Global Power System Simulation Market Size, Share, Trends, & Growth Forecast Report – Segmented By Offering (Hardware, Software, and Services), Module (Short Circuit, Load Flow, Device Coordination Selectivity, Arc Flash, Others), End-User (Power Generation, Transmission and Distribution, Oil & Gas, Manufacturing, Metals and Mining, Others), & Region - Industry Forecast From 2026 to 2034

Global Power System Simulation Market Report Summary

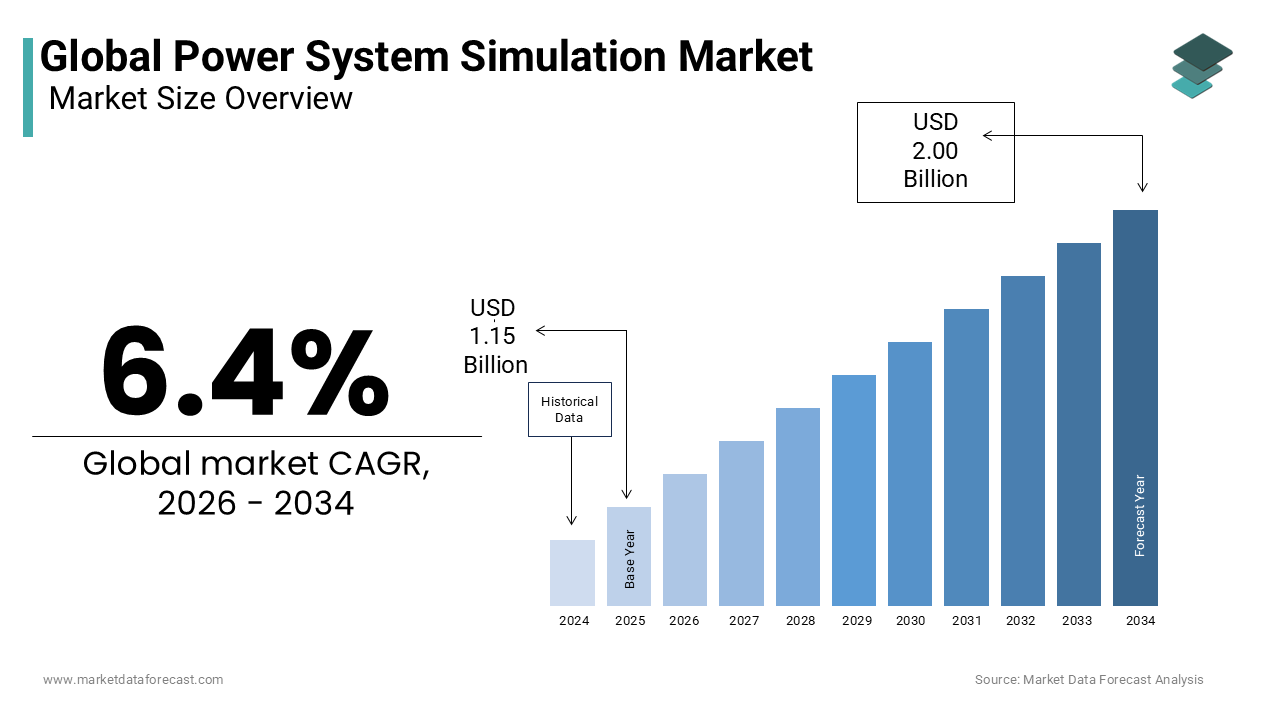

The global power system simulation market was valued at USD 1.15 billion in 2025 and is anticipated to reach USD 1.22 billion in 2026 from USD 2.00 billion by 2034, growing at a CAGR of 6.4% during the forecast period from 2026 to 2034. The growth of the global power system simulation market is driven by the rapid integration of renewable energy sources, increasing modernization of aging power infrastructure, and rising investments in smart grid technologies. Growing demand for reliable grid operation, increasing adoption of digital substations, and expanding deployment of distributed energy resources are further accelerating market growth. Moreover, the emergence of digital twin technologies, integration of artificial intelligence with grid analytics, and rising investments in electric vehicle charging infrastructure are supporting the expansion of the global power system simulation market.

Key Market Trends

-

Rising adoption of digital twin technologies for real-time power grid monitoring and predictive maintenance.

-

Increasing integration of renewable energy sources requiring advanced grid stability and transient simulation.

-

Growing utilization of artificial intelligence and machine learning in power system analytics.

-

Rising investments in smart grids and grid modernization initiatives worldwide.

-

Increasing demand for simulation platforms supporting electric vehicle charging infrastructure planning.

Segmental Insights

Based on offering, the software segment dominated the global power system simulation market in 2025. The dominance of the segment is attributed to the increasing complexity of modern electrical grids, growing adoption of renewable energy integration, rising demand for power flow analysis, and continuous utilization of simulation software for contingency planning and operational optimization. Continuous technological advancements in modeling capabilities further strengthen segment growth.

The services segment is projected to witness the fastest CAGR during the forecast period owing to the growing shortage of skilled power system engineers, increasing outsourcing of simulation and consulting services, rising implementation of customized grid modeling solutions, and expanding demand for software integration, technical support, and training services.

Based on module, the load flow segment accounted for the largest share of the global power system simulation market in 2025. The dominance of the segment is driven by its essential role in voltage profiling, power flow calculations, transmission planning, contingency analysis, and day-to-day utility operations. Widespread deployment across transmission system operators and distribution utilities continues to support segment leadership.

The arc flash segment is anticipated to register the fastest CAGR during the forecast period due to increasingly stringent workplace electrical safety regulations, rising industrial safety awareness, growing compliance with NFPA and OSHA standards, and expanding adoption of arc flash hazard analysis across manufacturing, utilities, and commercial facilities.

Based on end-user, the transmission and distribution segment dominated the global power system simulation market in 2025. The growth of the segment is driven by massive investments in grid modernization, replacement of aging transmission infrastructure, increasing integration of distributed energy resources, and growing demand for reliable electricity transmission across expanding power networks.

The power generation segment is expected to witness the fastest growth during the forecast period owing to rapid deployment of renewable energy projects, increasing grid code compliance requirements, expanding installation of wind and solar power plants, and growing utilization of dynamic simulation tools for renewable energy integration and stability analysis.

Regional Insights

- The United States dominated the global power system simulation market in 2025 due to extensive investments in grid modernization, large-scale smart grid deployment, increasing renewable energy integration, and strong regulatory emphasis on grid reliability and resilience. The country's advanced utility infrastructure and significant investments in digital transformation continue to support market leadership.

- Germany held a significant position in the global market owing to aggressive renewable energy transition initiatives, widespread deployment of smart grid technologies, increasing offshore wind integration, and growing investments in cross-border transmission infrastructure. Strong regulatory support for energy transition further strengthens market expansion.

- China is projected to witness substantial growth during the forecast period due to rapid expansion of ultra-high-voltage transmission networks, increasing renewable energy installations, growing electricity demand, and significant government investments in digital grid infrastructure. The country's ambitious clean energy transition continues to accelerate adoption of advanced simulation platforms.

- Brazil continues to maintain a notable position in the global market due to modernization of transmission infrastructure, increasing hydropower optimization initiatives, growing renewable energy deployment, and rising investments in grid resilience against extreme weather conditions.

- Saudi Arabia is expected to experience rapid growth during the forecast period owing to major smart city developments, increasing utility-scale renewable energy projects, expanding power infrastructure under Vision 2030, and growing adoption of advanced digital grid management technologies.

Competitive Landscape

The global power system simulation market is highly competitive and characterized by the presence of multinational technology companies and specialized engineering software developers competing through technological innovation, cloud-based deployment, artificial intelligence integration, and digital twin capabilities. Leading companies are focusing on developing advanced simulation platforms, expanding software-as-a-service offerings, strengthening predictive analytics capabilities, and integrating simulation environments with real-time operational technologies. Strategic acquisitions, global expansion initiatives, partnerships with utilities, and continuous investments in research and development continue to strengthen competitive positioning across the global power system simulation market. The prominent players operating in the global power system simulation market include Siemens AG, General Electric, ABB Ltd., Schneider Electric SE, Eaton Corporation, ETAP (Operation Technology, Inc.), PowerWorld Corporation, Open Systems International, Inc., PSS® SINCAL, and NEPLAN AG.

Global Power System Simulation Market Size

The size of the global power system simulation market was worth USD 1.15 billion in 2025. The global market is anticipated to grow at a CAGR of 6.4% from 2026 to 2034 and be worth USD 2.00 billion by 2034 from USD 1.22 billion in 2026.

Power system simulation is advanced computational software and modeling tools designed to analyze the behavior, stability, and performance of electrical grids under various operational conditions. These sophisticated digital environments allow engineers to simulate power flow, transient stability, and fault analysis, ensuring the reliable delivery of electricity across complex networks. As per the International Energy Agency, global electricity demand is projected to reach an unprecedented 40,000 terawatt hours by the year 2030, driven by rapid industrialization and digitalization. To meet this colossal demand, the integration of decentralized and intermittent energy sources has become mandatory. According to the International Renewable Energy Agency, the global capacity of renewable power technologies expanded by a record 50% in the previous year, reaching over 500 gigawatts of new installations. This massive influx of variable energy sources fundamentally alters the traditional unidirectional flow of electricity, requiring grid operators to utilize advanced simulation platforms to predict fluctuations and maintain frequency balance. Furthermore, according to estimates by the World Economic Forum, the global power sector must invest approximately 1,500 billion dollars annually until 2030 to upgrade aging infrastructure and accommodate these new energy paradigms. Consequently, the necessity to virtually test grid modifications before physical implementation has made simulation software an indispensable asset for modern utility companies and independent system operators striving to maintain uninterrupted power delivery in an increasingly complex energy landscape.

MARKET DRIVERS

Rapid Integration of Variable Renewable Energy Sources

The massive integration of intermittent renewable energy sources is majorly driving the expansion of the global power system simulation market. Traditional electrical grids were designed for predictable, unidirectional power flow from centralized fossil fuel plants, but the modern landscape is dominated by decentralized solar and wind installations that generate electricity unpredictably. According to the International Renewable Energy Agency, the global installed capacity of solar photovoltaic and wind power surpassed 1,000 gigawatts recently, creating immense volatility in grid frequency and voltage levels. To prevent catastrophic blackouts and equipment damage, grid operators must continuously simulate thousands of operational scenarios to determine the optimal placement of energy storage systems and reactive power compensators. According to the International Energy Agency, variable renewable energy generation will account for nearly 40% of total global electricity production by the end of the decade. This profound shift necessitates the use of highly sophisticated electromagnetic transient simulation tools to analyze the complex interactions between power electronics and the physical grid infrastructure. By virtually testing the grid response to sudden drops in wind speed or cloud cover over solar farms, engineers can design robust control strategies that ensure absolute stability. Consequently, the relentless expansion of clean energy capacity directly mandates the continuous procurement of advanced simulation software to maintain the delicate balance of modern power networks.

Modernization and Capital Investment in Aging Grid Infrastructure

The urgent modernization of aging electrical infrastructure is further boosting the expansion of the global market. A significant portion of the global transmission and distribution network was constructed decades ago and is currently operating beyond its intended operational lifespan, leading to increased failure rates and inefficiencies. According to the American Society of Civil Engineers, nearly 70% of the transmission and distribution transformers in the United States are 25 years or older, and are approaching the end of their expected lifecycle. Replacing or upgrading this massive physical infrastructure requires immense capital investment, and carries severe risks if not properly planned. Utility companies utilize advanced power flow and contingency analysis software to simulate the exact electrical behavior of the grid before executing any physical modifications. According to the World Economic Forum, upgrading the global electricity network requires an annual investment of at least 800 billion dollars to prevent systemic failures and accommodate new load centers. By creating precise digital replicas of the physical grid, engineers can identify critical bottlenecks, optimize conductor routing, and ensure that new high-voltage equipment integrates seamlessly without causing unintended, cascading outages. This proactive virtual planning minimizes financial risks and ensures that physical infrastructure upgrades are executed flawlessly, thereby driving continuous demand for sophisticated simulation platforms across the global utility sector.

MARKET RESTRAINTS

High Capital Expenditure and Implementation Barriers for Small Utilities

The exorbitant initial capital expenditure and the complex technical implementation required for advanced simulation platforms severely restrict their widespread adoption among smaller utility providers, which is a significant restraint for the global market growth. Developing a highly accurate digital model of a vast electrical network requires purchasing expensive enterprise software licenses, procuring high-performance computing hardware, and hiring specialized engineering consultants. According to the Electric Power Research Institute, the total cost of implementing a comprehensive grid modernization and simulation framework can consume up to 30% of the overall capital budget allocated for digital transformation initiatives. For regional distribution companies operating on tight profit margins, these upfront financial barriers are often insurmountable without significant government subsidies or regulatory approval for rate hikes. Furthermore, the integration of these sophisticated platforms with existing legacy operational systems requires extensive custom programming and rigorous testing phases, which can delay project completion by several months. According to the Global Energy Monitor, smaller municipal utilities frequently lack the internal financial resources to justify the massive return on investment timeline associated with enterprise-grade simulation tools. Consequently, the prohibitive costs and the steep learning curve associated with deploying these advanced analytical environments act as a substantial bottleneck, preventing many smaller grid operators from fully leveraging modern simulation capabilities to optimize their network performance.

Talent Deficit and Looming Engineering Workforce Retirement

The critical shortage of highly skilled power systems engineers and specialized software analysts significantly hinders the expansion of the global market. Operating sophisticated electromagnetic transient and dynamic stability simulation platforms requires deep academic knowledge in electrical engineering, combined with extensive practical experience in software configuration and data interpretation. According to the Institute of Electrical and Electronics Engineers, the global power engineering sector is currently facing a severe talent deficit, with nearly 40% of senior grid experts approaching retirement age and an insufficient number of new graduates entering the specialized field. This massive knowledge gap leaves many utility companies unable to fully exploit the advanced features of their simulation software, leading to underutilization of expensive digital assets. According to the World Economic Forum, the rapid transition to complex smart grid architectures requires a workforce proficient in both traditional power systems theory and modern data analytics. Without adequately trained personnel, utilities cannot accurately model the intricate interactions of distributed energy resources or interpret the massive datasets generated by dynamic simulations. Consequently, this acute scarcity of specialized technical expertise severely limits the operational efficiency and strategic deployment of advanced simulation platforms across the global electrical infrastructure sector.

MARKET OPPORTUNITIES

Integration of Real-Time Digital Twins and Predictive Machine Learning

The rapid evolution of digital twin technology and advanced data analytics presents a promising opportunity for the global power system simulation market. A digital twin is a highly dynamic and continuously updated virtual replica of the physical electrical grid that ingests real-time data from thousands of sensors to simulate current and future operational states. According to Deloitte, the global market for digital twin technology in the energy sector is expanding at an unprecedented rate, with over 60% of major utility companies planning to implement comprehensive digital twin frameworks within the next three years. By integrating machine learning algorithms with traditional power flow simulation engines, providers can create predictive models that automatically forecast equipment failures and optimize power routing before physical anomalies occur. According to the International Energy Agency, the deployment of advanced analytics and digital replicas can reduce grid operational costs by up to 20%, while significantly improving overall system reliability. This paradigm shift transforms simulation software from a static planning tool into an active operational asset that continuously guides decision-makers in managing complex grid dynamics. Consequently, simulation vendors that successfully merge traditional physics-based modeling with modern digital twin architectures will capture immense value and secure long-term contracts with forward-thinking utility operators.

Fleet Electrification and EV Charging Infrastructure Modeling

The massive global transition toward the electrification of transportation and the widespread deployment of electric vehicle charging infrastructure is another prominent opportunity for the global market. The uncoordinated charging of millions of electric vehicles places extreme and highly unpredictable stress on local distribution transformers and low-voltage networks, potentially causing severe voltage drops and thermal overloads. According to the International Energy Agency, the global stock of electric cars surpassed 40 million units recently and is projected to exceed 300 million by the end of the decade, requiring a colossal expansion of charging infrastructure. To prevent localized grid collapse, distribution system operators must utilize advanced simulation tools to model the exact spatial and temporal impact of electric vehicle charging patterns on neighborhood networks. According to the Edison Electric Institute, proactive grid planning using advanced simulation software can defer the need for expensive physical infrastructure upgrades by up to 5 years through the strategic implementation of smart charging algorithms. By providing utilities with the ability to virtually test the integration of thousands of charging stations, simulation providers can unlock a massive new revenue stream. Consequently, the relentless electrification of the transport sector guarantees a sustained and growing demand for highly specialized distribution network modeling solutions.

MARKET CHALLENGES

Cybersecurity Vulnerabilities and False Data Injection Threats

The escalating frequency and sophistication of cyberattacks targeting critical energy infrastructure is primarily challenging the expansion of the global market. As simulation software becomes increasingly interconnected with live operational technology networks and cloud-based data repositories, it expands the potential attack surface for malicious actors seeking to disrupt national power supplies. According to the International Energy Agency, cyber incidents targeting the global electricity sector have increased by over 300% in the past five years, highlighting the extreme vulnerability of digital grid management tools. If a simulation platform is compromised, attackers could inject false data into the digital model, causing operators to make catastrophic physical switching decisions that lead to widespread blackouts. According to the World Economic Forum, securing the software supply chain and implementing zero-trust architectures within simulation environments requires massive and continuous financial investment. Furthermore, regulatory bodies are imposing stringent cybersecurity compliance mandates that force simulation vendors to constantly redesign their software architectures to patch emerging vulnerabilities. This relentless cat-and-mouse game with sophisticated threat actors significantly increases the operational burden and development costs for software providers. Consequently, maintaining absolute data integrity and protecting highly sensitive grid topology information from cyber espionage remains a formidable and ongoing challenge for the entire simulation industry.

Legacy Infrastructure Fragmentation and Interoperability Hurdles

The profound lack of seamless interoperability between modern simulation platforms and deeply entrenched legacy operational systems is further challenging the expansion of the global market. Many utility companies still rely on decades-old supervisory control and data acquisition systems and outdated energy management systems that utilize proprietary communication protocols incompatible with contemporary simulation software. According to the United States Department of Energy, nearly 40% of the digital infrastructure operating within regional transmission organizations was deployed before the year 2010, and lacks the open architecture required for modern data integration. These technological fragmentation forces simulation vendors to develop expensive and highly complex custom middleware, just to extract the necessary real-time data required to initialize and update their digital models. According to the Global Energy Monitor, data synchronization errors caused by poor interoperability can lead to inaccurate simulation results, which severely undermine operator confidence in the software outputs. Overcoming these deep-rooted integration barriers requires extensive collaboration between software developers, hardware manufacturers, and utility information technology departments to establish universal data exchange standards. Consequently, the persistent inability to seamlessly connect advanced simulation tools with aging legacy networks significantly delays project deployment and limits the overall effectiveness of modern grid management strategies.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 6.4% |

| Segments Covered | By Offering, Module, End-User, and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Siemens AG, General Electric, ABB Ltd., Schneider Electric SE, Eaton Corporation, ETAP/Operation Technology, Inc., PowerWorld Corporation, Open Systems International, Inc., PSS SINCAL, Neplan AG, and Others. |

SEGMENTAL ANALYSIS

By Offering Insights

The software segment dominated the market by holding the largest share of the global market in 2025. The absolute necessity for complex mathematical modeling and precise grid topology mapping establishes software as the undisputed leader in the market. Modern electrical grids comprise millions of interconnected nodes, requiring continuous computational analysis to maintain stability and prevent catastrophic failures. Software platforms provide the fundamental algorithms required to solve intricate differential equations that govern power flow and transient dynamics. According to the Institute of Electrical and Electronics Engineers, the average modern transmission network contains over 50,000 distinct operational nodes that must be simultaneously calculated during a single contingency analysis. This immense computational burden can only be managed by highly specialized software engines capable of processing massive datasets in milliseconds. Furthermore, according to the International Energy Agency, the integration of decentralized renewable energy sources has increased grid complexity by over 40% in the last decade. Grid operators rely entirely on advanced software modules to simulate the unpredictable behavior of solar and wind farms, ensuring that voltage levels remain within safe operational limits. Without these sophisticated digital tools, utility companies would be entirely blind to the dynamic electrical phenomena occurring within their networks, making software the indispensable core of all power system simulation endeavors.

On the other end, the services segment is a promising segment and is estimated to register a healthy CAGR in the global market during the forecast period. The critical shortage of specialized power systems engineering talent creates an immense demand for external consulting and custom model development services. Operating advanced electromagnetic transient simulation platforms requires deep academic knowledge, combined with extensive practical experience in software configuration and data interpretation. According to the World Economic Forum, the global power engineering sector is currently facing a severe talent deficit, with nearly 40% of senior grid experts approaching retirement age. This massive knowledge gap leaves many utility companies unable to fully exploit the advanced features of their simulation software without external assistance. Service providers step in to bridge this void by offering highly skilled consultants who can build precise digital replicas of complex physical networks. According to the International Energy Agency, over 50% of regional distribution operators now outsource their grid modeling tasks to specialized engineering firms to ensure absolute accuracy. By leveraging external expertise, utilities can avoid the massive costs associated with hiring and training permanent internal teams. Consequently, this acute scarcity of specialized technical expertise guarantees that professional services will expand at the fastest pace within the market.

By Module Insights

The load flow segment led the market by capturing the highest share of the global market in 2025. The fundamental requirement for steady-state grid analysis and comprehensive voltage profiling secures the load flow module as the primary market leader. Load flow studies form the absolute bedrock of all power system planning, allowing engineers to determine the voltage magnitude and phase angle at every single node in the network. According to the North American Electric Reliability Corporation, every major transmission operator must conduct rigorous load flow analyses daily to ensure that all equipment operates within its thermal and voltage limits. This module calculates the exact distribution of active and reactive power across thousands of transmission lines, preventing dangerous overloads that could trigger cascading failures. According to the Institute of Electrical and Electronics Engineers, over 80% of all routine grid planning activities rely entirely on load flow algorithms to evaluate the impact of new customer connections. Without this foundational analysis, utility companies would be unable to guarantee the quality of electricity delivered to end consumers, or ensure the safe loading of transformers. Consequently, the indispensable nature of steady-state voltage and power calculations ensures that the load flow module remains the most widely utilized and dominant segment in the entire simulation landscape.

However, the arc flash segment is estimated to record a prominent CAGR in the global market during the forecast period. The implementation of stringent global workplace safety regulations mandating comprehensive hazard analysis propels the arc flash module to the fastest growth rate. An arc flash is a catastrophic release of energy caused by an electrical short circuit, producing extreme heat and blinding light that can be fatal to nearby personnel. Governments and international safety bodies now strictly require facility operators to calculate the exact incident energy levels at every electrical panel to determine the necessary personal protective equipment. According to the Occupational Safety and Health Administration, workplace electrical injuries result in over 300 fatalities and over 3,000 severe burns annually, prompting aggressive enforcement of safety standards. According to regulations from the National Fire Protection Association, all commercial and industrial facilities must conduct detailed arc flash studies and update them whenever the power system configuration changes. Simulation software provides the precise mathematical modeling required to calculate the available fault current and the exact clearing time of protective devices. According to the International Labour Organization, compliance with these rigorous safety protocols is nonnegotiable and heavily penalized. Consequently, the legal and moral imperative to protect human life ensures that the arc flash analysis module will expand at an unprecedented pace across all industrial sectors.

By End-User Insights

The transmission and distribution segment held the major share of the global market in 2025. The massive global investments in upgrading aging grid infrastructure and expanding transmission networks establish the transmission and distribution sector as the dominant end-user. A significant portion of the global electrical network was constructed decades ago and is currently operating beyond its intended operational lifespan, requiring complete digital and physical modernization. According to the American Society of Civil Engineers, nearly 70% of the transmission and distribution transformers in the United States are 25 years or older, and are approaching the end of their expected lifecycle. Utility companies must utilize advanced simulation platforms to meticulously plan the replacement of these critical assets without causing widespread power outages. According to the World Economic Forum, upgrading the global electricity network requires an annual investment of at least 800 billion dollars to prevent systemic failures and accommodate new load centers. Every single physical upgrade must be preceded by rigorous contingency analysis and power flow studies to ensure that the modified network remains perfectly stable. Consequently, the sheer scale of the capital expenditure directed toward maintaining and expanding the physical wires and transformers guarantees that the transmission and distribution sector will remain the largest consumer of simulation technology.

However, the power generation segment is estimated to showcase a promising CAGR in the global market during the forecast period. The rapid deployment of renewable energy plants requiring dynamic stability studies and grid code compliance propels the power generation sector to the fastest growth rate. Unlike traditional synchronous generators, solar and wind farms rely on power electronics that respond entirely differently to grid disturbances, requiring highly specialized simulation models to prove their stability. According to the International Energy Agency, global renewable power capacity expanded by a record 50% in the previous year, reaching over 500 gigawatts of new installations. Every single new wind farm or solar park must undergo rigorous electromagnetic transient simulations to demonstrate to grid operators that it will not cause frequency collapses or voltage instability during a fault. According to the Global Wind Energy Association, modern grid codes now mandate detailed dynamic modeling of the entire wind turbine control system before physical connection is permitted. Power generation companies must continuously refine their simulation models to optimize the performance of their assets and avoid severe financial penalties for noncompliance. Consequently, the relentless global rush to build clean energy infrastructure guarantees that power generation entities will drive the most rapid expansion of advanced simulation technologies.

REGIONAL ANALYSIS

United States Power System Simulation Market Analysis

The United States is projected to face heightened demand for comprehensive grid modernization over the next few years due to escalating peak load pressures and strict clean energy mandates requiring massive structural upgrades. According to the United States Department of Energy, the national electricity grid requires over 70 billion dollars in annual upgrades to accommodate decentralized power generation and aging infrastructure replacement. This massive financial commitment drives the continuous procurement of advanced simulation platforms to ensure absolute grid stability and operational efficiency. Furthermore, according to directives from the Federal Energy Regulatory Commission, rigorous reliability standards are mandated that compel utility operators to perform extensive contingency analyses before implementing any physical modifications. According to the North American Electric Reliability Corporation, over 80% of transmission operators utilize dynamic modeling tools to prevent cascading failures during extreme weather events and peak demand periods. Consequently, the stringent regulatory environment and the sheer scale of infrastructure modernization projects guarantee that this region remains the most lucrative and technologically advanced hub for power system simulation software and services worldwide today.

Germany Power System Simulation Market Analysis

Germany is poised to accelerate its deployment of high-fidelity grid management software over the next few years as the country aggressively transitions away from conventional base-load plants toward decentralized offshore wind loops. Europe maintains a highly influential position in the regional sector, characterized by aggressive decarbonization targets and the widespread deployment of smart grid technologies. According to the European Commission, the integration of variable renewable energy sources requires an annual investment of 450 billion euros in energy infrastructure through the end of the decade. Grid operators must utilize sophisticated electromagnetic transient simulation tools to manage the complex bidirectional power flows generated by millions of rooftop solar panels and wind turbines. According to the European Network of Transmission System Operators for Electricity, cross-border interconnection projects require extensive dynamic stability studies to ensure seamless power exchange between neighboring nations. This profound commitment to ecological sustainability and interconnected grid management ensures continuous and robust demand for advanced modeling solutions across all European territories.

China Power System Simulation Market Analysis

China is anticipated to experience massive structural expansion in its network analytics segment over the next few years to orchestrate its growing ultra-high voltage direct current links and mega-scale solar corridors. Asia Pacific occupies a rapidly expanding position in the continental arena, fueled by explosive economic growth and the massive construction of new power generation facilities. According to the International Energy Agency, electricity demand in the region is projected to grow by over 4% annually, requiring the addition of hundreds of gigawatts of new generation capacity. Utility companies heavily rely on advanced load flow and short circuit simulation modules to plan the optimal routing of new high-voltage transmission lines. According to the Asian Development Bank, regional investments in smart grid infrastructure have surpassed 50 billion dollars recently to accommodate the rapid proliferation of electric vehicle charging stations. By leveraging these sophisticated digital tools, developing nations can ensure reliable power delivery while minimizing capital expenditure risks.

Brazil Power System Simulation Market Analysis

Brazil is expected to substantially broaden its grid modeling activities over the next few years to better manage hydrological variability and safeguard long-range transmission stability from remote generation basins to urban centers. Latin America holds a steadily growing position in the global landscape, supported by abundant renewable energy resources and the ongoing modernization of legacy electrical infrastructure. According to the Latin American Energy Organization, the regional power sector must attract over 100 billion dollars in private investments over the next decade to expand transmission capacity and prevent localized blackouts. Grid operators utilize advanced simulation platforms to model the complex interactions between long-distance transmission lines and variable renewable generation sources. According to the Inter-American Development Bank, extreme weather events and geological activity frequently disrupt power delivery, necessitating rigorous contingency planning and fault analysis. Consequently, the strategic imperative to modernize the grid and integrate diverse energy sources drives a sustained increase in the adoption of comprehensive simulation software across the continent.

Saudi Arabia Power System Simulation Market Analysis

Saudi Arabia is set to lead rapid digital integration within its regional network over the next few years by utilizing advanced steady-state and dynamic simulations to safely onboard landmark smart city installations and utility-scale solar arrays. The Middle East and Africa region maintains an emerging position in the international sector, characterized by massive utility-scale solar projects and the gradual digitalization of national power networks. According to the International Renewable Energy Agency, the Middle East and Africa region plans to add over 150 gigawatts of solar and wind capacity by the end of the decade, requiring extensive grid impact studies. Utility companies must utilize advanced simulation tools to manage the extreme temperature variations and high cooling loads that place unprecedented stress on local transformers and conductors. According to the African Development Bank, regional investments in cross-border power pools are accelerating to enhance energy security and facilitate electricity trade between neighboring nations. This strategic focus on renewable integration and regional interconnection guarantees a steady expansion of simulation technology adoption.

COMPETITIVE LANDSCAPE

The competition within the global sector is characterized by intense rivalry among multinational technology conglomerates and specialized engineering software developers worldwide today. Major corporations leverage their extensive financial resources and massive research budgets to dominate the enterprise software landscape globally. These industry leaders continuously invest in advanced algorithmic innovation to capture utility clients by introducing predictive analytics and digital twin capabilities. Meanwhile specialized regional players compete aggressively by emphasizing deep domain expertise and highly customized modeling solutions that resonate deeply with specific local grid architectures. The market also witnesses a surge in strategic mergers and acquisitions as companies seek to consolidate their technological capabilities and acquire emerging artificial intelligence startups. Furthermore cloud deployment models have become a critical competitive differentiator with firms transitioning from traditional on premise installations to scalable software as a service offerings to appeal to cost conscious buyers. Ultimately the competitive landscape demands continuous adaptation to the rapid integration of renewable energy sources ensuring that only the most technologically agile organizations maintain their long term profitability and client loyalty across all international utility markets today and tomorrow globally. This relentless pursuit guarantees exceptional industry evolution and continuous technological advancement across all global power networks.

KEY MARKET PLAYERS

Companies playing a prominent role in the global power system simulation market include

- Siemens AG

- General Electric

- ABB Ltd.

- Schneider Electric SE

- Eaton Corporation

- ETAP (Operation Technology, Inc.)

- PowerWorld Corporation

- Open Systems International, Inc.

- PSS® SINCAL

- NEPLAN AG

- Others

Top Players in the Market

Schneider Electric

Schneider Electric operates as a monumental force in the global energy management sector providing comprehensive simulation solutions for electrical grids. The corporation leverages its extensive digital portfolio to offer advanced power system modeling tools that ensure operational efficiency and sustainability. Recently the enterprise unveiled a new cloud based simulation platform designed to integrate seamlessly with smart grid infrastructure. This strategic innovation enables utility operators to perform real time dynamic analysis and optimize power distribution with unprecedented accuracy. By prioritizing digital transformation and ecological responsibility the organization successfully reinforces its industry leadership and drives substantial technological advancement across international markets today.

Siemens

Siemens functions as a premier technology conglomerate actively transforming the power system simulation landscape through deep domain expertise and innovative software development. The organization focuses heavily on creating highly accurate digital twin models that replicate the exact physical behavior of complex electrical networks. Recently the company completed the acquisition of a specialized engineering software firm to enhance its electromagnetic transient analysis capabilities. This massive strategic move significantly expands its computational power and allows clients to simulate complex fault scenarios with absolute precision. By prioritizing technological excellence the enterprise successfully attracts major utility clients and maintains a highly competitive edge globally.

ETAP

ETAP stands as a dominant entity in the electrical system analysis sector dedicating significant resources toward the development of enterprise grade simulation platforms. The corporation utilizes its proprietary analytical engines to provide comprehensive load flow short circuit and arc flash modeling solutions. In a recent strategic initiative the enterprise launched an advanced artificial intelligence module designed to automate grid contingency planning and predictive maintenance. This technological breakthrough enables facility managers to identify potential vulnerabilities before they cause catastrophic physical damage. Through continuous software innovation the company continues to solidify its formidable presence and accelerate enterprise adoption worldwide.

Top Strategies Used by Key Market Participants

Key players in the market employ several strategic approaches to reinforce their competitive standing and capture evolving technological demands. Product innovation remains central as companies develop advanced cloud based platforms and artificial intelligence modules tailored for real time grid monitoring and predictive maintenance. Strategic acquisitions are another common tactic with major firms purchasing specialized software developers to instantly acquire proprietary algorithms and expand their analytical capabilities. Geographic expansion particularly into emerging markets across Asia Pacific and Latin America allows access to new utility clients and diversified revenue streams. Furthermore strategic partnerships with hardware manufacturers and cloud service providers enable the seamless integration of simulation software with physical grid sensors and massive data repositories. Lastly continuous investment in research and development ensures that simulation models remain perfectly synchronized with the rapid proliferation of renewable energy sources and complex power electronics ensuring long term commercial viability.

MARKET SEGMENTATION

This research report on the global power system simulation market has been segmented and sub-segmented based on offering, module, end-user and region.

By Offering

- Hardware

- Software

- Services

By Module

- Short Circuit

- Load Flow

- Device Coordination Selectivity

- Arc Flash

- Others

By End-User

- Power Generation

- Transmission and Distribution

- Oil & Gas

- Manufacturing

- Metals and Mining

- Others

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Frequently Asked Questions

1. What is the CAGR of the Power System Simulation Market from 2024-2032?

The Power System Simulation Market is expected to grow with a CAGR of 6.4% during the forecast period.

2. Which is the dominating region for the Power System Simulation Market?

North America is currently dominating the power system simulation market by region.

3. Which End-User type is dominating the market for Power System Simulation Market?

The Power Generation segment is currently dominating the power system simulation market by end-user type.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com