Global Personal Mobility Devices Market Size, Share, Trends & Growth Forecast Report By Product, End-User and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa) – Industry Analysis, 2026 to 2034

Market Size, 2025

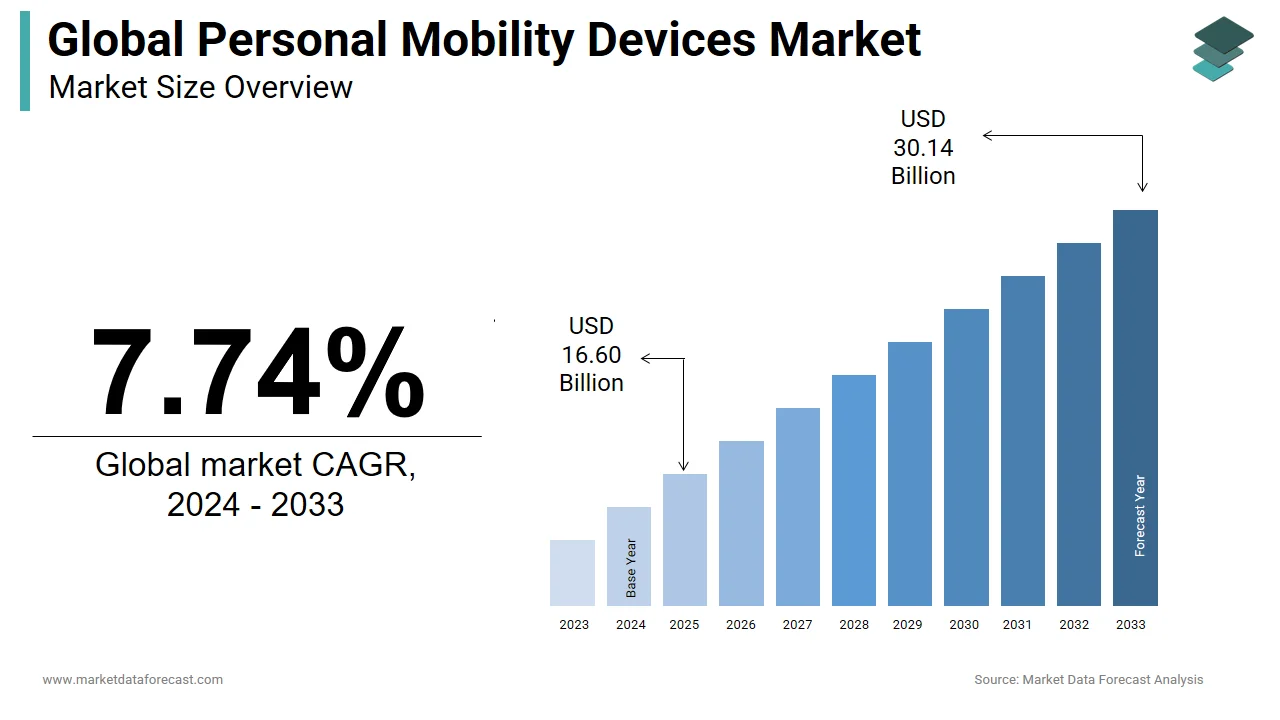

$16.60 BnMarket Estimate, 2026

$17.88 BnMarket Forecast, 2034

$32.47 BnCAGR, 2026–2034

7.74%Global Personal Mobility Devices Market Size

The global personal mobility devices market was valued at USD 16.60 billion in 2025, is estimated to reach USD 17.88 billion in 2026, and is projected to reach USD 32.47 billion by 2034, growing at a CAGR of 7.74% from 2026 to 2034.

Personal mobility devices (PMDs) are medical devices that assist people with physical disabilities or the elderly move from one location to another. These devices can be battery-powered or operated manually and can be combined with additional items for travel and self-sufficiency. PMDs allow people with disabilities to do basic tasks independently. Also, impaired athletes utilize these devices to compete in Paralympic sporting events. So, multiple models of these devices have been designed for different games. Individuals facing mobility issues due to age or disability use personal mobility devices. Governing bodies in several nations are already taking practical steps and initiatives to improve access to high-quality PMDs at a reasonable cost.

MARKET DRIVERS

The growing aging population worldwide, increasing number of product launches by the market participants and rising number of incidents resulting in disability are propelling the personal mobility devices market.

The personal mobility devices market is expected to grow significantly over the forecast period due to technological advancements in devices, such as portable systems. Furthermore, the prevalence of chronic diseases like coronary heart disease, heart failure, and diabetes is increasing, boosting the market growth. Similarly, the rise in the senior population across the world who are more vulnerable to injuries or medical issues that necessitate medical help contributes to developing the personal mobility devices market. In addition, non-fatal injuries and physical disabilities due to road traffic collisions are surging worldwide. Apart from this, the market's growth is aided by the widespread availability of reimbursement policies for purchased and rented PMDs. The use of bicycles and electric scooters in vacation destinations has also fuelled the market expansion. Further, the introduction of smart city efforts in several regional pockets caused advances in personal mobility device manufacture.

Personal mobility devices are becoming more popular in several regions worldwide. These devices are beneficial for those who have rheumatoid arthritis and osteoporosis, among other serious illnesses. Hence, the growing number of patients with these conditions is expected to elevate the demand for personal mobility devices during the forecast period. Also, in the coming years, innovations in medical device technology for patient mobility and a growth in the requirement for personal mobility devices in emerging nations are projected to create potential market expansion opportunities. Moreover, in recent years, the tourism industry has risen as a significant consumer of PMDs.

MARKET RESTRAINTS

High costs associated with these devices are majorly hampering the global market growth.

Some of the major factors hindering the market growth throughout the forecast period are the high cost of these devices, limited expertise, and complexities associated with personal mobility devices. In addition, the personal mobility devices market is likely to be hampered by a lack of awareness among individuals about novel and technologically advanced equipment, as well as the lack of rehabilitation centers and low access to rehabilitation centers.

People with flexibility issues use PMDs daily and are often bought on an emergency basis to walk stably. So, these devices should be affordable for patients. Most of the time prices are set targeting a particular customer category. For instance, the cost of an advanced wheelchair is close to USD 7100 whereas that of a wheelchair with extra functions ranges between USD 1000 and 2000. Moreover, a specialized wheelchair called Scewo BRO is priced at more than USD 40500. Also, the stable and strong rollator walkers can be purchased for around USD 600. Such variations in PDMs are a serious challenge for the developing and emerging economies.

MARKET OPPORTUNITIES

The increase in the elderly population in several countries, such as China, is providing lucrative prospects for the personal mobility devices market.

The emergence of IoT-based PMDs is also accelerating the market growth. This allows real-time data transfer to smartphones and tablets for continuous tracking. Day by day the ability to perform physically demanding tasks and activities is reducing among both young and old people. So, it is anticipated that more geriatric individuals will be using PMDs in the future. As per WHO, around 22 percent of people, up from 12 percent in 2015, will be more than 60 years of age. Further, low and middle-income countries will have close to 80 percent of old people. So, in November 2023, a handless sitting personal mobility device, “Uni-One,” was introduced by Honda for individuals with able-bodied and mobility issues.

MARKET CHALLENGES

The personal mobility devices market expansion is restricted due to regulatory problems and inefficiency in long distances. E-PMDs are well-suited for short journeys between 0.8 and 3.2 km. Also, because of their high expenditure on long trips, these will not be preferred over traditional alternatives. In addition, though Europe is the leading market, it is in a position where the excitement for technological advances usually leads to its general application. So, significant effort is required to avoid negative results instead of simply presenting it for large consumption. PMDs are in the early stages which has caused regulatory issues. For instance, the Australian road rules haven't been amended or modified for the rapid increase in PMDs. So, due to the absence of nationwide uniformity, they are used in an unspecified legal environment. Additionally, the adoption of modern personal mobility devices is also restricted because several governments in emerging countries still do not provide repayments for this product.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Connectivity, End User and Region |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Market Leaders Profiled | Drive DeVilbiss Healthcare, GF Health Products, Inc., Invacare Corporation, Carex Health Brands, Inc., Kaye Products, Inc., Briggs Healthcare, Medline Industries, Inc., NOVA Medical Products, Performance Health, and Rollz International |

SEGMENTAL ANALYSIS

By Product Insights

The wheelchair segment is leading the personal mobility devices market. It is a common form of personal mobility aid. Some of the factors driving the industry forward are a growing trend of wheelchair-mounting equipment, the rising spinal cord conditions and associated disablements and the growing ageing population. The wheelchair equipment includes the introduction of electric wheelchairs and those that can preserve the medical history of disabled people and also make emergency calls during disasters and monitor human health. Moreover, the growing geriatric population is another important driver of market expansion. These are more susceptible to mobility problems. For instance, in December 2023, Singapore’s Ministry of Transport is examining the suggestion to decrease the maximum speed to 6 Kmh from 10 Kmh for motorized PMAs. Also, it is preparing to notify that these can only be utilized by individuals with medical or walking issues. In addition, the market is propelled by the increased popularity of wheelchairs with enhanced features due to the expanding number of patients.

By End User Insights

The homecare segment is expected to capture the maximum share under this category of the personal mobility devices market because of the rising prevalence of arthritis and chronic impairments among the elderly. This age group is less mobile and necessitates mobility aids at home. Also, it provides a better customer experience, comfort, and usability, which makes it a favorable option for homecare facilities. Hence, these people are likely to utilize PMDs more frequently and propel the end-user segment's growth over time. Whereas the demand for personal mobility devices has increased in hospitals after COVID-19. It has come to light that people diagnosed with coronavirus suffer more heart and lung-related problems which is surging the market share of this segment.

REGIONAL ANALYSIS

Europe dominated the personal mobility devices market due to the increased frequency of age-related disorders, expanding senior population, improved healthcare infrastructure, high healthcare spending, and favourable reimbursement policies for purchase or rental services, the regional market will grow stable throughout the forecast years. The European countries have made significant investments in developing clean and environmentally friendly technologies. The usage of carbon-free mobility equipment has been made possible due to smart city projects. Electric scooters are popular among the region's youth, and this trend helps the market flourish. Footpaths are designed so personal mobility devices can easily be walked across them.

North America is likely to dominate the personal mobility devices market after Europe, and this dominance is expected to continue over the forecast period. This is due in significant part to the region's enormous patient population. Because of the growing senior population, which is more susceptible to mobility problems, including osteoporosis and rheumatoid arthritis, the demand for mobility aids has increased in North America. The United States and Canada make up most of the region's population. The combination of supportive government measures that minimize the burden of the devices' high cost, as well as expanding reimbursement regulations, has resulted in a significant level of personal mobility device adoption.

Asia Pacific is projected to register significant growth in the personal mobility devices market. Furthermore, the regional market is likely to be driven by considerable R&D operations carried out by various organizations, such as the China Rehabilitation Research Center (CRRC). Increasing disposable income levels, increased awareness, high healthcare expenditure, and government programs targeted at expanding healthcare access will help the Asia Pacific market grow.

The Latin America personal mobility market is predicted to propel further during the forecast period. The region is one of the major users of PMDs. In addition, the expansion can be linked to higher healthcare expenditure and improved economic recovery. The medical infrastructure varied from country to country in LA. There is a considerable gap between rural and urban healthcare facilities. Also, due to its culture family relationships and bonding matter the most to the people. Moreover, Brazil is the leading market in the region because of its rapid urbanization, public awareness campaigns and education programs.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global personal mobility devices market include

- Drive DeVilbiss Healthcare

- GF Health Products, Inc.

- Invacare Corporation

- Carex Health Brands, Inc.

- Kaye Products, Inc.

- Briggs Healthcare

- Medline Industries, Inc.

- NOVA Medical Products

- Performance Health

- Rollz International

Drive DeVilbiss Healthcare, GF Health Products, Inc., Invacare Corporation, Carex Health Brands, Inc., Kaye Products, Inc., Briggs Healthcare, Medline Industries, Inc., NOVA Medical Products, Performance Health, and Rollz International are some of the noteworthy companies operating in the global personal mobility devices market profiled in this report.

GLOBAL PERSONAL MOBILITY DEVICES MARKET NEWS

- In August 2023, Drive Devilbiss introduced the AstroLite. It is the lightest sliptable mobility scooter. This was part of its 2023 target to break the record of the lightest product under this category.

- In February 2023, Rollz Motion Electric was unveiled by the Rollz International. It is a revolutionary rollator electric wheelchair developed for zero effort mobility.

- Amid a global surge in bicycle demand, Gates announced to launch of new personal mobility products in 2020.

- In 2020, 1800Wheelchair announced the introduction of a new wheelchair brand called "Feather Chair," which includes the lightest mobility products for seniors, such as lightweight wheelchairs.

MARKET SEGMENTATION

This research report on the global personal mobility devices market has been segmented and sub-segmented based on product, end-user, and region.

By Product

- Walking Aids

- Rollators

- Premium

- Low-cost

- Others (Canes, Crutches, and Walkers)

- Rollators

- Wheelchairs

- Manual

- Powered

- Scooters

By End-User

- Hospitals

- Homecare

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

What is the global personal mobility devices market?

The global personal mobility devices market supplies wheelchairs scooters walkers enhancing independence for elderly mobility impaired users worldwide.

Why grow the global personal mobility devices market?

The global personal mobility devices market expands with aging populations chronic conditions independent living preferences strategically worldwide.

What drives the global personal mobility devices market?

Geriatric healthcare demands home care trends propel the global personal mobility devices market alongside accessibility regulations significantly.

Which products lead the global personal mobility devices market?

Wheelchairs dominate the global personal mobility devices market serving diverse mobility levels across institutional home environments comprehensively.

What role does home care play in the global personal mobility devices market?

Households consume growing volumes from the global personal mobility devices market enabling aging-in-place independent living solutions consistently.

How do scooters function in the global personal mobility devices market?

Powered scooters provide outdoor mobility covering longer distances safely in the global personal mobility devices market active users effectively.

Which end users define the global personal mobility devices market?

Hospitals clinics households lead adoption driving the global personal mobility devices market diverse care continuum requirements strategically.

What challenges face the global personal mobility devices market?

Device weight battery life challenge the global personal mobility devices market portability usability improvements technically continuously.

How do powered devices differ in the global personal mobility devices market?

Electric wheelchairs scooters offer effortless propulsion surpassing manual options in the global personal mobility devices market fatigue reduction significantly.

What innovations shape the global personal mobility devices market?

Smart connectivity lightweight composites trend enhancing the global personal mobility devices market user experience portability seamlessly.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com