UK Bus Market Size, Share, Trends & Growth Forecast Report By Type, Fuel Type, Seat Capacity, and Country – Industry Analysis and Forecast, 2026 to 2034

Market Size, 2025

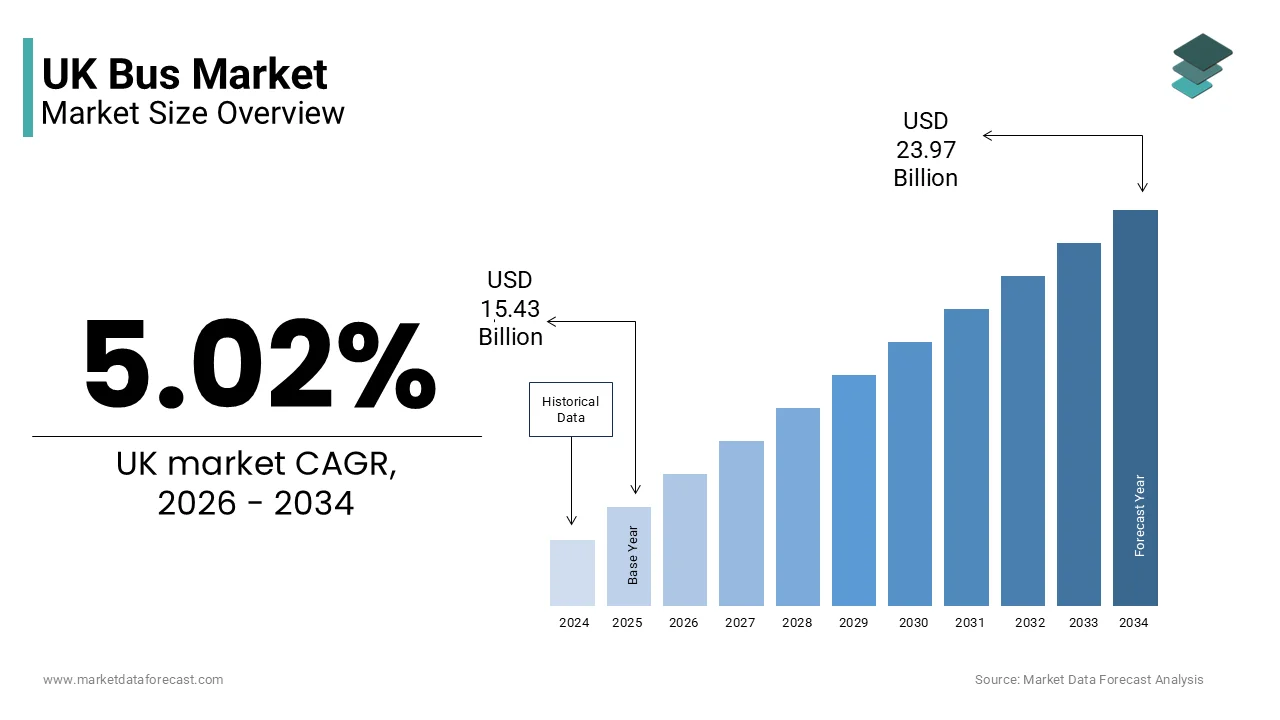

$15.43 BnMarket Estimate, 2026

$16.20 BnMarket Forecast, 2034

$23.97 BnCAGR, 2026–2034

5.02%UK Bus Market Report Summary

The UK bus market was valued at USD 15.43 billion in 2025, is estimated to reach USD 16.20 billion in 2026, and is projected to reach USD 23.97 billion by 2034, growing at a CAGR of 5.02% during the forecast period. Market growth is driven by increasing urbanization, rising public transportation demand, government investments in sustainable mobility solutions, and ongoing efforts to reduce traffic congestion and carbon emissions. The modernization of public transport infrastructure, fleet electrification initiatives, and smart mobility technologies are further supporting market expansion across the United Kingdom.

Key Market Trends

- Growing demand for affordable and sustainable public transportation is driving market growth.

- Increasing government investments in low emission and zero emission bus fleets are boosting market expansion.

- Rising urban population and daily commuting requirements are supporting industry development.

- Expansion of smart ticketing and connected transport solutions is enhancing passenger convenience.

- Innovation in electric and hydrogen powered buses is influencing market advancement.

Segmental Insights

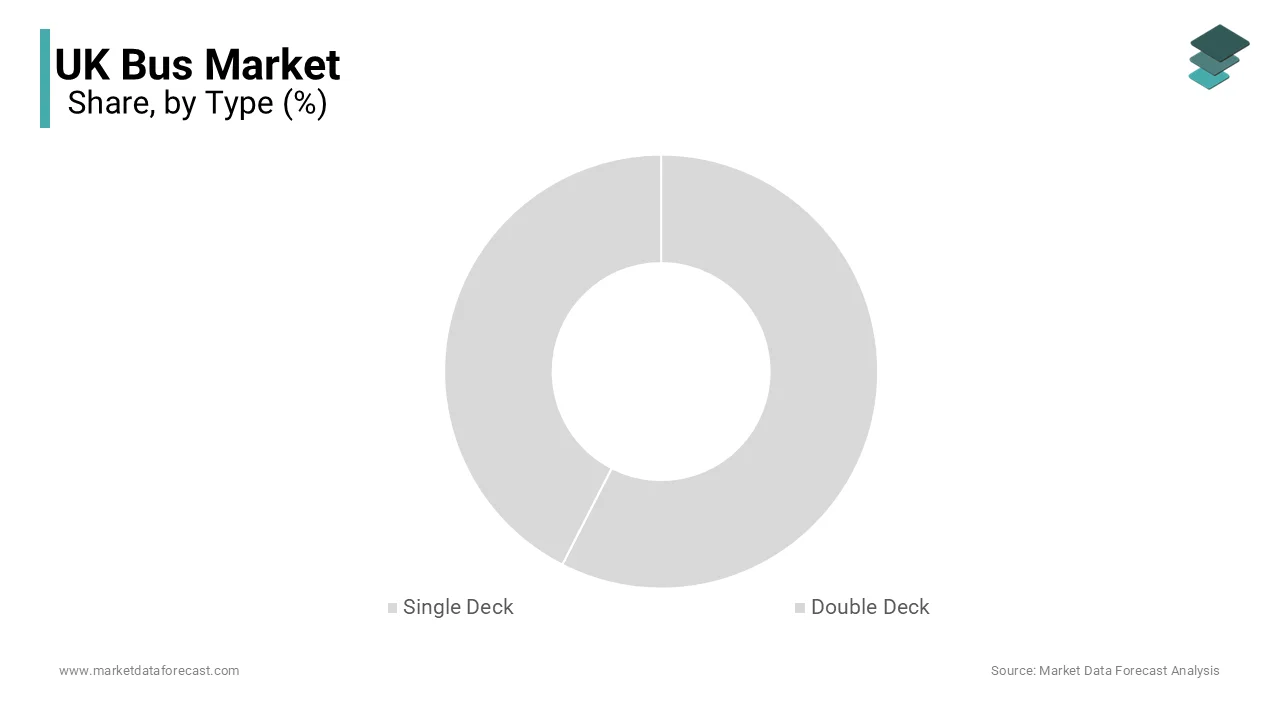

- Based on type, the single deck buses segment accounted for 64.3% of the UK bus market share in 2025. This dominance is attributed to their operational flexibility, lower acquisition costs, and suitability for a wide range of urban and suburban routes.

- Based on fuel type, the diesel powered buses segment held 71.3% of the UK market share in 2025, supported by the extensive existing fleet infrastructure and operational familiarity among transport operators.

- Based on seat capacity, the 31 to 50 seats segment accounted for 44.7% of the UK bus market share in 2025, driven by its balance between passenger capacity, operating efficiency, and route versatility.

Regional Insights

- England represents the largest regional market within the United Kingdom bus industry. Major urban centers such as London, Manchester, and Birmingham generate significant daily passenger traffic due to high population density and extensive public transportation networks. The region continues to benefit from substantial investments in transit infrastructure, fleet modernization, and sustainable mobility initiatives.

Competitive Landscape

The UK bus market is highly competitive, with operators and manufacturers focusing on fleet modernization, sustainability initiatives, passenger experience enhancement, and digital transportation solutions to strengthen their market position. Companies continue to invest in electric buses, intelligent fleet management systems, and low emission transportation technologies. Key companies operating in the UK bus market include FirstGroup, Stagecoach Group, Arriva Group, Go Ahead Group, National Express Group, Wrightbus, Alexander Dennis, McGill's Group, Transdev UK, and ComfortDelGro UK Bus.

UK Bus Market Size

The UK bus market size was valued at USD 15.43 billion in 2025, and is projected to reach USD 23.97 billion by 2034 from USD 16.20 billion in 2026, growing at a CAGR of 5.02%.

The UK bus market constitutes a critical pillar of the nation's public transport infrastructure, facilitating daily mobility for millions of citizens across urban centers and rural communities. This sector encompasses local service operations, intercity coaches, and specialized community transport solutions that connect diverse geographical regions. The network serves as an essential lifeline for individuals without access to private vehicles, including students, elderly populations, and low income households. As per the Department for Transport, bus journeys in Great Britain totalled approximately 4.1 billion trips in recent pre pandemic years, demonstrating the substantial reliance on this mode of transport. The industry operates under a complex regulatory framework involving local authorities, private operators, and government bodies that coordinate routes, fares, and service standards. Urban areas such as London maintain distinct operational models with integrated ticketing systems and high frequency services, while other regions rely more heavily on commercially viable routes supplemented by subsidized connections. The physical infrastructure supporting this market includes thousands of bus stops, dedicated lanes in major cities, and maintenance depots spread across the country. Environmental considerations have increasingly influenced fleet composition, with operators transitioning toward cleaner technologies. The social significance of bus services extends beyond mere transportation, contributing to community cohesion and economic accessibility by linking residential areas with employment hubs, educational institutions, and healthcare facilities throughout the UK.

MARKET DRIVERS

Rising Urban Population Density Drives Bus Service Demand

The growth of the UK bus market is primarily driven by the accelerating concentration of residents within UK urban centers creates substantial pressure on existing transport infrastructure, thereby amplifying demand for efficient bus services. According to the Office for National Statistics, approximately 84% of the UK population resides in urban areas, which is a figure that continues to grow as migration from rural locations persists. This demographic shift places immense strain on road networks, making private vehicle ownership increasingly impractical due to congestion and limited parking availability. Cities like Manchester and Birmingham have witnessed population increases of 10% over the past decade, necessitating expanded public transit options to maintain mobility standards. Bus services offer a scalable solution capable of transporting large passenger volumes through confined urban spaces without requiring extensive new infrastructure development. Local authorities recognize that each full bus can remove up to 40 private cars from congested streets, directly addressing traffic management challenges. The compact nature of British cities, with average commuting distances of 7 miles, aligns perfectly with bus route optimization strategies. Furthermore, younger demographics aged 16 to 24 show higher propensity for public transport usage, with 35% relying primarily on buses for daily commutes as per transport surveys. This generational preference combined with urban densification creates sustained demand growth. Municipal planning documents increasingly prioritize bus priority measures including dedicated lanes and signal prioritization to enhance service reliability. The economic imperative of connecting workers to employment centers efficiently further reinforces investment in bus network expansion and frequency improvements across densely populated metropolitan regions.

Government Environmental Policies Accelerate Fleet Electrification

Stringent environmental regulations implemented by the UK government compel bus operators to transition toward zero emission vehicles, which is fundamentally reshaping fleet composition and operational strategies and further boosting the UK bus market expansion. The Department for Environment Food and Rural Affairs has mandated that all new buses purchased for local services must be zero emission capable by 2035, creating an urgent timeline for infrastructure and vehicle procurement investments. For instance, electric buses constitute only 8% of the total national fleet, highlighting the massive scale of transformation required over the coming decade. London leads this transition with over 1,000 electric buses already in operation, which is representing nearly 15% of its total fleet as per Transport for London statistics. The Clean Air Strategy published by the government identifies transport as responsible for 27% of domestic nitrogen oxide emissions, with buses being significant contributors in urban environments. Financial incentives support this transition, including the Zero Emission Bus Regional Areas scheme which allocated 270 million pounds in funding during recent budget cycles. Operators face technical challenges regarding charging infrastructure deployment, with typical electric buses requiring 3 to 4 hours for complete battery replenishment using standard depot chargers. However, the operational benefits include reduced maintenance costs estimated at 30% lower than diesel equivalents due to fewer moving parts. Noise pollution reduction represents another advantage, with electric buses operating at decibel levels 10 times quieter than traditional diesel engines. These environmental mandates coupled with financial support mechanisms create powerful momentum for fleet modernization across the UK bus sector.

MARKET RESTRAINTS

Chronic Workforce Shortages Constrain Service Expansion

The UK bus market confronts severe staffing deficits that significantly impede service reliability and network expansion capabilities. According to the Confederation of Passenger Transport, the sector experiences an annual shortage of approximately 3,000 qualified bus drivers, representing nearly 10% of the total workforce requirement. This deficit stems from multiple structural issues including an aging driver demographic with 45% of current operators aged above 55 years, leading to substantial retirement waves without adequate replacement recruitment. The training pipeline remains insufficient, with only 2,500 new drivers obtaining licenses annually against industry needs of 5,500 replacements and expansions. Wage competitiveness presents another challenge, as bus driver salaries average 28,000 pounds per year compared to 32,000 pounds for comparable logistics positions, making recruitment difficult in tight labor markets. The complexity of obtaining a Passenger Carrying Vehicle license requires significant time investment of 8 to 12 weeks and costs exceeding 1,000 pounds, creating barriers for potential entrants. Recent industrial actions have exacerbated these issues, with several major operators reporting 15% service reductions due to unavailable staff during peak periods. Rural areas suffer disproportionately, where 20% of scheduled services experience cancellations monthly due to driver unavailability as per regional transport authority reports. The psychological demands of the role including irregular hours and passenger interaction contribute to high turnover rates of 18% annually. Addressing this crisis requires comprehensive strategies encompassing improved compensation structures, streamlined training pathways, and enhanced working conditions to attract younger demographics into the profession and stabilize service delivery across the national network.

Infrastructure Degradation Impedes Operational Efficiency

Deteriorating road infrastructure and inadequate bus priority measures substantially undermine service reliability and passenger satisfaction across the UK network, which is further hampering the UK bus market growth. The Local Government Association estimates that 12% of local roads require immediate repair, with potholes and surface damage causing increased vehicle maintenance costs averaging 1,200 pounds annually per bus operator. Dedicated bus lanes are critical for maintaining schedule adherence in congested urban environments that cover only 35% of major routes in cities outside London. This insufficient coverage forces buses into general traffic flows, resulting in average journey time increases of 25% during peak hours compared to off peak periods. Traffic signal priority systems, which allow buses to extend green lights or reduce red light waiting times, operate at merely 40% of intersections in medium sized cities. The financial burden of infrastructure maintenance falls unevenly across regions, with northern councils spending 30% less per capita on transport infrastructure than southern counterparts as per treasury allocation data. Bridge weight restrictions affect 8% of potential bus routes, forcing lengthy detours that increase operational costs and reduce service attractiveness. Winter weather exacerbates these issues, with snow and ice causing average delays of 15 minutes per journey during adverse conditions. Passenger perception surveys indicate that 60% of occasional users cite unreliability as their primary concern, directly linked to infrastructure limitations. Investment gaps remain substantial, with the Institution of Civil Engineers estimating a 12 billion pound backlog in local transport infrastructure repairs nationwide. Without systematic upgrades to road surfaces, junction designs, and priority systems, bus services will struggle to achieve the reliability standards necessary to attract and retain passengers in competitive transport markets.

MARKET OPPORTUNITIES

Zero Emission Technology Adoption Creates Market Expansion

The mandatory transition toward zero emission buses presents substantial commercial opportunities for manufacturers, technology providers, and innovative operators within the UK market. The Office for Zero Emission Vehicles projects that achieving the 2035 target will require investment exceeding 3 billion pounds in new vehicles and supporting charging infrastructure. This transformation creates demand for approximately 8,000 electric buses over the next decade, representing a complete fleet renewal cycle for most operators. Battery technology advancements have improved energy density by 40% since 2020, enabling ranges of 200 miles on single charges sufficient for most daily urban routes. Charging infrastructure deployment offers parallel opportunities, with each depot requiring investments of 500,000 to 2 million pounds depending on fleet size and charging speed requirements. Hydrogen fuel cell buses represent an alternative pathway, particularly suited for longer intercity routes where battery weight becomes prohibitive. The UK currently operates 50 hydrogen buses with plans to expand to 300 units by 2025 as per the Hydrogen Transport Hub initiatives. Maintenance ecosystem development creates additional revenue streams, as electric buses require specialized technicians trained in high voltage systems, with certification programs commanding premium pricing. Energy management software solutions enable operators to optimize charging schedules based on electricity tariff fluctuations, potentially reducing energy costs by 20%. Second life battery applications for grid storage present emerging opportunities as bus batteries reach end of vehicular use after 8 to 10 years. Supply chain localization efforts aim to establish domestic battery production facilities, with three major manufacturing plants planned offering 5,000 jobs. This technological revolution fundamentally restructures the industry value chain while delivering environmental compliance and long term operational savings.

Digital Integration Enhances Passenger Experience and Efficiency

Advanced digital technologies offer prominent opportunities to improve service attractiveness, operational efficiency, and data driven decision making within the UK bus sector. Contactless payment adoption has reached 85% of transactions in major urban networks, reducing boarding times by 15 seconds per passenger according to operator performance metrics. Real time tracking applications used by 60% of regular passengers provide accurate arrival predictions within 2 minute margins, significantly improving journey planning confidence. Dynamic routing algorithms powered by artificial intelligence can adjust service patterns based on demand fluctuations, with pilot programs demonstrating 12% efficiency improvements in vehicle utilization. Mobile ticketing platforms eliminate physical card requirements, with contactless bank cards now accepted on 95% of services nationwide. Data analytics enable predictive maintenance scheduling, reducing unexpected breakdowns by 30% through monitoring of vehicle telemetry including battery health, brake wear, and engine performance indicators. Integrated mobility applications combining bus services with rail, cycling, and ride sharing options appeal to multimodal travelers, with 40% of urban commuters using multiple transport modes weekly. Smart bus stops equipped with digital displays and emergency communication systems enhance safety and information accessibility, particularly benefiting elderly and disabled passengers. Open data initiatives allow third party developers to create innovative journey planning tools, expanding service visibility beyond traditional channels. Automation prospects include autonomous shuttle services for first mile last mile connections, with trials ongoing in five UK cities. These digital enhancements collectively modernize the passenger experience while providing operators with granular insights for service optimization and cost management in increasingly competitive transport environments.

MARKET CHALLENGES

Funding Uncertainty Threatens Long Term Viability

Inconsistent government funding commitments create substantial financial instability for bus operators, particularly those dependent on subsidized socially necessary routes, which is a major challenge to the UK market. The Department for Transport reduced direct bus service support grants by 20% in real terms between 2010 and 2020, forcing local authorities to make difficult decisions about service retention. Currently, 30% of rural bus routes operate below commercial viability thresholds, requiring public subsidies averaging 15,000 pounds per route annually to maintain minimum service levels. Budget pressures on local councils have resulted in 1,500 bus service withdrawals or reductions since 2010, disproportionately affecting smaller towns and villages as per Campaign for Better Transport analysis. The tendering process for supported services often prioritizes lowest cost bids over quality considerations, leading to service degradation including older vehicles and reduced frequencies. Fare revenue covers only 65% of operational costs on average, with the remainder dependent on uncertain public funding sources subject to political cycles and fiscal constraints. Inflationary pressures have increased operating costs by 18% over two years while fare increases remain politically sensitive and capped in many regions. The Bus Service Improvement Plans launched in 2021 provided 3 billion pounds in funding, but distribution mechanisms favor larger urban areas leaving rural operators with diminished resources. Long term contract uncertainty discourages private investment in fleet renewal and infrastructure, as operators cannot guarantee revenue streams beyond short term agreements. This funding volatility undermines strategic planning capabilities and threatens the social contract ensuring basic mobility access for non-driving populations across the UK geography.

Competition From Alternative Transport Modes Intensifies Pressure

The UK bus market faces escalating competition from diverse alternative transport options that capture passenger segments traditionally reliant on bus services. Ride hailing platforms have grown substantially with 4.5 million active users monthly, offering door to door convenience that appeals to time sensitive travelers despite higher costs. Cycling infrastructure investments have created safe urban routes, with bicycle commuting increasing by 43% in major cities over five years according to Department for Transport statistics. Electric scooter rentals launched in multiple cities provide flexible short distance mobility options attracting younger demographics who previously used buses for brief journeys. Remote work adoption has permanently altered commuting patterns, with 35% of office workers now hybrid working reducing peak hour bus demand by estimated 20% in business districts. Car sharing schemes membership has reached 2 million users nationally, providing occasional vehicle access without ownership burdens. Intercity coach services compete directly with local bus networks on overlapping routes, offering faster journey times through limited stop patterns. The proliferation of personal electric vehicles including e bikes and e scooters addresses first mile last mile connectivity gaps that previously required bus connections. Rail service improvements including electrification and frequency enhancements on suburban routes attract passengers willing to pay premium fares for faster journeys. Price sensitivity remains acute among bus users, with 70% citing cost as primary selection factor, making them vulnerable to switching when alternatives offer perceived value advantages. Demographic shifts show declining bus usage among 18 to 34 age groups who prefer flexible on demand services over fixed route schedules. This fragmented competitive landscape requires bus operators to differentiate through reliability, coverage, and integrated ticketing while managing cost structures to remain attractive against increasingly sophisticated mobility alternatives.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.02% |

| Segments Covered | By Type, Fuel Type, Seat Capacity, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Market Leaders Profiled | FirstGroup, Stagecoach Group, Arriva Group, Go Ahead Group, National Express Group, Wrightbus, Alexander Dennis, McGill's Group, Transdev UK, and ComfortDelGro UK Bus |

SEGMENTAL ANALYSIS

By Type Insights

The single deck buses segment accounted for 64.3% of the UK market share in 2025. This dominance is primarily driven by their exceptional versatility in navigating diverse urban environments and suburban routes where infrastructure constraints limit larger vehicles. The compact design allows single deck buses to operate efficiently on narrow residential streets and through historic city centers with low bridges or tight turning circles. According to the Department for Transport, single deck vehicles perform over 70% of all local service journeys outside of London, highlighting their critical role in regional connectivity. Their lower acquisition cost compared to double deck alternatives makes them financially viable for operators serving lower density areas with moderate passenger demand. The average capacity of 40 to 50 seats aligns well with typical off peak ridership levels, ensuring optimal load factors and operational efficiency. Maintenance costs are also reduced due to simpler mechanical structures and easier access to engine components. Furthermore, the rise of electric single deck models has reinforced their market position, as battery weight penalties are less severe than in larger double deck configurations. Local authorities prefer single deck units for community transport schemes and school services, which represent a stable revenue stream for operators. The flexibility to deploy these vehicles across varied route types without significant infrastructure modifications sustains their leadership in the national fleet composition.

On the other hand, the double deck buses segment is estimated to witness a CAGR of 5.5% during the forecast period owing to the intensifying urban congestion and the urgent need to maximize passenger throughput without increasing road space usage. Major metropolitan areas including London, Manchester, and Birmingham are prioritizing double deck deployment to address capacity shortages on high frequency corridors. As per Transport for London data, double deck vehicles carry nearly 80% of all bus passengers in the capital, demonstrating their unmatched efficiency in dense urban settings. The introduction of new generation electric double deckers has removed previous environmental restrictions, allowing cities to expand these high capacity fleets while meeting zero emission targets. Operators benefit from superior revenue potential per vehicle mile, as a single double deck bus can replace two single deck units during peak hours. The psychological appeal of upper deck seating also attracts leisure travelers and tourists, enhancing brand visibility for operators. Government funding initiatives specifically targeting high capacity zero emission vehicles have accelerated procurement cycles, with over 500 new electric double deckers ordered in the past two years. The integration of advanced passenger counting systems enables dynamic scheduling, ensuring these large assets maintain high utilization rates. This combination of spatial efficiency, environmental compliance, and economic viability drives the robust expansion of the double deck segment.

By Fuel Type Insights

The diesel-powered buses segment held 71.3% of the UK market share in 2025. This sustained dominance is attributed to the mature refueling infrastructure, proven reliability, and lower upfront capital costs compared to emerging alternatives. The extensive network of diesel depots and supply chains ensures uninterrupted service delivery across remote rural areas where electric charging infrastructure remains underdeveloped. According to the Confederation of Passenger Transport, diesel vehicles still account for 90% of intercity and long distance coach operations due to their superior range capabilities exceeding 400 miles per tank. The established maintenance ecosystem allows operators to service diesel engines with existing technical expertise, avoiding the substantial retraining investments required for electric or hydrogen technologies. While environmental pressures are mounting, the immediate transition barrier remains high for smaller operators who lack access to government grants for fleet renewal. Diesel engines also offer greater flexibility in varying weather conditions, with performance unaffected by extreme cold temperatures that can reduce electric battery efficiency by up to 30%. The residual value of diesel buses remains stronger in the secondary market, providing operators with better asset recovery options at end of life. Although policy mandates are shifting toward cleaner fuels, the sheer scale of the existing diesel fleet ensures it will remain the operational backbone of the UK bus network for the remainder of this decade.

On the other hand, the electric and hybrid buses segment is estimated to record a CAGR of 19.2% during the forecast period owing to the stringent government regulations mandating zero emission public transport fleets in major urban centers. The Zero Emission Bus Regional Areas scheme has injected over 270 million pounds into local authorities, accelerating the procurement of electric vehicles. London leads this transition with a target to achieve a fully zero emission bus fleet by 2034, having already deployed more than 1,000 electric buses as per Transport for London reports. Hybrid technology serves as a crucial transitional solution, offering 30% fuel savings and reduced emissions in stop start urban traffic without requiring complete charging infrastructure overhaul. The total cost of ownership for electric buses is becoming increasingly competitive, with energy costs 40% lower than diesel and maintenance expenses reduced by 30% due to fewer moving parts. Battery technology improvements have extended operational ranges to 200 miles, sufficient for most daily urban routes. Charging infrastructure investments are scaling rapidly, with depot based fast chargers reducing downtime significantly. Public perception favors clean transport, with surveys indicating 65% of passengers prefer electric buses due to quieter operation and improved air quality. These combined regulatory, economic, and social factors propel the rapid adoption of electric and hybrid technologies across the national bus network.

By Seat Capacity Insights

The 31 to 50 seats capacity segment led the market with 44.7% of the UK market share in 2025. This segment achieves dominance by offering an optimal balance between passenger capacity and operational flexibility, making it suitable for a wide variety of service types. These mid-sized vehicles are ideal for suburban routes, town center circulators, and interurban connections where demand is moderate but consistent. According to industry operational data, this capacity range delivers the highest average load factor of 60%, ensuring economic viability without the risk of running large empty vehicles. The physical dimensions allow access to narrower roads and smaller bus stops that cannot accommodate larger coaches, expanding network reach into residential neighbourhoods. Operators favor this segment for its versatility, as the same vehicle can serve peak hour commuter routes and off peak community services efficiently. The procurement cost is significantly lower than high capacity alternatives, reducing financial risk for private operators competing for local authority contracts. Maintenance requirements are standardized across major manufacturers, ensuring spare parts availability and competitive servicing rates. This segment also benefits from driver availability, as the licensing requirements are identical to larger buses but the driving experience is less stressful in congested areas. The adaptability of 31 to 50 seat buses to both commercial and subsidized service models cements their status as the workhorse of the UK bus market.

On the other end, the more than 50 seats capacity segment is expected to exhibit the fastest CAGR of 6.2% during the forecast period owing to the increasing urban population density and the strategic shift toward high frequency high capacity corridors in major cities. As urban centers expand, the economic imperative to move larger passenger volumes per vehicle mile becomes critical for maintaining service profitability and reducing congestion. Data from major metropolitan transport authorities indicates that routes utilizing high capacity buses have seen passenger number increases of 15% following fleet upgrades. The deployment of articulated and double deck vehicles in this category allows operators to meet peak demand surges without increasing service frequency, thereby optimizing driver utilization and reducing traffic impact. Government investment in bus priority infrastructure, including extended dedicated lanes and signal prioritization, enhances the operational efficiency of these larger vehicles. The tourism sector also contributes to this growth, with sightseeing services in cities like Edinburgh and York expanding their high capacity open top fleets to accommodate rising visitor numbers. Additionally, the transition to electric powertrains is more advanced in this segment, as larger chassis can accommodate heavier battery packs without compromising passenger space. The combination of urban densification, infrastructure improvements, and technological advancements drives the accelerated adoption of high capacity buses.

COUNTRY LEVEL ANALYSIS

England commands the largest share of the UK bus market. The region benefits from high population density in major urban conurbations such as London, Manchester, and Birmingham, which generate substantial daily transit demand. London alone contributes over 2 billion bus journeys annually, representing nearly half of all bus travel in Great Britain as per Department for Transport statistics. The devolved administrative structure allows local combined authorities to implement tailored Bus Service Improvement Plans, attracting significant central government funding. England has the most developed bus infrastructure, with extensive networks of dedicated lanes and real time information systems in major cities. The presence of large private operators and competitive tendering processes drives service innovation and efficiency gains. Rural areas in counties like Cornwall and Cumbria rely heavily on subsidized services, creating a mixed market model of commercial and supported routes. The concentration of manufacturing and maintenance facilities in the Midlands supports the operational ecosystem. England leads in electric bus adoption, with over 80% of new zero emission orders allocated to English operators. The robust regulatory framework enforced by the Traffic Commissioners ensures service standards and safety compliance. This combination of scale, infrastructure, and regulatory maturity solidifies England's dominant position in the national bus market landscape.

Scotland holds a significant position in the UK bus market, characterized by a unique blend of urban services in Glasgow and Edinburgh and extensive rural connectivity challenges. The region accounts for approximately 10% of total UK bus journeys, with a strong emphasis on social inclusion and remote area access. The Scottish Government implements distinct policy frameworks such as the National Concessionary Travel Scheme, which provides free bus travel for residents aged 60 and over, resulting in high usage rates among elderly demographics. According to Transport Scotland, bus patronage in Glasgow exceeds 100 million journeys annually, demonstrating strong urban demand. Rural routes are heavily subsidized through the Partnership Agreement Model, ensuring minimum service levels in Highlands and Islands communities where alternative transport is scarce. Scotland has been proactive in fleet decarbonization, with ambitious targets to achieve net zero emissions by 2035. The geographic dispersion of population requires flexible service models including demand responsive transport in low density areas. Investment in ferry bus integration enhances connectivity for island communities. The regulatory environment encourages community transport initiatives, with local cooperatives operating specialized services. Scotland's focus on equitable access and environmental sustainability distinguishes its market dynamics from other regions, maintaining a resilient and socially vital bus network despite lower overall population density.

Wales occupies a specialized niche in the UK bus market, focusing on integrating bus services with rail networks to enhance regional mobility. The region accounts for approximately 5% of total UK bus journeys, with key hubs in Cardiff and Swansea driving urban demand. The Welsh Government prioritizes public transport through its Llwybr Newydd strategy, aiming to increase bus passenger numbers by 25% by 2040. Cardiff Metro projects integrate bus rapid transit with rail electrification, creating seamless multimodal corridors. Rural Wales faces significant connectivity challenges, with community transport schemes playing a vital role in linking isolated villages to market towns. According to the Welsh Transport Statistics, bus services cover 95% of populated areas, though frequency remains low in remote locations. The introduction of regional franchising models is being explored to improve service coordination and accountability. Wales has made substantial progress in fleet electrification, with several zero emission zones planned in urban centers. The bilingual nature of the region influences customer communication strategies, with all signage and announcements provided in Welsh and English. Funding mechanisms emphasize social value outcomes, supporting services that connect residents to healthcare and education. The collaborative approach between local authorities and operators aims to create a cohesive and sustainable transport network tailored to Wales specific geographic and demographic needs.

Northern Ireland maintains a distinct position in the UK bus market, characterized by a state led operational model dominated by Translink, the public transport authority. The region accounts for a small but vital portion of UK bus activity, with services concentrated in Belfast and surrounding commuter belts. Unlike Great Britain, where private operators play a major role, Northern Ireland relies heavily on government owned entities for service delivery. According to the Department for Infrastructure, bus journeys in Northern Ireland totaled approximately 100 million annually pre pandemic, with steady recovery trends observed. The Geographic isolation and cross border dynamics with the Republic of Ireland influence route planning and service integration. Investment in modernizing the fleet includes introducing hybrid and electric buses to meet environmental targets. Rural connectivity remains a priority, with subsidized services ensuring access to essential services in counties like Fermanagh and Tyrone. The regulatory framework is centralized, allowing for coordinated planning and uniform fare structures across the region. Recent initiatives focus on improving bus priority measures in Belfast to reduce journey times and enhance reliability. The market faces challenges related to funding constraints and infrastructure aging, but strategic plans aim to increase public transport modal share. Northern Ireland unique operational structure provides stability and consistent service standards, distinguishing it from the deregulated markets in Great Britain.

COMPETITIVE LANDSCAPE

The UK bus market features a moderately consolidated competitive landscape dominated by a few large operators alongside numerous smaller regional companies. Major players compete intensely on service quality reliability and technological innovation rather than price alone due to regulated fare structures in many areas. The market dynamics vary significantly between London where franchising models ensure coordinated service and other regions where commercial competition prevails. Operators differentiate themselves through fleet modernization particularly the rapid adoption of electric and hybrid vehicles to meet environmental standards. Digital capabilities such as user friendly apps and contactless payment options have become essential competitive tools for attracting tech savvy passengers. Labor availability remains a critical differentiator as companies with stronger recruitment and retention strategies maintain more reliable services. Government funding allocations influence competitive positioning with operators securing contracts for subsidized routes gaining stable revenue streams. The threat from alternative transport modes including ride hailing and cycling forces bus companies to continuously enhance value propositions. Collaboration with local authorities through Bus Service Improvement Plans creates opportunities for joint investment in infrastructure and priority measures. This complex environment requires operators to balance financial sustainability with social obligations and environmental responsibilities effectively.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the UK bus market are

- FirstGroup

- Stagecoach Group

- Arriva Group

- Go Ahead Group

- National Express Group

- Wrightbus

- Alexander Dennis

- McGill's Group

- Transdev UK

- ComfortDelGro UK Bus

Top Players in the Market

- Stagecoach Group operates as one of the most prominent transport providers across the UK with extensive networks in Scotland and England. The company manages a diverse fleet serving urban centers and rural communities while prioritizing customer service excellence. Recent strategic initiatives include significant investments in zero emission vehicles to align with national environmental targets. Stagecoach has introduced numerous electric buses in cities like Perth and Oxford demonstrating commitment to sustainable mobility. The operator focuses on digital integration by enhancing mobile ticketing platforms and real time tracking applications for passengers. They actively collaborate with local authorities to improve service frequency and reliability through dedicated bus lanes. Staff training programs emphasize safety and customer engagement to enhance overall travel experience. Stagecoach continues to modernize depots with advanced charging infrastructure supporting their green transition goals. Their operational efficiency drives consistent service delivery despite challenging economic conditions and labor market pressures.

- FirstGroup maintains a substantial presence in the UK bus sector operating major services in London and other key regions. The company emphasizes innovation through its adoption of clean energy technologies and modern fleet renewal programs. FirstGroup has deployed hundreds of hydrogen and electric buses particularly in Aberdeen and Glasgow showcasing leadership in alternative fuel adoption. They prioritize passenger convenience by integrating contactless payment systems and open data feeds for journey planning apps. The operator works closely with municipal partners to deliver Bus Service Improvement Plans aimed at boosting ridership. FirstGroup invests heavily in driver recruitment and retention initiatives to address industry wide staffing shortages. Their focus on accessibility ensures vehicles meet high standards for disabled passengers including audio visual announcements. Strategic route optimizations help maintain commercial viability while serving essential community connections effectively.

- Go Ahead Group contributes significantly to the UK bus market through its operations in London and the North East. The company is renowned for managing complex urban networks with high frequency services and integrated ticketing solutions. Go Ahead has made considerable strides in electrification by introducing large fleets of electric double deckers in London boroughs. They leverage data analytics to optimize schedules and improve punctuality rates across their service areas. The operator engages in community outreach programs to understand local transport needs and tailor services accordingly. Go Ahead prioritizes sustainability by reducing carbon emissions through efficient driving techniques and eco friendly vehicle maintenance. They collaborate with technology providers to enhance passenger information systems and digital engagement tools. Investment in staff welfare and professional development remains central to their operational strategy ensuring high service standards. Their adaptive approach helps navigate regulatory changes and evolving passenger expectations in dynamic urban environments.

Major Strategies Used by Key Market Participants

Key players in the UK bus market primarily focus on fleet electrification to comply with stringent environmental regulations and reduce long term operational costs. Companies are aggressively procuring zero emission vehicles including battery electric and hydrogen fuel cell buses to meet government mandates. Digital transformation represents another critical strategy with operators investing in mobile ticketing real time tracking and data analytics platforms. These technologies enhance passenger experience and improve operational efficiency through better resource allocation. Workforce development initiatives aim to address chronic driver shortages by offering competitive wages improved training programs and better working conditions. Strategic partnerships with local authorities enable operators to secure funding for service improvements and infrastructure upgrades. Cost optimization measures include predictive maintenance using telematics to reduce breakdowns and extend vehicle lifecycles. Operators also diversify revenue streams by exploring advertising opportunities on buses and digital channels. Customer centric approaches focus on accessibility reliability and seamless multimodal integration to retain and attract passengers in a competitive transport landscape.

MARKET SEGMENTATION

This research report on the UK bus market is segmented and sub-segmented into the following categories.

By Type

- Single Deck

- Double Deck

By Fuel Type

- Diesel

- Electric and Hybrid

- Others

By Seat Capacity

- 15-30 Seats

- 31-50 Seats

- More than 50 Seats

Frequently Asked Questions

1. What is the UK bus market?

The UK bus market encompasses the manufacturing, sales, operation, and maintenance of buses used for public transportation, private services, and commercial applications across the country.

2. What factors are driving growth in the UK bus market?

Growth is driven by urbanization, increasing demand for public transportation, government investments in sustainable mobility, and the adoption of low emission vehicles.

3. How is electrification influencing the UK bus market?

The transition toward electric buses is accelerating as operators seek to reduce emissions, comply with environmental regulations, and lower operating costs.

4. What types of buses are commonly used in the UK?

Common bus types include single deck buses, double deck buses, mini buses, coaches, electric buses, and hybrid buses.

5. What role does government policy play in the UK bus market?

Government initiatives, funding programs, and emissions reduction targets support fleet modernization and the adoption of cleaner transportation technologies.

6. How are smart technologies transforming the UK bus market?

Technologies such as real time passenger information systems, contactless payments, telematics, and fleet management software are improving operational efficiency and passenger experience.

7. Which regions contribute significantly to bus demand in the UK?

Major urban areas and metropolitan regions contribute significantly due to high population density and extensive public transportation networks.

8. What challenges does the UK bus market face?

Challenges include rising operating costs, driver shortages, infrastructure limitations, fluctuating passenger demand, and regulatory compliance requirements.

9. What is the future outlook for the UK bus market?

The market is expected to grow steadily, supported by investments in zero emission buses, smart mobility solutions, public transport modernization, and increasing demand for sustainable transportation.

10. What role do private operators play in the UK bus market?

Private operators provide a substantial share of bus services, managing routes, fleets, and transportation solutions across urban and rural areas.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com