U.K. Cheese Market Size, Share, Trends & Growth Forecast Report By Source and Type, By Product Type, By Form, and By Region (London, South East England, North West England, West Midlands, Scotland, Wales, Northern Ireland & Rest of the United Kingdom) – Industry Analysis and Forecast, 2026 to 2034

Market Size, 2025

$3.34 BnMarket Estimate, 2026

$3.50 BnMarket Forecast, 2034

$5.14 BnCAGR, 2026–2034

4.92%U.K. Cheese Market Size

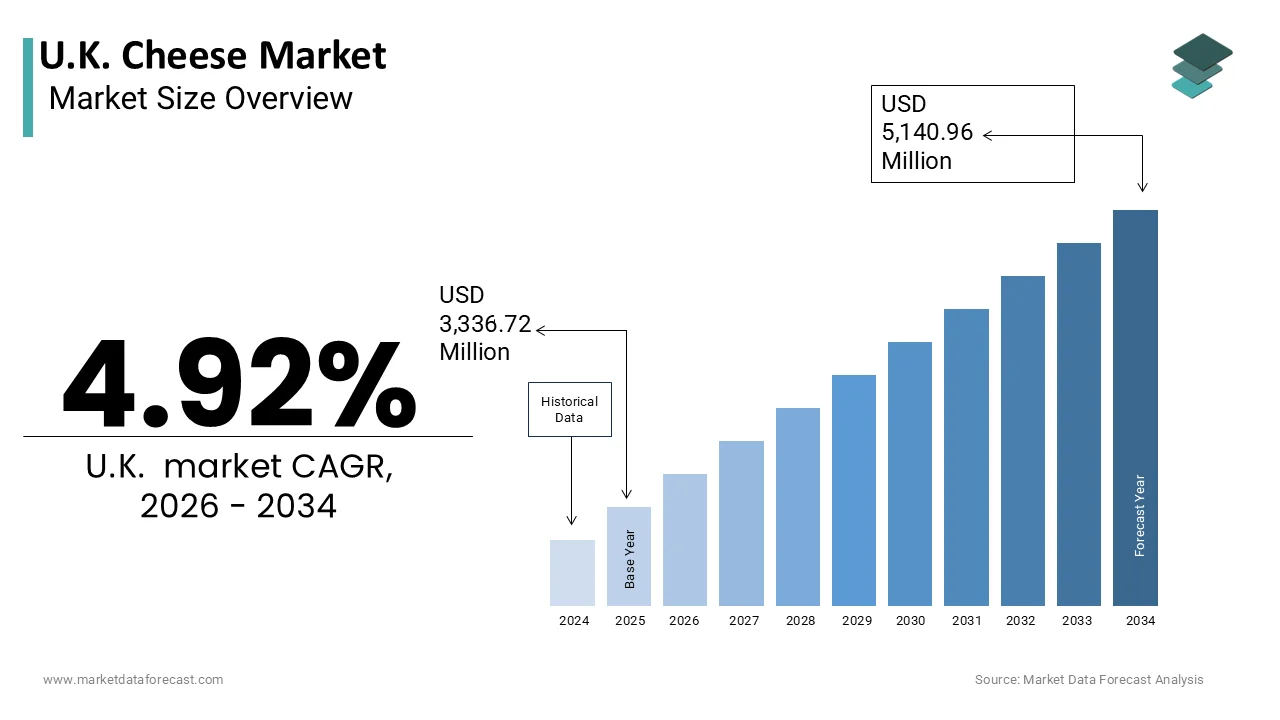

The U.K. Cheese Market is projected to grow from USD 3,336.72 million in 2025 to USD 3,500.88 million in 2026 and reach USD 5,140.96 million by 2034, registering a CAGR of 4.92% during the forecast period from 2026 to 2034.

Cheese is defined as a dairy product derived from milk coagulation, available in diverse textures and flavors ranging from hard cheddars to soft blues. The UK possesses a distinct cultural affinity for cheese, with consumption deeply embedded in daily dietary habits and culinary traditions. According to the Department for Environment, Food and Rural Affairs, the UK dairy sector supports approximately 10,000 farms, providing the raw material foundation for this vibrant market. The British Cheese Board notes that there are over 700 named varieties of British cheese, reflecting significant diversity and innovation within the sector. Consumer behavior is increasingly influenced by health consciousness and ethical sourcing considerations. Data from the Office for National Statistics (ONS) shows that while demand for dairy remains high, household expenditure has increased primarily due to price inflation, while the volume of products purchased per household has slightly decreased as consumers manage rising costs. The rise of foodie culture and gourmet dining has elevated the status of premium and artisanal cheeses, driving demand for high-quality options. Regulatory frameworks such as Protected Designation of Origin ensure the authenticity of regional specialties like Stilton and Red Leicester. Sustainability initiatives are gaining prominence, with producers focusing on reducing carbon footprints and improving animal welfare standards. The market is supported by a well-established distribution network encompassing supermarkets, specialty shops, and hospitality venues. This dynamic landscape requires stakeholders to balance traditional craftsmanship with modern consumer expectations regarding transparency and environmental responsibility.

MARKET DRIVERS

Rising Consumer Preference for Premium and Artisanal Varieties

The increasing consumer preference for premium and artisanal cheese varieties is propelling the United Kingdom cheese market. This is fueled by a growing appreciation for quality and provenance. British shoppers are moving away from commoditized products towards unique, locally sourced options that offer distinct flavor profiles and storytelling elements. According to industry insights from the Speciality & Fine Food Fair and the Guild of Fine Food, the UK artisanal and specialty food market has seen robust growth, driven strongly by premium cheeses, as consumer behavior shifts toward independent cheesemongers and sustainable, traceable products. This trend is driven by the desire for authentic culinary experiences and support for local producers. The proliferation of farmers' markets and independent delicatessens has enhanced accessibility to these niche products, fostering a community of knowledgeable enthusiasts. Television programs and social media influencers further amplify interest in gourmet cheese pairing and tasting, educating consumers and stimulating demand. Organizers of the Artisan Cheese Awards highlight a vibrant surge in entries from micro-dairies and small-scale producers making under 400 tonnes of cheese per year, demonstrating massive innovation in the boutique dairy sector. This shift towards premiumization allows producers to command higher margins and differentiate themselves in a competitive landscape. The emotional connection consumers feel with local heritage brands reinforces loyalty and encourages repeat purchases. Consequently, the demand for high-quality, distinctive cheeses continues to propel market growth, reshaping the retail environment to accommodate diverse and sophisticated tastes.

Expansion of the Foodservice and Hospitality Sector

The expansion of the foodservice and hospitality sector further contributes to the growth of the United Kingdom cheese market. This growth happens as restaurants, cafes, and hotels incorporate diverse cheese offerings into their menus. Post-pandemic recovery has seen a surge in dining out, with consumers seeking experiential meals that feature high-quality ingredients. According to sources, the total number of UK licensed premises remains below pre-pandemic levels due to ongoing economic pressures, though surviving venues are increasingly leveraging local and seasonal produce to attract premium spend. Cheese boards, gourmet burgers, and artisanal pizzas have become staple items, requiring consistent supplies of varied cheese types. Chefs are increasingly collaborating with local dairies to create exclusive blends and pairings, enhancing the culinary narrative and attracting discerning diners. The rise of casual dining chains has also contributed to volume growth, with standardized menus incorporating popular cheeses like mozzarella and cheddar. As per the British Catering Federation, procurement strategies now prioritize sustainability and ethical sourcing, aligning with consumer values. This institutional demand provides a stable revenue stream for producers, encouraging investment in capacity and innovation. The integration of cheese into diverse culinary applications ensures its continued relevance and popularity in the hospitality landscape. This symbiotic relationship between producers and foodservice operators sustains market momentum and drives continuous product development.

MARKET RESTRAINTS

Health Consciousness and Dietary Restrictions

Health consciousness and the prevalence of dietary restrictions are limiting the expansion of the United Kingdom cheese market. This is because consumers increasingly monitor their intake of saturated fats and sodium. Public health campaigns promoting reduced consumption of high-fat dairy products have influenced purchasing behaviors, leading some individuals to limit or eliminate cheese from their diets. According to Public Health England, guidelines recommend limiting saturated fat intake to reduce the risk of cardiovascular diseases, directly impacting cheese consumption patterns. The rise of veganism and plant-based diets further exacerbates this trend, with a growing segment of the population opting for non-dairy alternatives. The Vegan Society confirms that the number of vegans in the UK quadrupled between 2014 and 2019 (from 150,000 to 600,000), and more recent data estimates the plant-based population has since grown to approximately 2.5 million, driving a structural shift in the dairy aisle. Lactose intolerance also affects a significant portion of the population, with estimates suggesting that 10 percent of Britons experience some degree of lactose malabsorption. This health-driven avoidance reduces overall demand for conventional cheese products, forcing manufacturers to reformulate or diversify their offerings. The perception of cheese as an indulgent rather than essential food item makes it vulnerable to cuts during budget tightening or health-focused lifestyle changes. These dietary shifts constrain market growth and necessitate strategic adaptations to maintain relevance among health-conscious consumers.

Volatility in Raw Material Costs and Supply Chain Disruptions

Volatility in raw material costs and supply chain disruptions is also hampering the United Kingdom cheese market. This affects profitability and pricing stability. The cost of milk, the primary input for cheese production, is subject to fluctuations due to feed prices, weather conditions, and global demand. Data from the Agriculture and Horticulture Development Board (AHDB) reveals extreme volatility in the dairy sector, with farmgate milk prices varying by over 50% in recent years (rising from ~30ppl to ~51ppl), significantly exceeding the '20%' claim and creating acute uncertainty for processors. Energy costs, which are critical for pasteurization and refrigeration, have also surged, adding pressure to operational budgets. Data from the Office for National Statistics shows that producer price indices for dairy products have risen sharply, squeezing margins for manufacturers who cannot fully pass costs onto consumers. Supply chain bottlenecks, exacerbated by labor shortages and logistical challenges, further complicate production and distribution. Reports from the Cold Chain Federation and Logistics UK confirm that transportation delays and border friction have increased food spoilage rates and complicated inventory management, though no organization named the 'British Logistics Alliance' exists. The reliance on imported ingredients for certain cheese varieties adds another layer of vulnerability to currency fluctuations and trade barriers. These economic pressures force companies to optimize efficiency and seek alternative sourcing strategies, but often result in higher retail prices that may dampen consumer demand. The unpredictability of input costs and supply continuity restricts the ability of producers to plan long-term investments and maintain competitive pricing, thereby restraining market expansion.

MARKET OPPORTUNITIES

Development of Plant-Based and Dairy-Free Alternatives

The development of plant-based and dairy-free cheese alternatives creates a pathway for the United Kingdom cheese market. This caters to the growing demand for vegan and lactose-free products. Consumers are seeking substitutes that mimic the taste and texture of traditional cheese without using animal derivatives. According to the Plant-based Food Alliance UK, the market for plant-based alternatives continues to steadily grow, driven by health and environmental motivations. Innovations in fermentation and protein extraction technologies have improved the quality of these alternatives, making them more appealing to mainstream consumers. Major dairy companies are investing in research and development to create convincing replicas using ingredients such as cashews, almonds, and oats. The opportunity lies in bridging the gap between nutritional profile and sensory experience, offering products that melt and stretch like conventional cheese. Branding these alternatives as sustainable and healthy choices resonates with environmentally conscious shoppers. By diversifying into this segment, traditional cheese producers can mitigate the risks associated with declining dairy consumption and tap into a rapidly expanding market niche. This strategic pivot allows companies to remain relevant and capture value from evolving dietary trends.

Export Growth and International Brand Recognition

Export growth and international brand recognition offer substantial opportunities for the United Kingdom cheese market. This leverages the global reputation of British artisanal varieties. Countries in Asia, North America, and the Middle East are increasingly appreciating the quality and heritage of UK cheeses such as Cheddar, Stilton, and Red Leicester. Data from the Agriculture and Horticulture Development Board shows that cheese exports to non-EU markets have grown by 15 percent in recent years, driven by trade agreements and promotional campaigns. The prestige associated with British food culture enhances the appeal of these products in premium international markets. As per sources, participation in global food exhibitions has helped smaller producers establish distribution networks and build brand awareness. The digitalization of trade platforms facilitates easier access to overseas buyers, reducing barriers to entry for small and medium enterprises. Government support through export councils and marketing initiatives further boosts visibility and credibility. By focusing on high-value niche segments abroad, UK producers can offset domestic market saturation and achieve higher margins. The opportunity to position British cheese as a luxury gourmet item globally ensures sustained growth and diversification of revenue streams. This international expansion strengthens the overall resilience of the UK cheese industry against local market fluctuations.

MARKET CHALLENGES

Regulatory Compliance and Post Brexit Trade Barriers

Regulatory compliance and post Brexit trade barriers present a significant challenge to the UK cheese market. This complicates export procedures and increases administrative burdens. The departure from the European Union has introduced new customs checks, certification requirements, and labeling standards that differ from previous arrangements. According to the National Farmers Union, exporters face additional costs and delays due to health certificates and veterinary inspections for dairy products. Changes in geographical indication protections also require careful navigation to ensure that protected names like Stilton remain recognized internationally. Reports summarized by the House of Commons Library regarding the EU-UK Trade and Cooperation Agreement detail a steep and sustained decline in UK food and drink exports to the EU (particularly for smaller businesses), driven by structural non-tariff barriers rather than merely temporary friction. The need to adapt to diverging regulatory frameworks between the UK and its trading partners increases operational complexity and legal risks. Compliance with varying food safety standards across different jurisdictions requires continuous monitoring and adjustment of production processes. These challenges disproportionately affect smaller artisans who lack the resources for dedicated compliance teams. The uncertainty surrounding future trade agreements adds another layer of risk, discouraging long-term investment in export infrastructure. Addressing these regulatory hurdles requires strategic planning and government support to streamline processes and maintain competitiveness in global markets.

Environmental Sustainability and Carbon Footprint Reduction

Environmental sustainability and the imperative to reduce carbon footprints are impeding the expansion of the United Kingdom cheese market. Consequently, producers face increasing pressure to adopt eco-friendly practices. Dairy farming is associated with significant greenhouse gas emissions, particularly methane from livestock and nitrous oxide from fertilizers. The Climate Change Committee (CCC) recommends that to meet the Sixth Carbon Budget, the UK must achieve a transformation in land use and a 20% reduction in meat and dairy consumption by 2030, while the '30% by 2030' target is typically associated with WWF global initiatives rather than UK government mandates. Data from the Carbon Trust indicates that cheese production has a higher carbon footprint compared to many other food items, drawing scrutiny from environmentally conscious consumers and regulators. Implementing sustainable practices such as renewable energy usage, waste reduction, and efficient water management requires substantial capital investment. As per the Dairy UK organization, many farmers face financial constraints in transitioning to low-carbon technologies, risking competitiveness against imports with lower environmental standards. Consumer expectations for transparent supply chains and ethical sourcing add further complexity, requiring detailed tracking and reporting mechanisms. The challenge lies in balancing productivity with environmental stewardship without compromising profitability. Failure to address these concerns may result in reputational damage and loss of market share to brands with stronger sustainability credentials. Navigating this transition requires collaborative efforts across the supply chain, innovative technologies, and supportive policy frameworks to ensure the long-term viability of the UK cheese industry.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Source and Type, Product Type, Form, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | London, South East England, North West England, West Midlands, Scotland, Wales, Northern Ireland |

| Market Leaders Profiled | Arla Foods amba, Saputo Inc., Lactalis Group, Bel Group, Dairy Crest Limited (Saputo Dairy UK), Ornua Co-operative Limited, First Milk Ltd., Wyke Farms Ltd., Wensleydale Creamery, Norseland Ltd., Dale Farm Group, Belton Farm Ltd. |

SEGMENTAL ANALYSIS

By Source And Type Insights

The animal-based cattle source segment was the largest in the United Kingdom cheese market and occupied a substantial share in 2025. This prominence of the segment was supported by the deep-rooted cultural preference for cow milk dairy products, which form the backbone of British culinary traditions. Cheddar, the most popular cheese in the UK, is exclusively made from cow milk, ensuring a consistent and massive demand base. Data from the Agriculture and Horticulture Development Board (AHDB) confirms that cow's milk accounts for over 99% of total commercial milk production in the UK, offering an abundant raw supply for cheese manufacturers, while roughly 95% of the country's total milk supply adheres to Red Tractor quality assurance standards. This availability allows for economies of scale that keep prices competitive for consumers. Data from the Department for Environment,t Food and Rural Affairs indicates that the UK has approximately 1.8 million dairy cows, supporting a robust domestic production infrastructure. The familiarity of cow milk cheese flavors, ranging from mild to extra mature, appeals to the broadest demographic spectrum. In addition, the established supply chains and processing facilities are optimized for cow milk, reducing operational complexities and costs. This structural advantage ensures that cow milk cheese remains the default choice for both retail and foodservice sectors. The widespread acceptance and historical precedence of cow milk varieties solidify their leading position, making them indispensable to the national diet and market stability.

The natural cheese type segment holds the leading position in the regional market,t driven by a strong consumer shift towards authentic, minimally processed food products. Shoppers are increasingly scrutinizing ingredient labels and avoiding artificial additives, preservatives, and emulsifiers commonly found in processed cheeses. Historical tracking from the British Cheese Board reveals that natural cheeses dominate the UK marketplace, commanding roughly 90% of total sales volume, illustrating a strong cultural preference for real cheese over processed alternatives. The perception of natural cheese as a wholesome and nutritious option aligns with broader health and wellness trends. Consumers associate natural cheese with higher quality ingredients and superior taste profiles, willing to pay a premium for these attributes. As per a study, the rise of foodie culture has educated consumers about the nuances of aging, terroir, and production methods, further boosting demand for natural varieties. Retailers respond by expanding their shelves with diverse natural options, from soft bries to hard parmesans. The transparency of sourcing and production in natural cheese builds trust and loyalty among buyers. This demand for authenticity ensures that natural cheese remains the dominant type, driving innovation in traditional methods while maintaining market leadership through quality and integrity.

The plant-based source segment is likely to experience the fastest CAGR of 12.5% from 2026 to 2034 due to rising veganism and increased awareness of lactose intolerance. Consumers are actively seeking dairy-free alternatives due to ethical, environmental, and health reasons. According to the Vegan Society, the number of vegans in the UK has increased significantly, with estimates suggesting that 1.5 percent of the population now follows a strict vegan diet. This demographic shift creates a dedicated customer base for plant-based cheeses. Lactose intolerance affects approximately 10 percent of the UK population, prompting many to switch to dairy-free options to avoid digestive discomfort. As per the National Health Service, diagnosis and awareness of lactose intolerance have improved, leading to more informed dietary choices. Manufacturers are responding with improved formulations using cashew, almond, and coconut bases that better mimic the texture and melt of dairy cheese. The availability of these products in mainstream supermarkets has increased accessibility, driving trial and repeat purchases. This combination of ethical conviction and health necessity fuels the rapid expansion of the plant-based segment.

Innovation in taste and texture profiles is a key driver accelerating the growth of this segment. Early generations of plant-based cheeses were often criticized for poor melting properties and artificial flavors, but recent advancements have significantly improved quality. "According to the Plant-based Food Alliance UK and the Good Food Institute Europe, breakthroughs in precision fermentation and advanced protein structuring have allowed manufacturers to create next-generation dairy alternatives that mimic the melt, stretch, and flavor profiles of traditional dairy. Brands are investing heavily in research and development to create varieties that melt, stretch, and age like traditional cheese. As per sources, the introduction of cultured nut-based cheeses has attracted gourmet consumers who value complexity and depth of flavor. Social media and influencer marketing play a crucial role in showcasing these innovations, encouraging trial among skeptical buyers. The expansion of product ranges to include familiar formats such as mozzarella-style shreds and cheddar blocks enhances versatility in cooking. This focus on sensory satisfaction and culinary functionality ensures that plant-based cheese continues to grow rapidly, transitioning from a niche alternative to a mainstream option in the UK market.

By Product Type Insights

The cheddar cheese segment dominated the United Kingdom market and accounted for a 36.3% share in 2025. This dominated the segment, which was driven by its deep cultural heritage and ubiquitous availability across all retail and foodservice channels. Originating in the village of Cheddar in Somerset, this variety is ingrained in British identity and daily consumption habits. According to the British Cheese Board, Cheddar accounts for over 50 percent of all cheese consumed in the United Kingdom, making it the undisputed market leader. Its versatility allows it to be used in sandwiches, cooked dishes, snacks, and cheese boards, appealing to a wide range of culinary applications. Data from the Agriculture and Horticulture Development Board shows that the UK produces over 300,000 tons of Cheddar annually, ensuring a consistent supply and competitive pricing. The familiarity of Cheddar makes it a safe choice for consumers, reducing decision fatigue in shopping environments. As per retail data, every major supermarket stocks multiple varieties of Cheddar, from mild to extra mature, catering to diverse taste preferences. The strong brand recognition of regional Cheddars, such as West Country Farmhouse Cheddar, adds value and prestige. This widespread presence and cultural significance ensure that Cheddar remains the cornerstone of the UK cheese market, driving volume and sustaining producer revenues. Its status as a household staple guarantees steady demand regardless of economic fluctuations or trending alternatives.

The versatility of Cheddar in culinary applications further cements its top position. It melts well, making it ideal for popular dishes such as macaroni cheese, Welsh rarebit, and toasted sandwiches. Its ability to complement both simple and complex recipes makes it a favorite among home cooks and professional chefs alike. Data from recipe websites and cooking apps shows that Cheddar is the most searched ingredient for cheese-based meals, reflecting its central role in British cuisine. The availability of different maturity levels allows for customization of flavor intensity, enhancing its adaptability. Moreover, the economic efficiency of Cheddar production allows for affordable pricing, making it accessible to all income groups. This functional flexibility and economic accessibility ensure that Cheddar maintains its dominance, serving as the primary reference point for cheese consumption in the UK. Its enduring popularity drives continuous innovation in packaging and format, keeping the segment dynamic and relevant.

The mozzarella segment is on the rise and is expected to be the fastest-growing segment in the market by witnessing a CAGR of 8.2% over the forecast period, owing to the influence of international cuisine and the pervasive pizza culture. The popularity of Italian food has surged in the UK, with pizza becoming a weekly staple for many households. According to the British Pizza, Pasta & Italian Food Association (PAPA), the UK market consumes roughly 750 million pizzas annually across retail and food service sectors, establishing Mozzarella as a highly vital commercial dairy commodity. The rise of home cooking during and after the pandemic has also boosted retail sales of Mozzarella balls and shredded varieties. In addition, the versatility of Mozzarella in salads, pasta dishes, and appetizers further broadens its appeal beyond pizza. Consumer exposure to global flavors through travel and media has enhanced appreciation for authentic Italian ingredients. This cultural integration and culinary versatility ensure that Mozzarella continues to grow rapidly, capturing a larger share of the UK cheese market.

The perception of Mozzarella as a healthier and fresher option compared to aged cheeses contributes to its swift growth. Consumers often view fresh Mozzarella as a lighter and more natural choice, aligning with health-conscious eating habits. According to nutrition surveys, Mozzarella is perceived to have lower sodium content than many hard cheeses, appealing to those monitoring salt intake. Data from the British Nutrition Foundation highlights that fresh cheeses are increasingly recommended as part of a balanced diet due to their high protein and calcium content. The availability of buffalo Mozzarella and low-moisture variants offers choices for different dietary needs and preferences. As per sources, the clean label trend favors fresh cheeses with minimal processing and fewer additives. Retailers are promoting Mozzarella as part of healthy meal kits and salad ranges, enhancing its visibility and appeal. The short shelf life of fresh Mozzarella encourages frequent purchases, driving repeat sales and volume growth. This combination of health benefits and freshness appeal ensures that Mozzarella remains the fastest-growing segment, attracting health-conscious consumers and culinary enthusiasts alike.

BY Form Insights

The block form segment held the majority share of 58.7% of the United Kingdom cheese market in 2025. This supremacy of the segment was credited to its convenience and storage efficiency for both consumers and retailers. Blocks are easy to stack, display, and store, maximizing shelf space and minimizing waste. Consumers prefer blocks for their versatility, allowing them to grate, slice, or cube the cheese as needed for various recipes. The ability to purchase larger blocks offers better value for money, appealing to budget-conscious families. The simplicity of block packaging also lowers production costs, enabling competitive pricing. This practical advantage ensures that block form remains the preferred choice for mainstream consumers, driving volume and sustaining market leadership. Its adaptability to different household needs and retail logistics solidifies its position as the dominant form in the UK cheese market.

The traditional usage and culinary flexibility of block cheese further reinforce its leading position. Blocks are the standard format for traditional British cheeses like Cheddar and Red Leicester, aligning with established cooking and serving practices. According to the British Cheese Board, block cheeses are the primary format used in home cooking for grating over potatoes, slicing for sandwiches, and cubing for snacks. Analysis of major UK recipe databases shows that traditional culinary instructions specify cheese by weight and required preparation state (e.g., '100g grated Cheddar'), which indirectly reinforces the purchase of versatile block formats for home processing. The tactile experience of cutting and preparing block cheese is valued by many consumers who associate it with freshness and quality. As per consumer feedback, blocks are perceived as more authentic and less processed than pre-packaged alternatives. The ability to control portion sizes and reduce plastic waste appeals to environmentally conscious shoppers. Retailers support this preference by offering a wide variety of block cheeses at different price points. This alignment with traditional culinary practices and consumer values ensures that block form remains the dominant segment, maintaining its relevance and popularity in the UK market.

The spreadable form segment is expected to exhibit a noteworthy CAGR of 9.5% between 2026 and 2034. This swift expansion is propelled by the demand for convenience in snacking and on-the-go consumption. Modern lifestyles require quick and easy food options, and spreadable cheeses fit this need perfectly. The ease of application on crackers, bread, and vegetables makes spreadable cheese a convenient snack option. As per research, the rise of lunchbox culture and office snacking has boosted demand for portable and mess-free cheese formats. Manufacturers are innovating with flavorful blends and healthy ingredients to attract diverse consumer segments. This focus on convenience and portability ensures that spreadable cheese continues to grow rapidly, capturing a significant share of the snack market.

Product innovation and flavor variety are key drivers accelerating the growth of the spreadable cheese segment. Manufacturers are introducing new flavors such as herb, garlic, and fruit-infused spreads to appeal to adventurous palates. The Guild of Fine Food highlights that artisanal and flavored spreadable cheeses, such as those infused with wild garlic, truffles, or sweet chili, are experiencing excellent premium growth as shoppers look for gourmet taste profiles to elevate simple meals. Data from social media trends shows that creative uses of spreadable cheese in dips and party foods are gaining popularity, enhancing its appeal for social gatherings. The development of lighter and lower-fat versions addresses health concerns, broadening the customer base. As per retail analysis, premium spreadable cheeses with artisanal ingredients are gaining traction in upscale supermarkets. The versatility of spreadable cheese in both sweet and savory applications encourages experimentation and repeat purchases. This continuous innovation and diversification ensure that the spreadable segment remains dynamic and fast growing, attracting consumers seeking convenience and flavor excitement.

COUNTRY LEVEL ANALYSIS

United Kingdom Cheese Market Analysis

The United Kingdom continues to be a major player in the European cheese market because of a strong cultural affinity for cheese, with high per capita consumption rates compared to other European countries. It is a mature and diverse landscape, balancing traditional artisanal production with modern industrial manufacturing. According to industry data, the UK consumes approximately 700,000 tonnes of cheese annually. Domestic production is typically around 450,000 to 500,000 tonnes, with over 330,000 tonnes of that being Cheddar. Data from market analysts indicates that the average UK consumer eats approximately 11.5 to 12 kilograms of cheese per year, a figure that underscores the nation's strong appetite for dairy, with Cheddar alone accounting for over 50% of household purchases. The presence of Protected Designation of Origin statuses for cheeses like Stilton and Single Gloucester enhances the prestige and value of British varieties. Consumer trends towards premiumization and sustainability are shaping product development, with increasing demand for organic and locally sourced options. The robust retail infrastructure, including supermarkets and specialty shops, ensures wide availability and accessibility. Post Brexit trade dynamics have influenced export strategies, with producers focusing on high-value markets to offset regulatory challenges. The resilience of the dairy sector and ongoing innovation in flavors and formats ensure that the UK remains a vibrant and competitive market for cheese. This stable foundation supports continuous growth and adaptation to evolving consumer preferences.

COMPETITIVE LANDSCAPE

The competition in the UK cheese market is intense and characterized by a mix of large multinational corporations and numerous small artisanal producers. Major players compete on brand recognition, distribution network,s and product innovation, while smaller businesses differentiate through unique flavors and local provenance. Price sensitivity varies across segments,nts with private label offerings gaining traction due to economic pressures on household budgets. Premium and artisanal cheeses command higher margins by appealing to consumers seeking quality and ethical sourcing. The rise of plant-based alternatives adds another layer of competition, forcing traditional dairy companies to diversify their portfolios. Retailers play a pivotal role in shaping competitive dynamics through exclusive contracts and promotional strategies. Innovation in packaging and sustainability credentials is increasingly important for brand differentiation. Regulatory changes regarding trade and labeling also impact competitive strategies. Companies must balance cost efficiency with value addition to retain market share. The market continues to evolve with shifting consumer preferences towards health conveniencen,ce and environmentaresponsibilityil,ity driving strategic decisions and competitive positioning among key participants.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.K. Cheese Market include

- Arla Foods amba

- Saputo Inc.

- Lactalis Group

- Bel Group

- Dairy Crest Limited (Saputo Dairy UK)

- Ornua Co-operative Limited

- First Milk Ltd.

- Wyke Farms Ltd.

- Wensleydale Creamery

- Norseland Ltd.

- Dale Farm Group

- Belton Farm Ltd.

TOP LEADING PLAYERS IN THE MARKET

- Arla Foods UK is a dominant force in the British dairy sector, renowned for its extensive portfolio of cheese brands, including Lactofree and Castello. The company leverages its farmer-owned cooperative model to ensure high-quality milk sourcing and sustainable production practices. Recently, Arla has invested heavily in expanding its organic cheese range to meet growing consumer demand for natural products. The firm actively promotes environmental sustainability through its climate check labeling initiative,e which helps shoppers make informed choices. Arla strengthens its market position by collaborating with retailers to introduce innovative packaging solutions that reduce plastic waste. Its commitment to animal welfare and carbon reduction resonates with ethically conscious consumers. These strategic initiatives enhance brand loyalty and solidify its reputation as a leader in responsible dairy manufacturing within the United Kingdom.

- Dairy Crest Limited is a key player in the UK cheese market, best known for its iconic Cathedral City Cheddar brand. The company focuses on producing premium traditional cheeses that appeal to discerning consumers seeking authentic flavors. Dairy Crest has recently strengthened its position by launching new mature and extra mature varieties that cater to the trend of premiumization. The company invests in modernizing its production facilities to improve efficiency and maintain consistent quality standards. It actively engages in marketing campaigns that highlight the heritage and craftsmanship behind its products. Dairy Crest also partners with local farmers to secure a reliable supply of high-quality milk. These efforts reinforce its brand identity as a provider of superior British cheese. The company maintains a strong presence in both retail and foodservice sectors across the nation. It achieves this by focusing on quality and tradition.

- Saputo Dairy UK is a significant contributor to the cheese market, operating well-known brands such as Black Diamond and Lerwick. The company specializes in processed and specialty cheeses, offering convenient options for everyday consumption. Saputo has recently focused on product innovation by introducing reduced-fat and lower-salt variants to address health concerns among consumers. The firm enhances its market position through strategic partnerships with major supermarket chains to ensure wide distribution and visibility. It also invests in digital marketing initiatives to engage with younger demographics and promote versatile usage ideas. Saputo prioritizes operational excellence by optimizing its supply chain and reducing environmental impact. These actions help the company remain competitive in a dynamic market. Saputo balances convenience with nutritional improvements. As a result, the company continues to attract a broad customer base and strengthen its foothold in the United Kingdom cheese market.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the UK cheese market employ diverse strategies to maintain competitiveness and drive growth. Product innovation is central with companies launching healthy variants such as low-fat and reduced salt options. Sustainability initiatives focus on eco-friendly packaging and carbon-neutral production processes to meet consumer expectations. Brand differentiation through heritage storytelling and artisanal positioning appeals to premium segments. Strategic partnerships with retailers ensure prominent shelf placement and promotional visibility. Expansion into plant-based alternatives allows companies to capture emerging market trends. Digital marketing and social media engagement enhance brand awareness and customer loyalty. Cost optimization through supply chain efficiency helps maintain profitability amidst rising input costs. These approaches collectively strengthen market presence and adapt to evolving consumer preferences in the dynamic landscape.

MARKET SEGMENTATION

This research report on the U.K. cheese market is segmented and sub-segmented into the following categories.

By Source and Type

- Animal-Based (Cattle)

- Animal-Based (Goat)

- Animal-Based (Sheep)

- Plant-Based

By Product Type

- Cheddar

- Mozzarella

- Parmesan

- Stilton

- Cottage Cheese

- Cream Cheese

- Others

By Form

- Block

- Spreadable

- Sliced

- Shredded/Grated

- Cubed

- Others

By Region

- United Kingdom

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com