Global Beverage Packaging Market Size, Share, Trends, & Growth Forecast Report - Segmented By Material Type (Metal, Glass, Plastic, Paper & Paperboard), Packaging Type (Pouch, Cans, Bottles And Cartons), Product Type (Dairy Beverages, Alcoholic Beverages And Non-Alcoholic Beverages) And Region(North America, Europe, Asia-Pacific, Latin America, Middle East And Africa) - Global Industry Analysis, Size, Share, Growth, Trends And Forecast 2026 To 2034

Market Size, 2025

$171.6 BnMarket Estimate, 2026

$180.2 BnMarket Forecast, 2034

$266.4 BnCAGR, 2026–2034

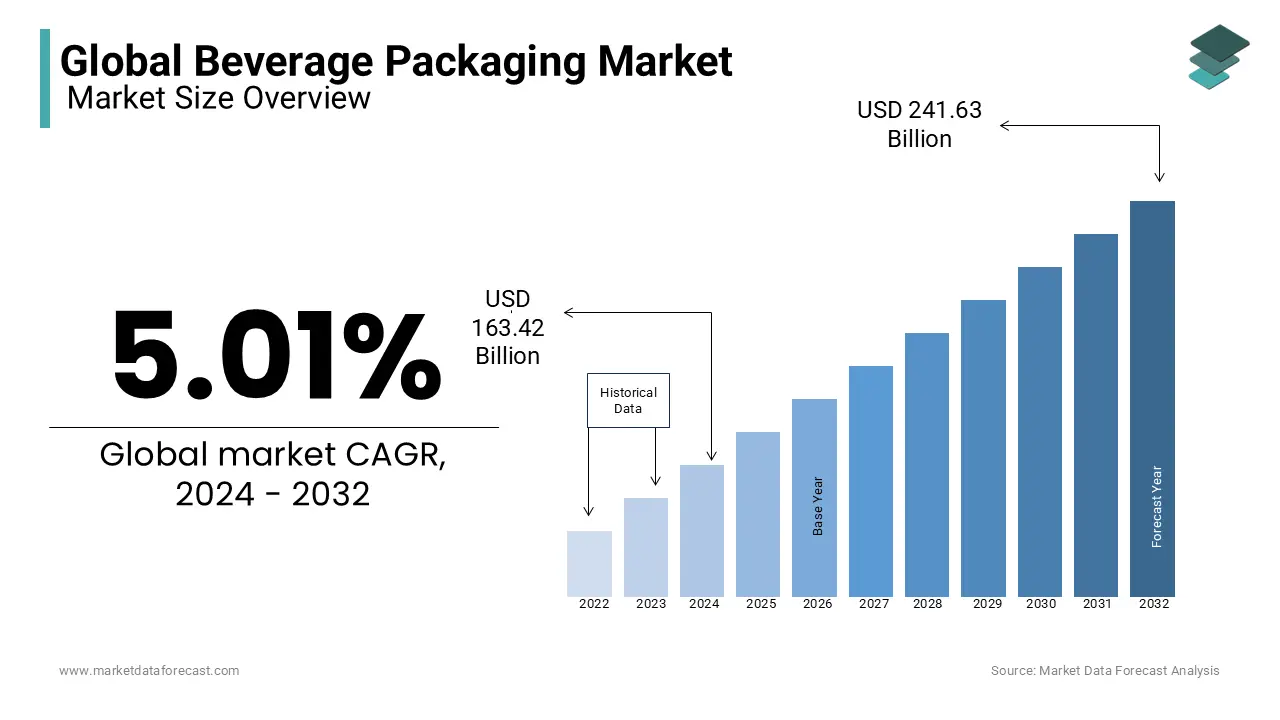

5.01%Global Beverage Packaging Market Size

The size of the global beverage packaging market was expected to be worth USD 171.61 billion in 2025 and is anticipated to be worth USD 266.46 billion by 2034, from USD 180.21 billion in 2026, growing at a CAGR of 5.01% during the forecast period.

Beverage packaging is the engineered material systems, predominantly aluminum, PET, glass, and paperboard composites, designed to preserve liquid integrity, ensure consumer safety, and communicate brand identity under dynamic logistical and regulatory conditions. Unlike generic containers, modern beverage packaging integrates barrier technologies, lightweighting architectures, and smart labeling to meet shelf-life, sustainability, and e-commerce durability benchmarks. As per the study, global beverage consumption was significant, each liter requiring primary packaging unit with defined oxygen transmission rates and UV resistance.

MARKET DRIVERS

Rising Demand for Functional RTD Beverages Driving Advanced Packaging Solutions

The global proliferation of ready-to-drink (RTD) formats, particularly functional beverages and cold-brew coffee, which require hermetic seals and light-blocking properties to preserve bioactive compounds, drives the growth of beverage packaging market. RTD functional beverages grew, with protein-enhanced and adaptogenic formulations demanding multilayer PET or aluminum cans with oxygen scavengers to prevent nutrient degradation. Simultaneously, in India, FSSAI's regulations for probiotics focus on the ingredients and labeling.

E-Commerce Logistics Requirements Accelerating Adoption of Durable Packaging

E-commerce logistics resilience, where packaging must survive drop-tests, compression loads, and variable humidity without leakage or label delamination, is also a key propellent for the expansion of beverage packaging market. As per the study, a percentage of online beverage returns were attributed to packaging failure during last-mile delivery, prompting Amazon to enforce ISTA 6-Amazon.com-SIOC certification for inbound beverage SKUs. In Southeast Asia, Lazada and Shopee require leak-proof certification for all liquid listings, accelerating adoption of induction-sealed aluminum closures and tamper-evident shrink bands across a portion of listed beverages.

MARKET RESTRAINTS

Regulatory Pressures on Recyclability and Material Compliance Constraining Market Growth

The tightening regulatory fragmentation around recyclability claims and material composition is constraining the growth of beverage packaging market. As per study, PET bottles must contain recycled content by 2030, yet only a portion of EU collection streams yield food-grade rPET, according to research. Simultaneously, California’s SB 54 mandates 65% plastic packaging recycling by 2032. This forces brands into costly redesigns. PepsiCo invested to remove carbon-black pigments from its LIFEWTR bottles to enable optical sorting, which compresses margins without guaranteeing collection infrastructure alignment.

Consumer Skepticism Toward Greenwashing and Functional Trade-Offs in Sustainable Packaging

Consumer skepticism toward greenwashed sustainable packaging, particularly when lightweighting compromises functionality, restrains the expansion of beverage packaging market. A share of consumers distrust recyclability claims on beverage packs unless certified by third parties. In Denmark, Coca-Cola's PlantBottle faced backlash after consumer complaints and an environmental group's report revealed the bottle, marketed as bio-based, used petroleum-derived terephthalic acid (PTA) for 70% of its composition. Similarly, paperboard bottles with plastic liners, launched by Diageo and Carlsberg, were rejected by a portion of surveyed UK consumers, who perceived them as recycling theater rather than genuine circular solutions.

MARKET OPPORTUNITIES

Digital Watermarking and AI-Powered Sorting Unlocking Recycling Opportunities

The deployment of digital watermarking technologies like HolyGrail 2.0 to enable AI-powered sorting of multilayer and sleeved beverage containers at material recovery facilities creates new opportunities for the expansion of beverage packaging market. As per the research, deployments in Austria and the Netherlands increased accurate sorting of complex PET bottles, unlocking food-grade rPET yields previously deemed unattainable. Early adopters gain regulatory foresight and EPR cost advantages as the EU requires digital watermark adoption under its Packaging and Packaging Waste Regulation.

Expansion of Refillable and Returnable Systems Driving Circular Packaging Models

Refillable and returnable packaging systems gaining institutional traction in urban center is setting new opportunities for the growth of beverage packaging market. Coca-Cola's Universal Bottle initiative in Latin America is a real program that reduces SKU complexity and emissions. Simultaneously, Loop's partnerships with Kroger and Walgreens involved pilot programs for reusable packaging that included online delivery and in-store collection bins, validating consumer willingness to participate in circular models when convenience is engineered into the retail interface.

MARKET CHALLENGES

Rising Adoption of In-Home Beverage Systems Reducing Demand for Traditional Packaging

The accelerating substitution of single-serve formats by in-home beverage systems such as soda makers and cold-brew dispensers, which bypass traditional packaging entirely, slows down the expansion of beverage packaging market. As per the study, U.S. households using SodaStream or Keurig Kold grew, reducing single-use bottle purchases. According to research, a portion of Nespresso Vertuo users in Europe have discontinued purchasing bottled cold brew, translating to millions of fewer PET units annually. Thus, traditional packagers risk structural volume erosion despite sustainability investments due to the absence of integration into home appliance ecosystems or offering branded cartridge refills.

Geopolitical Volatility in Aluminum and PET Resin Supply Chains Constraining Market Growth

The geopolitical fragility of aluminum and resin supply chains for specialty alloys and barrier-grade PET, is a barrier impacting the beverage packaging market. As per the research, a portion of global rolled aluminum for cans originates from China and Russia, both subject to export controls and carbon border tariffs. In 2023, the London Metal Exchange recorded a price spike in can sheet alloy after Russia restricted exports to the EU. Simultaneously, as per study, high IV PET resin which is important for carbonated drinks faced several weeks lead times in North America due to Texas freeze-related cracker outages. This forces brands into spot procurement at inflated costs or reformulation compromises that risk product integrity under pressure or UV exposure.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.01% |

| Segments Covered | By Material Type, Packaging Type, Product Type, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC; PESTLE Analysis. Porter’s Five Forces Analysis, Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Saint-Gobain S.A., Tetra Laval International S.A., Stora Enso Oyj, Owens-Illinois, Inc, Crown Holdings, Inc, Rexam PLC, Ball Corporation, Mondi PLC, Amcor Limited, Reynolds Group Holdings Limited, Alcoa Inc and Others. |

SEGMENTAL ANALYSIS

By Material Type Insights

The plastic segment dominated the beverage packaging market by accounting for 47.5% of share in 2025. The prominence of plastic segment is driven by its unmatched balance of clarity, carbonation retention, lightweighting, and moldability for ergonomic shapes. E-commerce compatibility also drives the growth of plastic segment. as per research, a percentage of compliant beverage SKUs utilize PET due to crush resistance and label adhesion under variable humidity. In India, PET bottle consumption is billions of units and is growing annually, as per the study, which is fueled by RTD tea and functional water brands requiring UV-blocking layers. Simultaneously, Coca-Cola’s Universal Lightweighting initiative reduced average bottle weight without compromising top-load strength, validating structural efficiency as a competitive lever.

The paper & paperboard segment is predicted to witness the highest CAGR of 8.6% over the forecast period due to regulatory bans on single-use plastics and consumer demand for fiber-based alternatives. The EU’s Single-Use Plastics Directive accelerated adoption of paperboard bottles with bio-based liners for juices and dairy, consumption grew, according to study. In the U.S., Starbucks’ rollout of paperboard cold cups with PLA coating displaced plastic lids, as per research. Simultaneously, Johnnie Walker paper-based bottles, announced in September 2025, were part of a limited on-trade trial, demonstrating scalability for premium spirits despite barrier limitations against ethanol permeation.

By Packaging Type Insights

The bottles segment was the largest segment in the beverage packaging market by capturing 58.5% share in 2025. Their versatility across carbonated soft drinks, water, dairy, and RTD coffee has majorly contributed to the growth of bottle segment in the global market. Moreover, resealability and brand visibility are further growth factors of the bottles segment. According to study, a portion of consumers choose beverages based on bottle shape and label real estate. In Southeast Asia, PET bottle usage for flavored water grew, as per research, driven by on-the-go consumption and Instagrammable transparent designs. Simultaneously, Coca-Cola’s contour glass bottle—protected under international design patents—remains the recognized packaging icon globally, which supports emotional loyalty. Light weighting innovations further entrench dominance by reducing logistics emissions without sacrificing rigidity.

The cans segment is predicted to witness the highest CAGR of 9.2% during the forecast period owing to premiumization in craft beer, RTD cocktails, and functional beverages requiring complete light and oxygen barriers. As per study, a percentage of craft beer launches opted for 355ml aluminum cans due to flavor preservation and portability. White Claw’s expansion into 16-oz formats consumed large number of cans, as per research. The format’s infinite recyclability and compatibility with digital printing for limited editions further accelerate adoption among Gen Z-targeted brands.

By Product Type Insights

The non-alcoholic beverages was the leading segment by capturing 63.7% of the beverage packaging market share in 2025. Water, carbonated soft drinks, and the explosive growth of functional and plant-based RTD categories are the factor attributed to the dominance of non-alcoholic beverages segment in the global market. Hydration culture and health consciousness are primary accelerants. Like, according to study, a portion of U.S. consumers now prioritize zero-sugar or vitamin-enhanced labels, which demands UV-blocking and oxygen-scavenging packs. In India, Bisleri and Paper Boat collectively added large number of PET units to meet demand for flavored and electrolyte water, as per research. Hence, all these validating technical packaging as a functional ingredient enabler.

The alcoholic beverages segment is estimated to register the fastest CAGR of 7.8% from 2026 to 2034 due to premium canned cocktails, hard seltzers, and ready-to-drink formats targeting convenience and portion control. As per the study, RTD cocktail volume surged, with a share packaged in slim 250ml aluminum cans for single-serve portability. Simultaneously, Brazil’s caipirinha-in-a-can trend consumed significant units, as per study, which validats local flavor authenticity in globally scalable formats. Premiumization drives adoption of tactile finishes, embossed cans, and NFC-enabled labels for authenticity verification.

REGIONAL ANALYSIS

Asia Pacific Market Analysis

Asia Pacific beverage packaging market was the largest contributor by holding 30.3% of share in 2025, which was propelled by India’s RTD boom and China’s e-commerce packaging resilience. India added billions of PET units, as per stuyd, driven by Paper Boat’s ethnic beverages and Tata Gluco+ in functional water. China’s JD.com and Alibaba enforced ISTA 6-SIOC certification for all inbound beverages by triggering ribbed-base PET adoption across a percentage of SKUs, as per study. Southeast Asia’s street-vendor culture accelerated adoption of tamper-evident shrink bands and induction-sealed aluminum closures, particularly in Indonesia and Vietnam, where beverage spoilage complaints dropped.

North America Market Analysis

North America is the second-largest in the beverage packaging market and accounted for 24.5% of the global market share in 2025. The growth of North America in the global market is primarily driven by RTD innovation and e-commerce logistics mandates. The region’s position is defined by regulatory foresight. California’s SB 54 compelled a portion of beverage brands to redesign for recyclability, as per research. Coca-Cola North America reduced virgin PET use through lightweighting and sleeve-free labeling. Simultaneously, Amazon’s Frustration-Free Packaging certification drove a share of beverage SKUs to adopt crush-resistant PET or aluminum cans, according to study. Craft beer canning surged, while PepsiCo’s LIFEWTR transitioned to clear rPET to enable optical sorting, which validats material circularity as a procurement criterion.

Latin America Market Analysis

Latin America grew steadily in the beverage packaging market. Brazil and Mexico are driving consumption through RTD expansion and returnable glass systems. Brazil’s caipirinha-in-a-can segment grew, consuming large number of aluminum units. Mexico’s Coca-Cola FEMSA participates in initiatives involving returnable glass bottles, but its specific bottle retrieval programs that involve OXXO convenience stores are focused on recycling. One such program uses biorecycling machines in OXXO stores for collecting PET and aluminum, rather than retrieving returnable glass bottles for reuse. Rising dairy consumption in Colombia and Peru accelerated adoption of aseptic cartons.

Europe Market Analysis

Europe stands as another key region in the beverage packaging market. The growth of Europe in the global market is propelled by Extended Producer Responsibility schemes and fiber-based substitution. Germany’s system diverted large metric tons of beverage packaging from landfill, as per study, which incentivises mono-material design. The EU’s Packaging and Packaging Waste Regulation mandated digital watermarking trials, HolyGrail 2.0 increased sorting accuracy in Dutch facilities, according to research. Simultaneously, Carlsberg’s Snap Pack eliminated metric tons of plastic rings annually, while Diageo’s paper Johnnie Walker bottle entered several markets. France’s anti-waste law banned opaque PET for water, which forces brands into clear rPET. This validates regulatory tailwinds as innovation drives.

Middle East and Africa Market Analysis

The Middle East & Africa is likely to grow in beverage packaging market, with Gulf premiumization and African sachet innovation shaping regional dynamics. Saudi Arabia’s NEOM project promoted returnable aluminum packaging for all on-site beverages by consuming millions of units, as per study. Egypt has undertaken national and local campaigns to reduce single-use plastics. Simultaneously, the Nigerian PureWater industry use 500ml sachets, which is primarily made of low-density polyethylene (LDPE) for affordability.

COMPETITION OVERVIEW

The beverage packaging market exhibits high fragmentation with intense rivalry pivoting on sustainability credentials, regulatory foresight, and e-commerce compatibility rather than cost alone. European and North American players emphasize circularity and digital traceability, while Asian producers leverage scale and rapid prototyping for RTD formats. Innovation centers on solving application-specific pain points, oxygen scavenging for functional beverages, tactile finishes for premium spirits, and crush resistance for last-mile delivery. New entrants face prohibitive barriers due to capital-intensive extrusion lines and stringent migration certifications.

Key Market Players

A few of the dominating players in the global beverage packaging market include

- Saint-Gobain S.A

- Tetra Laval International S.A

- Stora Enso Oyj

- Owens-Illinois, Inc

- Crown Holdings, Inc

- Rexam PLC

- Ball Corporation

- Mondi PLC

- Amcor Limited

- Reynolds Group Holdings Limited

- Alcoa Inc

- Others

Top Strategies Used By Key Market Participants

Leading beverage packaging producers prioritize circular design, developing mono-material and digitally watermarked structures to enhance sortability and recyclate purity. They vertically integrate recycling infrastructure to secure food-grade rPET and aluminum scrap, reducing dependency on volatile commodity markets. Strategic partnerships with FMCG giants embed packaging innovation into product launch roadmaps by ensuring co-engineered solutions for flavor preservation and e-commerce resilience. Companies deploy AI-driven leak detection and drop-test simulation to optimize wall thickness without compromising integrity. Export-focused players establish regional co-manufacturing hubs to tailor barrier layers and closure systems to local humidity, UV exposure, and regulatory thresholds.

Leading Players In The Market

Amcor plc

Amcor plc engineers high-performance, globally compliant beverage packaging across PET, aluminum, and specialty barrier films, serving carbonated drinks, dairy, and premium spirits with precision lightweighting and smart labeling. The company commissioned a rPET line. Amcor also partnered with Diageo to co-develop tactile aluminum cans with embossed regional motifs for Latin American RTD cocktails, which embeds cultural relevance into structural design.

Ball Corporation

Ball Corporation dominates aluminum can and bottle innovation, supplying global RTD, craft beer, and functional beverage brands with infinitely recyclable, digitally printable, and nitrogen-compatible vessels. It also signed supply agreement with White Claw to support number of unit annual volume, which strengthens integration into high-growth and Gen Z-targeted beverage ecosystems.

Tetra Pak

Tetra Pak leverages aseptic carton technology to preserve dairy, plant-based, and juice beverages without refrigeration, combining fiber-based structures with precision filling systems. The company partnered with India’s Mother Dairy to deploy 500ml cartons for probiotic lassi, extending shelf life to several days without preservatives.

MARKET SEGMENTATION

This research report on the global beverage packaging market has been segmented and sub-segmented based on material type, packaging type, product type, and region.

By Material type

- Metal

- Glass

- Plastic

- Paper & Paperboard

By Packaging Type

- Pouch

- Cans

- Bottles

- Cartons

By Product Type

- Dairy beverages

- Alcoholic beverages

- Non-alcoholic beverages

By Region

- North America

- Europe

- The Asia Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

1. What factors are driving the growth of the beverage packaging market?

Market growth is driven by rising beverage consumption, increasing demand for convenient packaging, growing urbanization, and advancements in sustainable packaging technologies.

2. What are the major types of beverage packaging materials?

Major packaging materials include plastic, glass, metal, paperboard, and flexible packaging materials.

3. Which beverage segment contributes significantly to the packaging market?

Carbonated soft drinks, bottled water, alcoholic beverages, dairy beverages, and ready-to-drink beverages are major contributors to the market.

4. What are the major packaging formats used in the beverage industry?

Common packaging formats include bottles, cans, cartons, pouches, and containers.

5. Why is sustainable packaging gaining importance in the beverage market?

Sustainable packaging helps reduce environmental impact, supports recycling initiatives, and meets increasing consumer demand for eco-friendly products.

6. What role does technology play in beverage packaging?

Technology supports smart packaging, lightweight materials, improved barrier protection, and automation in packaging production processes.

7. What are the major challenges faced by the beverage packaging market?

Challenges include fluctuating raw material prices, environmental concerns regarding plastic waste, and strict packaging regulations.

8. Which distribution channels are commonly used for beverage packaging products?

Beverage packaging products are distributed through direct supply contracts, wholesalers, distributors, and online procurement channels.

9. Who are the key players in the beverage packaging market?

Major companies include Amcor plc, Ball Corporation, Crown Holdings Inc., Tetra Pak, Berry Global Inc., and Ardagh Group.

10. What is the future outlook for the beverage packaging market?

The market is expected to grow steadily due to increasing beverage demand, rising sustainability initiatives, and innovations in smart and recyclable packaging solutions.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com