U.S Car Finance Market Size, Share, Trends & Growth Forecast Report Segmented By Source Type (OEM, Bank, Financial Institution), Flavor, Distribution Channel, And Country (California, Washington, Oregon, New York & Rest of the United States) – Industry Analysis And Forecast, 2026 To 2034

U.S. Car Finance Market Report Summary

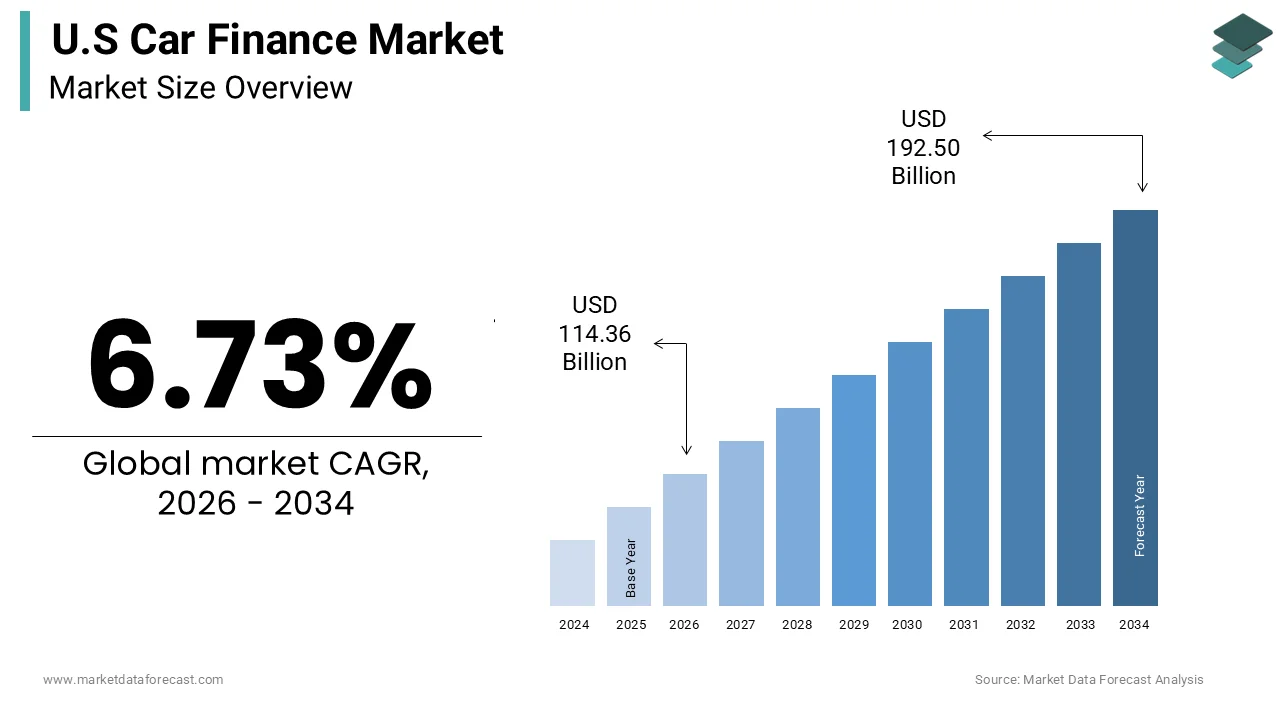

The United States car finance market was valued at USD 107.15 billion in 2025 and is projected to reach USD 192.50 billion by 2034, growing from USD 114.36 billion in 2026 at a CAGR of 6.73% during the forecast period. Market growth is driven by increasing vehicle ownership, rising demand for used cars, and expanding availability of flexible financing options. Digital lending platforms, competitive interest rates, and partnerships between automakers and financial institutions are further accelerating the growth of the U.S. car finance market.

Key Market Trends

- Rising demand for used vehicle financing

- Increasing adoption of digital and online auto loan platforms

- Growth in flexible financing and leasing options

- Expansion of AI-based credit assessment and loan approvals

- Increasing partnerships between banks, automakers, and fintech companies

Segmental Insights

- Based on source type, the bank segment dominated the U.S. auto finance market in 2025 by accounting for 46.7% of the market share, supported by competitive interest rates and strong consumer trust

- Based on vehicle type, the used car segment held the largest share in 2025 at 32.1%, driven by affordability and increased demand for pre-owned vehicles

- Based on purpose, the loan segment led the market in 2025 due to consumer preference for vehicle ownership and flexible repayment options

Competitive Landscape

- The U.S. car finance market is highly competitive, with companies focusing on digital transformation, faster loan approvals, and customer-centric financing solutions. Market players are investing in AI-driven lending technologies, flexible payment plans, and partnerships with automotive dealerships to strengthen their market presence.

- Prominent players in the U.S. car finance market include Ally Financial, Capital One, Bank of America, Wells Fargo, JPMorgan Chase, Toyota Financial Services, Ford Motor Credit Company, GM Financial, Santander Consumer USA, Honda Financial Services, BMW Financial Services, TD Auto Finance, USAA, Credit Acceptance Corporation, and Westlake Financial.

U.S Car Finance Market Size

The U.S car finance market size was calculated to be USD 107.15 billion in 2025 and is anticipated to be worth USD 192.50 billion by 2034, from USD 114.36 billion in 2026, growing at a CAGR of 6.73% during the forecast period.

Car finance is the acquisition of vehicles through loans, leases, and retail installment contracts for consumers and commercial entities. The ecosystem involves diverse lenders, including traditional banks, credit unions, captive finance arms of automakers, and independent finance companies. The average transaction price for new vehicles has surged significantly, with data from Kelley Blue Book indicating figures exceeding 48000 dollars, which necessitates longer loan terms and higher financing amounts. Consumers increasingly opt for terms extending beyond 60 months, with some reaching 72 or 84 months to manage monthly payments. The cost of used cars and trucks remains a significant component of the consumer price index, influencing borrowing behavior. The average credit score for new vehicle loans hovers around 73,0 while used vehicle loans average slightly lower. The integration of digital platforms has transformed the application process, enabling faster approvals and enhanced customer experiences. Regulatory oversight by the Consumer Financial Protection Bureau ensures transparency in lending practices, protecting borrowers from predatory tactics.

MARKET DRIVERS

Persistent Consumer Reliance on Personal Transportation Infrastructure

The enduring dependence on personal vehicles for daily commuting and logistical needs is significantly promoting the growth of the United States car finance market. Unlike many other developed nations, the US lacks comprehensive public transportation networks in suburban and rural areas, making private vehicle ownership a necessity rather than a luxury. Only a small fraction of households in non-urban areas have access to reliable public transit, forcing residents to rely on personal cars. This structural reality ensures a consistent baseline demand for vehicle acquisitions regardless of economic fluctuations. The Federal Highway Administration reports that there are over 280 million registered vehicles in the United States, underscoring the scale of automotive dependency. The geographic sprawl of American cities further exacerbates this need as distances between residential zones and commercial centers remain vast. The average American household makes multiple trips daily, most of which are conducted via personal vehicles. This habitual usage drives the replacement cycle for aging fleets, prompting consumers to seek financing for newer models. The lack of viable alternatives means that even during periods of high interest rates, consumers prioritize vehicle purchases to maintain mobility. Lenders recognize this inelastic demand and continue to extend credit to a broad spectrum of borrowers.

Expansion of Digital Lending Platforms and Fintech Integration

The rapid expansion of digital lending platforms and fintech integration is another attribute driving the growth of the US car finance market. Traditional brick-and-mortar dealership financing is increasingly being supplemented or replaced by online lenders, who offer streamlined application processes and competitive rates. The digital auto lending has grown substantially as consumers prefer the convenience of comparing offers from multiple lenders without visiting physical locations. Fintech companies utilize advanced algorithms and alternative data sources to assess creditworthiness, enabling faster approvals and broader access to credit for underserved populations. The time required to secure an auto loan has decreased from several days to mere minutes through automated underwriting systems. This technological advancement enhances the customer experience and reduces friction in the purchasing journey. Dealerships are also adopting digital tools to integrate financing options directly into their online sales platform,s creating a seamless end-to-end transaction. The use of artificial intelligence allows lenders to personalize loan terms based on individual risk profiles, improving approval rates and reducing default risks. The ability to pre-qualify for loans online empowers consumers to negotiate better deals at dealerships. Furthermore, digital platforms facilitate the management of loan servicing payments and refinancing options through user-friendly mobile applications. This technological shift lowers operational costs for lenders and passes savings onto borrowers in the form of competitive interest rates.

MARKET RESTRAINTS

Escalating Interest Rates and Monetary Policy Tightening

The escalation of interest rates driven by monetary policy tightening, by increasing the cost of borrowing for consumers, is impeding the growth of the United States car finance market. The Federal Reserve has raised benchmark interest rates to combat inflation, which directly influences the prime rate and subsequently auto loan rates. This substantially increases the total cost of vehicle ownership, making monthly payments less affordable for average households. As per Edmunds, the average monthly payment for a new vehicle has surpassed 700 dollars, placing a strain on household budgets. Higher interest rates discourage potential buyers from entering the market or prompt them to delay purchases until conditions improve. Lenders also become more risk-averse, tightening credit standards and requiring higher down payments, which further limits accessibility. The impact is particularly severe for subprime borrowers who face even higher rates and stricter qualification criteria. As per the New York Federal Reserve, delinquency rates on auto loans have increased as borrowers struggle to meet higher payment obligations. This financial pressure reduces the volume of new loan originations and slows down the overall growth of the market. Consumers may opt to repair existing vehicles rather than purchase new ones, extending the lifecycle of older cars and reducing demand for fresh financing. The uncertainty surrounding future rate hikes also creates hesitation among buyers and lenders alike.

Deteriorating Credit Quality and Rising Delinquency Rates

The deteriorating credit quality and rising delinquency rates among borrowers are another factor limiting the growth of the US car finance market. As economic pressures mount, many consumers are struggling to keep up with their auto loan payments, leading to an increase in defaults and repossessions. The delinquency rate for auto loans has climbed steadily, with subprime borrowers showing the highest rates of missed payments. This trend signals a weakening in the financial health of a significant segment of the borrowing population. Lenders respond to this heightened risk by tightening lending standards, which reduces the pool of eligible borrowers and slows loan origination volumes. The rise in delinquencies is attributed to various factors, including inflationary pressures on household expenses and the exhaustion of pandemic-era savings. High vehicle prices have also led to larger loan amounts and longer terms, which increase the likelihood of negative equity situations. When borrowers owe more than the vehicle is worth, they are more likely to default if faced with financial hardship. The number of repossessions has increased as lenders take action to recover losses. This environment creates a vicious cycle where tighter credit leads to fewer sales and higher risks lead to stricter lending.

MARKET OPPORTUNITIES

Growth of Electric Vehicle Adoption and Specialized Financing Products

The accelerating adoption of electric vehicles through the development of specialized financing products and incentives is creating new opportunities for the growth of the United States car finance market. Government policies and environmental concerns are driving a shift towards electrification, with federal tax credits and state rebates making EVs more attractive to consumers. Lenders are creating tailored financing solutions that account for the unique depreciation curves and maintenance costs of electric vehicles. The sales of electric vehicles are projected to constitute a growing share of total vehicle sales, requiring robust financial support structures. Captive finance companies are offering competitive lease rates and low-interest loans to promote EV adoption among mainstream consumers. The residual value risk associated with EVs is being managed through innovative lease structures that guarantee buyback values. The banks are partnering with charging network providers to bundle financing with home charger installation costs. This holistic approach enhances the appeal of EV ownership and expands the addressable market for lenders. The transition to electric fleets in the commercial sector also opens avenues for large-scale financing deals. Corporate sustainability goals are driving businesses to electrify their vehicle portfolios, creating demand for specialized commercial lending products. Lenders who develop expertise in EV valuation and risk assessment will gain a competitive advantage.

Expansion of Subscription-Based Mobility and Flexible Ownership Models

The emergence of subscription-based mobility and flexible ownership models for innovation is solely to leverage the growth of the US car finance market. Consumers increasingly seek alternatives to traditional long-term loans and leases, preferring short-term commitments that include insurance, maintenance, and roadside assistance. Finance companies are launching subscription services that allow customers to swap vehicles monthly or quarterly, catering to changing lifestyle needs. This model appeals to younger demographics and urban dwellers who value access over possession. The interest in vehicle subscriptions has risen among consumers who desire the ability to drive different types of vehicles for various occasions. Lenders can bundle financing with service packages, creating recurring revenue streams and deeper customer relationships. The data generated from subscription usage provides valuable insights into consumer preferences and vehicle performance. As per industry analysis, partnerships between automakers and tech firms are facilitating the development of seamless digital platforms for subscription management. This shift enables lenders to capture value beyond interest income through service fees and insurance commissions. The flexibility of subscriptions also reduces the risk of long-term depreciation for lenders as vehicles are returned frequently. Corporate clients are also adopting subscription models for employee mobility programs, creating B2B opportunities.

MARKET CHALLENGES

Volatility in Used Vehicle Valuations and Residual Value Risk

The volatility in used vehicle valuations and residual value risk for lenders and leasing companies is acting as a major barrier to the growth of the US car finance market. The unprecedented surge in used car prices during the pandemic, followed by a subsequent correction, has created uncertainty in forecasting future vehicle values. This volatility impacts lease structures, where residual values are set at the inception of the contract. The normalization of supply chains has led to an increase in inventory, which puts downward pressure on used car prices. Lenders must adjust their risk models frequently to account for these fluctuations, which increases operational complexity. High loan-to-value ratios exacerbate the problem as borrowers may find themselves underwater on their loans, leading to strategic defaults. The uncertainty complicates the pricing of loan products and lease agreements, forcing institutions to build larger buffers against potential losses. Insurance costs for financed vehicles also rise in volatile markets, adding to the burden on consumers. Lenders are becoming more conservative in setting residual values, which can make leases less attractive to consumers.

Regulatory Scrutiny and Compliance Burdens on Lending Practices

The intensifying regulatory scrutiny and compliance burdens on lending practices are another factor that hinders the growth of the US car finance market. The Consumer Financial Protection Bureau and other regulatory bodies are closely monitoring auto lending for unfair, deceptive, or abusive acts and practices. The enforcement actions have increased against lenders accused of discriminatory pricing or hidden fees in auto loan contracts. This regulatory environment requires financial institutions to invest heavily in compliance infrastructure and legal oversight. Lenders must ensure transparent disclosure of all loan terms, including interest rates, fees, and insurance requirements, to avoid penalties. The scrutiny extends to indirect lending channels where dealerships act as intermediaries, raising concerns about markup practices. The regulators are examining the use of algorithmic underwriting to ensure it does not perpetuate bias against protected classes. This examination requires lenders to audit their models regularly and provide explanations for automated decisions. The threat of litigation and fines creates a cautious atmosphere where lenders may restrict certain products or markets. State-level regulations also vary, adding complexity for national lenders who must adhere to multiple legal frameworks. The need for continuous adaptation to changing rules slows down product launches and increases operational friction.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 6.73% |

| Segments Covered | By Source Type, Vehicle Type, Purpose, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado. |

| Market Leaders Profiled | Ally Financial, Capital One Financial Corporation, Bank of America, Wells Fargo, JPMorgan Chase & Co., Toyota Financial Services, Ford Motor Credit Company, GM Financial, Santander Consumer USA, Honda Financial Services, BMW Financial Services, TD Auto Finance, USAA, Credit Acceptance Corporation, Westlake Financial |

SEGMENTAL ANALYSIS

By Source Type Insights

The bank segment was the dominant one by holding 46.7% of the United States auto finance market share in 2025 due to its extensive branch networks and established customer relationships. Banks leverage their existing deposit bases to offer competitive interest rates that attract prime borrowers seeking stability and trust. The trust factor associated with traditional banking institutions further amplifies their prominence, as borrowers prefer dealing with regulated entities during high-value transactions. Additionally, banks have invested heavily in digital platforms enabling quick approval processes that rival online only lenders while maintaining the security standards expected by risk-averse customers. The comprehensive suite of financial products offered by banks allows for bundled services such as insurance and home loans, which creates stickiness and reduces churn rates among auto loan customers. This holistic approach to customer relationship management ensures that banks remain the primary choice for a significant portion of American car buyers who value long-term financial partnerships over transient lending options.

The financial institution segment is projected to grow at the fastest CAGR of 6.2% throughout the forecast period. Credit unions are gaining traction due to their member-owned structure, which typically results in lower interest rates and more flexible underwriting criteria for individuals with varied credit histories. Captive finance companies affiliated with original equipment manufacturers are also contributing to this rapid growth by offering promotional financing deals, such as 0% interest rates, to stimulate vehicle sales. These specialized lenders have deep insights into vehicle residual value,s allowing them to structure attractive lease and loan packages that independent lenders cannot match easily. The agility of these institutions in adopting new technologies for faster loan processing, combined with their targeted marketing strategies towards specific consumer segments, drives their accelerated market penetration.

By Vehicle Type Insights

The used car segment was the largest by capturing 32.1% of the United States auto finance market share in 2025, with the significant price disparity between new and pre-owned vehicles. This price sensitivity drives higher volume in used car loans, as buyers seek to minimize monthly payments and total interest costs over the life of the loan. Lenders have responded by expanding their used car lending programs with longer terms extending up to 84 months to make these loans more manageable for average income earners. The widespread availability of certified pre-owned programs from major dealerships has also enhanced consumer confidence in the quality and reliability of used vehicles, reducing the perceived risk associated with such purchases. Furthermore, the robust supply of off-lease vehicles is entering a steady stream of relatively new models with low mileage that appeal to budget-conscious buyers who still desire modern features and safety technologies.

The new car segment is expected to grow at the fastest CAGR of 5.8% from 2026 to 2034, with the increasing adoption of electric vehicles and advanced safety technologies. Consumers are increasingly willing to pay a premium for new vehicles that offer the latest innovations in connectivity, autonomous driving features, and electrification. The Alliance for Automotive Innovation reports that electric vehicle sales accounted for nearly 10% of all new car sales in the United States, reflecting a strong shift in consumer preference towards sustainable transportation options. Government incentives, such as federal tax credits for electric vehicle purchases, further stimulate demand for new cars by effectively lowering the upfront cost for buyers. Automakers are also focusing on direct-to-consumer sales models and subscription services that bundle financing with maintenance and insurance, making new car ownership more convenient and predictable. The scarcity of used electric vehicles due to their recent market entry means that buyers interested in electrification must often purchase new thus driving growth in this segment. Additionally, the improved residual values of certain new vehicle segments, particularly trucks and sport utility vehicles, make them attractive assets for financing as lenders perceive lower risk in lending against these high-demand categories.

By Purpose Insights

The loan segment held a prominent share of the United States auto finance market in 2025 due to the cultural preference for ownership and the flexibility it offers to consumers. Most American buyers view vehicle ownership as a long-term asset-building strategy rather than a temporary usage right, which aligns naturally with loan structures that lead to full equity upon completion. The ability to customize loan terms, including down payment amounts and repayment periods, allows borrowers to tailor financing to their specific cash flow situations, making loans accessible to a broader demographic. Unlike leases, loans do not impose mileage restrictions or wear and tear penalties, which appeals to families and individuals who use their vehicles extensively for daily commutes and road trips. The rise of buy here, pay here dealerships and subprime lending has also expanded the reach of auto loans to consumers with less than perfect credit histories who may not qualify for lease agreements. These lenders often focus exclusively on loan products providing a pathway to vehicle ownership for underserved populations.

The lease segment is growing at an anticipated CAGR of 7.5% during the forecast period, with the desire for lower monthly payments and access to newer vehicles more frequently. Leasing allows consumers to drive higher-end models with advanced features for a fraction of the cost of purchasing them outright, which appeals to status-conscious buyers and tech enthusiasts. The business model of leasing aligns well with the rapid pace of technological change in the automotive industry, as it enables drivers to upgrade to the latest safety and infotainment systems every few years without the hassle of selling a used car. Corporate fleets and small businesses also contribute to this growth as leasing offers tax advantages and simplifies expense management by bundling maintenance and depreciation into a single monthly payment. The emergence of flexible lease terms and early termination options has reduced the perceived rigidity of traditional leases, making them more attractive to younger consumers who value mobility and adaptability.

COMPETITION OVERVIEW

The competition in the United States auto finance market is characterized by intense rivalry among traditional banks, credit unions, captive finance companies, and independent lenders. Traditional banks leverage their extensive branch networks and established customer relationships to maintain a strong foothold in the prime lending space. Credit unions attract members with lower rates and personalized service,e appealing to community-oriented borrowers seeking favorable terms. Captive finance companies affiliated with automakers use subsidized rates and promotional deals to stimulate vehicle sales and capture market share at the point of purchase. Independent lenders and fintech firms disrupt the status quo by offering rapid online approvals and flexible criteria for on-prem borrowers. The convergence of these players creates a dynamic ecosystem where convenience and cost efficiency are paramount. Digital platforms have lowered entry barriers, allowing new entrants to challenge incumbents with agile business models. Regulatory compliance remains a critical factor influencing competitive strategies as institutions navigate evolving legal requirements. The constant pressure to innovate drives continuous improvement in customer experience and operational efficiency across the industry.

KEY MARKET PLAYERS

A few major players of the U.S auto finance market include

- Ally Financial

- Capital One Financial Corporation

- Bank of America

- Wells Fargo

- JPMorgan Chase & Co

- Toyota Financial Services

- Ford Motor Credit Company

- GM Financial

- Santander Consumer USA

- Honda Financial Services

- BMW Financial Services

- TD Auto Finance

- USAA

- Credit Acceptance Corporation

- Westlake Financial

Top Strategies Used by Key Market Participants

Key participants in the United States auto finance market employ diversification of funding sources to ensure liquidity and stability during economic shifts. They invest heavily in digital transformation initiatives to automate underwriting processes and enhance customer engagement through mobile applications. Strategic partnerships with original equipment manufacturers allow lenders to offer exclusive incentives that drive volume and brand loyalty. Companies utilize advanced data analytics to refine risk assessment models, enabling more precise pricing and reduced default rates. Expansion into subprime lending segments provides growth opportunities by catering to underserved populations with tailored financial products. Mergers and acquisitions are common strategies used to consolidate market presence and acquire technological capabilities quickly. Lenders also focus on improving customer retention by offering flexible repayment options and loyalty rewards programs. Cybersecurity enhancements are prioritized to protect sensitive borrower information and maintain trust in digital platforms.

MARKET SEGMENTATION

This research report on the US car finance market has been segmented and sub-segmented based on source type, vehicle type, purpose & region.

By Source Type

- OEM

- Bank

- Financial Institution

By Vehicle Type

- Used car

- New car

By Purpose

- Loan

- Lease

By Region

- New York

- Texas

- Florida

- Georgia

- California

- Rest of U.S.

Frequently Asked Questions

1. What factors are driving the growth of the U.S. car finance market?

Rising vehicle prices, growing demand for used cars, flexible financing options, and digital lending platforms are driving market growth.

2. Who are the leading companies in the U.S. car finance market?

Major players include Ally Financial, Capital One Financial Corporation, and Ford Motor Credit Company.

3. What are the common types of car financing available in the U.S.?

Common financing options include direct auto loans, dealership financing, leasing, refinancing, and online auto lending.

4. Why is used car financing becoming more popular?

Used car financing is increasing due to affordability concerns and rising prices of new vehicles.

5. What role do banks play in the U.S. car finance market?

Banks provide vehicle loans, refinancing services, and competitive interest rates for consumers and businesses.

6. What are the major challenges in the U.S. car finance market?

Key challenges include rising interest rates, loan defaults, inflation, and stricter lending regulations.

7. What is the importance of vehicle leasing in the market?

Leasing provides lower monthly payments and allows consumers to upgrade to newer vehicles more frequently.

8. Which distribution channels are important in car finance services?

Banks, credit unions, automotive dealerships, captive finance companies, and online lenders are major channels.

9. What are the future growth opportunities in the U.S. car finance market?

Growth opportunities include EV financing, AI-driven lending, digital loan processing, and subscription-based vehicle ownership models.

10. How is technology improving customer experience in car financing?

Technology enables faster approvals, digital documentation, automated credit assessments, and personalized financing solutions.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com