Global Thermoform Packaging Market Size, Share, Trends & Growth Forecast Report By Material, By Product Type, By Application, and By Region (North America, Europe, Asia Pacific, Latin America, Middle East & Africa) – Industry Analysis and Forecast, 2026 to 2034

Market Size, 2025

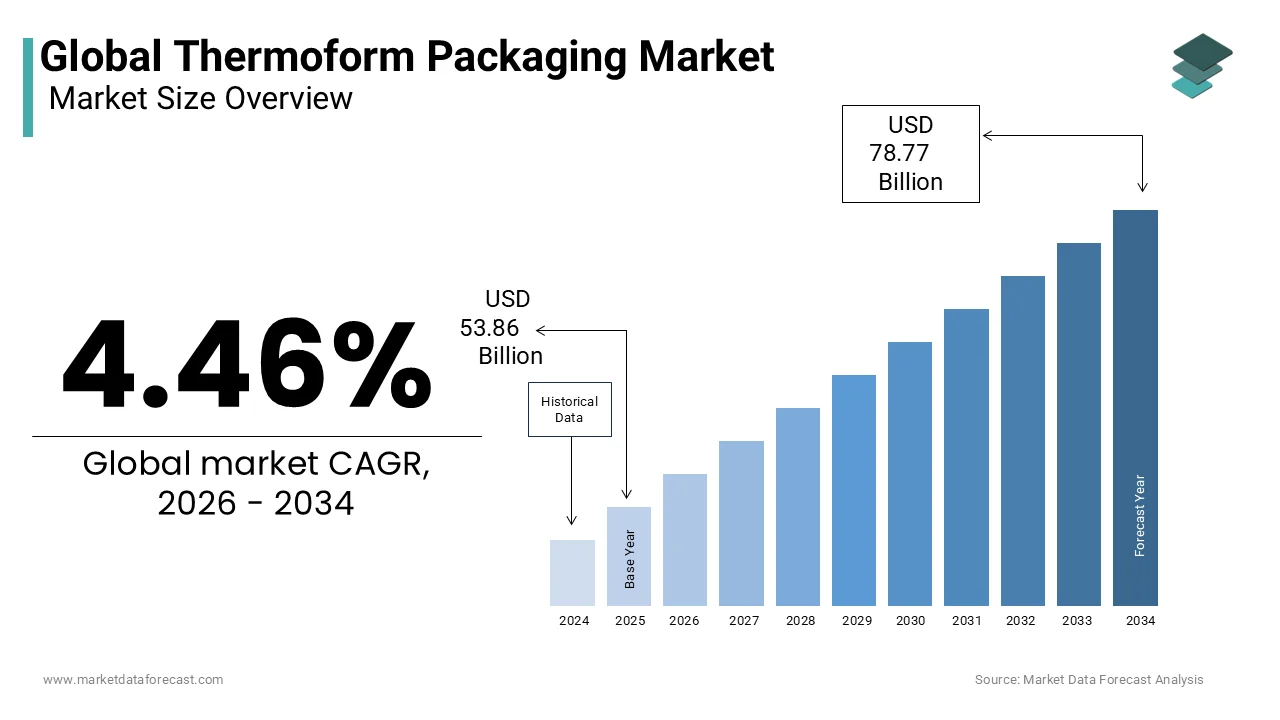

$53.86 BnMarket Estimate, 2026

$56.26 BnMarket Forecast, 2034

$78.77 BnCAGR, 2026–2034

4.46%Global Thermoform Packaging Market Size

The global thermoform packaging market size was valued at USD 53.86 billion in 2025 and is anticipated to reach USD 56.26 billion in 2026 and USD 78.77 billion by 2034, growing at a CAGR of 4.46% during the forecast period from 2026 to 2034.

The thermoform packaging is the use of molded plastic sheets shaped under heat and pressure to create durable yet lightweight packaging solutions across food, pharmaceuticals, electronics, and consumer goods. This method is valued for its versatility, cost-effectiveness, and ability to preserve product integrity. Its growing importance is closely tied to the rising demand for packaged foods and healthcare products.

MARKET DRIVERS

Rising Consumption of Packaged Foods

The demand for thermoform packaging is strongly driven by the surge in ready-to-eat and convenience foods, which require lightweight and tamper-proof packaging. The United Nations Department of Economic and Social Affairs has projected that by 2050, nearly 68% of the global population will live in urban areas, accelerating dependence on packaged goods. Thermoform trays and clamshells preserve freshness while ensuring safe transportation, making them indispensable in modern supply chains. As per the Food and Agriculture Organization, foodborne diseases impact over 600 million people annually, which enhances the appeal of hygienic and sealed thermoformed solutions.

Growth in Pharmaceutical Packaging Needs

Pharmaceutical demand for blister packs is propelling the growth of the thermoform packaging market. According to the International Federation of Pharmaceutical Manufacturers and Associations, global pharmaceutical spending reached over USD 1.4 trillion in 2020, with Asia Pacific contributing a rising share. Thermoform packaging safeguards drugs against moisture, contamination, and counterfeiting, crucial for maintaining therapeutic efficacy. Additionally, the World Health Organization states that up to 10% of medical products in low- and middle-income nations are substandard or falsified, reinforcing the value of secure packaging systems.

MARKET RESTRAINTS

Environmental Concerns over Plastic Waste

The sustainability challenges linked to plastic pollution are degrading the growth of the thermoform packaging market. According to the Organisation for Economic Co-operation and Development, only 9% of the 353 million tonnes of plastic waste generated globally in 2019 was recycled, with packaging materials accounting for the largest share. Governments worldwide are imposing stringent regulations on single-use plastics, limiting the adoption of conventional thermoform packaging. This trend is particularly challenging for producers relying on petroleum-based polymers, as consumer sentiment increasingly favors eco-friendly alternatives. The inability to adapt to circular economy requirements poses a significant restraint to long-term industry growth.

Volatility in Raw Material Prices

The cost structure of thermoform packaging is heavily influenced by fluctuations in petrochemical-based resin prices. As per the U.S. Energy Information Administration, crude oil prices experienced over 50% volatility in 2022 due to supply disruptions and geopolitical tensions, directly affecting raw polymer costs. These unpredictable price shifts translate into unstable production expenses for thermoform packaging manufacturers. For small and mid-sized enterprises, the inability to hedge against these fluctuations hampers profitability and competitiveness.

MARKET OPPORTUNITIES

Emergence of Sustainable and Bio-Based Materials

Sustainability initiatives are creating substantial opportunities for thermoform packaging innovation, which is solely aimed at enhancing the growth of the thermoform packaging market in the coming years. This shift enables thermoform packaging producers to replace petroleum-based polymers with polylactic acid (PLA) and polyhydroxyalkanoates (PHA), meeting consumer and regulatory demand for eco-friendly solutions. Companies adopting recyclable and compostable formats can tap into premium markets while aligning with circular economy frameworks.

Expansion of E-commerce and Cold Chain Logistics

The rapid growth of e-commerce and cold chain networks enhances the role of thermoform packaging in ensuring product safety during transit, which is another attribute to escalate the growth of the thermoform packaging market. Thermoform clamshells, blister packs, and insulated trays ensure secure delivery of electronics, perishables, and pharmaceuticals. Similarly, the Food and Agriculture Organization emphasizes that maintaining cold chain integrity is crucial in preventing spoilage for dairy, meat, and seafood.

MARKET CHALLENGES

Complex Recycling Processes

A persistent challenge lies in the difficulty of recycling thermoformed products, particularly when multiple polymer layers are used for durability, which is hindering the growth of the thermoform packaging market. The Ellen MacArthur Foundation has stressed that over 30% of plastic packaging globally cannot be effectively recycled due to its material complexity. Multi-layer thermoform structures combining PET, PE, and barrier coatings often evade current recycling infrastructure, ending up in landfills. This lack of recyclability not only tarnishes industry reputation but also increases compliance costs for producers in regions enforcing extended producer responsibility (EPR) schemes. Addressing recyclability remains a technical and regulatory hurdle for the industry.

Rising Competition from Alternative Packaging

Thermoform packaging faces competition from flexible packaging and molded fiber solutions that are often considered more sustainable. As per the U.S. Environmental Protection Agency, paper and paperboard packaging accounted for 31.9 million tonnes of municipal solid waste in 2018, indicating their extensive use as alternatives to plastics. This competitive shift could erode thermoform packaging’s dominance unless manufacturers invest in hybrid designs that combine functionality with sustainability credentials.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Material Type, Product Type, Application, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | Asia Pacific North America Europe Latin America Middle East & Africa |

| Market Leaders Profiled | Amcor plc, Sonoco Products Company, Pactiv LLC, Anchor Packaging Inc., Berry Global, Inc., Constantia Flexibles Group GmbH, Placon Corporation, Dart Container Corporation, Display Pack, Inc., Tray-Pak Corporation |

SEGMENTAL ANALYSIS

By Material Insights

The plastic segment was the largest and held 62.53% of the thermoform packaging market share in 2025, with the plastic’s exceptional barrier properties by protecting against moisture, oxygen, and light, and its lightweight nature, which cuts transportation costs and carbon emissions, especially for food packaging. Plastic materials like rPET trays and PP cups continue to outperform due to high barrier performance against spoilage and contaminants, along with affordability and ease of manufacturing. These strengths help secure over 60% of revenue share, reinforcing plastic’s hold on the market.

The bio-based polymers (e.g., PLA blends) segment is likely to grow with an expected CAGR of 8.46% during the forecast period, as the major foodservice chains adopt low-carbon packaging for sustainability goals.

By Type Insights

The blister packaging segment held 40.3% of the thermoform packaging market share in 2025, with the pharmaceutical demand unit-dose blisters offering tamper resistance, dosage accuracy, and product protection by making it essential in drug packaging. The design of blister packaging provides individual protection, easy handling, and shelf-safe storage that makes it uniquely suited for pharmaceuticals.

The blister packaging segment is likely to grow with a CAGR of 4.3% in the coming years, with the versatility across industries, visibility in retail, and robust protection features. Its transparent design, security aspects, and flexibility support growth across pharmaceuticals, electronics, and consumer goods.

By Heat Seal Coating Insights

The water-based segment was the largest and held 40.1% of the thermoform packaging market share in 2025, with the ability to form excellent bonds, such as between polyethylene films and corrugated surfaces, while minimizing sticking issues, making them highly efficient in thermoforming operations.

The solvent-based segment is likely to grow with an expected CAGR of 6.4% the n coming years, with a rapid increase in popularity due to superior water and grease resistance, strong adhesion, and performance across a varied temperature range for products needing durable seals. Their robustness makes them ideal for demanding packaging such as blister and food trays.

By End-Use Industry Insights

The food & beverage segment accounted in holding 50.21% of the thermoform packaging market share in 2025, with the increasing demand for ready meals, snacks, and on-the-go food items packaged in thermoformed materials that preserve freshness and convenience. Thermoform packaging in this sector offers lightweight, protective, and shelf-fresh solutions tailored to consumer demand for ready or fresh meals. These benefits, combined with growing quick-serve trends, establish food & beverage as the sector driving over half of market revenue.

The pharmaceuticals segment is growing lucratively with an expected CAGR of 9.31% in the coming years. Growth is powered by increasing prevalence of chronic conditions, biologics, diagnostics, and self-administered therapies, areas where thermoform packaging ensures unit-dose precision, sterility, and protection.

REGIONAL ANALYSIS

Asia-Pacific Market Analysis

Asia-Pacific was the top performer of the thermoform packaging market by capturing 45.3% of the share in 202,4, owing to the rising population, urbanization, disposable incomes, and booming packaged goods demand in markets like China and India.

North America Market Analysis

North America was positioned second by holding 25.3% the thermoform packaging market share in 2025, with advanced manufacturing, tech-driven packaging innovation, and robust food and healthcare industries demanding high-performance thermoform packaging.

Europe Market Analysis

Europe's market is growing with prominent growth opportunities in the coming years, with growth driven by a sustainability push, regulatory frameworks (e.g., eco-labeling), and strong food and pharma sectors adopting recyclable and efficient packaging. Latin America, the Middle East, and the Caribbean are expected to have significant growth in the thermoform packaging market in the coming years.

COMPETITIVE LANDSCAPE

The competitive landscape of the thermoforming packaging market is marked by technological differentiation, regulatory adaptation, and increasing pressure to balance performance with environmental responsibility. While large multinational converters dominate in terms of innovation and global reach, regional players are gaining ground by offering cost-effective, locally tailored solutions. Competition is less price-driven and more focused on material sustainability, supply chain reliability, and compliance with evolving food safety and environmental standards. The shift toward recyclable, compostable, and mono-material structures is reshaping product portfolios, with companies investing in R&D to overcome the technical limitations of bio-based resins. Strategic alliances with retailers and e-commerce platforms are becoming key differentiators.

KEY MARKET PLAYERS

Some of the major companies in the global thermoform packaging market are:

- Amcor plc

- Sonoco Products Company

- Pactiv LLC

- Anchor Packaging Inc.

- Berry Global, Inc

- Constantia Flexibles Group GmbH

- Placon Corporation

- Dart Container Corporation

- Display Pack, Inc.

- Tray-Pak Corporation

TOP LEADING PLAYERS IN THE MARKET

- Huhtamäki Oyj is a global leader in sustainable food packaging, with a strong and expanding footprint across the Asia Pacific region. The company has strategically invested in thermoforming operations in India, China, and Southeast Asia to meet rising demand for hygienic, ready-to-eat meal packaging. In 2023, Huhtamäki launched a fully recyclable PET thermoformed tray under its AWARÉ™ brand in India, designed for e-grocery platforms and urban retail chains. It also inaugurated a new production facility in Ho Chi Minh City, focusing on fiber-based and plastic thermoformed solutions for foodservice clients. The company’s collaboration with Singapore-based GrabFood to develop compostable meal containers has reinforced its position as an innovation driver.

- Amcor plc plays a pivotal role in advancing high-performance thermoformed packaging for food, pharmaceutical, and personal care applications across the Asia Pacific. The company has strengthened its regional presence through localized R&D centers in Japan and Australia, focusing on lightweighting, barrier enhancement, and recyclability. In 2025, Amcor introduced a mono-material PP thermoformed tray in South Korea that is fully compatible with existing recycling streams, developed in partnership with major retailers like Shinsegae. It also expanded its medical thermoforming capabilities in Malaysia to supply sterile packaging for diagnostic kits and surgical instruments to ASEAN healthcare providers. Amcor’s integration of digital printing on thermoformed lids enables brand customization and anti-counterfeiting features, meeting evolving consumer and regulatory demands.

- Pactiv Evergreen Inc. has established a significant presence in the Asia Pacific thermoforming sector by introducing advanced plastic and fiber-based packaging solutions tailored to regional consumption patterns. The company has focused on expanding its export capabilities from North America while building strategic partnerships with food processors and retailers in Japan and Australia. In 2023, Pactiv Evergreen collaborated with a leading Australian dairy producer to launch a curd-compatible thermoformed cup with enhanced moisture resistance, extending shelf life by 40%. It also introduced a line of microwave-safe, recyclable PET trays for ready-meal providers in Taiwan, addressing the growing demand for convenience foods. By leveraging its expertise in material science and cold-chain packaging, the company is addressing performance challenges in tropical climates and high-humidity environments.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the thermoforming packaging market are focusing on material innovation, regional capacity expansion, sustainability certification, strategic partnerships with brand owners, and integration of smart packaging technologies to strengthen their competitive positioning. Companies are investing heavily in mono-material and bio-based resins to comply with tightening environmental regulations across Europe and Asia. Expansion into high-growth emerging markets is being achieved through localized manufacturing and technical support centers. Collaborations with retailers and foodservice chains enable co-development of application-specific packaging that enhances shelf appeal and logistics efficiency. Firms are also adopting digital printing and traceability features such as QR codes and time-temperature indicators to meet consumer demand for transparency.

MARKET SEGMENTATION

This research report on the global thermoform packaging market is segmented and sub-segmented into the following categories.

By Material

- Plastic

- Aluminium

- Paper & Paperboard

By Type

- Clamshell

- Blister

- Skin

- Others

By Heat Seal Coating Insights

- Water-Based

- Solvent-Based

- Hot Melt

By End-Use Industry Insights

- Food & Beverage

- Electronics

- Personal Care & Cosmetics

- Pharmaceuticals

- Others

By Region

- North America

- Europe

- Latin America

- Asia Pacific

- Middle East & Africa

Frequently Asked Questions

1. Why are sustainability trends important for the Global Thermoforming Packaging Market?

Sustainability plays a significant role in the Global Thermoform Packaging Market, with increasing focus on recyclable and biodegradable materials. Environmental regulations and consumer demand for eco-friendly packaging are key growth drivers, prompting industry players to offer greener solutions and reduce plastic waste.

2. How does the Global Thermoforming Packaging Market address plastic waste concerns?

The market addresses plastic waste by emphasizing the use of recyclable materials, encouraging government regulations on single-use plastics, and developing packaging that is easier to recycle or compost.

3. What are the major end-user industries in the Global Thermoform Packaging Market?

The food and beverage industry represents the largest end-user segment in the Global Thermoform Packaging Market, followed by pharmaceuticals, consumer goods, electronics, and healthcare. These sectors demand packaging that ensures safety, product visibility, and extended shelf life.

4. How does customization impact the Global Thermoform Packaging Market?

Customization is a key selling point for the Global Thermoform Packaging Market, allowing manufacturers to design packaging tailored to specific product needs. This includes creating packaging in unique shapes, sizes, and designs for enhanced branding and functionality.

5. What are the main types of packaging in the Global Thermoform Packaging Market?

Common types of packaging in the Global Thermoform Packaging Market are blister packaging, clamshells, trays, and skin packaging. Each type serves different products, providing tamper-evidence, protection, and ease of handling.

6. What drives technological innovation in the Global Thermoform Packaging Market?

Technological advancements in automation, design software, and eco-friendly materials drive change in the Global Thermoforming Packaging Market. These innovations increase production efficiency, reduce costs, and support the growing need for sustainability.

7. Which materials dominate the Global Thermoforming Packaging Market?

The predominant materials in the Global Thermoform Packaging Market include PET (polyethylene terephthalate), PVC (polyvinyl chloride), and polystyrene. Innovations in materials are leading to more recyclable and environmentally safe options, aligning with global sustainability goals

8. How do raw material prices affect the Global Thermoform Packaging Market?

Fluctuations in raw material prices, especially plastics, directly impact costs within the Global Thermoforming Packaging Market. Price changes can affect profit margins, product pricing, and market competitiveness.

9. What are the key regional trends in the Global Thermoform Packaging Market?

The Global Thermoform Packaging Market is seeing rapid growth in Asia-Pacific due to expanding urbanization, rising packaged food consumption, and industrial development. North America and Europe also show robust demand owing to stricter sustainability standards.

10. Why is food safety a priority in the Global Thermoforming Packaging Market?

Food safety is prioritized in the Global Thermoforming Packaging Market because packaging technologies like tamper-evidence and extended shelf life are critical for protecting food products during distribution and storage

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com