Global Precision Medicine Market Size, Share, Trends & Growth Forecast Report - Segmented By Technology (Big Data Analytics, Bioinformatics, Gene Sequencing, Drug Discovery and Companion Diagnostics), Application (Oncology, CNS, Immunology, Respiratory and Others) and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa) – Industry Analysis From 2025 to 2033

Global Precision Medicine Market Size

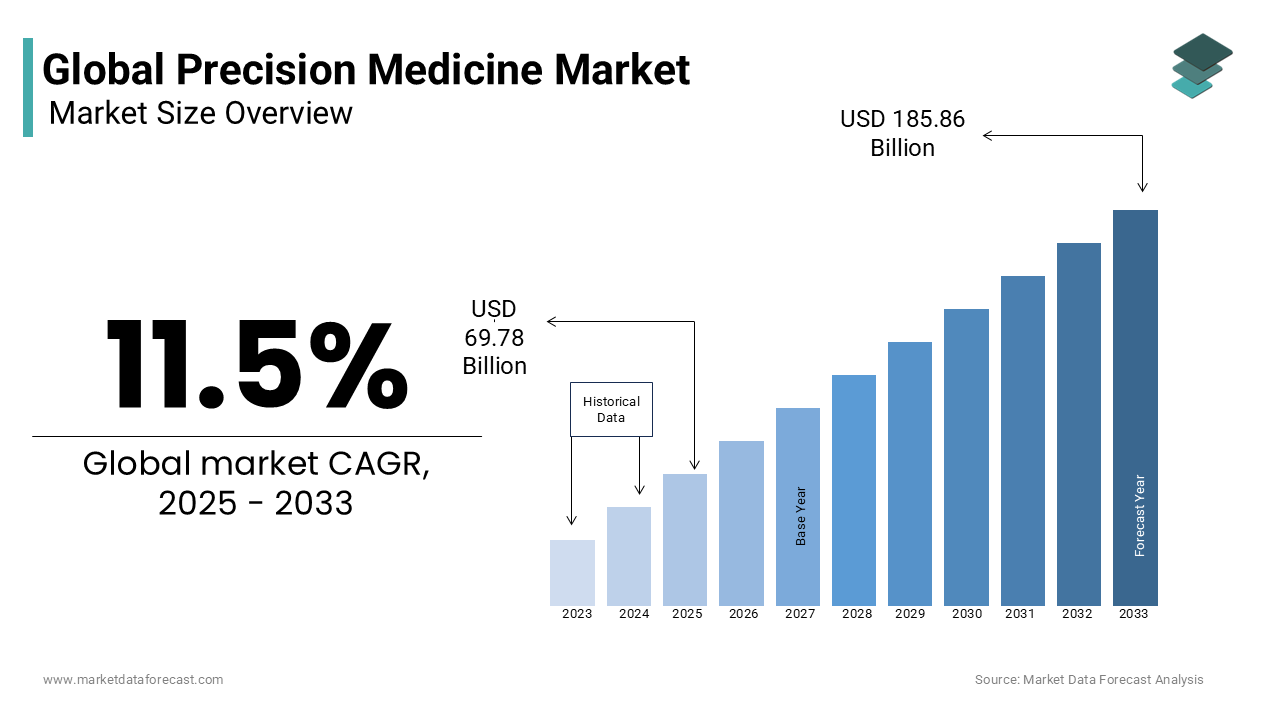

The global precision medicine market size was valued at USD 69.78 billion in 2024 and is anticipated to reach USD 77.80 billion in 2025 from USD 185.86 billion by 2033, growing at a CAGR of 11.5% during the forecast period from 2025 to 2033.

Precision medicine is a transformative approach to disease prevention and treatment that leverages individual variability in genetics, environment, and lifestyle to guide clinical decision-making. Rather than adopting a one-size-fits-all model, this paradigm utilizes molecular diagnostics, genomic sequencing, and bioinformatics to identify specific biomarkers that inform targeted therapies. The FDA provides a pharmacogenomic biomarker table listing drugs with genetic information in labeling. The National Institutes of Health’s All of Us Research Program has enrolled more than 600,000 participants to build a diverse genomic and health data repository, enhancing representation in precision health research. With increasing evidence of improved therapeutic outcomes and reduced adverse drug reactions, precision medicine is redefining standards of care across complex chronic diseases.

MARKET DRIVERS

Expansion of Genomic Sequencing Capabilities and Declining Costs of Testing

The rapid advancement and cost reduction in next-generation sequencing (NGS) have significantly accelerated the adoption of precision medicine in clinical settings. In 2003, the Human Genome Project completed the first full human genome sequence at a cost of approximately $2.7 billion; by 2023, the same process cost under $500, as per the National Human Genome Research Institute. This 99.98% reduction has democratized access to genomic data across research institutions and hospitals. Clinical labs in the U.S., Europe, and China now offer comprehensive NGS panels for cancer and rare diseases, enabling oncologists to match patients with targeted therapies based on tumor mutational profiles. The integration of sequencing into routine diagnostics, particularly in pediatric genetics and hereditary cancer screening, has solidified its role as a foundational tool in personalized care pathways.

Increasing Integration of Biomarker-Driven Therapies in Oncology

Oncology remains the most advanced therapeutic area for precision medicine, with biomarker-guided treatments transforming patient outcomes. Also, over 60% of new cancer drugs approved between 2018 and 2023 were designated as targeted therapies, requiring companion diagnostics for patient selection. For example, non-small cell lung cancer patients with EGFR mutations treated with osimertinib demonstrated a median progression-free survival of 18.9 months, compared to 10.2 months with chemotherapy, per the FLAURA trial. Additionally, the FDA has approved several companion diagnostic tests to support targeted therapies, reinforcing the clinical necessity of genomic testing. This alignment between diagnostics and therapeutics has created a self-reinforcing cycle of innovation, driving demand for comprehensive genomic analysis across global oncology networks.

MARKET RESTRAINTS

Expansion of Genomic Sequencing Capabilities and Declining Costs of Testing

The rapid advancement and cost reduction in next-generation sequencing (NGS) have significantly accelerated the adoption of precision medicine in clinical settings. In 2003, the Human Genome Project completed the first full human genome sequence at a cost of approximately $2.7 billion; by 2023, the same process cost under $500, as per the National Human Genome Research Institute. This 99.98% reduction has democratized access to genomic data across research institutions and hospitals. Clinical labs in the U.S., Europe, and China now offer comprehensive NGS panels for cancer and rare diseases, enabling oncologists to match patients with targeted therapies based on tumor mutational profiles. The integration of sequencing into routine diagnostics, particularly in pediatric genetics and hereditary cancer screening, has solidified its role as a foundational tool in personalized care pathways.

Increasing Integration of Biomarker-Driven Therapies in Oncology

Oncology remains the most advanced therapeutic area for precision medicine, with biomarker-guided treatments transforming patient outcomes. Also, over 60% of new cancer drugs approved between 2018 and 2023 were designated as targeted therapies, requiring companion diagnostics for patient selection. For example, non-small cell lung cancer patients with EGFR mutations treated with osimertinib demonstrated a median progression-free survival of 18.9 months, compared to 10.2 months with chemotherapy, per the FLAURA trial. Additionally, the FDA has approved several companion diagnostic tests to support targeted therapies, reinforcing the clinical necessity of genomic testing. This alignment between diagnostics and therapeutics has created a self-reinforcing cycle of innovation, driving demand for comprehensive genomic analysis across global oncology networks.

MARKET OPPORTUNITIES

Expansion of Genomic Sequencing Capabilities and Declining Costs of Testing

The rapid advancement and cost reduction in next-generation sequencing (NGS) have significantly accelerated the adoption of precision medicine in clinical settings. In 2003, the Human Genome Project completed the first full human genome sequence at a cost of approximately $2.7 billion; by 2023, the same process cost under $500, as per the National Human Genome Research Institute. This 99.98% reduction has democratized access to genomic data across research institutions and hospitals. Clinical labs in the U.S., Europe, and China now offer comprehensive NGS panels for cancer and rare diseases, enabling oncologists to match patients with targeted therapies based on tumor mutational profiles. The integration of sequencing into routine diagnostics, particularly in pediatric genetics and hereditary cancer screening, has solidified its role as a foundational tool in personalized care pathways.

Increasing Integration of Biomarker-Driven Therapies in Oncology

Oncology remains the most advanced therapeutic area for precision medicine, with biomarker-guided treatments transforming patient outcomes. Also, over 60% of new cancer drugs approved between 2018 and 2023 were designated as targeted therapies, requiring companion diagnostics for patient selection. For example, non-small cell lung cancer patients with EGFR mutations treated with osimertinib demonstrated a median progression-free survival of 18.9 months, compared to 10.2 months with chemotherapy, per the FLAURA trial. Additionally, the FDA has approved several companion diagnostic tests to support targeted therapies, reinforcing the clinical necessity of genomic testing. This alignment between diagnostics and therapeutics has created a self-reinforcing cycle of innovation, driving demand for comprehensive genomic analysis across global oncology networks.

MARKET CHALLENGES

Limited Access and Health Inequities in Genomic Testing Across Populations

Despite progress, significant disparities persist in access to precision medicine, particularly among racial, ethnic, and socioeconomically disadvantaged groups. Also, 78% of participants in large-scale genomic databases were of European ancestry, limiting the applicability of polygenic risk scores in non-European populations. In the U.S., Black and Hispanic patients are 30–50% less likely to receive germline genetic testing for hereditary cancers, as per the Journal of Clinical Oncology. In low- and middle-income countries, genomic testing remains largely inaccessible due to cost, lack of infrastructure, and trained personnel. These inequities compromise the validity and inclusivity of precision medicine, risking the entrenchment of health disparities rather than their mitigation, and undermining the ethical foundation of personalized care.

Regulatory Complexity and Evolving Approval Pathways for Companion Diagnostics

The co-development of drugs and companion diagnostics presents significant regulatory hurdles due to divergent approval timelines and jurisdiction-specific requirements. The FDA and EMA have different evidentiary standards for analytical and clinical validity, complicating global submissions. The In Vitro Diagnostic Regulation (IVDR) increased compliance requirements and led to a backlog of pending applications. Smaller diagnostic firms lack the resources to navigate these evolving frameworks, slowing innovation. Additionally, the classification of laboratory-developed tests (LDTs) remains contentious, with inconsistent oversight across countries, creating uncertainty for developers and healthcare providers alike.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Technology, Application, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis, Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leader Profiled | Pfizer, Roche, Covance, Novartis, Qiagen, Biocrates Life Sciences, Teva Pharmaceutical, Nanostring Technologies, Laboratory Corporation of America Holdings, Tepnel Pharma Services, Intomics, Ferrer InCode, Silicon Biosystems, Eagle Genomics, Medtronic & Quest Diagnostics. |

SEGMENTAL ANALYSIS

By Technology Insights

The gene sequencing was the largest technology in the precision medicine market and accounted for 34.8% of the total share in 2024. This dominance is primarily driven by the foundational role of sequencing in identifying disease-associated genetic variants and enabling targeted interventions. Also, a substantial number of human genomes or exomes were sequenced globally, a figure that has surged rapidly since 2020. The widespread adoption of next-generation sequencing (NGS) in clinical diagnostics, particularly in oncology and rare disease programs, has cemented its indispensability. Additionally, large-scale national initiatives have institutionalized sequencing in public health systems, reinforcing its integration into routine care and research.

The big data analytics segment is the fastest-growing segment and is projected to expand at a CAGR of 22.4% from 2025 to 2033. This surge is fueled by the exponential growth of multi-omics and electronic health record (EHR) data, which require advanced computational tools for meaningful interpretation. The FDA’s approval of machine learning-based clinical decision support systems has accelerated adoption in oncology and pharmacogenomics. Additionally, the All of Us Research Program in the U.S. is aggregating genomic, environmental, and lifestyle data from over 600,000 participants, creating a massive dataset that relies on big data infrastructure for analysis. These developments are transforming raw biological data into actionable clinical insights, making analytics the engine of scalable precision medicine.

By Application Insights

The oncology segment commanded the precision medicine market by capturing 60.5% of total application-based revenue in 2024. This lead position is due to the high mutational burden of cancers and the proven efficacy of biomarker-guided therapies. The FDA has approved many targeted cancer drugs, each linked to specific genetic alterations such as EGFR, ALK, BRAF, and BRCA. Additionally, tumor mutational burden (TMB) and microsatellite instability (MSI) testing now guide immunotherapy use across multiple cancer types. This deep integration of genomics into oncology care pathways, supported by clinical guidelines and payer coverage, solidifies oncology as the most mature and impactful domain of precision medicine.

The immunology segment is the fastest-growing application segment and is projected to grow at a CAGR of 18.3% from 2025 to 2033. This acceleration is driven by the rising understanding of genetic and immune system interactions in autoimmune and inflammatory diseases. Conditions such as rheumatoid arthritis, lupus, and inflammatory bowel disease (IBD) exhibit significant inter-patient variability in treatment response, prompting the use of biomarkers to guide therapy. The advent of single-cell RNA sequencing has enabled immune cell subtyping, revealing patient-specific immune signatures that inform biologic selection. With increasing investment in immune profiling and biologics development, immunology is emerging as a high-potential frontier for precision interventions.

REGIONAL ANALYSIS

North America led the global precision medicine market with a 45.6% share in 2024, with the United States serving as the epicenter of innovation and clinical integration. The U.S. leads in genomic research funding, with the National Institutes of Health allocating substantial amount annually to precision medicine initiatives, including the All of Us program. The country hosts the highest concentration of genomic testing laboratories and FDA-approved companion diagnostics, with several NGS-based tests cleared for clinical use as of 2023. Major cancer centers like MD Anderson and Dana-Farber have embedded genomic tumor boards into standard care, ensuring rapid translation of sequencing data into treatment decisions. Additionally, private insurers such as UnitedHealthcare and Medicare Advantage plans now cover comprehensive genomic profiling for advanced cancers. This confluence of research leadership, regulatory support, and payer adoption establishes North America as the most advanced and influential region in the global precision medicine landscape.

Europe is also a major player in the market, with the United Kingdom, Germany, and France leading in national genomics adoption. The UK’s National Health Service (NHS) operates one of the world’s most integrated genomic medicine services, having sequenced over 250,000 whole genomes through the 100,000 Genomes Project and its successor, Genomic Medicine Service. As per NHS England, all patients with rare diseases or certain cancers are now eligible for genomic testing within the public system. Germany has established 12 certified genomic medicine centers under its National Decade Against Cancer initiative, promoting standardized biomarker testing. France’s Plan France Médecine Génomique 2025 has invested €600 million to expand sequencing capacity and data infrastructure. The European Medicines Agency has harmonized regulatory pathways for companion diagnostics, accelerating market access. With strong public funding, ethical frameworks, and cross-border research collaboration, Europe maintains a robust and equitable approach to precision medicine deployment.

Asia Pacific is a lucrative region in the global market, with China and Japan emerging as strategic leaders in genomic infrastructure and clinical implementation. China has made precision medicine a national priority, investing over $9 billion in its Precision Medicine Initiative, aiming to sequence 10 million genomes by 2030, as per the Chinese Academy of Medical Sciences. BGI Genomics alone processed a large number of NGS tests in 2023, supporting oncology, prenatal, and rare disease diagnostics. Japan’s healthcare system mandates insurance coverage for cancer genomic profiling (NCD and NGS-GP tests), with over 60,000 patients tested annually, according to the National Cancer Center Japan. The country’s stringent quality control and centralized reporting system ensure high diagnostic accuracy. South Korea and Australia are also advancing with national biobanks and AI-driven interpretation platforms. With rising government support and rapid technological adoption, the Asia Pacific region is poised for accelerated growth in both research and clinical applications.

Latin America holds notable share of the market, with Brazil and Mexico representing the most developed ecosystems for precision medicine. Brazil has initiated the Genoma Brasil Project, aiming to sequence 15,000 genomes to capture the genetic diversity of its mixed-ancestry population, as per the Brazilian Ministry of Science, Technology, and Innovation. The country’s public health system, SUS, provides limited but growing access to BRCA and EGFR testing in major oncology centers. Mexico has seen increased private-sector investment in molecular diagnostics, with over 30 private labs offering NGS-based cancer panels in urban areas like Mexico City and Monterrey. However, access remains highly unequal. Despite financial and infrastructural constraints, academic collaborations with U.S. and European institutions are fostering capacity building and clinical trial participation.

The Middle East and Africa collectively represent a small share, yet exhibit emerging potential driven by strategic national investments. Saudi Arabia has launched the Saudi Human Genome Program, aiming to sequence 100,000 genomes to identify region-specific disease variants. The country has established genomic centers in Riyadh and Jeddah, integrating testing into major hospitals. The UAE has invested in the Centre for Arab Genomic Studies and launched the Dubai Genomics Initiative to build a population-specific reference database. In South Africa, the University of Cape Town leads in pharmacogenomic research, particularly in HIV and tuberculosis treatment optimization. With rising awareness and infrastructure development, the region is laying the foundation for future precision health integration, particularly in monogenic and infectious diseases.

COMPETITIVE LANDSCAPE

Competition in the precision medicine market is intensifying as global technology providers, diagnostic firms, and pharmaceutical companies vie for dominance across genomics, data analytics, and clinical integration. The sector is characterized by a convergence of capabilities, sequencing hardware, bioinformatics, companion diagnostics, and therapeutic development, requiring players to adopt end-to-end strategies. While Illumina and Thermo Fisher lead in sequencing infrastructure, Roche and Foundation Medicine dominate in clinically validated assays and oncology integration. Emerging biotech firms in China and India are challenging incumbents with lower-cost, region-specific panels tailored to local disease profiles. Differentiation is increasingly achieved through speed of analysis, regulatory approvals, data interpretation accuracy, and seamless integration into clinical workflows. Moreover, national genomics initiatives and data sovereignty laws are reshaping market access, favoring companies that align with public health priorities and ethical frameworks. This dynamic environment demands continuous innovation, cross-sector collaboration, and deep regulatory expertise to sustain leadership in a rapidly evolving field.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global precision medicine market include

- Pfizer

- Roche

- Covance

- Novartis

- Qiagen

- Biocrates Life Sciences

- Teva Pharmaceutical

- Nanostring Technologies

- Laboratory Corporation of America Holdings

- Tepnel Pharma Services

- Intomics

- Ferrer InCode

- Silicon Biosystems

- Eagle Genomics

- Medtronic & Quest Diagnostics.

Top Players in the Precision Medicine Market

Illumina, Inc. has solidified its leadership in the Asia Pacific precision medicine landscape through widespread adoption of its next-generation sequencing (NGS) platforms in clinical and research settings. The company established a regional genomics hub in Singapore in 2023 to support local laboratories with technical training, bioinformatics integration, and regulatory guidance. Illumina partnered with Australia’s Garvan Institute to enhance whole-genome sequencing capabilities for rare disease diagnosis and launched a collaborative initiative with Japan’s RIKEN Center to expand cancer genomics research. Additionally, Illumina engaged with China’s National Center for Clinical Laboratories to align its assays with local validation standards. These efforts reflect a strategic focus on regulatory alignment, capacity building, and localized support to drive the integration of genomic testing across diverse healthcare systems in the region.

Thermo Fisher Scientific has expanded its footprint in the Asia Pacific precision medicine market by advancing its portfolio of targeted sequencing panels and companion diagnostics. The company’s Oncomine suite of NGS assays is widely used in oncology centers across South Korea, Australia, and Taiwan for tumor profiling and therapy selection. The company also launched a localized version of its Ion Torrent Genexus System in Japan, enabling fully automated, rapid sequencing with minimal hands-on time. In India, Thermo Fisher supported the rollout of pharmacogenomic testing in tertiary hospitals through partnerships with Apollo Hospitals and MedGenome. By combining platform automation, regulatory submissions, and clinical validation support, Thermo Fisher has positioned itself as a key enabler of scalable, precision-driven diagnostics across the region.

Roche Diagnostics has deepened its engagement in the Asia Pacific precision medicine ecosystem through its integrated diagnostics-therapeutics model and regulatory leadership. The company’s cobas BRCA and cobas EGFR tests are approved and reimbursed in multiple countries, including Japan, Australia, and South Korea, facilitating access to targeted therapies like olaparib and osimertinib. The company also collaborated with the National University Hospital in Singapore to implement comprehensive genomic profiling in routine oncology care. Roche further strengthened its digital infrastructure by integrating its NAVIFY™ Decision Support platform with hospital EHRs in Thailand and Malaysia. These initiatives underscore a strategy centered on clinical utility, regulatory excellence, and data integration, ensuring that diagnostic insights translate directly into actionable treatment pathways across diverse healthcare environments.

Top Strategies Used by Key Market Participants

Key players in the precision medicine market are deploying integrated diagnostics-therapeutics models, regional regulatory alignment, and AI-powered data interpretation to strengthen their competitive edge. Companies are co-developing companion diagnostics alongside targeted therapies to ensure synchronized market entry and clinical adoption. Strategic partnerships with national health systems and academic institutions are being leveraged to validate tests in local populations and support reimbursement dossiers. Investment in automated sequencing platforms and cloud-based bioinformatics enables rapid, scalable genomic analysis even in resource-constrained settings. Firms are also expanding into multi-omics integration, combining genomics, transcriptomics, and proteomics, to enhance diagnostic accuracy. Additionally, digital health platforms that link genomic results with electronic health records are improving clinical decision-making and longitudinal care. These strategies collectively enhance reliability, accessibility, and real-world impact, positioning leaders at the forefront of personalized healthcare transformation

RECENT MARKET HAPPENINGS

- In January 2023, Illumina launched a genomics training hub in Singapore, providing technical and bioinformatics support to laboratories across Southeast Asia to strengthen its market presence.

- In August 2022, Thermo Fisher Scientific collaborated with Singapore’s National Cancer Centre to validate its Oncomine liquid biopsy panels for lung cancer, enhancing clinical credibility in the Asia Pacific region.

- In May 2024, Roche Diagnostics introduced the AVENIO ctDNA surveillance kit in Hong Kong, expanding its minimal residual disease monitoring portfolio in oncology.

- In March 2023, Illumina partnered with Japan’s RIKEN Center to advance cancer genomics research using its NovaSeq 6000 platform, reinforcing its scientific leadership.

- In November 2023, Thermo Fisher launched a localized version of the Ion Torrent Genexus System in Japan, enabling fully automated NGS workflows for faster clinical turnaround.

MARKET SEGMENTATION

This global precision medicine market report has been segmented and sub-segmented based on the technology, application, and region.

By Technology

- Big Data Analytics

- Bioinformatics

- Gene Sequencing

- Drug Discovery

- Companion Diagnostics

By Application

- Oncology

- CNS

- Immunology

- Respiratory

- Others

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

What is the Europe Precision Medicine Market?

The Europe Precision Medicine Market focuses on tailored healthcare approaches that use genetic, environmental, and lifestyle data to customize medical treatments and preventive strategies for individual patients.

What are the main drivers of the Europe Precision Medicine Market?

Key drivers include growing prevalence of chronic diseases, rapid genomic research advancements, integration of AI in healthcare, and government initiatives promoting personalized medicine.

What are the major restraints in the Europe Precision Medicine Market?

Challenges include high cost of genetic testing, data privacy concerns, limited infrastructure in developing regions, and complex regulatory frameworks.

What are the key components of precision medicine?

Core components include genomic sequencing, molecular diagnostics, big data analytics, targeted therapies, and personalized treatment plans.

Which application segment dominates the Europe Precision Medicine Market?

The oncology segment dominates the market due to the growing use of genomic profiling for cancer diagnosis, prognosis, and targeted drug therapies.

Which technologies are driving the precision medicine industry?

Technologies include next-generation sequencing (NGS), CRISPR gene editing, bioinformatics, liquid biopsy diagnostics, and cloud-based genomic databases.

Which countries lead the Europe Precision Medicine Market?

Germany, the United Kingdom, France, Switzerland, and the Netherlands lead the market due to advanced healthcare systems, genomic research centers, and government funding.

How is big data influencing the precision medicine landscape?

Big data analytics help integrate clinical, genomic, and lifestyle information to create accurate predictive models for personalized treatment.

Who are the leading companies in the Europe Precision Medicine Market?

Key players include F. Hoffmann-La Roche AG, Illumina, Inc., Thermo Fisher Scientific Inc., Qiagen N.V., Novartis AG, AstraZeneca plc, Agilent Technologies, Inc., IBM Corporation, Pfizer Inc., and Bayer AG.

What is the future outlook for the Europe Precision Medicine Market?

The market is expected to expand significantly as genomic data accessibility, AI-powered analytics, and personalized drug discovery revolutionize healthcare delivery across the region.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com