UK Healthcare IT Market Size, Share, Trends & Growth Forecast Report By Technology, End User, and Country – Industry Analysis and Forecast, 2026 to 2034

UK Healthcare IT Market Report Summary

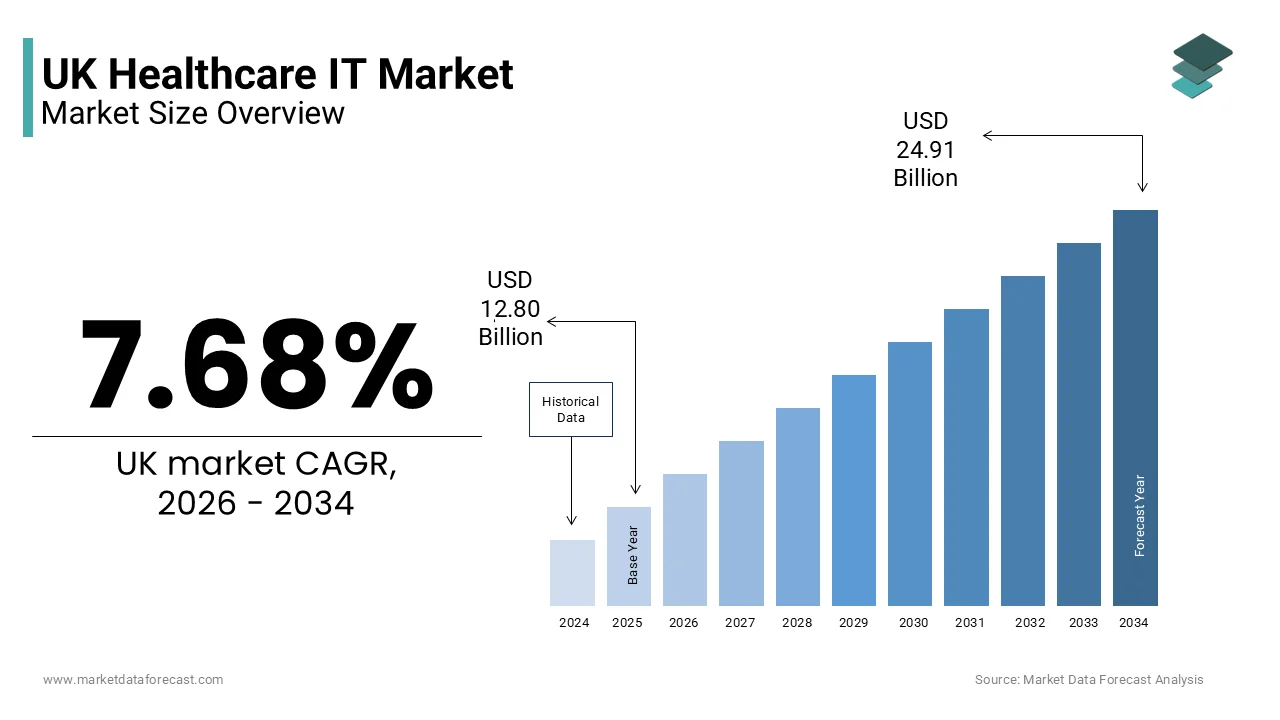

The UK healthcare IT market was valued at USD 12.80 billion in 2025, is estimated to reach USD 13.78 billion in 2026, and is projected to reach USD 24.91 billion by 2034, growing at a CAGR of 7.68% during the forecast period. Market growth is driven by increasing digital transformation across healthcare systems, rising adoption of electronic health records, growing demand for telehealth services, and the need to improve healthcare efficiency and patient outcomes. Government initiatives supporting healthcare digitization, advancements in data analytics, and the integration of artificial intelligence technologies are further accelerating market expansion across the United Kingdom.

Key Market Trends

- Growing adoption of telehealth and virtual care solutions is driving market growth.

- Increasing implementation of electronic health records and digital patient management systems is boosting market expansion.

- Rising use of artificial intelligence and predictive analytics in healthcare is supporting industry development.

- Expansion of cloud based healthcare platforms and interoperability solutions is enhancing market opportunities.

- Growing focus on patient centric care and healthcare data integration is influencing market advancement.

Segmental Insights

- Based on technology, the tele healthcare segment accounted for the largest share of the UK healthcare IT market in 2025. This dominance is attributed to its ability to provide remote consultations, improve healthcare accessibility, reduce pressure on healthcare facilities, and enhance patient engagement.

- Based on end user, the healthcare providers segment held the leading share of the UK healthcare IT market in 2025, driven by increasing adoption of digital solutions to streamline clinical workflows, improve diagnostic capabilities, enhance operational efficiency, and strengthen patient safety measures.

Regional Insights

- The United Kingdom represents one of the most advanced and centrally coordinated digital healthcare markets in Europe. The presence of a highly integrated healthcare system, strong government support for digital transformation, and increasing investments in healthcare technologies continue to support market growth and innovation.

Competitive Landscape

The UK healthcare IT market is highly competitive, with technology providers focusing on interoperability, cloud based healthcare solutions, artificial intelligence integration, and patient engagement technologies to strengthen their market position. Companies continue to invest in digital health platforms, data management systems, and advanced clinical decision support tools.

Key companies operating in the UK healthcare IT market include Oracle Corporation, GE HealthCare, Philips Healthcare, IQVIA, Accenture, Epic Systems Corporation, InterSystems Corporation, Veradigm Inc., Athenahealth, Inc., Cerner Corporation, The Phoenix Partnership (TPP), Agfa Gevaert Group, and SAP SE.

UK Healthcare IT Market Size

The UK healthcare IT market size was valued at USD 12.80 billion in 2025, and is projected to reach USD 24.91 billion by 2034 from USD 13.78 billion in 2026, growing at a CAGR of 7.68%.

Healthcare IT includes encompasses a sophisticated array of digital solutions designed to enhance clinical outcomes, operational efficiency, and patient engagement across the National Health Service and private sector providers. This ecosystem includes electronic health records, telemedicine platforms, data analytics tools, and interoperability frameworks that facilitate seamless information exchange between disparate care settings. The strategic imperative for digital transformation has intensified as the system grapples with an aging population and rising chronic disease prevalence. According to the Office for National Statistics, approximately 19 percent of the UK population was aged 65 or over in 2024, placing unprecedented demand on healthcare resources and necessitating efficient digital management. The NHS Long Term Plan mandates significant investment in technology to enable paperless operations and integrated care systems by 2025. As per Department of Health and Social Care data, over 90 percent of general practices now utilize digital appointment booking systems, reflecting widespread adoption of basic digital infrastructure. However, challenges remain in achieving full interoperability and leveraging advanced analytics for predictive care. Cybersecurity concerns have also escalated following high-profile ransomware attacks, prompting robust investment in secure cloud architectures. The market is characterized by a mix of large global vendors and innovative domestic startups focusing on artificial intelligence and remote monitoring. Regulatory frameworks, such as the General Data Protection Regulation, ensure strict data privacy standards, influencing solution design and deployment strategies across the nation.

MARKET DRIVERS

Government Mandates for Digital Transformation and Interoperability

Government mandates for digital transformation and interoperability primarily drive the expansion of the UK healthcare IT market forward through structured policy initiatives and funding allocations. The NHS Long Term Plan explicitly targets the creation of a fully digital health service, enabling patients to access their records and manage appointments online while supporting clinicians with real-time data. According to NHS England statistics, over 28 million patients are now registered for online access to their GP records, demonstrating the scale of consumer-facing digital adoption driven by policy. The establishment of Integrated Care Systems requires seamless data sharing between hospitals, general practitioners, and social care providers, necessitating robust interoperability standards and application programming interfaces. As per Department of Health and Social Care reports, the government has committed billions of pounds toward upgrading legacy infrastructure and implementing electronic patient records across acute trusts. These mandates create a guaranteed demand for compliant software solutions that meet national standards for security and data exchange. The push for a paperless NHS by 2025 has accelerated the retirement of outdated systems and the procurement of modern, cloud-based platforms. Regulatory pressure ensures that healthcare providers prioritize IT investments to avoid penalties and meet performance targets. This top-down approach provides stability and direction for technology vendors, who align their product roadmaps with national strategic objectives, ensuring sustained market growth and widespread implementation of critical digital tools.

Aging Population and Rising Prevalence of Chronic Diseases

The demographic shift toward an aging population and the corresponding rise in chronic diseases further boosts the growth of the UK healthcare IT market. Older adults typically require frequent monitoring, multiple medications, and coordinated care across various specialists, which traditional manual processes cannot efficiently support. According to the Office for National Statistics, the number of people aged 85 and over in the UK is projected to double by 2040, creating an urgent need for scalable digital care models. Chronic conditions, such as diabetes, cardiovascular disease, and respiratory illnesses, account for a substantial portion of NHS workload, requiring continuous data tracking and intervention. As per Public Health England data, approximately 15 million people in the UK live with at least one long-term condition, driving adoption of remote patient monitoring devices and digital therapeutics. Telehealth platforms enable regular virtual consultations, reducing hospital admissions and improving quality of life for immobile patients. Electronic health records facilitate a comprehensive view of patient history, allowing clinicians to make informed decisions quickly. Predictive analytics help identify high-risk individuals for early intervention, preventing costly emergency episodes. The economic burden of chronic care necessitates efficiency gains that only digital tools can provide. Consequently, healthcare providers invest heavily in IT infrastructure to manage this growing patient cohort effectively, ensuring sustainability of the health system amidst increasing demand.

MARKET RESTRAINTS

Legacy Infrastructure and Interoperability Fragmentation

Legacy infrastructure and interoperability fragmentation are majorly impeding the expansion of the UK healthcare IT market. Many National Health Service trusts still operate on outdated systems that were not designed to communicate with modern, cloud-based applications, creating data silos and inefficiencies. According to NHS Digital audits, a considerable proportion of acute trusts rely on legacy patient administration systems that lack standard application programming interfaces required for real-time data exchange. This technical debt forces organizations to maintain expensive parallel systems or engage in complex custom integrations that are prone to errors and delays. As per King’s Fund analysis, the lack of uniform data standards across different regions and care settings impedes the flow of critical patient information during referrals and emergency care. Clinicians often spend excessive time manually transferring data between systems, reducing time available for direct patient care. The fragmented landscape makes it difficult for new vendors to deploy solutions that work universally across the estate. Upgrading these entrenched systems requires substantial capital investment and operational disruption, which many cash-strapped trusts cannot afford simultaneously. The absence of a single, unified national record means that patient data remains scattered, leading to duplicated tests and medication errors. These structural barriers slow down the realisation of digital benefits and frustrate both providers and patients seeking cohesive care experiences.

Cybersecurity Threats and Data Privacy Concerns

Cybersecurity threats and escalating data privacy concerns are further hindering the healthcare IT market growth in the UK. Healthcare organizations are prime targets for ransomware attacks and data breaches, which can disrupt critical services and compromise patient confidentiality. According to National Cyber Security Centre statistics, the health sector experienced a significant increase in cyber incidents in 2024, with several major trusts reporting service disruptions due to malicious attacks. The General Data Protection Regulation imposes stringent requirements for data handling, storage, and breach notification, with hefty fines for non-compliance adding legal and financial risk. As per Information Commissioner's Office enforcement actions, healthcare providers face intense scrutiny regarding consent management and data minimization practices. Fear of reputational damage and regulatory penalties makes healthcare leaders cautious about adopting new technologies, particularly those involving third-party cloud providers or artificial intelligence. Implementing robust security measures, such as encryption, multi-factor authentication, and continuous monitoring, requires specialized expertise and ongoing investment that strains limited IT budgets. Staff training on cybersecurity hygiene is essential but often inconsistent across large, decentralized organizations. The complexity of securing interconnected devices, including Internet of Things medical equipment, expands the attack surface further. These security challenges necessitate rigorous due diligence and slower procurement cycles, delaying innovation and limiting the speed at which new digital solutions can be deployed safely across the healthcare estate.

MARKET OPPORTUNITIES

Expansion of Artificial Intelligence and Predictive Analytics

The expansion of artificial intelligence and predictive analytics offer substantial opportunities for the UK healthcare IT market. These technologies enable the analysis of vast datasets to identify patterns, predict disease outbreaks, and optimize resource allocation in real time. According to Accelerated Access Review partnerships, AI-driven diagnostic tools have demonstrated accuracy rates exceeding 90 percent in detecting certain cancers from imaging scans, offering potential for earlier intervention. Hospitals are increasingly adopting predictive models to forecast patient admission rates, allowing for better staff rostering and bed management. As per NHS AI Lab case studies, algorithms that analyze electronic health records can identify patients at high risk of deterioration, enabling proactive care interventions that reduce emergency admissions. Machine learning applications also streamline administrative tasks, such as coding, billing, and documentation, freeing up clinical time for patient interaction. The integration of natural language processing allows for automated extraction of insights from unstructured clinical notes, enhancing data utility. Government support through the Life Sciences Vision encourages collaboration between tech firms and healthcare providers to develop validated AI solutions. The ability to personalize treatment plans based on genetic and lifestyle data opens new avenues for precision medicine. As computational power increases and data quality improves, the scope for AI applications will expand, driving significant value creation and improved health outcomes across the system.

Growth of Remote Patient Monitoring and Telehealth Services

The growth of remote patient monitoring and telehealth services offers significant opportunities to the expansion of the UK healthcare IT market. Connected devices, such as wearable sensors and home monitoring kits, transmit vital signs directly to clinicians, enabling continuous oversight of chronic conditions without frequent hospital visits. According to NHS England data, virtual wards have expanded rapidly, with thousands of patients managed at home using remote monitoring technology, reducing bed occupancy pressures. Telehealth platforms facilitate video consultations, mental health therapy, and follow-up appointments, enhancing convenience and reducing travel burdens for patients. As per Royal College of Physicians surveys, patient satisfaction with remote consultations remains high, particularly for routine check-ups and minor ailments. The integration of these services with electronic health records ensures that remote data informs clinical decisions seamlessly. Reimbursement models are evolving to support digital consultations, encouraging wider adoption among general practitioners and specialists. The pandemic accelerated acceptance of remote care among both providers and patients, creating a lasting behavioral shift. Technology providers can innovate with user-friendly interfaces and interoperable devices that integrate easily into existing workflows. The potential to prevent complications through early detection of anomalies drives cost savings for the healthcare system. This trend supports the shift toward value-based care and empowers patients to take active roles in managing their health.

MARKET CHALLENGES

Workforce Shortages and Digital Skills Gap

Workforce shortages and a pronounced digital skills gap present major challenges to the UK healthcare IT market expansion. Clinical staff often lack the necessary training to leverage advanced digital tools effectively, leading to underutilization and resistance to change. According to NHS People Plan estimates, the health and care sector faces a vacancy rate of approximately 11 percent, exacerbating the burden on existing staff who must balance patient care with learning new technologies. As per Health Education England surveys, a significant proportion of healthcare professionals report feeling inadequately trained in digital literacy, affecting their confidence in using electronic records and decision support systems. The rapid pace of technological advancement outstrips the capacity of traditional training programs to upskill the workforce adequately. Recruitment of specialized IT personnel, such as data scientists and cybersecurity experts, is difficult due to competition from other sectors offering higher salaries. High turnover rates among clinical staff disrupt continuity in digital adoption efforts, requiring constant retraining. The stress associated with navigating complex interfaces during busy shifts can contribute to burnout and errors. Addressing this challenge requires substantial investment in comprehensive training programs, intuitive user interface design, and change management strategies. Without a digitally competent workforce, the potential benefits of healthcare IT investments remain unrealized, compromising patient safety and operational efficiency. Bridging this gap is essential for sustainable digital transformation.

High Implementation Costs and Budget Constraints

High implementation costs and persistent budget constraints are further challenging the healthcare IT market growth in the UK. The total cost of ownership for enterprise healthcare systems includes not only software licensing but also hardware upgrades, integration services, training, and ongoing maintenance, which can be prohibitive. According to Nuffield Trust analysis, many NHS trusts operate with tight financial margins, limiting their ability to fund large-scale digital transformation projects without external support. Capital expenditure restrictions force organizations to prioritize immediate clinical needs over long-term technological improvements, leading to deferred upgrades and continued reliance on obsolete systems. As per Local Government Association reports, social care providers face even greater funding gaps, making adoption of integrated care platforms difficult despite policy mandates. The complexity of migrating data from legacy systems adds unexpected costs and delays, often exceeding initial budgets. Vendor lock-in and proprietary standards can lead to inflated renewal fees and reduced flexibility. Smaller practices and independent providers struggle to achieve economies of scale, making advanced solutions inaccessible. The uncertainty of future funding allocations creates hesitation in committing to multi-year contracts. These financial pressures hinder the pace of innovation and widen the digital divide between well-funded institutions and resource-constrained providers. Sustainable financing models are required to ensure equitable access to healthcare IT capabilities across the entire system.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 7.68% |

| Segments Covered | By Technology, End User, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Market Leaders Profiled | Oracle Health, GE HealthCare, Philips Healthcare, IQVIA, Accenture, Epic Systems Corporation, InterSystems Corporation, Veradigm Inc. (formerly Allscripts), Athenahealth, Inc., The Phoenix Partnership (TPP), Cerner Corporation, Agfa Gevaert Group, and SAP SE |

SEGMENTAL ANALYSIS

By Technology Insights

The tele-healthcare segment dominated the market by holding the largest share of the UK market in 2025, as it provides essential remote consultation capabilities that alleviate pressure on physical healthcare facilities and improve patient access to medical advice. This dominance is underpinned by widespread adoption across primary care settings, where general practitioners utilize video and telephone consultations to manage routine appointments efficiently. According to NHS England data, over 30 million virtual consultations were conducted in 2024, representing a significant portion of total primary care interactions and demonstrating the entrenched role of remote care in daily practice. The establishment of virtual wards allows hospitals to monitor patients at home using connected devices, reducing bed occupancy rates and enabling earlier discharge for stable patients. As per Department of Health and Social Care reports, the expansion of virtual ward capacity to 50,000 beds by 2025 has driven substantial investment in telehealth infrastructure and software platforms. Patients benefit from reduced travel time and waiting periods, while clinicians can manage larger caseloads with greater flexibility. The integration of telehealth services with electronic health records ensures continuity of care and accurate documentation. Regulatory support through reimbursement models for remote consultations further incentivizes provider adoption. The convenience and cost-effectiveness of tele-healthcare make it the cornerstone of modern digital health strategies, ensuring its continued leadership in the technology landscape.

However, the healthcare analytics segment is anticipated to showcase a CAGR of 17.4% during the forecast period in the UK market, as organizations increasingly rely on data insights to optimize operations and improve population health outcomes. This accelerated growth is driven by the vast amounts of data generated by electronic health records, wearable devices, and genomic sequencing, which require advanced analytical tools to extract meaningful patterns and predictions. According to NHS Digital statistics, the volume of healthcare data doubles every two years, creating an urgent need for sophisticated analytics platforms capable of processing large datasets in real time. Predictive analytics enable providers to forecast disease outbreaks, patient admission rates, and resource requirements, enhancing preparedness and efficiency. As per Deloitte UK research, healthcare organizations implementing advanced analytics report a 15 percent improvement in operational efficiency and a 10 percent reduction in readmission rates. Population health management tools help identify high-risk groups for targeted interventions, reducing the overall burden on the system. The integration of artificial intelligence enhances diagnostic accuracy and treatment personalization, driving clinical value. Government initiatives promoting data sharing and interoperability facilitate broader access to diverse data sources, enriching analytical models. These capabilities transform raw data into strategic assets, empowering leaders to make evidence-based decisions that drive quality and sustainability.

By End User Insights

The healthcare providers segment occupied the leading share of the UK market in 2025, as they are the primary adopters of technologies designed to streamline clinical workflows, enhance diagnostic accuracy, and improve patient safety. Hospitals, general practices, and community care centers utilize digital health systems to manage patient records, schedule appointments, and coordinate care across multidisciplinary teams. According to NHS Digital census data, nearly all general practices in the UK use electronic health record systems, demonstrating universal penetration among primary care providers. Acute trusts invest heavily in digital patient flow management tools to reduce waiting times and optimize bed utilization amidst capacity constraints. As per Royal College of Physicians surveys, 80 percent of clinicians report that digital tools improve access to patient information and facilitate faster decision-making during consultations. The mandate for paperless operations drives continuous upgrades and integration of new modules, such as e-prescribing and digital imaging archives. Providers seek solutions that reduce administrative burden, allowing more time for direct patient care. Reimbursement structures increasingly link payments to quality metrics tracked through digital systems, incentivizing adoption. The central role of providers in delivering care ensures they remain the largest purchasers and users of digital health technologies, driving market dominance.

The healthcare payers segment is another major segment and is predicted to record a CAGR of 15.4% during the forecast period, as insurers and commissioning bodies leverage technology to contain costs and transition toward value-based care models. Payers utilize digital health data to assess risk, stratify populations, and design targeted intervention programs that prevent costly acute episodes. According to Association of British Insurers data, private health insurers are increasingly integrating wearable data and telehealth services into their policies to encourage healthy behaviors and reduce claims frequency. Digital platforms enable automated claims processing and fraud detection using artificial intelligence, reducing administrative overhead and improving accuracy. As per NHS Integrated Care Boards reports, commissioning groups use predictive analytics to allocate resources more effectively, based on projected population health needs rather than historical spending patterns. Value-based contracts tie payments to patient outcomes tracked through digital metrics, encouraging providers to deliver high-quality, efficient care. Payers also offer digital wellness programs and mental health apps to members as preventive benefits, reducing long-term liability. The shift from fee-for-service to outcome-based reimbursement drives demand for data transparency and interoperability. These strategic imperatives ensure that payers rapidly adopt digital health solutions to maintain financial sustainability and competitive advantage.

COUNTRY LEVEL ANALYSIS

The UK stands as the most advanced and centrally coordinated digital health market in Europe, characterized by a single-payer system that facilitates standardized implementation and large-scale data aggregation. The market status is defined by strong government leadership through NHS England, which sets national strategies and funding priorities for digital transformation across the country. According to NHS Digital's annual report, the UK has achieved near-universal adoption of electronic health records in primary care and significant progress in acute settings, providing a robust foundation for advanced analytics and interoperability. London serves as a global hub for health tech innovation, hosting numerous startups, incubators, and venture capital firms focused on digital health solutions. The regulatory environment is supportive yet rigorous, with the Medicines and Healthcare products Regulatory Agency providing clear pathways for software as a medical device approval. As per Office for Life Sciences data, the UK health tech sector attracted over 2 billion pounds in investment in 2024, reflecting strong investor confidence. The presence of world-class research institutions and teaching hospitals fosters collaboration between academia, industry, and clinicians, driving evidence-based innovation. Data privacy laws ensure high standards of protection, building public trust in digital services. The centralized nature of the NHS allows for rapid scaling of successful pilots across the nation, unlike fragmented systems in other regions. This unique combination of scale, coordination, and innovation capability positions the UK as a leader in digital health adoption and the export of best practices globally.

COMPETITIVE LANDSCAPE

The competition within the UK healthcare IT market is intense and characterized by the presence of global technology giants alongside specialized domestic providers catering to specific clinical or administrative needs. Established multinational corporations leverage their extensive product portfolios and financial resources to secure large scale contracts with NHS trusts and private hospital groups. These leaders continuously innovate by embedding advanced technologies such as artificial intelligence and blockchain to differentiate their offerings and address complex healthcare challenges. Meanwhile agile local vendors compete effectively by offering highly customizable cost effective solutions tailored specifically for primary care networks and community services. The market sees frequent strategic collaborations between software providers and telecommunications companies to enhance connectivity and data transmission capabilities. Price competition remains significant particularly in the procurement of commodity IT services where standardization allows for easier comparison. Differentiation increasingly depends on interoperability features regulatory compliance and integration capabilities with existing legacy systems. Customer retention strategies focus on continuous product updates proactive support and training programs to ensure long term value realization. The dynamic nature of regulatory changes requires constant adaptation forcing competitors to balance innovation with stability to maintain trust and reliability among discerning healthcare clients seeking sustainable digital transformation partners.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the UK healthcare IT market are

- Oracle Corporation

- GE HealthCare

- Philips Healthcare

- IQVIA

- Accenture

- Epic Systems Corporation

- InterSystems Corporation

- Veradigm Inc. (formerly Allscripts)

- Athenahealth, Inc.

- Cerner Corporation

- The Phoenix Partnership (TPP)

- Agfa Gevaert Group

- SAP SE

Top Players in the Market

- Oracle Corporation maintains a significant presence in the UK healthcare IT sector by providing robust cloud based infrastructure and electronic health record solutions tailored for large hospital trusts. The company focuses on integrating clinical data with financial and supply chain operations to enhance overall organizational efficiency. Recent strategic initiatives include the expansion of its health data intelligence platform which leverages artificial intelligence to improve patient outcomes and operational decision making. Oracle has strengthened partnerships with local system integrators to ensure seamless implementation and compliance with NHS digital standards. By offering secure scalable and interoperable systems Oracle supports the transition toward paperless care environments. These efforts aim to modernize legacy infrastructure while ensuring data security and regulatory adherence thereby reinforcing its position as a trusted technology partner for complex healthcare organizations across the nation.

- Cerner Corporation now operating under Oracle Health plays a pivotal role in the UK market by delivering comprehensive clinical information systems that support patient care across acute and community settings. The organization is deeply involved in major digital transformation programs including the deployment of electronic patient records in several NHS trusts. Recent actions involve enhancing its population health management tools to enable proactive care coordination and reduce hospital admissions. Cerner has invested in user experience improvements to minimize clinician burnout and streamline workflow efficiency. The company actively collaborates with healthcare providers to customize solutions that meet specific local needs while maintaining national interoperability standards. By focusing on data driven insights and connected care models Cerner strengthens its reputation for delivering high value IT solutions that improve clinical quality and operational performance in the British healthcare landscape.

- Epic Systems Corporation contributes significantly to the UK healthcare IT market by providing integrated software platforms that connect hospitals general practices and patients through a single shared record. The company has gained traction with major NHS foundations seeking to unify disparate systems and improve data accessibility for clinicians. Recent developments include the expansion of its patient engagement apps which allow individuals to access test results book appointments and communicate securely with care teams. Epic has established local support centers to provide timely assistance and training for UK clients ensuring smooth adoption and utilization. The organization emphasizes open standards and interoperability facilitating seamless data exchange with other health IT vendors. By prioritizing ease of use and comprehensive functionality Epic reinforces its position as a leading provider of enterprise grade healthcare software supporting the digital ambitions of the National Health Service.

Top Strategies Used by Key Market Participants

Key players in the UK healthcare IT market predominantly employ strategic partnerships and product innovation to maintain competitive advantage and address evolving clinical needs. Companies invest heavily in research and development to integrate artificial intelligence machine learning and predictive analytics into their platforms enabling providers to achieve greater operational efficiency and improved patient outcomes. Developing interoperable solutions that comply with national standards such as those set by NHS Digital ensures seamless data exchange across different care settings. Strategic collaborations with local system integrators and consulting firms facilitate smoother implementation and customization for diverse healthcare organizations. Emphasizing cloud based architectures enhances scalability security and remote accessibility which are critical for modern healthcare delivery. Continuous focus on user experience design reduces clinician burden and increases adoption rates among medical staff. Providing robust cybersecurity measures protects sensitive patient data and builds trust with regulators and consumers. These combined strategies enable vendors to differentiate their offerings and capture diverse segments within the complex and regulated healthcare technology landscape.

MARKET SEGMENTATION

This research report on the UK healthcare IT market is segmented and sub-segmented into the following categories.

By Technology

- Wearable Devices

- Mobile Health Applications

- Cloud Computing

- Big Data Analytics

By End User

- Healthcare Providers

- Patients

- Pharmaceutical Companies

- Insurance Companies

Frequently Asked Questions

1. What is the UK Healthcare IT Market?

The UK Healthcare IT Market encompasses digital technologies, software, and services that support healthcare delivery, patient management, data analytics, and administrative operations across healthcare organizations.

2. What factors are driving the growth of the UK Healthcare IT Market?

Market growth is driven by increasing healthcare digitalization, rising adoption of electronic health records, expanding telehealth services, and government initiatives promoting digital healthcare transformation.

3. What are the key segments of the UK Healthcare IT Market?

Major segments include electronic health records, telemedicine, healthcare analytics, hospital information systems, practice management software, and healthcare cybersecurity solutions.

4. How are electronic health records improving healthcare delivery in the UK?

Electronic health records enhance patient data accessibility, improve care coordination, reduce administrative burdens, and support more informed clinical decision making.

5. What role does telemedicine play in the UK Healthcare IT Market?

Telemedicine enables remote consultations, improves access to healthcare services, enhances patient convenience, and helps healthcare providers manage resources more efficiently.

6. How is artificial intelligence being utilized in healthcare IT?

Artificial intelligence is used for clinical decision support, predictive analytics, medical imaging analysis, patient monitoring, and workflow automation.

7. Which healthcare facilities are the primary users of healthcare IT solutions?

Hospitals, clinics, diagnostic centers, ambulatory care centers, and specialty healthcare providers are among the leading adopters of healthcare IT technologies.

8. Why is healthcare data analytics important in the UK healthcare sector?

Healthcare analytics helps improve patient outcomes, optimize resource allocation, identify health trends, and support evidence based decision making.

9. What challenges does the UK Healthcare IT Market face?

Key challenges include cybersecurity threats, data privacy concerns, system interoperability issues, implementation costs, and the need for workforce training.

10. What is the future outlook for the UK Healthcare IT Market?

The market is expected to witness strong growth due to increasing investments in digital health infrastructure, wider adoption of AI driven solutions, and growing demand for connected and patient centric healthcare services.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com