Global Polyhydroxyalkanoate (PHA) Market Size, Share, Trends & Growth Forecast Report – Segmented By Type (Monomers, Co-Polymers and Terpolymers), Manufacturing Technology, Application, and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa) – Industry Analysis (2026 to 2034)

Market Size, 2025

$81.78 MnMarket Estimate, 2026

$91.43 MnMarket Forecast, 2034

$223.1 MnCAGR, 2026–2034

11.8%Global Polyhydroxyalkanoate (PHA) Market Report Summary

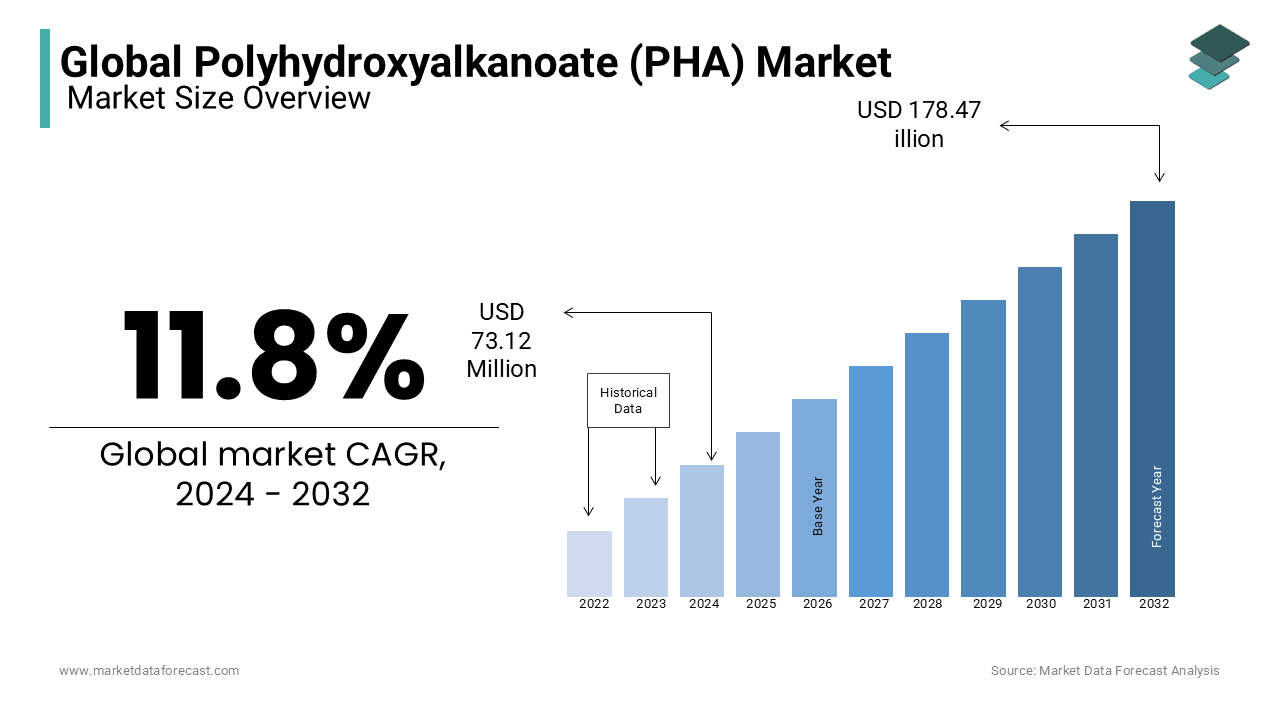

The global polyhydroxyalkanoate PHA market was valued at USD 81.78 million in 2025, is estimated to reach USD 91.43 million in 2026, and is projected to reach USD 223.16 million by 2034, growing at a CAGR of 11.80% during the forecast period. Market growth is driven by increasing demand for biodegradable plastics, rising environmental concerns, and strict regulations on single use plastics. PHA is a bio based and biodegradable polymer widely used as a sustainable alternative to conventional plastics. The growing focus on circular economy practices and eco friendly materials is further supporting strong market expansion globally.

Key Market Trends

- Rising demand for biodegradable and eco friendly plastics is driving market growth.

- Increasing regulatory restrictions on single use plastics is boosting adoption.

- Growing focus on sustainability and circular economy is supporting market expansion.

- Expansion of bio based materials in packaging and industrial applications is enhancing demand.

- Technological advancements in biopolymer production are improving efficiency and scalability.

Segmental Insights

- Based on type, the short chain length PHA segment was the largest and held 71.7% of the global PHA market share in 2025. This dominance is attributed to its favorable mechanical properties and wide applicability in packaging and consumer goods.

- Based on application, the packaging segment accounted for 61.6% of the global PHA market share in 2025. The segment’s growth is driven by increasing demand for sustainable packaging solutions.

Regional Insights

- The global PHA market is experiencing rapid growth across regions, supported by sustainability initiatives and regulatory support.

- Europe was the largest contributor in 2025, driven by strong environmental regulations, high consumer awareness, and increasing adoption of biodegradable materials.

Competitive Landscape

The global PHA market is moderately competitive, with key players focusing on technological innovation, production capacity expansion, and strategic partnerships to strengthen their market position. Companies are investing in advanced biopolymer technologies, sustainable production methods, and commercial scale manufacturing. Prominent players in the global PHA market include Meredian Inc, Tianan Biologic Materials Co Ltd, Polyferm Canada Inc, Shenzhen Ecomann Biotechnology Co Ltd, LIC PHB Industrial S A, Newlight Technologies, BioMatera Inc, Metabolix Inc, Biomer, Biomatera, and Kaneka Corporation.

Global Polyhydroxyalkanoate (PHA) Market Size

The global polyhydroxyalkanoate (PHA) market size was valued at USD 81.78 million in 2025, and the global market size is expected to reach USD 223.16 million by 2034 from USD 91.43 million in 2026. The market is growing at a CAGR of 11.80% during the forecast period.

Polyhydroxyalkanoate (PHA) represents a transformative segment within the global bioplastics industry, characterized by fully biodegradable polyesters produced through bacterial fermentation of renewable feedstocks. Unlike conventional plastics derived from fossil fuels, PHA offers a circular solution that decomposes naturally in various environments, including soil and marine settings. This unique property positions it as a critical material in the fight against plastic pollution. According to the United Nations Environment Programme, global plastics production reached over 431 million tons per year as of 2025, with only a fraction being recycled, leading to severe environmental degradation. The urgency to address this crisis has accelerated the adoption of bio-based alternatives. As per the Joint Research Centre of the European Commission, the global production capacity of bio-based and biodegradable plastics is approximately 2.3 million tonnes in 2025 and is projected to reach 4.7 million tonnes by 2030, with PHA identified as one of the fastest-growing categories due to its superior biodegradability profile. The technology leverages microbial processes to convert sugars, lipids, and agricultural waste into high-performance polymers. These materials exhibit diverse physical properties ranging from rigid to elastic, making them suitable for packaging, agriculture, and medical applications. Regulatory frameworks such as the European Union Single-Use Plastics Directive further catalyze market expansion by restricting conventional plastic items. The integration of PHA into mainstream manufacturing requires overcoming cost barriers, but its environmental credentials provide a compelling value proposition for sustainability-focused industries. This market is poised for substantial growth as technological advancements improve production efficiency and scalability.

MARKET DRIVERS

Stringent Global Regulations Banning Single-Use Plastics Drive Demand for Biodegradable Alternatives

The implementation of stringent global regulations banning single-use plastics is driving the growth of the global polyhydroxyalkanoate (PHA) market as governments seek effective solutions to mitigate plastic waste. Legislative measures across major economies are increasingly prohibiting non-biodegradable plastic products such as bags, straws, and cutlery, thereby creating a vacuum that PHA is well-positioned to fill. According to the European Commission, the Single-Use Plastics Directive aims to reduce the consumption of certain single-use plastic takeaway containers and specific items like plates and straws by 50% by 2025 compared to 2019 levels. This regulatory pressure forces manufacturers to transition towards compliant materials that offer similar functionality without the environmental burden. As per the New York State Department of Environmental Conservation, expanded polystyrene containers used for cold storage are banned effective January 1, 2026, prompting businesses to adopt certified compostable alternatives like PHA. The legal mandate ensures a baseline demand for biodegradable polymers regardless of price differentials. Furthermore, international agreements such as the Global Plastics Treaty are pushing for standardized reductions in plastic pollution, which encourages multinational corporations to preemptively switch to sustainable materials. PHA stands out because it meets the rigorous criteria for home and industrial compostability, unlike some other bioplastics that require specific conditions. This regulatory tailwind provides a stable and growing market for PHA producers who can demonstrate compliance and environmental benefit. The shift is not merely voluntary but legally enforced, ensuring sustained adoption rates.

Growing Consumer Awareness and Preference for Sustainable Packaging Solutions Fuel Market Expansion

Rising consumer awareness regarding environmental issues and a strong preference for sustainable packaging solutions significantly propel the growth of the Polyhydroxyalkanoate (PHA) Market. Modern consumers are increasingly educated about the detrimental effects of plastic pollution on ecosystems and human health, leading to a shift in purchasing behavior towards eco-friendly products. According to a NielsenIQ report, the global outlook for 2026 indicates that continued volatility has deeply ingrained a lingering caution into consumer psychology, though consumers report feeling slight relief from pressures as the number concerned about the impact of geopolitical conflict rose from 12% to 14%. This sentiment is particularly strong among millennials and Generation Z who prioritize transparency and ethical sourcing. As per the Ellen MacArthur Foundation, nearly everyone, everywhere, every day comes into contact with plastics, and decoupling plastics from fossil feedstocks would allow the industry to participate in a low-carbon world. Brands responding to this demand are incorporating PHA into their packaging strategies to enhance their sustainability credentials and appeal to conscious buyers. The ability of PHA to degrade in natural environments resonates with consumers who worry about microplastic accumulation. Retailers are also leveraging this trend by highlighting biodegradable packaging as a key selling point. Social media campaigns and educational initiatives further amplify the message, driving grassroots demand. This consumer-led push complements regulatory efforts, creating a dual force that accelerates the adoption of PHA in retail, food service, and consumer goods sectors.

MARKET RESTRAINTS

High Production Costs Compared to Conventional Plastics Restrict Widespread Commercial Adoption

High production costs associated with Polyhydroxyalkanoate (PHA) synthesis is impeding the growth of the global polyhydroxyalkanoate (PHA) market. The fermentation process required to produce PHA is energy-intensive and requires expensive substrates such as pure sugars or vegetable oils which constitute a large portion of operational expenses. According to the Joint Research Centre of the European Commission, producing bio-based plastics is generally 1.5 to 2 times more onerous than fossil-fuels-based plastics, which often face significant production costs compared to virgin fossil-based alternatives. This substantial price disparity makes it difficult for PHA to compete in price-sensitive markets without subsidies or regulatory mandates. As per the Biodegradable Products Institute, many manufacturers hesitate to switch to PHA due to the impact on profit margins, especially for low-margin disposable items. The complexity of downstream processing, including extraction and purification, further adds to the cost burden. Additionally, the scale of production for PHA is currently much smaller than that of fossil-based plastics, preventing economies of scale from lowering prices. Until technological breakthroughs reduce fermentation times and improve yield using cheaper feedstocks, PHA will remain a niche premium product. This economic barrier limits its application to high-value segments where sustainability commands a price premium. Without cost parity, the mass-market transition to PHA remains challenging despite its environmental benefits.

Limited Availability of Scalable and Cost Effective Raw Material Feedstocks Impacts Supply Stability

The limited availability of scalable and cost-effective raw material feedstocks is another major restraint to the growth of the polyhydroxyalkanoate (PHA) market by impacting supply stability and production consistency. Currently, most PHA production relies on first-generation feedstocks such as corn starch, sugarcane, and vegetable oils, which compete with food supplies and are subject to volatile agricultural prices. According to the OECD-FAO Agricultural Outlook 2025-2034, real international reference prices for agricultural commodities are expected to maintain a slightly declining trend, while global agricultural and fish production is expected to increase by 14% over the next decade. This volatility creates uncertainty for PHA manufacturers who struggle to maintain consistent pricing and supply contracts. As per the American Chemical Society, research into second-generation feedstocks such as agricultural residues and municipal solid waste is ongoing, but commercial-scale technologies are not yet fully mature or cost-competitive. The logistical challenges of collecting and preprocessing heterogeneous waste streams further complicate the supply chain. Dependence on food crops also raises ethical concerns regarding land use and food security, which can hinder public acceptance and policy support. The lack of a diversified and robust feedstock base limits the ability of the industry to expand production capacity rapidly. Until alternative low-cost and abundant feed sources are commercially viable, the PHA market faces constraints in scaling up to meet potential demand. This supply-side bottleneck restricts market growth and innovation.

MARKET OPPORTUNITIES

Advancements in Metabolic Engineering and Fermentation Technology Offer Significant Cost Reduction Opportunities

Advancements in metabolic engineering and fermentation technology is a major opportunity for the Polyhydroxyalkanoate (PHA) Market by offering pathways to significantly reduce production costs and improve efficiency. Scientists are developing genetically modified bacterial strains that can produce higher yields of PHA from cheaper and more diverse feedstocks, including waste gases and lignocellulosic biomass. According to the National Renewable Energy Laboratory, researchers have demonstrated tar removal greater than 99% and have developed a method to tune CO2 content in final syngas from 1% to 15%, showcasing the ability to evaluate critical process integration parameters for waste feedstocks. This innovation not only lowers raw material costs but also enhances the sustainability profile of the product by utilizing greenhouse gases. As per the Journal of Industrial Microbiology and Biotechnology, optimized fermentation processes have increased productivity by up to 50% in pilot scales, demonstrating the potential for commercial viability. Companies investing in these technologies can achieve a competitive advantage by producing PHA at prices closer to conventional plastics. Furthermore, the ability to tailor the polymer structure through genetic manipulation allows for the creation of specialized PHAs with unique properties for high-value applications in medicine and electronics. These technological strides are attracting venture capital and strategic partnerships, accelerating the transition from lab to market. By leveraging biotechnology, the industry can overcome current economic barriers and unlock massive growth potential.

Expansion into High Value Medical and Pharmaceutical Applications Drives Premium Market Segments

The expansion of Polyhydroxyalkanoate (PHA) into high-value medical and pharmaceutical applications offers a lucrative opportunity for market growth by tapping into premium segments that prioritize biocompatibility and safety. PHA possesses excellent biocompatibility and biodegradability, making it ideal for use in sutures, drug delivery systems, tissue engineering scaffolds, and implantable devices. According to the World Health Organization, the average daily per capita intake of nutrient-rich food in lower-middle-income countries will increase by 25% by 2034, reflecting the broader health and biological focus in emerging economies. As per the American Chemical Society, PHA-based implants degrade naturally in the body, eliminating the need for secondary surgeries to remove them, which reduces healthcare costs and patient discomfort. The regulatory approval pathway for medical devices is rigorous, but once established, it creates high barriers to entry and long-term revenue streams. Companies are collaborating with research institutions to develop specialized PHA formulations for nerve regeneration and bone repair. The high-margin nature of the medical sector allows manufacturers to offset the higher production costs of PHA. Furthermore, the growing trend towards personalized medicine and regenerative therapies increases the demand for customizable biomaterials. By focusing on these specialized applications, PHA producers can diversify their revenue sources and establish a strong foothold in the healthcare industry. This strategic shift enhances the overall value proposition of PHA beyond packaging.

MARKET CHALLENGES

Inconsistent Global Standards for Biodegradability and Compostability Create Market Confusion

The inconsistent global standards for biodegradability and compostability that create confusion among consumers, regulators, and waste management facilities is a significant challenge to the growth of the global polyhydroxyalkanoate (PHA) market. Different countries and regions have varying definitions and testing protocols for what constitutes biodegradable or compostable, leading to fragmented certification requirements. According to the International Organization for Standardization, the ISO 17088 test provides guidelines for disintegration during composting requiring at least 90% dry weight pass through a 2.0-mm sieve over 84 days, but there is a lack of harmonized guidelines for home composting and marine degradation. As per the Biodegradable Products Institute, many products labeled as biodegradable do not break down effectively in local waste management systems, leading to contamination and skepticism. This inconsistency hinders the development of efficient recycling and composting infrastructure as facilities are unsure how to process PHA-containing waste. Manufacturers face high costs and delays in obtaining multiple certifications to access different markets. The lack of clear labeling also misleads consumers who may dispose of PHA products incorrectly, assuming they will degrade anywhere. This ambiguity undermines the environmental benefits of PHA and slows down its adoption. Until global standards are aligned and clearly communicated, the market will struggle to realize its full potential. Harmonization is essential for building trust and enabling seamless integration into circular economy systems.

Lack of Adequate Industrial Composting Infrastructure Limits Effective End of Life Management

The lack of adequate industrial composting infrastructure is another key challenge to the Polyhydroxyalkanoate (PHA) Market by limiting the effective end-of-life management of these biodegradable products. Although PHA is designed to degrade in composting environments, many municipalities lack the facilities to process bioplastics separately from conventional plastics and organic waste. According to the European Compost Network, only a limited number of European cities have access to industrial composting plants that accept bioplastics, leading to most PHA products ending up in landfills or incinerators. As per the United States Environmental Protection Agency, the majority of municipal solid waste in the United States is disposed of in landfills where anaerobic conditions may prevent proper degradation of PHA. This infrastructure gap means that the environmental benefits of PHA are not fully realized as the material does not return to the soil as intended. Contamination of recycling streams with bioplastics can also degrade the quality of recycled conventional plastics. Investment in separate collection and processing facilities is required but often lacks political and financial support. Without a robust infrastructure network, the value proposition of PHA is weakened. Stakeholders must collaborate to build the necessary waste management systems to support the circular lifecycle of biodegradable plastics.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 11.80% |

| Segments Covered | By Type, Production Method, and Region. |

|

Various Analyses Covered | Global, Regional, and Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa. |

| Market Leaders Profiled | Meredian, Inc., Tianan Biologic Materials Co. Ltd., PolyfermVanada, Inc., Shenzhen Ecomann Biotechnology Co, Ltd., LIC PHB Industrial S.A., Newlight Technologies, BioMatera, Inc., Metabolix Inc., Biomer, Biomatera, Kaneka Corporation., and Others. |

SEGMENTAL ANALYSIS

By Type Insights

The short chain length PHA segment led the market by accounting for 71.7% of the global market share in 2025. The dominance of short chain length PHA segment in the global market is driven by the commercial maturity of polyhydroxybutyrate (PHB) and its copolymers, which are easier to produce at scale compared to medium chain length variants. These polymers exhibit high crystallinity and stiffness, making them ideal replacements for conventional plastics like polypropylene in rigid packaging applications. According to European Bioplastics, short chain length PHAs account for the majority of current global production capacity due to well-optimized fermentation processes using standard bacterial strains such as Cupriavidus necator. The availability of raw materials like glucose and sucrose from abundant agricultural sources further supports cost-effective manufacturing. As per the United States Department of Agriculture, the extensive infrastructure for processing corn and sugarcane provides a reliable supply chain for the substrates required in short chain PHA synthesis. This logistical advantage reduces production risks and ensures consistent output quality. Furthermore, regulatory approvals for food contact applications have been secured for many short chain PHA formulations, facilitating their adoption in single-use items such as cutlery, containers, and films. The mechanical properties of these polymers can be enhanced through blending with other biodegradable materials, expanding their utility. Consequently, the combination of technological readiness, regulatory acceptance, and material versatility cements the leading position of short chain length PHA in the global market.

On the other hand, the medium chain length PHA segment is estimated to register a CAGR of 19.2% over the forecast period in the global market owing to their superior material properties and niche high value applications. These polymers are increasingly sought after for specialized applications in biomedical devices, flexible packaging, and adhesives where durability and elasticity are critical. According to the National Institutes of Health, research into medium chain length PHAs has accelerated due to their biocompatibility and ability to degrade into non-toxic byproducts, making them suitable for tissue engineering and drug delivery systems. As per the Journal of Polymers and the Environment, advancements in metabolic engineering have enabled the production of these complex polymers from renewable waste streams such as vegetable oils and fatty acids, reducing dependency on food crops. The growing demand for high-performance bioplastics in the automotive and electronics sectors also contributes to this growth trajectory. Manufacturers are investing in pilot plants to scale up production techniques that utilize Pseudomonas species which naturally synthesize medium chain length PHAs. The premium pricing associated with these specialized materials allows producers to offset higher production costs. Additionally, the increasing focus on circular economy principles drives interest in materials that offer both functionality and environmental sustainability. This convergence of scientific innovation and market demand positions medium chain length PHA as the most dynamic growth driver in the type segment.

By Production Method Insights

The packaging segment led the market by holding 61.6% of the global market share in 2025. The dominance of the packaging segment is driven by the urgent need to replace conventional petroleum-based plastics in single-use items such as bags, bottles, and food containers. Governments worldwide are implementing bans on non-biodegradable plastics, creating a mandatory shift towards compostable alternatives like PHA. According to the European Commission, the Single-Use Plastics Directive mandates a significant reduction in plastic waste, pushing retailers and manufacturers to adopt certified biodegradable materials. PHA offers the distinct advantage of marine biodegradability, which is crucial for preventing ocean pollution. As per the Ellen MacArthur Foundation, 95% of plastic packaging material value is lost to the economy annually after a short first-use cycle, representing a loss of between USD 80 billion and USD 120 billion. This high volume of waste generation creates a substantial market opportunity for PHA producers. Major consumer goods companies are committing to 100% reusable, recyclable, or compostable packaging by 2025, accelerating adoption. The ability of PHA to maintain barrier properties against moisture and oxygen makes it suitable for food preservation. Furthermore, advancements in film blowing and injection molding technologies have improved the processability of PHA, enabling mass production. The alignment of regulatory pressure, corporate sustainability goals, and consumer preference ensures that packaging remains the largest application segment for PHA globally.

The bio medical segment is estimated to record a promising CAGR of 23.2% over the forecast period owing to the exceptional biocompatibility and bioresorbability of PHA, which eliminates the need for secondary surgeries to remove implants. These properties make PHA ideal for sutures, bone fixation devices, tissue engineering scaffolds, and controlled-release drug delivery systems. According to the World Health Organization, global fish and agricultural production is expected to increase by 14% over the next decade, underlining the resource availability for medical-grade biopolymers. As per the American Chemical Society, clinical trials involving PHA-based nerve guides and cardiovascular patches have shown promising results, leading to increased investment in medical-grade PHA production. The high-value nature of medical devices allows manufacturers to absorb the higher production costs of PHA compared to commodity plastics. Regulatory bodies such as the Food and Drug Administration are streamlining approval pathways for novel biomaterials that demonstrate safety and efficacy. Furthermore, the rise in chronic diseases and sports injuries drives the need for innovative solutions that support tissue regeneration without causing immune responses. Research institutions and pharmaceutical companies are collaborating to develop customized PHA formulations for specific medical applications. This synergy between medical innovation and material science positions the bio-medical sector as the most rapidly expanding area in the PHA market.

REGIONAL ANALYSIS

Europe Polyhydroxyalkanoate (PHA) Market Analysis

Europe dominated the PHA market worldwide in 2025. The growth of Europe in the global market is attributed to the robust regulatory frameworks and strong consumer awareness regarding sustainability. Europe maintains its leadership position due to the aggressive implementation of environmental policies such as the European Green Deal and the Circular Economy Action Plan, which prioritize the reduction of plastic waste. The region boasts a high density of bioplastic manufacturers and research institutions, driving innovation in PHA production and application. According to European Bioplastics, Europe accounts for nearly 25% of the global bioplastics production capacity with significant investments in PHA facilities. As per the German Federal Ministry for the Environment, strict labeling requirements and composting standards encourage the use of certified biodegradable materials like PHA in packaging and agriculture. Consumer willingness to pay a premium for eco-friendly products further supports market growth. The presence of major chemical companies transitioning towards bio-based portfolios enhances supply chain stability. Additionally, the European Union funding programs support collaborative projects aimed at scaling up PHA production from waste feedstocks. The well-developed waste management infrastructure, including industrial composting facilities, ensures that PHA products can be effectively processed at end-of-life. This comprehensive ecosystem of policy, innovation, and infrastructure solidifies Europe's dominance in the global PHA market.

North America Polyhydroxyalkanoate (PHA) Market Analysis

North America represents a significant market for PHA and the growth of North America is driven by technological advancements and increasing corporate sustainability commitments. North America holds a prominent position in the market due to the presence of leading PHA producers and advanced biotechnology research capabilities. The United States and Canada are witnessing growing adoption of PHA in packaging and agricultural applications, supported by state-level bans on single-use plastics. According to the Biodegradable Products Institute, certification for compostable products has increased significantly, facilitating market entry for PHA-based items. As per the United States Department of Energy, federal initiatives promoting the bioeconomy provide financial incentives for the development of renewable materials. Major retail chains and food service providers are partnering with PHA manufacturers to replace conventional plastics in their supply chains. The region's strong focus on innovation leads to continuous improvements in fermentation efficiency and polymer performance. Additionally, the growing awareness of microplastic pollution among consumers drives demand for marine degradable alternatives. Investment from venture capital firms in start-ups specializing in PHA production further accelerates market expansion. The integration of PHA into existing manufacturing processes is facilitated by the region's advanced industrial base. These factors collectively establish North America as a key driver of growth and innovation in the global PHA landscape.

Asia Pacific Polyhydroxyalkanoate (PHA) Market Analysis

Asia Pacific is the fastest growing region in the global PHA market due to the rapid industrialization and increasing government support for green technologies. Asia Pacific is emerging as a critical hub for PHA production and consumption, driven by countries like China, Japan, and India, which are investing heavily in bio-based materials. The region's large manufacturing base provides a vast market for sustainable packaging solutions as exporters face pressure to meet international environmental standards. According to the Chinese Ministry of Industry and Information Technology, national plans aim to significantly increase the production capacity of biodegradable plastics to address severe pollution issues. As per the Japan Bioplastics Association, collaborations between academic institutions and industry players are advancing PHA technology and reducing production costs. The abundance of agricultural residues in the region offers a cost-effective feedstock source for PHA fermentation. Rising middle-class populations are becoming more environmentally conscious, driving demand for green products. Government subsidies and tax incentives encourage local production, reducing reliance on imports. Furthermore, the expansion of e-commerce in the region increases the demand for sustainable packaging materials. The combination of policy support, resource availability, and market demand positions Asia Pacific as a dynamic and rapidly expanding segment in the global PHA market.

Latin America Polyhydroxyalkanoate (PHA) Market Analysis

Latin America is predicted to account for a notable share of the global polyhydroxyalkanoate (PHA) market during the forecast period due to its strong agricultural sector and potential for sustainable feedstock production. Latin America is leveraging its abundant agricultural resources to emerge as a potential leader in PHA feedstock supply and production. Countries like Brazil and Argentina are exploring the use of sugarcane and corn derivatives for PHA fermentation, aligning with their existing biofuel industries. According to the Inter-American Development Bank, initiatives promoting the circular economy are gaining traction in the region, encouraging the adoption of biodegradable materials. As per the Brazilian Association of Technical Standards, certifications for compostable plastics are being standardized to facilitate market growth. The tourism industry in coastal areas is driving demand for marine degradable packaging to protect natural ecosystems. Local governments are implementing waste management reforms that favor biodegradable options. Although production capacity is currently limited compared to other regions, investment in pilot plants is increasing. The region's commitment to sustainable development goals supports long-term market expansion. Partnerships with international technology providers are enhancing local manufacturing capabilities. These efforts position Latin America as a promising emerging market with significant growth potential in the PHA sector.

Middle East and Africa Polyhydroxyalkanoate (PHA) Market Analysis

The Middle East and Africa represent an emerging market for PHA owing to the initial stages of adoption and growing environmental awareness. The Middle East and Africa are beginning to explore PHA as part of broader strategies to diversify economies and address environmental challenges. Countries in the Gulf Cooperation Council are investing in sustainability initiatives as part of their vision plans, which include reducing plastic waste. According to the United Nations Environment Programme, regional campaigns against plastic pollution are raising awareness and encouraging the adoption of alternative materials. As per the South African Bureau of Standards, discussions on regulating single-use plastics are prompting businesses to consider biodegradable options. The region's focus on water conservation and agriculture creates opportunities for PHA-based mulch films that degrade naturally. Limited local production capacity means the market currently relies on imports, but interest in local manufacturing is growing. International collaborations and technology transfers are facilitating knowledge exchange and capacity building. The hot climate poses challenges for waste management, making biodegradable solutions attractive. While the market is small compared to other regions, the foundational steps being taken suggest future growth potential as infrastructure and regulations develop.

COMPETITIVE LANDSCAPE

The competition in the Polyhydroxyalkanoate (PHA) Market is characterized by a mix of established chemical giants and specialized biotechnology start ups striving to commercialize scalable production methods. Leading players compete on the basis of production efficiency cost reduction and product performance to capture market share from conventional plastics. The market is moderately fragmented with several key companies holding significant intellectual property rights related to fermentation strains and processing technologies. Competitive advantage is often derived from the ability to produce PHA at lower costs using non food feedstocks which addresses sustainability concerns and price sensitivity. Regulatory compliance and certification for biodegradability serve as critical differentiators as customers seek verified solutions for plastic waste reduction. Collaboration across the value chain including partnerships with waste management firms and brand owners is essential for creating a robust ecosystem. New entrants face high barriers due to capital intensive infrastructure requirements and complex technical challenges. However increasing government support and consumer demand for sustainable materials are lowering these barriers. Overall the market rewards innovation and scalability driving continuous improvement in technology and application diversity.

Key Market Players

- Meredian, Inc.

- Tianan Biologic Materials Co. Ltd.

- PolyfermVanada, Inc.

- Shenzhen Ecomann Biotechnology Co., Ltd.

- LIC PHB Industrial S.A.

- Newlight Technologies

- BioMatera, Inc.

- Metabolix Inc.

- Biomer

- Biomatera

- Kaneka Corporation

Top Players in the Market

- Danimer Scientific is a leading innovator in the development and production of biodegradable polymers including its proprietary Nodax PHA. The company contributes to the global market by providing scalable solutions for single use plastics that degrade in natural environments. Danimer has recently expanded its manufacturing capacity in Kentucky and Georgia to meet rising demand from consumer goods companies. They have secured partnerships with major brands to replace conventional plastics in packaging and disposable items. The company focuses on vertical integration by controlling the entire production process from fermentation to polymer extraction. Recent investments in research and development aim to improve the thermal properties and processability of PHA. These strategic moves strengthen their position as a key supplier of sustainable materials and support the transition towards a circular economy while reducing reliance on fossil based plastics.

- Kaneka Corporation is a prominent Japanese chemical company that produces PHA under the brand name Green Planet. The company plays a vital role in the global market by offering high quality biodegradable polymers for various applications including agriculture and packaging. Kaneka has recently enhanced its production capabilities in Japan to ensure a stable supply of PHA resins. They actively collaborate with downstream manufacturers to develop new formulations that meet specific performance requirements. The company emphasizes sustainability by utilizing renewable feedstocks and optimizing energy efficiency in its processes. Kaneka also engages in educational initiatives to promote the benefits of biodegradable plastics among consumers and regulators. Their commitment to innovation and quality assurance helps drive the adoption of PHA in diverse industries. By leveraging its extensive chemical expertise Kaneka strengthens its market presence and supports global efforts to reduce plastic pollution effectively.

- RWDC Industries is a pioneer in the commercialization of PHA based products focusing on sustainable alternatives to single use plastics. The company contributes to the global market by producing Solon a fully biodegradable material suitable for straws cutlery and packaging. RWDC has recently scaled up its production facilities in Singapore and the United States to increase output and reduce costs. They partner with hospitality and retail chains to implement eco friendly solutions that align with regulatory mandates. The company invests heavily in proprietary fermentation technology to enhance yield and purity of PHA. RWDC also advocates for policy changes that support the adoption of biodegradable materials. Their strategic focus on high volume applications helps drive market penetration and awareness. By delivering consistent quality and performance RWDC Industries strengthens its position as a leader in the bioplastics sector and promotes environmental sustainability through innovative material science.

Top Strategies Used by the Key Market Participants

Key players in the Polyhydroxyalkanoate (PHA) Market primarily focus on scaling production capacity to achieve cost competitiveness with conventional plastics. Companies invest heavily in expanding fermentation facilities and optimizing downstream processing techniques to improve yield and efficiency. Strategic partnerships with major consumer goods brands are common to secure long term off take agreements and validate product performance in real world applications. Innovation in genetic engineering is employed to develop bacterial strains that produce PHA from low cost waste feedstocks such as agricultural residues and municipal solid waste. This approach reduces raw material costs and enhances sustainability credentials. Manufacturers also prioritize obtaining certifications for compostability and biodegradability to meet regulatory requirements and build consumer trust. Diversification into high value applications like biomedical devices and agriculture helps mitigate risks associated with commodity packaging markets. These strategies collectively enable participants to overcome economic barriers and accelerate the widespread adoption of PHA globally.

MARKET SEGMENTATION

This research report on the global polyhydroxyalkanoate (PHA) market has been segmented and sub-segmented based on type, production method, and region.

By Type

- Short-Chain Length

- Medium-Chain Length

By Production Method

- Packaging

- Bio-Medical

- Food

- Agriculture

- Others

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Frequently Asked Questions

1. What is polyhydroxyalkanoate (PHA)?

Polyhydroxyalkanoate is a biodegradable and bio based polymer produced by microorganisms and used as an alternative to conventional plastics.

2. What is the PHA market?

The PHA market covers production, processing, and application of PHA materials across packaging, medical, and consumer goods industries.

3. What factors are driving growth of the PHA market?

Growth is driven by environmental regulations, demand for sustainable materials, and increasing awareness of plastic pollution.

4. What are the major applications of PHA?

PHA is widely used in packaging, agricultural films, medical devices, disposable products, and consumer goods.

5. Which regions are key contributors to the PHA market?

North America, Europe, and Asia Pacific are key regions due to strong research activity and sustainability initiatives.

6. How does PHA differ from conventional plastics?

PHA is biodegradable and bio based, while conventional plastics are petroleum based and non biodegradable.

7. What role does PHA play in sustainable packaging?

PHA supports sustainable packaging by offering compostable and environmentally friendly alternatives to single use plastics.

8. What challenges affect the PHA market?

Challenges include high production costs, limited large scale manufacturing, and performance limitations in some applications.

9. Who are the major end users of PHA?

Major end users include packaging manufacturers, medical device companies, agricultural producers, and consumer product brands.

10. What is the future outlook for the PHA market?

The market is expected to grow significantly due to rising sustainability demand, innovation, and regulatory support.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com