Global Islamic Finance Market Size, Share, Trends, & Growth Forecast Report Segmented By Financial Sector (Islamic Banking, Islamic Insurance-Takaful, Islamic Bonds ‘Sukuk’, Other Islamic Financial Institutions (OIFI’s) and Islamic Funds) and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa), Industry Analysis From 2026 to 2034

Market Size, 2025

$2.71 BnMarket Estimate, 2026

$2.99 BnMarket Forecast, 2034

$6.5 BnCAGR, 2026–2034

10.2%Global Islamic Finance Market Summary

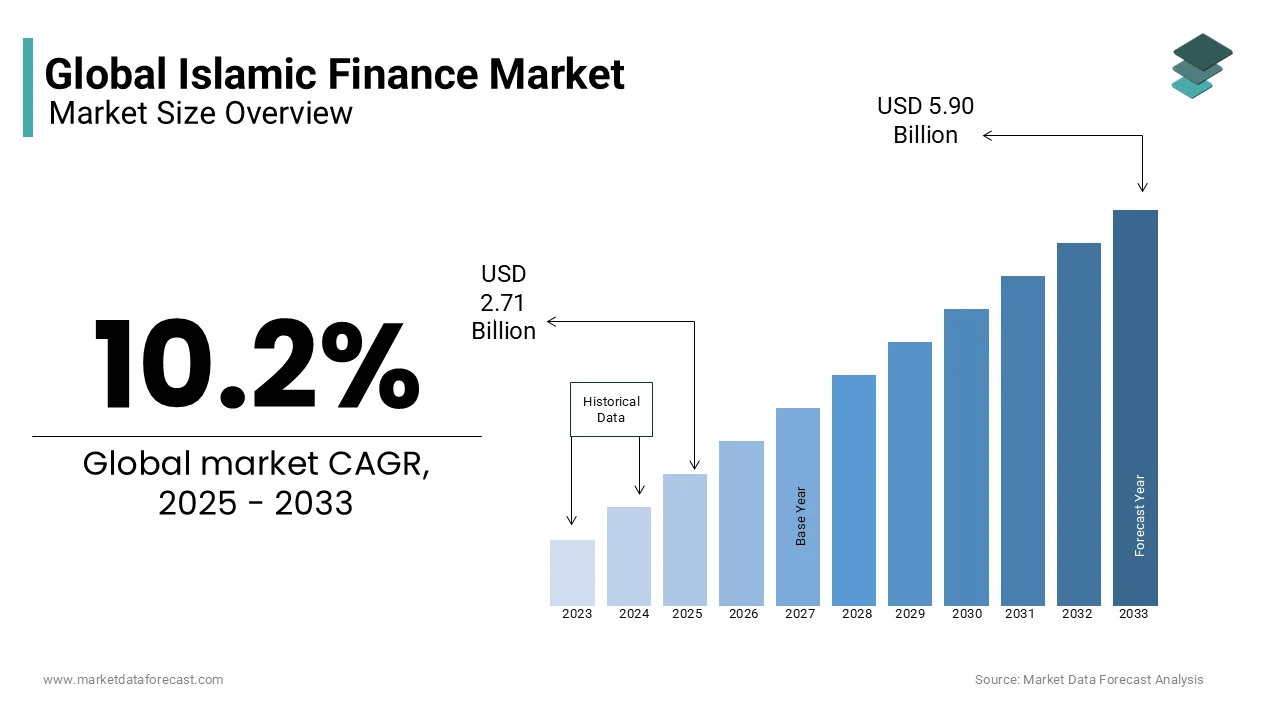

The global Islamic finance market was valued at USD 2.71 billion in 2025 and is projected to reach USD 6.50 billion by 2034, increasing from USD 2.99 billion in 2026 at a healthy CAGR of 10.2% (2026 to 2034). Growth is supported by rising demand for Sharia-compliant financial products, increasing Islamic banking penetration, and supportive regulatory frameworks across key regions.

Key Market Trends

- Expansion of Sharia-compliant banking products across emerging economies.

- Growing adoption of Sukuk (Islamic bonds) for infrastructure financing.

- Increasing demand for Islamic fintech solutions, including digital banking and mobile wallets.

- Rising preference for ethical and socially responsible investments aligned with Islamic principles.

Segmental Insights

- Based on the financial sector, the Islamic banking segment dominated the market in 2024, driven by increasing customer preference for Sharia-compliant savings, loans, and financing solutions.

- Islamic insurance (Takaful) and capital markets are also witnessing strong adoption as awareness of Islamic finance principles expands.

Regional Insights

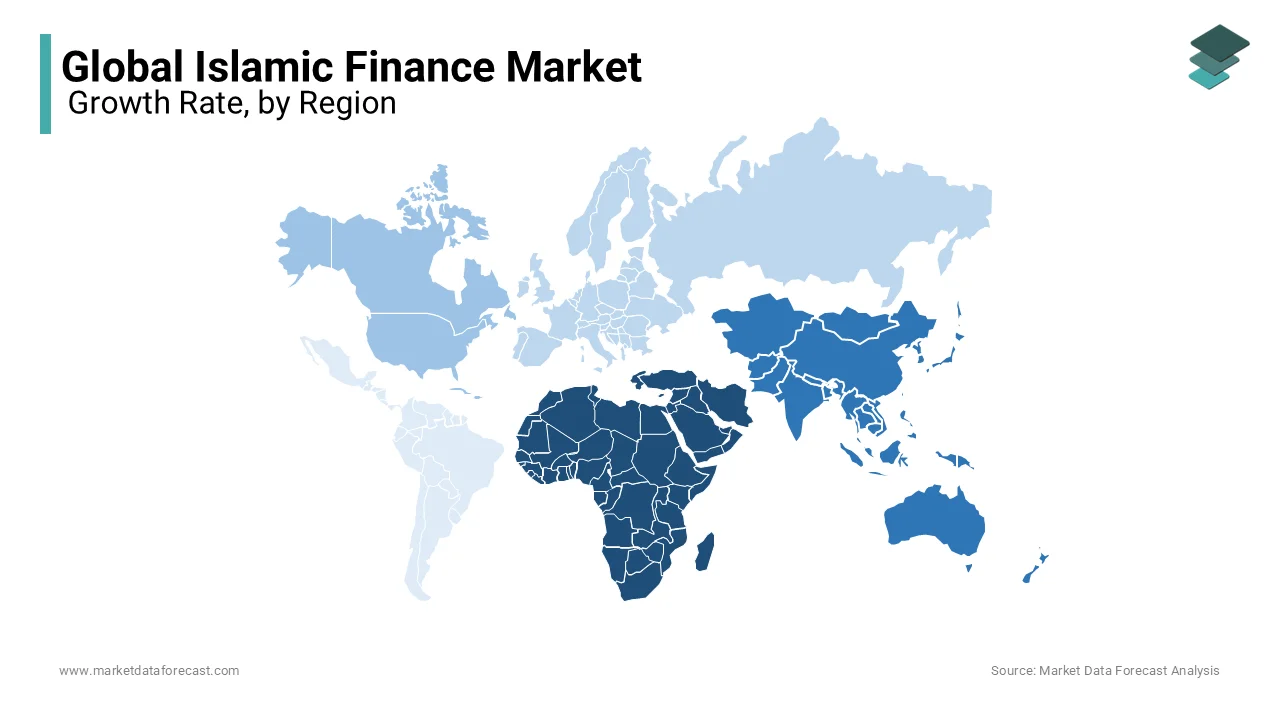

- Asia Pacific led the global market in 2024, accounting for a 42.3% share, supported by strong demand in countries such as Malaysia, Indonesia, and Pakistan.

- Middle East & Africa is expected to remain a key growth hub, led by Saudi Arabia, UAE, and other Gulf countries with well-established Islamic banking institutions.

- Europe is witnessing gradual adoption, with the UK positioning itself as a leading non-Muslim hub for Islamic finance.

- North America and Latin America are emerging regions, with growing interest in ethical financing models.

Competitive Landscape

The Islamic finance market is dominated by leading players such as Bank Al-Rajhi, Dubai Islamic Bank, Kuwait Finance House, Bank Mellat Iran, Bank Meli Iran, National Commercial Bank Saudi Arabia, Bank Maskan Iran, Qatar Islamic Bank, and Abu Dhabi Islamic Bank, all of which are expanding their Sharia-compliant offerings and digital solutions.

Global Islamic Finance Market Size

The global Islamic finance market was worth USD 2.71 billion in 2025. The global market is predicted to grow to USD 6.50 billion by 2034 from USD 2.99 billion in 2026, rising at a CAGR of 10.2% from 2026 to 2034.

Islamic finance is a financial system grounded in the principles of Sharia law, which prohibits interest (riba), speculative uncertainty (gharar), and investments in activities deemed unethical, such as gambling, alcohol, and pork-related industries. Instruments such as Murabaha (cost-plus financing), Ijara (leasing), Musharaka (joint venture), and Sukuk (Islamic bonds) form the backbone of this ecosystem. The network of Islamic financial institutions spans more than 70 countries, with Malaysia, Saudi Arabia, and the United Arab Emirates serving as pivotal hubs. According to the State of the Global Islamic Economy Report 2023, issued by DinarStandard, approximately 44% of Muslims globally express a preference for Islamic financial products, even in non-majority Muslim countries, indicating a growing consciousness of religiously aligned economic behavior. Furthermore, the Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI) has standardized over 100 Sharia governance rulings, enhancing institutional credibility.

MARKET DRIVERS

Rising Global Muslim Population and Income Growth

The rapid expansion of the muslim population and rising disposable incomes among Muslim-majority populations are majorly driving the growth of the Islamic finance market. Projections indicate this figure will grow to 2.2 billion by 2030, with significant concentration in Asia, the Middle East, and Africa. This demographic surge is accompanied by increasing urbanization and a burgeoning middle class, particularly in Indonesia, Pakistan, and Malaysia. The Asian Development Bank notes that the combined GDP per capita in Indonesia and Malaysia surpassed USD 14,000 and USD 12,800, respectivel,y in 2023, enabling greater financial inclusion and demand for Sharia-compliant credit, savings, and investment vehicles. Moreover, younger, tech-savvy Muslims are increasingly seeking financial products that align with their ethical and religious values.

Institutionalization and Regulatory Support in Key Jurisdictions

The deepening institutional and regulatory infrastructure in leading Islamic financial centers is additionally to enhance the growth of the Islamic finance market. Countries such as Malaysia, the UAE, and Bahrain have established comprehensive legal and supervisory frameworks that legitimize and standardize Islamic financial operations. Malaysia, often regarded as a global leader, has implemented a dual-tier banking system since 1993, allowing full-fledged Islamic banks and Islamic windows within conventional banks to operate under the oversight of Bank Negara Malaysia. As of 2023, Islamic banking assets in Malaysia accounted for 31% of total banking assets, amounting to approximately USD 320 billion, as per data from the central bank. The UAE has similarly institutionalized Islamic finance through dedicated regulatory bodies like the Central Bank of the UAE and the Dubai Islamic Economy Initiative, which aims to position Dubai as the global capital of the Islamic economy. The country hosts over 20 fully licensed Islamic banks and financial institutions.

MARKET RESTRAINTS

Fragmentation in Sharia Governance and Standardization

The lack of uniformity in Sharia interpretation and governance across jurisdictions is hampering the growth of the Islamic finance market. While institutions like AAOIFI and the Islamic Financial Services Board (IFSB) have developed standards, national regulators often adopt divergent rulings based on local schools of Islamic jurisprudence (madhabs), leading to product incompatibility. For instance, Malaysia follows the Shafi’i school, while Saudi Arabia adheres predominantly to the Hanbali interpretation, resulting in differing acceptability of financial contracts. As of 2023, only 18 out of 70 countries with Islamic financial operations fully recognize AAOIFI standards, according to the IFSB’s Global Islamic Finance Development Report. This fragmentation complicates cross-border transactions and discourages institutional investors seeking regulatory harmonization. In 2022, a Sukuk issuance in Indonesia was delayed by three months due to disagreements between local Sharia boards and international investors over the permissibility of a profit-sharing mechanism. Additionally, the absence of a globally recognized Sharia auditing framework undermines transparency. A 2023 study by the International Centre for Education in Islamic Finance (INCEIF) revealed that 42% of Islamic banks in Africa operate without certified Sharia compliance officers, increasing the risk of non-compliance. This regulatory dissonance not only raises operational costs but also diminishes investor trust, particularly among non-Muslim stakeholders who rely on standardized due diligence.

Limited Talent Pool and Specialized Human Capital

The professionals equipped with dual expertise in Islamic jurisprudence and modern financial engineering are impeding the growth of the Islamic finance market. As of 2023, there are fewer than 1,200 qualified Sharia board members globally, according to the Islamic International Rating Agency (IIRA), serving over 2,000 Islamic financial institutions. Furthermore, the integration of fintech and digital banking has increased demand for professionals who understand both blockchain-based asset tokenization and Sharia-compliant contract law expertise that is exceedingly rare. A 2023 survey by the Cambridge Institute of Islamic Finance found that 67% of Islamic banks in the Gulf Cooperation Council (GCC) struggle to recruit staff with adequate Sharia-financial literacy.

MARKET OPPORTUNITIES

Expansion of Islamic Fintech and Digital Financial Inclusion

The integration of Islamic finance and financial technology is creating new opportunities for the growth of the Islamic finance market. As of 2023, over 600 Islamic fintech startups operate globally, with a 35% year-on-year increase in funding, according to the Cambridge Centre for Alternative Finance. Platforms such as Wahed Invest (Malaysia/US), Niyofr (UAE), and Amana (Indonesia) offer Sharia-compliant robo-advisory, peer-to-peer financing, and digital wallets, catering to younger, digitally native Muslims. In Indonesia, where 68 million adults remain unbanked, digital Islamic finance platforms have reached over 12 million users, as reported by the OJK. The integration of blockchain for transparent Wakf (endowment) management and smart contracts for automated Murabaha transactions enhances efficiency and trust. These innovations lower transaction costs, improve accessibility, and align with the UN Sustainable Development Goals by promoting inclusive finance.

Green and Sustainable Islamic Finance Initiatives

The alignment of Islamic finance principles with environmental, social, and governance (ESG) objectives is additionally at leveraging the growth of the Islamic finance market. The prohibition of harmful industries and emphasis on real asset-backing inherently support ethical and sustainable investment. As of 2023, global sustainable Sukuk issuance exceeded USD 22 billion, with Malaysia accounting for 58% of the total, according to the Climate Bonds Initiative. The concept of “green Waqf” is gaining traction, with Indonesia allocating 10,000 hectares of Waqf land for agroforestry and solar energy projects, as reported by the Ministry of Religious Affairs in 2023. Additionally, the Islamic Development Bank has committed USD 5 billion to climate finance by 2025, prioritizing water, energy, and food security in member countries.

MARKET CHALLENGES

Liquidity Management and Short-Term Sharia-Compliant Instruments

Liquidity management due to the scarcity of short-term is likely to decline the growth of the Islamic finance market. Conventional banks rely on interbank lending and interest-bearing securities for daily liquidity adjustments, but Islamic banks cannot engage in interest-based transactions, limiting their access to equivalent tools. In contrast, the conventional global money market exceeds USD 10 trillion. This imbalance forces Islamic banks to hold higher levels of liquid assets, reducing profitability. The absence of deep, liquid secondary markets for Sukuk further exacerbates the issue, as institutions struggle to meet sudden cash demands without incurring losses.

Cross-Border Regulatory and Taxation Disparities

Islamic financial institutions encounter significant hurdles in international operations due to inconsistent regulatory treatment and tax policies across jurisdictions. The United Kingdom, despite hosting a growing Islamic finance sector, does not offer specific tax exemptions for Sukuk, unlike Malaysia, which grants tax-free status for certain Islamic bonds. According to the OECD, only 12 out of 38 member countries have established clear tax guidelines for Islamic financial products. This disparity increases compliance costs and discourages foreign investment. Additionally, the absence of mutual recognition agreements between Sharia boards complicates product harmonization. In 2023, the European Commission acknowledged that divergent legal interpretations of Murabaha contracts across EU member states impede the development of a unified Islamic capital market. These regulatory frictions limit the global integration of Islamic finance, forcing institutions to tailor products for each jurisdiction, thereby reducing economies of scale.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 10.02% |

| Segments Covered | By Financial Sector and Region |

|

Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

|

Market Leaders Profiled | Bank Al-Rajhi, Dubai Islamic Bank, Kuwait Finance House, Bank Mellat Iran, Bank Meli Iran, National Commercial Bank Saudi Arabia, Bank Maskan Iran, Qatar Islamic Bank and Abu Dhabi Islamic Bank |

SEGMENTAL ANALYSIS

By Financial Sector Insights

The Islamic banking segment held a dominant share of the Islamic finance market in 2024 owing to the sector’s maturity, widespread institutional presence, and deep integration into national economies across Muslim-majority regions. Similarly, in Saudi Arabia, Islamic banks held a 58% share of the domestic banking market by asset size in 2023, as per the Saudi Central Bank (SAMA), driven by mandatory compliance with Sharia principles across all financial operations. The sector benefits from robust regulatory support, with 33 countries having established dedicated licensing and supervision frameworks for Islamic banks. The sector’s asset-backed model, emphasizing Murabaha and Ijara, ensures alignment with real economic activity by enhancing stability and public trust.

The Islamic funds segment is likely to grow with an expected CAGR of 12.4% from 2025 to 2033, with the rising investor demand for Sharia-compliant asset management solutions among high-net-worth individuals and institutional investors in the Gulf Cooperation Council (GCC) and Southeast Asia. In the UAE, the Securities and Commodities Authority reported a 28% year-on-year increase in Sharia-compliant mutual fund registrations in 2022, which signals strong market momentum. Another contributing factor is the integration of environmental, social, and governance (ESG) criteria, which aligns naturally with Islamic ethical principles. A 2023 survey by Morningstar found that 61% of investors in sustainable funds in Europe and North America perceived Islamic funds as inherently ESG-aligned.

REGIONAL ANALYSIS

Asia Pacific Islamic Finance Market Analysis

Asia Pacific was the largest and held 42.3% of the global Islamic finance market share in 2024, with the economic scale and institutional maturity of countries like Malaysia, Indonesia, and Pakistan, which collectively host over 60% of the world’s Muslim population. The country’s Islamic fintech sector has attracted over USD 1.2 billion in investment since 2020, driven by platforms like Amana and Alami. Pakistan’s Islamic banking sector, though smaller in absolute terms, has achieved a 22% market share in total banking assets, as per the State Bank of Pakistan, reflecting strong domestic demand.

The Middle East & Africa Islamic finance market held 30.2% of the share in 2024. The UAE, home to Dubai International Financial Centre (DIFC) has emerged as a global hub for Islamic capital markets, with over 20 licensed Islamic banks and USD 120 billion in Islamic banking assets as of 2023, as reported by the Central Bank of the UAE. Egypt has also advanced its Islamic finance framework, with the Capital Markets Authority approving the first Sharia-compliant exchange-traded fund in 2022.

Europe Islamic Finance Market Analysis

Europe Islamic finance market is likely to have significant growth opportunities in the coming years. The UK government issued the first sovereign Sukuk in a non-Muslim majority country in 2014, raising GBP 200 million, which signals a strong institutional commitment. France has followed suit, with the Paris Europlace initiative promoting Islamic finance as part of its financial diversification strategy. Luxembourg has become a preferred jurisdiction for Islamic fund domiciliation, hosting over 40 Sharia-compliant funds with combined AUM exceeding EUR 15 billion in 2023, as per the Luxembourg for Finance agency. The European Central Bank has acknowledged the need for regulatory clarity, particularly in harmonizing the treatment of profit-sharing investment accounts (PSIAs) across member states.

North America Islamic Finance Market Analysis

North America Islamic financial market is prompting new opportunities in the coming years. The U.S. Muslim population, estimated at 3.45 million in 2023 by the Pew Research Center, represents a growing consumer base with increasing demand for Sharia-compliant financial products. However, regulatory and tax barriers have limited institutional development. Canada has made more progressive strides, with the federal government exploring the feasibility of Sukuk issuance for infrastructure projects, as outlined in a 2022 report by the Canadian Securities Administrators. The province of Ontario has permitted the establishment of Islamic investment funds under its securities law.

Latin America Islamic Finance Market Analysis

Latin America Islamic finance market is deemed to grow with Brazil, Argentina, and the United Arab Emirates, with early-stage development. Brazil is home to the largest Muslim population in Latin America, estimated at 1.5 million, concentrated in São Paulo and Rio de Janeiro, according to the Brazilian Islamic Cultural Center. In 2022, the UAE and Brazil signed a bilateral agreement to promote Islamic finance cooperation, including the potential issuance of sovereign Sukuk for renewable energy projects. Argentina has explored Islamic finance as a tool for debt restructuring, with discussions in 2023 about issuing Sukuk to attract Gulf-based investors, as reported by the Central Bank of Argentina. Chile has hosted Islamic finance forums in collaboration with the Islamic International Rating Agency, aiming to position Santiago as a regional hub. The Inter-American Development Bank has recognized the potential of Islamic microfinance in poverty alleviation, particularly in rural areas. Although institutional infrastructure is underdeveloped, the region’s rich natural resources and growing interest in ethical finance present long-term opportunities.

KEY MARKET PLAYERS

Bank Al-Rajhi, Dubai Islamic Bank, Kuwait Finance House, Bank Mellat Iran, Bank Meli Iran, National Commercial Bank Saudi Arabia, Bank Maskan Iran, Qatar Islamic Bank, and Abu Dhabi Islamic Bank are some of the key companies in the global Islamic finance market.

TOP LEADING PLAYERS IN THE MARKET

- Dubai Islamic Bank, established in 1975, is widely recognized as the world’s first full-service Islamic bank and remains a pioneering force in shaping the global Islamic finance landscape. The bank has played a foundational role in developing Sharia-compliant financial instruments and structuring innovative financing models that align with both commercial viability and religious principles. DIB has consistently influenced industry standards through its robust governance framework and active participation in international Islamic finance forums. Its expertise in corporate financing, retail banking, and asset management has served as a benchmark for emerging institutions across Asia, Africa, and Europe.

- Maybank Islamic Berhad, the Islamic banking arm of Malaysia’s largest financial group, has been instrumental in positioning Malaysia as a global leader in Islamic finance. The institution has driven innovation through integrated digital platforms, sustainable finance initiatives, and cross-border collaborations that enhance the accessibility and scalability of Sharia-compliant services. Maybank Islamic has been at the forefront of green Sukuk development and Islamic fintech integration, setting precedents for environmentally responsible Islamic finance. Its holistic approach extends beyond banking to include takaful, wealth management, and advisory services, reinforcing a comprehensive ecosystem.

- Al Rajhi Bank, headquartered in Saudi Arabia, stands as one of the largest Islamic banks globally and a symbol of the successful fusion between traditional values and modern financial services. Rooted in centuries-old Islamic commercial practices, the bank has evolved into a sophisticated financial institution offering retail, corporate, and SME banking solutions grounded in Sharia principles. Al Rajhi has significantly contributed to financial inclusion in the Gulf region by expanding branch networks and digital services tailored to diverse customer needs. The bank’s conservative risk management and emphasis on asset-backed financing have reinforced stability and long-term resilience. Its operational model has inspired numerous institutions in the Middle East and South Asia, serving as a template for sustainable growth within an ethical framework.

RECENT MARKET DEVELOPMENTS

- In March 2024, Maybank Islamic launched a blockchain-powered platform for Sukuk issuance in collaboration with a regional regulatory authority by enabling faster, transparent, and tamper-proof bond transactions.

- In January 2024, Dubai Islamic Bank partnered with a European sustainable investment fund to co-develop a Sharia-compliant green infrastructure financing initiative targeting renewable energy projects in Africa.

- In June 2023, Al Rajhi Bank expanded its digital banking suite with AI-driven Sharia advisory tools by enhancing customer decision-making for investment and financing products.

- In February 2024, Kuwait Finance House formalized a strategic alliance with a leading Islamic fintech startup to integrate peer-to-peer financing solutions into its retail banking operations.

- In May 2023, CIMB Islamic established a dedicated sustainability office to oversee the development and certification of ESG-aligned Islamic financial products across its ASEAN markets.

MARKET SEGMENTATION

This research report on the global Islamic finance market has been segmented and sub-segmented into the following categories.

By Financial Sector

- Islamic Banking

- Islamic Insurance – Takaful

- Islamic Bonds ‘Sukuk’

- Other Islamic Financial Institutions (OIFI’s)

- Islamic Funds

By Region

- North America

- The Middle East and Africa

- South Asia

- Asia-Pacific

- Europe

Frequently Asked Questions

1. What are the main products available in the Islamic Finance Market?

Key products in the Islamic Finance Market include Sukuk (Islamic bonds), Takaful (Islamic insurance), Mudarabah, Musharaka, Murabaha, and Ijara (leasing), all structured to comply with Shariah principles.

2. Why is the Islamic Finance Market growing rapidly worldwide?

The Islamic Finance Market is expanding due to rising demand for ethical finance, an increasing Muslim population, supportive regulations, and digital transformation in financial services.

3. Which regions dominate the Islamic Finance Market?

The Islamic Finance Market is most developed in the Middle East, Southeast Asia (Malaysia, Indonesia), and is expanding into Africa, Europe, and North America.

4. What role does Sukuk play in the Islamic Finance Market?

Sukuk are Shariah-compliant bonds central to the Islamic Finance Market, supporting capital raising for governments and corporations without interest-based structures.

5. How is the Islamic Finance Market regulated?

The Islamic Finance Market is regulated by national regulators, Shariah advisory boards, and international bodies like IFSB, ensuring compliance with both financial and religious standards.

6. What trends are shaping the future of the Islamic Finance Market?

Key trends include digitalization, rise of fintech, ESG/green sukuk, cross-border investment, and personalized online banking solutions in the Islamic Finance Market.

7.How does the Islamic Finance Market support financial inclusion?

By providing ethical and interest-free financial services, the Islamic Finance Market enables greater inclusion among unbanked Muslim and non-Muslim populations.

8. Are digital and fintech companies active in the Islamic Finance Market?

Yes, digital transformation, including neobanks and fintech startups, is rapidly enhancing accessibility and efficiency in the Islamic Finance Market.

9. What challenges face the Islamic Finance Market today?

Challenges include limited active secondary markets for certain products, regulatory harmonization, Shariah interpretation differences, and digital adoption pace.

10. How do Shariah boards influence the Islamic Finance Market?

Shariah boards play a critical role in product development, compliance, and trust-building within the Islamic Finance Market by enforcing religious guidelines.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com