UK Home Furnishings Market Size, Share, Trends & Growth Forecast Report By Product, By Material, By Distribution Channel, and By Country (United Kingdom) – Industry Analysis and Forecast, 2026 to 2034 Size, Share, Trends & Growth Forecast Report By Product, By Material, By Distribution Channel, and By Country (United Kingdom) – Industry Analysis and Forecast, 2026 to 2034

UK Home Furnishings Market Report Summary

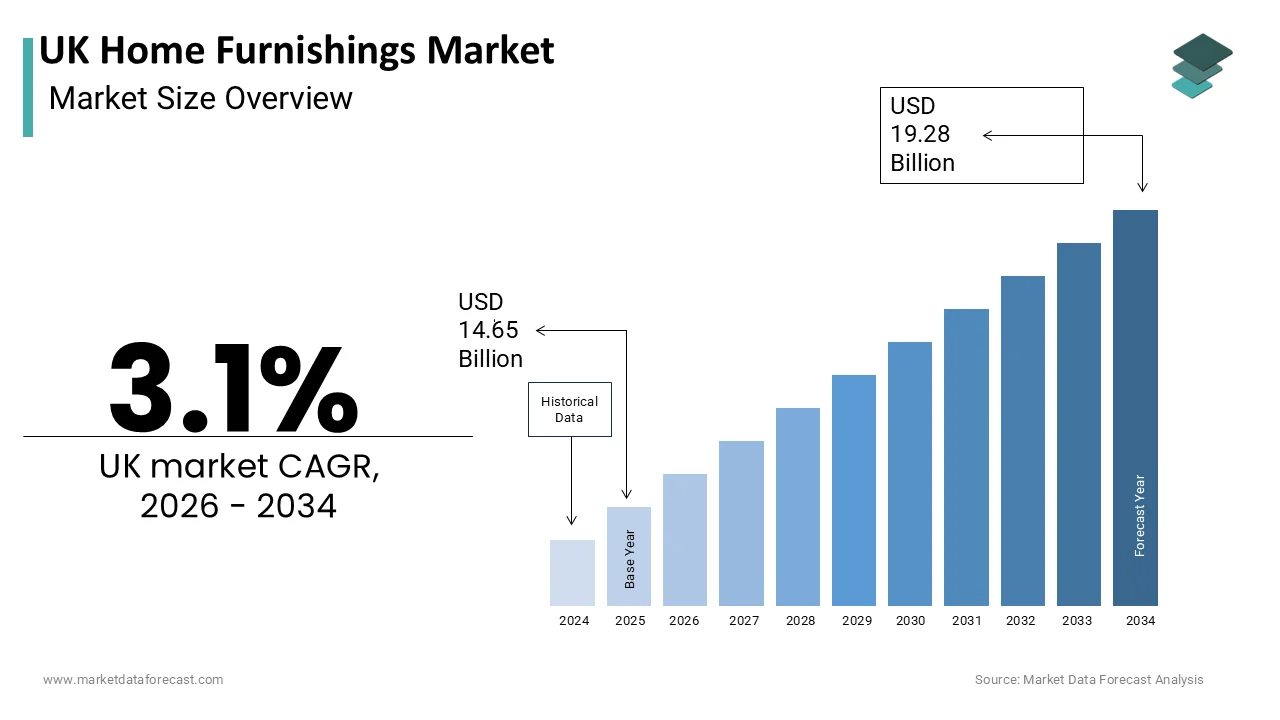

The UK Home Furniture Market was valued at USD 14.65 billion in 2025 and is projected to reach USD 19.28 billion by 2034, growing from USD 15.10 billion in 2026 at a CAGR of 3.10% during the forecast period. Growth is driven by housing market activity, rising focus on interior aesthetics, and expansion of sustainable and circular economy models. Economic uncertainty and competition from private label brands are shaping market dynamics.

Key Market Trends

- Growing consumer preference for sustainable and circular economy furniture models

- Rising adoption of augmented reality and digital visualization tools in retail

- Increasing demand for multifunctional and space-saving furniture in urban homes

- Growing competition from fast fashion and private label home decor brands

- Rising online furniture sales supported by improved AR-based visualization

Segmental Insights

- Based on product, living room and dining room furniture dominated the market in 2025, driven by its central role in social interaction and family gatherings.

- Based on material, wood led the market in 2025 by holding 54.5% of the market share, driven by its durability and perceived long-term value.

- Based on the distribution channel, specialty furniture stores led the market in 2025 by capturing 41.4% of the market share, supported by expert advice and showroom experiences.

Regional Insights

- England held the major share of the market in 2025 at approximately 85%, supported by high population density and strong retail infrastructure.

- Scotland holds a significant share, driven by heritage craftsmanship and a thriving design and tourism sector.

- Online retail is expected to witness considerable growth during the forecast period, projected at a CAGR of 10.2%, driven by digital convenience and AR visualization tools.

Competitive Landscape

The market is highly competitive, with retailers focusing on omnichannel integration, sustainable materials, and digital visualization tools. Companies are investing in circular economy initiatives and strategic partnerships with designers and influencers to strengthen brand loyalty.

Prominent players in the market include IKEA Systems B.V., DFS Furniture plc, Dunelm Group plc, Next plc, John Lewis plc, Wayfair Inc., Kingfisher plc, Homebase Ltd., Made.com (Next plc), Habitat (J Sainsbury plc), Herman Miller Inc. (MillerKnoll), and Kimball International Inc.

UK Home Furnishings Market Size

The UK Home Furniture Market is projected to grow from USD 14.65 billion in 2025 to USD 15.10 billion in 2026 and reach USD 19.28 billion by 2034, registering a CAGR of 3.1% during the forecast period from 2026 to 2034.

Home furnishings encompass a broad spectrum of interior decor items, including furniture, soft furnishings, lighting, and accessories, that transform residential and commercial spaces into functional and aesthetically pleasing environments. This sector is deeply intertwined with the housing market, consumer confidence, and evolving lifestyle trends, reflecting the cultural importance of home as a sanctuary. According to the Office for National Statistics, household disposable income spent on housing, water, electricity, and other fuels accounts for around 25% of total household spending, influencing the budget available for interior enhancements. According to the English Housing Survey, approximately 65% of households in England own their homes outright or with a mortgage, providing a stable basis for long-term investment in quality furnishings. The market is characterized by a mix of established high street retailers, independent boutiques, and rapidly growing online platforms that offer convenience and variety. Consumer preferences are increasingly driven by sustainability concerns, with shoppers seeking ethically sourced materials and durable designs that minimize environmental impact. The rise of remote work has further altered demand patterns, with greater emphasis on ergonomic home office solutions and multifunctional living spaces. Regulatory frameworks regarding fire safety and chemical usage ensure product standards, while trade dynamics affect the cost and availability of imported goods. This mature market continues to adapt through innovation in design, technology integration, and circular economy practices, ensuring relevance in a changing social and economic landscape.

MARKET DRIVERS

Housing Market Activity and Property Transactions Stimulate Renewal Demand

The level of activity in the housing market is primarily fuelling the expansion of the UK home furnishing market, as property transactions often trigger immediate needs for interior updates and new acquisitions. When individuals buy or rent new homes, they frequently seek to personalize spaces, replace worn items, or upgrade to better quality pieces that suit their new environment. According to HM Land Registry, there were approximately 1.02 million residential property transactions completed in the UK in 2024, providing a substantial pipeline of customers entering the furnishings market. As per the Building Societies Association, first-time buyers, who account for a significant portion of these transactions, are particularly likely to invest in essential furniture and decor items to establish their households. The turnover of rental properties also contributes to demand, as landlords refurbish units to attract tenants and comply with improving quality standards. Moving house creates a natural break point where consumers reassess their existing belongings and identify gaps in their inventory, leading to increased spending on sofas, beds, dining sets, and storage solutions. Estate agents and removal companies often partner with furniture retailers to offer bundled deals, further stimulating sales during peak moving seasons. This correlation between property mobility and furnishing purchases ensures a steady baseline of demand, regardless of broader retail trends.

Rising Focus on Home Improvement and Interior Aesthetics

The growing emphasis on home improvement and interior aesthetics is further boosting the expansion of the UK home furnishing market, as consumers view their living spaces as reflections of personal style and well-being. Social media platforms, such as Instagram and Pinterest, have democratized design inspiration, encouraging individuals to experiment with trends and invest in statement pieces that enhance visual appeal. According to Ofcom, over 85% of adults in the UK use social media regularly, with many following interior design influencers who showcase the latest styles and DIY projects. As per Houzz UK's annual survey data, 55% of homeowners planned to undertake decorative improvements in 2024, prioritizing items such as rugs, curtains, lighting, and accent furniture to refresh their interiors without major structural changes. The trend toward nesting and creating comfortable sanctuaries has persisted post-pandemic, with people willing to spend more on high-quality textiles and ergonomic furniture that support relaxation and productivity. Retailers respond by offering curated collections and styling services that help customers visualize cohesive looks. The psychological benefit of a well-decorated home contributes to mental health and satisfaction, reinforcing the value placed on aesthetic upgrades. This cultural shift ensures that home furnishings remain a priority for discretionary spending, even during periods of economic caution.

MARKET RESTRAINTS

Economic Uncertainty and Inflationary Pressures Limit Discretionary Spending

Persistent economic uncertainty and rising inflation rates significantly constrain consumer spending power in the UK, which is leading to deferred purchases and reduced budgets for home furnishings. Households face increased costs for essential items, such as energy, food, and mortgage payments, leaving less disposable income for non-essential home decor and furniture upgrades. According to the Office for National Statistics, the consumer price index for housing and household services rose by 4.3% in 2024, outpacing wage growth and eroding real purchasing power for many families. As per the Retail Economics report, over 40% of shoppers reported postponing planned furniture purchases or opting for cheaper alternatives due to financial pressures, affecting overall market volume. Consumers become more price-sensitive, seeking discounts, promotions, and second-hand options rather than investing in premium new items. The perception of furnishings as durable goods allows buyers to extend the life of existing pieces through repair and maintenance, rather than replacement. Mid-market retailers suffer most as customers trade down to budget brands or wait for significant sales events. This economic restraint limits the ability of companies to invest in new collections and marketing initiatives, as they focus on inventory clearance and cost management. The prolonged nature of these financial challenges creates a subdued market atmosphere, where growth is difficult to achieve without aggressive pricing strategies.

Supply Chain Disruptions and Raw Material Cost Volatility

Ongoing disruptions in global supply chains and volatility in raw material prices are further impeding the home furnishing market expansion in the UK, which is affecting production timelines and cost structures. The industry relies heavily on imported materials, such as timber, fabrics, metals, and foam, primarily sourced from Asia and Europe, making it vulnerable to geopolitical tensions, logistics bottlenecks, and trade policy changes. According to the British Chambers of Commerce, around 40% of UK businesses reported experiencing severe supply chain disruption and longer shipping lead times in 2024 due to geopolitical conflicts and port bottlenecks, delaying product launches and replenishment. As per the Federation of Small Businesses, rising costs of running operations and acquiring goods have forced over half of small businesses to increase their prices, forcing companies to either absorb losses or pass costs to consumers. These fluctuations create uncertainty in pricing strategies and inventory planning, leading to potential stockouts or excess inventory, depending on demand forecasting accuracy. Labor shortages in manufacturing hubs further exacerbate production delays, limiting output capacity during peak seasons. Retailers struggle to maintain consistent assortments, impacting customer satisfaction and loyalty. The complexity of managing multi-tier supply chains requires significant investment in risk mitigation strategies, such as diversifying suppliers and holding higher safety stocks. These operational hurdles restrict agility and profitability, hindering the industry's ability to respond quickly to emerging trends.

MARKET OPPORTUNITIES

Expansion of Sustainable and Circular Economy Models

The increasing consumer awareness of environmental issues presents a lucrative opportunity for home furnishings brands in the UK to differentiate themselves through sustainable and circular economy practices. Shoppers are actively seeking products made from recycled materials, responsibly sourced wood, and organic textiles, reducing the ecological footprint of their purchases. According to a survey by Deloitte, approximately 40% of UK consumers chose brands that have environmentally sustainable practices or values, indicating strong market potential for green innovations. As per the Ellen MacArthur Foundation, brands that adopt take-back schemes, repair services, and resale platforms build stronger emotional connections with environmentally conscious demographics. Innovations in materials science allow for the creation of durable furniture using reclaimed wood, recycled plastics, and bio-based foams, appealing to both ethical and aesthetic sensibilities. Certifications, such as FSC for wood and GOTS for textiles, enhance credibility and trust among skeptical buyers. Premium pricing is often accepted for sustainable products, as consumers view them as long-term investments in planetary health. Collaborations with environmental organizations amplify marketing messages and demonstrate genuine commitment beyond greenwashing. Retailers can leverage this trend by dedicating shelf space to eco-friendly collections and educating staff on sustainability benefits. This opportunity aligns with regulatory pushes for greater corporate responsibility, ensuring long-term viability.

Integration of Augmented Reality and Digital Visualization Tools

The integration of augmented reality (AR) and digital visualization tools offers a significant growth avenue for home furnishings retailers in the UK seeking to enhance customer confidence and reduce return rates. Advanced apps allow users to project virtual furniture into their actual living spaces using smartphone cameras, helping them assess size, scale, and style compatibility before purchasing. According to the UK Retail Tech report, the adoption of AR in retail is projected to grow by 20% annually, as consumers desire more interactive and informed shopping experiences. As per Shopify data, products with 3D content and AR views see a 94% higher conversion rate compared to those without, indicating the powerful impact of visual assurance. Retailers leverage these technologies to bridge the gap between online convenience and physical inspection, addressing one of the biggest barriers to online furniture sales. Virtual showrooms enable customers to explore entire room setups and mix and match items, fostering creativity and larger basket sizes. Partnerships with tech firms facilitate seamless integration of these features into existing e-commerce platforms, enhancing user engagement. The ability to offer personalized recommendations based on room dimensions and existing decor strengthens customer relationships. This technological frontier transforms the shopping journey from transactional to experiential, driving sales and loyalty in a competitive digital landscape.

MARKET CHALLENGES

Intense Competition from Fast Fashion and Private Label Brands

Fierce competition from fast fashion home retailers and private label brands poses a significant challenge to the UK home furnishings market, as they offer trendy designs at highly competitive prices. Supermarket chains and online giants leverage their economies of scale to produce affordable decor items that mimic high-end styles, attracting budget-conscious consumers who prioritize variety and low cost over longevity. According to the Retail Economics data, value retailers and private label brands captured 25% of the market volume in 2024, reflecting growing acceptance of store brands amid economic pressure. As per the British Retail Consortium, rapid turnover of fashion trends enables budget players to introduce new collections frequently, keeping shelves fresh and encouraging frequent visits. This dynamic forces traditional brands to accelerate their design cycles and reduce prices, eroding profit margins and diluting brand equity. Smaller independent retailers struggle to compete against the marketing budgets and distribution networks of large conglomerates. The perception of home decor as a disposable item rather than a durable good exacerbates the pressure to lower costs, potentially compromising quality and ethical standards. Established players must invest heavily in differentiation through superior craftsmanship, exclusive collaborations, or sustainability credentials to justify higher price points. However, price sensitivity remains high, making it difficult to maintain loyalty when cheaper alternatives are readily available.

Counterfeit Products and Intellectual Property Theft

The prevalence of counterfeit home furnishings and intellectual property theft presents a persistent challenge for branded manufacturers in the UK, damaging reputation, revenue, and consumer trust. Illicit copies of popular designer furniture and decor items flood online marketplaces and informal retail channels, offering superficially similar products at a fraction of the original price. According to the Intellectual Property Office, total losses due to counterfeit goods across all industries in the UK economy exceed billions of pounds annually, impacting legitimate businesses and tax revenues. As per Action Fraud, reports of online shopping fraud and fake online listings have risen steadily, as sophisticated manufacturing techniques make detection difficult for average consumers. These inferior products often lack quality control and safety standards, posing risks such as structural instability and toxic materials, which can be mistakenly attributed to the original brand. Counterfeits undermine the exclusivity and prestige associated with premium labels, reducing the incentive for innovation and design investment. Enforcement efforts are complicated by the cross-border nature of online sales, requiring complex legal actions and international cooperation. Brands must allocate significant resources to monitoring takedown requests and consumer education campaigns to combat this issue. The erosion of brand integrity affects long-term customer loyalty and market positioning, making it a critical operational and reputational risk that requires vigilant management.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Material, Distribution Channel, and Region |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | United Kingdom |

| Market Leaders Profiled |

|

SEGMENTAL ANALYSIS

By Product Insights

The living room and dining room furniture segment dominated the market by accounting for the highest share of the UK market in 2025. The dominance of the living room and dining room segment in the UK market is mainly driven by the central role these spaces play in social interaction, family gatherings, and daily relaxation. The living room serves as the primary communal area in British homes, necessitating substantial investment in sofas, armchairs, coffee tables, and dining sets that balance comfort with aesthetic appeal. According to the Office for National Statistics, adults in the UK spend an average of around 3 hours per day watching television and relaxing in living areas, highlighting the importance of durable and comfortable furnishings for prolonged use. As per the Retail Spending report, 65% of UK consumers prioritize upgrading their living room furniture when renovating or moving home, citing it as the most visible and impactful space for guests. The trend toward open-plan living has further integrated dining and lounge areas, increasing demand for cohesive furniture sets that define zones without physical barriers. Manufacturers respond by offering modular designs and multifunctional pieces, such as extendable dining tables and storage-integrated sofas, that maximize utility in varying room sizes. The emotional connection to hosting and family time ensures that consumers are willing to invest in higher-quality items that withstand frequent use. Retailers leverage this demand by showcasing complete room settings that inspire customers to purchase bundled items rather than individual pieces. This cultural emphasis on communal living sustains the dominance of this segment as the cornerstone of home furnishing expenditures.

On the other side, the bedroom furniture segment is a promising segment and is estimated to record a CAGR of 6.4% during the forecast period owing to the increasing consumer focus on sleep hygiene, wellness, and personal sanctuary creation. Individuals are increasingly viewing the bedroom as a retreat for rest and mental recovery, leading to higher investment in ergonomic beds, supportive mattresses, and calming decor elements. According to the Sleep Charity, over 70% of adults in the UK report that their sleep environment significantly impacts their quality of rest, prompting upgrades to beds and storage solutions that reduce clutter and noise. As per YouGov, sales of adjustable bed frames and blackout curtain-compatible furniture increased by 12% in 2024, as consumers sought to optimize their sleeping conditions. The rise of remote work has also blurred boundaries, with some individuals using bedroom spaces for quiet reading or meditation, further driving demand for versatile furniture such as bedside desks and comfortable seating. Manufacturers incorporate smart features, such as integrated lighting and charging ports, into bed frames, appealing to tech-savvy users who value convenience. The trend toward minimalism encourages the purchase of streamlined wardrobes and under-bed storage units that enhance tranquility. This health-driven shift positions bedroom furniture as a critical component of self-care, ensuring sustained growth as consumers prioritize restorative environments.

By Material Insights

The wood segment led the market by holding 54.5% of the UK market share in 2025. The dominance of the wood segment in the UK market is primarily attributed to its timeless aesthetic, durability, and perceived value. Consumers associate wood with quality craftsmanship and natural warmth, making it the preferred choice for major furniture pieces such as dining tables, beds, and cabinets. According to the Timber Development UK report, wood remains the primary material of choice across British furniture and construction sectors, reflecting its entrenched role in the industry. As per the Forest Stewardship Council, certified sustainable wood products have seen a 15% increase in sales, as environmentally conscious shoppers seek responsibly sourced materials. The versatility of wood allows it to be finished in various stains and paints, enabling it to complement diverse interior styles, from rustic to modern. Its longevity ensures that wooden furniture is often viewed as an investment rather than a disposable item, reducing replacement frequency. Manufacturers leverage traditional joinery techniques combined with modern engineering to create sturdy pieces that withstand daily wear. The tactile appeal and unique grain patterns of natural wood provide a sensory experience that synthetic materials struggle to replicate. This combination of heritage status, environmental credentials, and functional robustness ensures that wood remains the dominant material in the home furnishings sector.

On the other end, the plastic and polymer materials segment emerges as the fastest-growing segment in the UK home furnishings market and is projected to grow at a CAGR of 7.2% during the forecast period, owing to the advancements in manufacturing technology and demand for affordable, lightweight options. Innovations in high-density polyethylene and recycled plastics allow for the creation of durable, weather-resistant, and visually striking furniture suitable for both indoor and outdoor use. According to the British Plastics Federation, the use of recycled polymers in furniture production increased by 20% in 2024, as brands responded to sustainability mandates and consumer preferences for circular products. As per Euromonitor International, the affordability of plastic furniture appeals to younger demographics and renters who require flexible, low-cost solutions that are easy to move and maintain. The ability to mold plastic into complex organic shapes enables designers to create iconic, contemporary pieces that stand out in modern interiors. Weather resistance makes polymer furniture ideal for balconies and gardens, which are increasingly treated as extensions of living space. Manufacturers highlight the recyclability and low maintenance requirements of these materials to address environmental concerns. The vibrant color options and sleek finishes attract style-conscious buyers seeking bold statement pieces. This blend of economic accessibility, design freedom, and improved sustainability credentials positions plastic and polymer for rapid expansion in the competitive furnishings landscape.

By Distribution Channel Insights

The specialty furniture stores segment led the market by capturing 41.4% of the UK market share in 2025. The growth of the specialty furniture stores segment in the UK market can be credited to their ability to offer expert advice, extensive product ranges, and immersive showroom experiences. Consumers value the opportunity to physically test comfort, assess material quality, and visualize scale before making significant investments in large items such as sofas and beds. According to the British Furniture Confederation, independent and chain specialty retailers account for the majority of high-value furniture transactions, as shoppers seek personalized service and tailored solutions. As per the Retail Customer Insight report, 60% of customers prefer visiting physical specialty stores for major home purchases, citing the importance of staff knowledge and after-sales support in their decision-making process. These stores often provide interior design consultations, delivery, installation, and warranty services that enhance customer confidence and satisfaction. The curated selection of brands and exclusive collections differentiates them from generalist retailers, appealing to discerning buyers seeking unique styles. Showrooms are designed to inspire with fully styled room settings that help customers envision products in their own homes. This experiential approach builds trust and loyalty, encouraging repeat business and referrals. The integration of digital tools, such as tablets for inventory checks and customization options, further enhances the in-store experience, bridging the gap between physical and online retail.

However, the online retail segment is anticipated to register a promising CAGR of 10.2% during the forecast period in the UK market owing to the digital convenience, extensive choice, and improved visualization technologies. E-commerce platforms enable shoppers to browse thousands of products, compare prices, and read reviews from the comfort of their homes at any time. According to the Office for National Statistics, online sales of household goods increased by 14% in 2024, as consumers embraced digital shopping habits accelerated by pandemic-era changes. As per Statista, the integration of augmented reality tools allows users to project virtual furniture into their rooms, addressing previous concerns about fit and style compatibility. Direct-to-consumer brands leverage online channels to offer competitive pricing by eliminating middlemen and overhead costs associated with physical stores. Flexible return policies and white-glove delivery services mitigate the risks of buying large items online, building consumer trust. Social media integration facilitates discovery through influencer recommendations and targeted ads, driving impulse purchases. Data analytics enable personalized recommendations based on browsing history, ensuring relevant product discovery. Mobile optimization ensures seamless transactions on smartphones, which are increasingly the primary device for online shopping. This digital evolution continues to capture market share by offering speed, variety, and competitive pricing.

COUNTRY LEVEL ANALYSIS

UK Home Furnishings Market Analysis

England held the major share of the UK market in 2025 and is likely to experience sustained high demand and steady growth in the home furnishings market over the next few years, maintaining its position as the primary engine of the industry. England holds the dominant position in the UK home furnishings market, accounting for approximately 85% of total national sales, due to its high population density, extensive urban development, and robust retail infrastructure. London and other major cities serve as hubs for design innovation and consumer spending, driving demand for both luxury and practical furnishings. According to the Office for National Statistics, England is home to over 57 million people, representing the largest consumer base with significant disposable income for home improvements. As per the Ministry of Housing, Communities and Local Government, the continuous need for new home building and property development in urban centers creates a stable pipeline of customers needing to furnish new homes. Urban living trends, such as apartment living, drive demand for space-saving, multifunctional furniture and compact storage solutions. The presence of flagship stores for international brands ensures access to the latest global trends and exclusive collections. High employment rates in professional sectors support spending on home office ergonomics and premium decor. The dense network of logistics centers ensures efficient delivery across the region. Marketing campaigns often target English consumers through local design events and influencers, reinforcing brand relevance. This regional dominance is sustained by continuous investment in retail formats and strong consumer confidence, ensuring that England remains the primary engine of growth for the UK home furnishings industry.

Scotland Home Furnishings Market Analysis

Scotland is poised to expand its market share and demonstrate exceptional development potential over the coming years by leveraging its distinct design identity. Scotland holds a significant and distinct position in the UK home furnishings market, characterized by strong growth potential driven by its rich heritage in craftsmanship and thriving tourism sector. The region is renowned for high-quality textiles, leather goods, and wooden furniture, which appeal to consumers seeking authentic and durable products with a story. According to Scottish Enterprise, the creative and design industries sector in Scotland has shown consistent growth and contributes billions to the economy, highlighting the global appeal of local design talent. As per VisitScotland data, visitors and local consumers show a strong preference for purchasing home decor items that support local artisans and boutique brands, emphasizing traditional techniques and sustainable materials. The rugged landscape and historic architecture influence design preferences, with a tendency toward robust natural materials and classic styles. Cities like Edinburgh and Glasgow host design festivals and markets that showcase emerging talent, fostering a creative ecosystem. Government support for small businesses helps independent makers compete with larger brands by providing grants and training. The emphasis on quality over quantity aligns with consumer trends toward investment pieces that last. Online platforms allow Scottish brands to reach wider audiences beyond local borders. This unique combination of cultural heritage, natural inspiration, and entrepreneurial spirit positions Scotland as a dynamic and evolving segment within the broader UK home furnishings market landscape.

COMPETITIVE LANDSCAPE

The UK home furnishings market features intense competition characterized by a mix of specialized furniture retailers, general merchandise stores, and agile online pure players vying for consumer attention. Established brands leverage their physical showroom networks and heritage reputations to build trust while facing pressure from digital natives offering lower prices and greater convenience. Price sensitivity remains high during economic uncertainty,y prompting retailers to compete onvaluel, durability and flexible payment options. Innovation in sustainable materials and circular business models serves as a key differentiator for brands seeking to appeal to environmentally conscious shoppers. Private label offerings from supermarkets and department stores provide affordable alternatives that capture budget-conscious segments, putting pressure on mid-market specialists. The rise of augmented reality tools helps online retailers mitigate the inability to physically test products, enhancing conversion rates. Success depends on the ability to balance aesthetic appeal with functional practicality and ethical credentials. Companies must continuously invest in digital transformation and customer experience to retain loyalty in this fragmented and rapidly evolving industry landscape where style and substance intersect.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.K. Home Furnishings Market include

- IKEA Systems B.V.

- DFS Furniture plc

- Dunelm Group plc

- Next plc

- John Lewis plc

- Wayfair Inc.

- Kingfisher plc

- Homebase Ltd.

- Made.com (Next plc)

- Habitat (J Sainsbury plc)

- Herman Miller, Inc. (MillerKnoll)

- Kimball International, Inc.

TOP LEADING THREE PLAYERS IN THE MARKET

- DFS Furniture Plc stands as a leading retailer in the UK, specializing in sofas and living room furniture with a strong focus on customer service and product quality. The company operates an extensive network of showrooms across the country,ry allowing customers to test comfort and view fabric options in person. Recently,tly DFS has strengthened its market position by expanding its digital capabilities, ties including virtual consultation services and enhanced online visualization tools. They have introduced sustainable product lines made from recycled materials, aligning with growing environmental consciousness among consumers. Their commitment to manufacturing excellence is evident through partnerships with British suppliers, ensuring high standards and reduced lead times. By prioritizing customer experience and ethical sourcing,ourcing DFS maintains its reputation as a trusted provider of comfortable and durable home furnishings for British households.

- IKEA UK Limited contributes significantly to the market by offering af, functional and stylish home furnishings that appeal to a broad demographic range. The retailer leverages its global design expertise to provide modular solutions that maximize space efficiency, particularly in urban environments. Recent actions include the expansion of smaller city center click-and-collectand collect points to improve accessibility and convenience for shoppers. IKEA has invested heavily in circular economy initiatives such as furniture buy-back and resale programs, promoting sustainability and reducing waste. Their digital platform enhancements allow for better inventory management and personalized recommendations,s improving the overall shopping journey. By balancing cost-effectiveness with innovative design, IKEA continues to attract first-time buyers and families seeking practical home solutions.

- Next Plc Home Division plays a vital role in the UK home furnishings sector by integrating interior decor into its broader fashion and lifestyle retail strategy. The brand offers a curated selection of furniture, lighting,g and soft furnishings that complement its clothing lines, es creating a cohesive aesthetic forconsumers. Recentlyl,y Next has expanded its Total Platform service,ce enabling other brands to utilize its logistics and technology infrastructure, thereby increasing product variety without inventory risk. They have enhanced their online presence with improved search functionality and faster delivery options catering to the demand for convenience. Next focuses on trend-driven collections that refresh frequently, encouraging repeat visits and impulse purchases. By leveraging its strong supply chain and brand loyalty, Next maintains a competitive edge in the accessible mid-market segment.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the UK home furnishings market prioritize omnichannel integration by seamlessly connecting online browsing with in-store experiences to enhance customer convenience and engagement. Companies invest in sustainable practices such as using recycled materials and offering repair services to meet evolving consumer values and regulatory requirements. Strategic partnerships with interior designers and influencers help create aspirational content that drives brand awareness and desire. Retailers leverage data analytics to personalize marketing efforts and optimize inventory management, ensuring relevant products are available at the right time. Expansion into urban centers with smaller format stores improves accessibility for city dwellers. Enhanced delivery and assembly services reduce purchase friction and improve satisfaction. These strategies collectively enable companies to adapt to changing consumer preferences while maintaining competitiveness and driving long-term growth in the dynamic home sector.

MARKET SEGMENTATION

This research report on the UK home furnishings market is segmented and sub-segmented into the following categories.

By Product

- Living Room and Dining Room Furniture

- Bedroom Furniture

- Kitchen Furniture

- Bathroom Furniture

- Home Office Furniture

- Outdoor Furniture

- Others

By Material

- Wood

- Metal

- Plastic and Polymer

- Glass

- Upholstered Materials

- Others

By Distribution Channel

- Specialty Furniture Stores

- Home Improvement Stores

- Department Stores

- Online Retail

- Others

By Country

- United Kingdom

Frequently Asked Questions

1. Which product segment leads the market?

Home furniture leads the overall market by share

2. Which price segment is most important?

Mid‑range products hold a large share and remain a key focus for many retailers and consumers.

3. How are people buying home furnishings in the UK?

Online sales are growing strongly, while specialty stores and home centres also play a major role, especially for high‑value items.

4. Which regions show the strongest demand?

London and the South East show the highest demand due to higher incomes and a larger housing market.

5. Who are the major players?

Major players include IKEA, Dunelm, DFS, Bed Bath & Beyond, Villeroy & Boch, and other large furniture and homeware retailers

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com