UK Lingerie Market Size, Share, Trends & Growth Forecast Report By Lingerie Type, By Price Range, By Distribution Channel, and By Country (United Kingdom) – Industry Analysis and Forecast, 2026 to 2034

UK Lingerie Market Summary

Market Size & Growth

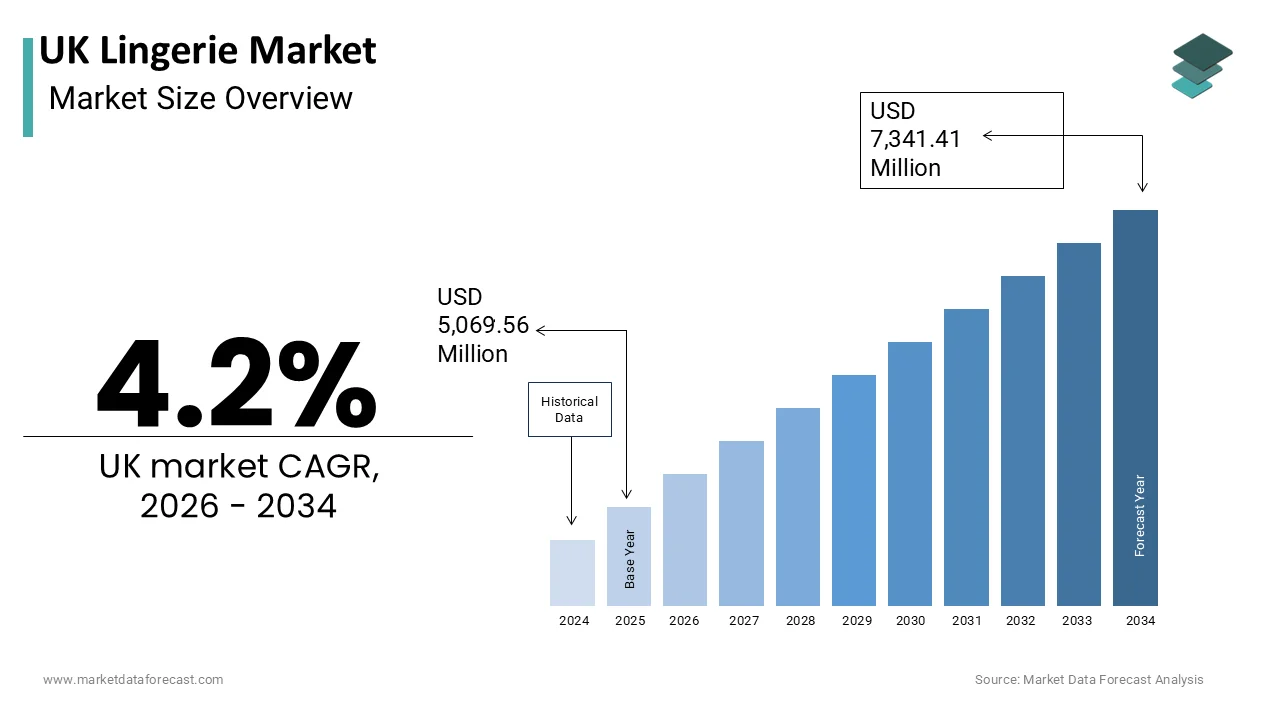

- UK Lingerie Market was valued at USD 5,069.56 million in 2025.

- Expected to reach USD 7,341.41 million by 2034, growing at a CAGR of 4.20% from 2026 to 2034.

- Market size projected at USD 5,282.48 million in 2026.

Key Market Segments

- By lingerie type: Bras (largest share), Shapewear (fastest-growing, CAGR of 8.4%)

- By price range: Economy (largest share), Premium (fastest-growing, CAGR of 7.2%)

- By distribution channel: Store-Based (largest share), Non-Store-Based (fastest-growing, CAGR of 10.2%)

Key Drivers

- Shift towards body positivity and inclusive sizing, with 60% of UK women reporting inadequate mainstream sizing per YouGov.

- Rising consumer preference for comfort and wellness, with 45% of UK consumers prioritizing comfort over style per Mintel.

- Growth of e-commerce, with UK online retail sales growing 15% annually per the Office for National Statistics.

Key Players

Marks and Spencer Group plc, Victoria's Secret & Co., Triumph International AG, Wacoal Holdings Corporation, Hunkemöller International B.V., Calvin Klein (PVH Corp.), Hanesbrands Inc., Ann Summers Ltd., Agent Provocateur Ltd., Boux Avenue, Next plc, ASOS plc.

UK Lingerie Market Size

The UK Lingerie Market is projected to grow from USD 5,069.56 million in 2025 to USD 5,282.48 million in 2026 and reach USD 7,341.41 million by 2034, registering a CAGR of 4.2% during the forecast period from 2026 to 2034.

The lingerie market represents a sophisticated segment of the apparel industry, characterized by a blend of functional necessity and fashion-driven expression. This sector encompasses bras, panties, shapewear, sleepwear, and intimate accessories, catering to diverse consumer preferences ranging from everyday comfort to luxury aesthetics. The cultural landscape of the UK has shifted significantly towards body positivity and inclusivity, which directly influences product development and marketing strategies. According to the Office for National Statistics, the female population in the UK stands at approximately 34 million, providing a substantial demographic base for intimate apparel consumption. Furthermore, as per data from the Department for Business and Trade, the textile and clothing sector remains a vital component of the retail economy with high consumer engagement levels. The rise of e-commerce has transformed purchasing behaviors, with online channels accounting for a significant portion of sales. According to the Office for National Statistics, over 25% of all retail sales are now conducted online. Consumer awareness regarding fabric quality and sustainability is also increasing, with shoppers prioritizing materials such as organic cotton and recycled synthetics. The market is further influenced by seasonal trends and promotional events, such as Black Friday and Valentine’s Day, which drive periodic spikes in demand. This dynamic environment requires brands to balance aesthetic innovation with ethical production practices to maintain relevance in a competitive landscape.

MARKET DRIVERS

Shift towards Body Positivity and Inclusive Sizing Drives Demand

The growing movement towards body positivity and inclusivity is a key factor propelling the UK lingerie market, expanding the range of available sizes and styles to cater to diverse body types. Consumers increasingly demand representation and products that fit comfortably regardless of shape or size, which has prompted brands to extend their size ranges significantly. According to a survey by YouGov, approximately 60% of UK women feel that mainstream retailers do not offer adequate sizing options, leading to a surge in demand for inclusive brands. This shift is supported by social media campaigns and influencer marketing that celebrate natural bodies and challenge traditional beauty standards. According to data from the Equality and Human Rights Commission, discrimination based on body image remains a concern, driving consumers towards brands that promote self-acceptance and diversity. Retailers, such as Marks and Spencer and Debenhams, have expanded their plus-size offerings in response to this trend, with some reporting a 20% increase in sales for extended sizes. The psychological impact of wearing well-fitting and aesthetically pleasing lingerie contributes to improved self-esteem, which further fuels demand. As per the Mental Health Foundation, positive body image is linked to better mental health outcomes, encouraging consumers to invest in high-quality intimate apparel. This cultural shift ensures that inclusivity is no longer a niche market but a central expectation driving growth and brand loyalty across the sector.

Rising Consumer Preference for Comfort and Wellness-Oriented Products

The increasing emphasis on comfort and wellness is further boosting the lingerie market expansion in the UK, as consumers prioritize health and physical well-being in their purchasing decisions. The pandemic accelerated this trend, with more people working from home and seeking versatile clothing that supports both relaxation and productivity. According to the British Heart Foundation, comfortable clothing reduces stress and improves circulation, which has led to a decline in sales for restrictive underwire bras and a rise in demand for wireless and soft cup alternatives. According to data from Mintel, 45% of UK consumers now prioritize comfort over style when buying lingerie, reflecting a significant change in consumer values. The use of breathable and hypoallergenic materials, such as bamboo and organic cotton, has gained popularity due to their skin-friendly properties. According to the Soil Association, sales of certified organic textiles have grown by 15% annually as consumers become more aware of chemical exposure risks. Additionally, the integration of wellness features, such as moisture-wicking and temperature regulation in lingerie designs, appeals to health-conscious buyers. This focus on holistic well-being extends to sleepwear, with many consumers investing in high-quality nightwear to improve sleep hygiene. As per the Sleep Council, poor sleep affects 36% of the UK population, which is driving demand for comfortable and supportive nightwear options. This enduring preference for comfort ensures sustained growth for brands that align with wellness-oriented lifestyles.

MARKET RESTRAINTS

Economic Pressure and Cost of Living Crisis Limit Discretionary Spending

The ongoing cost-of-living crisis in the UK is impeding market growth by reducing disposable income and limiting discretionary spending on non-essential items. High inflation rates and rising energy bills have forced households to prioritize essential goods over fashion and luxury items. According to the Office for National Statistics, the consumer prices index rose by 10.1% in the year leading up to early 2023, marking the highest level in decades. This economic pressure has led to a decline in consumer confidence, with many shoppers delaying purchases or opting for cheaper alternatives. As per data from the British Retail Consortium, footfall in high street stores has decreased by 8% as consumers cut back on non-essential shopping. The lingerie sector, which often relies on impulse buys and premium pricing, is particularly vulnerable to these economic shifts. Many consumers are extending the lifespan of their existing garments rather than replacing them frequently, which reduces overall market volume. As per the Money and Pensions Service, nearly 40% of adults report struggling to meet monthly expenses, further constraining their ability to purchase new clothing. This financial strain forces brands to compete on price, which can erode profit margins and limit investment in innovation. The uncertainty surrounding future economic conditions also makes consumers cautious about long-term commitments to higher-priced items, thereby restraining market growth.

Supply Chain Disruptions and Raw Material Volatility Impact Production

Supply chain disruptions and volatility in raw material costs are further hindering the expansion of the UK lingerie market. The global nature of the textile industry means that manufacturers rely on complex networks of suppliers for fabrics, trims, and components, which are susceptible to geopolitical tensions and logistical bottlenecks. According to the Confederation of British Industry, lead times for imported goods have increased by an average of 2 weeks due to port congestion and shipping shortages. This instability affects the ability of brands to maintain consistent inventory levels, leading to stockouts and lost sales opportunities. The price of key materials, such as cotton and synthetic fibers, has fluctuated significantly. According to the International Cotton Advisory Committee, there has been a 20% increase in cotton prices over the past two years. These cost increases are often passed on to consumers, making products less affordable and dampening demand. Additionally, Brexit-related trade barriers have introduced additional administrative burdens and tariffs for UK retailers sourcing from European suppliers. According to data from the British Fashion Council, 30% of fashion businesses have faced increased costs due to customs procedures. These operational challenges constrain the agility of brands to respond to fast-changing trends and consumer preferences, thereby restraining market efficiency and growth potential.

MARKET OPPORTUNITIES

Expansion of Sustainable and Ethical Product Lines

The growing consumer demand for sustainability and ethical production practices is a significant opportunity for the UK lingerie market to differentiate itself and capture environmentally conscious segments. Shoppers are increasingly aware of the environmental impact of fast fashion and are seeking transparent and responsible brands that prioritize eco-friendly materials and fair labor practices. According to a study by GlobalData, 55% of UK consumers are willing to pay more for sustainable products, indicating a strong market potential for green initiatives. Brands that utilize recycled plastics, organic cotton, and biodegradable packaging can appeal to this discerning audience and build long-term loyalty. According to the Ellen MacArthur Foundation, the circular economy model offers substantial economic benefits by reducing waste and resource consumption. Companies that implement take-back schemes and recycling programs can enhance their brand reputation and comply with upcoming regulatory requirements. As per the Environmental Audit Committee, the UK government is considering stricter regulations on textile waste, which will favor proactive brands. Additionally, certifications such as GOTS and Fair Trade provide credible validation of sustainability claims, helping consumers make informed choices. By integrating sustainability into their core business strategy, companies can tap into a growing niche market and mitigate risks associated with resource scarcity. This strategic shift not only addresses environmental concerns but also drives innovation and competitive advantage in the evolving retail landscape.

Growth of Direct-to-Consumer and Personalized Digital Experiences

The expansion of direct-to-consumer channels and personalized digital experiences offers a lucrative opportunity for UK lingerie brands to enhance customer engagement and drive sales. E-commerce platforms allow brands to bypass traditional retail intermediaries and establish direct relationships with consumers, enabling greater control over branding and pricing. According to the Office for National Statistics, online retail sales in the UK have grown by 15% annually, providing a robust infrastructure for digital expansion. Advanced technologies, such as artificial intelligence and augmented reality, enable personalized shopping experiences, including virtual try-ons and size recommendation tools, which reduce return rates and improve satisfaction. According to data from McKinsey, personalization can increase revenue by 10% to 12% by delivering relevant product suggestions and tailored content. Social media platforms also serve as powerful marketing channels where brands can interact with customers and build communities around shared values. The rise of subscription models for everyday essentials, such as underwear, provides a steady revenue stream and enhances customer retention. As per the Institute of Direct Marketing, personalized email campaigns have open rates 29% higher than generic ones, demonstrating the effectiveness of targeted communication. By leveraging data analytics and digital tools, brands can optimize their operations and create seamless omnichannel experiences that meet the expectations of modern consumers.

MARKET CHALLENGES

High Return Rates Due to Sizing Inconsistencies

High return rates caused by sizing inconsistencies are a significant challenge for the UK lingerie market, impacting profitability and operational efficiency. Unlike other apparel categories, lingerie requires a precise fit for comfort and support, making it difficult for consumers to purchase confidently online without trying items on. According to the British Retail Consortium, the return rate for online clothing purchases averages 25%, with lingerie often exceeding this figure due to fit issues. These returns incur substantial logistics costs, including shipping, handling, and restocking, which erode profit margins. Additionally, returned items may suffer damage or hygiene concerns that prevent them from being resold as new, leading to waste and inventory loss. The lack of standardized sizing across brands further complicates the shopping experience, with a size 34B varying significantly between manufacturers. According to data from the Size UK project, body shapes have changed over time, yet sizing charts have not kept pace, creating confusion for shoppers. This inconsistency leads to customer frustration and reduced brand loyalty as consumers struggle to find reliable fits. As per the Chartered Institute of Logistics and Transport, reverse logistics can cost retailers up to 60% of the original shipping fee. Addressing this challenge requires investment in accurate sizing technologies and clear communication, but it remains a persistent obstacle for many brands operating in the digital space.

Intense Competition from Fast Fashion and Private Label Brands

Intense competition from fast fashion retailers and private label brands is another major challenge for established lingerie companies, driving down prices and fragmenting market share. Large high street chains and online giants offer trendy and affordable lingerie collections that appeal to price-sensitive consumers who prioritize variety over longevity. According to Statista, the fast fashion segment accounts for a significant portion of the UK apparel market, with frequent new arrivals keeping customers engaged. Private label brands from supermarkets and department stores also compete aggressively on price and convenience, offering essentials at lower cost points. According to data from Kantar Worldpanel, private label penetration in the clothing sector has increased by 5% as consumers seek value for money during economic uncertainty. This competitive pressure forces specialized lingerie brands to constantly innovate and justify premium pricing through quality and brand equity. However, maintaining high standards while competing on price is difficult, especially when raw material costs are rising. The rapid turnover of fast fashion trends also shortens product lifecycles, requiring brands to accelerate their design and production processes, which can compromise quality and sustainability goals. As per the Competition and Markets Authority, aggressive pricing strategies can lead to market distortion, making it harder for smaller independent brands to survive. This dynamic environment requires constant adaptation and strategic differentiation to maintain relevance and profitability.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Lingerie Type, Price Range, Distribution Channel, and Region |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | United Kingdom |

| Market Leaders Profiled | Marks and Spencer Group plc, Victoria's Secret & Co., Triumph International AG, Wacoal Holdings Corporation, Hunkemöller International B.V., Calvin Klein (PVH Corp.), Hanesbrands Inc., Ann Summers Ltd., Agent Provocateur Ltd., Boux Avenue (Theo Paphitis Retail Group), Next plc, ASOS plc. |

SEGMENTAL ANALYSIS

By Lingerie Type Insights

The bras segment dominated the market by holding the highest share of the UK market in 2025 due to their essential nature and high replacement frequency among the female population. As a fundamental garment for support and comfort, bras are purchased more regularly than other intimate apparel items, driving consistent revenue streams for retailers. According to data from the Office for National Statistics, there are approximately 34 million women in the UK, creating a vast baseline demand for this category. The necessity of proper fit and support for daily activities ensures that bras remain a priority purchase regardless of economic fluctuations. Market research indicates that the average woman owns between 10 and 15 bras, replacing them every six to twelve months due to wear and tear. This cyclical consumption pattern sustains the dominance of the bra segment. Furthermore, the diversity of styles, ranging from sports bras to push-up and wireless options, allows brands to cater to specific functional needs and fashion trends. According to the British Heart Foundation, the importance of well-fitted bras for posture and back health is highly emphasized, reinforcing the functional necessity of this product type. Retailers report that bras account for nearly 40% of total lingerie sales volume, highlighting their central role in the market. The continuous innovation in fabric technology and design ensures that this segment remains dynamic and responsive to consumer preferences for both aesthetics and comfort.

However, the shapewear segment is the fastest-growing segment in the UK lingerie market and is projected to expand at a CAGR of 8.4% during the forecast period owing to the changing fashion trends that favor form-fitting clothing and the destigmatization of body-shaping garments. Modern shapewear is designed to be seamless and comfortable, allowing it to be worn as everyday underwear rather than just for special occasions. According to Mintel, 35% of UK women now own at least one piece of shapewear, reflecting its transition from a niche product to a mainstream staple. The influence of social media and celebrity endorsements has played a crucial role in normalizing shapewear usage and promoting body confidence, rather than concealment. Brands like Skims and Spanx have expanded their presence in the UK market, offering inclusive sizing and innovative fabrics that appeal to younger demographics. According to data from GlobalData, the demand for shapewear has increased by 20% among millennials, who view it as a tool for enhancing natural curves rather than altering body shape. The integration of shapewear into loungewear collections has further broadened its appeal, making it suitable for home wear and casual outings. This versatility, combined with effective marketing strategies, positions shapewear as a dynamic growth engine within the broader lingerie sector.

By Price Range Insights

The economy price range segment led the market by capturing the highest share of the UK market in 2025. The dominance of the economy price range segment in the UK market is primarily driven by high volume sales and the essential nature of basic intimate apparel. Consumers frequently purchase affordable basics, such as cotton briefs and simple bras for everyday wear, prioritizing value and practicality over luxury features. According to Kantar Worldpanel, economy brands account for approximately 55% of total lingerie unit sales in the UK, reflecting the broad consumer base that seeks cost-effective solutions. Supermarkets and large department stores play a significant role in this segment by offering competitive pricing and convenient access to essential items. The cost of living crisis has further reinforced the dominance of the economy segment as households tighten budgets and reduce spending on non-essential luxury goods. According to data from the Office for National Statistics, inflation has led to a 10% increase in price sensitivity among shoppers, driving traffic towards value-oriented retailers. Private label brands from major supermarkets, such as Tesco and Sainsbury’s, have gained market share by providing decent quality at low prices. This accessibility ensures that the economy segment remains resilient even during economic downturns. The high turnover rate of basic items also contributes to sustained demand as consumers replace worn-out garments regularly. Consequently, the economy segment maintains its leadership through volume-driven sales and widespread availability across multiple retail channels.

On the other end, the premium price range segment is the fastest-growing segment in the UK lingerie market and is expected to grow at a CAGR of 7.2% during the forecast period owing to the increasing disposable income among certain demographic groups and a shift towards treating lingerie as a form of self-care and luxury. Consumers are willing to invest in higher-quality materials, intricate designs, and brand prestige, which offer enhanced comfort and aesthetic appeal. According to Luxe Digital, the global luxury lingerie market is expanding, with UK consumers showing a particular interest in sustainable and ethically produced premium brands. The rise of direct-to-consumer brands has facilitated access to niche luxury labels that emphasize craftsmanship and exclusivity. According to data from Barclaycard, spending on premium fashion items has rebounded strongly post-pandemic, as consumers engage in revenge spending and seek rewarding experiences. The premium segment also benefits from gifting occasions, such as Valentine’s Day and anniversaries, where higher-priced items are preferred. Social media influencers and celebrity collaborations have elevated the status of luxury lingerie, making it aspirational for younger consumers. This cultural shift towards valuing quality over quantity supports the growth of the premium segment as shoppers seek long-lasting and distinctive pieces that reflect their personal style and values.

By Distribution Channel Insights

The store-based distribution channels segment occupied the major share of the UK market in 2025 due to the critical importance of fit and tactile experience in purchasing decisions. Unlike other apparel categories, lingerie requires precise sizing and comfort assessment, which is difficult to achieve through online shopping alone. According to the British Retail Consortium, physical stores still account for approximately 60% of total lingerie sales as consumers prefer to try on items before buying. Department stores and specialized lingerie boutiques offer professional fitting services that help customers find the correct size and style, reducing the likelihood of returns. The sensory experience of touching fabrics and evaluating construction quality also drives footfall to physical locations. According to data from Springboard, while overall retail footfall has declined, specialized stores with strong service offerings have maintained stable visitor numbers. The immediate gratification of taking purchases home and the ability to seek expert advice from staff further reinforce the dominance of store-based channels. Major retailers, like Marks and Spencer and Debenhams, have invested in upgrading their store environments to enhance the shopping experience with private fitting rooms and knowledgeable staff. This focus on service and convenience ensures that physical stores remain the primary channel for lingerie purchases, particularly for first-time buyers and those seeking specific fits.

On the other side, the non-store-based distribution channels segment is projected to expand at a CAGR of 10.2% during the forecast period due to the convenience of online shopping, extensive product variety, and advanced digital tools that mitigate fit concerns. Consumers appreciate the ability to browse vast selections from the comfort of their homes and access detailed product information and reviews. According to the Office for National Statistics, online retail sales in the UK have grown consistently, with clothing and footwear being among the top categories. The development of virtual try-on technologies and AI-driven size recommendation algorithms has improved the accuracy of online purchases, reducing return rates. According to data from IMRG, conversion rates for lingerie websites have improved by 15% due to better user experience and personalized recommendations. The privacy offered by online shopping also appeals to consumers who may feel uncomfortable discussing intimate apparel in person. Subscription models for everyday essentials have further boosted online sales by providing convenience and regular delivery. The integration of social commerce, where users can purchase directly from social media platforms, has also expanded reach. These technological and behavioral shifts ensure that non-store-based channels continue to capture increasing market share.

COUNTRY LEVEL ANALYSIS

UK LINGERIE MARKET ANALYSIS

The UK held a major share of the European market in 2025 and is likely to see steady innovation and remain a primary hub for ethical consumption in the European lingerie market for the next few years. This significant presence is driven by a mature retail infrastructure, high consumer spending power, and a strong culture of fashion consciousness. According to the Office for National Statistics, the UK apparel market is one of the largest in Europe, with lingerie representing a stable and resilient segment. The market status is characterized by a blend of established high street brands and emerging digital-native companies that cater to diverse consumer needs. According to data from the British Retail Consortium, the UK has a high penetration of online shopping, with consumers comfortable purchasing intimate apparel through digital channels. The emphasis on inclusivity and sustainability has positioned the UK as a leader in ethical fashion trends, influencing broader European markets. The presence of major global retailers and innovative startups fosters a competitive environment that drives product quality and service excellence. As per the Department for Business and Trade, the UK fashion industry contributes significantly to the national economy, with lingerie playing a key role in export and domestic sales. The regulatory framework supporting consumer rights and environmental standards further enhances market stability. This combination of economic strength, technological adoption, and cultural leadership ensures that the UK remains a central hub for lingerie innovation and consumption in Europe.

COMPETITIVE LANDSCAPE

The competition in the UK lingerie market is intense and characterized by a mix of established high street retailers, specialized boutiques,s and digital native brands. Market leaders differentiate themselves through product quality, their brand heritage, and customer service rather than price alone. The rise of direct-to-consumer startups has disrupted traditional models by offering niche products and personalized experiences that appeal to specific demographic segments. Inclusivity and sustainability have become key battlegrounds with brands competing to offer the widest size ranges and most eco-friendly materials. Online platforms have lowered barriers to entry, allowing new players to gain visibility through social media marketing and influencer partnerships. However,r incumbent retailers leverage their extensive physical networks and loyal customer bases to maintain dominance. The market sees frequent innovation in fabric technology and design to meet evolving consumer demands for comfort and style. Price sensitivity during economic downturns drives competition in the economy segment,nt while premium brands focus on exclusivity and craftsmanship. Overall success depends on balancing operational efficiency with strong brand identity and customer-centric values.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.K. Lingerie Market include

- Marks and Spencer Group plc

- Victoria's Secret & Co.

- Triumph International AG

- Wacoal Holdings Corporation

- Hunkemöller International B.V.

- Calvin Klein (PVH Corp.)

- Hanesbrands Inc.

- Ann Summers Ltd.

- Agent Provocateur Ltd.

- Boux Avenue (Theo Paphitis Retail Group)

- Next plc

- ASOS plc

TOP LEADING PLAYERS IN THE MARKET

- Marks and Spencer remains a cornerstone of the UK lingerie sector, renowned for its extensive range of bras and everyday essentials. The retailer leverages its strong brand heritage to maintain customer loyalty through consistent quality and inclusive sizing options. Recently, the company has invested heavily in digital transformation by enhancing its online fitting tools and expanding its direct-to-consumer capabilities. Marks and Spencer has also strengthened its sustainability credentials by introducing more products made from recycled materials and organic cotton. Their focus on comfort-driven innovation, such as wireless bras and adaptive clothing for diverse needs, has resonated well with modern consumers. By integrating omnichannel strategies and improving supply chain efficiency, the brand continues to solidify its position as a trusted household name in British intimate apparel retailing.

- Next plc operates as a major multi-channel retailer in the UK lingerie market, offering a wide variety of styles through its high street stores and popular online platform. The company utilizes its sophisticated Total Platform logistics network to ensure rapid delivery and efficient inventory management for lingerie products. Next has recently focused on expanding its private label ranges, which offer trendy designs at competitive price points to attract younger demographics. The retailer has also enhanced its digital experience by incorporating virtual styling advice and improved search functionalities on its website. By leveraging data analytics to predict fashion trends and optimize stock levels, Next ensures high availability of popular items. Their strategic emphasis on convenience and value has helped them capture a significant portion of the mainstream lingerie market across the UK.

- Wacoal Europe Wacoal Europe is a leading specialist in premium lingerie known for its superior fit engineering and high-quality craftsmanship. The company owns several respected brands, including Wacoal and Frey, which are widely available in UK department stores and independent boutiques. Wacoal has recently strengthened its market position by launching innovative collections that cater to specific body types and lifestyle needs such as sports and maternity wear. The company has also expanded its professional fitting services both in-store and through digital consultations to ensure customer satisfaction. By focusing on technical excellence and durability, Wacoal appeals to consumers seeking long-term value and comfort. Their commitment to research and development in fabric technology and ergonomic design continues to differentiate them in the competitive UK premium lingerie segment.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the UK lingerie market primarily focus on digital integration and inclusivity to enhance customer engagement and drive sales. Companies are investing in advanced sizing technologies such as artificial intelligence fit tools to reduce return rates and improve online shopping experiences. Strategic expansion of size ranges to include plus sizes and adaptive options allows brands to cater to diverse body types and promote body positivity. Sustainability initiatives, including the use of recycled fabrics and ethical production practices, are increasingly central to brand positioning and consumer appeal. Omnichannel strategies that seamlessly blend physical store experiences with e-commerce convenience help retailers maintain strong customer relationships. Collaborations with influencers and social media campaigns are utilized to build brand awareness and connect with younger demographics. These approaches enable market participants to adapt to changing consumer preferences and maintain competitiveness in a dynamic retail environment.

MARKET SEGMENTATION

This research report on the UK lingerie market is segmented and sub-segmented into the following categories.

By Lingerie Type

- Bras

- Briefs & Panties

- Shapewear

- Sleepwear & Loungewear

- Others

By Price Range

- Economy

- Mid-Range

- Premium

By Distribution Channel

- Store-Based

- Non-Store-Based

By Country

- United Kingdom

Frequently Asked Questions

1 Which product category leads the market?

Bras have the largest share in the women’s underwear and lingerie segment.

2. Which lingerie type is growing fastest?

Shapewear is expected to grow the fastest among the main product categories.

3. What are the main consumer trends?

Consumers are showing stronger interest in comfort, adaptive designs, inclusive sizing, and everyday wearability.

4. How important is online shopping?

Online sales are a major growth driver because they make it easier for shoppers to compare styles, sizes, and prices.

5. What does the broader underwear market look like?

The broader UK underwear and nightwear market is stabilising and remains a significant consumer category.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com