Global Plywood Market Size, Share, Trends & Growth Forecast Report By Type (Softwood Plywood, Hardwood Plywood), By Application (Construction, Industrial), By Use Type (New Construction, Rehabilitation), and By Region (Asia Pacific, North America, Europe, Latin America, Middle East & Africa) – Industry Analysis and Forecast in Terms of Value (USD), 2026 to 2034

Global Plywood Market Summary

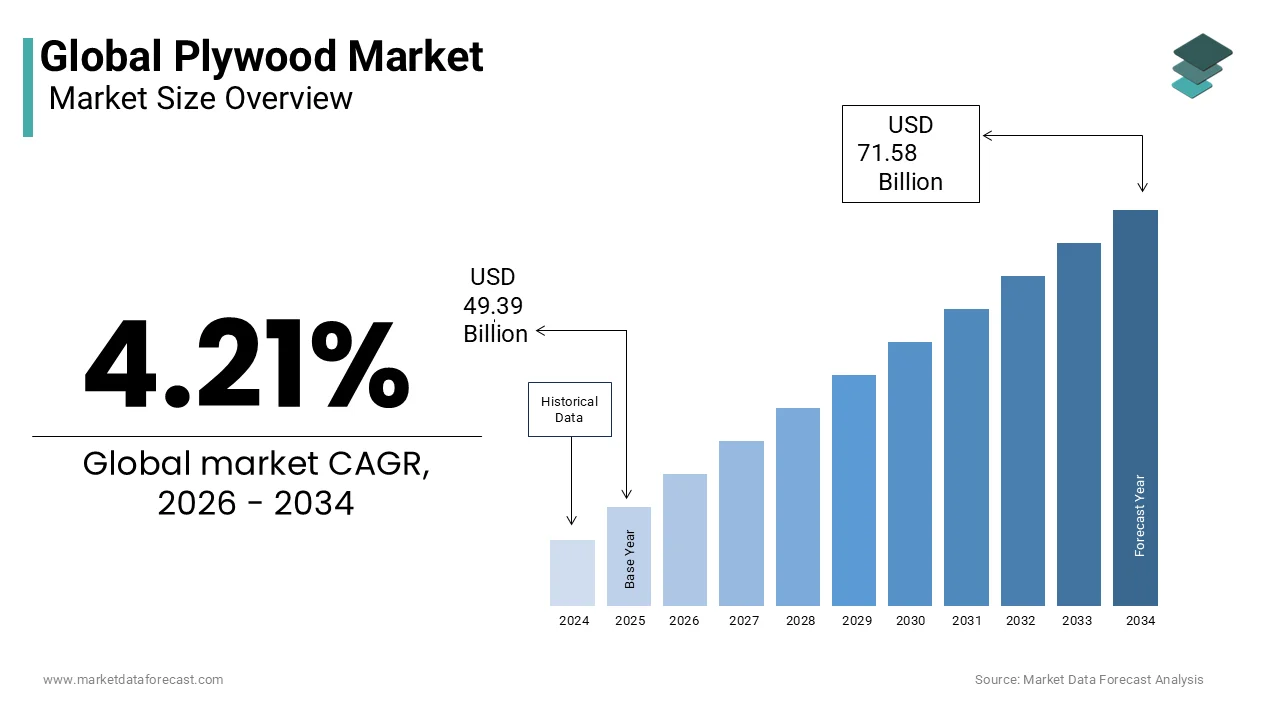

The global plywood market was valued at USD 49.39 billion in 2025 and is projected to grow from USD 51.46 billion in 2026 to USD 71.58 billion by 2034, registering a CAGR of 4.21% from 2026 to 2034.

Key Market Highlights

- 2025 Market Size: USD 49.39 Billion

- 2026 Estimate: USD 51.46 Billion

- 2034 Forecast: USD 71.58 Billion

- CAGR (2026–2034): 4.21%

- Largest Type Segment: Softwood Plywood (58.2% share in 2025)

- Fastest-Growing Type: Hardwood Plywood (8.6% CAGR)

- Largest Application: Construction

- Largest Region: Asia Pacific (46.6% share in 2025)

Quick Growth Drivers

- Accelerated urbanization in emerging economies

- Massive infrastructure investment pipelines (housing, transport, smart cities)

- Expansion of modular & prefabricated construction

- Rising demand for lightweight structural materials

- Growth in rehabilitation and retrofitting programs

Principal Restraints

- Deforestation restrictions and timber harvesting regulations

- Compliance burdens under EU Deforestation Regulation (EUDR)

- Volatility in petrochemical-based adhesive prices

- Health concerns related to formaldehyde emissions

High-Value Opportunities

- Bio-based & formaldehyde-free adhesive innovation

- Digital manufacturing & CNC-based precision fabrication

- Smart plywood with embedded sensors for structural monitoring

- Growth in premium interior & decorative applications

- Green building certifications boosting certified plywood demand

Key Market Challenges

- Proliferation of substandard & uncertified plywood in price-sensitive markets

- Low automation levels in SMEs across Southeast Asia & Africa

- Raw material traceability requirements

- Increasing sustainability compliance costs

What Wins Commercially (Competitive Edge)

- FSC/PEFC certified sourcing

- Low-formaldehyde & bio-adhesive innovations

- Automated high-yield production

- Digital contractor sales channels

- Premium decorative & specialty plywood lines

Top Strategic Ask for Executives

- Accelerate transition to bio-based adhesives

- Invest in automation to improve yield & quality

- Strengthen supply traceability systems

- Target rehabilitation & green retrofit programs

- Expand premium hardwood product lines

Leading Players

Some of the companies that are playing a dominating role in the global plywood market include:

- Georgia-Pacific

- Boise Cascade Company

- Weyerhaeuser Company

- UPM

- SVEZA Group

- Austral Plywoods

- PotlatchDeltic Corporation

- Greenply Industries Limited

- Metsä Group

- CenturyPly

Global Plywood Market Size

The global plywood market was valued at USD 49.39 billion in 2025 and is projected to grow from USD 51.46 billion in 2026 to USD 71.58 billion by 2034, at a CAGR of 4.21%. from 2026 to 2034

Plywood is an engineered wood product composed of thin layers or plies of wood veneer bonded together with adhesives, typically arranged with alternating grain directions to enhance strength, dimensional stability, and resistance to warping. Its layered construction provides superior structural integrity compared to solid wood, which makes it a preferred material in construction, furniture, and industrial applications. As per the study, millions of cubic meters of tropical and temperate hardwoods are processed annually for veneer and plywood production, with Indonesia, China, and Russia serving as primary sourcing regions. According to research, plywood accounts for a portion of all structural panel use in residential construction in North America, where its strength is important in resisting lateral forces from wind and seismic events.

MARKET DRIVERS

Accelerated Urbanization and Infrastructure Development in Emerging Economies

The surge in urban population and large-scale infrastructure projects is propelling the growth of the plywood market. According to the United Nations Department of Economic and Social Affairs, over 1.4 billion people are expected to be added to urban centers by 2050, with 90% of this growth occurring in developing nations. In India, the National Infrastructure Pipeline forecasts USD 1.4 trillion in infrastructure investment by 2025, covering housing, transportation, and smart cities, all major consumers of plywood for formwork, shuttering, and interior finishes. As per the study, plywood usage in concrete formwork increased due to rapid public building construction. Similarly, plywood is the most accessible and cost-effective material for low-cost housing projects, where timber scarcity limits solid wood use. These macro-level urban expansion efforts necessitate vast quantities of durable and easily workable materials, which positions plywood as a foundational component in emerging construction ecosystems.

Expansion of the Modular and Prefabricated Construction Sector

The global shift toward off-site and modular building techniques is expected to drive the growth of the plywood market. This is due to its compatibility with precision manufacturing and lightweight structural systems. As per the research, the prefabricated construction business grew annually, with the Asia Pacific leading adoption. Plywood, particularly oriented strand board (OSB) and laminated veneer lumber (LVL), is integral to wall panels, flooring, and roof cassettes in modular units. In Sweden, a portion of single-family homes incorporates engineered wood panels, with plywood-based systems reducing on-site construction time. The integration of digital design tools like BIM further enhances plywood’s role in prefabrication by enabling exact cutting and assembly. Therefore, this process minimizes waste and labor costs in mass housing and commercial developments.

MARKET RESTRAINTS

Depletion of Natural Forest Resources and Regulatory Restrictions on Timber Harvesting

Deforestation and environmental regulations are threatening the sustainability of plywood production, which is restricting the growth of the plywood market. As reported by the World Resources Institute, global tree cover loss reached 28.3 million hectares in 2023, primarily due to a dramatic increase in fire-driven loss in boreal forests (notably Canada). Indonesia has revoked large hectares of logging licenses since 2019 to curb illegal deforestation, reducing raw material supply for its plywood market, which once accounted for a portion of global tropical plywood exports. The European Union’s Deforestation Regulation (EUDR), effective in 2023, requires traceability for wood imports, imposing compliance burdens on exporters. These constraints limit the availability of sustainably certified veneer, increase procurement costs, and compel manufacturers to seek alternative feedstocks or face production delays.

Volatility in Adhesive Costs and Dependence on Petrochemical-Based Resins

Heavy reliance on synthetic adhesives such as urea-formaldehyde (UF), phenol-formaldehyde (PF), and melamine-urea-formaldehyde (MUF), which are derived from petrochemical feedstocks, is restricting the growth of the plywood market. As per the research, global benzene and formaldehyde prices fluctuated due to supply chain disruptions and energy market volatility, directly impacting resin production costs. In India, it recorded an increase in adhesive expenses, forcing small and medium producers to raise prices or reduce margins. Apart from these, formaldehyde emissions from conventional resins have raised health concerns.

MARKET OPPORTUNITIES

Advancement in Bio-Based and Formaldehyde-Free Adhesives

The development of sustainable bonding agents that align with environmental and health standards is ascribed to bolstering the growth of the plywood market. Researchers at the Fraunhofer Institute for Wood Research have engineered tannin-based and lignin-derived adhesives that achieve bond strength comparable to phenol-formaldehyde resins without carcinogenic emissions. As per a study, bio-adhesive usage in wood composites grew annually. Apart from these, soy protein and casein-based glues are being commercialized in China and Brazil, which reduces reliance on fossil fuels.

Integration of Digital Manufacturing and Smart Plywood Systems

The integration of digital fabrication and smart materials for high-tech construction and design provides an opportunity for the plywood market. Computer numerical control (CNC) machining and robotic assembly now enable intricate, waste-minimized plywood structures for architectural and interior applications. The Massachusetts Institute of Technology’s Mediated Matter Group has developed programmable plywood that changes shape in response to humidity, using differential layering and laser patterning. In Japan, Daiwa House Industry employs AI-driven cutting systems to produce custom plywood components for prefabricated homes with material utilization efficiency. Apart from these, embedded sensors in plywood panels are being tested for structural health monitoring in bridges and high-rises.

MARKET CHALLENGES

Proliferation of Substandard and Legally Sourced Plywood in Price-Sensitive Markets

The rising counterfeit and non-compliant products in South Asia, the Middle East, and Africa are challenging the growth of the Hollywood market. These inferior products, often priced lower than certified alternatives, affect consumer trust and distort competition. Legitimate manufacturers incur higher compliance costs for FSC or PEFC certification, making it difficult to compete on price. Such practices erode sustainability efforts and compromise building safety, particularly in seismic zones where structural integrity is paramount. Combating this shadow market requires coordinated enforcement, consumer education, and digital verification systems, which remain underdeveloped in many regions.

Limited Adoption of Automation in Small-Scale and Regional Plywood Mills

Limited adoption of advanced manufacturing technologies by small and medium enterprises (SMEs) is also challenging the growth of the plywood market. According to the study, a portion of plywood mills in Southeast Asia and Sub-Saharan Africa operate manually or with outdated machinery, resulting in yield losses during veneer peeling and pressing. Labor productivity in these facilities is less than half that of automated plants in Europe or South Korea. Furthermore, inconsistent thickness and glue spread compromise structural performance, which restricts market access to premium construction and export sectors. Government initiatives in Vietnam and India aim to modernize the sector through subsidies and technology parks. However, capital constraints and skills shortages are impeding widespread automation and creating a fragmented, low-efficiency production landscape.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Application, Use Type, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | North America, Europe, Asia Pacific, Latin America, the Middle East, and Africa |

| Market Leaders Profiled | Georgia-Pacific (US), Boise Cascade Company (US), Weyerhaeuser Company (US), UPM (Finland), SVEZA Group (Russia), Austral Plywoods (Australia), PotlatchDeltic Corporation (US), Greenply Industries Limited (India), Metsa Group (Finland), CenturyPly (India).

|

SEGMENTAL ANALYSIS

By Type Insights

The softwood plywood segment dominated the plywood market by capturing 58.2% of the global market share in 2025. The growth of the softwood plywood segment is driven by the widespread availability of coniferous timber, primarily spruce, pine, and fir, from sustainably managed boreal and temperate forests in North America and Northern Europe. Canada alone harvested millions of cubic meters of softwood, providing a steady feedstock for plywood production. The material’s high strength-to-weight ratio and dimensional stability make it ideal for structural applications, particularly in residential construction. The U.S. confirms that many single-family homes in the United States utilize softwood plywood for roof sheathing, wall bracing, and subflooring due to its compliance with International Building Code standards. Apart from these, its compatibility with prefabricated wood-frame systems has strengthened its role in modern, rapid-build methodologies.

The hardwood plywood segment is predicted to witness a CAGR of 8.6% from 2025 to 2033 due to rising demand in high-value applications such as interior design, furniture, and specialty industrial uses. Hardwood species like birch, beech, and eucalyptus offer superior surface finish, durability, and aesthetic appeal, which makes them preferred for visible components in cabinetry and architectural millwork. Apart from these, tropical hardwoods such as okoume and meranti are extensively used in the marine and transportation sectors for their moisture resistance. The rise of luxury residential developments in China and India, where polished wood interiors are culturally favored, is further boosting demand.

By Application Insights

The construction segment led the plywood market by capturing a significant share in 2025. The growth of the construction segment is driven by plywood’s indispensable role in formwork, flooring, roofing, and wall sheathing across residential, commercial, and infrastructure projects. In high-rise construction, plywood is used as shuttering for concrete pouring, with one square meter of formwork reused when coated with film-faced treatments, according to the study. In the United States, as per the research, an average single-family home uses many square feet of structural plywood. The material’s ability to withstand harsh on-site conditions, combined with ease of cutting and fastening, makes it irreplaceable in both conventional and modular building practices. This ensures its entrenched position as a foundational construction material.

The industrial application segment is predicted to witness the highest CAGR of 9.1% during the forecast period, owing to the expanding use in specialized sectors such as transportation, packaging, and machinery. Plywood is increasingly used in truck and container flooring due to its load-bearing capacity and resistance to moisture and abrasion. As per the study, a portion of dry freight trailers in North America use plywood flooring, with annual replacement demand exceeding millions of square meters. In packaging, custom plywood crates protect high-value equipment in aerospace and medical device shipping, where dimensional stability is important. Hence, demand for durable and lightweight industrial plywood solutions is accelerating, particularly in emerging manufacturing hubs across Southeast Asia and Eastern Europe.

By Use Type Insights

The new construction segment dominated the plywood market by capturing a significant share in 2025. The growth of the new construction segment is driven by the scale of urban expansion, population growth, and government-backed housing initiatives in both developed and emerging economies. Like, vast quantities of new residential space have been completed in China, and plywood is used in various applications within the country's construction industry. Even in mature markets like the United States. The integration of plywood into prefabricated and panelized building systems further amplifies its use in new builds, where speed, precision, and code compliance are paramount.

The rehabilitation segment is predicted to witness the highest CAGR of 7.9% from 2025 to 2033. The growth of the rehabilitation segment is driven by aging building stock, rising retrofitting mandates, and increasing investment in energy efficiency and seismic upgrades. According to research, a portion of the EU’s building stock was constructed before 2000, with a number classified as energy inefficient, necessitating extensive renovations. Plywood is widely used in re-sheathing walls, replacing subfloors, and strengthening structural diaphragms during retrofits. Apart from these, heritage restoration projects in cities like Paris and Kyoto employ specialty plywood for non-invasive repairs. Thus, rehabilitation is emerging as a sustained growth vector for plywood in mature urban markets due to green renovation incentives under the EU’s Renovation Wave and the U.S. Inflation Reduction Act.

REGIONAL ANALYSIS

Asia Pacific Plywood Market Insights

Asia Pacific was the top performer in the plywood market by capturing 46.6% of the share in 2025, with its functioning as both the largest producer and a high-growth consumption hub. China is the dominant force, producing millions of cubic meters of plywood annually, as per the research, with a few provinces serving as primary manufacturing centers. Indonesia, despite export restrictions on raw logs, remains a major supplier of tropical hardwood plywood, particularly for Japan and the Middle East. India’s domestic demand is surging due to urbanization and affordable housing programs like Pradhan Mantri Awas Yojana, which aims to construct homes, as per the study. The region’s competitive advantage lies in low-cost labor, established supply chains, and proximity to construction markets.

North America Plywood Market Insights

North America was positioned second by occupying 22.5% of the plywood market share in 2025, with high per-capita consumption and advanced manufacturing standards. The United States is a notable consumer, with the U.S. Forest Service estimating annual plywood consumption at significant square feet, primarily for residential construction. Softwood plywood from Pacific Northwest forests supplies a portion of the domestic market, as per the study. Canada contributes significantly through its sustainably managed boreal forests, with Quebec and British Columbia housing major production facilities. The region’s prowess in prefabricated housing and modular construction has increased demand for performance-rated plywood meeting APA – The Engineered Wood Association standards. Apart from these, hurricane-prone regions require plywood sheathing for wind resistance, as per research.

Europe Plywood Market Insights

Europe's plywood market growth is likely to grow with the highest CAGR in the coming years due to stringent environmental regulations and a focus on sustainable, high-performance materials. Russia is a key producer. The European Union’s revised Construction Products Regulation [(EU) 2025/3110] requires CE marking for structural panels covered by a harmonized standard. Manufacturers must issue a Declaration of Performance (DoP) and provide product traceability. New, mandatory lifecycle assessments (LCA) and environmental data reporting, favoring manufacturers with low-emission production, will be phased in over the coming years. Germany is a notable consumer, utilizing plywood in energy-efficient retrofitting and prefabricated timber housing, where the German Sustainable Building Council requires renewable materials. As per the study, formaldehyde-free and bio-adhesive plywood now represents a portion of sales in Western Europe. Apart from these, cross-laminated timber (CLT) production, which often incorporates plywood elements, has grown annually since 2020, according to research.

Latin America Plywood Market Insights

Latin America grew steadily in the global plywood markett with Brazil and Chile serving as the primary production and consumption centers. Brazil’s plywood market, concentrated in Paraná and Santa Catarina, produces notable cubic meters annually. Eucalyptus and pine plantations, managed under FSC certification, supply most of the raw material. The country’s growing middle class and urbanization are driving demand for housing and furniture. Chile exports high-quality radiata pine plywood to North America and Asia, leveraging its robust forestry sector. However, limited domestic processing capacity forces reliance on imports for specialty grades.

Middle East & Africa Plywood Market Insights

The Middle East and Africa are likely to grow in the global plywood market, with demand concentrated in construction and infrastructure development. The United Arab Emirates regularly ranks as one of the largest importers of plywood in the Middle East. In 2025, the UAE was the second-largest importer of plywood in the region by volume, as per the study. Major projects are driving demand for formwork and architectural plywood. South Africa produces limited quantities domestically. However, inconsistent quality and lack of regulation in informal markets hinder standardization.

KEY MARKET PLAYERS

A few of the notable players in the global plywood market profiled in the report include Georgia-Pacific (US), Boise Cascade Company (US), Weyerhaeuser Company (US), UPM (Finland), SVEZA Group (Russia), Austral Plywoods (Australia), PotlatchDeltic Corporation (US), Greenply Industries Limited (India), Metsa Group (Finland), CenturyPly (India).

TOP LEADING PLAYERS IN THE MARKET

Georgia-Pacific (US)

Georgia-Pacific (US) has a robust presence in the global plywood industry with a strong product portfolio catering to construction, furniture, and packaging sectors. The company focuses on producing sustainable wood-based solutions, with key offerings such as structural plywood panels and specialty wood products. In recent years, Georgia-Pacific has expanded its digital distribution channels and introduced eco-friendly product lines meeting green building certifications. The company also invests in modernizing mills with automation and energy-efficient technologies, reinforcing its leadership in North America and beyond.

Boise Cascade Company (US)

Boise Cascade Company (US) is a leading manufacturer and distributor of plywood and engineered wood products across North America. The company leverages a vertically integrated business model, combining manufacturing with a strong wholesale distribution network. Boise Cascade emphasizes product customization for builders and contractors, offering fire-rated, moisture-resistant, and industrial-grade plywood varieties. With consistent investment in expanding distribution facilities and improving logistics, the company ensures faster delivery times, strengthening customer loyalty and expanding its market footprint.

Weyerhaeuser Company (US)

Weyerhaeuser Company (US) plays a transformative role in the plywood market through sustainable forest management and advanced wood product innovations. Its plywood offerings are widely used in residential and commercial construction across the United States and Canada. The company is known for integrating digital forest management systems that ensure efficient raw material supply and long-term environmental stewardship. Weyerhaeuser also collaborates with construction technology firms to enhance the performance of engineered wood products, aligning with the growing demand for durable and lightweight building materials.

UPM (Finland)

UPM (Finland) has established a strong position in the European plywood market with a focus on premium-quality birch plywood products. The company’s portfolio serves industries such as construction, transport, furniture, and marine applications. UPM prioritizes sustainability, with products certified under FSC and PEFC standards, and invests in bio-based adhesives to reduce formaldehyde emissions. In recent years, UPM has expanded its production capacity in Finland and Estonia, enhancing supply reliability across Europe and Asia. Its brand reputation for quality and sustainability continues to drive growth in high-value markets.

Greenply Industries Limited (India)

Greenply Industries Limited (India) is one of Asia’s leading plywood manufacturers, offering a wide range of decorative and structural plywood products. The company has established a significant presence in India and international markets through innovative designs, termite-resistant plywood, and eco-friendly manufacturing practices. Greenply has invested in automation and digital supply chain systems to streamline distribution. The company is also driving growth through its “Green” brand positioning, focusing on zero-emission products and aligning with India’s green building movement.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the plywood market employ a mix of sustainability-driven innovation, capacity expansion, and digital transformation to strengthen their positions. Companies are investing in eco-friendly adhesives, low-emission plywood, and FSC-certified sourcing to meet regulatory and consumer demands. Strategic mergers, acquisitions, and partnerships enable geographic expansion and portfolio diversification. Manufacturers also focus on automation in mills, improved logistics, and customized product offerings to serve the construction, furniture, and marine industries. Additionally, players are developing digitized sales channels and direct-to-contractor platforms to increase market accessibility.

RECENT MARKET DEVELOPMENTS

- In January 2022, UPM expanded its plywood mill in Estonia, boosting production capacity for birch plywood to meet growing demand in Europe and Asia.

- In June 2022, Greenply Industries announced its investment in a zero-emission manufacturing facility in Gujarat, India, emphasizing eco-friendly plywood production.

- In September 2022, Boise Cascade Company opened a new distribution center in Texas, enhancing supply chain efficiency and faster delivery to contractors and builders.

- In March 2023, Weyerhaeuser partnered with a leading construction technology firm to test next-generation engineered plywood products designed for high-strength and lightweight applications.

- In November 2023, Georgia-Pacific launched an eco-certified plywood product line targeting the green building sector, strengthening its sustainability-driven brand positioning.

MARKET SEGMENTATION

This research report on the global plywood market is segmented and sub-segmented into the following categories.

By Type

-

Softwood Plywood

-

Hardwood Plywood

By Application

-

Construction

-

Industrial

By Use Type

-

New Construction

-

Rehabilitation

By Region

-

Asia Pacific

-

North America

-

Europe

-

Latin America

-

Middle East & Africa

Frequently Asked Questions

1. What factors are driving growth in the Global Plywood Market?

Rapid urbanization, increased construction activity, and government investments propel the Global Plywood Market. Modular construction, furniture design, and eco-friendly practices boost demand

2. Which regions are leading in the Global Plywood Market?

Asia-Pacific holds the largest share of the Global Plywood Market, driven by fast-growing construction and furniture industries in China, India, and Southeast Asia. Europe and North America follow with stable demand.

3. What are the major applications of plywood in the Global Plywood Market?

The Global Plywood Market covers applications in building structures, flooring, wall panels, roofing, and in manufacturing furniture such as cabinets, store fixtures, and doors.

4. Who are the leading manufacturers in the Global Plywood Market?

Top companies in the Global Plywood Market include Georgia-Pacific, Boise Cascade, Weyerhaeuser, UPM, SVEZA, Austral Plywoods, Greenply, and CenturyPly, among others.

5. What types of plywood are most popular in the Global Plywood Market?

Softwood plywood is the largest segment in the Global Plywood Market due to affordability and wide use in construction. Hardwood plywood is valued for strength in premium furniture

6. How is sustainability shaping the Global Plywood Market?

Eco-friendly sourcing, certified sustainable forest practices, and a focus on recycled materials are increasingly integral to the Global Plywood Market, reflecting consumer and government demand.

7. What is the expected growth rate of the Global Plywood Market?

The Global Plywood Market is projected to expand at a CAGR between 4% and 6% from 2025 to 2034, indicating steady and significant sector development worldwide.

8. What challenges does the Global Plywood Market face today?

The Global Plywood Market is dealing with issues of raw material supply, deforestation, competition from alternative materials, and regulatory pressures on environment and safety.

9. How does technology influence the Global Plywood Market?

AI, robotics, and advanced manufacturing techniques are elevating product quality, defect detection, and cost-efficiency in the Global Plywood Market, making innovative plywood panels accessible.

10. What are the main end-users of products in the Global Plywood Market?

The primary end-users in the Global Plywood Market are the construction sector, furniture manufacturers, packaging companies, and interior design firms worldwide.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com