UK Remittance Market Size, Share, Trends, and Growth Analysis Report, Segmented by Mode of Transfer, Type, Channel, and End-Use – Industry Forecast From 2026 to 2034

UK Remittance Market Report Summary

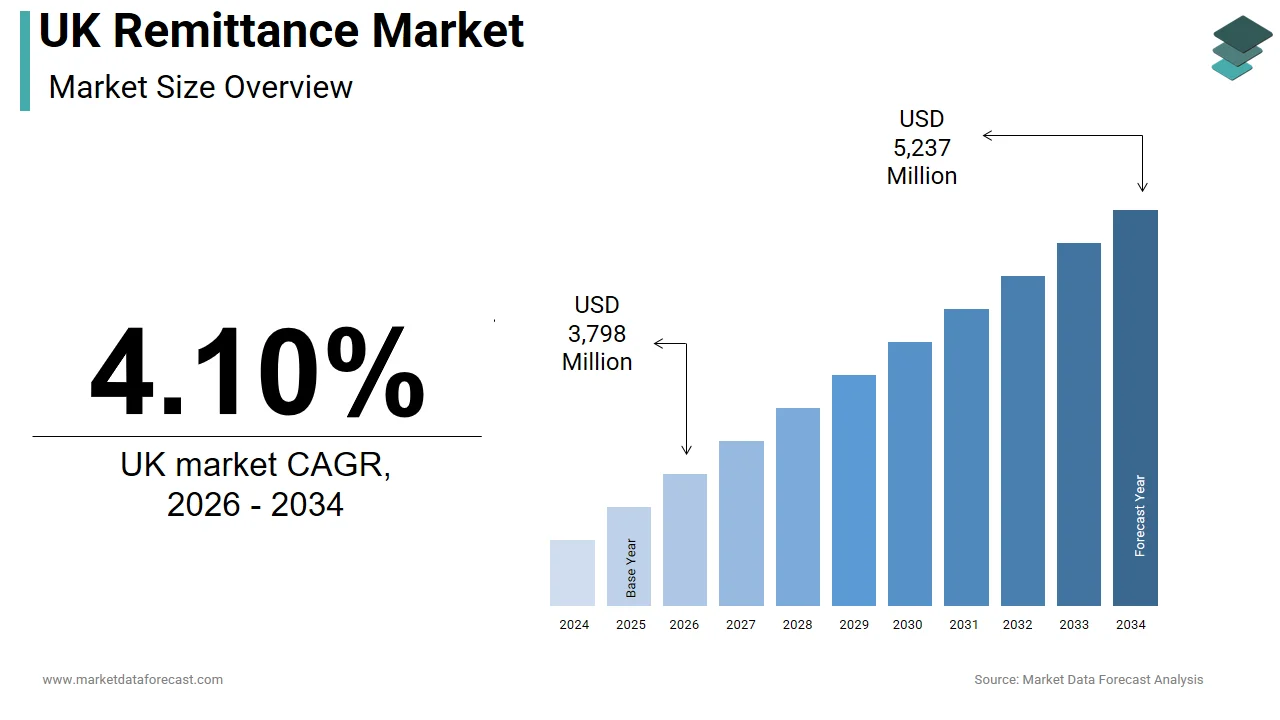

The UK remittance market was valued at USD 3,648 million in 2025, is estimated to reach USD 3,798 million in 2026, and is projected to reach USD 5,237 million by 2034, growing at a CAGR of 4.10% from 2026 to 2034. Market growth is driven by increasing international migration, rising cross-border financial transactions, and the growing adoption of digital money transfer platforms. The United Kingdom remains a major hub for global remittance flows due to its large expatriate population, diverse workforce, and strong international economic ties. Advancements in fintech solutions, mobile payment technologies, and real-time transfer capabilities are further supporting market expansion by improving transaction speed, accessibility, and cost efficiency.

Key Market Trends

- Rising adoption of digital remittance platforms and mobile money transfer services.

- Increasing demand for fast, low-cost cross-border payment solutions.

- Growing influence of fintech companies in international money transfers.

- Expansion of real-time payment infrastructure and digital wallets.

- Strengthening regulatory focus on transaction security, compliance, and anti-money laundering measures.

Segmental Insights

- Based on mode of transfer, the digital segment dominated the UK remittance market by accounting for 56.4% share in 2025, driven by increasing smartphone penetration, enhanced user convenience, and the growing popularity of online money transfer services.

- Based on type, the outward remittance segment held the largest share of 54.3% in 2025, supported by the significant number of migrant workers and expatriates sending funds to family members and beneficiaries abroad.

- Based on channel, the money transfer operators segment accounted for a dominant share of the market in 2025, owing to their extensive international networks, reliable transfer services, and broad customer reach.

- Based on end use, the migrant labor workforce segment led the market by capturing 32.3% share in 2025, driven by continuous remittance flows from foreign workers supporting households in their home countries.

Regional Insights

The UK remittance market continues to demonstrate steady growth, supported by strong migration trends, increasing digital payment adoption, and expanding cross-border financial connectivity.

- The United Kingdom remains one of Europe's most important remittance corridors due to its diverse international workforce and global business connections.

- Growing adoption of digital remittance platforms and mobile-based transfer services is transforming the remittance landscape by improving accessibility and reducing transaction costs.

- Continued fintech innovation, regulatory modernization, and rising demand for efficient cross-border payment solutions are expected to support long-term market growth.

UK Remittance Market Size

The UK remittance market was valued at USD 3,648 million in 2025, is estimated to reach USD 3,798 million in 2026, and is projected to reach USD 5,237 million by 2034, growing at a CAGR of 4.10% from 2026 to 2034.

The remittance is the cross-border transfer of funds by migrant workers to their countries of origin. The regulations are governed by the Financial Conduct Authority, which enforces strict anti-money laundering protocols and consumer protection standards. According to data from the Office for National Statistics, approximately 14% of the UK workforce consists of non-UK-born individuals, creating a substantial base for outward remittances. The cultural diversity of the nation ensures steady demand for transfers to regions, such as South Asia, Africa, and Eastern Europe. The UK remains one of the top ten source countries for global remittance flows, contributing billions annually to recipient economies. The shift toward digital platforms has transformed user experience, enabling faster and cheaper transactions compared to traditional bank wires. Mobile applications and fintech solutions have democratized access, allowing users to send money with minimal friction.

MARKET DRIVERS

Large Migrant Population and Diaspora Networks

The substantial presence of migrant communities and established diaspora networks is fuelling the growth of the United Kingdom remittance market. Individuals who relocate for work or education maintain strong familial and social ties with their home countries, necessitating regular financial support. According to data from the Office for National Statistics, there are over 9 million foreign-born residents in the UK, many of whom send money back to relatives abroad. This demographic reality creates a consistent baseline volume of transactions regardless of broader economic cycles. Indian, Pakistani, and Polish communities represent some of the largest groups driving significant flows to South Asia and Eastern Europe. These networks often rely on informal recommendations to choose service providers, fostering loyalty to specific brands. The cultural obligation to support family members during festivals, emergencies, or daily expenses ensures a high frequency of transfers. Remittances act as a lifeline for many households in developing nations, funding essential needs, such as food and medical care. The emotional connection between migrants and their families reinforces the necessity of reliable and fast transfer services. This social fabric underpins the structural demand for remittance products. Service providers tailor their offerings to cater to specific cultural preferences and language needs, enhancing accessibility.

Digital Transformation and Fintech Innovation

The rapid adoption of digital technologies and the proliferation of fintech innovations are fundamentally enhancing convenience and reducing costs, amplifying the growth of the United Kingdom remittance market. Traditional banking methods often involve high fees and slow processing times, whereas digital platforms offer instant transfers at competitive rates. User-friendly interfaces allow customers to track transactions in real time, providing transparency and peace of mind. The integration of open banking APIs facilitates seamless fund withdrawals from bank accounts without manual entry errors. Automated compliance checks using artificial intelligence speed up verification processes, reducing wait times for users. Younger demographics, particularly millennials and Generation Z, prefer digital-first experiences, driving the shift away from physical agent locations. The ability to store beneficiary details and schedule recurring payments adds further convenience for regular senders. Marketing efforts by fintech firms emphasize speed and ease of use, resonating with modern consumer expectations. This technological leap transforms remittances from a cumbersome chore into a simple digital interaction.

MARKET RESTRAINTS

Stringent Regulatory Compliance and Anti-Money Laundering Rules

The strict regulatory compliance requirements and rigorous anti-money laundering protocols is increasing operational costs and complexity, which is hampering the growth of the United Kingdom remittance market. Financial institutions and money service businesses must adhere to detailed guidelines set by the Financial Conduct Authority to prevent illicit financial flows. The failure to comply with these regulations can result in substantial fines and loss of operating licenses. These expenses are often passed on to consumers in the form of higher fees or less favorable exchange rates. The need to verify the source of funds for every transaction slows down processing times, causing frustration for users seeking immediate transfers. Small providers struggle to bear the burden of comprehensive compliance teams, leading to market consolidation. The complexity of navigating different regulatory regimes for various destination countries adds another layer of difficulty. Enhanced scrutiny on high-risk corridors may lead to de-risking, where banks terminate relationships with money transfer operators. This reduction in banking access limits the options available to consumers. The administrative burden diverts resources away from product innovation and customer service improvements.

Economic Volatility and Exchange Rate Fluctuations

The economic volatility and unpredictable exchange rate fluctuations affect the value received by beneficiaries, which is also impeding the growth of the United Kingdom remittance market. Senders are often concerned that currency depreciation in the recipient country will erode the purchasing power of their transfers. The pound sterling has experienced significant variability against major currencies such as the euro and dollar in recent years. This uncertainty discourages some migrants from sending money during times of instability, preferring to hold funds in stronger currencies. The lack of transparent pricing regarding hidden margins in exchange rates further complicates decision-making for consumers. Many users feel they do not receive fair value due to opaque fee structures. Inflationary pressures in both the UK and recipient countries reduce the disposable income available for remittances. When living costs rise in the UK, migrants may prioritize local expenses over sending money abroad. The fear of losing value through poor timing leads to hesitation and delayed transfers. This behavioral response reduces transaction frequency and volume. Providers face challenges in hedging currency risks, which can impact their profitability.

MARKET OPPORTUNITIES

Expansion into Underbanked Corridors and Emerging Markets

The expansion into underbanked corridors to tap into underserved populations is to have a positive impact on the growth of the United Kingdom remittance market. Many recipients in rural areas of Africa, Asia, and Latin America lack access to traditional banking services but possess mobile phones. According to data from the Global Findex Database, over 1 billion adults worldwide remain unbanked, representing a vast potential customer base. Mobile money accounts have grown significantly in sub-Saharan Africa, offering a viable channel for digital remittances. Partnerships with local mobile network operators allow UK providers to facilitate cash-out services at local agents. This last-mile connectivity ensures that funds reach beneficiaries directly without requiring a bank account. The lower infrastructure costs of mobile money compared to brick-and-mortar branches make it an attractive model for expansion. UK fintechs can leverage their technological expertise to integrate with these local systems seamlessly. Government initiatives in recipient countries promoting financial inclusion further support this growth. The high volume of small-value transactions in these regions offers steady revenue streams.

Integration of Blockchain and Cryptocurrency Technologies

The integration of blockchain and cryptocurrency technologies to enhance speed, transparency, and cost efficiency is also expected to escalate the growth of the United Kingdom remittance market. Distributed ledger technology enables peer-to-peer transfers without intermediaries, reducing settlement times from days to seconds. The institutional interest in stablecoins for remittances is rising due to their price stability and ease of conversion. UK providers can utilize blockchain to create immutable records of transactions, enhancing trust and auditability. Smart contracts can automate compliance checks and currency conversions, streamlining the entire process. The use of cryptocurrencies allows for 24/7 operations, bypassing traditional banking hours and holidays. This availability appeals to users who require urgent transfers outside standard business times. Regulatory clarity around crypto assets in the UK is improving, encouraging legitimate firms to explore these innovations. Early adopters can differentiate themselves by offering cutting-edge services that appeal to tech-savvy migrants. The potential for programmable money opens new possibilities for conditional transfers and financial products.

MARKET CHALLENGES

Cybersecurity Threats and Fraud Risks

The cybersecurity threats and fraud risks, as digital adoption increases the attack surface for criminals, are a challenge to the growth of the United Kingdom remittance market. Phishing scams, identity theft, and account takeover attempts target unsuspecting users seeking to steal funds or personal data. Financial fraud losses in the UK exceeded 1 billion pounds in recent years, with a significant portion linked to online payments, as per a study. The remittance platforms are frequent targets for sophisticated cyber-attacks aiming to exploit vulnerabilities in software systems. Providers must invest heavily in advanced encryption, multi-factor authentication, and real-time monitoring systems to protect user data. The evolving nature of cyber threats requires constant vigilance and updates to security protocols. Educating customers about safe practices is also crucial, but difficult to enforce consistently. The anonymity of some digital channels facilitates money laundering activities, complicating detection efforts. Regulators impose strict liability on firms for security failures, increasing operational pressure. The cost of maintaining a robust cybersecurity infrastructure strains profit margins, especially for smaller players. Balancing user convenience with stringent security measures remains a delicate task.

Intense Price Competition and Margin Compression

The intense price competition among service providers leads to margin compression challenging the profitability and sustainability is to decline the growth of the United Kingdom remittance market. The entry of numerous fintech startups has driven down fees and exchange rate margins as companies vie for market share. Consumers are highly price sensitive and readily switch providers for better deals, reducing brand loyalty. This race to the bottom forces companies to operate on thin margins, relying on high transaction volumes to remain viable. The pressure to lower costs may compromise investment in customer service and security infrastructure. Established banks struggle to compete with agile fintechs that have lower overheads and innovative business models. The expectation of free or near-free transfers sets a difficult precedent for long-term revenue generation. Providers must find alternative income streams, such as foreign exchange trading or ancillary financial services, to sustain operations. The commoditization of remittance services makes it difficult to justify premium pricing.

SEGMENTAL ANALYSIS

By Mode of Transfer Insights

The digital mode of transfer segment was the largest by holding 56.4% of the United Kingdom remittance market share in 2025, with the widespread adoption of smartphones and internet connectivity among migrant populations. The convenience, speed, and lower costs associated with digital transactions compared to traditional methods are also propelling the growth of the segment. The user-friendly interfaces of fintech companies have simplified the process, removing the need for physical visits to agent locations. Digital platforms often offer competitive exchange rates and transparent fee structures, which appeal to price-sensitive consumers. The integration of open banking allows for direct bank account linking, reducing friction during transactions. Younger people, particularly those aged 18 to 35, exhibit a near-universal preference for digital channels, driving high adoption rates. The COVID-19 pandemic accelerated this shift as lockdowns restricted movement and forced reliance on contactless services. Security features, such as biometric authentication and encryption, have built trust in digital platforms.

The digital mode segment is estimated to witness the fastest CAGR of 12.5% from 2026 to 2034, with the continuous migration of users from traditional cash-based methods to app-based solutions. The integration of artificial intelligence for fraud detection and customer support enhances the reliability of digital platforms. UK fintechs are attracting significant venture capital funding, enabling aggressive marketing and product development. The rise of neobanks offering built-in remittance features further accelerates adoption by bundling services. Younger generations entering the workforce prefer digital native solutions, driving long-term behavioral shifts. The ability to store multiple currencies and convert them instantly adds functionality that traditional methods lack. Regulatory sandboxes allow new players to test innovative features safely, fostering competition. The pandemic-induced habit formation has proven sticky, with users reluctant to return to slower methods. This structural shift ensures that digital remittance will continue to outpace all other modes.

By Type Insights

The outward segment was the largest by accounting for 54.3% of the United Kingdom remittance market share in 2025, with the large population of migrant workers sending earnings to their home countries. The UK is a net sender of remittances due to its status as a major destination for international labor. The demographic reality creates a massive volume of outbound transactions. The cultural obligation to support relatives in developing nations where wages are lower drives consistent demand. Major corridors include transfers to India, Poland Nigeria, and Pakistan, reflecting the composition of the migrant population. Outward remittances are often regular and recurring, forming a stable revenue base for providers. The economic disparity between the UK and recipient countries means that even small amounts have significant purchasing power abroad. This impact motivates senders to prioritize these transfers. Service providers focus heavily on optimizing outward flows through targeted marketing and competitive rates.

The Inward segment is also growing at the fastest CAGR of 8.5% during the forecast period, with the increasing migration levels and the rising disposable income of migrant workers. The net migration to the UK has reached record highs, expanding the base of potential senders. The digitalization of remittance channels has made it easier and cheaper to send money, encouraging a higher frequency of transfers. New entrants are focusing on niche corridors, driving volume growth. The increasing awareness of financial inclusion in recipient countries encourages more families to receive formal remittances. Government initiatives to reduce transfer costs that further spur the growth of the segment. The resilience of migrant employment in key sectors supports consistent income for remitting. The growing middle class in recipient countries increases the demand for imported goods and services funded by remittances. This economic linkage drives sustained growth. The expansion of digital wallets in recipient countries facilitates easier receipt of funds.

By Channel Insights

The money transfer operators segment held a dominant share of the United Kingdom remittance market in 2025 due to their specialized focus, extensive networks, and brand recognition among migrant communities. Companies, such as Western Union, MoneyGram, and Ria, have established a strong presence over the decades. As per the study, 50% of users prefer MTOs for their reliability and wide reach in rural areas of recipient countries. These operators have invested heavily in building agent networks that allow for cash pickup, which is in unbanked regions. Their expertise in compliance and cross-border regulations ensures smooth transactions. MTOs offer a variety of payment options, including cash card and bank deposit, catering to diverse needs. The trust built over years of operation makes them the default choice for many first-time senders. Their marketing efforts are highly targeted towards specific ethnic communities, enhancing visibility. The ability to handle large volumes efficiently keeps costs competitive. MTOs have also adapted by launching digital apps to complement their physical presence. This hybrid model combines convenience with accessibility.

The online platforms and digital wallets segment is likely to grow at the fastest CAGR of 15.2% during the forecast period, with the convenience of mobile apps and the integration of additional financial services. The number of digital wallet users in the UK is projected to grow significantly as smartphones become ubiquitous. Fintech companies like Wise, Revolut, and PayPal offer seamless user experiences with low fees and fast transfers. These platforms attract younger users, who prefer digital-first interactions. The ability to hold multiple currencies and convert them instantly adds value. Integration with e-commerce and bill payment services creates a holistic financial ecosystem. Social features, such as splitting bills and sending money to friends, enhance engagement. The lower cost structure of digital platforms allows for competitive pricing. Marketing through social media reaches target audiences effectively. The continuous addition of new features keeps users engaged. This innovation drives rapid adoption.

The unparalleled convenience of a mobile-first experience serves as a major driver for the rapid growth of online platforms and digital wallets in the United Kingdom remittance market. Users can send money anytime and anywhere using their smartphones without visiting physical locations. According to data from Ofcom, the majority of internet users access the web via mobile devices, making apps the natural choice. As per surveys by App Annie, remittance apps with intuitive interfaces see higher retention rates. The ability to save beneficiary details and schedule recurring transfers saves time and effort. Push notifications provide real-time updates on transaction status, reducing anxiety. The integration of biometric login ensures security without compromising ease of use. Users appreciate the simplicity of the process, which often takes just a few clicks. The elimination of paperwork and long queues is a significant benefit. This convenience appeals to busy professionals and young migrants. The ability to track spending and manage budgets within the app adds value. This seamless experience drives frequent usage. It transforms remittance into a simple daily task. This user-centric design sustains rapid growth. It meets the expectations of modern consumers.

By End-use Insights

The migrant labor workforce segment was the largest by holding 32.3% of the United Kingdom remittance market share in 2025, with the primary motivation of supporting families in home countries. There are millions of foreign-born workers in the UK, contributing significantly to outward flows. Remittances from this group are often regular and essential for household survival in recipient nations. The cultural norm of familial support ensures high priority for these transfers. Workers in sectors such as healthcare, construction, and hospitality are major contributors. The stability of their income allows for consistent remittance patterns. This segment is less sensitive to economic fluctuations in the UK, as sending money home is a fixed commitment. The emotional bond with family drives the volume and frequency of transfers. Service providers focus heavily on this segment with tailored products and marketing.

The small businesses segment is likely to grow at an anticipated CAGR of 10.5% during the forecast period, owing to the globalization of small enterprises and the need for cross-border payments for suppliers and partners. Many UK SMEs source materials or services from abroad, requiring efficient payment solutions. B2B cross-border payments are increasingly digitized for speed and transparency. Small businesses prefer platforms that offer competitive exchange rates and quick settlement to manage cash flow. The rise of e-commerce has enabled small firms to sell globally, increasing inbound and outbound flows. The need to pay freelancers and contractors in other countries also drives this growth. Digital platforms offer invoicing and tracking features that simplify business accounting. The lower costs compared to bank wires make these platforms attractive for SMEs. The flexibility of digital wallets supports varied payment needs.

COMPETITIVE LANDSCAPE

The United Kingdom remittance market features intense competition characterized by established global giants, agile fintech startups, and traditional banks vying for customer loyalty. Major players leverage brand recognition and extensive agent networks to maintain strong positions, while newer entrants differentiate through lower fees and superior digital experiences. Regulatory compliance with Financial Conduct Authority standards ensures high barriers to entry but also fosters trust among consumers. Price competition remains fierce as digital providers disrupt traditional pricing models by offering real exchange rates and minimal fees. Customer retention strategies focus on user-friendly interfaces and additional financial services such as currency conversion and budgeting tools. The rise of open banking facilitates integration with other financial platforms, creating interconnected ecosystems.

KEY MARKET PLAYERS

The major players in the UK remittance market include

- Western Union

- MoneyGram

- Wise

- PayPal

- TransferWise

- Revolut

- Remitly

- Skrill

- WorldRemit

- Xoom

TOP PLAYERS IN THE MARKET

- Wise operates as a leading digital money transfer service in the United Kingdom, renowned for its transparent pricing and real exchange rate model. The company has revolutionized the market by eliminating hidden fees and providing fast international transfers through its innovative platform. Wise recently expanded its multi-currency account features, allowing users to hold and manage funds in various currencies seamlessly. The firm has strengthened its position by obtaining additional banking licenses in key markets, which enhances trust and regulatory compliance. Their investment in artificial intelligence improves fraud detection and customer support efficiency significantly. Wise continues to partner with major financial institutions to integrate its infrastructure into existing banking apps. This strategic expansion ensures broader accessibility and reinforces its reputation as a cost-effective and reliable solution for modern cross-border payments.

- Western Union maintains a significant presence in the United Kingdom remittance market, leveraging its extensive global network of agents and digital platforms. The company serves millions of customers who rely on its established brand for secure and reliable money transfers worldwide. Western Union recently accelerated its digital transformation by enhancing its mobile application and online services to offer faster transaction speeds. The firm has strengthened its market position by integrating blockchain technology for select corridors to improve transparency and reduce settlement times. They have also expanded partnerships with local banks and fintech companies to increase payout options for recipients. Western Union focuses on compliance and security, ensuring adherence to strict regulatory standards. These initiatives demonstrate their commitment to modernizing traditional remittance services while maintaining their vast physical reach.

- Revolut serves as a prominent digital banking alternative in the United Kingdom, offering integrated remittance services within its comprehensive financial super app. The company allows users to send money internationally at competitive rates directly from their accounts without needing separate providers. Revolut recently introduced enhanced business accounts with specialized tools for cross-border payments and currency exchange for small enterprises. The firm has strengthened its market position by expanding its license approvals across Europe, which facilitates smoother operations post Brexit. They have invested heavily in customer experience improvements, including instant notifications and spending analytics. Revolut continues to add new currency pairs and payout methods to cater to diverse user needs. This holistic approach integrates remittance into daily banking, making it a convenient choice for tech-savvy consumers and businesses alike.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the United Kingdom remittance market employ digital innovation as a primary strategy to enhance user experience and reduce operational costs. Companies invest heavily in mobile applications and artificial intelligence to streamline transactions and improve fraud detection capabilities. This technological integration allows for faster processing times and greater transparency in pricing, which attracts cost-conscious consumers. Strategic partnerships with local financial institutions and mobile network operators expand reach into underserved regions and facilitate cash payouts. Firms also focus on regulatory compliance by implementing robust anti-money laundering systems to maintain trust and avoid penalties. Diversification of services such as multi-currency accounts and bill payments creates sticky ecosystems that retain customers. Marketing efforts target specific diaspora communities through culturally relevant campaigns to build brand loyalty. These multifaceted approaches enable participants to differentiate themselves while addressing evolving consumer expectations for speed, security, and affordability in the dynamic UK remittance landscape.

MARKET SEGMENTATION

This research report on the UK remittance market has been segmented and sub-segmented based on the following categories.

By Mode of Transfer

- Digital

- Traditional (Non-digital)

By Type

- Inward Remittance

- Outward Remittance

By Channel

- Banks

- Money Transfer Operators

- Online Platforms (Wallets)

By End-Use

- Migrant Labor Workforce

- Personal

- Small Businesses

- Others

Competitive Landscape

The UK remittance market is characterized by intense competition among traditional money transfer operators, digital remittance providers, fintech companies, and payment service platforms. Market participants are focusing on enhancing transaction speed, reducing transfer fees, expanding international payment networks, and improving user experience through digital channels. Strategic partnerships, technological innovation, and regulatory compliance remain key factors shaping competitive dynamics across the market.

Prominent companies operating in the UK remittance market include Western Union, MoneyGram, Wise, PayPal, TransferWise, Revolut, Remitly, Skrill, WorldRemit, and Xoom.

UK Remittance Market Size

The UK remittance market was valued at USD 3,648 million in 2025, is estimated to reach USD 3,798 million in 2026, and is projected to reach USD 5,237 million by 2034, growing at a CAGR of 4.10% from 2026 to 2034.

The remittance is the cross-border transfer of funds by migrant workers to their countries of origin. The regulations are governed by the Financial Conduct Authority, which enforces strict anti-money laundering protocols and consumer protection standards. According to data from the Office for National Statistics, approximately 14% of the UK workforce consists of non-UK-born individuals, creating a substantial base for outward remittances. The cultural diversity of the nation ensures steady demand for transfers to regions, such as South Asia, Africa, and Eastern Europe. The UK remains one of the top ten source countries for global remittance flows, contributing billions annually to recipient economies. The shift toward digital platforms has transformed user experience, enabling faster and cheaper transactions compared to traditional bank wires. Mobile applications and fintech solutions have democratized access, allowing users to send money with minimal friction.

MARKET DRIVERS

Large Migrant Population and Diaspora Networks

The substantial presence of migrant communities and established diaspora networks is fuelling the growth of the United Kingdom remittance market. Individuals who relocate for work or education maintain strong familial and social ties with their home countries, necessitating regular financial support. According to data from the Office for National Statistics, there are over 9 million foreign-born residents in the UK, many of whom send money back to relatives abroad. This demographic reality creates a consistent baseline volume of transactions regardless of broader economic cycles. Indian, Pakistani, and Polish communities represent some of the largest groups driving significant flows to South Asia and Eastern Europe. These networks often rely on informal recommendations to choose service providers, fostering loyalty to specific brands. The cultural obligation to support family members during festivals, emergencies, or daily expenses ensures a high frequency of transfers. Remittances act as a lifeline for many households in developing nations, funding essential needs, such as food and medical care. The emotional connection between migrants and their families reinforces the necessity of reliable and fast transfer services. This social fabric underpins the structural demand for remittance products. Service providers tailor their offerings to cater to specific cultural preferences and language needs, enhancing accessibility.

Digital Transformation and Fintech Innovation

The rapid adoption of digital technologies and the proliferation of fintech innovations are fundamentally enhancing convenience and reducing costs, amplifying the growth of the United Kingdom remittance market. Traditional banking methods often involve high fees and slow processing times, whereas digital platforms offer instant transfers at competitive rates. User-friendly interfaces allow customers to track transactions in real time, providing transparency and peace of mind. The integration of open banking APIs facilitates seamless fund withdrawals from bank accounts without manual entry errors. Automated compliance checks using artificial intelligence speed up verification processes, reducing wait times for users. Younger demographics, particularly millennials and Generation Z, prefer digital-first experiences, driving the shift away from physical agent locations. The ability to store beneficiary details and schedule recurring payments adds further convenience for regular senders. Marketing efforts by fintech firms emphasize speed and ease of use, resonating with modern consumer expectations. This technological leap transforms remittances from a cumbersome chore into a simple digital interaction.

MARKET RESTRAINTS

Stringent Regulatory Compliance and Anti-Money Laundering Rules

The strict regulatory compliance requirements and rigorous anti-money laundering protocols is increasing operational costs and complexity, which is hampering the growth of the United Kingdom remittance market. Financial institutions and money service businesses must adhere to detailed guidelines set by the Financial Conduct Authority to prevent illicit financial flows. The failure to comply with these regulations can result in substantial fines and loss of operating licenses. These expenses are often passed on to consumers in the form of higher fees or less favorable exchange rates. The need to verify the source of funds for every transaction slows down processing times, causing frustration for users seeking immediate transfers. Small providers struggle to bear the burden of comprehensive compliance teams, leading to market consolidation. The complexity of navigating different regulatory regimes for various destination countries adds another layer of difficulty. Enhanced scrutiny on high-risk corridors may lead to de-risking, where banks terminate relationships with money transfer operators. This reduction in banking access limits the options available to consumers. The administrative burden diverts resources away from product innovation and customer service improvements.

Economic Volatility and Exchange Rate Fluctuations

The economic volatility and unpredictable exchange rate fluctuations affect the value received by beneficiaries, which is also impeding the growth of the United Kingdom remittance market. Senders are often concerned that currency depreciation in the recipient country will erode the purchasing power of their transfers. The pound sterling has experienced significant variability against major currencies such as the euro and dollar in recent years. This uncertainty discourages some migrants from sending money during times of instability, preferring to hold funds in stronger currencies. The lack of transparent pricing regarding hidden margins in exchange rates further complicates decision-making for consumers. Many users feel they do not receive fair value due to opaque fee structures. Inflationary pressures in both the UK and recipient countries reduce the disposable income available for remittances. When living costs rise in the UK, migrants may prioritize local expenses over sending money abroad. The fear of losing value through poor timing leads to hesitation and delayed transfers. This behavioral response reduces transaction frequency and volume. Providers face challenges in hedging currency risks, which can impact their profitability.

MARKET OPPORTUNITIES

Expansion into Underbanked Corridors and Emerging Markets

The expansion into underbanked corridors to tap into underserved populations is to have a positive impact on the growth of the United Kingdom remittance market. Many recipients in rural areas of Africa, Asia, and Latin America lack access to traditional banking services but possess mobile phones. According to data from the Global Findex Database, over 1 billion adults worldwide remain unbanked, representing a vast potential customer base. Mobile money accounts have grown significantly in sub-Saharan Africa, offering a viable channel for digital remittances. Partnerships with local mobile network operators allow UK providers to facilitate cash-out services at local agents. This last-mile connectivity ensures that funds reach beneficiaries directly without requiring a bank account. The lower infrastructure costs of mobile money compared to brick-and-mortar branches make it an attractive model for expansion. UK fintechs can leverage their technological expertise to integrate with these local systems seamlessly. Government initiatives in recipient countries promoting financial inclusion further support this growth. The high volume of small-value transactions in these regions offers steady revenue streams.

Integration of Blockchain and Cryptocurrency Technologies

The integration of blockchain and cryptocurrency technologies to enhance speed, transparency, and cost efficiency is also expected to escalate the growth of the United Kingdom remittance market. Distributed ledger technology enables peer-to-peer transfers without intermediaries, reducing settlement times from days to seconds. The institutional interest in stablecoins for remittances is rising due to their price stability and ease of conversion. UK providers can utilize blockchain to create immutable records of transactions, enhancing trust and auditability. Smart contracts can automate compliance checks and currency conversions, streamlining the entire process. The use of cryptocurrencies allows for 24/7 operations, bypassing traditional banking hours and holidays. This availability appeals to users who require urgent transfers outside standard business times. Regulatory clarity around crypto assets in the UK is improving, encouraging legitimate firms to explore these innovations. Early adopters can differentiate themselves by offering cutting-edge services that appeal to tech-savvy migrants. The potential for programmable money opens new possibilities for conditional transfers and financial products.

MARKET CHALLENGES

Cybersecurity Threats and Fraud Risks

The cybersecurity threats and fraud risks, as digital adoption increases the attack surface for criminals, are a challenge to the growth of the United Kingdom remittance market. Phishing scams, identity theft, and account takeover attempts target unsuspecting users seeking to steal funds or personal data. Financial fraud losses in the UK exceeded 1 billion pounds in recent years, with a significant portion linked to online payments, as per a study. The remittance platforms are frequent targets for sophisticated cyber-attacks aiming to exploit vulnerabilities in software systems. Providers must invest heavily in advanced encryption, multi-factor authentication, and real-time monitoring systems to protect user data. The evolving nature of cyber threats requires constant vigilance and updates to security protocols. Educating customers about safe practices is also crucial, but difficult to enforce consistently. The anonymity of some digital channels facilitates money laundering activities, complicating detection efforts. Regulators impose strict liability on firms for security failures, increasing operational pressure. The cost of maintaining a robust cybersecurity infrastructure strains profit margins, especially for smaller players. Balancing user convenience with stringent security measures remains a delicate task.

Intense Price Competition and Margin Compression

The intense price competition among service providers leads to margin compression challenging the profitability and sustainability is to decline the growth of the United Kingdom remittance market. The entry of numerous fintech startups has driven down fees and exchange rate margins as companies vie for market share. Consumers are highly price sensitive and readily switch providers for better deals, reducing brand loyalty. This race to the bottom forces companies to operate on thin margins, relying on high transaction volumes to remain viable. The pressure to lower costs may compromise investment in customer service and security infrastructure. Established banks struggle to compete with agile fintechs that have lower overheads and innovative business models. The expectation of free or near-free transfers sets a difficult precedent for long-term revenue generation. Providers must find alternative income streams, such as foreign exchange trading or ancillary financial services, to sustain operations. The commoditization of remittance services makes it difficult to justify premium pricing.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Mode of Transfer, Type, Channel, End-Use, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Western Union, MoneyGram, Wise, PayPal, TransferWise, Revolut, Remitly, Skrill, WorldRemit, Xoom |

SEGMENTAL ANALYSIS

By Mode of Transfer Insights

The digital mode of transfer segment was the largest by holding 56.4% of the United Kingdom remittance market share in 2025, with the widespread adoption of smartphones and internet connectivity among migrant populations. The convenience, speed, and lower costs associated with digital transactions compared to traditional methods are also propelling the growth of the segment. The user-friendly interfaces of fintech companies have simplified the process, removing the need for physical visits to agent locations. Digital platforms often offer competitive exchange rates and transparent fee structures, which appeal to price-sensitive consumers. The integration of open banking allows for direct bank account linking, reducing friction during transactions. Younger people, particularly those aged 18 to 35, exhibit a near-universal preference for digital channels, driving high adoption rates. The COVID-19 pandemic accelerated this shift as lockdowns restricted movement and forced reliance on contactless services. Security features, such as biometric authentication and encryption, have built trust in digital platforms.

The digital mode segment is estimated to witness the fastest CAGR of 12.5% from 2026 to 2034, with the continuous migration of users from traditional cash-based methods to app-based solutions. The integration of artificial intelligence for fraud detection and customer support enhances the reliability of digital platforms. UK fintechs are attracting significant venture capital funding, enabling aggressive marketing and product development. The rise of neobanks offering built-in remittance features further accelerates adoption by bundling services. Younger generations entering the workforce prefer digital native solutions, driving long-term behavioral shifts. The ability to store multiple currencies and convert them instantly adds functionality that traditional methods lack. Regulatory sandboxes allow new players to test innovative features safely, fostering competition. The pandemic-induced habit formation has proven sticky, with users reluctant to return to slower methods. This structural shift ensures that digital remittance will continue to outpace all other modes.

By Type Insights

The outward segment was the largest by accounting for 54.3% of the United Kingdom remittance market share in 2025, with the large population of migrant workers sending earnings to their home countries. The UK is a net sender of remittances due to its status as a major destination for international labor. The demographic reality creates a massive volume of outbound transactions. The cultural obligation to support relatives in developing nations where wages are lower drives consistent demand. Major corridors include transfers to India, Poland Nigeria, and Pakistan, reflecting the composition of the migrant population. Outward remittances are often regular and recurring, forming a stable revenue base for providers. The economic disparity between the UK and recipient countries means that even small amounts have significant purchasing power abroad. This impact motivates senders to prioritize these transfers. Service providers focus heavily on optimizing outward flows through targeted marketing and competitive rates.

The Inward segment is also growing at the fastest CAGR of 8.5% during the forecast period, with the increasing migration levels and the rising disposable income of migrant workers. The net migration to the UK has reached record highs, expanding the base of potential senders. The digitalization of remittance channels has made it easier and cheaper to send money, encouraging a higher frequency of transfers. New entrants are focusing on niche corridors, driving volume growth. The increasing awareness of financial inclusion in recipient countries encourages more families to receive formal remittances. Government initiatives to reduce transfer costs that further spur the growth of the segment. The resilience of migrant employment in key sectors supports consistent income for remitting. The growing middle class in recipient countries increases the demand for imported goods and services funded by remittances. This economic linkage drives sustained growth. The expansion of digital wallets in recipient countries facilitates easier receipt of funds.

By Channel Insights

The money transfer operators segment held a dominant share of the United Kingdom remittance market in 2025 due to their specialized focus, extensive networks, and brand recognition among migrant communities. Companies, such as Western Union, MoneyGram, and Ria, have established a strong presence over the decades. As per the study, 50% of users prefer MTOs for their reliability and wide reach in rural areas of recipient countries. These operators have invested heavily in building agent networks that allow for cash pickup, which is in unbanked regions. Their expertise in compliance and cross-border regulations ensures smooth transactions. MTOs offer a variety of payment options, including cash card and bank deposit, catering to diverse needs. The trust built over years of operation makes them the default choice for many first-time senders. Their marketing efforts are highly targeted towards specific ethnic communities, enhancing visibility. The ability to handle large volumes efficiently keeps costs competitive. MTOs have also adapted by launching digital apps to complement their physical presence. This hybrid model combines convenience with accessibility.

The online platforms and digital wallets segment is likely to grow at the fastest CAGR of 15.2% during the forecast period, with the convenience of mobile apps and the integration of additional financial services. The number of digital wallet users in the UK is projected to grow significantly as smartphones become ubiquitous. Fintech companies like Wise, Revolut, and PayPal offer seamless user experiences with low fees and fast transfers. These platforms attract younger users, who prefer digital-first interactions. The ability to hold multiple currencies and convert them instantly adds value. Integration with e-commerce and bill payment services creates a holistic financial ecosystem. Social features, such as splitting bills and sending money to friends, enhance engagement. The lower cost structure of digital platforms allows for competitive pricing. Marketing through social media reaches target audiences effectively. The continuous addition of new features keeps users engaged. This innovation drives rapid adoption.

The unparalleled convenience of a mobile-first experience serves as a major driver for the rapid growth of online platforms and digital wallets in the United Kingdom remittance market. Users can send money anytime and anywhere using their smartphones without visiting physical locations. According to data from Ofcom, the majority of internet users access the web via mobile devices, making apps the natural choice. As per surveys by App Annie, remittance apps with intuitive interfaces see higher retention rates. The ability to save beneficiary details and schedule recurring transfers saves time and effort. Push notifications provide real-time updates on transaction status, reducing anxiety. The integration of biometric login ensures security without compromising ease of use. Users appreciate the simplicity of the process, which often takes just a few clicks. The elimination of paperwork and long queues is a significant benefit. This convenience appeals to busy professionals and young migrants. The ability to track spending and manage budgets within the app adds value. This seamless experience drives frequent usage. It transforms remittance into a simple daily task. This user-centric design sustains rapid growth. It meets the expectations of modern consumers.

By End-use Insights

The migrant labor workforce segment was the largest by holding 32.3% of the United Kingdom remittance market share in 2025, with the primary motivation of supporting families in home countries. There are millions of foreign-born workers in the UK, contributing significantly to outward flows. Remittances from this group are often regular and essential for household survival in recipient nations. The cultural norm of familial support ensures high priority for these transfers. Workers in sectors such as healthcare, construction, and hospitality are major contributors. The stability of their income allows for consistent remittance patterns. This segment is less sensitive to economic fluctuations in the UK, as sending money home is a fixed commitment. The emotional bond with family drives the volume and frequency of transfers. Service providers focus heavily on this segment with tailored products and marketing.

The small businesses segment is likely to grow at an anticipated CAGR of 10.5% during the forecast period, owing to the globalization of small enterprises and the need for cross-border payments for suppliers and partners. Many UK SMEs source materials or services from abroad, requiring efficient payment solutions. B2B cross-border payments are increasingly digitized for speed and transparency. Small businesses prefer platforms that offer competitive exchange rates and quick settlement to manage cash flow. The rise of e-commerce has enabled small firms to sell globally, increasing inbound and outbound flows. The need to pay freelancers and contractors in other countries also drives this growth. Digital platforms offer invoicing and tracking features that simplify business accounting. The lower costs compared to bank wires make these platforms attractive for SMEs. The flexibility of digital wallets supports varied payment needs.

COMPETITIVE LANDSCAPE

The United Kingdom remittance market features intense competition characterized by established global giants, agile fintech startups, and traditional banks vying for customer loyalty. Major players leverage brand recognition and extensive agent networks to maintain strong positions, while newer entrants differentiate through lower fees and superior digital experiences. Regulatory compliance with Financial Conduct Authority standards ensures high barriers to entry but also fosters trust among consumers. Price competition remains fierce as digital providers disrupt traditional pricing models by offering real exchange rates and minimal fees. Customer retention strategies focus on user-friendly interfaces and additional financial services such as currency conversion and budgeting tools. The rise of open banking facilitates integration with other financial platforms, creating interconnected ecosystems.

KEY MARKET PLAYERS

The major players in the UK remittance market include

- Western Union

- MoneyGram

- Wise

- PayPal

- TransferWise

- Revolut

- Remitly

- Skrill

- WorldRemit

- Xoom

TOP PLAYERS IN THE MARKET

- Wise operates as a leading digital money transfer service in the United Kingdom, renowned for its transparent pricing and real exchange rate model. The company has revolutionized the market by eliminating hidden fees and providing fast international transfers through its innovative platform. Wise recently expanded its multi-currency account features, allowing users to hold and manage funds in various currencies seamlessly. The firm has strengthened its position by obtaining additional banking licenses in key markets, which enhances trust and regulatory compliance. Their investment in artificial intelligence improves fraud detection and customer support efficiency significantly. Wise continues to partner with major financial institutions to integrate its infrastructure into existing banking apps. This strategic expansion ensures broader accessibility and reinforces its reputation as a cost-effective and reliable solution for modern cross-border payments.

- Western Union maintains a significant presence in the United Kingdom remittance market, leveraging its extensive global network of agents and digital platforms. The company serves millions of customers who rely on its established brand for secure and reliable money transfers worldwide. Western Union recently accelerated its digital transformation by enhancing its mobile application and online services to offer faster transaction speeds. The firm has strengthened its market position by integrating blockchain technology for select corridors to improve transparency and reduce settlement times. They have also expanded partnerships with local banks and fintech companies to increase payout options for recipients. Western Union focuses on compliance and security, ensuring adherence to strict regulatory standards. These initiatives demonstrate their commitment to modernizing traditional remittance services while maintaining their vast physical reach.

- Revolut serves as a prominent digital banking alternative in the United Kingdom, offering integrated remittance services within its comprehensive financial super app. The company allows users to send money internationally at competitive rates directly from their accounts without needing separate providers. Revolut recently introduced enhanced business accounts with specialized tools for cross-border payments and currency exchange for small enterprises. The firm has strengthened its market position by expanding its license approvals across Europe, which facilitates smoother operations post Brexit. They have invested heavily in customer experience improvements, including instant notifications and spending analytics. Revolut continues to add new currency pairs and payout methods to cater to diverse user needs. This holistic approach integrates remittance into daily banking, making it a convenient choice for tech-savvy consumers and businesses alike.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the United Kingdom remittance market employ digital innovation as a primary strategy to enhance user experience and reduce operational costs. Companies invest heavily in mobile applications and artificial intelligence to streamline transactions and improve fraud detection capabilities. This technological integration allows for faster processing times and greater transparency in pricing, which attracts cost-conscious consumers. Strategic partnerships with local financial institutions and mobile network operators expand reach into underserved regions and facilitate cash payouts. Firms also focus on regulatory compliance by implementing robust anti-money laundering systems to maintain trust and avoid penalties. Diversification of services such as multi-currency accounts and bill payments creates sticky ecosystems that retain customers. Marketing efforts target specific diaspora communities through culturally relevant campaigns to build brand loyalty. These multifaceted approaches enable participants to differentiate themselves while addressing evolving consumer expectations for speed, security, and affordability in the dynamic UK remittance landscape.

MARKET SEGMENTATION

This research report on the UK remittance market has been segmented and sub-segmented based on the following categories.

By Mode of Transfer

- Digital

- Traditional (Non-digital)

By Type

- Inward Remittance

- Outward Remittance

By Channel

- Banks

- Money Transfer Operators

- Online Platforms (Wallets)

By End-Use

- Migrant Labor Workforce

- Personal

- Small Businesses

- Others

Frequently Asked Questions

What is the UK remittance market?

The UK remittance market is the sector facilitating cross-border money transfers between the United Kingdom and other countries, serving expatriates, migrant workers, and families sending funds internationally.

How does the UK remittance market work?

In the UK remittance market, senders transfer money through banks or digital platforms to recipients abroad, with providers handling currency conversion and ensuring funds reach overseas accounts securely and efficiently.

What types exist in the UK remittance market?

The UK remittance market includes inward remittance where funds enter the UK from overseas, and outward remittance where UK residents send money to recipients in other countries for various purposes.

Who uses the UK remittance market?

The UK remittance market serves expatriates, migrant workers, international families, students, and businesses needing to transfer funds across borders for consumption, savings, or investment purposes globally.

What drives growth in the UK remittance market?

The UK remittance market grows due to increasing global diaspora, rising digital finance adoption, shift from cash to digital transactions, and expanding cross-border transactions among migrant communities worldwide.

Which countries receive remittances from the UK remittance market?

Top recipient countries from the UK remittance market include India, Pakistan, Nigeria, France, and Germany, reflecting strong migrant community connections and family funding relationships with these nations.

What sources feed the UK remittance market?

Main sources of remittances to the UK remittance market include Australia, the United States, Canada, Spain, and Ireland, where expatriates working in the UK receive funds from their home countries.

Who operates in the UK remittance market?

Major players in the UK remittance market include Revolut, Wise, Remitly, and WorldRemit, with Revolut being the most popular app for money transfers among UK consumers sending funds internationally.

Is the UK remittance market digital?

The UK remittance market has shifted significantly from cash to digital transactions, with mobile-based payment and internet banking channels dominating modern cross-border money transfer activities across the country.

What are the benefits of the UK remittance market?

The UK remittance market offers benefits like convenient digital transfer platforms, competitive exchange rates, fast transaction speeds, secure fund delivery, and accessible services for diverse expatriate communities.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com