Global Alcoholic Beverages Market Size, Share, Trends & Growth Forecast Report Segmented By Type (Beer, Wine, And Spirit), Packaging (Glass Bottles, Tin And Plastic Bottles), Sales Channel (Specialty Stores, Online Retailers, Hotels/Bars/Restaurants, And Convenience Stores), And Region (North America, Europe, Asia Pacific, Latin America, And Middle East & Africa) - Global Industry Analysis, Size, Share, Growth, Trends And Forecast 2026 To 2034

Global Alcoholic Beverages Market Size

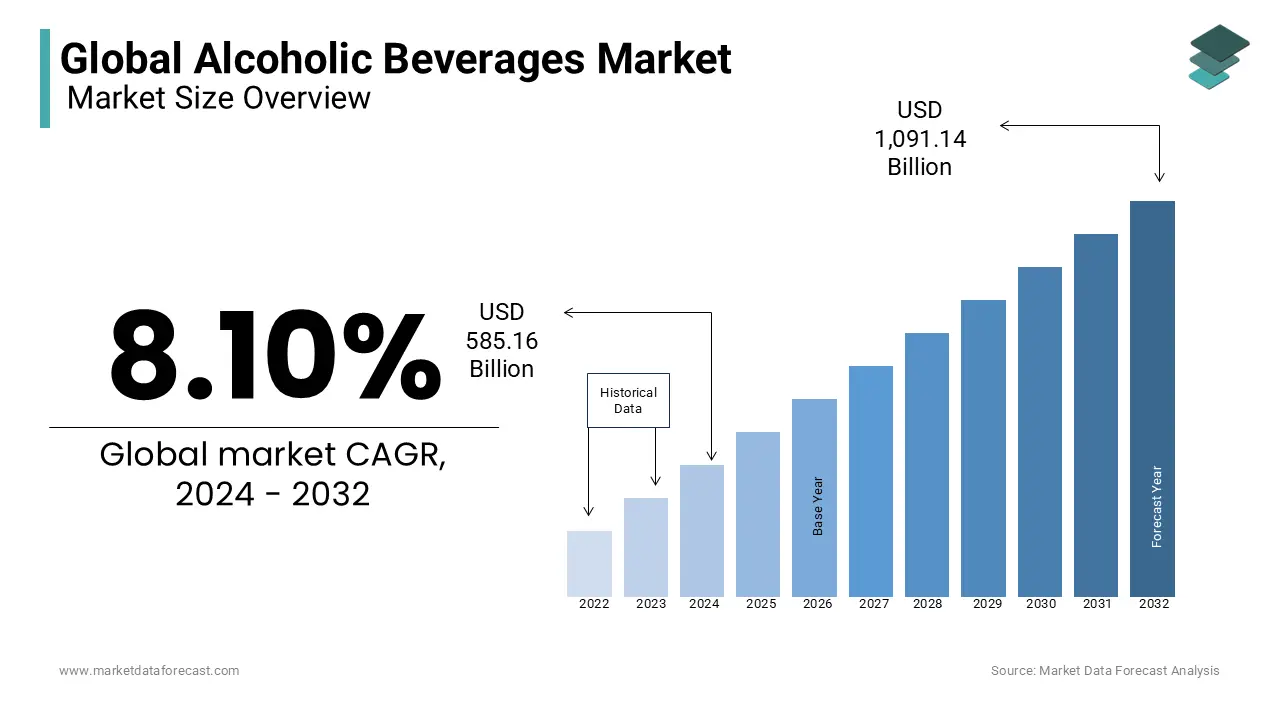

The size of the global alcoholic beverages market is expected to be worth USD 632.56 billion in 2025 and is anticipated to be worth USD 1,275.07 billion by 2034 from USD 683.80 billion in 2026, growing at a CAGR of 8.10% during the forecast period.

The alcoholic beverages are fermented and distilled products, including beer, wine, spirits, and ready-to-drink cocktails that serve as central elements in social interactions and cultural traditions worldwide. According to the World Health Organization, global alcohol consumption stands at approximately 5.5 liters of pure alcohol per person aged 15 years or older, reflecting deep-rooted drinking habits across diverse demographics. In Europe, where wine culture is deeply entrenched, the International Organisation of Vine and Wine reports that the continent accounts for nearly 45% of global wine production, underscoring its regional significance. Conversely, the Asia Pacific region is witnessing rapid growth in beer and spirits consumption driven by rising disposable incomes and urbanization. Regulatory bodies, such as the European Commission and the United States Alcohol and Tobacco Tax and Trade Bureau, enforce strict labeling and advertising standards to mitigate public health risks.

MARKET DRIVERS

Rising Disposable Income and Premiumization Trends in Emerging Economies

The expansion of the middle class in emerging economies is fueling demand for premium and super premium products, as disposable incomes rise, which is one of the major factors boosting the growth of the alcoholic beverages market. Consumers in countries such as China, India, and Brazil are shifting from traditional local brews to international branded spirits and wines, seeking status symbols and enhanced sensory experiences. This economic empowerment allows for greater expenditure on leisure and luxury goods, including high-quality alcoholic beverages. The sales of premium spirits in the Asia Pacific have outpaced volume growth by reflecting a clear preference for quality over quantity. Younger consumers in these regions are particularly influenced by global trends and digital marketing, driving demand for craft beers, single malt whiskies, and artisanal gins. The aspiration to align with global lifestyle standards encourages experimentation with new categories and flavors. Furthermore, the proliferation of modern retail channels and e-commerce platforms has improved access to a wider variety of premium products, removing geographical barriers.

Social Cultural Integration and Hospitality Sector Recovery

The deep integration of alcoholic beverages into social and cultural rituals globally continues to drive consistent demand that is further amplified by the robust recovery of the hospitality and tourism sectors. The social and cultural integration and hospitality sector recovery is. Alcohol remains a staple at celebrations, business gatherings, and dining experiences, creating a resilient baseline for consumption. The reopening of bars, restaurants, and nightclubs post-pandemic has led to a surge in on-premise consumption for cocktails and draft beers, which rely on social settings. In regions like Europe and North America, the culture of pub crawling and wine tasting tours attracts millions of tourists annually, supporting local producers and distributors. The rise of experiential dining, where beverage pairing is central to the culinary experience, has elevated the importance of curated alcohol selections. Additionally, the normalization of moderate drinking as part of a balanced lifestyle in many cultures sustains regular purchase patterns. Social media platforms further reinforce this by showcasing drinking trends and venue experiences, influencing consumer behavior, and driving foot traffic to hospitality venues.

MARKET RESTRAINTS

Stringent Government Regulations and High Taxation Policies

The stringent government regulations and high taxation policies are increasing operational costs and suppressing consumer demand, which is hindering the growth of the alcoholic beverages market. Governments worldwide impose excise duties, value-added taxes, and specific alcohol levies to generate revenue and discourage excessive consumption due to public health concerns. The alcohol taxes account for a significant portion of retail prices in many countries, with some nations imposing rates exceeding 50% of the final price. These fiscal measures reduce affordability for lower-income demographics and encourage the growth of illicit trade as consumers seek cheaper alternatives. The World Health Organization advocates for comprehensive bans on alcohol advertising, which several countries have implemented, hindering brand visibility and customer acquisition. Labeling requirements that mandate health warnings or calorie counts can also deter potential buyers by highlighting negative health associations. Compliance with these diverse and often changing regulatory frameworks requires substantial legal and administrative resources, diverting funds from innovation and expansion.

Growing Health Consciousness and Shift Toward Sobriety

The growing global emphasis on health and wellness, as consumers increasingly adopt sober curious lifestyles and reduce alcohol intake, is also hampering the growth of the alcoholic beverages market. Awareness of the adverse health effects of alcohol, including liver disease, cancer risk, and mental health issues, has prompted many individuals to cut back or abstain completely. This shift is particularly pronounced among millennials and Generation Z, who prioritize physical and mental health over traditional social drinking norms. The rise of functional beverages and non-alcoholic alternatives offers competitive substitutes that provide social inclusion without the physiological drawbacks. Retailers are responding by expanding their non-alcoholic sections, which cannibalize sales from traditional beer and wine categories. Public health campaigns and medical advice further reinforce this trend by creating a cultural stigma around heavy drinking.

MARKET OPPORTUNITIES

Expansion of Low Alcohol and Non Alcoholic Beverage Segments

The rapid expansion of low alcohol and non-alcoholic beverages to capture health-conscious consumers and diversify revenue streams is setting up new opportunities for the expansion of the alcoholic beverages market. Major breweries and distilleries are investing heavily in research and development to create sophisticated non-alcoholic beers, wines, and spirits that mimic the taste and mouthfeel of their alcoholic counterparts without the intoxicating effects. Brands are leveraging advanced dealcoholization technologies, such as vacuum distillation and reverse osmosis, to preserve flavor profiles by appealing to consumers who wish to participate in social drinking rituals without consuming alcohol. This trend aligns with broader wellness movements and allows companies to retain customers who are reducing their intake rather than leaving the brand entirely. Marketing these products as inclusive options for drivers, pregnant women, and health enthusiasts expands the total addressable market. Retailers are dedicating more shelf space to these innovations, recognizing their high growth potential.

Digital Direct to Consumer Sales and E-Commerce Integration

The integration of digital direct-to-consumer sales channels to bypass traditional distribution bottlenecks and engage directly with customers is also expected to boost new opportunities for the growth of the alcoholic beverages market. The acceleration of e-commerce adoption during the pandemic has normalized online alcohol purchases, with many consumers preferring the convenience of home delivery. The online alcohol sales have seen sustained growth, with projections indicating that digital channels will account for an increasing share of total beverage revenue in the coming years. Brands are utilizing subscription models, personalized recommendations, and virtual tasting events to build loyalty and gather valuable consumer data. This direct interaction allows for higher margins by eliminating intermediary markups and provides insights into purchasing behavior that inform product development. Regulatory changes in various jurisdictions are gradually easing restrictions on online alcohol sales, facilitating broader market access. Social commerce features on platforms like Instagram and TikTok enable seamless purchasing through influencer endorsements and targeted ads. This digital transformation not only enhances customer experience but also creates new revenue streams and strengthens brand resilience against supply chain disruptions in traditional retail networks, positioning early adopters for long-term competitive advantage.

MARKET CHALLENGES

Supply Chain Disruptions and Raw Material Volatility

The supply chain disruptions and raw material volatility, by affecting production consistency and profit margins, are a major challenge for the growth of the alcoholic beverages market. The industry relies heavily on agricultural inputs such as barley, hops, grapes, and sugarcane, which are susceptible to climate change, extreme weather events, and geopolitical instability. According to the Food and Agriculture Organization, climate variability has led to unpredictable harvest yields and quality fluctuations, forcing producers to source materials from alternative regions at higher costs. Energy prices, which are for brewing, distilling, and packaging processes, have also experienced sharp increases, exacerbating operational expenses. Logistics bottlenecks, including port congestion and transportation shortages, delay the movement of finished goods and raw materials, leading to inventory imbalances and stockouts. These disruptions compel companies to hold larger safety stocks, tying up capital and increasing storage costs. Additionally, the scarcity of glass and aluminum for packaging has driven up material costs by forcing price increases that may dampen consumer demand. Managing these complexities requires agile supply chain strategies and diversified sourcing, which are difficult to implement quickly.

Illicit Trade and Counterfeit Product Proliferation

The proliferation of illicit trade and counterfeit products, undermining brand integrity and causing significant revenue losses, is another challenge for the growth of the alcoholic beverages market. Illicit alcohol, which includes untaxed smuggled goods and fake products made with unsafe ingredients, competes unfairly with legitimate brands by offering lower prices. The illicit alcohol market accounts for billions of dollars in lost tax revenue globally and poses serious health risks to consumers due to contamination with methanol and other toxic substances. Counterfeit products damage brand reputation by delivering inferior quality experiences, leading to consumer distrust. Combating this issue requires substantial investment in security technologies such as holographic labels, blockchain tracking, and consumer education campaigns. However, the sheer scale of the informal market makes enforcement difficult, particularly in regions with weak regulatory oversight. Legitimate manufacturers face an uneven playing field as they bear the burden of compliance and taxation while illicit operators do not. This disparity discourages investment in quality and innovation. Furthermore, the presence of cheap illicit alcohol can distort market data and hinder accurate demand forecasting.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 8.10% |

| Segments Covered | By Type, Distribution Channel, Packaging Type, & Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC; PESTLE Analysis. Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Bacardi Limited, Beam Suntory Inc, Boston Beer, Brown-Forman, Constellation Brands, Anheuser-Busch InBev SA/NV, Constellation Brands Inc, Heineken Holding NV, Asahi Breweries Ltd, Accolade Wines Ltd, Diageo Plc, Carlsberg A/S, Molson Coors Brewing Co, SABMiller Ltd, Pernod Ricard SA, United Spirits Ltd, Thai Beverage Public Co., Ltd, Treasury Wine Estates, Tsingtao Brewery Co. Ltd, Rémy Cointreau SA, Wine Group, and China Resources Beer Company Limited |

SEGMENTAL ANALYSIS

By Type Insights

The beer segment was the largest by holding 43.2% of the global alcoholic beverages market share in 2025 due to its universal appeal, affordability, and deep entrenchment in social and cultural traditions across diverse demographics. It is the most widely consumed alcoholic beverage globally, favored for its lower alcohol content, which allows for prolonged social consumption without immediate intoxication. The versatility of beer, ranging from light lagers to dark stouts, caters to varied taste preferences, making it a staple at sporting events, festivals, and casual gatherings. In regions like Europe and North America, beer gardens and pubs serve as central community hubs, reinforcing habitual consumption. The relatively low price point compared to spirits and wine makes it accessible to a broader consumer base, including younger adults entering the legal drinking age. Furthermore, the proliferation of craft breweries has revitalized interest in beer, offering unique flavors and local identities that resonate with consumers seeking authenticity.

Based on type, the beer segment dominates the global alcoholic beverages market growth during the forecast period. Beer is treated as the most popular alcoholic beverage in the world, containing between 4 and 7 percent alcohol. Brew sales are also being driven by an increase in demand for craft beer. Beer's high silicon content may aid in the development of stronger bones. Dietary silicon in the soluble form of orthosilicic acid (OSA) may be beneficial to bone and connective tissue growth and development, as well as lowering the risk of osteoporosis, a bone-thinning disease. On the other hand, Wine, which contains 6-20 percent alcohol, is the second largest segment after beer, and spirits include 40-80 percent alcohol.

The spirits segment is likely to register the fastest CAGR of 5.2% from 2026 to 2034 with a global shift toward premiumization and the rising popularity of mixology culture. Consumers are moving away from volume consumption toward quality experiences, favoring aged whiskies, small batch gins, and artisanal tequilas. According to the study, the premium and super premium spirits categories are outpacing standard segments, with value growth significantly exceeding volume growth. The cocktail renaissance, fueled by social media and television shows, has educated consumers about complex spirit profiles and preparation techniques, driving demand for high-quality base spirits. Bars and restaurants are expanding their spirits menus, offering curated tasting flights and signature cocktails that highlight specific brands. This trend is particularly strong among millennials and Generation Z, who view spirits as a form of self-expression and status. The perception of spirits as a sophisticated choice for special occasions and gifting further boosts sales. Additionally, the flexibility of spirits in mixing allows for creative experimentation, keeping the category dynamic and engaging.

By Packaging Insights

The glass bottles segment accounted in holding 39.2% of the alcoholic beverages packaging market share in 2025 due to their superior ability to preserve product quality, flavor integrity, and premium brand perception. Glass is inert and impermeable, ensuring that the taste and aroma of wine, spirits, and premium beers remain unchanged over time. This chemical stability is crucial for aged products like whisky and wine, where long-term storage is common. Furthermore, glass conveys a sense of luxury and tradition by aligning with the premium positioning of many alcoholic brands. The weight and clarity of glass bottles enhance the visual appeal of the product on shelves, influencing consumer purchase decisions. High-end brands rely on distinctive bottle shapes and designs to differentiate themselves, using glass as a canvas for branding. The recyclability of glass also appeals to environmentally conscious consumers, as it can be recycled indefinitely without loss of quality.

The tin cans segment is projected to grow at a CAGR of 8.5% during the forecast period, with its convenience, portability, and sustainability advantages. Cans are lightweight, shatterproof, and easy to transport, making them ideal for outdoor activities, festivals, and on-the-go consumption. The aluminum cans have a recycling rate of nearly 50% in the United States, significantly higher than glass or plastic, appealing to environmentally aware consumers. The compact size of cans allows for efficient storage and transportation, reducing logistics costs and carbon emissions. Brands are increasingly launching ready-to-drink cocktails, hard seltzers, and craft beers in cans to cater to younger demographics who prioritize convenience and mobility. The ability to seal cans tightly preserves carbonation and freshness, ensuring consistent quality. Additionally, cans cool down faster than glass bottles, enhancing the drinking experience in warm weather. The versatility of can printing allows for vibrant and eye-catching designs that stand out in retail environments.

By Sales Channel Insights

The hotels, bars, and restaurants segment was the largest by capturing alcoholic beverages, driven by the inherent link between alcohol consumption and social dining or entertainment experiences. On-premise consumption allows consumers to enjoy professionally prepared cocktails, curated wine lists, and draft beers in a controlled and atmospheric setting. According to the National Restaurant Association, on-premise sales account for a significant portion of total alcohol revenue, as consumers are willing to pay a premium for the service, ambiance, and expertise provided by hospitality venues. Bars and restaurants serve as social hubs where friends and colleagues gather, fostering habitual consumption and brand discovery. The rise of craft cocktail bars and wine bars has elevated the status of alcoholic beverages, turning them into focal points of culinary experiences. Hospitality venues also benefit from exclusive partnerships with brands, offering limited-edition products that drive foot traffic. The ability to sample different varieties before purchasing encourages experimentation and loyalty.

The online retailers are likely to grow at the fastest CAGR of 12.3% during the forecast period, with the digital convenience and expanded product accessibility. E-commerce platforms allow consumers to browse vast selections of alcoholic beverages from the comfort of their homes, overcoming geographical limitations and stock issues in physical stores. The ability to compare prices, read reviews, and access detailed product information empowers consumers to make informed decisions. Online retailers often offer exclusive deals and bundles that are not available in brick-and-mortar stores, attracting price-sensitive shoppers. The integration of fast delivery services ensures that products arrive quickly, meeting the demand for immediacy. During periods of restricted mobility, such as the pandemic, online channels became essential for maintaining supply and accelerating adoption rates.

REGIONAL ANALYSIS

North America Alcoholic Beverages Market Analysis

North America was the top performer of the global alcoholic beverages market by holding 44.3% of the share in 2025, with a premiumization and regulatory evolution. The premium and super premium spirits have seen consistent double-digit growth by reflecting consumer preference for quality over quantity. Canada also contributes substantially, with a growing interest in local craft breweries and indigenous spirits. The region is witnessing a shift toward health-conscious options, with low alcohol and non-alcoholic beverages gaining traction. Regulatory frameworks vary by state and province, influencing distribution models and taxation. The rise of direct-to-consumer shipping laws in several US states has boosted online sales and small producer visibility. Economic stability and high disposable incomes support sustained spending on premium products.

Europe Alcoholic Beverages Market Analysis

Europe alcoholic beverages market growth held 32.4% of the share in 2025. Countries like France, Italy, and Spain are leading wine producers, while Germany and the United Kingdom are major contributors. The region is experiencing a decline in overall volume consumption due to health awareness and demographic changes, but value growth remains strong due to premiumization. Consumers are trading up to higher-quality wines and craft beers, seeking authentic and sustainable products. Regulatory pressures regarding health warnings and advertising restrictions are shaping marketing strategies.

Asia Pacific Alcoholic Beverages Market Analysis

Asia Pacific alcoholic beverages market growth is driven by rapid urbanization, rising disposable incomes, and a young demographic profile. China, India, and Japan are key markets, with China being the largest consumer of spirits globally, primarily baijiu. According to the analysis, the Asia Pacific region is expected to account for the majority of global alcohol volume growth in the coming decade. Beer consumption is surging in Southeast Asia, while wine is gaining popularity in urban centers as a symbol of sophistication. The middle class expansion is fueling demand for international brands and premium products. Local producers are innovating to compete with global giants, offering products tailored to regional tastes. Regulatory environments are evolving, with some countries liberalizing alcohol laws to boost tourism and tax revenue. Digital adoption is high, with e-commerce playing a significant role in distribution.

Latin America Alcoholic Beverages Market Analysis

Latin America's alcoholic beverages market growth is likely to grow with the strong local traditions and increasing integration into global trends. Brazil, Mexico, and Argentina are major contributors, with beer being the most consumed alcoholic beverage in the region. According to Euromonitor International, the Latin American market is seeing a rise in premium beer and spirits consumption as economic conditions stabilize in certain countries. Tequila and mezcal from Mexico have gained global acclaim, driving export growth and domestic pride. Wine production in Argentina and Chile is renowned worldwide, supporting both local consumption and international trade. The region is witnessing a craft beverage revolution, with microbreweries and distilleries emerging in major cities. Social culture in Latin America places a high value on gatherings and celebrations, sustaining a steady demand for alcohol. However, economic volatility and inflation pose challenges to pricing and affordability.

Middle East And Africa Alcoholic Beverages Market Analysis

The Middle East and Africa alcoholic beverages market growth is anticipated to have significant opportunities in the coming years. South Africa, Nigeria, and Kenya are key markets in Africa, with beer and traditional brews dominating consumption. In the Middle East, consumption is restricted in many countries, but duty-free sales and tourism in hubs like Dubai and Bahrain drive significant revenue. The region is seeing growth in non alcoholic and low alcohol alternatives, catering to local preferences and regulatory constraints. International brands are entering the market through partnerships and localized marketing strategies. Economic development in Gulf countries is supporting demand for premium imported spirits and wines among expatriate and affluent local populations. Infrastructure improvements and retail expansion are improving access to alcoholic beverages in permissible areas.

COMPETITION OVERVIEW

The competition in the alcoholic beverages market is intense and characterized by a mix of multinational conglomerates and agile local producers vying for consumer attention and shelf space. Major players leverage their extensive distribution networks and marketing budgets to maintain dominance, while smaller craft brands differentiate themselves through unique flavors and authentic storytelling. Premiumization is a key battleground as companies compete to offer higher-quality and exclusive products that appeal to affluent consumers. Regulatory pressures regarding health warnings and taxation create a challenging operating environment that requires constant adaptation. The rise of non-alcoholic alternatives introduces new competitors from the soft drink industry, further fragmenting the market. Digital channels have lowered barriers to entry, allowing direct-to-consumer brands to gain traction quickly. Mergers and acquisitions are common strategies used to consolidate market power and access new technologies or regions.

KEY MARKET PLAYERS

A few major key players in the global alcoholic beverages market include

- Bacardi Limited

- Beam Suntory Inc

- Boston Beer

- Brown-Forman

- Constellation Brands

- Anheuser-Busch InBev SA/NV

- Constellation Brands Inc

- Heineken Holding NV

- Asahi Breweries Ltd

- Accolade Wines Ltd

- Diageo Plc

- Carlsberg A/S

- Molson Coors Brewing Co

- SABMiller Ltd

- Pernod Ricard SA

- United Spirits Ltd

- Thai Beverage Public Co., Ltd

- Treasury Wine Estates

- Tsingtao Brewery Co. Ltd

- Rémy Cointreau SA

- Wine Group

- China Resources Beer Company Limited

Top Strategies Used by Key Market Participants

Key players in the alcoholic beverages market primarily focus on premiumization and product diversification to drive value growth and attract discerning consumers. Companies invest heavily in acquiring craft brands and launching limited edition products to capture niche markets. Sustainability initiatives such as reducing carbon emissions and using recyclable packaging strengthen brand reputation and comply with regulations. Digital transformation through e-commerce platforms and data analytics enhances direct consumer engagement and personalization. Strategic partnerships with hospitality venues ensure visibility and promote experiential consumption. Expansion into emerging countries leverages rising disposable incomes and changing lifestyle trends. Responsible drinking campaigns mitigate regulatory risks and build public trust. Innovation in low and no alcohol segments addresses health concerns while retaining customers.

Leading Players in the Global Alcoholic Beverages Market

- Anheuser Busch InBev SA NV stands as a global leader in the alcoholic beverages market with a diverse portfolio spanning beer, spirits, and non alcoholic options. The company leverages its extensive distribution network to reach consumers in over one hundred countries. Recent actions include significant investments in sustainable brewing practices and water stewardship programs to reduce environmental impact. The company has expanded its craft beer offerings through strategic acquisitions of local breweries to cater to premiumization trends. Their commitment to responsible drinking campaigns strengthens brand reputation and regulatory compliance.

- Diageo plc contributes significantly to the global alcoholic beverages market through its premium spirits and beer brands, including Johnnie Walker and Guinness. The company focuses on luxury positioning and high-value growth strategies to capture affluent consumers. Recent initiatives involve expanding production capacity for tequila and American whiskey to meet rising global demand. Diageo has invested heavily in sustainability goals such as achieving net-zero emissions across its value chain. The company enhances consumer engagement through immersive brand experiences and digital marketing campaigns. Strategic partnerships with hospitality groups ensure prominent placement in key on-premise locations. Diageo also prioritizes diversity and inclusion within its workforce and supply chain.

- Heineken NV plays a pivotal role in the global alcoholic beverages market with a strong presence in beer and cider categories. The company emphasizes innovation and sustainability by launching low alcohol and non alcoholic variants to address health-conscious trends. Recent actions include the expansion of its small brewery network to support local craft beer movements. Heineken invests in renewable energy sources for its brewing operations to reduce its carbon footprint. The company utilizes advanced digital tools to optimize supply chain efficiency and enhance customer experience. Marketing campaigns focus on social connectivity and responsible enjoyment of beverages. Heineken also engages in community development projects to build strong local relationships.

MARKET SEGMENTATION

This research report on the global alcoholic beverages market has been segmented and sub-segmented based on type, distribution channel, packaging type, and region.

By Type

- Beer

- Wine

- Spirit

By Distribution Channel

- Supermarkets/Hypermarkets

- Online trade

- Convenience stores

- Others

By Packaging Type

- Glass bottles

- Plastic bottles

- Tins

- Others

By Region

- North America

- Middle East and Africa

- Europe

- Asia and the Pacific

- Latin America

Frequently Asked Questions

1. What is driving the growth of the Alcoholic Beverages Market?

Market growth is mainly driven by rising disposable income, expanding urban population, increasing demand for premium beverages, and evolving consumer preferences.

2. Which product segment dominates the Alcoholic Beverages Market?

Beer dominates the market due to its widespread global consumption and affordability compared to other alcoholic beverages.

3. Which region dominates the Alcoholic Beverages Market?

Asia Pacific holds the largest share of the global alcoholic beverages market due to the presence of a large consumer base and growing middle-class population.

4. What are the major applications of alcoholic beverages?

Alcoholic beverages are widely consumed in social gatherings, hospitality services, restaurants, bars, and events.

5. What trends are shaping the Alcoholic Beverages Market?

Key trends include increasing demand for craft beverages, flavored alcoholic drinks, premium spirits, and low-alcohol variants.

6. Which distribution channel dominates the market?

On-trade channels such as bars, pubs, restaurants, and clubs hold a significant share of the market.

7. What challenges are faced by the Alcoholic Beverages Market?

Stringent government regulations and rising health concerns related to alcohol consumption may restrain market growth.

8. Which packaging formats are widely used?

Bottles, cans, and kegs are commonly used packaging formats in the alcoholic beverages market.

9. How does premiumization impact market growth?

Consumers are shifting toward premium alcoholic beverages, creating growth opportunities for manufacturers.

10. What is the future outlook of the Alcoholic Beverages Market?

The market is expected to witness steady growth due to increasing product innovation and expanding e-commerce alcohol sales channels.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com