Global Whiskey Market Size, Share, Trends & Growth Forecast Report - Segmented By Product (Malt Whisky, Wheat Whisky, Rye Whisky, Corn Whisky, Blended Whisky, Others), Premium (Premium, High End Premium, Super Premium), And Region (North America, Europe, APAC, Latin America, Middle East And Africa) – Industry Analysis From 2026 To 2034

Market Size, 2025

$69.82 BnMarket Estimate, 2026

$74.29 BnMarket Forecast, 2034

$122.03 BnCAGR, 2026–2034

6.4%Global Whiskey Market Size

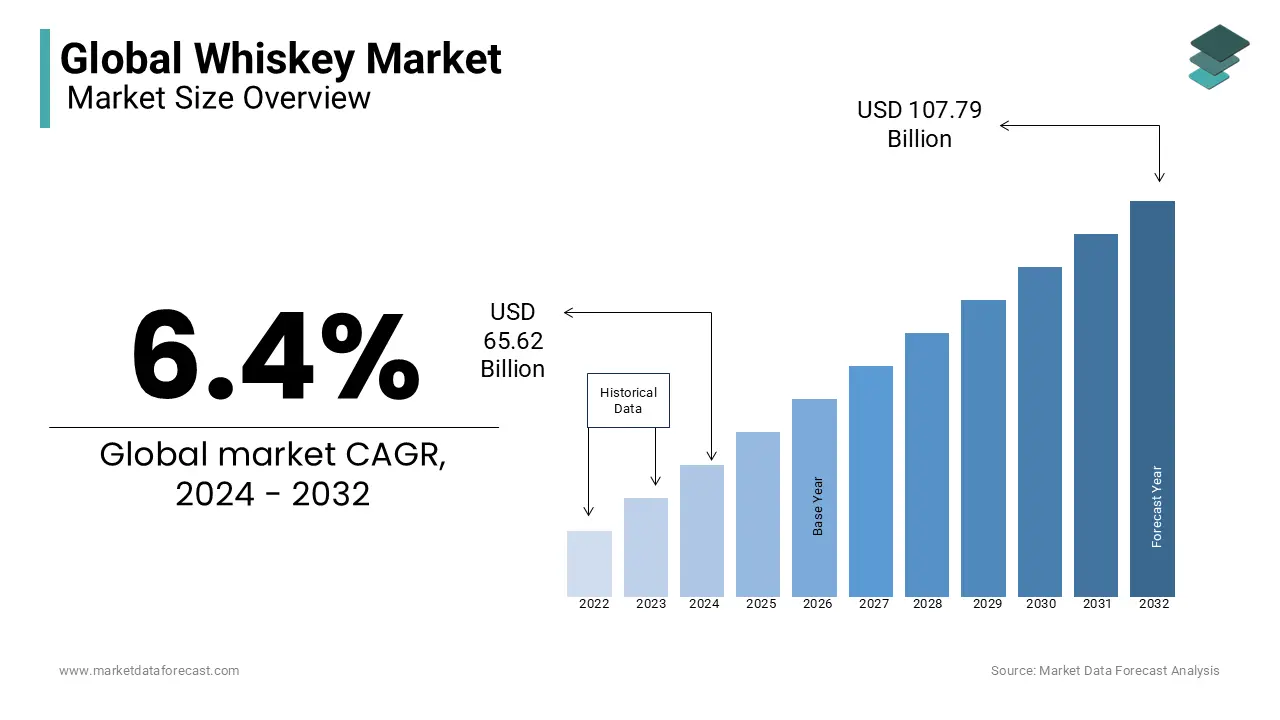

The global whiskey market size was calculated to be USD 69.82 billion in 2025 and is anticipated to be worth USD 122.03 billion by 2034 from USD 74.29 billion in 2026, growing at a CAGR of 6.4% during the forecast period. The whiskey is distilled alcoholic beverage derived from fermented grain mash, including variants such as Scotch, bourbon, rye, Irish, and Japanese whiskey.

MARKET DRIVERS

The rising engagement of younger consumers, particularly millennials and Gen Z, who are redefining consumption patterns through experiential and premiumization trends is accelerating the growth of the Whiskey Market. As per a 2023 study by the International Wine and Spirit Research (IWSR), consumers aged 21–35 now account for 38% of global whiskey volume growth, favoring small-batch, craft, and flavored expressions. The growing demand for the transparency, provenance, and mixability, integrating whiskey into cocktails rather than consuming it neat is also to elevate the growth of the Whiskey Market.

The expansion of global trade networks and duty-friendly export agreements that facilitate market access in emerging economies is accelerating the growth of the Whiskey Market. According to the World Trade Organization, bilateral alcohol tariff reductions between the U.S. and South Korea have led to a 35% increase in American whiskey exports to Asia over the past three years. These regulatory and logistical advancements are lowering entry barriers and accelerating the global diffusion of regional whiskey varieties beyond their traditional strongholds.

MARKET RESTRAINTS

The prolonged production cycle inherent to aged spirits, which limits supply elasticity and responsiveness to demand surges is impeding the growth of the whiskey market. As per the Distilled Spirits Council of the United States, bourbon must be aged in new charred oak barrels for at least two years to qualify as "straight," with many premium expressions requiring 10 to 20 years of maturation. This creates a time lag where increased demand today cannot be met for over a decade, risking market shortages. In 2022, the Scotch Whisky Association reported that some single malt inventories had dwindled to less than five years of supply due to unforeseen global demand spikes post-pandemic. Additionally, climate conditions in aging warehouses directly impact evaporation rates; in Kentucky, the "angel’s share" averages 4% per year, rising to 12% in hotter regions like India, according to the University of Kentucky’s Department of Food Science.

The tightening of alcohol regulation and taxation in multiple jurisdictions, which dampens consumer affordability and retail availability is degrading the growth of the whiskey market. According to the World Health Organization, 126 countries have implemented or increased excise taxes on spirits since 2020, with Lithuania imposing a 50% tax hike on whiskey in 2023 and Thailand raising duties by 30% in 2022. These fiscal policies are often justified by public health objectives, but they disproportionately affect moderate-income consumers and independent retailers.

MARKET OPPORTUNITIES

The digitization of whiskey commerce and ownership through blockchain-enabled provenance tracking and fractional investment platforms is greatly influencing the growth of the whiskey market. As per PwC’s 2025 Global Spirits Report, blockchain adoption in premium spirits has grown by 40% since 2022, allowing consumers to verify authenticity, distillation date, and barrel lineage via QR codes. This trend is particularly strong among high-net-worth individuals in Asia and the Middle East, where collectible Japanese and Scotch whiskies have appreciated by an average of 14% annually over the past five years, according to Knight Frank’s Luxury Investment Index.

The strategic localization of production in non-traditional markets, where craft distilleries are leveraging regional ingredients and terroir to create distinctive expressions, which is ascribed to bolster the growth of the whiskey market. As per the Asia Pacific Spirits Conference 2023, Japan’s Nikka and Taiwan’s Kavalan have earned global acclaim, with Kavalan winning over 300 international awards since 2008, challenging Scotch dominance. India now hosts more than 180 craft distilleries producing single malts from locally grown barley and Himalayan water, with Amrut and Paul John gaining export traction.

MARKET CHALLENGES

The vulnerability of supply chains to climate change in sourcing raw materials and maintaining consistent water quality is to slow down the growth of the whiskey market. The Scotch Whisky Association warns that prolonged droughts could disrupt production at over 140 distilleries reliant on local rivers and aquifers. Similarly, in the U.S., the 2022 Midwest drought reduced corn output by 12%, a key component in bourbon mash bills, as reported by the U.S. Department of Agriculture. Rising temperatures also affect barrel aging dynamics; warmer warehouses increase evaporation and alter flavor development, leading to inconsistent batch profiles.

The proliferation of counterfeit whiskey, which undermines brand integrity, consumer safety, and revenue is additionally to enhance the growth of the whiskey market. As per INTERPOL’s Operation Ostro 2023, authorities seized over 1.2 million liters of fake spirits across 40 countries, with premium Scotch and Japanese whiskies being the most replicated. The economic toll is substantial; the European Union Intellectual Property Office estimates that counterfeit spirits cost legitimate producers over €2.3 billion annually in lost sales.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 6.4% |

| Segments Covered | By product, premium & Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC; PESTLE Analysis. Porter’s Five Forces Analysis, Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Accolade Wines, Angus Dundee Distillers Plc, Constellation Brands, Inc., Allied Blenders and Distillers Pvt. Ltd., Bacardi Limited, Affymetrix, Inc., Alko, Asahi Brewers, Bruker Corporation, and Danaher Corporation |

SEGMENTAL ANALYSIS

By Product Insights

The blended whiskey segment dominated the global whiskey market by capturing 52.3% of the share in 2025 with its broad consumer accessibility and cultural entrenchment in high-volume markets such as India and the Philippines. Blended whiskey combines malt and grain spirits, offering a smoother, more approachable flavor profile that appeals to novice drinkers and those preferring milder alcoholic beverages. In India, where blended whiskey accounts for over 90% of total whiskey consumption, brands like Officer’s Choice and Royal Stag achieve annual sales exceeding 40 million cases, according to the Confederation of Indian Alcoholic Beverage Companies.

The rye whiskey segment is expected to grow at a CAGR of 9.6% during the forecast period with the resurgence in classic cocktail culture in North America and Western Europe. The Distilled Spirits Council of the United States reports that American rye whiskey sales increased by 18% in volume between 2021 and 2023, outpacing overall whiskey growth. Consumer interest in authenticity and bold flavor profiles, coupled with mixology-driven demand, is propelling rye into a new era of premium relevance.

By Quality Insights

The premium whiskey segment was the largest and held 48.3% of the whiskey market share in 2025 with a shift toward elevated drinking experiences, where consumers increasingly associate quality with craftsmanship, provenance, and brand storytelling. In the United States, premium spirits represent 62% of total whiskey sales by value, according to the Distilled Spirits Council, with brands like Maker’s Mark and Talisker experiencing double-digit growth. These products benefit from strategic marketing, limited editions, and aging narratives that enhance desirability.

The super premium segment is lucratively growing with a projected CAGR of 11.3% during the forecast period owing to the rising disposable incomes, the expansion of luxury retail, and the growing influence of collectors and investors.

REGIONAL ANALYSIS

North America was the top performer in the global whiskey market with a 41.3% of share in 2025 with the commercial and cultural epicenter of bourbon and rye production. The United States dominated the market due to its robust domestic distilling industry and deeply rooted whiskey heritage. Domestic consumption remains strong, with over 75% of U.S. households purchasing whiskey at least once a year, as reported by the U.S. Census Bureau’s Current Expenditure Survey. Urban centers like Louisville and Nashville have become whiskey tourism hubs, while digital platforms facilitate direct-to-consumer sales.

The Europe whiskey market held 28.3% of the share in 2025 with its historical stewardship of Scotch, Irish, and continental whiskey traditions. Scotland alone produces over 1.3 billion liters of Scotch annually, with 90% exported to more than 200 countries, as reported by the Scotch Whisky Association. In Western Europe, on-premise consumption in high-end bars and restaurants drives demand for aged and single cask expressions. Eastern Europe, particularly Poland and the Baltic states, has seen rising domestic consumption, with local distilleries adopting Scottish and American techniques.

Asia-Pacific (APAC) whiskey market growth is propelled by rapid economic development and shifting social attitudes toward premium spirits. Japan with Japanese single malts like Hibiki and Hakushu winning international acclaim and reshaping global taste preferences. The Japan Distilling Association confirms that domestic whiskey production has doubled since 2015, despite supply constraints from aging stock shortages.

Latin America's whiskey market growth is driven by the consumer preferences and increasing penetration of international brands. According to the Latin American Spirits Monitor, whiskey sales in Mexico grew by 12% in 2023, driven by American bourbon and Canadian blends.

Middle East and Africa (MEA) whiskey market growth is propelled with the concentrated in affluent Gulf states and select African economies. High-net-worth travelers from across Asia and Africa contribute significantly to luxury whiskey purchases, particularly limited-edition Scotch and Japanese releases.

LEADING PLAYERS IN THE WHISKEY MARKET

Diageo

Diageo maintains a dominant presence in the global whiskey market by leveraging an extensive portfolio that includes Johnnie Walker, Talisker, and Bulleit Bourbon. In the Asia-Pacific region, the company has intensified its focus on premiumization and digital engagement, launching augmented reality (AR)-enabled labels for Johnnie Walker Blue Label in China and South Korea to enhance consumer interaction. In 2023, Diageo opened a dedicated APAC Whiskey House in Singapore, serving as a cultural hub for tastings, education, and brand storytelling. The company has also partnered with luxury hotels and high-end bars across Tokyo, Sydney, and Mumbai to promote exclusive releases.

Pernod Ricard

Pernod Ricard has dominant position in the whiskey market through strategic ownership of premium brands such as Chivas Regal, The Glenlivet, and Jameson, with a strong emphasis on innovation and sustainability in the Asia-Pacific region. The company launched Chivas Regal Ultis, a luxury blended malt, specifically targeting high-net-worth consumers in China and Southeast Asia, supported by VIP gifting programs and art-inspired packaging. In 2022, Pernod Ricard established a whiskey innovation lab in Shanghai to develop region-specific flavor profiles and consumer experiences. It has also committed to carbon-neutral distillation across its APAC operations by 2030, aligning with regional environmental priorities.

Suntory Global Spirits

Suntory Global Spirits, renowned for its Japanese whiskey legacy through Yamazaki, Hakushu, and Hibiki, has elevated the global perception of Asian whiskey craftsmanship. In the Asia-Pacific market, the company has capitalized on national pride and cultural heritage, positioning its premium expressions as symbols of Japanese excellence. Despite supply constraints due to aging stock shortages, Suntory has maintained exclusivity through limited annual releases and digital allocation systems in Japan and Hong Kong. In 2023, it launched the “House of Suntory Whisky” in Tokyo, integrating education, tasting, and archival exhibits to deepen consumer connection. The company has also expanded distribution partnerships in Vietnam and Indonesia, while promoting responsible consumption through its “Savour the Moment” campaign.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the whiskey market are deploying brand premiumization, digital innovation, geographic expansion, product diversification, and sustainability initiatives to strengthen their global standing. Companies are launching limited editions and aged expressions to appeal to collectors and high-income consumers. Digital tools such as blockchain authentication, AR labeling, and virtual tastings are enhancing engagement. Expansion into emerging markets like India, China, and Southeast Asia is prioritized through localized flavors and e-commerce integration. Distilleries are diversifying portfolios with flavored whiskeys, ready-to-drink (RTD) variants, and non-alcoholic alternatives. Sustainability efforts include carbon-neutral distillation, water recycling, and eco-friendly packaging. Strategic acquisitions of craft distilleries and experiential spaces like whiskey houses further consolidate brand authority and consumer loyalty across evolving market landscapes.

KEY MARKET PLAYERS AND COMPETITION OVERVIEW

Key Market Players of the Whiskey Market include Accolade Wines, Angus Dundee Distillers Plc, Constellation Brands, Inc., Allied Blenders and Distillers Pvt. Ltd., Bacardi Limited, Affymetrix, Inc., Alko, Asahi Brewers, Bruker Corporation, and Danaher Corporation

The competition in the whiskey market is intensifying as multinational corporations, regional distillers, and craft producers vie for dominance across value, quality, and experiential dimensions. While legacy brands leverage heritage and global distribution, emerging players differentiate through terroir-driven expressions and agile innovation. The battleground has shifted from mere availability to storytelling, authenticity, and digital engagement in high-growth regions like Asia-Pacific. Premiumization and scarcity marketing are central to brand positioning, with limited releases fueling secondary market speculation. E-commerce and direct-to-consumer models are disrupting traditional retail hierarchies. Simultaneously, sustainability and ethical production are becoming competitive differentiators.

RECENT HAPPENINGS IN THE MARKET

- In June 2023, Diageo launched an augmented reality experience for Johnnie Walker Blue Label in China that allows consumers to scan bottles and access immersive content on heritage and craftsmanship by enhancing brand engagement in high-value retail channels.

- In February 2025, Pernod Ricard opened a whiskey innovation center in Shanghai dedicated to developing Asia-specific flavor profiles and digital consumer experiences with its regional relevance and premium positioning.

- In October 2023, Suntory Global Spirits introduced a blockchain-powered authentication system for Yamazaki 18-Year-Old by enabling buyers in Hong Kong and Singapore to verify provenance and combat counterfeiting.

- In January 2025, Brown-Forman expanded its Jack Daniel’s distillery in Lynchburg, Tennessee by increasing production capacity by 40% to meet surging global demand, particularly in Europe and Latin America.

- In August 2023, Chivas Brothers launched a carbon-neutral distillation pilot at its Strathisla facility in Scotland that aligns with Diageo’s broader net-zero strategy and strengthening environmental credibility in premium markets.

DETAILED SEGMENTATION OF GLOBAL WHISKEY MARKET INCLUDED IN THIS REPORT

This research report on the global whiskey market has been segmented and sub-segmented based on product, premium, & region.

By Product

- Malt Whisky

- Wheat Whisky

- Rye Whisky

- Corn Whisky

- Blended Whisky

By Quality

- Premium

- High-End Premium

- Super Premium

By Region

- North America

- Europe

- The Asia Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

1. What factors influence the price of whiskey?

Several factors can influence whiskey's price, including its age (older whiskies tend to be more expensive), rarity or limited availability, brand reputation, and quality of the ingredients and production process.

2. What are some emerging trends in the whiskey market?

Some emerging trends in the whiskey market include the rise of craft distilleries, increased interest in experimental and innovative whiskey styles, growing demand for premium and luxury whiskies, and a focus on sustainability and environmental practices in production.

3. Is whiskey a good investment?

Whiskey can be a good investment for collectors and enthusiasts, especially rare or limited-edition bottles from reputable distilleries. However, like any investment, it comes with risks and requires knowledge of the market and industry trends.

4. What are the main types of whiskey available in the market?

Major types include Scotch whisky, Irish whiskey, American whiskey (bourbon and rye), Canadian whisky, and other regional and craft whiskies.

5. What factors are driving the growth of the whiskey market?

Key drivers include premiumization, rising disposable incomes, growing interest in craft and aged spirits, expanding cocktail culture, and increasing global exports.

6. How does premium and super-premium whiskey impact market growth?

Premium and super-premium whiskey segments drive higher value growth due to consumer willingness to pay for aged, small-batch, and heritage brands.

7. What role does aging play in whiskey production and pricing?

Aging enhances flavor and quality, increases production costs, and significantly influences pricing, making aged whiskies more valuable in the market.

8. What are the key distribution channels for whiskey?

Key channels include liquor stores, supermarkets and hypermarkets, bars and restaurants, duty-free outlets, and e-commerce platforms where permitted.

9. What challenges does the whiskey market face?

Challenges include strict alcohol regulations, high taxation, long production cycles, supply chain constraints, and growing competition from other spirits.

10. What is the future outlook for the whiskey market?

The market is expected to grow steadily, supported by premiumization, global brand expansion, emerging markets, and continued innovation in flavors and finishes.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com