Global Smart Thermostat Market Size, Share, Trends, & Growth Forecast Report, Segmented By Technology (Wi-Fi, Bluetooth, Zigbee and Others), Application (Air Conditioning, Heating, and Ventilation), End User (Residential, Commercial, Industrial and Others) & Region, Industry Forecast From 2026 to 2034

Global Smart Thermostat Market Size

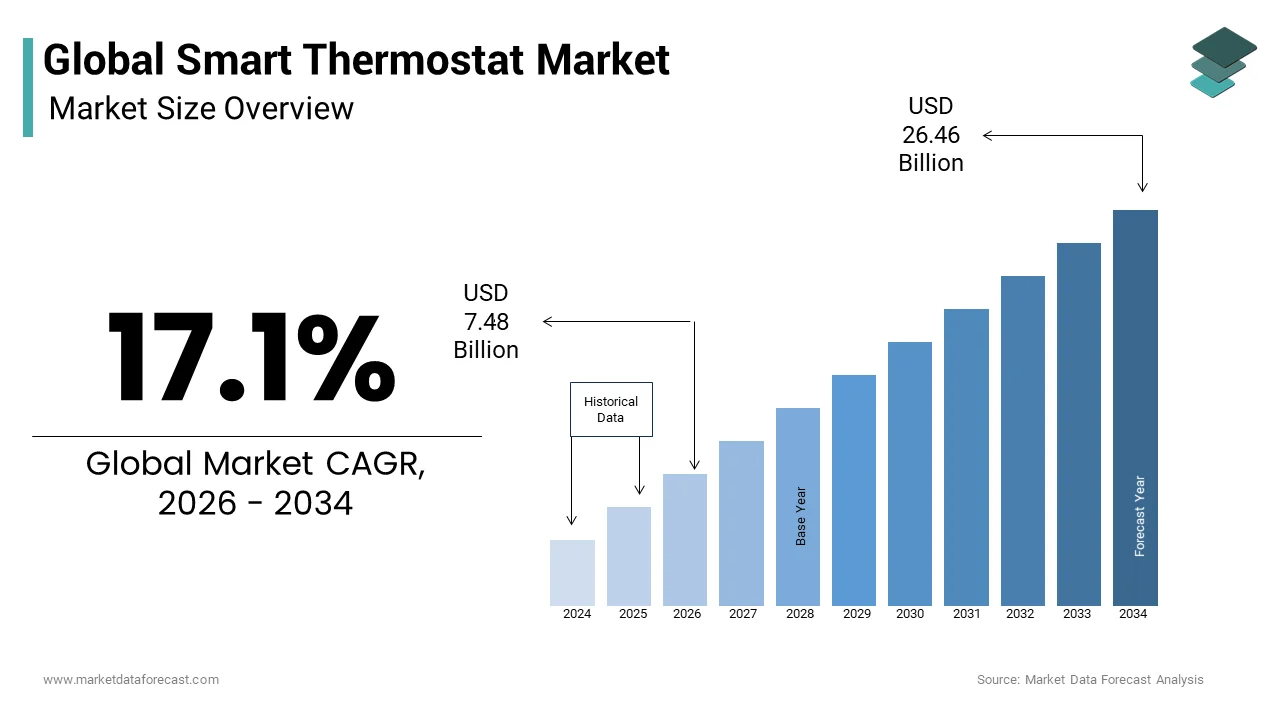

The global smart thermostat market size was valued at USD 6.39 billion in 2025 and is anticipated to reach USD 7.48 billion in 2026 from USD 26.46 billion by 2034, growing at a CAGR of 17.1% from 2026 to 2034.

Current Introduction Of The Smart Thermostat Market

A smart thermostat is a Wi-Fi-enabled climate control device that connects to the internet, allowing you to monitor and adjust your home's heating, ventilation, and air conditioning (HVAC) system remotely via a smartphone app or voice commands. Unlike conventional programmable thermostats, these devices adapt to occupancy patterns, weather conditions, and user preferences, offering remote access via smartphones and integration with broader smart home ecosystems. The market is shaped by global decarbonization imperatives, rising energy costs, and evolving building codes that increasingly mandate intelligent environmental controls. According to the International Energy Agency, heating requirements in the residential sector constitute a massive portion of total energy demand in buildings, making it a primary target for energy efficiency initiatives. As per the United Nations Environment Programme, over 130 countries now include building energy efficiency in their national climate strategies, many referencing smart controls as key enablers. Furthermore, the International Telecommunication Union shows massive growth in Internet of Things (IoT) technologies, with connected, smart home products representing one of the fastest-expanding sectors in the technology landscape. This convergence of climate policy, digital infrastructure, and consumer demand for convenience defines the structural momentum of the Smart Thermostat Market worldwide.

MARKET DRIVERS

Global Building Energy Efficiency Regulations and Green Construction Standards

Governments and international bodies are increasingly embedding Wi-Fi-enabled climate control devices into mandatory building codes and green certification frameworks, which drives the growth of the global smart thermostat market. These initiatives are transforming the devices from optional upgrades into regulatory requirements. The 2024 International Energy Conservation Code promotes advanced, connected HVAC systems by offering them as a recognized option in its enhanced, flexible compliance paths for new homes. Similarly, the World Green Building Council’s Net Zero Carbon Buildings Commitment emphasizes high-efficiency operational measures and smart technology as fundamental requirements for achieving net zero carbon in new and renovated buildings. In the United States, California’s Energy Code (Title 24) demands that new homes implement advanced, occupancy-based temperature controls and smart HVAC technologies to reduce energy waste. Canada provides federal and provincial financial incentives for installing energy-efficient smart thermostats in homes. Global building codes are moving towards increased stringency, with a strong focus on incorporating automated controls to enhance energy efficiency. These policies create predictable, large-scale demand that de-risks manufacturer investment and accelerates market penetration far beyond early adopter segments.

Escalating Residential Energy Costs and Consumer Demand for Bill Control

Soaring electricity and heating fuel prices have intensified household focus on energy consumption management, which propels the expansion of the smart thermostat market. Consequently, smart thermostats have become a practical tool for financial resilience. According to the International Energy Agency, despite a surge in global electricity demand, wholesale electricity prices eased in many major economies during 2024, although they remain high compared to pre-crisis levels; heating continues to represent a dominant portion of utility bills in temperate regions during winter. Smart thermostats address this pressure by delivering verified energy savings. A meta-analysis from the American Council for an Energy-Efficient Economy indicates that properly installed smart thermostats generate significant, measurable reductions in annual heating energy usage. Consumer adoption reflects this urgency. Nest emphasizes that consumers are increasingly purchasing smart thermostats primarily to reduce energy bills, rather than simply for convenience or remote control functionality. Utility companies globally are amplifying this trend through rebate programs. This economic imperative, validated by real-world savings, positions smart thermostats as essential household infrastructure in an era of energy volatility.

MARKET RESTRAINTS

Incompatibility with Legacy and Region-Specific HVAC Systems

A significant portion of the global housing stock relies on heating, ventilation, and air conditioning (HVAC) systems that lack the necessary wiring, communication protocols, or modulating capabilities to support smart thermostats. This incompatibility poses a major restraint on the smart thermostat market. In older homes across North America, Europe, and Asia, common configurations include two-wire heat-only systems, millivolt gas valves, or high-voltage electric baseboard heaters—all incompatible with standard low-voltage smart thermostats without costly retrofits. Many American households operate aging heating and cooling systems that require professional electrical modifications, such as the addition of a common wire, to integrate smart control technologies. In regions like Japan and parts of Eastern Europe, proprietary boiler interfaces further complicate compatibility. Even when technically feasible, the need for electricians or HVAC technicians increases total cost and deters DIY adoption. Until universal adapters or simplified retrofit kits become standard, this technical fragmentation will constrain market growth, particularly in emerging economies and aging urban centers.

Persistent Data Privacy and Cybersecurity Concerns

Smart thermostats collect highly sensitive data, including occupancy patterns, sleep schedules, and absence periods, and raise legitimate privacy and security concerns among consumers and regulators alike, which is another factor hindering the expansion of the smart thermostat market. The Federal Trade Commission in the United States has issued multiple warnings about IoT device data practices, noting that some smart home brands share anonymized usage data with third-party advertisers without explicit consent. A significant portion of consumers worldwide distrust connected home devices, driven by fears that these products collect excessive, intimate, or "creepy" data, coupled with apprehension about how that information is shared or stored by manufacturers. High-profile vulnerabilities, such as the 2023 exploit affecting a major brand’s cloud API, have eroded trust further. Compliance with evolving regulations like the EU’s GDPR and the U.S. NIST Cybersecurity Framework requires significant investment in encryption, secure boot, and vulnerability disclosure programs, increasing development costs. These perceptual and regulatory hurdles suppress trial, especially among privacy-conscious demographics, limiting the market’s ability to achieve mass adoption despite clear functional benefits.

MARKET OPPORTUNITIES

Integration into Utility-Led Demand Response and Virtual Power Plant Programs

These devices are emerging as critical assets in grid modernization efforts, which enable utilities to balance supply and demand through aggregated residential flexibility, and thereby offer strong potential for the smart thermostat market. Rising penetration of renewable energy necessitates that grid operators utilize distributed resources to handle intermittent supply. Aggregated smart thermostats can temporarily adjust heating or cooling loads during peak events, acting as a virtual power plant. Throughout the United States, a vast network of smart thermostats is increasingly utilized in demand response initiatives managed by major utilities like Pacific Gas & Electric to create substantial flexible energy capacity during peak summer periods, a trend closely monitored by the Brattle Group. Similarly, in Australia, AGL Energy is expanding its involvement in virtual power plant initiatives, specifically by acquiring large-scale household battery networks to alleviate pressure on the electrical grid during extreme weather events. Regulatory shifts allow distributed energy resources to participate in wholesale markets, creating new revenue streams for consumers. This transformation from passive appliance to active grid participant enhances the economic value proposition and aligns smart thermostats with global energy transition goals.

Expansion into Affordable Housing and Energy Poverty Alleviation Initiatives

Smart thermostats are gaining recognition as tools for addressing energy poverty, which paves the way for fresh prospects for the smart thermostat market. Global energy access reports show a substantial portion of the population still lacks reliable access to electricity and adequate cooling, driving the need for affordable, automated energy solutions. Governments and non-profits are deploying these devices in social housing to ensure efficient, dignified climate control without excessive bills. In Canada, the federal government’s Greener Homes Grant covers up to 5,000 CAD for energy retrofits, including smart thermostats. According to an NRCan update in February 2024, over $700 million had been issued to approximately 165,000 homeowners. However, by the end of 2024 and through 2025, that number grew significantly. By Jan 2026, over 400,000 households had received a grant. Similarly, South Africa’s Eskom utility distributes subsidized smart controls to low-income households to reduce grid strain and prevent disconnections. These programs demonstrate that smart thermostats can deliver both social equity and systemic efficiency, opening a high-impact public-sector channel. They serve as scalable solutions for inclusive climate action in both developed and developing economies by combining affordability, comfort, and conservation.

MARKET CHALLENGES

Consumer Confusion Over Value Proposition and Installation Complexity

Many consumers remain unclear about the tangible benefits of smart thermostats or perceive installation as overly complex, particularly in owner-occupied homes without professional support, despite technological advances, which challenges the growth of the smart thermostat market. As per a study, only a portion of homeowners could accurately identify whether their HVAC system was compatible with smart controls. DIY installation fears, fueled by wiring diagrams and boiler-specific configurations, lead to abandoned purchases or improper setups that undermine performance. Unlike in commercial settings, where certified integrators handle deployment, the residential market lacks standardized installation networks in many regions. Utility rebate programs often fail to include labor support, reducing effectiveness. Expansion will remain stalled among non-technical users until manufacturers streamline compatibility, improve setup guides, and grow their certified installer networks.

Intense Price Competition and Margin Pressure from Low-Cost Alternatives

Mounting pressure from low-cost alternatives gives basic connectivity at a fraction of the price, compressing margins and diluting brand differentiation, which constrains the expansion of the smart thermostat market. Chinese manufacturers now offer Wi-Fi-enabled thermostats for under 50 USD on global e-commerce platforms, featuring app control and simple scheduling but lacking adaptive learning or energy analytics. The trend forces premium brands like Nest and Ecobee to justify higher prices through software features and ecosystem integration, which may not resonate with budget-conscious buyers. Simultaneously, HVAC equipment makers like Carrier and Trane bundle proprietary thermostats with new systems, locking out third-party options. In an environment of economic uncertainty and rising interest rates, consumers prioritize upfront affordability over long-term savings, threatening the viability of innovation-driven business models and slowing the adoption of advanced energy-saving technologies worldwide.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2024 |

| Forecast Period | 2026 to 2034 |

| CAGR | 17.1% |

| Segments Covered | By Application, Technology, End User, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Emerson Electric Co., Ecobee Inc., Honeywell International Inc., Johnson Controls, Nest Labs Inc., Control4 Corporation, Schneider Electric SE, Tado GmbH, and Others. |

SEGMENTAL ANALYSIS

By Product Insights

The connected segment dominated the Smart Thermostat Market by accounting for a 58.5% share in 2025. The dominance of the connected segment is driven by its balance of affordability, remote accessibility, and integration with existing smart home ecosystems without requiring advanced AI capabilities. Connected thermostats allow users to adjust temperature settings via smartphone apps and receive basic energy usage reports, making them ideal for cost-conscious consumers and rental properties. According to analysis from the International Energy Agency, the adoption of connected thermostats has seen strong growth, driven by high demand in North America and Europe. This expansion is supported by widespread broadband availability, which enables smart home technology integration for improved energy management. Major HVAC manufacturers like Honeywell and Johnson Controls bundle these devices with new heating systems, ensuring broad distribution through contractor networks. Additionally, utility rebate programs in countries like Canada and Australia prioritize connected models due to their lower cost and proven ability to reduce peak demand. This combination of accessibility, utility support, and seamless integration into mainstream home improvement channels solidifies the connected segment as the market’s foundational pillar.

The learning thermostat segment is predicted to witness the highest CAGR of 16.3% from 2026 to 2034 due to increasing consumer demand for hands-free, adaptive climate control that optimizes both comfort and energy use without manual programming. Learning thermostats use occupancy sensors, geofencing, and machine learning algorithms to automatically build personalized schedules, reducing user effort and improving savings accuracy. Learning-enabled smart thermostats provide greater energy savings than non-learning connected models due to their ability to automatically adapt to household behavioral patterns. Google Nest and Ecobee dominate the market, with learning-based units representing the majority of sales for leading brands. Utility partnerships further amplify adoption. Learning thermostats are rapidly moving from luxury gadgets to essential tools for home energy efficiency, driven by affordable AI and growing demand for automation.

By End User Insights

The residential segment led the Smart Thermostat Market by capturing a substantial share in 2025. The leading position of the residential segment is attributed to direct consumer control over home energy decisions, rising awareness of energy costs, and supportive government incentives for household efficiency upgrades. Homeowners and renters increasingly view smart thermostats as essential tools for managing heating expenses, which constitute a significant portion of winter utility bills in temperate climates. American households are increasingly adopting smart thermostats, driven by a growing desire for energy-efficient, app-controlled home technology, supported by federal and local utility incentives. In Europe, national renovation schemes like France’s MaPrimeRénov and Germany’s Building Energy Act further accelerate adoption. The proliferation of DIY installation guides and compatibility checkers has also lowered barriers to entry. The worldwide demand for smart thermostats is primarily driven by the need to decarbonize homes, which house billions of existing HVAC systems.

The commercial segment is estimated to register the fastest CAGR of 18.7% during the forecast period, owing to corporate sustainability mandates, green building certifications, and the need to reduce operational costs in offices, retail spaces, and hospitality venues. The World Green Building Council emphasizes that, to achieve net-zero carbon goals, building owners are increasingly prioritizing the integration of intelligent, automated HVAC systems to optimize energy performance. In the United States, LEED v5 certification awards points for adaptive thermal zoning, driving adoption in new constructions. Companies like WeWork and Marriott International have deployed networked smart thermostats across thousands of locations to optimize energy use based on occupancy analytics. Additionally, commercial-grade platforms from Siemens and Schneider Electric now offer cloud-based dashboards that integrate with building management systems, enabling centralized control and predictive maintenance. Mandatory ESG reporting in regions like the EU and California is driving high-growth investment in intelligent climate systems, as companies seek to fulfill regulatory, compliance, and reputational goals, making this sector a booming market.

By Technology Insights

The Wi-Fi technology segment held the majority share of the smart thermostat market in 2025 because of ubiquitous home broadband infrastructure, ease of setup, and seamless integration with popular smart home platforms like Amazon Alexa, Google Assistant, and Apple HomeKit. Unlike proprietary protocols, Wi-Fi requires no additional hubs or gateways, reducing complexity and cost for consumers. In highly developed regions, the vast majority of city-based households now possess reliable wireless internet infrastructure capable of supporting smart home technology, including standard smart thermostats. Major brands, including Nest, Ecobee, and Honeywell,l design their flagship models exclusively for Wi-Fi to ensure broad compatibility and over-the-air update capability. Utility companies also favor Wi-Fi devices for demand response programs due to direct cloud connectivity without intermediary hardware. This combination of consumer familiarity, ecosystem alignment, and utility support ensures Wi-Fi remains the default connectivity choice for mainstream smart thermostat adoption globally.

The ZigBee segment is anticipated to witness the fastest CAGR of 21.4% from 2026 to 2034. The rapid expansion of the ZigBee segment is propelled by its low power consumption, mesh networking capability, and integration into professional-grade smart home and building automation systems. ZigBee enables thermostats to communicate with other devices, such as window sensors and blinds, without relying on home Wi-Fi, enhancing reliability and reducing bandwidth strain. The protocol is a core component of the Matter smart home standard, which promotes cross-brand interoperability. Commercial integrators prefer ZigBee for large-scale deployments due to its self-healing mesh topology, which ensures signal stability across multi-story buildings. Brands like Trane and Lennox now offer ZigBee-compatible thermostats that interface with Control4 and Crestron systems. ZigBee is positioned as the high-growth backbone for integrated climate control as the smart home market shifts toward professional, whole-home solutions.

REGIONAL ANALYSIS

North America Market Analysis

North America was the top performer in the Global Smart Thermostat Market by accounting for a 38.5% share in 2025. The dominance of the German market is driven by high consumer awareness, robust utility incentive programs, and progressive building codes. The United States alone accounts for millions of annual installations, supported by federal tax credits under the Inflation Reduction Act and state-level rebates from utilities like Pacific Gas & Electric. According to research, a portion of American households owned a smart thermostat in 2024, the highest penetration globally. Canada complements this through its Greener Homes Grant, covering up to 5,000 CAD for energy retrofits. The region’s mature broadband infrastructure, DIY culture, and strong presence of innovators like Nest and Ecobee further accelerate adoption. North America remains the premier hub for smart climate control, propelled by stringent regulatory standards like those in California and expanding corporate sustainability commitments.

Europe Market Analysis

Europe was the second largest country in the smart thermostat market by occupying a share of 28.2% share in 2025. The expansion of the European market is fuelled by its regulatory-driven adoption and focus on energy poverty alleviation. Revised EU legislation mandates that all new residential and non-residential constructions incorporate smart building automation and control systems, establishing a long-term structural demand for intelligent room-by-room temperature controls. Member states are aligning with EU goals by offering financial support for renovations, specifically in Germany, which requires neww efficient heating systems that include adaptive controls in subsidized renovations. The European smart thermostat market is undergoing a structural shift driven by regulatory pressure in new constructions and increased adoption of automated energy management in existing residential renovations, as consumers and policymakers target improved energy performance. The modernization of heating systems is being leveraged as a strategic tool to combat widespread energy poverty in Europe, focusing on reducing energy demand in the most poorly performing housing stock. The region’s high electricity prices further incentivize efficiency. Europe’s approach to smart home deployment, combining regulatory frameworks, social inclusivity, and responsiveness to energy costs, serves as a global model for sustainability.

Asia Pacific Market Analysis

Asia Pacific is expected to be the most lucrative region in the global market from 2026 to 2034 due to rapid urbanization, rising middle-class affluence, and government-led smart city initiatives. China leads the regional shift towards intelligent climate management, with major local manufacturers integrating connectivity into home appliances and broader IoT platforms to drive adoption. Japan focuses on elderly care, deploying smart thermostats in aging-in-place programs to prevent hypothermia. Meanwhile, Australia’s energy retailers, such as AGL and EnergyAustralia, offer subsidized devices to manage grid stress during heatwaves. According to the International Energy Agency, the rapid growth in worldwide cooling demand necessitates the widespread deployment of intelligent climate control systems to prevent unsustainable pressure on power grids. Asia-Pacific is rapidly emerging as a high-growth hub for innovative smart thermostats, fueled by a unique combination of strong manufacturing, digital literacy, and heightened climate vulnerability.

Latin America Market Analysis

Latin America grew steadily in the Global Smart Thermostat Market owing to economic recovery, expanding broadband access, and rising awareness of energy efficiency. Brazil and Mexico are leading the regional energy transition, with Brazil significantly accelerating distributed solar and electric vehicle adoption, supported by favorable regulatory frameworks, high solar capacity, and growing e-commerce availability. Local brands like Intelbras in Brazil offer affordable Wi-Fi models tailored to tropical climates, focusing on humidity control and cooling optimization. Government programs, such as Mexico’s Sustainable Housing Initiative, are beginning to include smart controls in green building standards. While still nascent, Latin America’s young, urban population and increasing climate volatility position it as a promising frontier for scalable, cost-effective smart thermostat solutions.

Middle East & Africa Market Analysis

The Middle East & Afriare is anticipated to expand in the smart thermostat market from 2026 to 2034 due to divergent trajectories between oil-rich Gulf states and emerging African economies. In the UAE and Saudi Arabia, smart thermostats are integral to luxury smart home projects and national sustainability visions lthe ike Saudi Green Initiative, which targets substantial renewable energy by 2030. Dubai’s Green Building Regulations mandate intelligent HVAC controls in all new constructions. Conversely, in South Africa and Nigeria, adoption is driven by grid instability and load-shedding, with consumers using smart thermostats to minimize generator fuel use. The convergence of extreme weather and urban energy gaps creates a massive opening for durable, independent cooling technologies designed for a wide range of social and financial backgrounds.

COMPETITIVE LANDSCAPE

Competition in the Smart Thermostat Market is intensifying as technology giants, traditional HVAC manufacturers, and specialized IoT startups vie for dominance in a landscape defined by interoperability, energy intelligence, and ecosystem integration. Google’s Nest leverages AI and consumer brand strength, while Honeywell and Johnson Controls capitalize on decades of HVAC expertise and professional installer networks. Chinese manufacturers compete on price with basic Wi-Fi models, pressuring margins in the entry-level segment. Differentiation increasingly hinges on software sophistication, such as predictive occupancy and grid-responsive algorithms, rather than hardware alone. Regulatory tailwinds from building codes and utility incentives create volume opportunities, but success depends on navigating fragmented HVAC infrastructures, data privacy concerns, and regional energy dynamics. Ultimately, the market is evolving into a dual-tier structure: premium, AI-driven platforms for engaged users and cost-effective, utility-backed devices for mass deployment, with winners excelling in both innovation and strategic partnerships.

KEY MARKET PLAYERS

Companies playing a major role in the global smart thermostat market include

- Emerson Electric Co

- Ecobee Inc

- Google (Nest)

- Honeywell International Inc

- Johnson Controls

- Nest Labs Inc

- Control4 Corporation

- Schneider Electric SE

- Tado GmbH

- Nortek Inc.

- Ingersoll Rand plc.

Top Players In The Market

- Google’s Nest division is a global pioneer in the smart thermostat market, renowned for its learning algorithms, sleek design, and deep integration with the Google Home ecosystem. Nest thermostats leverage artificial intelligence to adapt to user behavior, optimize energy use, and support demand response programs with utilities worldwide. The company has strengthened its position by enhancing compatibility with Matter, the universal smart home standard, ensuring seamless operation across platforms. It also deepened partnerships with utility providers in North America and Europe to offer subsidized devices tied to dynamic pricing tariffs. These initiatives reinforce Nest’s role as both a consumer brand and a grid-enabling technology platform in the global energy transition.

- Honeywell International Inc maintains a strong presence in the smart thermostat market through its Home and Building Technologies segment, offering a broad portfolio spanning residential, commercial, and light industrial applications. Known for reliability and HVAC system compatibility, Honeywell’s T series and Lyric models cater to both DIY consumers and professional installers. The company has recently enhanced its RedLINK wireless protocol to support ZigBee and Matter, enabling broader ecosystem integration. It also launched cloud-based analytics dashboards for commercial clients to monitor energy performance across multiple sites. Honeywell bridges traditional building automation with modern smart home demands, ensuring relevance across diverse global markets by leveraging its century-old reputation in climate control and expanding into software-driven services.

- Johnson Controls plays a pivotal role in the smart thermostat market through its York and Lux brands, focusing on high-efficiency solutions for residential and light commercial buildings. The company integrates its thermostats into broader OpenBlue digital platforms that connect HVAC, lighting, and security systems for holistic building management. Recently, Johnson Controls expanded its AI-driven occupancy prediction algorithms to improve energy savings in variable occupancy environments like hotels and offices. It also partnered with European social housing authorities to deploy smart thermostats in energy poverty alleviation programs. Johnson Controls strengthens its position as a key enabler of intelligent, efficient built environments worldwide by combining hardware expertise with enterprise-grade software and sustainability-focused deployments.

Top Strategies Used By The Key Market Participants

Key players in the Smart Thermostat Market are prioritizing integration with the Matter interoperability standard to ensure cross-platform compatibility and reduce consumer friction. They are expanding partnerships with utility companies to offer subsidized devices linked to demand response and time-of-use pricing programs. Companies are enhancing artificial intelligence capabilities to enable adaptive learning, occupancy detection, and carbon-aware scheduling. Strategic investments in commercial and multi-family building segments are being made to capture high-volume institutional deployments. Additionally, firms are developing ruggedized andoff-gridd compatible models for emerging markets with unstable power infrastructure to broaden global accessibility.

MARKET SEGMENTATION

This research report on the global smart thermostat market has been segmented and sub-segmented based on technology, application, end-user, and region.

By Technology

- Wi-Fi

- Bluetooth

- Zigbee

By Application

- Air Conditioning

- Heating

- Ventilation

By End User

- Residential

- Commercial

- Industrial

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

What is the global smart thermostat market?

It refers to the industry for internet-connected thermostats that monitor, control, and optimize heating and cooling systems in homes and buildings.

What drives growth in the smart thermostat market?

Rising energy efficiency awareness, government energy regulations, and demand for connected home solutions drive market expansion.

How does a smart thermostat work?

Smart thermostats use sensors, Wi-Fi connectivity, and algorithms to adjust HVAC settings based on occupancy and user preferences.

What are the key benefits of smart thermostats?

They save energy, reduce utility costs, offer remote control via mobile apps, and improve indoor comfort.

What technologies are integrated into smart thermostats?

Machine learning, mobile app connectivity, voice control, geofencing, and IoT integration are common features.

Which end users adopt smart thermostats most?

Residential households, commercial buildings, and smart office spaces are primary adopters.

How do smart thermostats support energy savings?

By learning user behavior and optimizing HVAC cycles, smart thermostats reduce unnecessary heating and cooling.

Are smart thermostats compatible with smart home systems?

Yes, they often integrate with smart speakers, home automation platforms, and energy management systems.

What role do government regulations play in the market?

Energy efficiency standards and building codes encourage adoption of smart energy controls like smart thermostats.

What challenges does the smart thermostat market face?

Data privacy concerns, high upfront costs, and interoperability issues can limit adoption.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com