ensures maximum yield potential. For example, nitrogen-based liquid fertilizers enriched with micronutrients have been shown to increase corn yields.

Focus on Sustainable Farming Practices

Sustainability has become a cornerstone of modern agriculture, propelling the adoption of liquid fertilizers as a tool for reducing environmental impact. Liquid fertilizers play a vital role in this transition by minimizing nutrient runoff and improving soil health. Liquid fertilizers are central to these efforts, as they enable farmers to implement targeted nutrient applications that reduce excess fertilizer use. For instance, slow-release liquid fertilizers can decrease nitrogen leaching into groundwater. These benefits align closely with government initiatives promoting eco-friendly farming methods, making liquid fertilizers a strategic choice for compliance and long-term sustainability.

MARKET RESTRAINTS

High Costs Associated with Advanced Formulations

One of the most significant restraints affecting the North American Liquid Fertilizers Market is the elevated cost associated with advanced formulations. This financial burden disproportionately affects small-scale farmers who operate on tight margins and lack the resources to invest in premium solutions. Such challenges create barriers to widespread adoption, particularly among smaller operations where profit margins are already constrained. Larger enterprises may absorb these costs more easily, but they too face pressure to balance input expenses against market pricing dynamics. In addition, the complexity of integrating new liquid fertilizers into existing farming systems often requires additional training and infrastructure investments, further inflating operational costs.

Stringent Regulatory Frameworks

Another critical restraint stems from stringent regulatory frameworks governing the development and commercialization of liquid fertilizers. The Food and Drug Administration (FDA) mandates rigorous testing protocols to ensure safety and efficacy before any new product enters the market. This prolonged timeline poses significant challenges for manufacturers aiming to introduce groundbreaking solutions tailored to emerging industry needs. Moreover, discrepancies between federal and state-level regulations often lead to fragmented compliance requirements, complicating distribution efforts. For example, California’s Proposition 65 imposes strict labeling standards for chemical residues, creating additional hurdles for companies operating nationwide.

MARKET OPPORTUNITIES

Expansion into Organic Farming Systems

A burgeoning opportunity lies in expanding the application of liquid fertilizers to organic farming systems, driven by growing consumer demand for sustainably produced food. These products, derived from natural sources like fish emulsion and seaweed extracts, provide essential nutrients while adhering to organic certification standards. Simultaneously, the rise of regenerative agriculture presents a novel avenue for innovation. Like, regenerative practices could sequester up to 1.5 gigatons of carbon dioxide annually, with liquid fertilizers serving as a cornerstone of these systems. For instance, bioactive liquid fertilizers enriched with humic acids are effective in improving soil fertility and water retention, as reported by the University of Nebraska-Lincoln.

Adoption of Customized Nutrient Solutions

The advent of customized nutrient solutions presents a transformative opportunity for the North American Liquid Fertilizers Market. This paradigm shift involves leveraging data analytics and soil testing technologies to develop formulations that address specific nutrient deficiencies in crops. For example, precision mapping technologies enable farmers to identify areas with optimal nutrient uptake potential, ensuring maximum crop yields. Besides, customized liquid fertilizers can reduce nutrient wastage, directly impacting profitability. These innovations not only cater to economic considerations but also align with consumer preferences for sustainably produced food, thereby fueling the expansion of the liquid fertilizers market.

MARKET CHALLENGES

Resistance to the Adoption of New Technologies

A persistent challenge facing the North American Liquid Fertilizers Market is the resistance to the adoption of new technologies exhibited by traditional farmers entrenched in conventional practices. In addition, a significant portion of crop producers remain hesitant to adopt precision-based liquid fertilizers due to skepticism about their effectiveness or unfamiliarity with implementation processes. This reluctance is particularly pronounced among older generations who prioritize tried-and-tested methods over experimental approaches. Furthermore, cultural and regional disparities exacerbate this issue. For example, Southern states tend to have lower adoption rates compared to technologically progressive regions like the Midwest, where large-scale operations dominate.

Concerns Over Environmental Impact and Regulation

Environmental concerns pose another formidable challenge for the North American Liquid Fertilizers Market, especially regarding nutrient runoff and water contamination. Liquid fertilizers, despite their efficiency, are often scrutinized for their potential contribution to these issues if not applied correctly. Such sentiments place immense pressure on manufacturers to develop low-impact alternatives while adhering to complex regulatory frameworks. For example, the Clean Water Act imposes strict limits on nitrogen and phosphorus levels in water bodies, creating additional hurdles for companies operating nationwide. Additionally, misinformation spread via social media platforms amplifies public distrust, creating reputational risks for brands associated with controversial fertilizer practices.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 3.25% |

| Segments Covered | By Nutrient Type, Form, Application, Crop Typ,e Pla,nt and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | United States, Canada, Mexico |

| Market Leaders Profiled | Haifa Chemicals Ltd., Kugler Company, Yara International ASA, Israel Chemicals Ltd, Agrium Inc., and Sociedad Quimica Y Minera SA (SQM). |

SEGMENTAL ANALYSIS

By Nutrient Type Insights

The nitrogen segment dominated the North American Liquid Fertilizers Market by holding approximately 40% of the market share in 2025. This leading position is driven by nitrogen's critical role in plant growth, particularly in crops like corn and wheat, which require high levels of this nutrient for optimal yields. A key factor driving this dominance is nitrogen's versatility in application methods. Moreover, advancements in formulation technologies have enabled the development of slow-release nitrogen fertilizers, which reduce leaching into groundwater and align with environmental regulations.

The micronutrients segment represented the fastest-growing segment in the North America Liquid Fertilizers Market, with a projected CAGR of 9.5%. This rapid growth is fueled by the increasing recognition of micronutrients' role in addressing hidden hunger in crops, particularly under intensive farming practices. Zinc, boron, and manganese are among the most sought-after micronutrients, as they enhance crop resilience and quality. A major driver of this growth is the rising adoption of high-yield crop varieties, which often exhibit micronutrient deficiency.cies

Insights By Form Insights

The synthetic liquid fertilizers dominate the North America Liquid Fertilizers Market by capturing a 65.7% of the total share in 2024. This prominence is attributed to their affordability, scalability, and consistent performance across diverse climatic conditions. A key factor driving this leadership is their ability to deliver precise nutrient formulations tailored to specific crop requirements. Additionally, their compatibility with modern farming technologies, such as fertigation and precision agriculture, ensures uniform nutrient distribution and reduces wastage.

The organic liquid fertilizers segment is the fastest-growing segment, with a CAGR of 10.2%, propelled by increasing demand for sustainably produced food. Another factor fueling this growth is the growing emphasis on soil health and environmental conservation. Also, bioactive organic fertilizers enriched with humic acids have been shown to increase crop resilience to drought and disease.

By Application Insights

The soil application segment dominated the North America Liquid Fertilizers Market by holding a 50.9% of the market share in 2024. This is driven by its widespread use in large-scale farming operations, where liquid fertilizers are directly applied to the soil to ensure deep nutrient penetration and sustained availability. A large portion of row crop farmers rely on soil-applied liquid fertilizers to optimize yields. A key factor driving this dominance is the ability of soil-applied fertilizers to address macro and micronutrient deficiencies effectively. Also, advancements in drip irrigation systems have enhanced the efficiency of soil applications, reducing nutrient runoff and aligning with environmental regulations.

The fertigation segment is quickly moving ahead, with a CAGR of 11.3%. This is supported by the increasing adoption of precision agriculture technologies. A major driver of this growth is the ability of fertigation to deliver nutrients directly to plant roots, minimizing waste and maximizing efficiency. Like, fertigation can reduce fertilizer usage, directly impacting profitability. Additionally, fertigation systems help minimize nutrient runoff, aligning with regulatory frameworks aimed at protecting water resources.

By Crop Type Insights

The segment of grains and cereals commanded the North America Liquid Fertilizers Market by holding a 45.5% of the market share in 2024. This control over the market is rooted in the region's extensive cultivation of crops like corn, wheat, and barley, which require high nutrient inputs to sustain productivity. A large share of acres of corn are cultivated annually in the U.S., creating immense demand for liquid fertilizers. A key factor driving this dominance is the critical role of liquid fertilizers in optimizing yield potential. Besides, advancements in formulation technologies have enabled the development of slow-release fertilizers, which reduce environmental impact and align with sustainability goals.

The segment of fruits and vegetables exhibited the quickest growth, with a CAGR of 10.8%. This is due to the increasing demand for high-quality, nutrient-rich produce. Also, sales of organic fruits and vegetables in North America have surged annually, creating significant demand for liquid fertilizers that enhance flavor, texture, and shelf life. A major driver of this growth is the rising adoption of foliar-applied liquid fertilizers, which deliver nutrients directly to plant leaves. As per the University of California, Davis, foliar-applied micronutrient fertilizers can increase fruit yields while improving resistance to pests and diseases. Besides, adopting regenerative agricultural practices has amplified the demand for fertilizers that support soil health and biodiversity.

COUNTRY ANALYSIS

Top Leading Countries in the Market

United States Liquid Fertilizers Market Analysis

The United States led the North American Fertilizers Market. This dominance is rooted in the country's vast agricultural infrastructure, which supports large-scale cultivation of crops like corn, soybeans, and wheat. A key driver of this leadership is the presence of advanced farming technologies. Also, stringent environmental regulations enforced by the EPA have accelerated the adoption of eco-friendly fertilizers, ensuring compliance with consumer expectations.

Canada Liquid Fertilizers Market Analysis

Canada is holding a notable portion of the regional share. The country's strong emphasis on sustainable farming practices has positioned it as a hub for innovative fertilizer solutions. Another factor driving Canada's prominence is its thriving oilseed industry. In addition, government incentives for adopting organic farming methods have spurred the use of bioactive fertilizers, further bolstering the market's growth.

Mexico Liquid Fertilizers Market Analysis

Mexico possesses a smaller regional market share. The country's rapidly expanding agricultural sector, particularly in fruits and vegetables, has created a fertile ground for liquid fertilizer innovation. A key driver of this growth is the increasing adoption of imported liquid fertilizers, facilitated by favorable trade agreements with the U.S. and Canada. Like micronutrient-rich fertilizers have gained traction due to their ability to improve crop resilience and quality. Also, efforts to modernize agricultural practices through government-funded programs have encouraged small-scale farmers to invest in premium fertilizer solutions, contributing to Mexico's steady market expansion.

The "Rest of North America" encompasses smaller economies like Bermuda and the Caribbean nations. These regions are witnessing the gradual adoption of liquid fertilizers due to their growing focus on export-oriented agriculture. Another factor influencing this segment's growth is the influx of foreign expertise and technology. Also, partnerships with international organizations have introduced cost-effective fertilizer solutions tailored to local conditions.

Puerto Rico represents a niche yet emerging player in the North American Liquid Fertilizers Market. The island's agricultural sector is transforming, with a focus on self-sufficiency and resilience against external shocks. Recent hurricanes have underscored the need for fortified fertilizers to mitigate production losses. A key driver of this progress is the adoption of bioactive liquid fertilizers, which safeguard soil health during adverse weather conditions. Additionally, government subsidies aimed at revitalizing rural economies have incentivized farmers to invest in advanced fertilizer solutions, fostering incremental growth in the market.

COMPETITIVE LANDSCAPE

The North America Liquid Fertilizers Market is characterized by intense competition, driven by the presence of established multinational corporations and emerging niche players. Companies strive to differentiate themselves through innovation, sustainability, and customer-centric strategies, creating a dynamic and rapidly evolving landscape. Leaders like Nutrien Ltd., Yara International, and Agrium Inc. dominate the market by leveraging their extensive R&D capabilities and global reach to deliver high-performance solutions. At the same time, smaller firms focus on specialized products that cater to specific agricultural segments or address unique challenges such as nutrient efficiency and environmental sustainability. Regulatory pressures and shifting consumer preferences further intensify competition, compelling companies to adopt sustainable practices and transparent labeling. Collaborations, mergers, and acquisitions are common strategies used to consolidate market share and expand product portfolios.

KEY MARKET PLAYERS

The market is categorized by the existence of diversified international and national companies, where global retailers lead the market and are predicted to grow exponentially by securing regional or local players. These retailers pose a tough test for the small vendors in terms of price, accessibility, and variability.

The major companies dominating the Liquid Fertilizers market in this region are

- Haifa Chemicals Ltd.

- Nutrien Ltd.

- Kugler Company

- Yara International ASA

- Israel Chemicals Ltd

- Agrium Inc

- Sociedad Quimica Y Minera SA (SQM).

Top Players in the Market

- Nutrien Ltd. is a global leader in the North American liquid Fertilizers Market, renowned for its innovative and sustainable fertilizer solutions tailored to meet the diverse needs of modern agriculture. The company specializes in producing high-performance liquid fertilizers enriched with nitrogen, phosphorus, and micronutrients, which are designed to enhance crop yields while minimizing environmental impact. Nutrien’s commitment to research and development has positioned it as a pioneer in creating eco-friendly formulations that align with regulatory standards.

- Yara International plays a pivotal role in the North American liquid Fertilizers Market by offering advanced nutrient solutions that integrate seamlessly with modern farming technologies. The company focuses on developing liquid fertilizers that optimize nutrient delivery, improve soil health, and support sustainable agricultural practices. Yara’s emphasis on sustainability aligns with its efforts to reduce greenhouse gas emissions and promote water conservation, making its products a preferred choice for eco-conscious farmers.

- Agrium Inc., now integrated into Nutrien Ltd., has historically been a prominent player in the North American liquid Fertilizers Market, specializing in the production of premium nitrogen-based liquid fertilizers. The company emphasizes sustainable sourcing practices and invests heavily in developing bioactive formulations to cater to the growing demand for environmentally friendly agricultural solutions. Agrium’s vertically integrated business model allows it to maintain control over the entire supply chain, ensuring quality and traceability.

Top Strategies Used By Key Market Participants

Strategic Acquisitions and Partnerships

Key players in the North America Liquid Fertilizers Market have prioritized strategic acquisitions and partnerships to expand their product portfolios and strengthen their market presence. By acquiring smaller firms specializing in niche fertilizer formulations or forming alliances with research institutions, these companies gain access to cutting-edge technologies and innovative solutions. Such collaborations enable them to address unmet needs in the agricultural sector while enhancing their competitive edge.

Investment in Sustainable Solutions

Sustainability has emerged as a cornerstone of competitive strategy in the liquid fertilizers market. Leading companies are investing heavily in the development of eco-friendly formulations that reduce nutrient runoff, improve soil health, and promote water conservation. By focusing on reducing the ecological footprint of agriculture, these players position themselves as champions of sustainable farming practices.

Emphasis on Research and Development

R&D is a critical driver of innovation in the North America Liquid Fertilizers Market. Key players are channeling significant resources into exploring novel formulations and advanced nutrient delivery systems that improve crop resilience and productivity. By staying at the forefront of technological advancements, these companies can introduce groundbreaking solutions tailored to specific climatic and soil conditions.

RECENT MARKET NEWS

- In April 2024, Nutrien Ltd. launched a new line of bioactive liquid fertilizers designed to enhance soil health and reduce environmental impact. This move aims to address growing concerns about sustainability in the North American market.

- In June 2023, Yara International partnered with a leading agricultural research institute to develop micronutrient-rich liquid fertilizers. This collaboration underscores Yara’s commitment to advancing precision farming practices through innovation.

- In January 2023, Agrium Inc. acquired a startup specializing in organic liquid fertilizer production. This acquisition strengthens Agrium’s ability to cater to the rising demand for certified organic agricultural solutions.

- In September 2022, Helena Chemical Company introduced a range of slow-release nitrogen fertilizers aimed at supporting regenerative agriculture. This initiative aligns with consumer preferences for environmentally friendly farming practices.

- In November 2022, Koch Agronomic Services expanded its production facilities in the Midwest to increase the supply of foliar-applied liquid fertilizers. This expansion supports the company’s goal of meeting rising demand in the North American Liquid Fertilizers Market.

MARKET SEGMENTATION

This research report on the North America Liquid Fertilizers Market is segmented and sub-segmented into the following categories.

By Nutrient Type

- Potassium

- Micronutrients

- Phosphate

- Nitrogen

By Form

- Organic

- Synthetic

By Application

- Soil

- Fertigation

- Foliar

- Others

By Crop Type

- Oil seeds

- Fruits & Vegetables

- Grains & Cereals

- Others

By Country

- US

- Canada

- Mexico

- Rest of North America

Frequently Asked Questions

What are liquid fertilizers used for in agriculture?

Liquid fertilizers provide essential nutrients in a dissolved form that plants can absorb quickly for improved growth.

Why is the demand for liquid fertilizers increasing in North America?

Farmers are adopting liquid fertilizers to achieve precise nutrient application and improve crop productivity.

Which crops commonly use liquid fertilizers in North America?

Crops such as corn, wheat, soybeans, fruits, and vegetables widely use liquid fertilizer applications.

What advantages do liquid fertilizers offer compared to solid fertilizers?

They allow uniform nutrient distribution, faster absorption, and compatibility with modern irrigation systems.

Which nutrients are commonly found in liquid fertilizers?

Nitrogen, phosphorus, potassium, and micronutrients are typically included in liquid fertilizer formulations.

What factors are driving growth in the North America liquid fertilizers market?

Increasing adoption of precision farming and the need for higher agricultural efficiency are major growth drivers.

How do liquid fertilizers support modern farming techniques?

They can be easily applied through fertigation and spraying systems used in advanced agricultural practices.

What challenges affect the liquid fertilizers market in North America?

Higher storage and transportation costs compared to solid fertilizers can influence market adoption.

Which countries dominate the North America liquid fertilizers market?

The United States leads the market, followed by Canada and Mexico due to their large agricultural sectors.

What future trend is expected in the North America liquid fertilizers market?

Growing use of precision agriculture technologies is expected to increase demand for liquid nutrient solutions.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com