Global Wine Market Size, Share, Trends, Growth Report & Analysis By Color (Rose Wine, White Wine, Red Wine, And Others), Taste (Dry, Medium, And Sweet Wine), Product Type (Still Wine, Sparkling Wine, Dessert Wine, And Fortified Wine), Distribution Channel (Online And Offline), And Regional Forecast 2026 To 2034

Market Size, 2025

$357.6 BnMarket Estimate, 2026

$378.4 BnMarket Forecast, 2034

$594.1 BnCAGR, 2026–2034

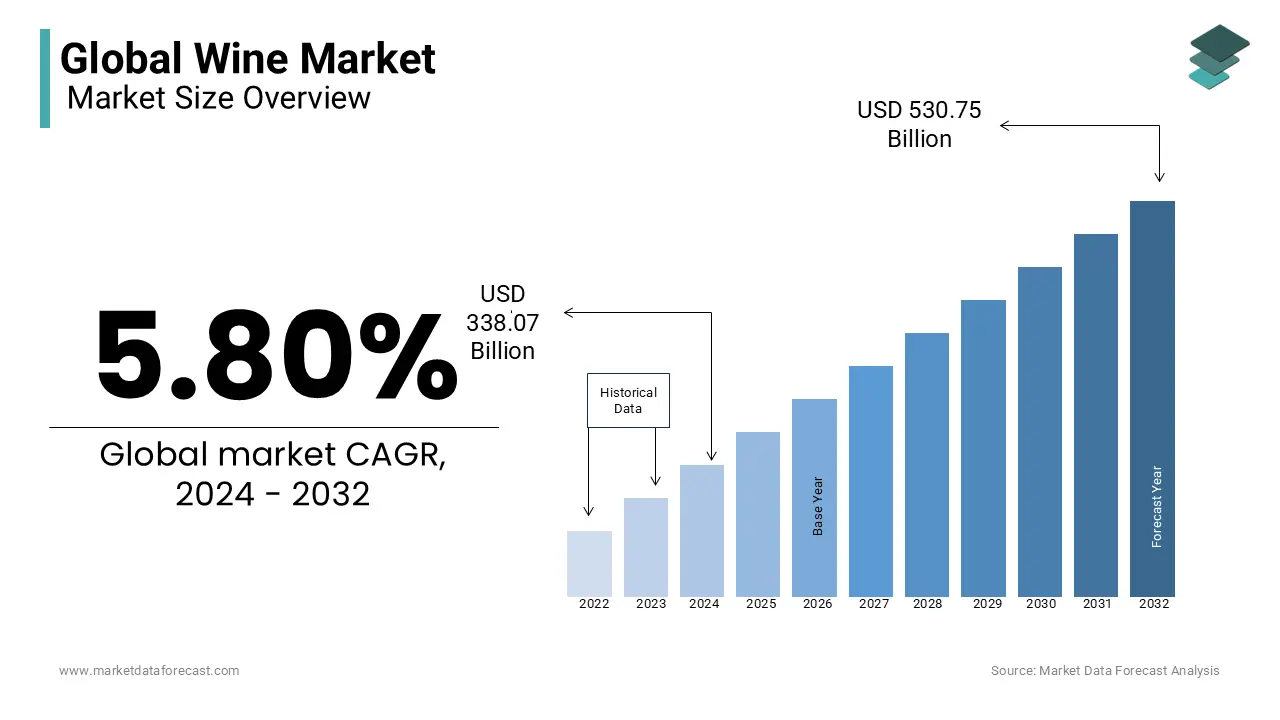

5.8%Global Wine Market Size

The global wine market size was calculated to be USD 357.68 billion in 2025 and is anticipated to be worth USD 594.12 billion by 2034, from USD 378.43 billion in 2026, growing at a CAGR of 5.8% during the forecast period.

Wine functions not only as a beverage but also as a cultural artifact, deeply embedded in social rituals, gastronomy, and regional identity. According to the Food and Agriculture Organization, global vineyard area totaled 7.3 million hectares in 2023, with traditional producers like Italy, Spain, and France accounting for over 45% of cultivated land. Additionally, UNESCO recognizes viticulture in regions such as Champagne and Burgundy as intangible cultural heritage, underscoring wine’s role beyond commerce, as a symbol of terroir, craftsmanship, and historical continuity.

MARKET DRIVERS

Shifting Consumer Preferences Toward Premiumization and Origin Transparency is a primary driver of modern wine market dynamics. Today’s consumers, particularly Millennials and Gen Z, prioritize authenticity, sustainability, and storytelling over volume consumption. According to a 2023 study by the International Wine Council, 62% of wine drinkers in the U.S. and UK are willing to pay a premium for bottles with traceable provenance, including details on vineyard practices and winemaking techniques. The rise of “natural wine”, defined by minimal intervention, native yeasts, and the absence of additives, has gained traction. Besides, blockchain-enabled labels now allow consumers to scan a QR code and access real-time data on grape sourcing and carbon footprint. This demand for transparency is reshaping winery strategies, pushing producers to adopt digital traceability and eco-certifications, thereby enhancing perceived value and brand loyalty in an increasingly discerning marketplace.

Expansion of Wine Culture in Emerging Economies is fueling demand beyond traditional consumption hubs. In countries like China, India, and Brazil, rising disposable incomes and Westernization of dining habits have elevated wine from a luxury novelty to a status symbol and social lubricant. As per the Asian Development Bank, the number of middle- and upper-income households in Asia is projected to reach 1.8 billion by 2030, creating a fertile ground for wine adoption. In China, the Chinese Ministry of Commerce reported that urban wine consumption grew by 9.3% annually between 2018 and 2022, particularly among professionals aged 28–45 who associate wine with sophistication and health. Indian fine-dining establishments now feature curated wine lists, and private clubs in Mumbai and Bangalore host regular tasting events. Educational initiatives by importers and sommelier certifications are demystifying wine, reducing cultural barriers, and accelerating mainstream acceptance in regions historically dominated by spirits and beer.

MARKET RESTRAINTS

Stringent Alcohol Regulations and Taxation Policies significantly constrain market growth in multiple jurisdictions. Governments worldwide impose high excise duties, advertising restrictions, and age verification requirements that increase operational costs and limit consumer access. In the United Kingdom, wine is subject to a 20% VAT and an alcohol duty of £23.50 per 100 liters of pure alcohol, according to HM Revenue & Customs, making mid-tier bottles less affordable. In India, state-level alcohol monopolies and variable taxes, ranging from 45% to 120%, distort pricing and discourage legal retail. Besides, countries like Norway and Finland enforce state-controlled distribution through monopolistic retailers such as Vinmonopolet and Alko, limiting product variety and innovation. These regulatory barriers hinder market penetration, particularly for small and independent wineries lacking the resources to navigate complex compliance frameworks.

Declining Per Capita Consumption in Traditional Markets poses a persistent restraint, particularly in Western Europe and North America. Cultural and generational shifts are reducing wine’s centrality in daily life. As per the European Commission, per capita wine consumption in France, a historic leader, has declined from 50 liters annually in the 1980s to just 32 liters in 2023. A 2023 survey by the U.S. National Institute on Alcohol Abuse and Alcoholism found that alcohol abstinence among American adults rose to 26%, the highest in three decades, with Millennials and Gen Z leading the trend. Health awareness, fitness culture, and the rise of sobriety movements such as “Dry January” have contributed to reduced drinking frequency. Additionally, the popularity of low- and no-alcohol alternatives has surged; in the UK, non-alcoholic wine sales grew by 42% in 2023. This behavioral shift challenges the long-term viability of volume-based growth models, compelling producers to focus on value rather than quantity.

MARKET OPPORTUNITIES

Growth of Direct-to-Consumer (DTC) and E-Commerce Wine Platforms presents a transformative opportunity for wineries to bypass traditional distribution bottlenecks. According to the Wine Institute, DTC wine sales in the U.S. reached $5.2 billion in 2023, accounting for over 10% of total industry revenue. Digital platforms such as Naked Wines, Vivino, and Cellars.com leverage data analytics and personalized recommendations to match consumers with niche or artisanal labels. A 2023 McKinsey & Company analysis revealed that DTC customers exhibit 2.5 times higher lifetime value than retail buyers and are more likely to engage with brand storytelling and virtual tastings. Subscription models and club memberships enhance retention, while blockchain authentication ensures provenance and reduces counterfeit risks. In China, Alibaba’s Tmall Global has become a key channel for European wineries, offering live-streamed tastings and same-day delivery. These digital ecosystems enable small producers to compete globally, democratizing access and redefining wine commerce.

Rise of Sustainable and Regenerative Viticulture offers a strategic growth avenue aligned with environmental and consumer priorities. As per the Intergovernmental Panel on Climate Change, vineyards are highly sensitive to temperature fluctuations, with rising global temperatures altering grape ripening cycles and regional suitability. The California Sustainable Winegrowing Alliance certifies over 50,000 acres of vineyards under its sustainability program, representing 40% of the state’s total. Consumers increasingly reward eco-conscious producers.

MARKET CHALLENGES

Climate Change-Induced Variability in Grape Yields and Quality remains a critical challenge for viticulture. Unpredictable weather patterns—such as early frosts, droughts, and excessive heat—are disrupting harvests and altering wine profiles. In 2021, a late spring frost in France destroyed an estimated 60% of potential grape production in Bordeaux and Burgundy, according to FranceAgriMer, leading to the smallest wine harvest in 60 years. The Journal of Agricultural and Food Chemistry points out that rising temperatures accelerate sugar accumulation in grapes while reducing acidity and aromatic complexity, compromising balance and typicity. In Australia, prolonged droughts have forced irrigation restrictions, with the Murray-Darling Basin Authority limiting water allocations by up to 30% in 2023. Additionally, increased pest pressure due to warmer winters threatens vine health. These climatic disruptions necessitate costly adaptations, including relocation of vineyards to cooler altitudes and investment in shade systems, challenging the economic and geographical stability of traditional wine regions.

Counterfeiting and Fraud in Premium Wine Segments undermine consumer trust and brand integrity, particularly in high-value markets. The most targeted labels include Domaine de la Romanée-Conti, Château Lafite Rothschild, and Screaming Eagle, with counterfeit bottles often fabricated using recycled authentic packaging. To combat this, producers are adopting forensic techniques such as carbon dating, isotope analysis, and NFC-embedded labels. However, the high cost of authentication infrastructure limits widespread implementation, leaving the premium segment vulnerable to reputational and financial risk.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.8% |

| Segments Covered | By Color, Taste, Product Type, Distribution Channel, and Region |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | E&J Gallo Winery, Constellations Brand, The Wine Group, Compagnia Del Vino SRL, Bacardi Limited, Caviro, Torres, Grupo Peñaflor SA, Treasury Wine Estates, Castel Group, Vina Conch, Toro, Distell Group, International Beverage Holdings, Global Drinks Finland, Amvyx SA, John Distilleries, Constellation Brands, Pernod Ricard, Gruppo Campari, Accolade Wines, Soyuz Victan, SPI Group, The Wine Group, and Diageo plc |

SEGMENTAL ANALYSIS

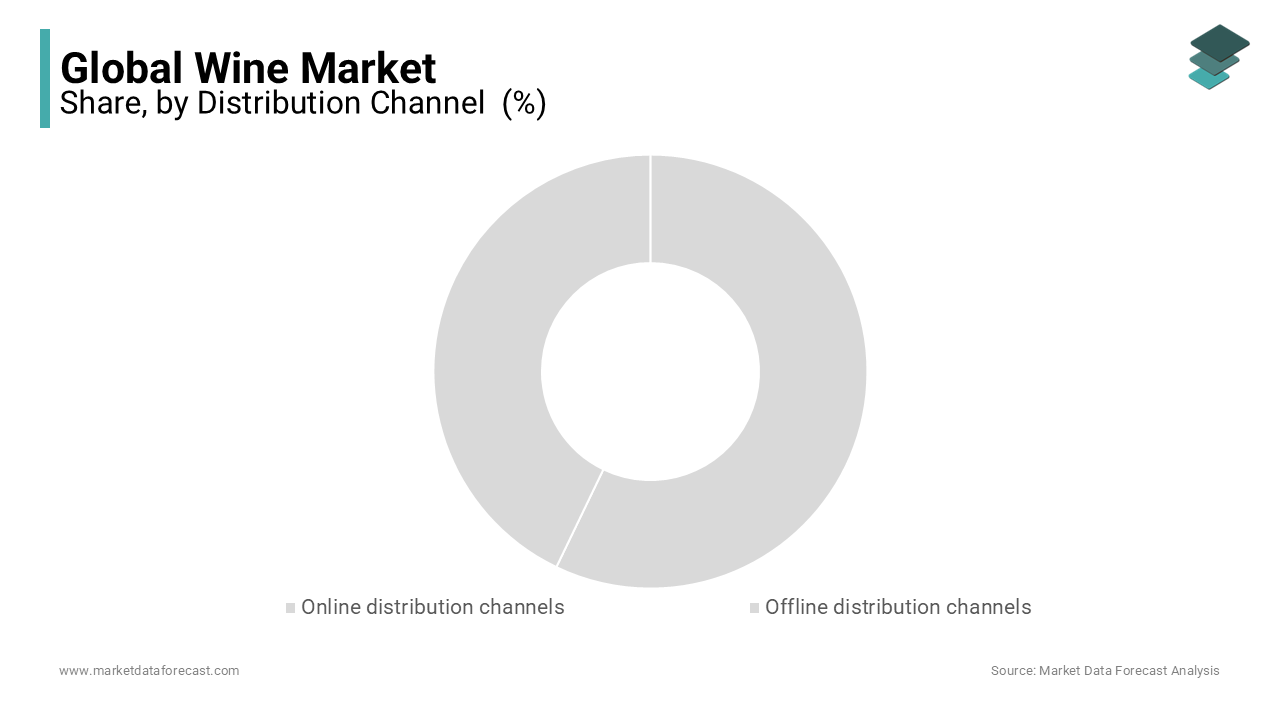

By Distribution Channel

The offline distribution segment continued to dominate the wine market by holding a significant share of total sales in 2025. This dominance is sustained by the tactile nature of wine purchasing, where consumers rely on in-store expertise, sensory evaluation, and immediate availability. Supermarkets, specialty wine shops, and restaurants remain primary access points, particularly for gift purchases and dining pairings. In Europe, independent cavistes and enotecas provide curated selections and personalized recommendations, enhancing trust. The immediacy of consumption and integration into social experiences reinforce offline retail’s entrenched role in wine commerce.

The online distribution segment is the fastest-growing channel and is projected to grow at a CAGR of 12.4% from 2026 to 2034. The surge is driven by digital adoption, subscription models, and enhanced consumer confidence in wine e-commerce. Platforms like Vivino, Naked Wines, and Amazon Wine leverage AI-driven recommendations, user reviews, and virtual tastings to guide purchasing decisions. Subscription clubs such as Firstleaf and Splendid Wines use algorithm-based curation to personalize offerings, increasing retention. With improved cold-chain logistics and age-verification systems, online platforms are overcoming earlier barriers, transforming digital wine retail into a scalable, high-margin channel.

By Color Insights

The red wine segment dominated the global wine market by capturing 54.6% of total volume consumption in 2025. This position is driven by its deep-rooted cultural integration in Mediterranean diets and perceived health benefits linked to moderate consumption. The American Heart Association shows that red wine contains resveratrol and polyphenols, compounds associated with reduced cardiovascular risk, which has reinforced its image as a functional beverage. Additionally, red varietals such as Cabernet Sauvignon, Merlot, and Pinot Noir are central to fine wine collecting and aging, with premium bottles from Bordeaux and Napa Valley commanding high auction values. These factors—ranging from health narratives to gastronomic tradition—have cemented red wine’s dominance across both casual and connoisseur segments.

The rose wine segment is the fastest-growing color segment and is projected to expand at a CAGR of 8.6% from 2026 to 2034. Its surge is fueled by shifting consumer preferences toward lighter, versatile, and Instagrammable beverages, particularly among Millennials and Gen Z. Rosé’s pale pink hue has become a symbol of lifestyle and leisure, heavily promoted in social media campaigns and summer festivals. Provence rosé from France has set the premium standard, inspiring New World producers in California, Spain, and South Africa to replicate its dry, crisp profile. Additionally, rosé’s adaptability in cocktails and food pairings enhances its appeal in casual dining and outdoor settings. With rosé now featured in canned, sparkling, and low-alcohol formats, its market evolution reflects broader trends in convenience, aesthetics, and experiential consumption.

By Taste Insights

The dry wine segment held the largest share of the taste segment of 68% of global wine consumption in 2025. This dominance is due to its alignment with contemporary palates that favor low-sugar, complex, and food-compatible profiles. The rise of health-conscious drinking has diminished the appeal of sweet wines, with the World Health Organization urging reductions in free sugar intake to below 10% of daily calories. Dry reds and whites, such as Sauvignon Blanc, Chardonnay, and Tempranillo, are staples in restaurant pairings and sommelier recommendations. Furthermore, dry wines are central to wine education and certification programs, reinforcing their status in professional and enthusiast circles. The expansion of wine tourism in regions like Tuscany and Mendoza further promotes dry varietals through tastings and vineyard experiences, solidifying their cultural and commercial preeminence.

The sweet wine segment is the fastest-growing taste category in terms of value and is projected to grow at a CAGR of 7.3% from 2026 to 2034. This growth is driven by strategic repositioning in emerging markets and premiumization in dessert and gifting segments. In Asia, particularly China and India, sweet wines such as Moscato, Port, and late-harvest Rieslings are perceived as approachable entry points for novice consumers. Besides, luxury sweet wines like Sauternes and Tokaji are gaining traction among high-net-worth collectors due to their rarity and aging potential. Wineries in Hungary and Germany have invested in limited-edition releases with artisanal packaging, enhancing exclusivity. With effective marketing and cultural relevance, sweet wine is overcoming historical stigmas and carving a niche in both mass and premium markets.

By Product Type

The still wine segment remained the largest product type by commanding a substantial share of the global wine market by volume in 2025. Its dominance is rooted in its ubiquity as the default form of wine consumed with meals, celebrations, and social gatherings. Still wine, encompassing red, white, and rosé varieties without carbonation, is produced in over majority of the world’s vineyards, from traditional regions like Tuscany and Rioja to emerging areas in South America and China. Consumer familiarity, lower production costs, and compatibility with diverse cuisines sustain its market leadership. Besides, still wine forms the base for many wine-based education programs, certifications, and competitions, reinforcing its centrality in both trade and culture. Its versatility across price points, from everyday table wine to Grand Cru, ensures broad accessibility and enduring relevance across geographies and demographics.

The sparkling wine segment is the fastest-growing product type and is projected to expand at a CAGR of 9.1% from 2026 to 2034. This acceleration is driven by its association with celebration, premiumization, and evolving consumption occasions beyond formal events. While Champagne remains iconic, Prosecco from Italy and Cava from Spain have democratized access with affordable, high-volume offerings. Besides, rosé sparkling wines and low-alcohol variants are attracting younger consumers. Brands like Freixenet and La Marca have leveraged digital marketing and influencer partnerships to rebrand sparkling wine as a lifestyle product, fueling sustained demand across urban and aspirational markets.

REGIONAL ANALYSIS

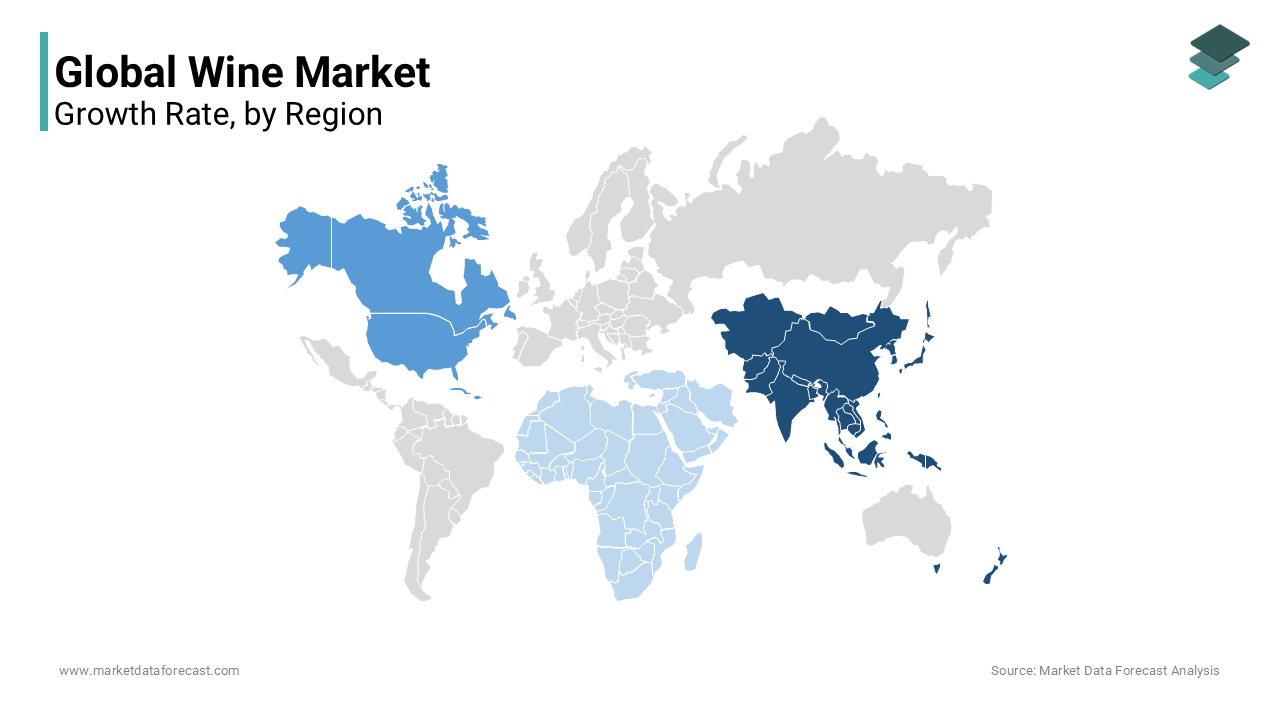

Europe led the global wine market with a 46.3% share in 2025. The region’s dominance is anchored in its status as both the largest producer and consumer, with countries like Italy, France, and Spain dominating global vineyard area. The European Commission confirms that the EU produces approximately 160 million hectoliters of wine annually, nearly half the world’s total. Wine is deeply embedded in daily life and gastronomy, with per capita consumption in Portugal and Italy exceeding 50 liters annually. Additionally, the EU’s Protected Designation of Origin (PDO) system safeguards regional authenticity, enhancing export value. Germany and the UK are major import hubs, with strong demand for premium and organic wines. With robust infrastructure, centuries-old winemaking traditions, and supportive agricultural policies, Europe remains the cultural and commercial nucleus of the global wine industry.

North America is also a major player in the market. The U.S. is the world’s fourth-largest wine producer and the largest importer by value, with California’s Napa and Sonoma valleys setting global quality benchmarks. The growth of wine tourism, generating over $8 billion annually, according to Visit California, has strengthened brand engagement. Canadian consumers are also shifting toward premium imports, particularly from France and Italy. With high disposable income, evolving palates, and digital retail maturity, North America remains a dynamic engine of innovation and consumption.

Asia Pacific holds a significant share. China is the world’s largest red wine market by volume, with urban consumers associating wine with modernity and social status. In Japan, aging demographics and shrinking beer consumption have increased interest in wine, particularly dry reds. Australia, both a producer and consumer, has seen domestic wine sales grow annually since 2020, driven by premiumization and sustainability claims. E-commerce platforms like Tmall and Rakuten are accelerating access, while wine education programs are reducing knowledge gaps. Despite cultural barriers, rising affluence and Western influence are steadily expanding the region’s wine footprint.

Latin America accounts for a notable share of the global market, with Argentina, Brazil, and Chile driving regional dynamics. Argentina is renowned for its Malbec, which constitutes over 50% of domestic red wine production. Brazilian consumers are increasingly shifting from beer to wine in social settings. Chile, a major exporter, produced a notable liters in 2023. Domestic markets are expanding due to rising middle-class affluence and the growth of wine bars in cities like São Paulo and Santiago. While traditional consumption lags behind Europe, urbanization and culinary globalization are fostering a new wine culture, positioning Latin America as a producer and emerging consumer market.

Middle East and Africa collectively hold 6% of the market, with South Africa, Israel, and the UAE leading development. South Africa is Africa’s largest wine producer. Chenin Blanc and Pinotage are signature varietals gaining international acclaim. In the Gulf, expatriate demand and luxury hospitality drive premium wine sales in Dubai and Doha. The UAE’s free-trade zones allow duty-free import and distribution, making it a regional hub. Israel’s boutique wineries, such as Yatir and Golan Heights, have earned global accolades, boosting export potential. Despite religious restrictions in some countries, secular urban centers and tourism sectors sustain demand. With growing wine tourism and investment in sustainable viticulture, the region is gradually expanding its footprint in the global wine ecosystem.

LEADING PLAYERS IN THE WINE MARKET

Treasury Wine Estates (TWE) has solidified its leadership in the Asia Pacific wine market through strategic brand positioning and deep regional integration. The Australian-based company owns premium labels such as Penfolds, Wolf Blass, and 19 Crimes, with Penfolds Grange achieving iconic status among Chinese collectors. The company also expanded its direct-to-consumer (DTC) model through e-commerce partnerships with Alibaba’s Tmall and JD.com, enabling live-streamed tastings and same-day delivery. Additionally, TWE invested in sustainable viticulture across its Barossa Valley and Napa estates, aligning with regional demand for eco-conscious luxury products. By combining heritage branding with technological innovation, TWE has strengthened its dominance in high-value urban markets across China, South Korea, and Singapore.

Pernod Ricard has significantly influenced the Asia Pacific wine landscape through its portfolio of premium and accessible brands, including Jacob’s Creek, Brancott Estate, and Campo Viejo. The company has localized its marketing strategies to align with cultural preferences, such as launching limited-edition Lunar New Year packaging for Jacob’s Creek in China and Taiwan. The company also partnered with luxury hotels and fine-dining chains across India and Southeast Asia to integrate its wines into curated beverage menus. By leveraging its global distribution network and emphasizing sustainability, Brancott Estate achieved carbon neutrality in 2023. Pernod Ricard has enhanced brand credibility and accessibility, positioning itself as a bridge between Old World tradition and New World consumer dynamics.

E. & J. Gallo Winery has expanded its footprint in the Asia Pacific by focusing on quality segmentation, digital engagement, and strategic imports. The U.S.-based winery introduced its premium brands—Orin Swift, William Hill, and MacMurray Ranch—into Japan, South Korea, and Australia, targeting affluent urban consumers and wine enthusiasts. In 2023, Gallo partnered with Australian retailers like Dan Murphy’s to launch exclusive single-vineyard releases, supported by augmented reality labels that provide immersive storytelling. The company also acquired a stake in a New Zealand sauvignon blanc producer to strengthen its cool-climate portfolio for export. Gallo’s investment in cold-chain logistics ensures product integrity across tropical markets. By combining technological innovation with premium branding and regional adaptation, Gallo has elevated its presence beyond bulk imports, establishing itself as a curator of high-quality, experience-driven wine offerings in the region.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Wine Market are deploying premiumization, digital traceability, direct-to-consumer models, regional flavor adaptation, and sustainability certification to strengthen their market positions. Companies are investing in blockchain authentication and QR-coded labels to combat counterfeiting and enhance transparency. Expansion into e-commerce and subscription platforms enables personalized engagement and higher margins. Premium brands emphasize terroir, limited editions, and vintage storytelling to appeal to collectors and affluent consumers. In emerging markets, localization of packaging, flavor profiles, and gifting formats enhances cultural relevance. Additionally, investment in regenerative viticulture and carbon-neutral production aligns with environmental expectations. Strategic partnerships with luxury hospitality, airlines, and retail chains amplify visibility and reinforce brand prestige across diverse consumer touchpoints.

KEY MARKET PLAYERS AND COMPETITION OVERVIEW

Major Key Players in the global wine market are E&J Gallo Winery, Constellation Brands, The Wine Group, Compagnia Del Vino SRL, Bacardi Limited, Caviro, Torres, Grupo Peñaflor SA, Treasury Wine Estates, Castel Group, Vina Conch, Toro, Distell Group, International Beverage Holdings, Global Drinks Finland, Amvyx SA, John Distilleries, Constellation Brands, Pernod Ricard, Gruppo Campari, Accolade Wines, Soyuz Victan, SPI Group, The Wine Group, and Diageo plc.

The competition in the Wine Market is intensifying as global conglomerates, boutique wineries, and new-market entrants compete across quality, provenance, and consumer experience. Established players leverage brand equity, distribution scale, and technological innovation to maintain dominance, while smaller producers differentiate through terroir authenticity, organic certification, and artisanal narratives. Digital platforms and DTC models are disrupting traditional retail hierarchies, enabling niche brands to reach global audiences. Pricing polarization is evident, with growth concentrated in both ultra-premium and value segments. Regulatory complexity, climate vulnerability, and shifting consumption patterns add layers of strategic risk. As consumer expectations evolve toward sustainability, transparency, and experiential value, companies must innovate continuously to preserve relevance, loyalty, and long-term market positioning in a culturally rich yet commercially volatile industry.

RECENT HAPPENINGS IN THE MARKET

- In January 2023, Treasury Wine Estates launched a blockchain-based authentication system for Penfolds in China, allowing consumers to verify the provenance of premium bottles in the Wine Market.

- In May 2023, Pernod Ricard introduced limited-edition Lunar New Year packaging for Jacob’s Creek in Taiwan and Hong Kong, enhancing cultural resonance and gifting appeal in the Wine Market.

- In September 2023, E. & J. Gallo Winery partnered with Dan Murphy’s in Australia to release an exclusive line of single-vineyard wines with augmented reality labels in the Wine Market.

- In February 2025, Constellation Brands expanded its distribution of Kim Crawford wines in Japan through a collaboration with Suntory’s retail network in the Wine Market.

- In April 2025, Accolade Wines launched a carbon-neutral version of Hardys Ultimate Collection in Singapore, certified under the CarbonTrust standard in the Wine Market.

DETAILED SEGMENTATION OF THE GLOBAL WINE MARKET IS INCLUDED IN THIS REPORT

This research report on the global wine market has been segmented and sub-segmented based on color, taste, product type, distribution channel & region.

By Color

- Rosé wines

- Red wines

- White wines

By Taste

- Dry

- Medium

- Sweet

By Product Type

- Sparkling wines

- Dessert wines

- Still wines

- Fortified wines

By Distribution Channels

- Online distribution channels

- Offline distribution channels

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. What are the current trends in the wine market?

The current trends in the wine market are increased demand for organic and sustainable wines, Growth of online wine sales and direct-to-consumer models, rising popularity of premium and luxury wines, and Expansion of wine tourism and experiential offerings.

2. What are the challenges facing in the wine market?

The Challenges facing the wine market are Competition from other alcoholic beverages like craft beer and spirits, Fluctuations in grape yields and quality due to climate variability, and Compliance with regulatory requirements and labeling standards.

3. What factors are influencing the growth of the wine market?

The factors influencing the growth of the wine market are changing consumer lifestyles and preferences, the Influence of social media and digital marketing on consumer behavior, and the Growing interest in wine as a cultural and social experience.

4. What factors are driving growth in the wine market?

Growth is driven by increasing global wine consumption, premiumization trends, rising interest in wine tourism, and growing demand for organic and sustainably produced wines.

5. Which types of wine dominate the market?

Still wine dominates the market, followed by sparkling wine and fortified wine, with red, white, and rosé wines catering to diverse consumer preferences.

6. Who are the major consumers in the wine market?

Key consum77ers include millennials, premium alcohol consumers, hospitality industry customers, and wine enthusiasts seeking quality and variety.

7. How is premiumization influencing the wine market?

Premiumization is driving demand for high-quality, aged, and limited-edition wines as consumers prioritize taste, origin, and brand storytelling.

8. How is e-commerce affecting wine sales?

Online wine retail is growing rapidly due to convenience, wider product selection, and direct-to-consumer sales enabled by digital platforms.

9. What innovations are emerging in the wine market?

Innovations include low-alcohol and alcohol-free wines, smart vineyard technologies, sustainable packaging formats, and flavor experimentation.

10. What is the future outlook for the wine market?

The wine market is expected to grow steadily, supported by premiumization, sustainability initiatives, expanding wine culture in emerging markets, and digital transformation.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com