Global Steam Autoclave Market Size, Share, Trends & Growth Forecast Report By Configuration, Technology, End-user and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Industry Analysis From 2026 To 2034

Market Size, 2025

$2.54 BnMarket Estimate, 2026

$2.74 BnMarket Forecast, 2034

$4.99 BnCAGR, 2026–2034

7.8%Global Steam Autoclave Market Report Summary

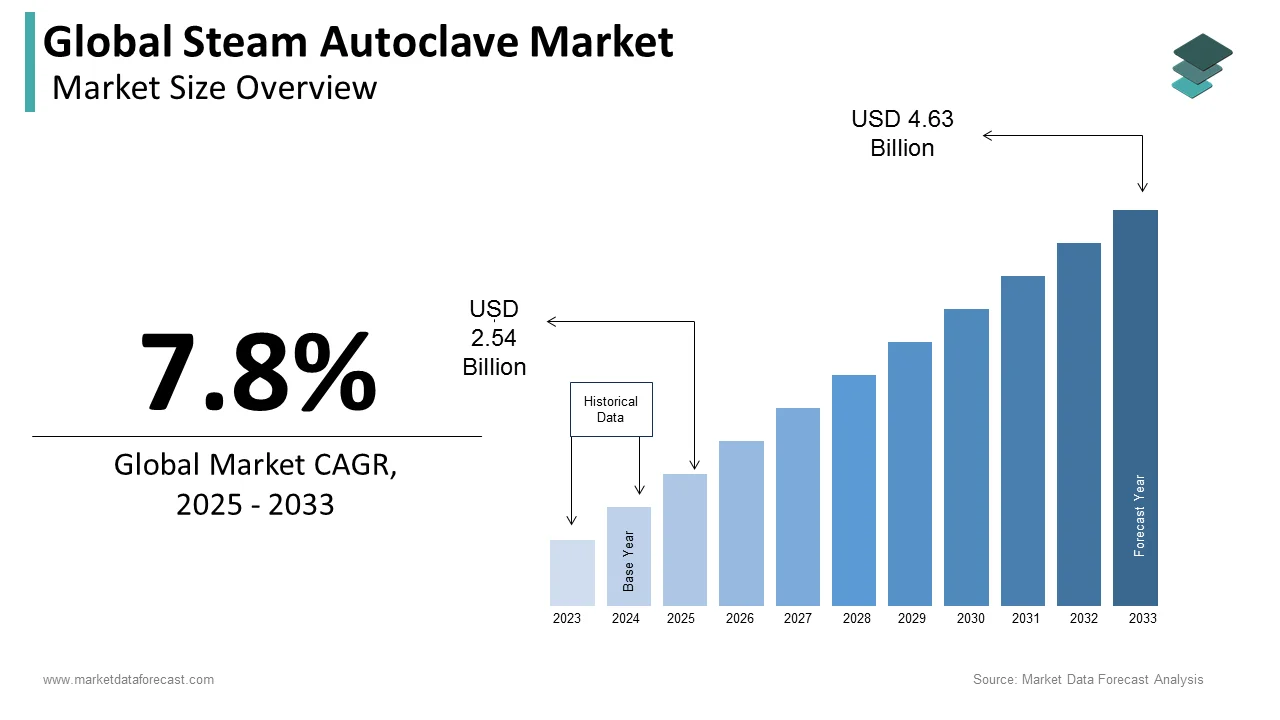

The global steam autoclave market was valued at USD 2.54 billion in 2025, is estimated to reach USD 2.74 billion in 2026, and is projected to reach USD 4.99 billion by 2034, growing at a CAGR of 7.8% from 2026 to 2034. Market growth is driven by the increasing need for effective sterilization in healthcare, pharmaceuticals, and research laboratories. The rising number of surgical procedures, growing awareness of infection control, and stringent regulatory standards for sterilization are key factors supporting market expansion. Additionally, advancements in autoclave technology, including energy-efficient and automated systems, are enhancing operational efficiency and adoption across industries.

Key Market Trends

- Increasing demand for infection control and sterilization solutions.

- Rising number of surgical procedures globally.

- Growing adoption in pharmaceutical and research laboratories.

- Technological advancements in automated and energy-efficient autoclaves.

- Stringent regulatory standards for sterilization processes.

Segmental Insights

- Based on configuration, the floor-standing segment dominated the global steam autoclave market by capturing 42.3% share in 2025, driven by its suitability for high-capacity sterilization.

- Based on technology, the pre-vacuum technology segment led the market with 55.4% share in 2025, supported by its superior sterilization efficiency.

- Based on end user, the hospitals segment held the largest share of 48.3% in 2025, due to high surgical volumes and strict infection control requirements.

Regional Insights

The global steam autoclave market is expanding steadily across regions due to increasing healthcare investments and regulatory compliance.

- North America led the market in 2025 with 34.3% share, supported by advanced healthcare infrastructure and strict sterilization standards.

- Europe followed with 28.3% share, driven by standardized regulatory frameworks and sustainable sterilization practices.

- Asia-Pacific is expected to witness strong growth due to increasing healthcare infrastructure investments and rising awareness of infection control.

Competitive Landscape

The global steam autoclave market is competitive, with companies focusing on technological innovation, product efficiency, and expanding their global footprint. Strategic partnerships and advancements in sterilization technologies are key competitive strategies.

Prominent companies operating in the global steam autoclave market include Steris Corporation, Belimed Deutschland, Priorclave Ltd., Getinge Infection Control, 3M Health Care, Panasonic Healthcare, LTE Scientific Ltd., Medisafe International, Belimed Group, Mitsubishi Electric Corporation, and Melag Medizintechnik.

Global Steam Autoclave Market Size

The size of the global steam autoclave market was worth USD 2.54 billion in 2025. The global market is anticipated to grow at a CAGR of 7.8% from 2026 to 2034 and be worth USD 4.99 billion by 2034 from USD 2.74 billion in 2026.

The steam autoclave utilizes saturated steam to achieve sterilization of medical instruments, laboratory equipment, and pharmaceutical products. These systems operate by exposing items to high temperature and pressure conditions, typically reaching 121 degrees Celsius or higher, to eliminate all forms of microbial life, including spores. In Europe, this technology serves as the cornerstone of infection control protocols within hospitals, surgical centers, and research facilities. The critical nature of these devices is underscored by the persistent burden of healthcare-associated infections, which affect approximately 4.3 million hospitalized patients annually, across the European Union and European Economic Area. Furthermore, the European Centre for Disease Prevention and Control indicates that nearly 9.8% of patients staying in intensive care units acquire an infection during their treatment, highlighting the urgent need for reliable sterilization infrastructure.

MARKET DRIVERS

Escalating Prevalence of Healthcare-Associated Infections Demands Rigorous Sterilization Protocols

The rising incidence of healthcare-associated infections is the primary factor boosting the growth of the steam autoclave market. This alarming statistic forces healthcare administrators to invest heavily in high-performance steam autoclaves that guarantee the elimination of pathogens from reusable surgical instruments and patient care items. The European Centre for Disease Prevention and Control further emphasizes this urgency by reporting that more than 3.5 million cases of healthcare-associated infections occur annually in long-term care facilities alone. Consequently, hospitals are upgrading their sterilization departments with larger capacity and more efficient autoclaves to handle the increased throughput required to maintain hygiene standards. This financial shift directly benefits the steam autoclave sector as facilities replace aging units with modern devices capable of faster cycle times and better validation tracking. The direct correlation between infection rates and equipment procurement ensures that steam autoclaves remain a critical capital expenditure item for health systems aiming to reduce patient mortality and avoid regulatory penalties associated with poor hygiene outcomes.

Surge in Surgical Procedure Volumes Amplifies Requirement for Sterile Instrument Processing

The substantial increase in the volume of surgical procedures performed necessitates the rapid and reliable sterilization of vast quantities of surgical tools, which is another attribute bolstering the growth of the steam autoclave market. This expansion in surgical activity includes both elective and emergency operations, which generate a continuous stream of contaminated instruments requiring immediate decontamination before reuse. Steam autoclaves are uniquely positioned to meet this demand due to their ability to process large loads of metal instruments efficiently and cost-effectively compared to alternative methods. This growth places immense pressure on central sterile supply departments to optimize their workflows, leading to the adoption of automated pass-through autoclaves and integrated washer-disinfectant systems. The reliance on steam sterilization remains unchallenged for heat-stable items, ensuring that market demand scales linearly with the number of surgeries performed in both public and private healthcare sectors throughout the region.

MARKET RESTRAINTS

High Capital Expenditure and Operational Energy Costs Limit Market Penetration

The significant financial burden associated with the acquisition and operation of industrial steam autoclaves, with the adoption among smaller clinics and budget-constrained facilities, is limiting the growth of the steam autoclave market. High investment costs for large capacity sterilizers often exceed the available capital budgets of many healthcare providers, forcing them to delay upgrades or rely on outdated equipment. Industrial electricity prices in the European Union were more than twice as high as those in the United States and China during the first half of 2025, placing severe strain on energy-intensive industries, including healthcare sterilization. Steam autoclaves require substantial amounts of electricity and water to generate and maintain high-pressure steam, making them costly to run on a daily basis. The European Commission has noted that energy-intensive industries are urging for affordable electricity benchmarks to unlock electrification, yet prices remain a barrier to efficient operations. Additionally, the Clean Industrial Deal launched in February 2025 aims to address these issues, but immediate relief remains elusive for many end users. These economic factors compel some facilities to outsource sterilization or reduce the frequency of sterilization cycles, which ultimately caps the potential sales volume for new steam autoclave units in the short term.

Increasing Preference for Single-Use Disposable Medical Devices Reduces Reusable Instrument Load

The growing shift toward single-use disposable medical devices, by diminishing the volume of reusable instruments that require sterilization, is limiting the growth of the steam autoclave market. Healthcare facilities are increasingly adopting disposable syringes, catheters, surgical drapes, and even complex instrumentation to eliminate the risk of cross-contamination and reduce the logistical burden of reprocessing. This trend is driven by the desire to minimize healthcare-associated infections and streamline workflow efficiency without relying on centralized sterilization departments. The increasing use of disposable products in healthcare settings is a key factor hindering the growth of the global steam autoclaves market. The convenience of disposables removes the need for washing, inspecting, and autoclaving items, thereby directly reducing the utilization rate of existing steam sterilization equipment. Furthermore, the regulatory environment supports this shift as manufacturers seek to avoid the rigorous validation requirements associated with reusable device reprocessing cycles. While steam autoclaves remain essential for certain heavy metal instruments, the overall basket of goods requiring sterilization is shrinking in specific segments like minor surgery and outpatient care. This transition limits the necessity for purchasing additional autoclave units and may lead to a consolidation of sterilization services into fewer, larger facilities rather than widespread distribution of equipment.

MARKET OPPORTUNITIES

Integration of Internet of Things and Smart Monitoring Technologies Creates New Value Propositions

The incorporation of Internet of Things capabilities and smart monitoring features for manufacturers to differentiate their products and capture premium quality is certainly to create new opportunities for the growth of the steam autoclave market. Modern healthcare facilities are increasingly demanding connected devices that offer remote monitoring, real-time data analytics, and predictive maintenance to ensure uninterrupted sterilization operations. As per research, the steam sterilizers autoclave sector includes the integration of smart technologies such as remote monitoring and data analytics to enhance operational efficiency. These advanced systems allow facility managers to track cycle parameters, validate sterilization efficacy, and receive instant alerts regarding maintenance needs from any location. The ability to digitally document every sterilization cycle also aids in complying with strict European Medical Device Regulations and audit requirements without manual record keeping. LinkedIn industry reports highlight that innovations such as digital controls and faster cycle times enhance the appeal of modern autoclaves, driving adoption in high-tech laboratories and pharmaceutical plants. Furthermore, the connection of autoclaves to hospital information systems enables seamless tracking of instrument usage and patient safety metrics, creating a comprehensive ecosystem for infection control. This technological evolution transforms the autoclave from a standalone appliance into a critical node in the digital health infrastructure, opening avenues for recurring revenue through software subscriptions and service contracts. Manufacturers who successfully embed these intelligent features can command higher prices and secure long-term partnerships with forward-thinking healthcare organizations seeking to modernize their sterile processing departments.

Expansion of Pharmaceutical and Biotechnology Manufacturing Drives Specialized Sterilization Needs

The robust growth of the pharmaceutical and biotechnology sectors through the demand for specialized industrial sterilization solutions is also driving the growth of the steam autoclave market. As the production of biologics vaccines and sterile injectables increases, manufacturers require large-scale and highly reliable steam sterilizers for processing raw materials, equipment, and final product containers. The growth in the pharmaceutical and biotech sectors necessitates reliable sterilization due to increased production of biologics and sterile pharmaceuticals. Steam autoclaves are indispensable in this industry for depyrogenation and sterilization of glassware, fermentation tanks, and filling lines, where absolute sterility is non-negotiable. The stringent regulatory framework governing drug manufacturing ensures that pharmaceutical companies invest in top-tier autoclave systems with advanced validation and control capabilities. This sectoral expansion allows autoclave manufacturers to introduce customized high-capacity units designed specifically for industrial applications, thereby diversifying their revenue streams beyond traditional healthcare settings. The alignment of market growth in life sciences with the fundamental need for steam sterilization creates a fertile ground for innovation and sales expansion in the coming decade.

MARKET CHALLENGES

Complex Maintenance Requirements and Skilled Labor Shortages Impede Operational Efficiency

The intricate maintenance demands of steam autoclave systems, coupled with a shortage of skilled technical personnel, affect equipment uptime, and user confidence is one of the challenges for the growth of the steam autoclave market. Steam autoclaves operate under high-pressure and temperature conditions, requiring regular calibration, seal replacement, and valve inspections to function safely and effectively. As per the study, maintenance and servicing requirements for autoclaves can be costly and time-consuming, acting as a deterrent for potential buyers and straining existing operators. The lack of trained biomedical engineers and technicians capable of performing these specialized tasks leads to prolonged downtime when machines malfunction, disrupting critical sterilization workflows. Furthermore, the complexity of modern automated autoclaves with digital interfaces and integrated sensors requires a higher level of technical expertise than older mechanical models. This skills gap is particularly acute in rural areas or smaller clinics where access to certified service providers is limited. The challenge is compounded by the need for strict adherence to validation protocols, which demand precise documentation and testing that untrained staff may struggle to execute correctly.

Stringent Regulatory Compliance and Validation Burdens Increase Time to Market and Costs

The rigorous regulatory governing medical device sterilization for manufacturers by imposing heavy compliance and validation burdens is solely degrading the growth of the steam autoclave market. Adherence to standards, such as EN 556 and ISO 11137, requires extensive documentation, testing, and verification processes that increase both the development time and the cost of bringing new products to market. As per the European Commission, harmonized standards for medical device sterilization mandate strict requirements for designating devices as sterile, which manufacturers must meticulously follow to avoid legal repercussions. The European Medical Device Regulation has further tightened these controls, requiring notified body audits and continuous post-market surveillance of sterilization equipment. Pure Clinical notes that new harmonized standards on biocompatibility and sterilization processing have been introduced, adding layers of complexity for manufacturers to navigate. These regulatory hurdles can delay product launches and limit the ability of smaller companies to compete with established players who have dedicated compliance teams. Additionally, end users face challenges in validating their sterilization cycles to meet these standards, often requiring expensive external consulting services and specialized test equipment. The constant evolution of these regulations means that manufacturers must continuously update their designs and software to remain compliant, diverting resources away from innovation. This environment of high regulatory scrutiny, while essential for patient safety, acts as a barrier to entry and slows down the overall pace of market expansion for steam autoclave technologies.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Configuration, Technology, End-user & Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Steris, Belimed Deutschland, Priorclave, Getinge Infection Control, 3M Health Care, Panasonic Healthcare, LTE Scientific, Medisafe International, Belimed Group, and Melag.

|

SEGMENTAL ANALYSIS

By Configuration Insights

The floor-standing segment accounted in holding 42.3% of the European steam autoclave market share in 2025. The high throughput capacity in large-scale healthcare and industrial facilities where bulk sterilization is mandatory is one of the major factors fuelling the growth of the segment. The sheer volume of surgical instruments processed in major hospitals necessitates equipment that can handle large loads efficiently without frequent cycling. According to the European Hospital and Healthcare Federation, the average number of beds in large acute care hospitals across Europe exceeds 500, creating a massive daily demand for sterile processing that only floor-standing units can satisfy. These systems often feature pass-through designs that integrate directly into clean room workflows, minimizing cross-contamination risks between dirty and clean zones. Furthermore, the pharmaceutical sector relies heavily on these robust units for sterilizing fermentation tanks and large production batches, ensuring compliance with Good Manufacturing Practices.

The table top segment is expected to register the fastest CAGR of 8.9% during the forecast period, driven by the proliferation of small-scale medical practices and decentralized care models. The increasing number of outpatient clinics and dental offices that require on-site sterilization capabilities without the space or budget for large industrial units is also driving the growth of the segment. These units offer significant advantages in terms of ease of installation and lower energy consumption, making them ideal for facilities with limited utility infrastructure. As per LinkedIn industry analysis, the shift toward ambulatory surgery centers, which now perform over 60% of minor surgical procedures in Europe, has further accelerated the adoption of tabletop autoclaves. Their ability to provide rapid cycle times for small loads ensures that practitioners can maintain high patient turnover rates while adhering to strict hygiene protocols. Additionally, advancements in technology have allowed manufacturers to pack features like automatic water filling and digital validation into these smaller footprints, enhancing their appeal to modern healthcare providers seeking efficiency and compliance in compact spaces.

By Technology Insights

The pre-vacuum technology segment was the largest by holding 55.4% of the steam autoclave market share in 2025, with the superior air removal capabilities of pre-vacuum systems, which ensure complete steam penetration into complex instrument lumens and porous loads essential for modern surgical tools. The European Centre for Disease Prevention and Control mandates rigorous sterilization standards for hollow instruments, which can only be reliably achieved through the multiple vacuum pulses employed by this technology. According to the Association for Professionals in Infection Control and Epidemiology, failures in sterilizing lumened devices are a leading cause of surgical site infections, prompting hospitals to exclusively adopt pre-vacuum units for critical care areas. The growing complexity of minimally invasive surgical instruments with long, narrow channels has made gravity displacement methods insufficient for many applications, thereby driving the preference for pre-vacuum systems. Furthermore, the integration of Bowie Dick testing within pre-vacuum cycles provides immediate verification of air removal, offering an additional layer of safety that regulatory bodies highly recommend.

The steam flush pressure pulse segment is anticipated to witness the fastest CAGR of 9.4% from 2026 to 2034, owing to its ability to sterilize heat-sensitive and porous materials without the risk of wet packs. This technology is gaining traction because it eliminates the need for a deep vacuum, which can damage delicate instruments or cause liquids to boil over, making it ideal for laboratory and pharmaceutical applications. The SFPP method offers a gentler yet effective sterilization process that preserves the integrity of sensitive media and plasticware, which constitute a growing portion of laboratory consumables. Unlike pre-vacuum systems, SFPP units require less maintenance due to the absence of complex vacuum pumps, reducing the total cost of ownership for research institutions. The versatility of this technology in handling both solid and liquid waste streams positions it as the preferred choice for expanding life science facilities seeking operational flexibility and equipment longevity.

By End-user Insights

The hospitals segment held 48.3% of the steam autoclave market share in 2025, with the immense volume of surgical procedures and the requirement for infection control within inpatient settings. Hospitals serve as the primary hub for sterile processing, managing thousands of reusable instruments daily, which necessitates the deployment of multiple high-capacity autoclave units. According to the study, the average number of surgeries performed per 1000 inhabitants in European Union countries reached 115 in 2025, reflecting the heavy operational load on hospital sterilization departments. The stringent regulatory framework enforced by national health authorities requires hospitals to maintain impeccable sterilization records and validate every cycle, a task facilitated by the advanced monitoring systems in modern hospital-grade autoclaves. As per the European Society of Clinical Microbiology and Infectious Diseases, healthcare-associated infections cost European health systems over 7 billion EUR annually, compelling hospitals to invest heavily in state-of-the-art sterilization infrastructure to mitigate these risks. The consolidation of healthcare services into larger hospital networks has further centralized sterilization processes, increasing the demand for industrial-scale floor-standing units. Additionally, the rise in trauma cases and emergency surgeries due to an aging population ensures a consistent and growing need for reliable steam sterilization capabilities within acute care facilities across the region.

The pharmaceutical segment is projected to witness the fastest CAGR of 10.2% from 2026 to 2034 with the expansion of biologics manufacturing and stringent Good Manufacturing Practice requirements. The production of sterile injectable vaccines and cell therapies demands absolute sterility for both product contact parts and production environments, driving significant investment in industrial steam autoclaves. Data from the European Federation of Pharmaceutical Industries and Associations indicates that pharmaceutical production output in Europe grew by 8% in 2025, with a specific focus on sterile formulations requiring robust sterilization validation. The shift towards personalized medicine and small batch production has increased the need for flexible yet compliant sterilization solutions that can handle diverse container types and volumes. Regulatory inspections by agencies such as the European Medicines Agency have become more rigorous regarding sterilization protocols, prompting companies to replace older units with advanced systems featuring real-time data logging and automated control.

REGIONAL ANALYSIS

North America Steam Autoclave Market Analysis

North America was the largest contributor in the global steam autoclave market by holding 34.3% of the share in 2025, with its rigorous infection control mandates and advanced healthcare infrastructure. The region sets the global standard for sterilization protocols, with regulatory bodies enforcing strict compliance measures that necessitate the continuous upgrading of equipment. According to the Centers for Disease Control and Prevention, healthcare-associated infections affect nearly 1.7 million patients annually in the United States alone, creating an imperative for hospitals to invest in state-of-the-art steam sterilization systems to mitigate these risks. The high concentration of ambulatory surgery centers, which performed over 50 million procedures in 2025, as per the Ambulatory Surgery Center Association, further amplifies the demand for efficient tabletop and floor-standing autoclaves. Furthermore, the robust pharmaceutical and biotechnology sectors in the region require industrial-grade sterilizers for manufacturing sterile injectables and medical devices adhering to Current Good Manufacturing Practices. The presence of major market players and a strong culture of research and development also fosters the early adoption of smart autoclaves with Internet of Things connectivity

Europe Steam Autoclave Market Analysis

Europe was ranked second by holding 28.3% of the share in 2025, with its highly standardized regulatory framework and growing emphasis on sustainable sterilization practices. The region operates under the stringent European Medical Device Regulation, which mandates comprehensive validation and traceability for all sterilization processes, driving hospitals to replace aging units with compliant modern systems. Data from the European Centre for Disease Prevention and Control indicates that healthcare-associated infections remain a critical challenge affecting over 4 million patients annually across the European Union, prompting aggressive investment in infection prevention infrastructure. The strong preference for energy-efficient autoclaves as governments' push for carbon neutrality in healthcare facilities under the European Green Deal initiatives. As per Eurostat, the healthcare sector in Europe accounts for a significant portion of national energy consumption, leading facility managers to prioritize water and electricity-saving sterilization technologies. Germany, France, and the United Kingdom serve as the primary growth engines within the region due to their large hospital networks and advanced pharmaceutical manufacturing bases.

Asia-Pacific Steam Autoclave Market Analysis

The Asia-Pacific steam autoclave market is expected to witness prominent growth opportunities in the coming years, 22% driven by massive investments in healthcare infrastructure and rising awareness of infection control standards. Countries such as China, India, and Japan are witnessing an unprecedented expansion of hospital beds and surgical centers to cater to their growing and aging populations, creating a surge in demand for sterilization equipment. According to the World Bank, healthcare expenditure in the Asia-Pacific region has grown at an average annual rate of 7% over the last decade, enabling governments and private providers to upgrade from outdated manual sterilizers to automated steam autoclaves. The region is also becoming a global hub for pharmaceutical manufacturing, with companies establishing large-scale production facilities that require industrial sterilization solutions to meet international export standards. Furthermore, the rise of medical tourism in nations like Thailand and Singapore drives the need for world-class sterilization infrastructure to attract international patients. Government initiatives to reduce hospital-acquired infections and the increasing number of accredited healthcare facilities further accelerate market penetration.

Latin America Steam Autoclave Market Analysis

Latin America steam autoclave market is likely to have steady opportunities in the coming years with the ongoing modernization of public health systems and the expansion of private healthcare networks in key economies. According to the Pan American Health Organization, healthcare-associated infection rates in some Latin American countries are up to three times higher than in developed nations, prompting ministries of health to launch nationwide sterilization improvement programs. Brazil and Mexico are major contributors due to their large populations and increasing number of surgical procedures performed annually in both public and private sectors. As per the Brazilian Ministry of Health, recent regulations mandating stricter sterilization protocols for all healthcare facilities have triggered a wave of equipment procurement to replace non-compliant units. The growing middle class is also driving demand for private healthcare services, where patients expect higher standards of hygiene and safety, further boosting the installation of modern autoclaves. Additionally, the expansion of the pharmaceutical industry in the region to serve local and export markets creates a steady demand for industrial sterilization equipment.

Middle East and Africa Steam Autoclave Market Analysis

The Middle East and Africa steam autoclave market growth is expected to grow with a dichotomy between highly advanced healthcare systems in the Gulf Cooperation Council nations and developing infrastructure in sub-Saharan Africa. The Gulf states, including Saudi Arabia and the United Arab Emirates, are aggressively investing in world-class medical cities and hospitals to become regional healthcare hubs, driving demand for premium steam autoclave systems. As per the World Health Organization, strengthening sterilization services is a key priority in African health strategies to support safe surgery initiatives and reduce maternal and neonatal mortality. The increasing number of accredited hospitals seeking international certification also forces facilities to adopt validated steam autoclaves that meet global standards. Furthermore, the growth of the pharmaceutical sector in North Africa creates a niche demand for industrial sterilizers.

COMPETITIVE LANDSCAPE

The competition in the steam autoclave market is characterized by intense rivalry among established global manufacturers and emerging regional players striving for technological superiority and market penetration. Leading companies differentiate themselves through continuous innovation in automation, digital monitoring, and energy efficiency to meet the evolving needs of the healthcare and life science sectors. The market sees frequent product launches featuring advanced connectivity options that allow remote management and data analytics, which are becoming standard requirements for modern facilities. Price competition remains moderate as buyers prioritize reliability, compliance, and service support over initial cost savings, given the critical nature of sterilization processes. Strategic mergers and acquisitions are common as larger entities seek to broaden their product portfolios and enter new geographic markets rapidly. Regulatory compliance acts as a significant barrier to entry, ensuring that only firms with robust quality management systems can compete effectively in this specialized domain.

KEY MARKET PLAYERS

Companies playing a prominent role in the global steam autoclave market are

- Steris

- Belimed Deutschland

- Priorclave

- Getinge Infection Control

- 3M Health Care

- Panasonic Healthcare

- LTE Scientific

- Medisafe International

- Belimed Group

- Mitsubishi Electric Corporation

- Melag

TOP PLAYERS IN THE MARKET

- Steris plc stands as a global leader providing comprehensive infection prevention and procedural solutions, including advanced steam autoclaves. The company actively contributes to the market by offering a wide range of sterilization equipment designed for hospitals, laboratories, and pharmaceutical facilities worldwide. Steris recently launched new generations of high-capacity floor-standing autoclaves featuring integrated digital monitoring and remote diagnostics to enhance operational efficiency. Their strategic focus involves expanding service networks across emerging markets to ensure rapid support and maintenance for clients. The firm continues to invest heavily in research and development to create energy-efficient models that reduce water and power consumption while maintaining rigorous sterilization standards.

- Getinge AB is a prominent Swedish manufacturer renowned for its high-quality life science technologies and sterilization equipment, including state-of-the-art steam autoclaves. The company serves a diverse global customer base ranging from acute care hospitals to biotechnology firms with robust sterilization solutions. Getinge has recently strengthened its market position by introducing smart connected autoclaves that utilize Internet of Things technology for real-time performance tracking and predictive maintenance. They have also expanded their production capabilities in Asia and Europe to meet the rising demand for sterile processing equipment driven by increased surgical volumes. Their dedication to improving patient safety is evident through continuous product upgrades that ensure compliance with the latest international regulatory standards.

- Mitsubishi Electric Corporation plays a significant role in the global steam autoclave market through its advanced industrial automation and sterilization technologies. The company leverages its extensive expertise in electrical systems to produce highly reliable and efficient autoclaves for medical and industrial applications. Mitsubishi has recently focused on integrating artificial intelligence into its sterilization units to optimize cycle times and energy usage automatically. They have formed strategic partnerships with major hospital groups in North America and Europe to deploy large-scale sterilization centers equipped with their latest machinery. The firm is also enhancing its supply chain resilience to ensure the timely delivery of equipment amidst global logistical challenges.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the steam autoclave market primarily employ product innovation and strategic acquisitions to maintain competitive advantages and expand their global reach. Companies consistently invest in research and development to introduce smart autoclaves with digital connectivity and automated features that appeal to modern healthcare facilities. Another prevalent strategy involves forming strategic partnerships with hospital networks and pharmaceutical manufacturers to secure long-term supply contracts and service agreements. Market participants also focus on geographic expansion by establishing local manufacturing units and distribution centers in emerging economies to reduce costs and improve delivery times. Enhancing after-sales service through comprehensive maintenance packages and training programs is crucial for retaining customers and ensuring equipment longevity.

MARKET SEGMENTATION

This market research report on the global steam autoclave market has been segmented and sub-segmented based on configuration, technology, end-user & region.

By Configuration

- Table Top

- Vertical

- Horizontal

- High Pressure

- Floor Standing

By Technology

- Gravity Displacement

- Steam Flush

- Pre-vacuum

By End-user

- Medical

- Hospitals

- Clinics

- Medical Waste Management

- Laboratory

- Pharmaceutical

- Bio-hazardous Waste Management

- Dental clinics

- Health Care Organizations

- Academics

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Frequently Asked Questions

1. Which product types dominate the global steam autoclave market?

Steris, Belimed Deutschland, Priorclave, Getinge Infection Control, 3M Health Care, Panasonic Healthcare, LTE Scientific, Medisafe International, Belimed Group, and Melag are a few of the notable players in the steam autoclave market.

2. How do steam autoclaves contribute to infection control?

North America held the most significant share of the global market in 2024.

3. What are the key applications of steam autoclaves in healthcare?

Tabletop, vertical, and horizontal steam autoclaves lead in market share, with tabletop autoclaves growing rapidly in small clinics and research labs

4. Which regions lead the global steam autoclave market?

Steam autoclaves use high-pressure steam to sterilize medical instruments, effectively eliminating pathogens and reducing hospital-acquired infections, critical in healthcare sectors

5. How has COVID-19 impacted the global steam autoclave market?

They are widely used in hospitals, dental clinics, laboratories, pharmaceutical manufacturing, and biohazard waste management for sterilization

6. What technological advancements are impacting the global steam autoclave market?

North America and Europe lead, driven by stringent sterilization regulations, while Asia Pacific shows the fastest growth due to expanding healthcare infrastructure

7. What role do regulatory standards play in the global steam autoclave market?

Demand surged due to increased sterilization needs during the pandemic, accelerating adoption in healthcare and research facilities

8. How do dental clinics impact the market growth?

Automation, IoT-enabled monitoring, energy-efficient designs, and faster sterilization cycles are key innovations propelling the market

9. How important is environmental sustainability in the steam autoclave market?

Strict sterilization and infection control standards from bodies like the CDC and WHO drive demand for high-quality steam autoclaves

10. How do automated steam autoclaves improve healthcare operations?

Increasing dental procedures and CDC sterilization guidelines boost demand for dental steam autoclaves, a fast-growing segment

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com