Global Rice Market Size, Share, Trends, & Growth Forecast Report Segmented By Product (Long-grain, Medium-grain, Short-grain), Distribution Channel, and Region (Latin America, North America, Asia Pacific, Europe, Middle East and Africa), Industry Analysis from 2026 to 2034

Global Rice Market Report Summary

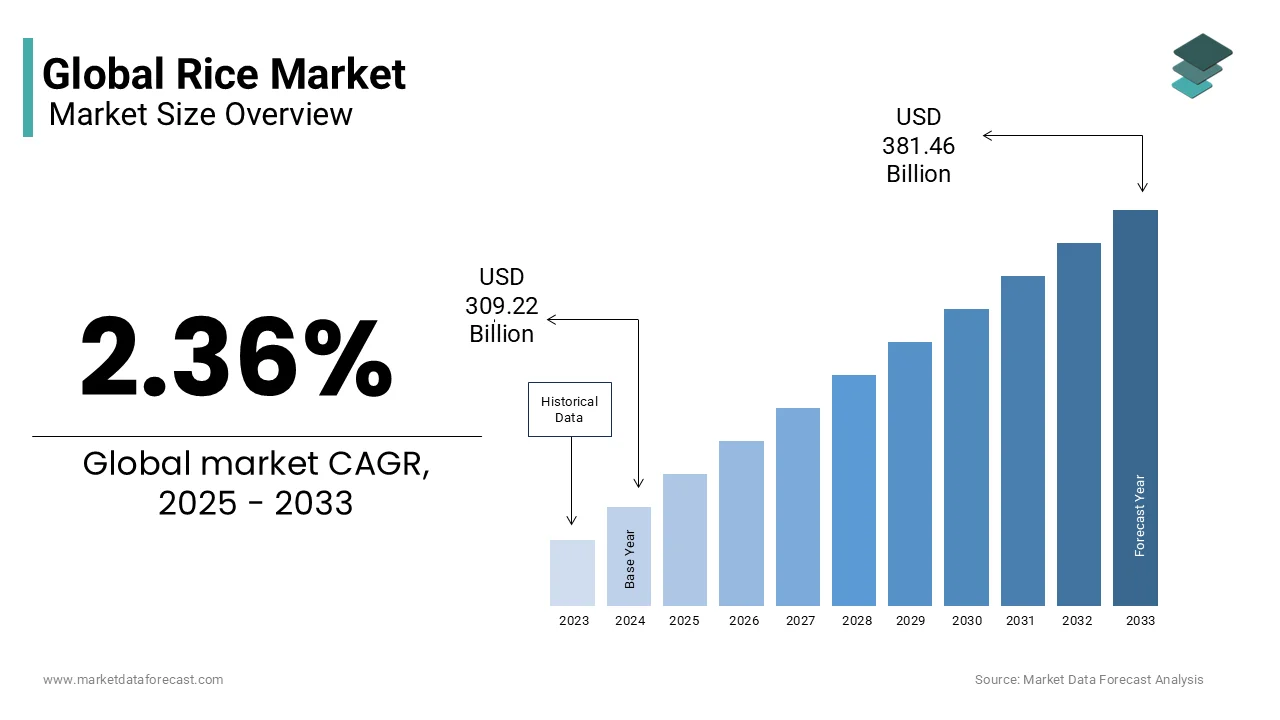

The global rice market was valued at USD 316.51 billion in 2025 and is estimated to reach USD 323.98 billion in 2026, and is projected to reach USD 390.45 billion by 2034, growing at a CAGR of 2.36% during the forecast period. The growth of the global rice market is driven by its status as a staple food for a large portion of the world’s population, particularly across Asia and Africa. Increasing population, rising food demand, and expanding consumption in emerging economies are key factors supporting market growth. In addition, government support for rice production, advancements in agricultural practices, and the growing demand for packaged and branded rice products are further contributing to the steady expansion of the global rice market.

Key Market Trends

- Increasing global population and food security concerns driving consistent demand for rice as a staple food.

- Rising demand for premium and branded rice varieties such as basmati and jasmine in international markets.

- Growing adoption of modern farming techniques improving yield and production efficiency.

- Expansion of packaged rice products in retail channels enhancing product accessibility and quality assurance.

- Increasing exports from major producing countries supporting global trade dynamics.

Segmental Insights

- Based on product type, the long grain rice segment accounted for 52.4% of the global rice market share in 2025. The dominance of this segment is attributed to its widespread consumption, versatility in cooking, and strong demand in both domestic and international markets.

- Based on distribution channel, the offline segment held a substantial share of the global rice market in 2025. The strong presence of supermarkets, hypermarkets, and traditional retail outlets continues to drive sales through offline channels.

Regional Insights

- The global rice market is heavily concentrated in the Asia Pacific region, which serves as both the largest producer and consumer of rice.

- Asia Pacific dominated the global rice market due to favorable climatic conditions, extensive cultivation practices, and high consumption levels across countries such as India, China, and Southeast Asian nations. The region’s strong agricultural base and government support for rice production are key factors driving its leadership position.

- Other regions are also witnessing steady demand for rice driven by increasing population, changing dietary patterns, and growing imports to meet domestic consumption needs.

Competitive Landscape

The global rice market is characterized by the presence of several regional and international players focusing on product quality, branding, and supply chain efficiency. Companies are investing in modern processing technologies, packaging innovations, and export expansion strategies to strengthen their market position. Strategic partnerships and distribution network expansion are also helping market players increase their global footprint. Key companies operating in the global rice market include Kohinoor Foods Ltd., Adani Wilmar Limited, LT Foods, KRBL Limited, Aeroplane Rice Ltd., Sridhar Agro Product Pvt. Ltd., Gautam General Trading LLC, Sri Sainath Industry Pvt. Ltd., Shriram Food Industry Pvt. Ltd., and Aashirvad International.

Global Rice Market Size

The global rice market size was valued at USD 316.51 billion in 2025 and is expected to reach USD 390.45 billion by 2034 from USD 323.98 billion in 2026. The market is projected to grow at a CAGR of 2.36%.

The rice market encompasses the production, trade, and consumption of Oryza sativa and Oryza glaberrima, staple cereals that serve as a primary caloric source for over 3.5 billion people globally, particularly across Asia, Sub-Saharan Africa, and Latin America. As per the Food and Agriculture Organization of the United Nations, rice provides approximately 20% of the world’s dietary energy supply, surpassing even wheat and maize in low-income food-deficit countries. The crop is cultivated in diverse agro-ecological zones, from flooded paddy fields to rainfed uplands, with smallholders dominate rice farming, especially in Asia. Rice exhibits extensive genetic diversity with tens of thousands of documented varieties. With rising urbanization and shifting dietary patterns, demand continues to evolve, encompassing specialty segments such as aromatic, organic, and fortified rice, further diversifying the global market landscape.

MARKET DRIVERS

Rapid Urbanization and Expanding Middle-Class Consumption in Asia

Urban population growth in Asia is reshaping rice consumption patterns, driving demand for processed, packaged, and premium-grade rice. Also, Asia is undergoing significant urbanization, with an increasing proportion of its population moving to cities. This demographic shift correlates with increased reliance on retail-purchased rice over traditional bulk or home-stored supplies. For instance, India has seen consistent growth in packaged rice demand, driven by convenience-oriented urban consumers. Urban households also show growing preference for value-added rice types, including parboiled, fortified, and ready-to-cook variants, reinforcing market expansion beyond basic staple supply.

Government Support and Food Security Policies in Key Producing Nations

National food security strategies in major rice-producing countries significantly bolster market stability and production incentives. In China, the Ministry of Agriculture and Rural Affairs maintains a minimum grain purchase price policy, ensuring farmers receive guaranteed returns, which has sustained rice cultivation on over 30 million hectares annually. This policy contributed to a year-on-year increase in rice output despite climatic challenges. Vietnam has launched long-term rice strategies that emphasize modernization, high-value varieties, and export competitiveness. Such interventions not only stabilize domestic supply but also enhance export competitiveness. These institutional frameworks reduce production volatility and ensure consistent market availability, reinforcing rice as a strategically managed commodity in national economies.

MARKET RESTRAINTS

Water Scarcity and Declining Irrigation Availability in Major Rice-Growing Regions

Rice cultivation is highly water-intensive, requiring significant liters to produce one kilogram, making it increasingly vulnerable to hydrological stress. According to the World Resources Institute, 17 countries, home to one-quarter of the global population, are facing “extremely high” baseline water stress, including major rice producers like India, Pakistan, and Iran. Groundwater depletion in India’s major rice belts is severe, with levels falling steadily over the past two decades. Long-term projections suggest water stress will negatively affect rice yields across South Asia. Additionally, climate-induced droughts in Southeast Asia have disrupted planting cycles, as noted by the Thai Department of Agriculture. These hydrological constraints are compelling a reevaluation of traditional paddy farming methods.

Post-Harvest Losses Due to Inadequate Storage and Processing Infrastructure

A significant portion of rice production is lost between harvest and consumption due to inefficient handling and storage systems. According to the Food and Agriculture Organization, post-harvest losses in rice range from 10% to 18% in developing countries, with India incurs substantial post-harvest rice losses annually, amounting to millions of tons. Post-harvest losses in Sub-Saharan Africa are among the highest globally, particularly in humid regions with limited storage technology. The International Rice Research Institute shows that traditional sun-drying methods often lead to grain cracking and contamination, reducing market value. These inefficiencies not only diminish supply but also compromise food safety and farmer incomes, constraining market efficiency and discouraging investment in quality improvement and value addition.

MARKET OPPORTUNITIES

Adoption of Climate-Resilient and High-Yielding Rice Varieties

The development and dissemination of stress-tolerant rice strains present a transformative opportunity for yield enhancement and environmental sustainability. Research organizations such as IRRI have developed hundreds of improved rice varieties, many of which are in wide use across South Asia. Saline- and flood-tolerant varieties in Bangladesh have demonstrated clear yield improvements in affected coastal zones. Similarly, in Nigeria, the adoption of NERICA (New Rice for Africa) varieties has boosted productivity by 30–50% compared to traditional landraces, as per the Africa Rice Center. With climate change intensifying, the scalability of such innovations offers a pathway to stabilize production, reduce import dependency, and enhance food security in vulnerable regions.

Growth of Specialty and Fortified Rice Segments in Urban and Export Markets

Consumer demand for nutritionally enhanced and premium rice varieties is creating high-margin market niches. Fortified rice, enriched with iron, zinc, and vitamins, is being promoted by global health agencies to combat micronutrient deficiencies. According to the World Health Organization, over 40 countries have implemented national programs to distribute fortified rice. Also, India is one of the largest adopters, with school meal programs distributing fortified rice to millions of children. In the export sector, aromatic varieties such as Basmati and Jasmine command price premiums; Aromatic varieties like Jasmine and Basmati consistently command higher export prices than regular white rice. Consumer preference for organic rice has grown steadily in North America in recent years, reflecting broader health and sustainability trends. These specialty segments offer producers opportunities to diversify income and align with global health and wellness trends.

MARKET CHALLENGES

Methane Emissions from Flooded Paddy Fields and Environmental Regulations

Traditional rice cultivation is a major source of anthropogenic methane, a potent greenhouse gas. According to the Intergovernmental Panel on Climate Change, rice paddies contribute approximately 8% of global agricultural methane emissions. Continuously flooded paddies emit measurable amounts of methane per hectare each growing season. In response, the European Union’s Green Deal and California’s Short-Lived Climate Pollutant Reduction Strategy are imposing indirect pressure on rice exporters to adopt low-emission practices. The International Rice Research Institute has demonstrated that alternate wetting and drying (AWD) can reduce methane emissions while conserving water. However, adoption remains limited due to labor requirements and yield variability concerns, creating a tension between environmental compliance and farmer livelihoods that complicates sustainable intensification.

Trade Disruptions Due to Export Restrictions and Geopolitical Tensions

Rice trade is increasingly vulnerable to unilateral export bans and geopolitical instability, undermining global supply reliability. Several major rice-exporting countries, including India, Vietnam, and Cambodia, imposed temporary export restrictions to safeguard domestic supplies during price spikes or production shortfalls. In 2023, India, the world’s largest rice exporter, restricted non-Basmati white rice shipments, affecting over 30 importing nations, as per the United Nations Conference on Trade and Development. Also, export restrictions contribute directly to higher global rice price volatility. These disruptions disproportionately impact import-dependent countries in Africa and the Middle East, where rice constitutes a dietary staple, and erode trust in long-term trade contracts, challenging market predictability and strategic planning.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 2.36% |

| Segments Covered | By Product, Distribution Channel, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Kohinoor Foods Ltd. Adani Wilmar Limited LT Foods KRBL Limited Aeroplane Rice Ltd. Sridhar Agro Product P Ltd Gautam General Trading LLC Sri Sainath Industry Pvt. Ltd Shriram Food Industry Pvt. Ltd. Aashirvad International, and others |

SEGMENTAL ANALYSIS

By Product Insights

The long-grain rice segment commanded an estimated 52.4% share of the global rice market by volume in 2025. Its dominance is due to widespread culinary preference across South Asia, the Americas, and the Middle East, where fluffy, non-sticky grains are favored in daily meals and traditional dishes. Also, India and Pakistan are the main consumers and exporters of Basmati rice, where long-grain aromatic varieties form an important part of both domestic diets and export earnings. The U.S. exports millions of tons of long-grain rice each year, with West Africa and the Middle East as major destinations. Additionally, milling yields for long-grain rice are generally higher than those for short-grain types, making it more cost-effective for processors, further reinforcing its market leadership.

The short-grain rice segment is expanding at a CAGR of 6.8% from 2026 to 2034. It is due to rising demand in processed food applications and health-oriented diets. Short-grain rice, particularly glutinous or sticky varieties, is essential in ready-to-eat meals, baby food, rice-based snacks, and fermented products like rice wine and yogurt alternatives. The use of short-grain rice in gluten-free and specialty processed foods has risen significantly in recent years due to its binding and textural properties. In Japan, as per the Ministry of Agriculture, Forestry and Fisheries, Koshihikari, a premium short-grain variety, now accounts for over 40% of domestic rice sales despite higher prices, reflecting consumer preference for quality and authenticity. Additionally, the growing popularity of sushi and Asian cuisine in Western markets has amplified demand for high-starch, cohesive rice types, accelerating global market penetration.

By Distribution Channel Insights

The offline channel holds substantial share of the global rice market in 2025. Traditional retail outlets, wet markets, and neighborhood grocers remain the primary access points, especially in rural and low-income regions where digital infrastructure and e-commerce penetration are limited. Informal and traditional markets handle the bulk of rice sales in Sub-Saharan Africa, with minimal cold chain or digital tracking. Also, small neighborhood stores remain the backbone of rice distribution in India, especially in smaller cities and rural areas. They continue to dominate packaged rice sales despite the growth of supermarkets and online platforms. Moreover, in Southeast Asia, floating markets and local rice mills continue to supply fresh, unbranded rice directly to consumers, preserving cultural purchasing habits. This entrenched retail ecosystem, supported by cash-based transactions and trusted vendor relationships, sustains offline dominance despite digital advancements.

The online rice distribution segment is growing at a CAGR of 13.4% during the forecast period. It is driven by digital adoption, urbanization, and demand for convenience in major consumer markets. Also, e-commerce sales of food staples in Asia Pacific grew in recent years, with rice among the top five purchased items on platforms like Amazon India, Lazada, and Alibaba. Likewise, online platforms in China, including JD.com, report substantial rice sales, with premium and organic categories making up a significant share. Further, subscription-based and app-driven grocery platforms in the U.S. are increasing rice sales through bundled promotions and personalized recommendations. Additionally, digital traceability and QR-coded origin verification are enhancing consumer trust in online purchases, accelerating the shift from physical to digital retail in both developed and emerging economies.

REGIONAL ANALYSIS

Asia Pacific Rice Market Insights

Asia Pacific dominated the global rice market with a substantial share, serving as both the largest producer and consumer. China and India alone account for over 50% of global rice production, supported by vast cultivation areas, as per the Food and Agriculture Organization. The region’s consumption is deeply embedded in cultural and dietary norms, with per capita intake exceeding 100 kilograms per year in countries like Bangladesh and Vietnam, according to the International Rice Research Institute. Government procurement, buffer stock policies, and minimum support prices in India and Thailand ensure production stability. Besides, rising demand for value-added rice, such as organic, fortified, and aromatic varieties, is reshaping supply chains. With rapid urbanization and modern retail expansion, the region is also leading the transition toward branded, packaged, and traceable rice, reinforcing its central role in shaping global market trends.

North America Rice Market Insights

North America is a niche but evolving consumer in the global rice market and is characterized by stable consumption and a shift toward specialty and health-focused products. The United States is both a significant producer and exporter of long-grain rice, with Arkansas, California, and Missouri contributing over 90% of domestic output, as per the U.S. Department of Agriculture. Per capita rice consumption in the U.S. has grown steadily since 2000, driven by shifting demographics and the popularity of diverse cuisines. Also, growing proportion of consumers in Canada and the U.S. prefer rice products marketed as organic, gluten-free, or whole grain, reflecting health-driven purchasing. The rise of plant-based diets and ready-to-cook meals has further boosted demand for parboiled and instant rice. While volume remains modest, the region commands premium pricing and leads in innovation, particularly in fortified and functional rice products.

Europe Rice Market Insights

Europe is a stable player the global rice market, with consumption patterns shaped by culinary diversity and regulatory emphasis on food safety. Italy, Spain, and Greece are major producers of medium-grain rice used in risotto, paella, and pilaf, with Southern European countries, especially Italy, Spain, and Greece, maintain significant rice cultivation areas dedicated mainly to medium-grain varieties. Moreover, packaged and branded rice dominates retail sales across the EU, supported by consumer trust in traceability and strict food safety regulations. Like in Europe, demand for organic rice grew rapidly in recent years, particularly in Germany and Scandinavia. Besides, the European Green Deal is encouraging sustainable rice production through incentives for low-methane farming methods. While domestic production meets only 60% of demand, the region’s focus on quality, traceability, and environmental standards positions it as a high-value import market.

Latin America Rice Market Insights

Latin America holds a significant share of the global rice market, with Brazil, Colombia, and Argentina leading both production and regional trade. Brazil is the largest rice producer in Latin America, with millions of hectares under cultivation and significant annual output. Rice is a dietary staple in countries like Peru and Ecuador, where per capita consumption exceeds 45 kilograms per year, according to the Economic Commission for Latin America and the Caribbean. However, yields remain below global averages due to limited mechanization and reliance on rainfed systems. Adoption of improved farming techniques and irrigation systems has gradually enhanced productivity in parts of Latin America. With rising urbanization and integration into global supply chains, Latin America is emerging as a competitive exporter of specialty and organic rice to North American and European markets.

Middle East & Africa Rice Market Insights

The Middle East and Africa collectively represent small share of the global rice market but are among the fastest-growing demand centers. Gulf Cooperation Council countries import over 90% of their rice, with Saudi Arabia and the UAE sourcing primarily from India, Thailand, and Vietnam, as per the Gulf Cooperation Council Secretariat. Rice consumption in Sub-Saharan Africa has grown sharply over the past two decades, displacing some traditional staples. Nigeria, the largest consumer in Africa, imports over 3 million tons annually despite efforts to boost domestic production. The African Development Bank’s “Rice Strategy for Africa” aims to reduce import dependency by promoting high-yielding varieties and mechanized farming. With rapid urbanization and youth-driven dietary shifts, rice is displacing traditional staples, making the region a critical growth frontier for global exporters and agri-investors.

COMPETITIVE LANDSCAPE

The competitive landscape of the rice market is shaped by a mix of state-backed exporters, private agribusinesses, and regional millers vying for dominance in quality, reliability, and innovation. While national policies and subsidies influence large-scale trade dynamics, private players are differentiating through branding, packaging, and value-added offerings such as fortified and organic rice. In Asia Pacific, competition is intensifying as companies invest in traceability, sustainability, and digital distribution to capture urban consumers. Smaller regional producers face pressure from economies of scale and export logistics managed by larger conglomerates. The absence of global standardization in grading and pricing allows for niche differentiation, but also creates fragmentation. Long-term competitiveness increasingly depends on technological integration, environmental stewardship, and the ability to align with evolving dietary and regulatory trends across both domestic and international markets.

KEY MARKET PLAYERS

Some of the key players in the rice market are

-

Kohinoor Foods Ltd.

-

Adani Wilmar Limited

-

LT Foods

-

KRBL Limited

-

Aeroplane Rice Ltd.

-

Sridhar Agro Product Pvt. Ltd.

-

Gautam General Trading LLC

-

Sri Sainath Industry Pvt. Ltd.

-

Shriram Food Industry Pvt. Ltd.

-

Aashirvad International

TOP PLAYERS IN THE MARKET

- LT Foods, headquartered in India, is a leading integrated rice company renowned for its flagship brand “Daawat,” which has become synonymous with premium basmati rice across global markets. In the Asia Pacific region, the company has strengthened its presence by expanding milling and packaging facilities in Haryana and Uttar Pradesh to meet rising domestic and export demand. In 2023, LT Foods launched Daawat Smart Cook, a low-glycemic rice variant, targeting health-conscious consumers in urban India, Singapore, and Australia. The company also introduced blockchain-based traceability for its export-grade basmati, allowing consumers to verify farm origin and processing history via QR codes. Additionally, LT Foods partnered with e-commerce platforms like Flipkart and Lazada to enhance digital reach, while investing in sustainable farming initiatives through direct farmer procurement programs in Punjab, reinforcing supply chain transparency and quality control.

- As a state-owned enterprise and one of Vietnam’s largest rice exporters, Vinafood plays a pivotal role in shaping the country’s position as a top-tier global rice supplier. The company manages a vast network of procurement centers, silos, and processing units across the Mekong Delta, enabling efficient aggregation and export of high-quality Jasmine and OM series rice. In 2022, Vinafood collaborated with the Ministry of Agriculture and Rural Development to pilot climate-smart rice farming techniques across 50,000 hectares, improving yield stability amid salinity intrusion and drought. The company has also prioritized export diversification, securing new contracts with importers in the Philippines, South Africa, and the Middle East. By modernizing storage infrastructure and adopting digital auction platforms for domestic sales, Vinafood is enhancing market responsiveness and reinforcing Vietnam’s reputation for reliable, competitively priced rice in the Asia Pacific trade ecosystem.

- Charoen Pokphand Foods, a subsidiary of Thailand’s CP Group, operates as a vertically integrated agribusiness leader with a strong footprint in rice production, processing, and distribution across Southeast Asia. The company leverages its extensive feed and animal husbandry network to promote integrated farming models, supplying high-yield rice seeds and technical support to contracted farmers in Thailand and Cambodia. In 2023, CPF launched a premium organic rice line under the “CP Best” brand, certified by the Thai Organic Agriculture Association, targeting upscale retailers in Japan and South Korea. The company also invested in automated sorting and vacuum-sealing technology to extend shelf life and maintain grain integrity. Through its retail arm, CP All, which operates over 13,000 7-Eleven stores in Thailand, CPF ensures direct market access for its packaged rice, creating a seamless farm-to-consumer supply chain that enhances brand visibility and consumer trust.

TOP STRATEGIES USED BY KEY MARKET PLAYERS

Key players in the rice market are deploying a combination of vertical integration, product differentiation, and digital transformation to strengthen their competitive positioning. Companies are investing in end-to-end supply chains—from seed development and contract farming to modern milling and traceable packaging—to ensure quality consistency and reduce post-harvest losses. Strategic branding is being leveraged to promote premium segments such as organic, fortified, and aromatic rice, commanding higher margins in urban and export markets. Firms are increasingly adopting blockchain and QR-code traceability to build consumer trust and comply with international food safety standards. Expansion into e-commerce and direct-to-consumer models is accelerating, particularly in Asia, where digital grocery adoption is rising. Additionally, partnerships with governments and agricultural institutes to promote climate-resilient farming are enhancing long-term supply security and sustainability credentials.

MARKET SEGMENTATION

This research report on the global rice market has been segmented and sub-segmented based on product, distribution channel, and region.

By Product

- Long-grain

- Medium-grain

- Short-grain

By Distribution Channel

- Offline

- Online

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. What is the Rice Market?

The rice market covers global production, trade, and consumption of rice as a staple food crop.

2. What drives growth in the Rice Market?

Population growth, rising food demand, and government support for agriculture drive market expansion.

3. Which are the major types in the Rice Market?

Key types include basmati rice, non-basmati rice, brown rice, and jasmine rice.

4. Which regions dominate the Rice Market?

Asia-Pacific leads due to high production in India, China, and Thailand, followed by the Middle East and Africa.

5. Who are the leading players in the Rice Market?

Key players include KRBL Limited, LT Foods, Adani Wilmar, Kohinoor Foods Ltd., and Aeroplane Rice Ltd.

6. What are the key applications of rice globally?

Rice is used for direct consumption, processed foods, beverages, animal feed, and industrial uses.

7. What are the current trends in the Rice Market?

Growing demand for organic, fortified, and ready-to-cook rice products are major trends.

8. What challenges does the Rice Market face?

Challenges include price volatility, storage issues, and trade restrictions in major producing countries.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com