Global Cocktail Market Size, Share, Trends & Growth Forecast Report Segmented By Type (Short Drink and Long Drink), Application (Wedding Ceremonies, Backyard BBQ, Cocktail Party and Others), Distribution Channel (Supermarkets and Hypermarkets, Convenience Stores, Bars and Restaurants and Online Retail), And Region (North America, Europe, Asia Pacific, Latin America and Middle East & Africa), Industry Analysis from 2026 to 2034

Global Cocktail Market Summary

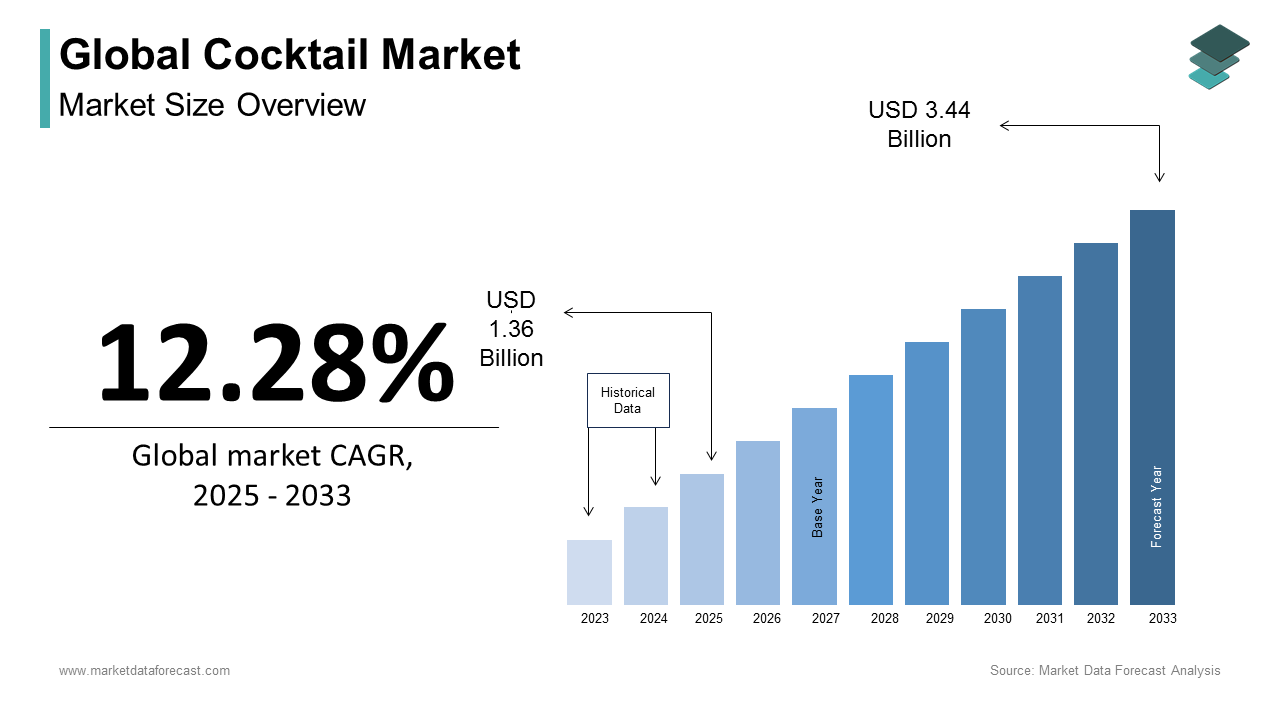

The global cocktail market size was calculated to be USD 1.36 billion in 2025 and is anticipated to be worth USD 3.86 billion by 2034, growing from USD 1.53 billion in 2026 at a CAGR of 12.28% during the forecast period.

The Cocktail Market refers to the global segment featuring mixed alcoholic beverages—using spirits like gin, vodka, whiskey, tequila, rum, and brandy combined with juices, syrups, herbs, dairy, and botanical ingredients. It has expanded due to rising incomes, evolving lifestyles, the rise of mixology culture, and growing interest in botanical and vegetable-infused drinks. The trend of pairing cocktails with immersive experiences such as the Japanese ‘kissa’ music-themed bars like Black Lacquer in London, also drives interest

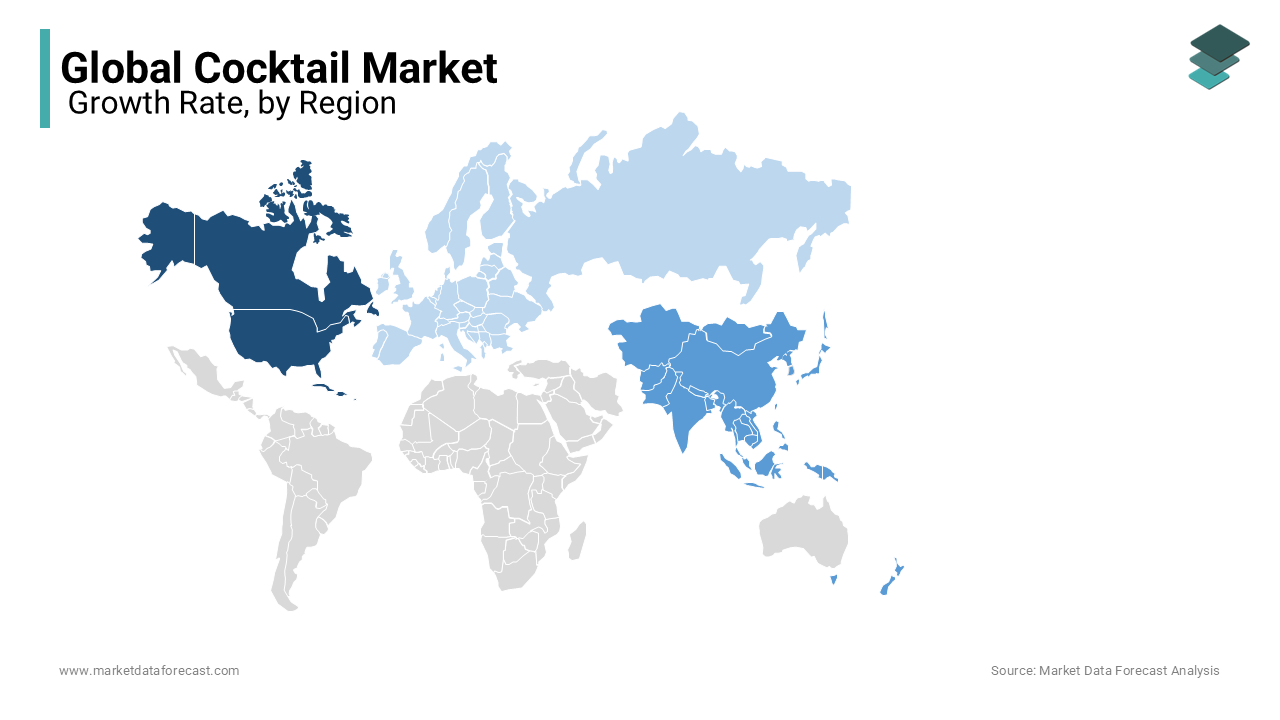

- North America dominated the cocktail market in 2025, driven by strong bar and restaurant culture, mixology influence, and demand for premium and RTD (ready-to-drink) cocktails

- Asia-Pacific is projected to be the fastest-growing region over the forecast period, supported by rising urbanization, disposable incomes, and expanding cocktail culture in markets like China and

- Europe remains a major global market, backed by its vibrant nightlife, cocktail artistry, and established premium spirits sector

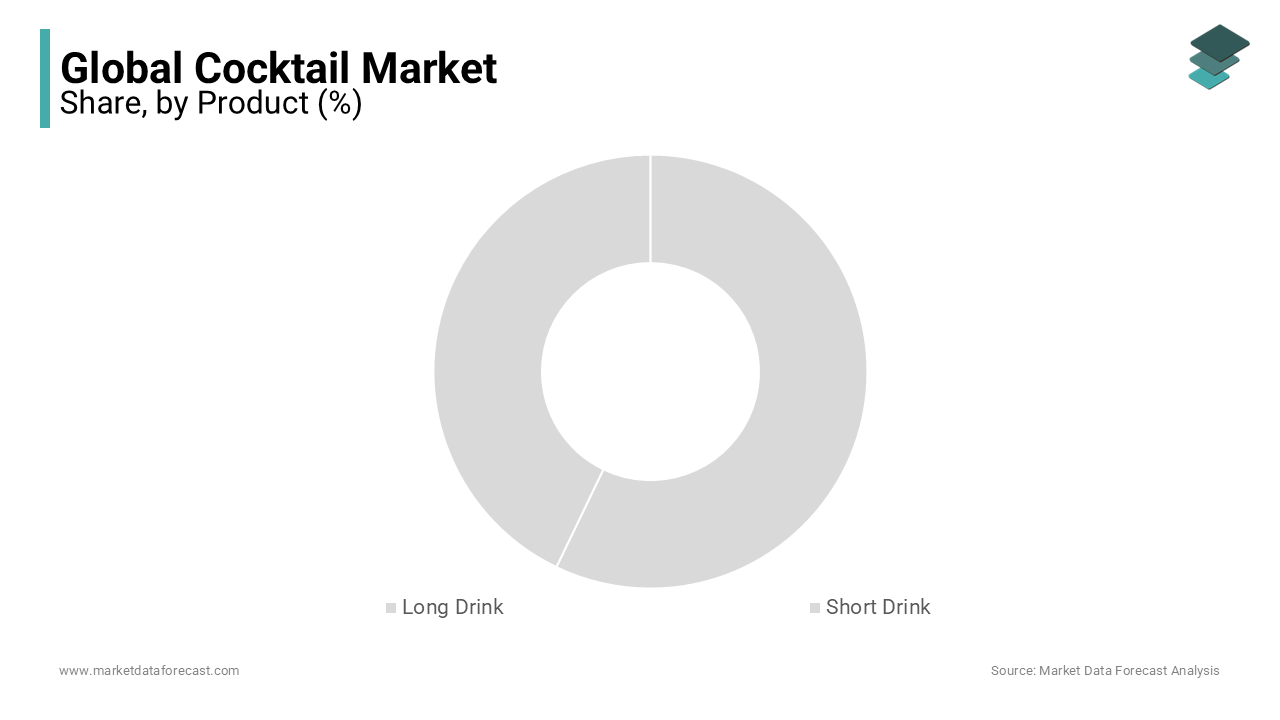

- Based on type, the long drink segment held the largest share in 2025, catering to those who prefer lower-alcohol, easy-to-enjoy cocktails. The short drink category is witnessing the fastest CAGR through 2032, catering to trends in quick gatherings and premium sipping.

- Based on the distribution channel, bars & restaurants remain dominant given their role in introducing consumers to novel cocktails. Meanwhile, online retail and RTD formats are growing rapidly, driven by convenience and health-conscious consumption trends.

Global Cocktail Market Size

The global cocktail market size was calculated to be USD 1.36 billion in 2025 and is anticipated to be worth USD 3.86 billion by 2034, growing from USD 1.53 billion in 2026 at a CAGR of 12.28% during the forecast period.

A cocktail is the artful blending of distilled spirits, mixers, and flavoring agents to produce both classic and innovative drinks. These beverages, traditionally served in bars, restaurants, and lounges, have evolved beyond their social roots to become emblematic of cultural expression and culinary craftsmanship. In recent years, the concept of the cocktail has transcended its conventional boundaries, integrating into lifestyle trends, premiumization movements, and experiential consumption.

The rise of mixology as a professional discipline has further elevated the sector. Additionally, the integration of locally sourced botanicals and heritage spirits has redefined regional offerings, particularly in markets like Japan and Australia, where craft distillation has surged. This confluence of craftsmanship, cultural adaptation, and consumer sophistication positions the cocktail market as a nuanced intersection of gastronomy, tradition, and innovation, one that is far removed from mere alcoholic beverage sales.

KEY MARKET DRIVERS

Rising Urbanization and the Expansion of Premium Nightlife Infrastructure

Urbanization across emerging economies has catalyzed the proliferation of high-end hospitality venues, directly influencing cocktail consumption. As cities expand and disposable incomes rise, particularly in Southeast Asia, consumers increasingly frequent lifestyle-centric venues where cocktails serve as signature offerings. This shift is mirrored in Indonesia. These venues prioritize curated drink menus, often featuring artisanal cocktails priced above standard bar offerings, reflecting a willingness to pay for experiential value. The urban professional demographic, particularly millennials and Gen Z, exhibits a pronounced preference for socializing in aesthetically designed spaces where mixology is showcased as performance art. This behavioral shift is reinforced by digital influence, with platforms like Xiaohongshu and Instagram amplifying the visibility of cocktail culture. As urban density increases and the middle class expands, the demand for elevated drinking experiences continues to surge, making infrastructure development a pivotal demand driver.

Consumer Demand for Premiumization and Craft Spirits

A discernible shift toward premium alcoholic beverages has significantly bolstered cocktail market growth, with consumers increasingly favoring quality, provenance, and uniqueness over volume. In Japan, craft gin production rose from 12 licensed distilleries in 2018 to 47 in 2023, according to the Japan Distillers Association, enabling locally inspired cocktails that appeal to national pride and authenticity. This willingness to pay reflects a broader cultural movement toward mindful consumption, where ingredients such as small-batch rums, barrel-aged whiskeys, and organic modifiers are highly valued. The rise of “slow drinking” culture—emphasizing savoring complex flavors over rapid consumption—further aligns with cocktail appeal. This trend is reinforced by regulatory support. Thus, premiumization is not merely a pricing phenomenon but a holistic transformation of consumer expectations, directly fueling cocktail demand.

MARKET RESTRAINTS

Stringent Alcohol Regulations and Taxation Policies

Government-imposed restrictions on alcohol sales and consumption present a formidable barrier to the expansion of the cocktail market, particularly in regions with conservative social policies or public health mandates. In India, alcohol is regulated at the state level, with prohibitions enforced in Bihar, Gujarat, and parts of Nagaland, affecting over 150 million people, as per the Ministry of Social Justice and Empowerment 2023 report. Even in permitted states, excise duties on imported spirits can exceed 150%, rendering premium cocktail ingredients prohibitively expensive. Malaysia enforces a halal compliance framework that restricts alcohol advertising and limits retail availability, effectively curtailing market visibility. These fiscal policies disincentivize both consumer purchases and business investment in cocktail-centric establishments. Additionally, restrictions on operating hours—such as Vietnam’s 11 PM curfew for alcohol service—reduce revenue-generating windows, discouraging high-cost mixology ventures. These regulatory headwinds, deeply entrenched in cultural and political contexts, remain a persistent drag on market maturation.

Health Consciousness and Shifting Consumer Attitudes Toward Alcohol

Growing public awareness of alcohol-related health risks has led to a measurable decline in per capita consumption among key demographic segments, particularly in developed Asia-Pacific markets. This behavioral shift is mirrored in Japan, the steepest decline in decades. The rise of the “sober curious” movement has further accelerated demand for non-alcoholic alternatives. This trend is particularly pronounced among white-collar professionals, who associate excessive drinking with diminished productivity. While innovation in zero-proof spirits offers partial mitigation, the overarching health narrative challenges the foundational premise of cocktail culture, constraining long-term volume growth despite premiumization.

MARKET OPPORTUNITIES

Integration of Technology and Digital Platforms in Mixology

The fusion of digital innovation with cocktail service presents a transformative opportunity for market differentiation and customer engagement. Smart bars equipped with AI-powered dispensing systems, such as those deployed by Tokyo-based Bar Atomix, have reduced preparation time. Mobile applications now enable consumers to customize cocktails remotely. Blockchain traceability is also gaining traction; in New Zealand, distilleries like Antiquum Farm use QR codes to provide real-time data on botanical origins and carbon footprint, appealing to eco-conscious consumers. These technologies not only improve operational efficiency but also create novel engagement models, particularly among tech-savvy youth. By embracing digital integration, the cocktail market can transcend traditional service limitations and unlock scalable, data-driven personalization.

Expansion of Cocktail Culture into Non-Traditional Venues and Formats

The migration of cocktail experiences beyond conventional bars into hotels, retail spaces, and even residential settings represents a significant growth vector. This growth is driven by convenience and premium packaging, with brands like Four Pillars and Matcha Moon capturing shelf space in high-end supermarkets. Additionally, corporate wellness programs are incorporating mocktail mixology workshops. This diversification of consumption contexts allows the cocktail market to tap into new revenue streams and audience segments, reducing dependency on traditional nightlife and fostering sustainable expansion.

MARKET CHALLENGES

Supply Chain Volatility for Specialty Ingredients

The reliance on geographically specific and often perishable ingredients exposes the cocktail market to significant supply chain vulnerabilities. Premium cocktails frequently feature rare botanicals, such as wasabi root in Japanese saké-based drinks or finger limes in Australian native-inspired mixes, which are susceptible to climatic disruptions. These fluctuations strain profit margins, particularly for independent venues with limited purchasing power. Import dependencies further complicate logistics. The 2022 disruption at the Port of Shanghai alone delayed Spirit shipments. Moreover, the cold chain requirements for fresh modifiers like house-made syrups and infused liqueurs increase storage costs. These systemic inefficiencies challenge consistency and scalability, making ingredient security a critical operational hurdle.

Skilled Labour Shortage in Professional Mixology

The cocktail market’s reliance on highly trained mixologists creates a structural challenge, as the supply of qualified professionals fails to keep pace with demand. The apprenticeship model, which traditionally spans 3–5 years, deters rapid workforce scaling, particularly given the physically demanding nature of the role. Australia faces a similar gap. This shortage compromises service quality and innovation capacity. Meanwhile, attrition rates in the sector exceed 45% within the first two years. The issue is exacerbated by visa restrictions; in Singapore, foreign mixologists require specialized work permits, limiting recruitment from global talent pools. Additionally, wage disparities discourage long-term career commitment—average bartender earnings in Bangkok remain low, well under the city’s cost of living. Without systemic investment in education, certification, and career pathways, the talent gap will persist, constraining the market’s ability to deliver consistent, high-caliber experiences essential for sustained growth.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 12.28% |

| Segments Covered | By Product Type, Application, Distribution Channel, and Region |

| Various Analyses Covered | Global, Regional, and Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Captain Morgan, Bols, Snobar Cocktails, Cointreau, Kold Cocktails, Manchester Drinks Co. Ltd, Bodega Co. de Siam Ltd, Rio Wine, Cocktail Natives, Miami Cocktail Co, Harvest Hill Beverage Company, Arbor Mist Winery, Snake Oil Cocktail Company, N1CE Company Ltd, Four Blue Palms, Inc., Belvedere, Bombay Sapphire, and The Absolut Company |

SEGMENTAL ANALYSIS

By Product Type Insights

The long drink segment commanded the global cocktail market by accounting for 55.3% of total volume consumption in 2025.

Characterized by higher volume, lower alcohol concentration, and extended drinking duration, long drinks such as mojitos, spritzes, and highballs align with evolving consumer preferences for sociable, sessionable beverages. This dominance is primarily driven by the rising popularity of low-alcohol and refreshing formats, particularly in warm-climate regions and among younger demographics. The resurgence of ready-to-drink (RTD) variants has further amplified this trend; Finland’s long drink, a gin-based carbonated beverage, saw exports grow, propelled by U.S. market entry. Additionally, the integration of functional ingredients—such as adaptogens and electrolytes—into long drink formulations has expanded their appeal beyond recreation into wellness-oriented consumption. The scalability of long drink production, particularly in automated bar systems, also enhances profitability for operators. These interwoven behavioral, operational, and product innovation factors collectively sustain the long drink’s preeminence.

The short drink segment is experiencing the fastest growth within the cocktail market and is registering a CAGR of 9.7% from 2026 to 2034.

The acceleration of this segment is fueled by the premiumization of mixology and the increasing demand for high-margin, craft-oriented beverages. Short drinks—such as martinis, old fashioneds, and negronis—are emblematic of artisanal expertise, often requiring aged spirits, house-made bitters, and precise dilution techniques, which elevate their perceived value. The growth is further amplified by the rise of speakeasy-style venues. These spaces emphasize ritualistic preparation, where the theatricality of crafting a short drink enhances customer engagement. Moreover, the concentration of flavor in short drinks makes them ideal for pairing with gourmet cuisine, a trend gaining traction in luxury hotels and Michelin-starred restaurants. This convergence of craftsmanship, exclusivity, and gastronomic alignment positions the short drink as the most dynamically expanding segment.

By Application Insights

The cocktail parties segment constituted the biggest application by capturing 44.3% of the global cocktail market by consumption volume in 2025.

These events, traditionally associated with urban elites and corporate gatherings, have evolved into mainstream social rituals, particularly in metropolitan centers across North America and Western Europe. The dominance of cocktail parties is underpinned by their role as curated social experiences, where beverage variety, presentation, and ambiance are central. The format’s adaptability to both formal and semi-formal settings has broadened its appeal. Additionally, the professionalization of event mixology has elevated service standards. The integration of themed menus, such as Prohibition-era or botanical-inspired cocktails, further enhances experiential value. These factors collectively cement cocktail parties as the most voluminous application segment.

The backyard BBQ segment is emerging as the fastest-growing application and is projected to expand at a CAGR of 10.3% from 2026 to 2034.

The surge of this segment is driven by the normalization of informal, home-based entertaining and the increasing accessibility of premium cocktail ingredients for domestic use. The trend is reinforced by the proliferation of pre-batched cocktail kits and portable mixology tools; sales of such products rose between 2021 and 2023. Brands like Cutwater Spirits and Haus have capitalized on this shift, offering canned cocktails specifically marketed for outdoor grilling events. Social media platforms such as Pinterest and TikTok have further amplified the trend. The convenience of ready-to-serve formats, coupled with the desire for elevated yet relaxed gatherings, has transformed the backyard from a casual space into a venue for curated beverage experiences. This cultural shift, supported by product innovation and digital influence, positions backyard BBQs as the most rapidly expanding application segment.

By Distribution Channel Insights

The bars and restaurants segment remained the dominant distribution channel by accounting for 52.6% in 2025.

This lead position is due to the experiential nature of cocktail consumption, where ambiance, service, and mixological theater are integral to the purchase decision. In urban centers, the density of cocktail-focused venues has surged. The channel’s dominance is further reinforced by higher price points—cocktails served in bars typically retail more than the cost of equivalent retail products, enabling significant margin generation. Additionally, the rise of destination bars, venues designed as experiential landmarks, has strengthened on-premise appeal. The integration of food pairing menus has also elevated the bar experience. These dynamics underscore the enduring centrality of bars and restaurants as the primary conduit for cocktail consumption.

Online retail is the fastest-growing distribution channel and is registering a CAGR of 12.8% from 2026 to 2034.

This rapid expansion is fueled by shifting consumer behavior toward digital convenience, subscription models, and direct-to-consumer brand engagement. Subscription services like Boozed and Mixxit delivered millions of cocktail boxes globally in 2023, reflecting sustained demand for at-home mixology. The pandemic accelerated digital adoption, but post-lockdown growth indicates lasting behavioral change. Platforms like Drizly and Dan Murphy’s have enhanced user experience with AI-driven recommendations and same-day delivery, reducing friction in purchasing. With logistics networks improving and regulatory frameworks adapting, online retail is poised to disrupt traditional distribution hierarchies, making it the most dynamically advancing channel.

REGIONAL ANALYSIS

North America held a commanding position in the global cocktail market by securing a 37.6% share in 2025.

The region’s position is anchored in a mature hospitality ecosystem, a deep-rooted culture of mixology, and robust consumer spending on experiential dining. The United States alone contributes significantly to North America’s cocktail revenue, driven by a proliferation of craft distilleries and cocktail bars. The infrastructure supports innovation, with cities like New Orleans and San Francisco leading in cocktail tourism. Premiumization is a key driver. The region’s regulatory environment, while fragmented, increasingly supports direct-to-consumer sales, enabling digital expansion. With strong brand loyalty, high disposable income, and a culture that celebrates cocktail craftsmanship, North America remains the epicenter of global cocktail innovation and consumption.

Europe maintains a significant market share.

The region’s cocktail culture is deeply interwoven with its gastronomic heritage, particularly in Western and Northern Europe, where mixology is treated as a culinary art. The United Kingdom leads the regional market, driven by London’s status as a global mixology hub. In Scandinavia, the long drink phenomenon has gained commercial momentum; Finland’s “lonkero” category, a premixed gin-grapefruit drink. Southern Europe leverages its climate and tourism to boost outdoor cocktail consumption. Regulatory support in countries like Germany, where alcohol advertising restrictions were relaxed in 2022, has further stimulated market activity. With a blend of tradition, innovation, and strong tourism inflows, Europe remains a pivotal force in shaping global cocktail trends.

Asia-Pacific captures a notable share of the global cocktail market.t

The region’s growth is propelled by rapid urbanization, rising disposable incomes, and the localization of Western drinking formats. Japan stands out as the market leader, with a strong preference for whisky-based and low-ABV cocktails. South Korea’s cocktail market expanded in 2023, driven by the “meokbang” (eating broadcast) and “jipjum” (home party) trends. China’s premium bar scene is burgeoning. India’s market is nascent but accelerating, with cocktail sales in five-star hotels growing year-on-year. The region’s diversity presents challenges, but also opportunities for hyper-localized offerings, such as yuzu-infused gin in Japan or arrack-based cocktails in Sri Lanka. With a young, digitally connected population and expanding luxury hospitality, the Asia-Pacific is poised for sustained growth.

Latin America is another key player in the global cocktail market.

While smaller in scale, the region is rich in indigenous spirits and traditional mixed drinks that are gaining international recognition. Brazil leads the regional market. Mexico’s cocktail culture is deeply tied to tequila and mezcal. Urban centers like São Paulo and Mexico City are witnessing a craft cocktail renaissance. However, economic volatility and regulatory inconsistencies constrain broader expansion. Despite these challenges, the region’s vibrant social culture and growing middle class offer long-term potential. The inclusion of Latin-inspired cocktails in global bar menus—such as the Oaxaca Old Fashioned—signals rising influence. With increasing investment in premiumization and tourism, Latin America is gradually transforming from a traditional market into a source of global cocktail innovation.

The Middle East and Africa collectively account for a smaller share of the global cocktail market.

The market is highly segmented, with Gulf Cooperation Council (GCC) countries driving premium consumption, while sub-Saharan Africa remains constrained by regulatory and cultural factors. The United Arab Emirates leads the region, supported by a luxury tourism ecosystem and a large expatriate population. Saudi Arabia’s Vision 2030 initiative has spurred entertainment sector growth, with licensed venues expanding in entertainment zones like Qiddiya, as reported by the Saudi General Entertainment Authority. South Africa is an exception, with a developed bar culture and growing craft distillery scene. The region’s growth is contingent on regulatory liberalization and urban affluence. While currently modest, the Middle East and Africa represent a frontier market with latent potential, particularly as social reforms unfold in the Gulf.

COMPETITIVE LANDSCAPE

The competitive landscape of the cocktail market is defined by a dynamic interplay between heritage, innovation, and experiential differentiation. Major players strive not only to dominate through brand recognition but also to lead cultural movements within mixology. The rivalry extends beyond product formulation to encompass storytelling, sustainability, and the cultivation of global communities of bartenders and enthusiasts. Companies are increasingly investing in craftsmanship, positioning themselves as curators of lifestyle rather than mere beverage suppliers. The emergence of craft distillers and niche brands adds further complexity, challenging established players to balance scalability with authenticity. Geographic expansion, particularly into emerging markets, has intensified competition, with localization of flavors and service models becoming critical. Strategic partnerships with hospitality chains, event organizers, and digital platforms enable deeper consumer penetration. The race to innovate in ready-to-drink formats and non-alcoholic alternatives further heightens the competitive tension. Ultimately, success in this market hinges on the ability to merge tradition with modernity, delivering not just a drink but a memorable experience that resonates across diverse consumer segments.

Key Market Participants

A few of the notable companies in the global cocktail market include

- Captain Morgan

- Bols

- Snobar Cocktails

- Cointreau

- Kold Cocktails

- Manchester Drinks Co. Ltd

- Bodega Co. de Siam Ltd

- Rio Wine

- Cocktail Natives

- Miami Cocktail Co

- Harvest Hill Beverage Company

- Arbor Mist Winery

- Snake Oil Cocktail Company

- N1CE Company Ltd

- Four Blue Palms, Inc.

- Belvedere

- Bombay Sapphire

- The Absolut Company

LEADING PLAYERS IN THE COCKTAIL MARKET

- Diageo Plc has established itself as a dominant force in the global cocktail market through its strategic focus on premium spirits and innovation in ready-to-drink (RTD) formats. The company leverages its extensive portfolio of iconic brands to craft cocktail experiences that resonate across cultures and consumer segments. By investing in mixology education and partnering with elite bartenders worldwide, Diageo has elevated the craftsmanship associated with cocktail preparation. Its commitment to sustainability and digital engagement further strengthens consumer trust and brand loyalty. The firm’s influence extends beyond product offerings, shaping industry standards and driving trends in flavor development and responsible consumption, making it a pivotal architect of the modern cocktail landscape.

- Bacardi Limited has long been a trailblazer in the cocktail domain, renowned for its cultural integration of rum-based mixed drinks into global social rituals. The company champions experiential marketing, hosting immersive cocktail events and bartender competitions that amplify brand visibility and foster community. Its emphasis on heritage, authenticity, and ingredient quality has positioned its products as staples in both home and professional mixology. Bacardi’s agility in adapting to evolving consumer tastes—such as low-alcohol and plant-based modifiers—has allowed it to remain at the forefront of innovation. Through strategic collaborations with mixologists and lifestyle brands, Bacardi continues to redefine the boundaries of cocktail culture.

- Pernod Ricard excels in blending tradition with modernity, offering a diverse range of spirits that serve as foundational elements in classic and contemporary cocktails. The company’s deep investment in bartender training programs and global cocktail competitions underscores its dedication to elevating mixology as an art form. With a strong presence in both on-premise and retail channels, Pernod Ricard bridges the gap between professional bars and at-home consumers. Its emphasis on cultural storytelling and regional flavor profiles enables it to connect with diverse audiences. By championing sustainable practices and digital innovation, the company maintains a leadership role in shaping the future of the cocktail experience.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

- One major strategy employed by leading players is the elevation of mixology through education and community engagement. Companies invest in global bartender academies, certification programs, and live demonstrations to cultivate expertise and brand loyalty. These initiatives not only enhance the quality of cocktail preparation but also position the brands as authorities in the craft, fostering long-term relationships with both professionals and consumers.

- Another key approach is the expansion into ready-to-drink (RTD) and portable cocktail formats. By offering pre-mixed, premium beverages in convenient packaging, companies cater to evolving lifestyles that prioritize ease without compromising on taste. This shift allows brands to extend their reach beyond traditional bars into retail, e-commerce, and outdoor settings, aligning with the growing demand for at-home and on-the-go consumption.

- A third pivotal strategy is the integration of digital and experiential marketing. Brands are leveraging augmented reality, social media storytelling, and pop-up lounges to create immersive narratives around their products. These experiences transform passive consumers into active participants, deepening emotional connection and driving engagement in an increasingly competitive and experience-driven market.

Cocktail Market Recent News

- In March 2023, Diageo launched a global mixology residency program, partnering with award-winning bartenders to create limited-edition cocktail experiences in major cities. This initiative is anticipated to deepen consumer engagement and reinforce the brand’s leadership in premium cocktail culture.

- In July 2023, Bacardi introduced a sustainable cocktail series made with upcycled ingredients and eco-conscious packaging. This move is expected to enhance brand relevance among environmentally aware consumers and set new standards in responsible mixology.

- In November 2023, Pernod Ricard opened a digital mixology hub offering virtual training, recipe development tools, and live bartender sessions. This platform is projected to strengthen its connection with professional mixologists and home enthusiasts alike.

- In January 2025, Brown-Forman expanded its cocktail portfolio by launching a premium ready-to-drink line under the Woodford Reserve brand. This expansion is anticipated to capture the growing demand for convenient yet high-quality cocktail experiences.

- In May 2025, Constellation Brands partnered with a luxury hotel group to establish signature cocktail lounges across Asia. This collaboration is expected to elevate brand visibility and drive premiumization in emerging markets.

MARKET SEGMENTATION

This research report on the global cocktail market has been segmented and sub-segmented based on type, application, distribution channel, and region.

By Product Type

- Long Drink

- Short Drink

By Application

- Backyard BBQ

- Wedding Ceremonies

- Cocktail Party

- Others

By Distribution

- Bars and Restaurants

- Supermarkets and Hypermarkets

- Convenience Stores

- Online Retail

By Region

- North America

- Europe

- The Asia Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

1. What factors are driving the growth of the cocktail market?

Several factors contribute to market growth are Increased spending on leisure and entertainment, Growing popularity of cocktail bars and mixology, Development of new flavors, ingredients, and ready-to-drink (RTD) cocktails, and Demand for low-alcohol and non-alcoholic options.

2. What are the key challenges in the cocktail market?

The key challenges in the cocktail market are Varying alcohol regulations and legal drinking ages, Rising awareness about alcohol consumption and its health impacts, High competition among brands and bars, and Availability and cost of quality ingredients.

3. What are the future trends in the cocktail market?

The future trends in the cocktail market are Ready-to-Drink (RTD) Cocktails are Increasing popularity of pre-mixed, convenient cocktail options, Use of eco-friendly packaging and sustainably sourced ingredients, Rise of artisanal and small-batch cocktails with unique flavors, and Growth in low-calorie, low-sugar, and non-alcoholic cocktails.

4. Who are the key players in the cocktail market?

Leading players include Diageo plc, Bacardi Limited, Beam Suntory, Brown-Forman Corporation, Pernod Ricard, Campari Group, Constellation Brands, E. & J. Gallo Winery, and various craft cocktail brands.

5. What is the role of RTD (Ready-to-Drink) cocktails in market growth?

RTD cocktails are one of the fastest-growing segments due to convenience, portability, and the increasing demand for premium, bar-quality drinks at home.

6. Which regions are the largest consumers of cocktails?

North America leads the cocktail market, followed by Europe and Asia-Pacific, with significant growth in urban areas and among younger, social consumers.

7. What are the latest trends in the cocktail market?

Trends include the rise of low-alcohol and non-alcoholic cocktails, sustainable and organic ingredients, craft and artisanal cocktails, and exotic flavor innovations.

8. How is the cocktail market affected by consumer health trends?

Consumers are increasingly opting for cocktails with natural ingredients, lower sugar, and reduced alcohol content, prompting brands to innovate with healthier formulations.

9. What is the impact of mixology culture on the cocktail market?

The rise of mixology has popularized craft cocktails, boosting demand for premium spirits, exotic ingredients, and bartender-driven experiences in bars and at home.

10. What role do social media and digital marketing play in the cocktail market?

Social media platforms like Instagram and TikTok significantly influence cocktail trends, as consumers seek visually appealing and unique drink experiences, driving market growth.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com