Global Packaging Market Size, Share, Trends & Growth Forecast Report Segmented By Packaging Type (Plastic Packaging, Paper Packaging, Container Glass, Metal Cans and Containers), Packaging Format, End-Use Industry, and Region (North America, Europe, Asia Pacific, Latin America, Middle East, and Africa), Industry Analysis from 2025 to 2033

Global Packaging Market Summary

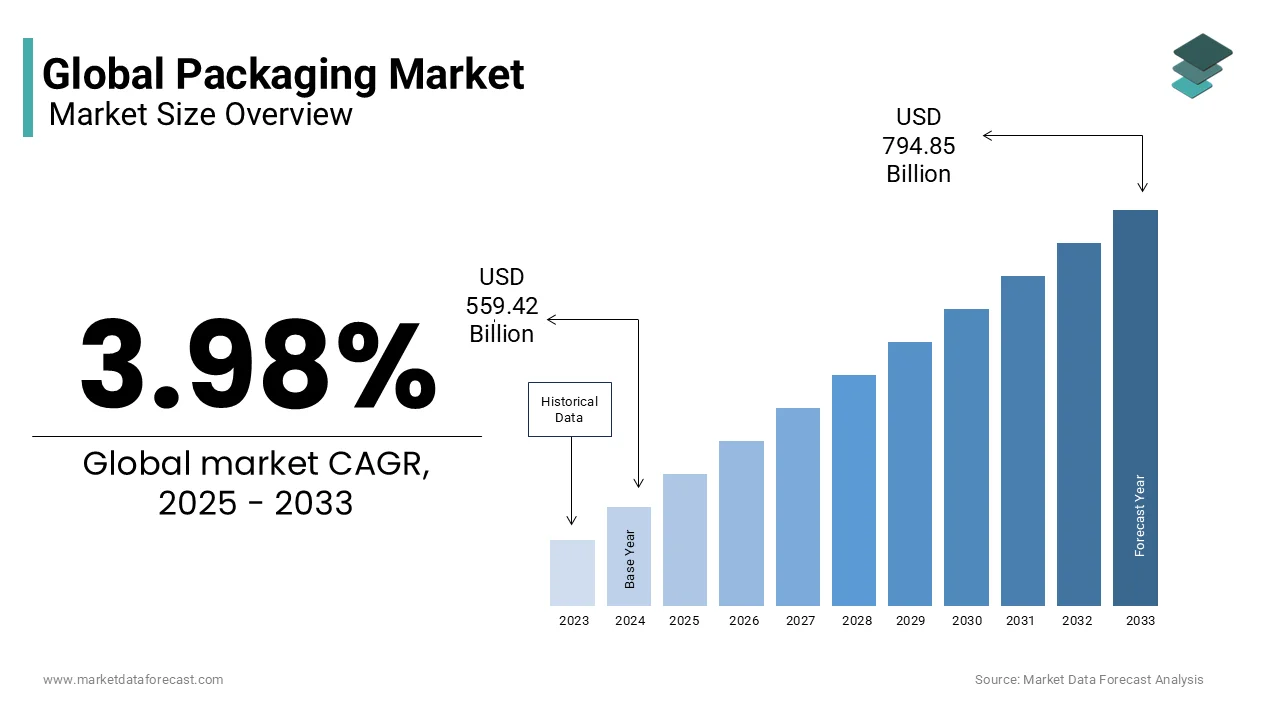

The global packaging market was valued at USD 559.42 billion in 2024 and is projected to reach USD 581.68 billion in 2025 and USD 794.85 billion by 2033, expanding at a CAGR of 3.98% from 2025 to 2033. The growth of the packaging market is driven by increasing demand for packaged goods across food, beverages, pharmaceuticals, and e-commerce sectors, rising consumer awareness of sustainability, and innovations in packaging materials and design.

Key Market Trends

- Increasing adoption of plastic and flexible packaging solutions for cost-effectiveness and convenience.

- Rising demand for sustainable and recyclable packaging materials.

- Growth in the e-commerce and retail sectors, fueling packaging requirements.

- Technological advancements in smart and active packaging to improve shelf life and product safety.

- Expansion of personalized and customized packaging solutions for brand differentiation.

Segmental Insights

- Based on packaging type, the plastic segment dominated the market in 2024 with a 38.2% share, due to its versatility, lightweight properties, and widespread usage across industries.

Regional Insights

- Asia-Pacific led the global packaging market by occupying 42.3% share in 2024, driven by rapid industrialization, a growing consumer base, and the expansion of food, beverage, and e-commerce industries.

- North America experienced steady growth due to technological innovations and demand for sustainable packaging solutions.

- Europe witnessed moderate growth supported by environmental regulations and high adoption of recyclable packaging.

- Latin America showed gradual growth due to expanding retail and consumer goods sectors.

- Middle East & Africa is emerging as a potential market with increasing packaged goods consumption.

Competitive Landscape

The global packaging market is competitive, with key players focusing on product innovation, sustainability initiatives, and regional expansion. Major players include Amcor Limited, Mondi Group, Sealed Air Corporation, International Paper, Sonoco Group, WestRock Company, Berry Global Inc., Constantia Flexibles, Huhtamaki, and Coveris Holdings.

Global Packaging Market Size

The global packaging market size was valued at USD 559.42 billion in 2024, and the market size is expected to be worth USD 794.85 billion by 2033 from USD 581.68 billion by 2025. The market is growing at a CAGR of 3.98% during the forecast period.

The packaging is a connective tissue between production and consumption, safeguarding products while shaping consumer perception and environmental outcomes. Its role is magnified by global shifts in consumption, urbanization, and sustainability pressures.

MARKET DRIVERS

Expansion of e-commerce and direct-to-consumer logistics

The explosion of e-commerce, which requires durable, lightweight, and sustainable solutions for product protection is driving the growth of packaging market. This surge creates rising demand for corrugated boxes, flexible packaging, and protective materials that can withstand multiple handling points. Additionally, the proliferation of direct-to-consumer models in food, cosmetics, and electronics necessitates branding opportunities directly on packaging, turning it into a marketing tool.

Growing focus on food safety and shelf-life extension

The increasing demand for the preserving food safety and extending shelf life is additionally to fuel the growth of packaging market. According to the Food and Agriculture Organization, around 13% of food is lost in supply chains before reaching retailers, often due to inadequate packaging and storage solutions. Rising consumer preference for ready-to-eat meals, perishable produce, and fortified beverages requires innovations such as modified-atmosphere packaging, antimicrobial films, and vacuum-sealed formats. Companies investing in active and intelligent packaging technologies are not only responding to regulatory standards but also to consumer demand for transparency and product integrity, which is cementing food safety as a long-term driver of packaging innovation.

MARKET RESTRAINTS

Environmental impact and plastic waste concerns

Packaging waste, which is a mounting restraint on the industry as governments and consumers demand greener alternatives. According to the United Nations Environment Programme, 11 million tonnes of plastic enter oceans annually, much of it originating from packaging. This has spurred regulatory bans on single-use plastics in countries such as India, China, and Australia, compelling firms to redesign packaging portfolios. Transitioning to biodegradable or recyclable alternatives entails high research, sourcing, and production costs, particularly for small and medium enterprises. Moreover, consumer skepticism over “greenwashing” requires companies to demonstrate verifiable sustainability claims, adding compliance burdens.

Rising raw material costs and supply chain volatility

The volatility of raw material prices such as paper pulp, aluminum, plastics, and glass, which is restricting the growth of packaging market. Similarly, fluctuations in crude oil directly affect the cost of plastic resins, which is impacting flexible packaging and PET bottles. Transportation bottlenecks and geopolitical tensions have further increased lead times and procurement challenges for packaging manufacturers. For companies operating on tight margins, these unpredictable cost swings reduce profitability and discourage long-term capital investments.

MARKET OPPORTUNITIES

Shift toward sustainable and circular packaging

The sustainability is opening vast opportunities for companies innovating in biodegradable, recyclable, and reusable packaging formats. Companies adopting compostable films, bio-based plastics, and refillable solutions are aligning with both consumer expectations and regulatory mandates. For instance, rising adoption of extended producer responsibility schemes across Asia and Europe incentivizes sustainable design. The consumer base, particularly younger demographics, actively prefers brands demonstrating eco-consciousness, making sustainable packaging a strategic differentiator.

Smart and digital packaging integration

Smart packaging technologies present a forward-looking opportunity, blending IoT, sensors, and data-driven features into traditional formats is also to set up new opportunities for the growth of packaging market. The International Telecommunication Union confirms that 5.4 billion people globally use the internet as of 2023, supporting digital-physical convergence. QR codes, NFC tags, and embedded freshness indicators enhance consumer engagement, supply chain transparency, and brand loyalty. For example, pharmaceutical packaging integrated with track-and-trace systems helps fight counterfeiting, a concern flagged by the World Health Organization, which states that one in ten medical products in low- and middle-income countries is substandard or falsified. Beyond pharmaceuticals, smart packaging supports food traceability, regulatory compliance, and personalized marketing.

MARKET CHALLENGES

Regulatory divergence and compliance complexity

The packaging market faces major challenges from fragmented regulatory landscapes, where requirements vary widely across countries is likely to hamper the growth of packaging market. The Organisation for Economic Co-operation and Development observes that regulatory divergence adds billions in trade costs annually, especially for sectors like packaging that intersect with food safety, health, and sustainability standards. Companies must navigate overlapping frameworks on recycling mandates, chemical safety restrictions, and labeling requirements, often leading to costly reformulations and re-certifications. For multinational firms, this complexity slows down product launches, while for smaller companies it acts as a market entry barrier.

Technological adoption and cost barriers for SMEs

Although advanced packaging solutions such as smart sensors, bioplastics, and automation are transforming the industry, adoption remains skewed toward large enterprises. According to the International Labour Organization, SMEs account for over 90% of businesses worldwide, yet they often lack access to capital and technology needed for transformation. For small-scale packaging manufacturers, high investment requirements in R&D, equipment, and workforce training pose significant barriers. Without modernization, SMEs risk exclusion from supply chains dominated by global brands demanding compliance with sustainability and traceability standards.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 3.98% |

| Segments Covered | By Packaging Type, Packaging Format, End-Use Industry, and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Amcor Limited, Mondi Group, Sealed Air Corporation, International Paper, Sonoco Group, WestRock Company, Berry Global Inc., Constantia Flexibles, Huhtamaki, and Coveris Holdings, and Others. |

SEGMENTAL ANALYSIS

By Packaging Type Insights

The plastic segment was accounted in holding 38.2% of the global packaging market share in 2024, with its widespread application in food and beverage packaging, where demand is supported by urban consumption and convenience needs. According to the Food and Agriculture Organization, global food losses reach 1.3 billion tonnes annually, much of it preventable with proper protective packaging, a role plastics fulfill efficiently by extending shelf life. Another driver is the lightweight nature of plastic compared to metal or glass, which reduces transportation costs and carbon emissions per unit shipped.

The paper and paperboard packaging segment is expected to grow with an expected CAGR of 5.6% from 2025 to 2033. According to the United Nations Environment Programme, 170 countries have pledged to significantly reduce plastic use by 2030, which is accelerating paper’s substitution role in retail, foodservice, and e-commerce. Consumers increasingly equate paper packaging with sustainability, creating competitive advantage for brands making the switch. Another accelerant is e-commerce, where corrugated cartons and paperboard dominate.

REGIONAL ANALYSIS

Asia Pacific Packaging Market Analysis

Asia-Pacific was the top performer of the global packaging market by occupying 42.3% of share in 2024, with the rapid industrialization and e-commerce growth. As per the United Nations, Asia will house 4.9 billion people by 2050, which is fueling rising demand for food, beverages, and pharmaceuticals, all heavily dependent on packaging. In China alone, the National Bureau of Statistics recorded that online retail sales of physical goods reached USD 1.8 trillion in 2023, which is directly boosting packaging demand.

North America Packaging Market Analysis

North America was positioned second by holding 24.2% of the global packaging market share in 2024 with its advanced retail systems and highly regulated food and pharma sectors. The U.S. Food and Drug Administration enforces stringent labeling and safety standards, compelling packaging innovation.

Europe Packaging Market Analysis

The market growth in Europe is likely to grow with sustainability and circular economy models. The European Commission has set a directive that all packaging on the EU market must be reusable or recyclable by 2030, which is driving rapid innovation in paperboard and bio-based plastics. Europe also has one of the world’s highest per-capita packaged food consumption levels, supported by its urbanized population.

Latin America Packaging Market Analysis

Latin America is likely to grow with rising middle-class consumption. Ait is expected that over 180 million Latin Americans joined the middle-income bracket between 2000 and 2020 that is leading to higher demand for packaged goods. Brazil’s thriving agribusiness and food exports also push the need for durable export-grade packaging.

Middle East & Africa Packaging Market Analysis

The Middle East & Africa packaging market growth is due to rising disposable incomes and expanding retail infrastructure. In the Middle East, fast-growing packaged food and beverage markets in Saudi Arabia and the UAE accelerate packaging demand. The World Health Organization has emphasized urban dietary shifts toward processed and packaged foods in Africa, further stimulating packaging requirements.

COMPETITIVE LANDSCAPE

KEY MARKET PLAYERS

Companies playing a dominating role in the global packaging market include

- Amcor Limited

- Mondi Group

- Sealed Air Corporation

- International Paper

- Sonoco Group

- WestRock Company

- Berry Global Inc.

- Constantia Flexibles

- Huhtamaki

- Coveris Holdings

TOP STRATEGIES USED BY KEY MARKET PLAYERS

Key players in the packaging market employ a combination of sustainability-driven innovation, strategic partnerships, and regional expansions to maintain competitive advantage. A leading strategy is the acceleration of eco-friendly packaging, as consumers and regulators intensify pressure on reducing single-use plastics. Amcor and Nippon Paper have heavily invested in recyclable and biodegradable solutions to cater to environmentally conscious markets. Another strategy is technological innovation, with Tetra Pak advancing smart packaging and renewable material integration to meet customer expectations. Companies also focus on expansion across high-growth markets in Asia-Pacific, where urbanization and e-commerce demand create strong opportunities. Mergers, acquisitions, and capacity expansions remain vital in strengthening regional supply chains and improving distribution efficiency.

COMPETITION OVERVIEW

The packaging market is highly competitive, characterized by a mix of multinational corporations and regional players vying for sustainability, innovation, and scalability. Companies are under mounting pressure to address global sustainability commitments while ensuring cost efficiency for customers. Amcor, Tetra Pak, and Nippon Paper exemplify global leaders with extensive investments in recyclable and renewable packaging, setting the pace for industry transformation. At the same time, regional manufacturers in Asia-Pacific are leveraging proximity to fast-growing markets to challenge incumbents with cost-competitive solutions.

TOP PLAYERS IN THE MARKET

- Amcor Plc plays a pivotal role in the Asia-Pacific packaging market through its extensive portfolio of flexible and rigid packaging solutions. The company focuses heavily on sustainable innovation, offering recyclable and bio-based packaging that caters to food, beverage, and healthcare sectors. Amcor has consistently invested in research facilities across Asia, enabling localized product development that aligns with evolving consumer expectations.

- Tetra Pak is a leading player in the Asia-Pacific packaging market, renowned for its dominance in carton-based packaging for beverages and dairy products. The company has significantly expanded in developing Asian economies, where rising milk and juice consumption fuels demand. Its focus on renewable materials has resonated strongly in regions with increasing sustainability regulations. In 2024, Tetra Pak launched paper-based straws in Southeast Asia, a step towards its goal of fully renewable packaging.

- Nippon Paper Industries has dominant role in the Asia-Pacific packaging market by advancing paper and paperboard packaging solutions. Leveraging Japan’s strong innovation culture, the company has accelerated the development of biodegradable and recyclable materials that respond to rising environmental concerns. Nippon Paper has expanded operations in China and Southeast Asia, particularly in corrugated and cartonboard segments tied to the growth of e-commerce. In late 2023, it announced the construction of a new paper packaging facility in Vietnam, aimed at supporting regional exports.

MARKET SEGMENTATION

This research report on the global packaging market has been segmented and sub-segmented based on packaging type, packaging format, end-use industry, and region.

By Packaging Type

- Plastic Packaging

- Paper Packaging

- Container Glass

- Metal Cans and Containers

By Packaging Format

- Rigid

- Flexible

By End-Use Industry

- Food

- Beverage

- Pharmaceuticals and Healthcare

- Personal Care and Cosmetics

- Industrial

- E-Commerce

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Frequently Asked Questions

1. What is the packaging market?

The packaging market refers to the industry that designs, produces, and supplies materials such as plastic, paper, glass, and metal used to protect, store.

2. What is driving the growth of the packaging market?

Growth is driven by rising e-commerce, increasing demand for convenience packaging, sustainability initiatives, and the expansion of the food & beverage and healthcare industries.

3. What are the main types of packaging materials?

The major packaging materials include plastic, paper, container glass, and metal cans/containers.

4. Which industries are the largest consumers of packaging?

Food, beverages, pharmaceuticals & healthcare, personal care & cosmetics, industrial, and e-commerce are the key end-use industries.

5. Which region leads the global packaging market?

Asia-Pacific leads due to strong industrial growth, population expansion, and high consumption in China and India.

6. What are the latest trends in the packaging market?

Key trends include smart packaging, eco-friendly designs, digital printing, lightweight materials, and personalized packaging.

7. What challenges does the packaging industry face?

Challenges include fluctuating raw material prices, strict regulatory standards, and environmental concerns over plastic waste.

8. Who are the major players in the packaging market?

Leading companies include Amcor Limited, Mondi Group, Sealed Air Corporation, International Paper, Sonoco, WestRock, Berry Global, Constantia Flexibles, Huhtamaki, and Coveris Holdings.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com