U.S Diaper Market Size, Share, Trends & Growth Forecast Report Segmented By End User (Babies, Adults), Material, Price Range, Distribution Channel, And Country (California, Washington, Oregon, New York & Rest of The United States) – Industry Analysis and Forecast, 2026 To 2034

U.S. Diaper Market Report Summary

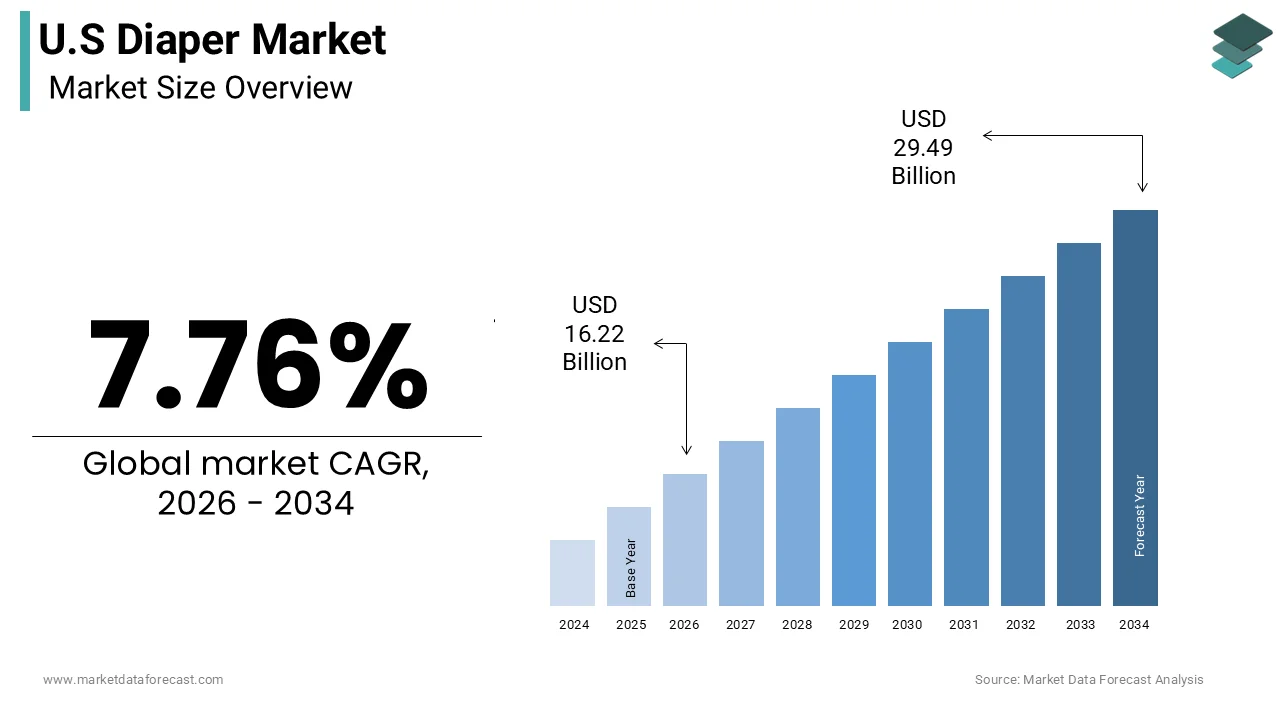

The United States diaper market was valued at USD 15.05 billion in 2025 and is projected to reach USD 29.49 billion by 2034, growing from USD 16.22 billion in 2026 at a CAGR of 7.76% during the forecast period. Market growth is driven by rising awareness regarding infant hygiene, increasing demand for premium baby care products, and growing adoption of convenient disposable diapers. Expanding adult incontinence product demand and innovations in eco-friendly diaper materials are further supporting the growth of the U.S. diaper market.

Key Market Trends

- Rising demand for biodegradable and eco-friendly diapers

- Increasing consumer preference for premium and skin-friendly products

- Growth in adult incontinence and elderly care products

- Expansion of online retail and subscription-based diaper delivery services

- Increasing innovation in absorbent and leak-proof diaper technologies

Segmental Insights

- Based on end user, the babies segment dominated the U.S. diaper market in 2025 by accounting for 53.2% of the market share, driven by consistent demand for infant hygiene products

- Based on material, the conventional material segment held the dominant share in 2025 due to affordability, widespread availability, and strong consumer acceptance

- Based on price range, the mid-range segment led the market in 2025 by capturing 33.8% of the market share, supported by balanced pricing and product quality

- Based on distribution channel, the hypermarkets and supermarkets segment accounted for a significant market share in 2025, driven by convenience, product variety, and promotional offers

Competitive Landscape

- The U.S. diaper market is highly competitive, with companies focusing on comfort, absorbency, sustainability, and premium baby care solutions. Market players are investing in biodegradable materials, hypoallergenic products, and advanced absorbent technologies to strengthen their market presence.

- Prominent players in the U.S. diaper market include Procter & Gamble, Kimberly-Clark, Johnson & Johnson, The Honest Company, Unicharm Corporation, Ontex Group, Domtar Corporation, First Quality Enterprises, Parasol Co, and Bambo Nature.

U.S Diaper Market Size

The U.S diaper market was valued at USD 15.05 billion in 2025, is estimated to reach USD 16.22 billion in 2026, and is projected to reach USD 29.49 billion by 2034, growing at a CAGR of 7.76% from 2026 to 2034.

The diaper is an absorbent hygiene product designed for infants, toddlers, and adults, including disposable diapers, cloth alternatives, and training pants. Consumer engagement is driven by the non-negotiable nature of infant care and the growing demographic of aging populations requiring adult incontinence solutions. According to the United States Census Bureau, there were approximately 3.6 million births in the country in recent years, providing a consistent baseline demand for infant hygiene products. Furthermore, data from the Centers for Disease Control and Prevention indicates that the population aged 65 and older is projected to reach 95 million by 2060, highlighting the expanding need for adult care solutions. The shift toward premiumization has transformed diapers from commodity items into specialized health products featuring organic materials and hypoallergenic properties. The average annual expenditures on baby supplies per consumer unit have remained stable, demonstrating the resilience of this category against economic fluctuations. Environmental consciousness is reshaping production standards as consumers increasingly prioritize biodegradable options and reduced plastic usage.

MARKET DRIVERS

Rising Birth Rates Among Millennial and Gen Z Parents

The sustained fertility rates among younger people for infant diapers are boosting the growth of the United States diaper market. Millennial and Generation Z parents are entering their prime childbearing years, bringing distinct preferences for high-quality, safe, and convenient baby care products. According to the National Center for Health Statistics, the total fertility rate has stabilized around 1.6 to 1.7 births per woman, ensuring a steady influx of new consumers into the diaper market. These younger parents are characterized by higher educational attainment and digital connectivity, which influences their purchasing decisions toward premium and technologically advanced diaper brands. The millennial parents are more likely to spend on premium baby products compared to previous generations, prioritizing features, such as wetness indicators and superior absorbency. The trend toward smaller family sizes allows parents to allocate more resources per child, resulting in higher per-unit spending on diapers. Social media platforms play a crucial role in shaping brand loyalty, as parents seek recommendations and reviews from peer networks. The emphasis on skin health and allergy prevention drives demand for hypoallergenic and fragrance-free options. Additionally, the increasing participation of women in the workforce necessitates reliable and long-lasting diaper solutions that reduce the frequency of changes.

Growing Prevalence of Adult Incontinence Due to Aging Population

The expanding elderly population is another attribute enhancing the growth of the United States adult diaper market. According to the United States Census Bureau, the number of individuals aged 65 and older is growing rapidly and is expected to constitute nearly 22% of the total population by 2040. This demographic shift creates a substantial and expanding market for adult absorbent products. The destigmatization of incontinence through public health campaigns encourages more individuals to seek professional solutions rather than managing symptoms silently. Healthcare providers and insurance programs are increasingly covering adult diapers as essential medical supplies, further boosting accessibility. The preference for discreet and comfortable designs that mimic regular underwear enhances user dignity and compliance. Advances in material technology have improved the thinness and absorbency of adult diapers, making them more appealing to active seniors. The rise of home healthcare services also contributes to demand as caregivers require reliable products for daily assistance.

MARKET RESTRAINTS

Environmental Concerns Regarding Waste and Non-Biodegradable Materials

The significant environmental footprint associated with disposable diapers, as consumers become increasingly aware of waste management issues, is stringently declining the growth of the United States diaper market. Traditional disposable diapers contain plastics and superabsorbent polymers that can take hundreds of years to decompose in landfills. According to the Environmental Protection Agency, disposable diapers constitute approximately 2% of all municipal solid waste in the United States, amounting to millions of tons annually. This substantial volume of non-biodegradable waste has sparked a backlash among environmentally conscious consumers, who seek sustainable alternatives. The average child will use nearly 8000 disposable diapers before potty training, creating a long-term accumulation of waste. The lack of widespread recycling infrastructure for used hygiene products exacerbates the disposal challenge. Many municipalities do not accept soiled diapers in composting or recycling programs, limiting viable disposal options. Consumers are increasingly turning to reusable cloth diapers or hybrid systems to reduce their ecological impact. Regulatory pressures are mounting as states consider bans on single-use plastics and extended producer responsibility laws. Manufacturers face challenges in developing fully biodegradable diapers that maintain performance and cost competitiveness. The higher cost of eco-friendly materials often deters price-sensitive buyers.

High Cost of Premium Diapers and Economic Sensitivity

The substantial financial burden associated with purchasing high-quality diapers for many households, particularly during periods of economic uncertainty, is additionally hampering the growth of the United States diaper market. Premium diapers with advanced features, such as organic cotton and chlorine-free processing, command higher prices that may be prohibitive for budget-constrained families. The cost of baby supplies has risen in line with inflation, placing additional pressure on household budgets. For low and middle-income families, diapers represent a recurring and significant expense that competes with other essential needs. The estimated cost of raising a child includes thousands of dollars for diapers alone over the first few years. Economic downturns and inflationary pressures lead consumers to trade down to lower-priced private-label brands or reduce usage frequency. The lack of government subsidies for diapers in most states means that families bear the full cost without financial relief. Diaper need affects millions of children, leading to health issues such as diaper rash and infections when parents stretch supplies. This financial strain limits the ability of manufacturers to maintain premium pricing strategies. Retailers respond by offering discounts and bulk packs, but margins remain tight.

MARKET OPPORTUNITIES

Expansion of Eco-Friendly and Biodegradable Product Lines

The growing consumer demand for sustainable products is prompting manufacturers to innovate with biodegradable and plant-based materials, which is certain to elevate new opportunities for the growth of the United States diaper market. Brands that prioritize environmental responsibility can differentiate themselves and capture the loyalty of eco-conscious parents. According to a survey, over 70% of consumers express willingness to pay more for products with sustainable packaging and sourcing credentials. This shift creates a niche for companies that utilize materials, such as bamboo, corn starch, and wood pulp, to create compostable diapers. The certification programs for compostable hygiene products are gaining traction, providing a verified label for ethical sourcing. Manufacturers can leverage these certifications to build trust and transparency with buyers. Marketing campaigns that highlight carbon footprint reduction and water conservation resonate strongly with younger demographics. Partnerships with environmental organizations can amplify brand credibility and reach. The introduction of plastic-free packaging aligns with broader waste reduction goals and regulatory trends. This strategic pivot toward sustainability not only addresses ecological concerns but also opens new revenue streams.

Integration of Smart Technology and Health Monitoring Features

The integration of smart technology into diaper products for enhancing parental convenience and infant health monitoring is another major factor to escalate the growth of the United States diaper market. Connected diapers equipped with sensors can detect wetness levels and alert caregivers via mobile applications, reducing the need for manual checks. Brands can leverage this trend by developing proprietary apps that track diaper changes, sleep patterns, and skin health. The sales of connected health devices continue to grow, driven by the desire for data-driven parenting. Smart diapers allow for early detection of health issues such as dehydration or urinary tract infections by analyzing urine composition. This proactive approach appeals to tech-savvy parents who value precision and peace of mind. The data generated by these systems enables personalized care recommendations and timely interventions. Partnerships with pediatricians and healthcare providers can validate the clinical benefits of smart diapers. Direct-to-consumer channels allow for targeted marketing of these high-tech products to affluent demographics. Subscription models ensure recurring revenue and customer retention for connected services.

MARKET CHALLENGES

Supply Chain Disruptions and Raw Material Volatility

The complex global supply chain for components, such as wood pulp, superabsorbent polymers, and non-woven fabrics, also hinders the growth of the United States diaper market. Disruptions in these supply chains due to geopolitical tensions, trade policies, and logistical hurdles pose significant challenges to production and delivery. Fluctuations in commodity prices directly impact manufacturing costs and profit margins. The producer price index for pulp and paper products has shown considerable volatility, creating uncertainty for long-term contracts. Tariffs on imported materials further increase costs, forcing companies to reassess sourcing strategies. Inventory management becomes challenging as businesses strive to balance stock levels against uncertain supply conditions. Delays in component availability can halt production lines and delay project completions, leading to customer dissatisfaction. The transition to new materials also requires changes in manufacturing processes and supply chains, adding complexity. Companies must invest in diversifying supplier bases and enhancing logistics resilience.

Regulatory Compliance and Chemical Safety Scrutiny

The increasing regulatory scrutiny regarding the chemical composition of products, including fragrances, dyes, and absorbent materials, is also expected to impede the growth of the United States diaper market. Consumers and advocacy groups are demanding greater transparency and safety assurances, leading to stricter compliance requirements. Several common chemicals used in diaper processing, such as phthalates and volatile organic compounds, have raised health concerns, prompting calls for bans. The recalls and warnings related to contaminated or unsafe diaper products have increased visibility of these issues. Manufacturers must invest in rigorous testing and reformulation to meet evolving safety standards and avoid liability. The complexity of navigating varying state and federal regulations adds operational burdens and costs. The presence of allergens and irritants requires clear warning labels to prevent liability issues. Failure to comply can result in legal penalties, reputational damage, and loss of consumer trust. The demand for natural and organic options requires changes in production processes and sourcing. Educating consumers about safety improvements is challenging amidst widespread misinformation. The need for third-party certifications adds another layer of complexity and expense. This regulatory landscape demands vigilance and adaptability from all market participants.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 7.76% |

| Segments Covered | By End User, Material, Price Range, Distribution Channel, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado. |

| Market Leaders Profiled | Procter & Gamble, Kimberly-Clark Corporation, Johnson & Johnson, The Honest Company, Unicharm Corporation, Ontex Group, Domtar Corporation, First Quality Enterprises, Parasol Co., Bambo Nature |

SEGMENTAL ANALYSIS

By End User Insights

The babies segment was the largest by holding 53.2% of the United States diaper market share in 2025, with the fundamental and non-negotiable need for infant hygiene products during the first few years of life. Every newborn requires a consistent supply of diapers, creating a stable and predictable demand base that is largely immune to economic fluctuations. The intensive usage rate results in the consumption of roughly 8000 diapers per child before potty training is complete, as per research. Parents prioritize safety, comfort, and absorbency, leading to brand loyalty and repeat purchases. The cultural expectation of maintaining high hygiene standards for infants further reinforces this demand. Healthcare providers recommend frequent changes to prevent diaper rash and infections, which sustains volume sales. Additionally, the rise of dual-income households has increased the reliance on convenient disposable options over cloth alternatives. The emotional investment parents make in their children's well-being drives willingness to pay for premium features.

The adult segment is likely to witness the fastest CAGR of 7.5% from 2026 to 2034, owing to the rapidly aging population and the increasing prevalence of age-related incontinence conditions. The shift toward an older society, where chronic health issues necessitate long-term care solutions. According to the United States Census Bureau, the population aged 65 and older is projected to double by 2060, reaching nearly 95 million individuals. The destigmatization of adult incontinence through public health campaigns encourages more individuals to seek professional products rather than managing symptoms silently. Advances in product design have improved discretion and comfort, making adult diapers more appealing to active seniors. The rise of home healthcare services also contributes to demand as caregivers require reliable products for daily assistance. Insurance coverage for adult incontinence supplies is expanding, further improving accessibility. The preference for dignity-preserving designs that mimic regular underwear enhances user compliance.

By Material Insights

The conventional material segment held a dominant share of the United States diaper market in 2025, with its cost-effectiveness, widespread availability, and established manufacturing infrastructure. Most diapers are made from wood pulp, plastics, and superabsorbent polymers, which offer superior absorbency and leak protection at affordable prices. The production of wood pulp remains robust, ensuring a steady and low-cost supply for manufacturers. The price sensitivity of a large portion of consumers, who prioritize affordability over eco-friendly attributes, is driving the growth of the United States diaper market. The conventional diapers are significantly cheaper than organic alternatives, making them accessible to low and middle-income families. The extensive distribution network for conventional brands ensures they are available in every retail outlet, from grocery stores to gas stations. Manufacturers have invested heavily in optimizing production processes for conventional materials, achieving economies of scale that lower unit costs. The performance reliability of conventional diapers in terms of dryness and fit has been proven over decades, building consumer trust. Retailers allocate the majority of shelf space to conventional brands due to their high turnover rates. The lack of widespread recycling infrastructure for biodegradable materials further limits the adoption of alternatives.

The organic material segment is projected to witness the fastest CAGR of 9.2% during the forecast period, with the increasing consumer awareness of environmental sustainability and chemical safety. Parents are increasingly seeking products free from chlorine fragrances and synthetic materials to protect their babies' sensitive skin. According to a survey, over 70% of consumers express willingness to pay more for products with sustainable and organic credentials. Certifications, such as USDA Organic and Global Organic Textile Standard, verify quality and safety, building trust with discerning buyers. Brands are responding by launching innovative organic lines that combine eco-friendliness with high performance. The availability of organic diapers in mainstream retail channels has improved, making them more accessible. Subscription services for organic brands enhance convenience and customer retention.

By Price Range Insights

The mid-range segment was the largest by occupying 33.8% of the United States diaper market share in 2025, with its balance of quality and affordability, which appeals to the broadest consumer base. These products offer reliable performance and comfort without the premium price tag of luxury brands or the perceived lower quality of economy options. The value proposition that mid-range brands provide is combining trusted brand names with competitive pricing. The mid-range diapers account for the largest share of unit sales in major retail chains due to their widespread acceptance. Parents often view these products as a safe choice that meets basic hygiene needs without excessive spending. Retailers promote mid-range brands through loyalty programs and bulk discounts, further driving volume. The consistency in quality and availability builds long-term brand loyalty among families. Private label brands from major retailers often compete in this segment, offering comparable quality at lower prices.

The premium segment is deemed to witness the fastest CGAR of 6.8% from 2026 to 2034, with the trend toward premiumization and the willingness of parents to invest in superior quality for their children. Consumers are increasingly seeking diapers with advanced features such as ultra-soft materials, wetness indicators, and hypoallergenic properties. Brands leverage marketing campaigns that escalate the clinical testing and dermatologist approval to justify higher prices. The influence of social media influencers showcasing premium brands further drives aspiration and trial. Direct-to-consumer models allow premium brands to offer personalized subscriptions and exclusive products. The emphasis on sustainability and ethical sourcing in premium lines appeals to eco-conscious shoppers.

By Distribution Channel Insights

The hypermarkets and supermarkets segment accounted for a significant share of the United States diaper market in 2025, with the convenience of one-stop shopping and the ability to purchase bulk quantities at competitive prices. These retailers offer a wide variety of brands and sizes, allowing consumers to compare options and take advantage of promotions. As per the study, approximately 60% of grocery purchases in the United States occur in supermarkets due to their dominance in household essentials. The habitual nature of diaper purchasing where families stock up during weekly shopping trips. The availability of private-label brands alongside national brands provides choices for different budget levels. Loyalty programs and digital coupons offered by these retailers further incentivize purchases. The physical presence of stores allows customers to inspect packaging and verify product details before buying. Immediate possession of goods eliminates shipping wait times and costs. The trust associated with established retail chains enhances consumer confidence.

The online channels segment is growing at an expected CAGR of 11.5% in the coming years, with the convenience of home delivery and the popularity of subscription services. Parents appreciate the ease of having diapers delivered regularly without the need to visit stores. The primary driver is the time-saving benefit of e-commerce, which appeals to busy families. According to the United States Census Bureau, e-commerce sales for baby products have grown significantly as logistics networks improve. The ability to access a wider range of brands, including niche and organic options not available locally, expands consumer choices. Digital platforms provide detailed product information and reviews, helping parents make informed decisions. Mobile apps facilitate easy reordering and management of subscriptions. The rise of quick commerce platforms offering rapid delivery further enhances the appeal of online purchasing. Packaging innovations ensure product integrity during shipping.

COMPETITION OVERVIEW

The competitive landscape of the United States diaper market is characterized by intense rivalry among established multinational corporations and aggressive private label offerings. Large players leverage strong brand equity and extensive distribution networks to maintain dominance while competing on price and innovation. Price competition is fierce as retailers promote their own brands to capture margin-sensitive consumers. Private label products have improved in quality, challenging national brands on value propositions. Innovation focuses on sustainability and skin health attributes to differentiate offerings. Supply chain efficiency is critical for maintaining profitability amidst fluctuating raw material costs. Regulatory pressures regarding environmental impact drive investments in green technologies. Consumer loyalty is fragile, with shoppers readily switching brands for better deals or safer options. Companies must balance cost management with product quality to sustain market position.

KEY MARKET PLAYERS

A few major players of the U.S diaper market include

- Procter & Gamble

- Kimberly-Clark Corporation

- Johnson & Johnson

- The Honest Company

- Unicharm Corporation

- Ontex Group

- Domtar Corporation

- First Quality Enterprises

- Parasol Co

- Bambo Nature

Top Strategies Used by Key Market Participants

Key players in the United States diaper market employ diverse strategies to maintain a competitive advantage and drive growth. Product innovation remains central with companies developing softer, more absorbent, and eco-friendly materials. Brands focus on direct-to-consumer channels by enhancing digital platforms and offering subscription services. Strategic investments in sustainability address environmental concerns through biodegradable packaging and responsible sourcing. Companies leverage data analytics to optimize supply chains and predict demand accurately. Omnichannel distribution ensures seamless access to products for both residential and commercial clients. Marketing campaigns emphasize trust, safety, and skin health to build brand loyalty.

Leading Players in the United States Diaper Market

- Procter and Gamble Company is a dominant force in the United States diaper market with its flagship brand, Pampers. The company contributes significantly by driving innovation in absorbency technology and skin health protection for infants. Recent actions include expanding its portfolio of premium and organic diaper lines to meet evolving consumer preferences for sustainability. Procter and Gamble has invested heavily in digital marketing campaigns that emphasize trust and scientific validation. The firm leverages its extensive distribution network to ensure widespread availability across retail and online channels.

- Kimberly-Clark Corporation holds a strong position in the US diaper sector through its trusted Huggies brand. The company drives growth by focusing on product differentiation and targeted marketing strategies for diverse consumer segments. Recent strategies involve launching specialized products for sensitive skin and overnight protection to address specific parental needs. Kimberly-Clark has enhanced its sustainability initiatives by introducing plant-based materials and recyclable packaging options. The firm actively engages with parents through digital platforms, offering educational resources and community support. Investments in supply chain optimization improve efficiency and reduce environmental impact. These initiatives ensure the company remains a preferred choice for families seeking reliable and gentle diaper solutions.

- Ontex Group NV is a key player in the US diaper market, known for its private label and branded offerings such as Little Movers. The company focuses on providing high-quality, affordable hygiene solutions to a broad consumer base. Recent actions include expanding its manufacturing capacity in North America to improve supply chain resilience and reduce lead times. Ontex has introduced innovative designs that enhance fit and comfort for active babies. The firm strengthens its market position through strategic partnerships with major retailers, ensuring prominent shelf placement. Investments in sustainable production processes align with growing environmental consciousness among consumers.

MARKET SEGMENTATION

This research report on the US diaper market has been segmented and sub-segmented based on end user, material, price range, distribution channel & region.

By End User

- Babies

- Adults

By Material

- Conventional

- Organic

By Price Range

- Economy

- Mid-range

- Premium

By Distribution Channel

- Hypermarkets & Supermarkets

- Specialty Stores

- Pharmacy Stores

- Online Channels

- Others

By Region

- New York

- Texas

- Florida

- Georgia

- California

- Rest of U.S.

Frequently Asked Questions

1. What is driving the growth of the United States diaper market?

The market is growing due to increasing birth rates, rising hygiene awareness, and growing demand for premium baby care products.

2. Which types of diapers are commonly used in the United States?

Disposable diapers, cloth diapers, training pants, swim diapers, and biodegradable diapers are widely used.

3. Why are disposable diapers popular in the U.S.?

Disposable diapers are preferred because of their convenience, high absorbency, and ease of use.

4. What factors influence consumer purchasing decisions in the diaper market?

Parents consider comfort, absorbency, skin-friendliness, pricing, and brand reputation before purchasing diapers.

5. Which distribution channels are important for diaper sales?

Supermarkets, pharmacies, baby stores, online platforms, and convenience stores are key sales channels.

6. What challenges does the U.S. diaper market face?

The market faces challenges such as rising raw material costs, environmental concerns, and intense competition.

7. What materials are commonly used in diapers?

Diapers are typically made using absorbent polymers, cotton, nonwoven fabrics, and elastic materials.

8. How does innovation affect the diaper market?

Companies are introducing smart diapers, skin-sensitive products, and sustainable materials to attract consumers.

9. What role does branding play in the diaper industry?

Strong branding and consumer trust significantly influence purchasing behavior in the diaper market.

10. What is the future outlook for the United States diaper market?

The market is expected to grow steadily due to product innovation, rising hygiene awareness, and demand for sustainable diaper solutions.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com