UK Stationery Market Size, Share, Trends, and Growth Analysis Report, Segmented by Type, Application, Distribution Channel and Country – Industry Forecast From 2026 to 2034

Market Size, 2025

$1.40 BnMarket Estimate, 2026

$1.44 BnMarket Forecast, 2034

$1.80 BnCAGR, 2026–2034

2.80%UK Stationery Market Report Summary

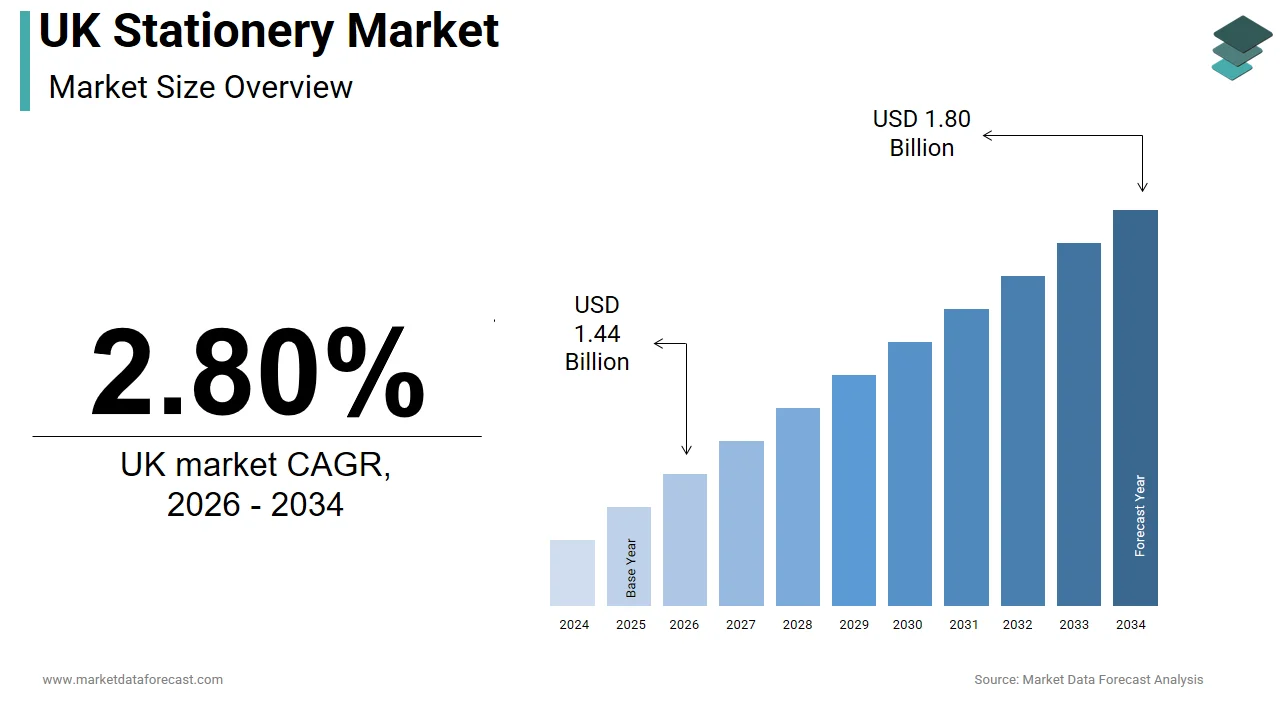

The UK stationery market was valued at USD 1.40 billion in 2025 and is projected to grow from USD 1.44 billion in 2026 to USD 1.80 billion by 2034, registering a CAGR of 2.80% from 2026 to 2034. Market growth is driven by sustained demand from educational institutions, offices, and households, along with increasing interest in creative, organizational, and premium stationery products. The market continues to benefit from rising school enrollments, hybrid work environments, and growing consumer preference for eco-friendly and customized stationery solutions. Additionally, innovations in product design and the expansion of omnichannel retail strategies are supporting steady market growth across the United Kingdom.

Key Market Trends

- Rising demand for sustainable and eco-friendly stationery products.

- Growing popularity of premium, personalized, and creative stationery items.

- Increasing adoption of stationery products for home offices and hybrid work environments.

- Expansion of omnichannel retail strategies combining online and offline sales.

- Continued demand from educational institutions, businesses, and residential consumers.

Segmental Insights

- Based on type, the paper products segment dominated the UK stationery market in 2025 by accounting for 38.9% market share, driven by its indispensable role in education, office administration, documentation, and personal organization.

- Based on application, the residential segment held the largest share of the market with 58.8% in 2025, supported by increasing use of stationery products for home-based learning, personal organization, creative activities, and remote work.

- Based on distribution channel, the offline retail segment remained dominant by capturing 62.6% share in 2025, driven by strong consumer preference for in-store product evaluation, immediate purchases, and established retail networks.

Regional Insights

The United Kingdom stationery market continues to demonstrate stable growth, supported by strong educational infrastructure, widespread office usage, and increasing consumer demand for premium stationery products.

- The United Kingdom accounted for 18.1% of the European stationery market share in 2025, making it one of the leading markets in the region.

- Market growth is supported by consistent demand from schools, universities, corporate offices, and residential users.

- Increasing interest in sustainable stationery products and the growing influence of online retail channels are further contributing to market development.

Competitive Landscape

The UK stationery market is characterized by the presence of established global and regional manufacturers competing through product innovation, sustainability initiatives, and extensive distribution networks. Companies are focusing on expanding eco-friendly product portfolios, introducing premium writing and paper products, and strengthening their presence across both physical and digital retail channels. Strategic partnerships, brand expansion, and product customization are key factors shaping competitive dynamics within the market.

Prominent companies operating in the UK stationery market include BIC Group, Staedtler Mars GmbH & Co. KG, Faber-Castell AG, Maped, Essentra plc, Pelikan International Corporation Berhad, Herlitz PBS AG, WH Smith PLC, Staples UK, Lamy, Stabilo International GmbH, ACCO Brands Corporation, and Hamelyn.

UK Stationery Market Size

The size of the UK stationery market was worth USD 1.40 billion in 2025. The market is anticipated to grow at a CAGR of 2.80% from 2026 to 2034 and be worth USD 1.80 billion by 2034 from USD 1.44 billion in 2026.

Stationery refers to a diverse array of writing instruments, paper products, organizational tools, and artistic supplies that serve both educational and professional sectors. This market is characterized by a blend of traditional physical products and evolving digital integrations reflecting the changing nature of work and study. Despite the pervasive shift towards digital communication, the tactile experience of writing and organizing remains deeply embedded in British culture. According to Department for Education data, the education sector in England comprises over 24,000 schools, establishing a massive, predictable institutional framework that consistently drives volume demand for classroom supplies and student materials. Furthermore, the creative industries contribute significantly to the economy. Backed by the Department for Culture, Media and Sport, economic indicators showing the creative sector consistently outpacing the general UK economy, a booming creative workforce has organically driven increased market demand for premium and artistic stationery. The market is also influenced by the rise of remote work, which has altered consumption patterns as individuals invest in home office setups. Broad UK office supply market reports confirm that consumer spending on home office essentials, including notebooks and pens, has stabilized at elevated levels compared to pre-pandemic figures, sustained by the permanent integration of hybrid and remote working models. Consumer preferences are increasingly leaning towards sustainable and eco-friendly options driven by environmental awareness. The integration of smart stationery that bridges physical notes with digital platforms represents an emerging trend. Thus, the UK stationery market is not merely a supplier of basic goods but a dynamic sector adapting to technological advancements and shifting lifestyle needs while maintaining its core relevance in daily personal and professional activities.

MARKET DRIVERS

Resurgence of Analog Methods for Mental Well-being

The growing recognition of the mental health benefits associated with analog activities, such as journaling and handwriting, fuels the growth of the UK stationery market. In an era dominated by digital screens, consumers are increasingly seeking tangible methods to disconnect and enhance mindfulness. According to Mental Health Foundation analysis of NHS data, one in six people in the UK experiences a common mental health problem in any given week, a statistic that highlights the growing need for accessible mental health support and resources. Handwriting and journaling have been identified as effective tools for reducing stress and improving cognitive processing. A study by the University of Washington found that handwriting activates neural circuits distinct from typing, specifically engaging regions crucial for learning and memory retention in ways that keyboarding does not. This psychological benefit has spurred a surge in the sales of premium journals, planners, and fountain pens. Retailers report increased demand for aesthetically pleasing and high-quality paper products that offer a superior writing experience. The trend is particularly strong among millennials and Generation Z, who view stationery as a form of self-care and personal expression. Social media platforms like Instagram and Pinterest amplify this trend by showcasing intricate bullet journals and calligraphy art, inspiring others to adopt similar practices. The tactile satisfaction of using high-grade paper and smooth ink flows provides a sensory experience that digital devices cannot replicate. This emotional and psychological connection to physical writing tools ensures a steady demand for specialized stationery items. Hence, manufacturers are innovating with ergonomic designs and premium materials to cater to this wellness-oriented segment, driving growth in the market.

Sustained Demand from the Education Sector

The education sector remains a foundational driver for the UK stationery market. This is due to the consistent and recurring need for learning materials across all levels of schooling. Despite the integration of digital technologies in classrooms, physical writing instruments and paper remain essential for examinations, note-taking, and creative projects. Department for Education census data confirms there are over 9 million pupils currently enrolled in schools in England, representing a massive, consistent user base for educational materials. The start of each academic year triggers a significant spike in stationery purchases as parents and institutions stock up on essentials. Guidance from the Institute of School Business Leadership (formerly NASBM) and general procurement data indicate that schools consistently allocate specific budget segments to "educational supplies," ensuring the steady procurement of classroom essentials like notebooks, pencils, and art materials. The government’s emphasis on foundational literacy and numeracy skills further reinforces the need for traditional writing tools. Additionally, the rise in homeschooling and supplementary tutoring has expanded the household consumption of stationery beyond school premises. Teachers often prefer physical resources for lesson planning and student feedback, which sustains demand for professional-grade products. The uniformity of curriculum requirements across the country ensures a standardized demand for specific types of stationery. Furthermore, initiatives promoting creativity in early childhood education drive the purchase of colorful and engaging art supplies. This institutional and familial reliance on physical materials provides a stable and predictable revenue stream for stationery manufacturers. The sheer volume of users in the education sector guarantees that it remains a primary pillar of market stability and growth.

MARKET RESTRAINTS

Digitalization and Paperless Office Initiatives

The accelerated adoption of digital technologies and paperless office initiatives is a substantial restraint on the growth of the UK stationery market. Organizations and individuals are increasingly transitioning to digital platforms for communication, documentation, and storage, reducing the reliance on physical paper and writing instruments. Research by the Confederation of British Industry (CBI) indicates that over 60% of UK firms have accelerated their adoption of new digital technologies and innovation since the pandemic, a shift that naturally enhances efficiency and reduces reliance on physical paper. Cloud computing and collaborative software tools allow for real-time editing and sharing of documents, eliminating the need for printed drafts and handwritten notes. A study reveals that the consumption of printing and writing papers in the UK has almost halved since 2017, reflecting a massive structural shift toward digital office environments. Educational institutions are also integrating tablets and laptops into curricula, which diminishes the frequency of notebook and pen usage among students. The convenience of digital search and retrieval makes electronic records more attractive than physical filing systems. This trend is further supported by environmental campaigns advocating for reduced paper waste to conserve forests and reduce carbon footprints. While niche markets for premium stationery persist, the overall volume demand for standard office supplies continues to erode. Manufacturers face the challenge of declining repeat purchases as digital alternatives offer cost-effective and space-saving solutions. The permanence of this technological shift suggests that the traditional stationery market must adapt by focusing on specialized or luxury segments rather than relying on bulk institutional sales.

Environmental Regulations and Sustainability Costs

Strict environmental regulations and the rising costs associated with sustainable production practices further hamper the expansion of the UK stationery market. Consumers and regulators are increasingly demanding eco-friendly products, which necessitates changes in manufacturing processes and material sourcing. Compliance with these regulations often requires investment in biodegradable materials and recyclable packaging, which are more expensive than conventional plastics and papers. Reports from the Federation of Small Businesses warn that small manufacturers face increasing difficulty absorbing rising compliance and operational costs, forcing many to raise prices in ways that may deter price-sensitive consumers. The transition to sustainable forestry certified paper also involves higher procurement costs and complex supply chain adjustments. Furthermore, the consumer perception of greenwashing has made brands cautious about marketing claims requiring rigorous verification and certification. These compliance burdens reduce profit margins and limit the ability of companies to compete on price with imported goods from regions with laxer environmental standards. The logistical challenges of sourcing sustainable raw materials can also lead to supply inconsistencies. While sustainability is a driver for some segments, it acts as a restraint for mass market products where the cost of competitiveness is paramount. The financial and operational pressures of adhering to high environmental standards constrain the flexibility and profitability of stationery producers in the UK market.

MARKET OPPORTUNITIES

Expansion of Eco-Friendly and Sustainable Product Lines

The growing consumer preference for environmentally responsible products offers a significant opportunity for the UK stationery market. Brands that prioritize sustainability through the use of recycled materials, biodegradable components, and ethical sourcing can differentiate themselves and capture a loyal customer base. According to sources, consumer sentiment data, the vast majority of UK shoppers express a preference for environmentally responsible brands, signaling a strong foundational market for businesses providing verified green alternatives. Companies can innovate by developing pens made from recycled plastics or wood paper produced from agricultural waste and packaging free from single-use plastics. Globally recognized certification frameworks like the Forest Stewardship Council (FSC), independently audited by bodies such as the Soil Association, provide vital marketplace credibility and clear appeal to eco-conscious shoppers. The introduction of refillable writing instruments reduces waste and offers a cost-effective long-term solution for consumers. Retailers are increasingly dedicating shelf space to sustainable brands, reflecting the shift in consumer values. Collaborations with environmental organizations can enhance brand reputation and engage communities in conservation efforts. The corporate sector is also seeking sustainable office supplies to meet its own environmental targets, creating B2B opportunities. By aligning product development with circular economy principles, manufacturers can tap into a growing segment that values ethical consumption. This opportunity allows brands to command premium prices and build long-term loyalty among environmentally aware consumers. The transition to sustainability is not just a regulatory requirement but a strategic avenue for growth and innovation in the stationery industry.

Growth in Personalized and Custom Stationery Solutions

The demand for personalized and custom stationery solutions provides a lucrative prospect for market players seeking to enhance customer engagement and value, which is likely to accelerate the expansion of the UK stationery market. Consumers are increasingly seeking unique items that reflect their individual identity and style, driving the popularity of customized notebooks, planners, and writing instruments. Digital printing technologies enable cost-effective customization, allowing customers to add names, initials, or unique designs to their stationery items. Etsy marketplace trend indicators show consistent demand for personalized stationery, custom journals, and tailored paper goods, validating a lucrative consumer niche for unique gifts and bespoke organizational tools. Corporate clients also seek branded stationery for promotional purposes and employee gifts, providing a steady B2B revenue stream. The rise of social media influencers has amplified the appeal of aesthetically pleasing and personalized desk setups, encouraging followers to purchase similar items. Brands can leverage online platforms to offer easy-to-use design tools that allow customers to visualize their custom products before purchase. This interactive experience enhances customer satisfaction and reduces return rates. The emotional connection formed through personalized items fosters brand loyalty and encourages repeat purchases. By offering customization options, stationery manufacturers can differentiate themselves in a crowded market and capture higher margins. This opportunity aligns with the broader trend towards individualization and self-expression in consumer goods.

MARKET CHALLENGES

Volatility in Raw Material Prices and Supply Chains

The volatility in raw material prices and disruptions in global supply chains continue to obstruct the growth of the UK stationery market. The production of stationery relies heavily on commodities such as paper pulp, plastics, and metals, which are subject to fluctuating global prices. Office for National Statistics (ONS) data confirms that historic inflationary pressures have led to significant increases in producer input costs, driving up the baseline expenses for UK manufacturers. The reliance on imported materials exposes the industry to currency fluctuations and trade barriers, particularly post Brexit. Also, the British Chambers of Commerce highlights that persistent supply chain disruptions and transit delays on essential components continue to restrict optimum inventory management and order fulfillment for UK enterprises. The scarcity of certain materials, such as high-quality paper pulp, has led to competitive bidding and increased costs. These challenges force manufacturers to either absorb the higher costs, reducing profit margins, or pass them on to consumers, risking reduced demand. Small and medium-sized enterprises are particularly vulnerable as they lack the bargaining power to secure favorable contracts. The unpredictability of supply chains makes long-term planning difficult and increases operational risks. Manufacturers must invest in diversified sourcing strategies and inventory management systems to mitigate these impacts. However, these adaptations require capital and expertise that may not be readily available. The ongoing instability in global markets necessitates agility and resilience from stationery producers to maintain competitiveness and profitability in the face of external shocks.

Intense Competition from Low-Cost Imports

Intense competition from low-cost imports is a serious challenge to domestic manufacturers in the UK stationery market. Global competitors, particularly from Asia, offer stationery products at lower prices due to cheaper labor and production costs. Trade data outlines a substantial volume of imported stationery goods arriving in the UK annually, creating a highly competitive pricing environment for domestic manufacturers to navigate. The prevalence of online marketplaces facilitates the entry of inexpensive imported products, making it easier for consumers to access low-cost alternatives. This price sensitivity is particularly acute in the mass market segment, where brand loyalty is low. Domestic manufacturers face the dilemma of maintaining quality and ethical standards while trying to remain price-competitive. The influx of cheap imports can also lead to perceptions of lower quality associated with the entire category if consumers have negative experiences. Protecting intellectual property and design rights against counterfeit imports is another costly and complex challenge. Local producers must focus on differentiation through quality innovation and sustainability to justify higher prices. However, this strategy limits their addressable market to premium segments. The constant pressure from low-cost competitors forces continuous efficiency improvements and cost-cutting measures, which can strain resources. This challenging competitive landscape requires strategic positioning and value addition to sustain domestic production in the UK stationery market.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Application, Distribution Channel, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | United Kingdom |

| Market Leaders Profiled | BIC Group, Staedtler Mars GmbH & Co. KG, Faber-Castell AG, Maped, Essentra plc, Pelikan International Corporation Berhad, Herlitz PBS AG, WH Smith PLC, Staples UK, Lamy, Stabilo International GmbH, ACCO Brands Corporation, Hamelyn, and Others. |

SEGMENTAL ANALYSIS

By Type Insights

In 2025, the paper products segment led the UK stationery market and captured a 38.9% share because of its indispensable role in education office administration and personal organization. This segment includes notebooks, diaries, printing paper, and envelopes, which remain essential despite digital advancements. While digital transformation has heavily shifted corporate operations toward e-signatures and cloud storage, specific regulatory compliance and legal archival mandates ensure a baseline requirement for physical documentation across selective UK business sectors. The main force moving this segment is the educational sector, where students and teachers require vast quantities of exercise books and revision materials. Moreover, the tactile nature of paper aids in learning and memory retention, which sustains its relevance in academic settings. Additionally, the rise of bullet journaling and planner culture has boosted sales of specialized paper products among adults seeking organizational tools. Retailers report consistent turnover in this category due to the consumable nature of paper, which necessitates frequent repurchasing. The versatility of paper allows it to serve multiple functions, from creative sketching to professional reporting. Manufacturers continue to innovate with eco-friendly and high-quality options to meet diverse consumer needs. This segment’s position is reinforced by the sheer volume of usage across households, schools, and offices, making it the backbone of the stationery industry. The inability of digital solutions to fully replace physical note-taking in certain contexts ensures that paper products maintain their market leadership.

On the other hand, the art and craft supplies segment is expected to exhibit a noteworthy CAGR of 6.8% between 2026 and 2034, owing to the increasing popularity of hobbies and creative expression among consumers. The segment’s growth is mainly fueled by the therapeutic benefits of artistic activities, which have gained prominence during and after the pandemic. Public health insights from the Mental Health Foundation emphasize that engaging in creative hobbies serves as an effective therapeutic outlet to reduce anxiety and improve mental well-being. Social media platforms like Instagram and TikTok have amplified this trend by showcasing DIY projects, painting tutorials, and calligraphy art, inspiring viewers to participate. The availability of affordable and high-quality supplies from both specialized retailers and online marketplaces has lowered barriers to entry for beginners. Schools are also placing greater emphasis on creative arts in the curriculum, driving institutional purchases. Furthermore, the rise of maker culture encourages people to create handmade gifts and decorations, boosting demand for diverse craft materials. This segment benefits from continuous innovation in product ranges, including eco-friendly paints and ergonomic tools. The emotional satisfaction derived from creating tangible art pieces ensures sustained interest and repeat purchases. Consequently, art and craft supplies are experiencing robust growth as they align with contemporary lifestyle trends focused on mindfulness and creativity.

By Application Insights

The residential segment occupied a 58.8% share to be the largest in the UK stationery market in 2025. This prominence of the segment was supported by the widespread use of stationery for household management education and leisure activities. Consumers purchase stationery for children’s school needs, home office setups, and personal hobbies, creating a large and consistent demand base. Office for National Statistics (ONS) data confirms there are now approximately 28.6 million households in the UK, representing a growing demographic base for essential consumer goods. The back-to-school rush is the main catalyst for this category, prompting parents to buy essential gear like pens, pencils, notebooks, and folders. Furthermore, the shift towards remote work has also increased residential demand as individuals equip home offices with necessary writing and organizational tools. Additionally, the popularity of journaling, planning, and crafting as home-based hobbies further boosts sales. Retailers cater to this segment by offering bundled packs and seasonal promotions that appeal to budget-conscious families. The convenience of purchasing stationery alongside grocery and household items in supermarkets enhances accessibility. Residential consumers also drive the trend towards personalized and aesthetically pleasing products, seeking items that reflect their personal style. This segment’s dominance is underpinned by the recurring nature of household needs and the emotional value placed on creative and organizational tools. The sheer volume of individual buyers ensures that the residential application remains the largest contributor to market revenue.

However, the commercial segment is predicted to witness the highest CAGR of 5.5% over the forecast period due to the recovery of the corporate sector and the emphasis on professional branding. The segment’s expansion is further supported by businesses restocking office supplies as employees return to physical workplaces following periods of remote work. Research by the British Promotional Merchandise Association (BPMA) confirms that companies consistently invest in branded stationery to enhance corporate identity, with 89% of respondents keeping promotional pens on their desks for long-term brand engagement. The demand for premium notebooks, executive pens, and customized organizational tools has risen as firms seek to project a professional image. Additionally, the expansion of small and medium enterprises in the UK contributes to increased procurement of office essentials. Corporate clients also prioritize sustainable and eco-friendly options to align with their environmental, social, and governance goals. Suppliers are responding by offering bulk purchasing agreements and tailored solutions that meet specific corporate needs. The integration of smart stationery for hybrid work environments further drives innovation and adoption in this segment. Businesses recognize the value of physical tools in facilitating collaboration and creativity during meetings and workshops. This strategic focus on quality and sustainability positions the commercial segment for rapid expansion as organizations rebuild and modernize their operational infrastructure.

By Distribution Channel Insights

The offline retail segment remained dominant in the UK stationery market and accounted for a 62.6% share in 2025. This dominance of the segment was driven by the tactile nature of the products and the immediate need for supplies. Consumers prefer to physically inspect items such as pens, notebooks, and art materials to assess quality, texture, and design before purchasing. The primary driver is the convenience of immediate availability, particularly for urgent needs such as school supplies or office replacements. In addition, the sensory experience of testing pen smoothness or paper thickness influences buying decisions significantly. Educational institutions and businesses often prefer offline procurement for bulk orders to ensure timely delivery and verify product specifications. Local stationery shops also provide personalized service and expert advice, which builds customer loyalty. The presence of major retail chains ensures wide geographic coverage, making stationery accessible to diverse demographics. Seasonal promotions and back-to-school campaigns in physical stores drive significant foot traffic and sales volumes. While online shopping is growing, the immediacy and tangibility offered by offline retail sustain its dominant position. The ability to see and feel products reduces the risk of dissatisfaction and returns, reinforcing consumer preference for brick-and-mortar channels.

But the online e-commerce segment is estimated to register the fastest CAGR of 9.2% from 2026 to 2034. This rapid growth of the segment is propelled by convenience, variety, and competitive pricing. Consumer trust in digital retail and unlimited product choices is driving the growth of this segment. E-commerce platforms allow customers to compare prices, read reviews, and access niche or imported products that may not be available locally. The convenience of home delivery appeals to busy professionals and parents who save time by ordering supplies in bulk. Subscription services for regular delivery of essential items like printer paper and ink cartridges further enhance customer retention. Social media marketing and influencer endorsements drive traffic to online stores, creating awareness for new and trendy stationery items. Digital tools such as virtual previews for personalized products enhance the shopping experience and reduce uncertainty. The ability to access global brands and unique artisanal products expands consumer choices beyond local offerings. As logistics improve and delivery times shorten, the appeal of online shopping continues to rise. This channel’s agility and reach enable it to capture a growing share of the market, particularly among younger demographics who prioritize ease and selection.

COUNTRY ANALYSIS

United Kingdom UK Stationery Market Analysis

The United Kingdom followed closely behind in the European stationery market and held a 18.1% share in 2025. This expansion of the UK market was propelled by high consumption rates and a strong cultural appreciation for quality writing instruments and paper goods. Moreover, the driving factors for the market include the mandatory requirement for physical writing materials in schools and universities, which ensures a consistent baseline demand. The UK market thrives on a mix of tradition and innovation, fueled by a strong education system and a robust corporate sector. The presence of over 21,000 state-funded and independent schools in the UK creates a vast institutional customer base that procures stationery in large volumes, often managed via decentralized School Procurement guidelines. Consumer preferences are shifting towards sustainable and premium products, reflecting broader environmental and lifestyle trends. As per the British Retail Consortium, retailers are expanding their eco-friendly ranges to meet this demand, enhancing market diversity. The creative industries in the UK also contribute significantly by driving sales of specialized art and craft supplies. Urban centers like London serve as hubs for design and innovation, influencing national trends. The aging population supports demand for easy-to-use and ergonomic stationery products. Additionally, the strong presence of international and local brands ensures a competitive landscape that fosters quality and variety. These factors combined ensure that the UK remains a key player in the regional market with steady growth potential driven by educational needs and evolving consumer values.

COMPETITIVE LANDSCAPE

The competition in the United Kingdom stationery market is characterized by a mix of established retailers, specialized distributors, and emerging online platforms. Major players compete on product variety, price, and service quality to capture both residential and commercial segments. The market sees intense rivalry in the premium segment, where brands differentiate through design and sustainability credentials. Online retailers challenge traditional brick-and-mortar stores by offering convenience and wider selections, often at lower prices. Private label products from supermarkets and large retailers exert pressure on branded manufacturers by providing cost-effective alternatives. Innovation in eco-friendly materials becomes a key competitive advantage as consumers prioritize environmental responsibility. Small independent shops compete by offering niche and artisanal products that appeal to specific customer interests. Strategic partnerships with schools and businesses help companies secure long-term contracts and stabilize revenue. The ease of switching suppliers in the commercial sector increases price sensitivity and demands high service standards. Overall, the market requires continuous adaptation to digital trends and consumer preferences to sustain growth and profitability in this fragmented and evolving industry.

KEY MARKET PLAYERS

The major players in the UK stationery market include

- BIC Group

- Staedtler Mars GmbH & Co. KG

- Faber-Castell AG

- Maped

- Essentra plc

- Pelikan International Corporation Berhad

- Herlitz PBS AG

- WH Smith PLC

- Staples UK

- Lamy

- Stabilo International GmbH

- ACCO Brands Corporation

- Hamelyn

TOP PLAYERS IN THE MARKET

- Essentra plc is a leading distributor of business-critical components, including packaging and stationery supplies, serving diverse industries across the United Kingdom. The company contributes significantly by providing efficient supply chain solutions and a vast product range to corporate clients. Recent actions include the expansion of its digital platform to enhance customer experience and streamline procurement processes for business users. Essentra has also focused on sustainability by introducing eco-friendly packaging options and reducing waste in its operations. The company strengthens its market position through strategic partnerships with manufacturers, ensuring reliable availability of high-quality products. By investing in logistics infrastructure, Essentra improves delivery speeds and service reliability. These initiatives help the company maintain strong relationships with existing clients while attracting new businesses seeking comprehensive supply solutions. Their commitment to innovation and customer-centric services ensures continued relevance in the evolving UK stationery and industrial supply landscape.

- WH Smith PLC remains a prominent retailer in the UK stationery market, leveraging its extensive network of high street and travel stores. The company offers a wide assortment of writing instruments, notebooks, and educational supplies catering to students and professionals. Recent strategies involve revitalizing store formats to create engaging shopping experiences and expanding its own brand offerings to provide value-driven options. WH Smith has enhanced its online presence by improving website functionality and offering click and collect services for greater convenience. The retailer actively participates in back-to-school campaigns,, driving seasonal sales through targeted promotions. By focusing on core categories and optimizing inventory management, WH Smith ensures product availability and competitive pricing. The company also emphasizes sustainability by sourcing responsible materials for its private label products. These efforts reinforce its brand loyalty and attract customers seeking reliable and accessible stationery solutions in both physical and digital channels.

- Staples UK serves as a key provider of office supplies and stationery solutions for businesses and consumers throughout the region. The company contributes by offering a comprehensive catalog of products ranging from basic writing tools to advanced office equipment. Recent actions include the enhancement of its B2B services with tailored contracts and bulk purchasing options for corporate clients. Staples has invested in technology to improve its e-commerce platform, enabling easier navigation and faster checkout processes. The company focuses on sustainability by promoting recycled paper products and energy-efficient office solutions. Staples also provides value-added services such as printing and tech support, which differentiate it from competitors. By maintaining a strong logistical network, Staples ensures timely deliveries and consistent stock levels. These initiatives help the company retain its competitive edge and meet the diverse needs of modern workplaces. Their customer-focused approach and operational efficiency strengthen their position in the dynamic UK stationery market.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the UK stationery market primarily employ product differentiation strategies to stand out in a crowded landscape. Companies focus on developing eco-friendly and sustainable products to appeal to environmentally conscious consumers. Digital transformation is another major strategy with firms enhancing their e-commerce platforms for a better user experience. Partnerships with educational institutions and corporations help secure bulk contracts and ensure steady revenue streams. Brands invest in marketing campaigns that highlight the mental health benefits of analog activities like journaling. Innovation in design and functionality such as ergonomic pens and smart notebooks, drives consumer interest. Retailers optimize supply chains to reduce costs and improve delivery speeds. Private label development allows companies to offer competitive pricing while maintaining profit margins. Customer loyalty programs are utilized to encourage repeat purchases and gather valuable data. These multifaceted approaches enable participants to adapt to changing trends and maintain competitiveness.

MARKET SEGMENTATION

This research report on the UK stationery market has been segmented and sub-segmented based on the following categories.

By Type

- Paper Products

- Writing Instruments

- Art & Craft

- Others

By Application

- Residential

- Commercial

By Distribution Channel

- Offline

- Online/ E-commerce

Frequently Asked Questions

What is the UK stationery market?

The UK stationery market includes pens, pencils, notebooks, paper, desk accessories, art supplies, greeting cards, envelopes, and writing materials used in offices, schools, and homes across the United Kingdom.

Why is the UK stationery market growing?

The UK stationery market is growing due to education sector demand, remote work trends, creative hobbies, personalized stationery preferences, and continued need for physical writing and organizational materials.

Who buys products from the UK stationery market?

Students, schools, offices, businesses, artists, crafters, households, and professionals purchase from the UK stationery market for writing, organization, creative projects, and administrative needs.

What products are included in the UK stationery market?

The UK stationery market includes pens, pencils, markers, notebooks, paper, staplers, folders, binders, desk organizers, art supplies, greeting cards, and school stationery essentials.

How does education impact the UK stationery market?

Education drives the UK stationery market through school supplies, student stationery needs, educational institutions, exam materials, and back-to-school seasonal purchasing cycles nationwide.

What challenges face the UK stationery market?

Challenges in the UK stationery market include digitalization reducing paper use, e-commerce competition, supply chain disruptions, price sensitivity, and changing workplace practices favoring digital tools.

Which demographic uses the UK stationery market most?

Students, teachers, office workers, artists, and craft enthusiasts represent the largest demographics in the UK stationery market for regular stationery purchases and supplies.

How does remote work affect the UK stationery market?

Remote work shapes the UK stationery market through increased home office setup demand, personal organization tools, writing materials, and planners for remote productivity.

What role does creativity play in the UK stationery market?

Creativity drives the UK stationery market through art supplies, craft materials, journaling, bullet planning, personalized stationery, and hobby-related writing and creative products.

Is the UK stationery market competitive?

Yes, the UK stationery market is highly competitive with major brands, budget retailers, specialty stationery shops, online marketplaces, and private label products across multiple channels.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com