Global Rum Market Size, Share, Trends & Growth Forecast Report Segmented By Type (Golden, Dark, White, and Spiced), Distribution channel (On-trade and Off-trade) and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa), Industry Analysis From 2026 to 2034

Global Rum Market Summary

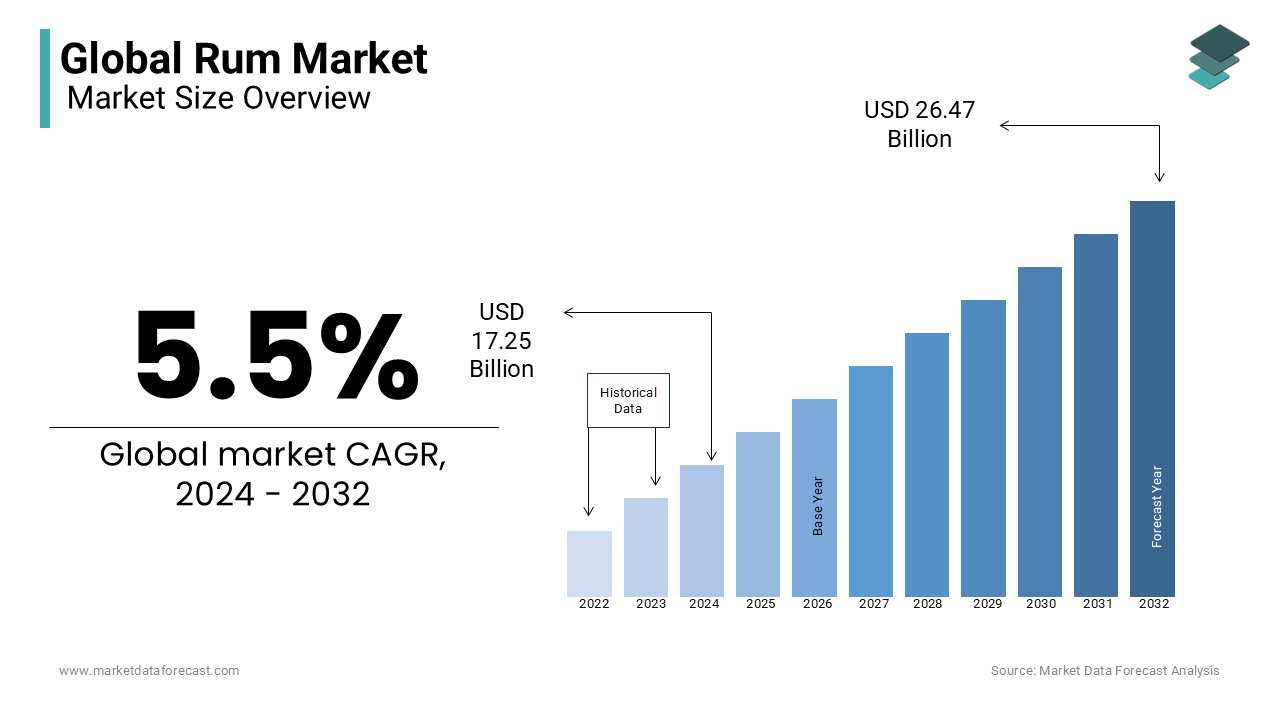

The global rum market was valued at USD 17.25 billion in 2024 and is projected to reach USD 27.93 billion by 2033, growing at a CAGR of 5.5% from 2025 to 2033. The growth of the global rum market is driven by rising consumer demand for premium and craft spirits, increasing popularity of cocktail culture, and expanding distribution through both on-trade and off-trade channels. Growing interest in flavored and spiced rums, coupled with innovation in packaging and marketing strategies, further supports market expansion.

Key Market Trends

- Increasing demand for premium and craft rum varieties.

- Rising popularity of cocktail culture and mixology trends.

- Expansion of e-commerce and retail distribution channels.

- Growing interest in flavored, spiced, and aged rums.

- Focus on sustainable sourcing and eco-friendly packaging by leading brands.

Segmental Insights

- Based on product type, the white rum segment dominated the global rum market in 2024, holding 42.3% share, supported by its wide use in cocktails and easy consumer acceptance.

- Based on distribution channel, the off-trade segment led the market in 2024, driven by sales through supermarkets, hypermarkets, retail stores, and e-commerce platforms.

Regional Insights

- North America was the top-performing region, capturing 38.3% share in 2024, driven by strong cocktail culture, premiumization trends, and a robust retail network.

- Europe shows steady demand, supported by rising consumption of spiced and flavored rum varieties.

- Asia-Pacific is expected to grow rapidly, fueled by changing consumer preferences, urbanization, and rising disposable incomes.

- Latin America remains a traditional market for rum, with increasing exports and premium product adoption.

- Middle East & Africa are emerging markets with gradual growth, supported by urban lifestyle changes and tourism.

Competitive Landscape

Key players in the global rum market include Bacardi Global Brands Ltd., Asahi Group Holdings Ltd., Demerara Distillers Ltd., Davide Campari-Milano Spa, Suntory Holdings Ltd., LT Group Inc., Diageo Plc, Pernod Ricard SA, Nova Scotia Spirit Co., and William Grant & Sons Ltd. These companies are focusing on premium product launches, innovative flavors, sustainability initiatives, and expanding distribution networks to strengthen their global presence.

Global Rum Market Size

The global rum market size was calculated to be USD 18.20 billion in 2025 and is anticipated to be worth USD 29.47 billion by 2034 from USD 19.20 billion in 2026, growing at a CAGR of 5.50% during the forecast period.

The rum is distilled alcoholic beverage derived primarily from sugarcane by-products such as molasses or sugarcane juice. The spirit varies widely in flavor, color, and aging process, ranging from light, unaged white rums to deeply aged, barrel-matured dark varieties. As of 2023, sugarcane remains one of the most widely cultivated crops globally, with over 190 million metric tons produced annually, primarily in Brazil, India, and Thailand, as per data from the Food and Agriculture Organization of the United Nations. Moreover, the International Organization of Legal Metrology notes that over 70 countries have established specific legal definitions for rum, reflecting its cultural and economic significance. The beverage is subject to varying regulatory frameworks governing alcohol content, aging duration, and labeling, which influence both domestic consumption and international trade dynamics.

MARKET DRIVERS

Rising Consumer Preference for Premium and Craft Spirits

The escalating consumer inclination toward premium and craft spirits, which is driving the growth of the global rum market. In recent years, affluent and younger demographics, particularly Millennials and Gen Z, have demonstrated a marked shift away from mass-market alcoholic beverages toward small-batch, artisanal, and aged rums that offer complex flavor profiles and transparent sourcing. This trend is mirrored in Europe, where the United Kingdom’s Wine and Spirit Trade Association recorded a 9% year-on-year rise in imports of aged Caribbean rums between 2021 and 2023, attributed largely to consumer demand for sipping rums suitable for neat consumption or sophisticated cocktails. Additionally, the global craft distillery movement has gained momentum, with over 2,000 independent rum producers now operating worldwide, as documented by the International Rum Conference in 2023.

Expansion of Rum Tourism and Cultural Heritage Promotion

The integration of rum production into cultural tourism has emerged as a powerful driver of market expansion in island nations where distilleries serve as both economic assets and heritage landmarks. Countries across the Caribbean and Latin America are increasingly leveraging their centuries-old rum-making traditions to attract tourists seeking immersive experiences, thereby boosting both direct sales and global brand recognition. These experiences often include historical narratives, plantation tours, and masterclasses, which is reinforcing emotional connections between consumers and the product. Furthermore, UNESCO’s recognition of certain rum-making traditions, such as Martinique’s AOC-labeled rhum agricole, that has elevated the spirit’s cultural stature by encouraging governments to invest in preservation and promotion.

MARKET RESTRAINTS

Stringent Alcohol Regulation and Taxation Policies

The increasingly stringent alcohol regulation and punitive taxation policies implemented across various jurisdictions is restraining the growth of global rum market. Governments worldwide are intensifying public health campaigns against excessive alcohol consumption, leading to restrictive legislative measures that directly impact rum accessibility and affordability. In India, for instance, several states including Bihar and Gujarat enforce complete alcohol prohibition, affecting over 150 million people, as reported by the Ministry of Health and Family Welfare in 2023. These fiscal policies disproportionately impact rum, which is often positioned as an affordable spirit in developing markets.

Volatility in Sugarcane Supply and Climate Vulnerability

The structural vulnerability due to its dependence on sugarcane, an agricultural commodity highly susceptible to climatic fluctuations and supply chain disruptions is hampering the growth of global rum market. Since rum is intrinsically tied to sugarcane or molasses output, any instability in cultivation directly affects production costs and availability. These supply shocks elevate input costs for distillers, particularly small-scale producers lacking hedging mechanisms. Moreover, climate projections from the Intergovernmental Panel on Climate Change indicate that by 2040, up to 30% of current sugarcane-growing regions in the tropics may face reduced suitability due to rising temperatures and erratic precipitation. This long-term environmental risk threatens the geographical concentration of rum production and necessitates costly adaptations such as irrigation infrastructure or alternative feedstocks.

MARKET OPPORTUNITIES

Growth of Ready-to-Drink (RTD) Rum-Based Beverages

The burgeoning ready-to-drink (RTD) alcoholic beverage rum market, particularly as consumer preferences shift toward convenience, portability, and lower-alcohol options is creating new opportunities for the growth of global rum market. RTD cocktails featuring rum as the base spirit are gaining traction, especially among urban professionals and younger drinkers who prioritize ease of consumption without compromising on flavor. The format’s appeal is further amplified by its alignment with health-conscious trends, as many RTDs now feature natural ingredients, reduced sugar, and alcohol content between 4% and 7% ABV.

Digital Engagement and Direct-to-Consumer (DTC) Sales Models

The digital transformation of alcohol retail has unlocked a significant opportunity for rum brands through direct-to-consumer (DTC) sales and online engagement platforms is also accelerating the growth of global rum market. In the United Kingdom, the off-trade spirits e-commerce market grew by 19% in 2022, with specialty rum retailers like Master of Malt reporting a 34% surge in sales of aged and limited-edition rums, as noted in their annual consumer behavior review.

MARKET CHALLENGES

Counterfeit and Illicit Rum Trade

The proliferation of counterfeit and illicit is undermining brand integrity, consumer safety, and tax compliance, which is limiting the growth of global rum market. Illicit distillation and falsified labeling are particularly rampant in regions with weak regulatory enforcement and high excise duties, where unlicensed producers offer cheaper alternatives to branded products. In India, the Federation of Indian Chambers of Commerce and Industry estimated that the unorganized sector accounts for nearly 40% of total spirit consumption, resulting in an annual revenue loss of USD 6.8 billion in excise duties alone. Moreover, global trade is affected, as counterfeit rum labeled as premium Caribbean exports has been intercepted in African and Middle Eastern markets, which is damaging regional reputations.

Shifting Social Attitudes Toward Alcohol Consumption

Evolving societal perceptions of alcohol consumption in urban and health-conscious demographics is also to hamper the growth of rum market. Increasing awareness of alcohol-related health risks, coupled with the rise of sobriety movements and mindful drinking, is altering consumption patterns across both developed and emerging economies. In response, a growing segment of consumers, especially Millennials and Gen Z, are adopting “sober curious” lifestyles or opting for alcohol-free alternatives. This cultural shift is mirrored in corporate environments and social spaces, where non-alcoholic options are increasingly normalized. While some rum brands have responded by launching alcohol-free infusions, the core market faces declining per capita consumption trends.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 5.5% |

| Segments Covered | By Product Type, Distribution Channel and Region |

| Various Analyses Covered | Global, Regional, and Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Bacardi Limited, Diageo plc, Pernod Ricard, Destilería Serrallés, Demerara Distillers Limited, Suntory Holdings Limited, Anheuser-Busch InBev, Remy Cointreau, Gruppo Campari, United Spirits Limited (USL), Maine Craft Distilling, Hampden Estate Rum, Mount Gay Distilleries Ltd. |

SEGMENTAL ANALYSIS

By Product Type Insights

The white rum segment was the largest and held 42.3% of the rum market share in 2024 with its versatility and widespread use in cocktail formulations, particularly in high-volume markets such as North America and the Caribbean. The clear, light-bodied spirit, typically aged for shorter durations and filtered to remove color, serves as the base for iconic mixed drinks like the mojito, daiquiri, and piña colada, which remain staples in bars and households alike. In India, the Federation of Indian Alcohol Producers noted a 21% increase in white rum sales between 2020 and 2023, driven by rising urban affluence and the popularity of Western-style mixology in metropolitan lounges.

The spiced segment is projected to expand at a CAGR of 7.8% during the forecast period with the evolving consumer palates seeking bolder, more experiential flavor profiles in mature markets where premiumization trends are reshaping spirits consumption. In the United Kingdom, the Wine and Spirit Trade Association recorded a 15% year-on-year increase in spiced rum sales in 2022, outpacing other rum subcategories, with brands like Captain Morgan leading market penetration through innovative limited editions and seasonal variants.

By Distribution Channel Insights

The off-trade channel segment dominated the global rum market share in 2024 with the consumer preferences for convenience, cost efficiency, and the growing normalization of home consumption, particularly in urban centers and regions with restrictive on-premise alcohol regulations. Similarly, in Australia, the Australian Bureau of Statistics noted that off-trade spirits sales grew by 9.3% in volume during 2021–2023, which is driven by younger consumers stocking home bars and hosting private gatherings. Moreover, off-trade pricing is typically 20–30% lower than on-trade due to reduced overheads by making it especially appealing in inflationary environments.

The off-trade channel segment dominated the global rum market share in 2024 with the consumer preferences for convenience, cost efficiency, and the growing normalization of home consumption, particularly in urban centers and regions with restrictive on-premise alcohol regulations. Similarly, in Australia, the Australian Bureau of Statistics noted that off-trade spirits sales grew by 9.3% in volume during 2021–2023, which is driven by younger consumers stocking home bars and hosting private gatherings. Moreover, off-trade pricing is typically 20–30% lower than on-trade due to reduced overheads by making it especially appealing in inflationary environments.

REGIONAL ANALYSIS

North America Rum Market Insights

North America was the top performer of the rum market by capturing 38.3% of share in 2024. American consumers exhibit a strong affinity for both classic and innovative rum expressions, with total rum imports reaching 218 million liters in 2022, a 5.4% increase from the previous year, as the U.S. Department of Commerce. Furthermore, the rise of premiumization has transformed consumer behavior; the Distilled Spirits Council of the United States reported that premium and super-premium rum sales grew by 14.2% in value in 2022, driven by brands like Plantation, Diplomático, and Zacapa.

Europe Rum Market Insights

Europe global rum market held 27.3% of share in 2024 with a sophisticated palate for aged and agricole-style rums, reflecting a growing appreciation for terroir and artisanal production. The European Union’s Geographical Indications framework has further elevated rum’s status, granting protected designations to rums from Martinique and Guadeloupe, reinforcing authenticity and quality. Additionally, the region’s dense network of specialty bars and rum festivals, such as the Berlin Rum Festival, fosters consumer education and brand loyalty.

Latin America Rum Market Insights

Latin America rum market is likely to grow with prominent growth opportunities in the coming years. Countries such as Jamaica, Barbados, Cuba, and Puerto Rico are not only major exporters but also custodians of distinct rum-making traditions that influence global standards. Jamaica alone produced 120 million liters of rum in 2022, with 75% destined for international markets, as reported by the Jamaica Rum Exporters Association.

Asia-Pacific Rum Market Insights

The Asia-Pacific rum market is ascribed to grow with domestic rum consumption exceeding 140 million liters annually. The Philippines, where rum is deeply embedded in local drinking culture, consumes over 55 million liters per year, with brands like Tanduay dominating both domestic and export markets, according to the Philippine Department of Trade and Industry. In Australia, the Alcohol Beverages Council reported a 9% compound annual growth in premium rum imports between 2018 and 2022, reflecting a shift toward craft and aged expressions. Furthermore, the expansion of international hotel chains and cruise tourism across Southeast Asia is increasing exposure to premium rum offerings.

Middle East and Africa Rum Market Insights

The Middle East and Africa rum market is likely to grow steadily in the coming years. The United Arab Emirates, a duty-free hub with a large expatriate population, imported 18.3 million liters of rum in 2022, primarily for on-trade consumption in luxury hotels and restaurants, as reported by the Dubai Department of Economic Development.

LEADING PLAYERS IN THE RUM MARKET

Bacardi Limited

Bacardi stands as the world’s largest privately held spirits company and the preeminent force in the global rum market. Originating in Cuba in 1862, the brand has cultivated a legacy of quality, consistency, and innovation that resonates across continents. Through strategic brand stewardship, global distribution networks, and a deep commitment to sustainability, Bacardi has maintained a dominant presence in key markets while expanding into emerging regions.

Diageo plc

Diageo is a British multinational alcoholic beverages giant plays a pivotal role in the rum market through its ownership of Captain Morgan, one of the most recognized spiced rum brands worldwide. Leveraging its vast global infrastructure, Diageo has elevated Captain Morgan from a regional favorite to a mainstream international brand, integrating it into a broader portfolio of spirits that benefit from unified marketing and distribution. The company’s expertise in brand development and consumer engagement has enabled consistent innovation, including flavored extensions and ready-to-drink formats that appeal to younger demographics.

Pernod Ricard

Pernod Ricard is a French leader in premium spirits that has its presence in the rum market through a portfolio that emphasizes craftsmanship, heritage, and terroir-driven production. The company owns Havana Club, a globally celebrated rum developed in partnership with Cuba’s state-owned spirits enterprise, which serves as a cornerstone of its rum strategy. Pernod Ricard differentiates itself by championing authentic, aged rums that appeal to connoisseurs and mixologists, positioning the spirit within the premium and super-premium segments. Its commitment to cultural preservation, distillery excellence, and responsible consumption aligns with the values of discerning consumers.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

One of the primary strategies employed by leading rum producers is brand premiumization, where companies shift focus from volume-driven sales to cultivating high-margin, aged, and artisanal expressions. This approach involves repositioning rum as a sipping spirit comparable to whisky or cognac, supported by sophisticated packaging, limited editions, and storytelling that emphasizes heritage and provenance.

Another strategy is geographic expansion into emerging markets, particularly in the Asia-Pacific, Africa, and Eastern Europe. Firms are tailoring product offerings to local tastes, establishing regional distribution partnerships, and investing in marketing campaigns that introduce rum to consumers unfamiliar with its cultural roots.

Another key tactic is vertical integration and sustainability initiatives, where major players secure control over sugarcane sourcing, distillation, and aging processes to ensure consistency and reduce environmental impact. Companies not only improve operational resilience but also strengthen brand reputation among ethically conscious consumers by promoting eco-friendly practices, reducing carbon footprints, and supporting local farming communities.

KEY MARKET PLAYERS AND COMPETITION OVERVIEW

Major Players of the global rum market include Bacardi Limited, Diageo plc, Pernod Ricard, Destilería Serrallés, Demerara Distillers Limited, Suntory Holdings Limited, Anheuser-Busch InBev, Remy Cointreau, Gruppo Campari, United Spirits Limited (USL), Maine Craft Distilling, Hampden Estate Rum, Mount Gay Distilleries Ltd.

The competitive landscape of the rum market is characterized by a dynamic interplay between global conglomerates and a rising wave of independent craft distillers, each vying for consumer attention through differentiation and innovation. Established players leverage their extensive distribution networks, financial resources, and brand recognition to maintain dominance, particularly in mass-market and premium segments. They invest heavily in marketing, sponsorships, and cocktail culture to reinforce brand loyalty and expand reach. At the same time, boutique producers are gaining traction by emphasizing authenticity, small-batch production, and regional identity, appealing to a growing cohort of discerning drinkers seeking unique and transparent spirits. This duality fosters a richly diverse market where heritage and modernity coexist.

Global Rum Market News

- In May 2024, Diageo partnered with a digital spirits platform to launch a direct-to-consumer subscription service for premium rum by allowing customers exclusive access to rare bottlings and personalized tasting experiences.

MARKET SEGMENTATION

This research report on the global rum market has been segmented and sub-segmented based on type, distribution channel and region.

By Product Type

- Golden

- Dark

- White

- Spiced

By Distribution Channel

- On-trade

- Off-trade

By Region

- North America

- The United States

- Canada

- Rest of North America

- Europe

- The United Kingdom

- Spain

- Germany

- Italy

- France

- Rest of Europe

- The Asia Pacific

- India

- Japan

- China

- Australia

- Singapore

- Malaysia

- South Korea

- New Zealand

- Southeast Asia

- Latin America

- Brazil

- Argentina

- Mexico

- Rest of LATAM

- The Middle East and Africa

- Saudi Arabia

- UAE

- Lebanon

- Jordan

- Cyprus

Frequently Asked Questions

1. What can be the compound annual growth rate of the global Rum market?

The global Rum market can expand with a CAGR of 5.5% during the forecast period.

2. Mention the major key players in the global Rum market?

Bacardi Global Brands Ltd, Asahi Group Holdings Ltd, Demerara Distillers Ltd, Davide Campari-Milano Spa, Suntory Holdings Ltd, and Others.

3. What are the major types of rum available in the market?

The market includes white rum, dark rum, spiced rum, gold rum, and premium aged rum, each catering to different taste preferences and consumption occasions.

4. What factors are driving the growth of the rum market?

Key drivers include rising global alcohol consumption, increasing popularity of cocktails and mixology, growing demand for premium and craft spirits, and expanding distribution networks.

5. Which regions are the largest consumers of rum?

North America, the Caribbean, Europe, and parts of Asia-Pacific are the largest consumers, with the Caribbean known for traditional rum production and exports.

6. What trends are shaping the rum market?

Current trends include the rise of craft and small-batch rums, increased demand for flavored and spiced rums, sustainable and organic production, and the growth of rum-based ready-to-drink (RTD) products.

7. What challenges does the rum market face?

Challenges include competition from other spirits like whiskey and vodka, taxation and regulatory issues, and shifting consumer preferences towards health-conscious beverages.

8. How is premiumization affecting the rum market?

Consumers are showing increased interest in premium and aged rums, which offer unique flavors and are often consumed neat or in high-end cocktails, driving growth in the premium segment.

9. How important is e-commerce in the rum market?

E-commerce has become a crucial distribution channel for rum, especially post-pandemic, with online alcohol delivery services and direct-to-consumer sales gaining popularity.

10. What is the future outlook for the global rum market?

The rum market is expected to grow at a moderate pace, driven by innovation in flavors, premium product launches, increasing cocktail culture, and the expansion of emerging markets.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com